Robust reduced-rank regression

Abstract

In high-dimensional multivariate regression problems, enforcing low rank in the coefficient matrix offers effective dimension reduction, which greatly facilitates parameter estimation and model interpretation. However, commonly-used reduced-rank methods are sensitive to data corruption, as the low-rank dependence structure between response variables and predictors is easily distorted by outliers. We propose a robust reduced-rank regression approach for joint modeling and outlier detection. The problem is formulated as a regularized multivariate regression with a sparse mean-shift parametrization, which generalizes and unifies some popular robust multivariate methods. An efficient thresholding-based iterative procedure is developed for optimization. We show that the algorithm is guaranteed to converge, and the coordinatewise minimum point produced is statistically accurate under regularity conditions. Our theoretical investigations focus on nonasymptotic robust analysis, which demonstrates that joint rank reduction and outlier detection leads to improved prediction accuracy. In particular, we show that redescending -functions can essentially attain the minimax optimal error rate, and in some less challenging problems convex regularization guarantees the same low error rate. The performance of the proposed method is examined by simulation studies and real data examples.

Keywords: low-rank matrix approximation; nonasymptotic analysis; robust estimation; sparsity.

1 Introduction

Given observations of response variables and predictors, denoted by and for , we consider the multivariate regression model

| (1) |

where , , is an unknown coefficient matrix, and is a random error matrix. Such a high-dimensional multivariate problem, in which both and may be comparable to or even exceed the sample size , has drawn increasing attention in both applied and theoretical statistics.

Conventional least squares linear regression ignores the multivariate nature of the problem and may fail when is large relative to . Dimension reduction holds the key to characterizing the dependence between responses and predictors in a parsimonious way. Reduced-rank regression (anderson1951; izenman1975) achieves this by restricting the rank of the coefficient matrix, i.e., by solving the problem

| (2) |

where and denote trace and rank, and is a pre-specified positive definite weighting matrix (reinsel1998). The ranks are typically much smaller than and . A global solution to (2) can be obtained explicitly. See reinsel1998 for a comprehensive account of reduced-rank regression under the classical large- asymptotic regime. Finite-sample theories on rank selection and estimation accuracy of the penalized form of reduced-rank regression were developed by bunea2011. The nuclear norm and Schatten -norms can also be used to promote sparsity of the singular values of or ; see yuan2007, koltch2011, Rohde2011, agarwal2012, Foygel2012, chen2012ann, among others. Reduced-rank regression is closely connected with principal component analysis, canonical correlation analysis, partial least squares, matrix completion, and many other multivariate methods (izenman2008).

Although reduced-rank regression can substantially reduce the number of free parameters in multivariate problems, it is extremely sensitive to outliers, which are bound to occur, and thus in real-world data analysis, the low-rank structure could easily be masked or distorted. This is even more serious in high-dimensional or big-data applications. For example, in cancer genetics, multivariate regression is commonly used to explore the associations between genotypical and phenotypical characteristics (vounou2010), where employing rank regularization can help to reveal latent regulatory pathways linking the two sets of variables. But pathway recovery should not be distorted by abnormal samples or subjects. As another example, financial time series, even after stationarity transformation, often contain anomalies or demonstrate heavier tails than those of a normal distribution, which may jeopardize the recovery of common market behaviors and asset return forecasting.

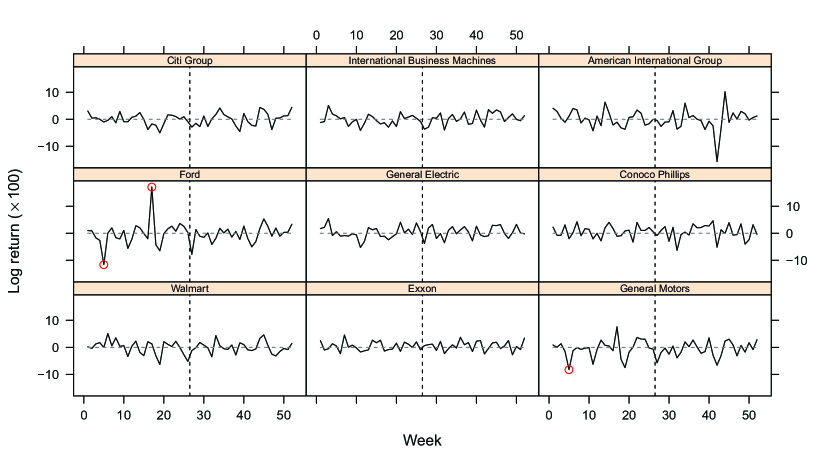

Consider the 52 weekly stock log-return data for nine of the ten largest American corporations in 2004 available from the R package mrce (Rothman2010), with () and . Chevron was excluded due to its drastic changes (yuan2007). The nine time series are shown in Figure 1. For the purpose of constructing market factors that drive general stock movements, a reduced-rank vector autoregressive model can be used, i.e., , with of low rank. By conditioning on the initial state and assuming the normality of , the conditional likelihood leads to a least squares criterion, so the estimation of can be formulated as a reduced-rank regression problem (Reinsel1997; Ltkepohl2007). However, as shown in the figure, several stock returns experienced short-term changes, and the autoregressive structure makes any outlier in the time series also a leverage point in the covariates.

Using the weekly log-returns in the first 26 weeks for training and those in the last 26 weeks for forecast, we analyzed the data with the reduced-rank regression and the proposed robust reduced-rank regression approach. While both methods resulted in unit-rank models, the robust reduced-rank regression automatically detected three outliers, i.e., the log-returns of Ford at weeks 5 and 17 and the log-return of General Motors at week 5.These correspond to two real major market disturbances attributed to the auto industry. Our robust method automatically took the outlying samples into account and led to a more reliable model. Table 1 displays the factor coefficients indicating how the stock returns are related to the estimated factors, and the -values for testing the associations between the estimated factors and the individual stock return series using the data in the last 26 weeks. The stock factor estimated robustly has positive influence over all nine companies, and overall, it correlates with the series better according to the reported -values. The out-of-sample prediction errors for least squares, reduced-rank regression and robust reduced-rank regression are , and , respectively, when measured by mean square error, and are , and , respectively, when measured by 40% trimmed mean square error. The robustification of rank reduction resulted in about 20% improvement in prediction.

| Reduced-rank regression | Robust reduced-rank regression | |||

|---|---|---|---|---|

| coefficient | -value | coefficient | -value | |

| Walmart | 046 | 044 | 036 | 023 |

| Exxon | 015 | 032 | 014 | 084 |

| General Motors | 096 | 042 | 090 | 002 |

| Ford | 120 | 064 | 059 | 018 |

| General Electric | 024 | 067 | 032 | 006 |

| Conoco Phillips | 004 | 019 | 036 | 008 |

| Citi Group | 027 | 093 | 045 | 000 |

| International Business Machines | 036 | 042 | 057 | 013 |

| American International Group | 019 | 001 | 058 | 000 |

In this work, we deem explicit outlier detection to be as important as robust low-rank estimation. Indeed, the reduced-rank component may not be of direct interest in some applications, as it often represents common background information shared across the response variables, while capturing unusual changes or jumps is helpful. The robustification of low-rank matrix estimation is non-trivial. A straightforward idea might be to use a robust loss function in place of the squared error loss in (2), leading to

| (3) |

but such an estimator may be difficult to compute. To the best of our knowledge, even when is Huber’s loss function (Huber1981), there is no algorithm for solving (3), let alone those nonconvex losses which are known to be more effective in dealing with multiple gross outliers with possibly high leverage values. Another motivation is that nonasymptotic theory on the topic is limited. Classical robust analysis, ignoring the low-rank constraint, falls in either deterministic worst-cases studies, or large- asymptotics with and held fixed, which may not meet modern needs.

We propose a novel robust reduced-rank regression method for concurrent robust modeling and outlier identification. We explicitly introduce a sparse mean-shift outlier component and formulate a shrinkage multivariate regression in place of (3), where and/or can be much larger than . The robust reduced-rank regression provides a general framework and includes M-estimation and principal component pursuit (Huber1981; Hampel1986; ZhouCandes2010; candes2011). It is worth mentioning that all the techniques developed in this work apply to high-dimensional sparse regression with a single response. In Section 2, we show that low-rank estimation can be ruined by a single rogue point, and propose a robust reduced-rank estimation framework. A universal connection between the proposed robustification and conventional M-estimation is established, regardless of the size of , or . Section LABEL:sec:theory performs finite-sample theoretical studies of the proposed robust estimators, with the intention of pushing classical robust analysis to multivariate data with possible large and/or . A computational algorithm developed in Section LABEL:sec:ipod is easy to implement and leads to a coordinatewise minimum point with theoretical guarantees. Section LABEL:sec:app shows some real applications. All proofs and simulation studies are given in the Appendices.

The following notation and symbols will be used throughout the paper. We denote by the set of natural numbers. We use to denote and to denote the Euler constant. Let . Given any matrix , denotes the orthogonal projection matrix onto the range of , i.e., , where - stands for the Moore–Penrose pseudoinverse. When there is no ambiguity, we also use to denote the column space of . Let denote the Frobenius norm, denote the spectral norm, with denoting the cardinality of the enclosed set. For , , and which gives the number of non-zero rows of . Given , we often denote by . Threshold functions are defined as follows.

Definition 1 (Threshold function).

A threshold function is a real-valued function defined for and such that (i) ; (ii) for ; (iii) ; (iv) for .

Definition 2 (Multivariate Threshold function).

Given any , is defined for any vector such that for and otherwise. For any matrix , .

2 Robust Reduced-Rank Regression

2.1 Motivation

Although reduced-rank regression is associated with a highly nonconvex problem (2), a global minimizer can be obtained in explicit form. Given any () with ,

| (4) |

where is formed by the leading eigenvectors of . See, e.g., reinsel1998 for a detailed justification. When , we abbreviate to . The reduced-rank regression estimator is denoted by to emphasize its dependence on the regularization parameter.

Outliers are unavoidable in real data. We define the finite-sample breakdown point for an arbitrary estimator , in the spirit of donoho1983bd: given finite data and an estimator , its breakdown point is

In addition to the reduced-rank regression estimator , we take into account a general low-rank estimator obtained by imposing a singular value penalty

| (5) |

Here, is a regularization parameter, and denote the singular values of . The penalty is constructed from an arbitrary thresholding rule by

| (6) |

for some nonnegative satisfying , for all .

Theorem 1.

The result indicates that a single outlier can completely ruin low-rank matrix estimation, whether one applies a rank constraint or, say, a Schatten -norm penalty. The conclusion limits the use of ordinary rank reduction in big data applications. Because with the low-rank constraint, directly applying a robust loss function, as in (3), may result in nontrivial computational and theoretical challenges, we will apply a novel additive robustification, motivated by she2011a.

2.2 The additive framework

We introduce a multivariate mean-shift regression model to explicitly encompass outliers,

| (7) |

where gives the matrix of coefficients, describes the outlying effects on , and has independently and identically distributed rows following . Obviously, this leads to an over-parameterized model, so we must regularize the unknown matrices appropriately. We assume that has low rank and is a sparse matrix with only a few nonzeros because outliers are inconsistent with the majority of the data. Given a positive definite weighting matrix , we propose the robust reduced-rank regression problem

| (8) |

Here, is a sparsity-promoting penalty function with to adjust the amount of shrinkage, but it can also be a constraint, such as (14). The following form of can handle element-wise outliers

| (9) |

which was used in the stock return analysis. It is more common in robust statistics to assume outlying samples, or outlying rows in , which corresponds to

| (10) |

where is the th row vector of . Unless otherwise specified, we consider row-wise outliers. But all our algorithms and analyses after simple modification can handle element-wise outliers.

In the literature on reduced-rank regression, it is common to regard the weighting matrix as known (reinsel1998; yuan2007; izenman2008). The choice of is flexible and is usually based on a pilot covariance estimate . For example, it can be when is nonsingular, or a regularized version for some . Although it sounds intriguing to consider jointly estimating the high-dimensional mean and the even higher-dimensional covariance matrix in the presence of outliers, this is beyond the scope of this paper. When a reliable estimate of is unavailable, a standard practice in finance and econometric forecasting is to reduce to a diagonal matrix, or equivalently, an identity matrix after robustly scaling the response variables. For ease of presentation, we take as the identity matrix unless otherwise noted, and mainly focus on the following robust reduced-rank regression criterion,

| (11) |

We show that the proposed additive outlier characterization indeed comes with a robust guarantee, and interestingly, it generalizes M-estimation to the multivariate rank-deficient setting. We write and .

Theorem 2.

(i) Suppose is an arbitrary thresholding rule satisfying Definition 1, and let be any penalty associated with through (6). Consider

| (12) |

For any fixed , a globally optimal solution for is . By profiling out with , (12) can be expressed as an optimization problem with respect to only, and it is equivalent to the robust M-estimation problem

| (13) |

where the robust loss function is given by

(ii) Given , consider

| (14) |

Similarly, (14), after profiling out , can be expressed as an optimization problem with respect to only, and is equivalent to the rank-constrained trimmed least squares problem

| (15) |

where are the order statistics of satisfying .

Remark 1.

Theorem 2 connects to through . As is well known, changing the squared error loss to a robust loss amounts to designing a set of multiplicative weights for (). Our additive robustification achieves the same robustness, but leaves the original loss function untouched. The connection is also valid in the case of element-wise outliers, with and applied in an element-wise manner. In fact, the identity built in Lemma LABEL:thresh-identity in the Appendices,

implies that the equivalence holds much more generally, with subject to an arbitrary constraint or penalty, and regardless of the number of response variables and the number of predictors. This extends the main result in she2011a to multiple-response models with possibly larger than .