An elementary derivation of first and last return times of 1D random walks

Abstract

Random walks, and in particular, their first passage times, are ubiquitous in nature. Using direct enumeration of paths, we find the first return time distribution of a 1D random walker, which is a heavy-tailed distribution with infinite mean. Using the same method we find the last return time distribution, which follows the arcsine law. Both results have a broad range of applications in physics and other disciplines. The derivation presented here is readily accessible to physics undergraduates, and provides an elementary introduction into random walks and their intriguing properties.

Thermal and statistical physics texts often begin with a discussion of random walksreif ; kittel ; krapivsky and their associated applications such as Brownian motion,brownian polymer physics,doi and laser cooling of atoms.coldatoms The first passage time distribution , i.e. the distribution of times at which a target is first reached, stands out as central to many natural phenomena such as quenching of fluorescent molecules,cichos molecular rupture (times over which molecules dissociate in, e.g., ligand-receptor complexes), and target site searches (e.g. transcription factors finding corresponding binding sites along DNA),chou as well as additional problems in biology.zilman In the context of finance, an optimal trading strategy might be to sell an asset when it first reaches a threshold value.finance ; bouchaud

Insofar as undergraduate texts give an impression that the bell-shaped curve rules the world, first passage time distributions supply a nice counterexample by their heavy-tailed behavior, e.g., in 1D. Here we supply an elementary derivation of this result by examining first returns on an infinite 1D lattice. While general resultsfeller ; redner are available for first return distributions on infinite -dimensional lattices, derivations rely on generating functions or Laplace transforms which may be unfamiliar to undergraduates. In contrast, the approach below yields the power law after just a few lines of mathematics by entirely elementary means. It can thus serve as a friendly primer to random walks, first passage, recurrence, and heavy-tailed distributions.

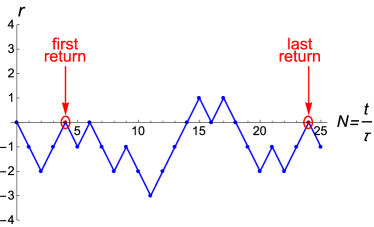

A 1D random walk is a succession of steps to the right or left with respective probabilities and , occurring at every time interval (hence ). We focus on the case of a symmetric walk () but the same formalism may be applied to biased walks (). All walks considered here begin at the origin () at time and have steps of identical length . The first return time is the time at which the walk first reaches the origin; similarly, the last return time is the time at which the origin is last visited. See Fig. 1 for an example of a 1D random walk trajectory with its first and last returns marked.

Assuming spatial and temporal initial conditions , the first return time distribution is , denoted as hereafter. Its cumulative is the probability to return to the origin by time . The complement is the survival probability , i.e. the probability to not return by time :

| (1) |

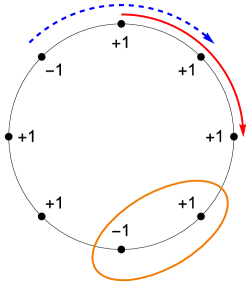

is found by enumerating all survival paths (those not returning to the origin) in the first steps. The probability of such a path occurring is given by the ballot theorem: In a ballot where candidates A and B have and total votes, respectively, the probability that A is always ahead of B throughout counting is . To enumerate survival paths we use a proof of the ballot theorem, known as the cycle lemma.renault The latter’s cyclical representation of paths is ideal for counting their partial sums and eliminating those which return to the origin, as explained below.

Consider a circular track with numbers, a fraction of which are and the rest are (see Fig. 2). The numbers and signify a step to the right and left, respectively. Such a configuration has possible clockwise paths along the circular track starting at each of the numbers. Consider first those survival paths which remain to the right of and never cross the origin: the sum of numbers along such paths is always positive. Any followed by a may be eliminated from the circular track as the two paths starting at either number are not in this class of right-of-the-origin survival paths; furthermore, their removal does not affect any other path’s sum since a pair’s net sum is zero. Repeating this procedure until no ’s remain yields the number of ’s in excess of ’s, i.e. the number of valid paths. The probability of choosing a valid path from a given track is then

| (2) |

where and denote the number of ’s and ’s, respectively. The probability in Eq. 2 is non-negative since for a path to remain to the right of the origin. To obtain the total number of valid paths from all possible circular track configurations, Eq. 2 is multiplied by the number of possible arrangements . The result is the ballot theorem: For a given , the number of paths remaining to the right of the origin is . Because must exceed for the walker to remain to the right of the origin, can range from 0 to where the latter floor function denotes the largest integer not greater than . Summing over these values yields the number of paths which remain to the right of the origin:

| (3) |

The summation in Eq. 3 is simplified by binomial identities and as follows:

| (4) |

Furthermore, which leads to the final result of Eq. 3. By symmetry, the number of paths which remain to the left of the origin is the same as in Eq. 3. Thus the number of survival paths is . The survival probability follows simply; each path has probability and therefore

| (5) |

In the continuum limit where is large (), Stirling’s approximation for Eq. 5 gives :

| (6) |

The survival probability decays to zero for long times , implying that the walk will eventually return to the origin with probability 1. This is in accord with Pólya’s recurrence theorempolya ; snell that symmetric random walks return to the origin on infinite lattices of dimension .

By Eq. 1, the first return distribution is

| (7) |

It follows that the distribution’s first moment, the average return time, diverges:

| (8) |

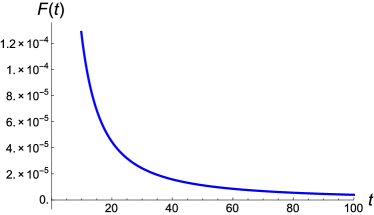

Diverging moments are the hallmark of heavy-tailed distributions; in this case, long return times dominate the average. Fig. 3 shows the heavy tail distribution of .

Our derivation yields insight into last return times as well. The probability to return for the last time at step (an even number of steps implied) is the product of the probabilities to be at the origin at step and of surviving steps thereafter. The former is since there are ways to take an equal number of steps right and left. For large the latter probability becomes by Stirling’s approximation. Multiplying by survival probability yields the probability that the last return occurs at step :

| (9) |

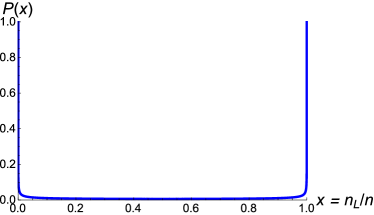

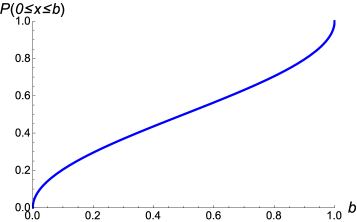

where . Eq. 9 is symmetric about its minimum with singular maxima occurring at and (see Fig. 4). Integrating Eq. 9 yields the arcsine lawfeller as shown in Fig. 5. The arcsine law also describes the number of positive partial sums in a sequence of mutually independent random variables from probability distributions other than the binomial.erdos While this rather counterintuitive result is seldom encountered in physics texts, the law has striking consequences likely to excite physics students. Fellerfeller (see Vol. 1, Section III.4) describes it in the context of coin-tossing games where losing and winning sides map to the left and right of the origin, respectively, and equalization of the fortunes signifies a return to the origin:

The results are startling. According to widespread beliefs a so-called law of averages should ensure that in a long coin-tossing game each player will be on the winning side for about half the time, and that the lead will pass not infrequently from one player to the other. Imagine then a huge sample of records of ideal coin-tossing games, each consisting of exactly trials. We pick one at random and observe the epoch of the last tie… With probability 1/2 no equalization occurred in the second half of the game, regardless of the length of the game. Furthermore, the probabilities near the end points are greatest… These results show that intuition leads to an erroneous picture of the probable effects of chance fluctuations.

The last return distribution is tied to the time spent on either side of the origin, which also follows the arcsine law.feller It is highly probable to remain on one side of the origin for nearly the entire walk, leading to long waiting times. Recent implications include hard-spheres gas particles colliding with the same neighbors for an extended period of time.fouxon Other examples where the arcsine law is obeyed include the time of maximal displacement in 1D Brownian motion,comtet ; levy lead changes within competitive team sports games,NBA and the probability distribution of longitudinal displacements of tracer particles in split flow.splitflow

In summary, we have reported on an elementary derivation of first and last return times which also serves as an introduction to a variety of important and broadly applicable concepts such as recurrence, first passage, heavy-tailed distributions, and the arcsine law.

Acknowledgements.

We thank Sidney Redner, Ori Hirschberg, and Michael P. Brenner for helpful comments. S.K. was supported by the U.S. Department of Defense through the NDSEG Program.References

- (1) F. Reif, Fundamentals of Statistical and Thermal Physics (McGraw-Hill, 1965), Ch. 1.

- (2) Charles Kittel, Elementary Statistical Physics, Dover edition (John Wiley & Sons, Inc., New York, 1958), see Part 1, Section 6.

- (3) Pavel L. Krapivsky, Sidney Redner, and Eli Ben-Naim, A Kinetic View of Statistical Physics (Cambridge University Press, Cambridge, UK, 2010).

- (4) Mark Kac, “Random Walk and the Theory of Brownian Motion,” Am. Math. Monthly 54 (7) 369–391 (1947).

- (5) Masao Doi, An Introduction to Polymer Physics (Oxford University Press, Oxford, UK, 1995), Chap. 1.

- (6) F. Bardou, J.-P. Bouchaud, A. Aspect, and C. Cohen-Tannoudji, Lévy Statistics and Laser Cooling: How Rare Events Bring Atoms to Rest (Cambridge University Press, Cambridge, UK, 2002).

- (7) F. Cichos, C. von Borczyskowski, and M. Orrit, “Power-law intermittency of single emitters,” Curr. Opin. Colloid & Interface Science 12 272–284 (2007).

- (8) T. Chou and M. R. D’Orsogna, “First passage problems in biology,” in First-passage phenomena and their applications, edited by R. Metzler, G. Oshanin, and S. Redner (World Scientific, Toh Tuck Link, Singapore, 2014).

- (9) S. Iyer-Biswas and A. Zilman, “First passage time processes in cellular biology,” Advances in Chemical Physics, Vol. 160 (John Wiley and Sons, 2015).

- (10) R. Chicheportiche and J.-P. Bouchaud, “Some Applications of First-Passage Ideas to Finance,” in First-passage phenomena and their applications, edited by R. Metzler, G. Oshanin, and S. Redner (World Scientific, Toh Tuck Link, Singapore, 2014).

- (11) Jean-Philippe Bouchaud and Marc Potters, Theory of Financial Risk and Derivative Pricing, 2nd edition, (Cambridge University Press, Cambridge, UK, 2003).

- (12) William Feller, An Introduction to Probability Theory and Its Applications, Vol. 1, 3rd edition (John Wiley & Sons, New York, 1950).

- (13) Sidney Redner, A guide to first-passage processes (Cambridge University Press, Cambridge, UK, 2001), Ch. 1.

- (14) M. Renault, “Four proofs of the ballot theorem,” Mathematics Magazine 80 (5), 345–352 (2007).

- (15) G. Pólya, “Ü̈ber eine Aufgabe der Wahrscheinlichkeitsrechnung betreffend die Irrfahrt im Strassennetz,” Math. Ann. 84, 149–160 (1921).

- (16) Peter G. Doyle and J. Laurie Snell, Random Walks and Electric Networks (The Carus Mathematical Monographs, Vol. 22, Mathematical Association of America, Washington, DC, 1984).

- (17) P. Erdös and M. Kac, “On the number of positive sums of independent random variables,” Bull. Amer. Math. Soc., 53 1011–1020 (1947).

- (18) A.J. Vidgop and I. Fouxon, “Emergence of distinguishability of patterns of collisions of particles in a non-equilibrium chaotic system,” Physica A 411 113–117 (2014).

- (19) J. Randon-Furling, S.N. Majumdar, and A. Comtet, “Convex Hull of Planar Brownian Motions: Exact Results and an Application to Ecology,” Phys. Rev. Lett. 103 140602-4 (2009).

- (20) P. Lévy, “Sur certains processus stochastiques homogènes,” Compos. Math. 7 283–339 (1939).

- (21) A. Clauset, M. Kogan, and S. Redner, “Safe leads and lead changes in competitive team sports,” Phys. Rev. E 91, 062815-11 (2015).

- (22) E. Ben-Naim, S. Redner, and D. ben-Avraham, “Bimodal diffusion in power-law shear flows,” Phys. Rev. A 45 (10) 7207–7213 (1992).