A new non-parametric detector of univariate outliers for distributions with unbounded support

Abstract

The purpose of this paper is to construct a new non-parametric detector of univariate outliers and to study its asymptotic properties. This detector is based on a Hill’s type statistic. It satisfies a unique asymptotic behavior for a large set of probability distributions with positive unbounded support (for instance: for the absolute value of Gaussian, Gamma, Weibull, Student or regular variations distributions). We have illustrated our results by numerical simulations which show the accuracy of this detector with respect to other usual univariate outlier detectors (Tukey, MAD or Local Outlier Factor detectors). The detection of outliers in a database providing the prices of used cars is also proposed as an application to real-life database.

Keywords: Outlier detection; order statistics; Hill estimator; non-parametric test.

1 Introduction

Let be a sample of positive, independent, identically distributed random variables with unbounded distribution. This article aims to provide a non-parametric outlier detector among the ”large” values of .

Remark 1.

If we wish to detect outliers among the ”small” values of , it would be possible to consider instead of , for . Moreover, if , , are not positive random variables, as in the case of quantile regression residuals, we can consider instead of .

There are numerous outlier detectors in such a framework. Generally, such detectors consist of statistics directly applied to each observation, deciding if this observation can be considered or not as an outlier (see for instance the books of Hawkins, 1980, Barnett and Lewis, 1994, Rousseeuw and Leroy, 2005, or the article of Beckman and Cook, 1983). The most frequently used, especially in the case of regression residuals, is the Student-type detector (see a more precise definition in Section 4). However, it is a parametric detector that is theoretically defined for a Gaussian distribution. Another well-known detector is the robust Tukey detector (see for example Rousseeuw and Leroy, 2005). Its confidence factor is computed from quartiles of the Gaussian distribution, though it is frequently used for non-Gaussian distributions. Finally, we can also cite the detector using a confidence factor computed from the median of absolute value of Gaussian distribution (see also Rousseeuw and Leroy, 2005).

Hence all the most commonly used outlier detectors are based on Gaussian distribution and they are not really accurate for heavier distributions (for regression residuals, we can also cite the Grubbs-Type detectors introduced in Grubbs, 1969, extended in Tietjen and Moore, 1972). Such a drawback could be avoided by considering a non-parametric outlier detector. However, in the literature there are few non-parametric outlier detectors. We could cite the Local Outlier Factor (LOF) introduced in Breunig et al. (2000), which is also valid for

multivariate outliers. For any integer , the LOF algorithm compares the density of each point to the density of its -closest neighbors.

Unfortunately a theoretical or numerical procedure for choosing the number of cells and its associated threshold still does not exist. There are also other detectors essentially based on a classification methodology (for instance: Knorr et al., 2000) or robust statistics (for instance: Hubert and Vendervieren, 2008, for univariate skewed data and Hubert and Van der Veeken, 2008, for multivariate ones).

An interesting starting point for defining a non-parametric detector of outlying observations is provided by the order statistics of . Thus, Tse and Balasooriya (1991) introduced a detector based on increments of order statistics, but only for the exponential distribution. Recently, a procedure based on the Hill estimator was also developed for detecting influential data points in Pareto-type distributions (see Hubert et al., 2012). The Hill estimator (see Hill, 1975) has been defined from the following property:

the family of r.v.

is asymptotically (when ) a sample of independent r.v. following exponential distributions (Rényi exponential representation) for distributions in the max-domain of attraction of where is the cumulative distribution function of the extreme value distribution (see Beirlant et al., 2004).

Here we will use an extension of this property for detecting a finite number of outliers among the sample . Indeed, an intuitive idea for detecting them is the following: the presence of outliers generates a jump in the family of r.v. , therefore we also see a jump in the family of the r.v. . Thus an outlying data detector can be obtained when the maximum of this family exceeds a threshold (see details in (2.12) or (3.3)). In the sequel, see some assumptions on probability distributions for applying this new test of outlier presence. This also provides an estimator of the number of outliers. It is relevant to say that this test is not only valid for Pareto-type distribution (for instance Pareto, Student or Burr probability distributions), but more generally to a class of regular variations distributions. It can also be applied to numerous probability distributions with an exponential decreasing probability distribution function (such as Gaussian, Gamma or Weibull distributions). So our new outlier detector is a non-parametric estimator defined from an explicit threshold, which does not require any tuning parameter and can be applied to a very large family of probability distributions.

Numerous Monte-Carlo experiments carried out in the case of several probability distributions attest to the accuracy of this new detector. It is compared to other famous outlier detectors or extended versions of these detectors and the simulation results obtained by this new detector are convincing especially since it ignores false outliers. Moreover, an application to real-life data (price, mileage and age of used cars) is done, allowing the detection of two different kinds of outliers.

We have drafted our paper along following lines. Section 2 contains the definitions and several probabilistic results while Section 3 describes how to use them to build a new outlier detector. Section 4 is devoted to Monte-Carlo experiments, Section 5 presents the results of the numerical application on used car variables and the proofs of this paper are to be found in Section 6.

2 Definition and first probabilistic results

For a sample of positive i.i.d.r.v. with unbounded distribution, define:

| (2.1) |

It is clear that is a decreasing function and when . Hence, define also the pseudo-inverse function of by

| (2.2) |

is also a decreasing function. Moreover, if the support of the probability distribution of is unbounded then when .

Now, we consider both the following spaces of functions:

-

•

, such as for any , when where satisfies and is a diffeomorphism .

-

•

, there exist and a function satisfying , and for all , .

Example 2.1.

We will show below that numerous famous ”smooth” probability distributions such as absolute values of Gaussian, Gamma or Weibull distributions satisfy . Moreover, numerous heavy-tailed distributions such as Pareto, Student or Burr distributions have .

Using the order statistics , define the following ratios by:

| (2.3) | |||

| (2.4) |

In the sequel, we are going to provide some probabilistic results on the maximum of these ratios.

Proposition 1.

Assume . Then, for any , and with a sequence of r.v. satisfying for where is a sequence of i.i.d.r.v. with exponential distribution of parameter ,

| (2.7) |

Here corresponds to in the manner described in the definition of .

Now, we consider a particular case of functions belonging to . Let be the following function space:

Example 2.2.

Here there are some examples of classical probability distributions satisfying :

-

•

Exponential distribution : In this case, , and this implies with and ( and ).

-

•

Gamma distributions In this case, for and we obtain, using an asymptotic expansion of the incomplete gamma function (see Abramowitz and Stegun, 1964):

As a consequence, we deduce with

-

•

Absolute value of standardized Gaussian distribution : In this case, we can write , where is the complementary Gauss error function. But we know (see for instance Blair et al., 1976) that for , then . As a consequence, for any ,

(2.8) Consequently with

implying and .

-

•

Weibull distributions: In this case, with and , with and , for . Then it is obvious that and therefore with and (implying and ).

When , it is possible to specify the limit distribution of (2.7). Thus, we show the following result:

Proposition 2.

Assume that . Then

| (2.11) |

Such a result is interesting since it provides the asymptotic behavior of a vector of normalized and centered ratios . Its asymptotic distribution is the distribution of a vector of independent exponentially distributed r.v’s. However the parameters of these exponential distributions are different. Thus, if we consider the statistic

| (2.12) |

the computation of the cumulative distribution function of requires consideration of the function . This function converges quickly to when increases. Hence we numerically obtain that for , . Then we deduce from (2.11) and (2.12) that for ,

This implies that for instance that for and large enough,

with the computation of for each distribution. We remark that the ratio is the main contributor to the statistic and it contains almost all the information. For giving equivalent weights to the other ratios , and so as not to be troubled by the nuisance parameter , it is necessary to modify the statistic . Then we consider:

| (2.13) |

For and two sequences of real numbers, denote when . The following proposition can be established:

Proposition 3.

Assume that . Then, for a sequence satisfying and ,

| (2.16) |

In the case where , similar results can also be established, we demonstrated below.

Example 2.3.

Here there are some examples of classical distributions such as :

-

•

Pareto distribution : In this case, with and , for , and this implies with .

-

•

Burr distributions : In this case, for and positive real numbers. Thus for , implying with .

-

•

Absolute value of Student distribution with degrees of freedom: In the case of a Student distribution with degrees of freedom, the cumulative distribution function is with and therefore , where is the normalized beta incomplete function. Using the handbook of Abramowitz and Stegun (1964), we have the following expansion for , where is the usual Beta function. Therefore,

Consequently with .

Remark 2.

The case of standardized log-normal distribution is singular. Indeed, the probability distribution of is the same than the one of where . Therefore, implying . Using the previous expansion (2.8), we obtain for any :

Therefore, the standardized log-normal distribution is such that .

For probability distributions such as we obtain the following classical result (see also Embrechts et al., 1997):

Proposition 4.

Assume that . Then,

| (2.19) |

Hence the case of also provides interesting asymptotic properties on the ratios. In the forthcoming section devoted to the construction of an outlier detector from previous results, we are going to consider a test statistic which could be as well applied to distributions with functions belonging to and .

3 A new non-parametric outlier detector

We are going to consider the following test problem:

| (3.1) |

However we have to specify which kind of outlier and therefore which kind of contamination we consider. Our guide for this is typically the case of oversized regression residuals. Thus we would like to detect from when there is a ”gap” between numerous coming from a common probability distribution and one or several (but not a lot!) which are larger than the other one and generated from another distributions. As a consequence the previous test problem can be specified as follows:

| (3.2) |

A consequence of this specification is the following: we would like to detect outliers which appear as oversized data. Hence, under we could expect that there exists a ”jump” between the smallest outlier and the largest non contaminated data. As a consequence under we could expect that the ratio is larger than it should be.

For doing such a job, we propose to consider the following outlier detector based on ratios and which could be used as well when belongs to or . Hence, define:

| (3.3) |

Then, we obtain the following theorem:

Theorem 3.1.

Assume that . Then, for a sequence satisfying and ,

| (3.6) |

Remark 3.

In the definition of we prefer an estimation of the parameter of the exponential distribution with a robust estimator (median) instead of the usual efficient estimator (empirical mean), since several outliers could corrupt this estimation.

Therefore, Theorem 3.1 can be applied for distributions with belonging to or , i.e. as well as for Gaussian, Gamma or Pareto distributions. Hence, for a type I error , the outlier detector can be computed, and with ,

-

•

If then we conclude that there is no outlier in the sample.

-

•

If then the largest index such as indicates that we decide that the observed data can be considered as outliers, implying that there are detected outliers.

As a consequence this outlier detector allows a decision of the test problem (3.1) and also the identification of the exact outliers.

4 Monte-Carlo experiments

We are going to compare the new outlier detector defined in (3.3) with usual univariate outlier detectors. After giving some practical details of the application of , we present the results of Monte-Carlo experiments under several probability distributions.

Practical procedures of outlier detections

The definition of is simple, and in practice just requires the specification of parameters:

-

•

The type I error is the risk to detect outliers in the sample while there is no outlier. Hence, a natural choice could be the ”canonical” . However, we chose to be strict concerning the risk of false detection, i.e. we chose (as it was chosen by Tukey himself for building boxplots) which implies that we prefer not to detect ”small” outliers and hence we avoid to detect a large number of outliers while there is no outlier.

-

•

The number of considered ratios. On the one hand, it is clear that the smaller , the smaller the detection threshold, therefore more sensitive is the detector to the presence of outliers. On the other hand, the larger , the more precise is the estimation of the parameter of asymptotic exponential distribution (the convergence rate of is ) and larger is the possible number of detected outliers. We carried out numerical simulations using independent replications, for several probability distributions (the seven distributions presented below) for several values of the number of outliers , sample size and parameter . Results are reported in Table 1. A first conclusion: the larger and the larger test power. Another conclusion, but this is not a surprise, is the fact that the ”optimal” choice of depends on and .

As a consequence, for at least detecting outliers, we use that is an arbitrary choice satisfying and fitting well the results of these simulations, i.e. for , , for , and for , .

| 12 | 14 | 16 | 18 | 20 | 22 | 24 | 26 | 28 | |

|---|---|---|---|---|---|---|---|---|---|

| , | 0.595 | 0.588 | 0.583 | 0.573 | 0.568 | 0.565 | 0.561 | 0.557 | 0.554 |

| 0.694 | 0.708 | 0.702 | 0.696 | 0.694 | 0.689 | 0.686 | 0.683 | 0.679 | |

| , | 0.727 | 0.719 | 0.712 | 0.705 | 0.700 | 0.691 | 0.687 | 0.685 | 0.680 |

| 0.796 | 0.818 | 0.823 | 0.822 | 0.817 | 0.813 | 0.811 | 0.810 | 0.804 | |

| , | 0.760 | 0.752 | 0.744 | 0.738 | 0.732 | 0.727 | 0.722 | 0.716 | 0.711 |

| 0.822 | 0.848 | 0.857 | 0.858 | 0.856 | 0.853 | 0.850 | 0.847 | 0.844 | |

| , | 0.802 | 0.793 | 0.786 | 0.779 | 0.773 | 0.769 | 0.763 | 0.759 | 0.754 |

| 0.846 | 0.878 | 0.891 | 0.894 | 0.896 | 0.893 | 0.890 | 0.888 | 0.887 |

We have compared the new detector to five common and well-known univariate outlier detectors computed from the sample .

-

1.

The Student’s detector (see for instance Rousseeuw and Leroy, 2005): an observation from the sample will be consider as an outlier when where and are respectively the usual empirical mean and variance computed from , and is a threshold. This threshold is usually computed from the assumption that is a Gaussian sample and therefore , where denotes the quantile of the Student distribution with degrees of freedom for a probability .

-

2.

The Tukey’s detector (see Tukey, 1977) which provides the famous and usual boxplots: is considered to be an outlier from if , where , with and the third and first empirical quartiles of . Note that the confidence factor was chosen by Tukey such that the probability of Gaussian random variable to be decided as an outlier is close which is good trade-off.

-

3.

An adjusted Tukey’s detector as it was introduced and studied in Hubert and Vandervieren (2008): is considered to be an outlier from if , where is the medcouple, defined by , where is the sample median and the kernel function is given by . This new outlier detector improves considerably the accuracy of the usual Tukey’s detector for skewed distributions.

-

4.

The detector (see for instance Rousseeuw and Leroy, 2005): is considered as an outlier from if . The coefficient is obtained from the Gaussian case based on the relation , while the confidence factor is selected for building a conservative test.

-

5.

The Local Outlier Factor (LOF), which is a non-parametric detector (see for instance Breunig et al., 2000). This procedure is based on this principle: an outlier can be distinguished when its normalized density (see its definition in Breunig et al., 2000) is larger than or than a threshold larger than . However, the computation of this density requires to fix the parameter of the used -distance and a procedure or a theory for choosing a priori does not still exist. The authors recommend and (generally). We chose to fix , where is used for the computation of . Then, using the same kind of simulations than those reported in Table 1, we tried to optimize the choice of a threshold defined by: if then the observation is considered to be an outlier. We remark that it is not really possible to choose a priori and with respect to . Table 2 provides the results of simulations from independent replications and the seven probability distributions. We have chosen to optimize a sum of empirical type I (case ) and II (case and ) errors. This leads one to choose for as well as for .

| 2 | 4 | 6 | 8 | 10 | 12 | ||

|---|---|---|---|---|---|---|---|

| 0.903 | 0.447 | 0.285 | 0.222 | 0.174 | 0.150 | ||

| 1.000 | 1.000 | 1.000 | 0.996 | 0.961 | 0.863 | ||

| 1.000 | 0.860 | 0.422 | 0.232 | 0.141 | 0.106 | ||

| 0.955 | 0.533 | 0.328 | 0.237 | 0.196 | 0.179 | ||

| 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.995 | ||

| 1.000 | 1.000 | 0.981 | 0.888 | 0.744 | 0.581 |

Student, Tukey and detectors are more or less based on Gaussian computations. We would not be surprised if those methods failed to detect outliers when the distribution of is ”far” from the Gaussian distribution (but these usual detections of outliers, for instance the Student detection obtained on Studentized residuals from a least squares regression, are done even if the Gaussian distribution is not attested). Moreover, the computations of these detectors’ thresholds are based on an individual detection of outlier, i.e. a test deciding if a fixed observation is an outlier or not. Hence, if we apply them to each observation of the sample, the probability to detect an outlier increases with . This is not exactly the same as deciding whether if there are no outliers in a sample, which is the object of test problem (3.1).

Then, to compare these detectors to , it is appropriate to change the thresholds of these detectors following test problem (3.1) and its precision (3.2). Hence we have to define a threshold of this test from the relation . Therefore, from the independence property implying that has to satisfy when is large and close to (typically ). In the sequel we are going to compute the confidence factors of previous famous detectors to the particular case of absolute values of Gaussian variables. Hence, when for a random variable and if is large, then with . Then, we define:

-

1.

The Student detector : we consider that from is an outlier when , with implying (here we assume that is a large number inducing that the Student distribution with degrees of freedom could be approximated by the standard Gaussian distribution).

-

2.

The Tukey detector : we consider that from is an outlier when . In the case of the absolute value of a standard Gaussian variable, and implying .

-

3.

The detector : we consider that from is an outlier when . In the case of the absolute value of a standard Gaussian variable, and . This induces .

First results of Monte-Carlo experiments for samples without outlier: the size of the test

We apply the different detectors in different frames and for several probability distributions which are:

-

•

The absolute value of Gaussian distribution with expectation and variance , denoted (case );

-

•

The exponential distribution with parameter , denoted (case );

-

•

The Gamma distribution with parameter , denoted (case );

-

•

The Weibull distribution with parameters , denoted (case );

-

•

The absolute value of a Student distribution with degrees of freedom, denoted (case );

-

•

The standard log-normal distribution, denoted (not case or );

-

•

The absolute value of a Cauchy distribution, denoted (case ).

In the sequel, we will consider samples following these probability distributions, for and , and for several numbers of outliers.

We begin by generating independent replications of samples without outlier, which corresponds to be under . Then we apply the outlier detectors. The results are reported in Table 3.

| Av. Freq. | 0.007 | 0.008 | 0.008 | 0.008 | 0.010 | 0.010 | 0.018 |

| Av. Freq. LOF | 0.001 | 0.029 | 0.013 | 0 | 0.643 | 0.259 | 0.970 |

| Av. Freq. Student | 0.861 | 0.993 | 0.921 | 0.308 | 1 | 1 | 1 |

| Av. Freq. Tukey | 0.804 | 0.991 | 0.918 | 0.327 | 1 | 1 | 1 |

| Av. Freq. Adj. Tukey | 0.213 | 0.344 | 0.408 | 0.353 | 0.844 | 0.710 | 0.981 |

| Av. Freq. | 0.751 | 0.995 | 0.879 | 0.163 | 1 | 1 | 1 |

| Av. Freq. Student | 0.002 | 0.110 | 0.017 | 0 | 0.655 | 0.515 | 0.936 |

| Av. Freq. Tukey | 0.022 | 0.486 | 0.119 | 0 | 0.951 | 0.937 | 1 |

| Av. Freq. | 0.023 | 0.624 | 0.112 | 0 | 0.971 | 0.975 | 1 |

| Av. Freq. | 0.009 | 0.009 | 0.009 | 0.009 | 0.014 | 0.011 | 0.016 |

| Av. Freq. LOF | 0.005 | 0.023 | 0.019 | 0.001 | 0.843 | 0.281 | 0.998 |

| Av. Freq. Student | 1 | 1 | 1 | 0.986 | 1 | 1 | 1 |

| Av. Freq. Tukey | 1 | 1 | 1 | 0.939 | 1 | 1 | 1 |

| Av. Freq. Adj Tukey | 0.492 | 0.899 | 0.950 | 0.796 | 1 | 1 | 1 |

| Av. Freq. | 1 | 1 | 1 | 0.664 | 1 | 1 | 1 |

| Av. Freq. Student | 0.006 | 0.552 | 0.112 | 0 | 1 | 0.998 | 1 |

| Av. Freq. Tukey | 0.008 | 0.943 | 0.259 | 0 | 1 | 1 | 1 |

| Av. Freq. | 0.008 | 0.991 | 0.246 | 0 | 1 | 1 | 1 |

A first conclusion from this simulations is the following: as we already said, the original Student, Tukey and detectors can not be compared to the detector because their empirical sizes came out larger: they are not constructed to answer to our test problem. Therefore we are going now to consider only their global versions Student , Tukey and . Moreover, as they have been constructed from the Gaussian case, these second versions of detectors provide generally poor results in case of non-Gaussian distributions especially for Student, log-normal and Cauchy distributions (where outliers are always detected while there are no generated outliers).

Second results of Monte-Carlo experiments for samples with outliers

Now, we consider the cases where there is a few number of outliers in the samples . Denote the number of outliers, and a real number which represents a positive real number. We generated kinds of contaminations:

-

•

A shift contamination: instead of . We chose . By the way the cluster of outliers is necessarily separated from the cluster of non-outliers.

-

•

A multiplicative contamination: instead of . By the way the cluster of outliers is necessarily separated from the cluster of non-outliers.

-

•

A point contamination: instead of . We chose . By the way, the cluster of outliers is generally separated to the cluster of non-outliers (but not necessary, especially for Student or Cauchy probability distributions).

First, we consider the second versions of Student, Tukey and detectors. But we also consider parametric versions of these detectors, which are denoted Student-para, Tukey-para and -para: the thresholds and confidence factors are computed and used with the knowledge of the probability distribution of the sample (these thresholds change following the considered probability distributions). Hence, they are parametric detectors while or LOF are non-parametric detectors. We chose these parametric versions because they allow to obtain the same size of all the detectors and then a comparison of the test powers is more significant.

First results are reported in Tables 4 () and 5 () for shifted outliers ( or ). From Tables 4 and 5, it appears:

-

•

Student , as well as Student-para detectors are not really good choices for the detection of outliers because they are not robust statistics (the empirical variance is totally modified by the values of outliers).

-

•

Tukey and detectors provide more and less similar results. But even their parametric versions are not able to detect outliers for skewed distributions (Student, log-normal and Cauchy distributions). With the same size, clearly provides better results, even if they are not very accurate (especially for the Cauchy distribution).

-

•

LOF detector does not provide accurate results (especially when ). It is certainly a more interesting alternative in case of multivariate data.

| Av. Freq. | 0 | 0.007 | 0.008 | 0.008 | 0.008 | 0.010 | 0.010 | 0.018 |

|---|---|---|---|---|---|---|---|---|

| 5 | 0.998 | 0.562 | 0.574 | 1 | 0.848 | 0.813 | 0.066 | |

| 10 | 1 | 0.973 | 0.959 | 1 | 1 | 1 | 0.076 | |

| Av. Numb. | 5 | 5.12 | 5.23 | 5.25 | 5.14 | 5.09 | 5.07 | 9.17 |

| 10 | 10.60 | 10.64 | 10.58 | 10.62 | 10.05 | 10.05 | 10.01 | |

| Av. Freq. Student 2 | 0 | 0.001 | 0.111 | 0.018 | 0 | 0.655 | 0.515 | 0.934 |

| 5 | 0 | 0.013 | 0.004 | 0 | 0.538 | 0.411 | 0.687 | |

| 10 | 0 | 0 | 0 | 0 | 0.241 | 0.126 | 0.628 | |

| Av. Numb. | 5 | 0 | 1 | 1 | 0 | 1.04 | 1.02 | 1.67 |

| 10 | 0 | 0 | 0 | 0 | 1.01 | 1 | 1.66 | |

| Av. Freq. Tukey 2 | 0 | 0.022 | 0.483 | 0.118 | 0 | 0.951 | 0.937 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 10 | 1 | 1 | 0.999 | 1 | 1 | 1 | 1 | |

| Av. Numb. | 5 | 5.01 | 5.35 | 5.05 | 5 | 5.10 | 5.09 | 10.32 |

| 10 | 10 | 10.14 | 9.67 | 10 | 10 | 10 | 13.19 | |

| Av. Freq. 2 | 0 | 0.023 | 0.619 | 0.109 | 0 | 0.971 | 0.975 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 10 | 1 | 1 | 0.999 | 1 | 1 | 1 | 1 | |

| Av. Numb. | 5 | 5.01 | 5.67 | 5.06 | 5 | 5.24 | 5.37 | 12.66 |

| 10 | 10 | 10.38 | 9.86 | 10 | 10 | 12.16 | 16.43 | |

| Av. Freq. LOF | 0 | 0.001 | 0.029 | 0.013 | 0 | 0.643 | 0.259 | 0.970 |

| 5 | 0.998 | 0.521 | 0.123 | 1 | 0.309 | 0.129 | 1 | |

| 10 | 0.046 | 0.011 | 0 | 0.200 | 0.03 | 0.003 | 0.548 | |

| Av. Numb. | 5 | 5 | 3.97 | 2.86 | 5 | 2.71 | 2.03 | 3.39 |

| 10 | 9.11 | 1.10 | - | 9.47 | 1.56 | 1.40 | 2.27 | |

| Av. Freq. Student-para | 0 | 0.002 | 0 | 0.001 | 0.005 | - | 0 | - |

| 5 | 0 | 0 | 0 | 1 | - | 0 | - | |

| 10 | 0 | 0 | 0 | 0 | - | 0 | - | |

| Av. Numb. | 5 | 0 | 0 | 0 | 5 | - | 0 | - |

| 10 | 0 | 0 | 0 | 0 | - | 0 | - | |

| Av. Freq. Tukey-para | 0 | 0.022 | 0.013 | 0.014 | 0.025 | 0.008 | 0.009 | 0.007 |

| 5 | 1 | 0.991 | 0.960 | 1 | 0.009 | 0.026 | 0.005 | |

| 10 | 1 | 0.903 | 0.782 | 1 | 0.007 | 0.026 | 0.004 | |

| Av. Numb. | 5 | 5.01 | 4.87 | 4.40 | 5.01 | 1 | 1.03 | 1.94 |

| 10 | 10 | 7.27 | 4.50 | 10 | 1 | 1.01 | 1.88 | |

| Av. Freq. -para | 0 | 0.023 | 0.014 | 0.013 | 0.025 | 0.007 | 0.009 | 0.007 |

| 5 | 1 | 0.995 | 0.969 | 1 | 0.009 | 0.024 | 0.006 | |

| 10 | 1 | 0.966 | 0.867 | 1 | 0.008 | 0.025 | 0.005 | |

| Av. Numb. | 5 | 5.01 | 4.92 | 4.47 | 5.01 | 1 | 1.02 | 1.94 |

| 10 | 10 | 8.51 | 5.46 | 10 | 1 | 1.02 | 1.89 |

| Av. Freq. | 0 | 0.009 | 0.009 | 0.009 | 0.009 | 0.014 | 0.011 | 0.016 |

|---|---|---|---|---|---|---|---|---|

| 5 | 1 | 0.892 | 1 | 1 | 0.241 | 0.517 | 0.072 | |

| 10 | 1 | 0.997 | 0.991 | 1 | 0.987 | 1 | 0.088 | |

| Av. Numb. | 5 | 5.23 | 5.27 | 5.32 | 5.27 | 5.34 | 5.14 | 8.85 |

| 10 | 10.37 | 10.82 | 10.75 | 10.41 | 10.05 | 10.06 | 7.83 | |

| Av. Freq. Student 2 | 0 | 0.006 | 0.565 | 0.111 | 0 | 1 | 0.998 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| Av. Numb. | 5 | 5 | 5.02 | 5.01 | 5 | 4.69 | 4.98 | 4.74 |

| 10 | 10 | 10 | 9.97 | 10 | 7.73 | 9.75 | 4.59 | |

| Av. Freq. Tukey 2 | 0 | 0.008 | 0.949 | 0.256 | 0 | 1 | 1 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| Av. Numb. | 5 | 5.01 | 7.90 | 5.27 | 5 | 22.34 | 20.09 | 64.41 |

| 10 | 10.01 | 12.64 | 10.23 | 10.01 | 22.49 | 20.06 | 67.76 | |

| Av. Freq. 2 | 0 | 0.008 | 0.992 | 0.237 | 0 | 1 | 1 | 1 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| Av. Numb. | 5 | 5.01 | 9.86 | 5.26 | 5 | 26.94 | 28.52 | 83.04 |

| 10 | 10.01 | 14.55 | 10.23 | 10.01 | 27.10 | 28.46 | 86.59 | |

| Av. Freq. LOF | 0 | 0.001 | 0.029 | 0.013 | 0 | 0.843 | 0.281 | 0.970 |

| 5 | 1 | 0.802 | 0.473 | 1 | 0.291 | 0.113 | 0.65 | |

| 10 | 0.961 | 0.014 | 0.004 | 1 | 0.125 | 0.011 | 0.571 | |

| Av. Numb. | 5 | 5.01 | 4.27 | 3.37 | 5 | 2.21 | 1.21 | 3.07 |

| 10 | 9.93 | 3.36 | 3.50 | 10 | 1.96 | 1.63 | 2.92 | |

| Av. Freq. Student-para | 0 | 0.006 | 0.004 | 0.005 | 0.007 | - | 0 | - |

| 5 | 1 | 0.652 | 0.979 | 1 | - | 0 | - | |

| 10 | 1 | 0.017 | 0.275 | 1 | - | 0 | - | |

| Av. Numb. | 5 | 5 | 1.21 | 2.48 | 5.01 | - | 0 | - |

| 10 | 10 | 1 | 1.07 | 10 | - | 0 | - | |

| Av. Freq. Tukey-para | 0 | 0.008 | 0.008 | 0.008 | 0.010 | 0.007 | 0.007 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 0.007 | 0.013 | 0.007 | |

| 10 | 1 | 1 | 1 | 1 | 0.007 | 0.013 | 0.007 | |

| Av. Numb. | 5 | 5.01 | 5.01 | 5.01 | 1.02 | 1.95 | 1 | 2.00 |

| 10 | 10.01 | 10.01 | 9.93 | 10.01 | 1 | 1 | 2 | |

| Av. Freq. -para | 0 | 0.008 | 0.007 | 0.008 | 0.010 | 0.007 | 0.007 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 0.007 | 0.013 | 0.037 | |

| 10 | 1 | 1 | 1 | 1 | 0.008 | 0.013 | 0.007 | |

| Av. Numb. | 5 | 5.01 | 5.01 | 5.01 | 5 | 1.01 | 1.01 | 2 |

| 10 | 10.01 | 10.01 | 9.94 | 10.01 | 1 | 1 | 2 |

Those conclusions are confirmed when both the other contaminations (multiplicative and point) are used for generating outliers (see Table 6 and 7).

| Av. Freq. | 0 | 0.007 | 0.008 | 0.008 | 0.008 | 0.010 | 0.010 | 0.018 |

|---|---|---|---|---|---|---|---|---|

| 5 | 1 | 0.620 | 1 | 1 | 0.743 | 0.797 | 0.221 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.910 | |

| Av. Numb. | 5 | 5.03 | 5.04 | 5.03 | 5.03 | 5.05 | 5.03 | 5.17 |

| 10 | 10.01 | 10.01 | 10.01 | 10.01 | 10 | 10 | 10 | |

| Av. Freq. Student-para | 0 | 0.002 | 0 | 0.001 | 0.005 | - | 0 | - |

| 5 | 0.022 | 0 | 0.021 | 1 | - | 0 | - | |

| 10 | 0.019 | 0 | 0.022 | 0.190 | - | 0 | - | |

| Av. Numb. | 5 | 1 | 0 | 1 | 4.08 | - | 0 | - |

| 10 | 1 | 0 | 1 | 1.04 | - | 0 | - | |

| Av. Freq. Tukey-para | 0 | 0.022 | 0.013 | 0.014 | 0.025 | 0.008 | 0.009 | 0.007 |

| 5 | 1 | 0.983 | 1 | 1 | 0.065 | 0.304 | 0.024 | |

| 10 | 1 | 0.980 | 1 | 1 | 0.063 | 0.305 | 0.022 | |

| Av. Numb. | 5 | 5 | 3.83 | 5 | 5 | 1.03 | 1.21 | 1 |

| 10 | 9.99 | 4.45 | 9.84 | 10 | 1.03 | 1.19 | 1.01 | |

| Av. Freq. -para | 0 | 0.023 | 0.014 | 0.013 | 0.025 | 0.007 | 0.009 | 0.007 |

| 5 | 1 | 0.981 | 1 | 1 | 0.065 | 0.303 | 0.023 | |

| 10 | 1 | 0.977 | 1 | 1 | 0.063 | 0.303 | 0.022 | |

| Av. Numb. | 5 | 5 | 3.81 | 5 | 5 | 1.03 | 1.21 | 1 |

| 10 | 9.99 | 4.48 | 9.77 | 10 | 1.03 | 1.20 | 1.01 | |

| Av. Freq. | 0 | 0.009 | 0.009 | 0.009 | 0.009 | 0.014 | 0.011 | 0.016 |

| 5 | 1 | 1 | 1 | 1 | 0.933 | 0.997 | 0.200 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.947 | |

| Av. Numb. | 5 | 5.06 | 5.06 | 5.06 | 5.06 | 5.08 | 5.06 | 5.34 |

| 10 | 10.02 | 10.03 | 10.03 | 10.03 | 10.03 | 10.03 | 10.02 | |

| Av. Freq. Student-para | 0 | 0.006 | 0.004 | 0.005 | 0.007 | - | - | - |

| 5 | 1 | 0.996 | 1 | 1 | - | 0 | - | |

| 10 | 1 | 0.664 | 1 | 1 | - | 0 | - | |

| Av. Numb. | 5 | 5 | 2.46 | 5 | 5 | - | 0 | - |

| 10 | 10 | 1.25 | 5.10 | 10 | - | 0 | - | |

| Av. Freq. Tukey-para | 0 | 0.008 | 0.008 | 0.008 | 0.010 | 0.007 | 0.007 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 0.061 | 0.441 | 0.021 | |

| 10 | 1 | 1 | 1 | 1 | 0.061 | 0.443 | 0.021 | |

| Av. Numb. | 5 | 5 | 5 | 5 | 5 | 1.02 | 1.32 | 1.01 |

| 10 | 10 | 9.97 | 10 | 10 | 1.03 | 1.34 | 1.01 | |

| Av. Freq. -para | 0 | 0.008 | 0.007 | 0.008 | 0.010 | 0.007 | 0.007 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 0.061 | 0.441 | 0.021 | |

| 10 | 1 | 1 | 1 | 1 | 0.060 | 0.450 | 0.022 | |

| Av. Numb. | 5 | 5 | 5 | 5 | 5 | 1.03 | 1.32 | 1.01 |

| 10 | 10 | 9.97 | 10 | 10 | 1.03 | 1.34 | 1.01 |

| Av. Freq. | 0 | 0.007 | 0.008 | 0.008 | 0.008 | 0.010 | 0.010 | 0.018 |

|---|---|---|---|---|---|---|---|---|

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 0.719 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.979 | |

| Av. Numb. | 5 | 5.11 | 5.14 | 5.19 | 5.15 | 5.43 | 5.27 | 5.83 |

| 10 | 10.63 | 10.67 | 10.75 | 10.68 | 11.10 | 10.98 | 11.25 | |

| Av. Freq. Student-para | 0 | 0.002 | 0 | 0.001 | 0.005 | - | 0 | - |

| 5 | 0 | 0 | 0 | 1 | - | 0 | - | |

| 10 | 0 | 0 | 0 | 0 | - | 0 | - | |

| Av. Numb. | 5 | 0 | 0 | 0 | 5 | - | 0 | - |

| 10 | 0 | 0 | 0 | 0 | - | 0 | - | |

| Av. Freq. Tukey-para | 0 | 0.022 | 0.013 | 0.014 | 0.025 | 0.008 | 0.009 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 0.005 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.004 | |

| Av. Numb. | 5 | 5.01 | 5 | 5.01 | 5.01 | 5 | 5 | 1.01 |

| 10 | 10 | 10 | 10 | 10 | 10 | 10 | 1 | |

| Av. Freq. -para | 0 | 0.023 | 0.014 | 0.013 | 0.025 | 0.007 | 0.009 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 0.006 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.006 | |

| Av. Numb. | 5 | 5.01 | 5.01 | 5.01 | 5.01 | 5.01 | 5.01 | 1.03 |

| 10 | 10 | 10 | 10 | 10 | 10 | 10 | 1 | |

| Av. Freq. | 0 | 0.009 | 0.009 | 0.009 | 0.009 | 0.014 | 0.011 | 0.016 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 0.246 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.709 | |

| Av. Numb. | 5 | 5.23 | 5.27 | 5.32 | 5.26 | 5.69 | 5.28 | 7.76 |

| 10 | 11.03 | 11.11 | 11.22 | 11.13 | 11.09 | 11.35 | 12.73 | |

| Av. Freq. Student-para | 0 | 0.006 | 0.004 | 0.005 | 0.007 | - | 0 | - |

| 5 | 1 | 1 | 1 | 1 | - | 0 | - | |

| 10 | 1 | 1 | 1 | 1 | - | 0 | - | |

| Av. Numb. | 5 | 5 | 5 | 5 | 5 | - | 0 | - |

| 10 | 10 | 10 | 10 | 10 | - | 0 | - | |

| Av. Freq. Tukey-para | 0 | 0.008 | 0.008 | 0.008 | 0.010 | 0.007 | 0.007 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 0.007 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.007 | |

| Av. Numb. | 5 | 5.01 | 5.01 | 5.01 | 5.01 | 5.01 | 5.01 | 1 |

| 10 | 10.01 | 10.01 | 10.01 | 10.01 | 10.01 | 10.01 | 1.01 | |

| Av. Freq. -para | 0 | 0.008 | 0.007 | 0.008 | 0.010 | 0.007 | 0.007 | 0.007 |

| 5 | 1 | 1 | 1 | 1 | 1 | 1 | 0.007 | |

| 10 | 1 | 1 | 1 | 1 | 1 | 1 | 0.008 | |

| Av. Numb. | 5 | 5.01 | 5.01 | 5.01 | 5.01 | 5.01 | 5.01 | 1 |

| 10 | 10.01 | 10.01 | 10.01 | 10 | 10.01 | 10.01 | 1.01 |

Conclusions of simulations

The log-ratio detector provide a very good trade-off for the detection of outliers for a very large choice of probability distributions compared with usual outliers detectors or their fitted versions. The second non-parametric outlier detector, LOF, is not really as accurate (especially for ), its size is not controlled and results did not depend on the choice of (a theoretical study should be done for writing the threshold as a function of ).

5 Application to real data

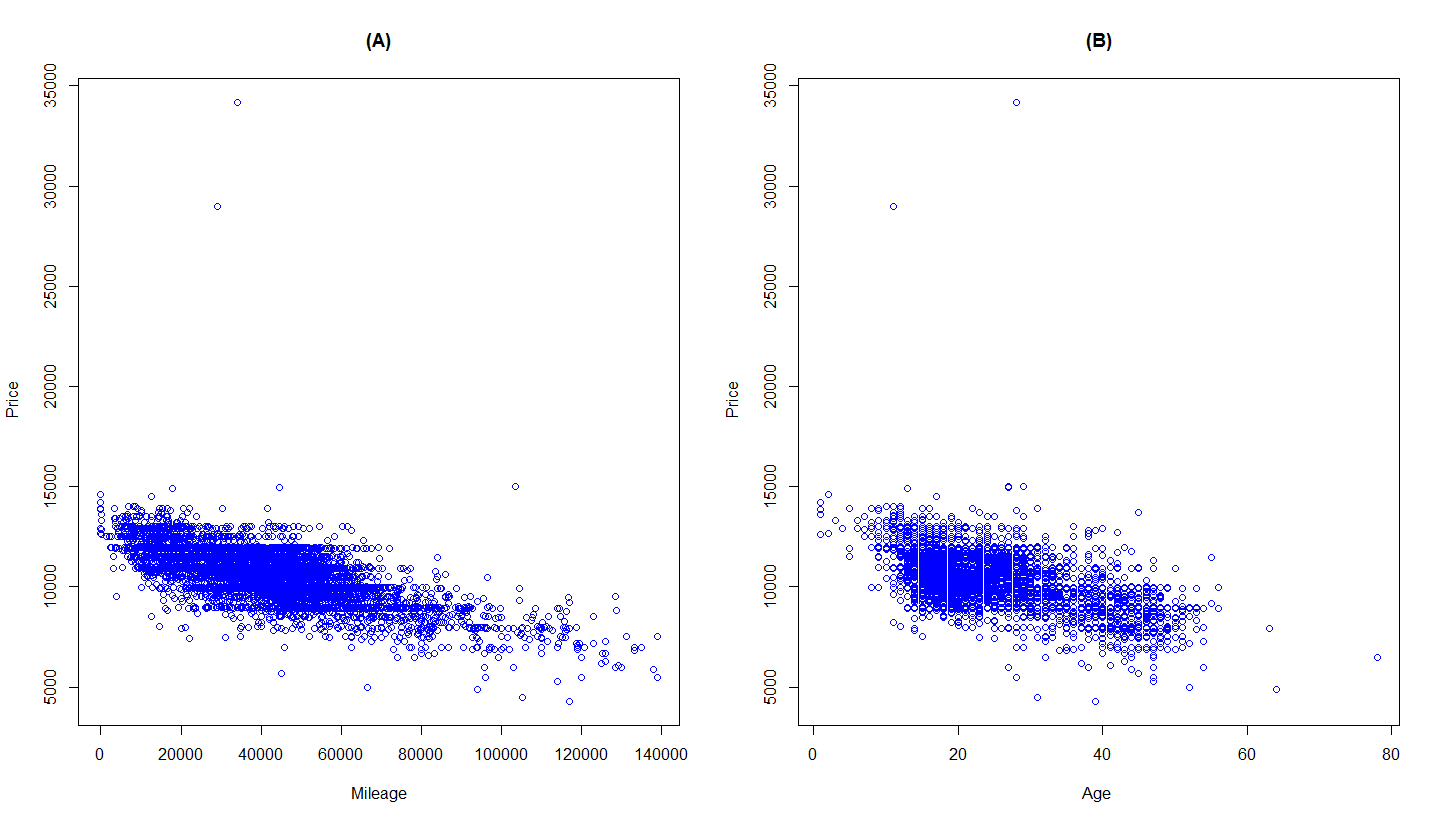

We apply the theoretical results to real datasets of detailed data on individual transactions in the used car market. The purpose of the experiment was to detect as many outliers as possible. The original dataset contains information about transactions on the car Peugeot 207 1.4 HDI 70 Trendy Berline including year and month which is the manufacture date, the price, and the number of kilometres driven. We then define variables: Age (the age of the car, in months), Price (in euros) and Mileage (in km). We chose these cars because they were advertised often enough to permit us to create a relatively homogeneous sample. Figure 1 depicts the relationship between the price and some variables: Price with Mileage, Price with Age. Such data were collected by Autobiz society, and can be used for forecasting the price of a car following its age and mileage. Hence it is crucial to construct a model for the price from a reliable data set including the smallest number of outliers.

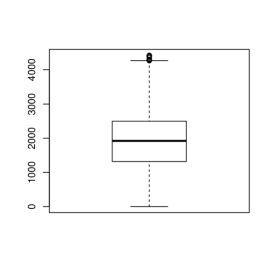

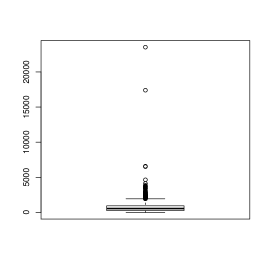

We now apply our test procedure to identify eventual outlying observations or atypical combination between variables. After preliminary studies, we chose two significant characteristics for each car of the sample. The first one is the number of kilometres per month. The second one is the residual obtained, after an application of the exponential function, from a robust quantile regression between the logarithm of the price as the dependent variable and Age and Mileage as exogenous variables (an alternative procedure for detecting outliers in robust regression has been developed in Gnanadesikan and Kettenring, 1972). The assumption of independence is plausible for both these variables’ residuals. Figure 2 exhibits the boxplots of the distributions of those two variables.

The outlier test is carried out on those two variables with (given by the empirical choice obtained in Section 4 with ). As the sample size is large, we can accept to eliminate data detected as outliers while there are not really outliers and we chose . The results are presented in Tables 8, 9 and 10. Note that, concerning the study of kilometres per month (km/m), we directly applied the test to this variable for detecting eventual ”too” large values, but also to for detecting eventual ”too” small values.

Conclusions of the applications

We first remark that we did not get the same outliers from the different analysis. It could be expected because the test on residuals worked as a multivariate test and identify atypical association between the three variables Age, Mileage and Price while the tests done on kilometres/month identifies outlying values in a bivariate case i.e. a typical association between the two variables Age and Mileage. From a practitioner’s point of view it may be advisable to apply the test for the two cases together one by one to be sure to detect the largest number of outliers. A second remark concerns the ”type” of the detected outliers. We can state that concerning kilometres/month, outliers are simply the largest values (the test did not identify outliers for ”too” small values). But for the regression residuals, the detected outliers clearly correspond to typing errors on the prices (the prices have been replaced by the mileages!). Thus, two kinds of outliers have been detected.

| Sample | t | Outliers | ||

|---|---|---|---|---|

| km/m (Sup) | 20 | 6.7232 | 5.96721 | |

| km/m (Inf) | 20 | 5.1200 | 5.96721 | |

| Res | 20 | 6.3322 | 5.96721 |

| Detected Outliers | Price | Mileage | Age | Kilometers per Month | Predicted Price |

|---|---|---|---|---|---|

| outlier(1) | 9590 | 70249 | 16 | 4391 | 9909 |

| outlier(2) | 11690 | 61484 | 14 | 4392 | 10286 |

| outlier(3) | 10490 | 61655 | 14 | 4404 | 10280 |

| outlier(4) | 9390 | 61891 | 14 | 4421 | 10272 |

| outlier(5) | 11500 | 39826 | 9 | 4425 | 11285 |

| outlier(6) | 11900 | 65411 | 15 | 4361 | 10111 |

| Detected Outliers | Price | Mileage | Age | Predicted Price |

|---|---|---|---|---|

| Outlier(1) | 34158 | 34158 | 28 | 10626 |

| Outlier(2) | 29000 | 29000 | 11 | 11600 |

6 Proofs

Proof of Proposition 1.

We begin by using the classical following result (see for example Embrechts et al. 1997):

| (6.1) |

where is a sequence of random variables such as for and is a sequence of i.i.d.r.v. with distribution . Consequently, we have

But for , . From the strong law of large numbers, , therefore since , we almost surely obtain:

Using once again the strong law of large numbers, we have almost surely. Hence, we can write for all ,

| (6.2) | |||||

using a Taylor expansion. By considering now the family defined by and the limit of the previous expansion, we obtain

| (6.3) |

The function is a continuous function on and therefore we obtain (2.7). ∎

Proof of Proposition 2.

We use the asymptotic relation (2.7). Since , for ,

But the random variable is absolutely continuous with respect to Lebesgue measure since and are independent random variables. Using once again the property (6.1), and since for an exponential distribution , , then

where is a sequence of i.i.d.r.v. following a distribution and is the order statistic from . Consequently,

With and using (2.7), this implies

The explicit computation of this probability is possible. Indeed:

Then, we obtain (2.11).

∎

Proof of Proposition 3.

Such a result can be obtained by modifications of Propositions 1 and 2. Indeed, we begin by extending Proposition 1 in the case where and . This is possible since with from usual Central Limit Theorem. Using the Delta-method, we also obtain with . Hence, for any , from (6.3),

Denote the cumulative distribution function of , and the one of . Then, using the second equation of the proof of Proposition 1, for all ,

with . But it is clear that the probability measure of is absolutely continuous with respect to the Lebesgue measure on . Thus, the partial derivatives of the function exist. Then from a Taylor-Lagrange expansion,

where . Hence, we obtain for some positive real numbers and . Consequently, we have:

Now, we are going back to the proof of Proposition 2 by computing . This leads to compute the following integral:

with , and with the same iteration than in the proof of Proposition 2, we obtain

Then, by considering the vector and the continuity of the function , we have for all

| (6.6) |

To achieve the proof, we use the Slutsky’s Theorem. Indeed, we have with . As a consequence,

| (6.7) | |||||

| (6.8) | |||||

| (6.9) |

with a family of i.i.d.r.v. with exponential distribution of parameter . Using the Law of Large Numbers and the condition , we deduce that

| (6.10) |

Then the proof can be concluded using (6.6), (6.10) and Slutsky’s Theorem. ∎

Proof of Proposition 4.

Proof of Theorem 3.1.

First consider the case . Using the proof of Proposition 1, we have

Consequently, using and therefore the definition of , we obtain:

To prove (3.6), it is sufficient to use again the proof of Proposition 3, to normalize the numerator and denominator with and therefore to consider , which converges in probability to (indeed, the median of the sample converges to which is the median of the distribution of the distribution).

When , we can use the same argument that the ones of the proof of Proposition 3 with replaced by (the reminder obtained from the definition of allows the achievement the proof when

is negligible compared to ).

∎

Acknowledgements. The authors are extremely grateful to the referees for their impressive and scrupulous reports with many relevant corrections, suggestions and comments which helped to improve the contents

of the paper. We also would like to thank Mia Hubert for having kindly provided R routines.

References

- Abramowitz and Stegun (1964) Abramowitz, M. and Stegun, I.A. (1964). Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. New York: Dover Publications.

- Barnett and Lewis (1994) Barnett,V. and Lewis, T. (1994). Outliers in Statistical Data. Wiley Series in Probability & Statistics, Wiley.

- Beckman and Cook (1983) Beckman, R.J. and Cook, R.D. (1983). Outlier….s, Technometrics, 25, 119-149.

- Beirlant et al. (2004) Beirlant, J., Goegebeur, Y., Teugels, J. and Segers, J. (2004). Statistics of Extremes: Theory and Applications. Wiley Series in Probability & Statistics, Wiley.

- Beirlant et al. (1996) Beirlant, J., Vynckiera P. and Teugels, J. (1996). Tail Index Estimation, Pareto Quantile Plots Regression Diagnostics, Journal of the American Statistical Association, 91, 1659-1667.

- Blair et al. (1976) Blair, J.M., Edwards C.A. and Johnson J.H. (1976). Rational Chebyshev approximations for the inverse of the error function, Math. Comp. 30, 827-830.

- Breunig et al. (2000) Breunig, M.M., Kriegel, H.-P., Ng, R.T. and Sander, J. (2000). LOF: Identifying Density-based Local Outliers. Proceedings of the 2000 ACM SIGMOD International Conference on Management of Data.

- Embrechts et al. (1997) Embrechts, P., Kleppelberg, C. and Mikosch, T. (1997). Modelling Extreme Events for Insurance and Finance. Springer.

- Gnanadesikan and Kettenring (1972) Gnanadesikan, R. and Kettenring, J.R. (1972). Robust estimates, residuals, and outlier detection with multiresponse data, Biometrics, 28, 81-124.

- Grubbs (1969) Grubbs, F.E. (1969). Procedures for Detecting Outlying Observations in Samples. Technometrics, 11, 1-21.

- Hawkins (1980) Hawkins, D.M. (1980). Identification of Outliers. Chapman and Hall

- Hill (1975) Hill, B. (1975). A simple general approach to inference about the tail of a distribution. The Annals of Statistics, 3, 1163-1174.

- Hubert et al. (2013) Hubert, M., Dierckx, G. and Vanpaemel, D. (2013). Detecting influential data points for the Hill estimator in Pareto-type distributions. Computational Statistics and Data Analysis, 65, 13-28.

- Hubert and Van der Veeken (2008) Hubert, M. and Van der Veeken, S. (2008). Outlier detection for skewed data. Journal of Chemometrics, 22, 235-246.

- Hubert and Vandervieren (2008) Hubert, M. and Vandervieren, E. (2008). An adjusted boxplot for skewed distributions. Computational Statistics and Data Analysis, 52, 5186-5201.

- Knorr et al. (2000) Knorr, E.M., Ng, R.T. and Tucakov, V. (2000). Distance-based outliers: algorithms and applications, The VLDB Journal, 8, 237-253.

- Rousseeuw and Hubert (2011) Rousseeuw, P.J. and Hubert, M. (2011). Robust statistics for outlier detection WIREs Data Min. Knowl. Disc., 1, 73-79.

- Rousseeuw and Leroy (2005) Rousseeuw, P.J. and Leroy, A.M. (2005). Robust Regression and Outlier Detection. Wiley Series in Probability and Statistics, Wiley.

- Tietjen and Moore (1972) Tietjen, G.L. and Moore, R.H. (1972). Some Grubbs-Type Statistics for the Detection of Several Outliers, Technometrics, 14, 583-597.

- Tse and Balasooriya (1991) Tse, Y.K. and Balasooriya, U. (1991). Tests for Multiple Outliers in an Exponential Sample, The Indian Journal of Statistics, Series B, 53, 56-63.

- Tukey (1977) Tukey, J.W. (1977). Exploratory data analysis. Reading, MA, Addison-Wesley.