Improved Second Order Estimation in the Singular Multivariate Normal Model

Abstract

We consider the problem of estimating covariance and precision matrices, and their associated discriminant coefficients, from normal data when the rank of the covariance matrix is strictly smaller than its dimension and the available sample size. Using unbiased risk estimation, we construct novel estimators by minimizing upper bounds on the difference in risk over several classes. Our proposal estimates are empirically demonstrated to offer substantial improvement over classical approaches.

keywords:

Covariance matrix, precision matrix, discriminant function, LDA, unbiased risk estimator, Moore-Penrose inverse, singular normal, singular Wishart.MSC:

Primary 62C15; secondary 62F10, 62H12.1 Introduction

With the recent explosion of high throughput data, much interest has arisen in applications where the number of feature parameters is greater than the sample size. In this situation, it is typically assumed that, despite their number, the underlying components are linearly independent, or in other words that their covariance matrix has full rank. However, little attention has been given to the situation where there is dependence between the components, that is, where the covariance matrix would be singular.

Recently, Tsukuma and Kubokawa (2015) investigated the problem of estimating the mean vector of a multivariate normal distribution when the unknown covariance matrix is singular. By deriving an unbiased risk estimator for the quadratic loss, they were able to give sufficient conditions for an estimator to dominate the maximum likelihood estimator.

This article is concerned with the same model as Tsukuma and Kubokawa (2015), but we consider three different estimation problems. Unlike the mean estimation problem, all three estimation scenarios depend the second order moment of the distribution. In each case we provide decision-theoretic results that lead to improved inference. The first task is the estimation of the singular covariance matrix itself, under an invariant squared loss. This problem was first considered in the full rank case by Haff (1980), and in the high-dimensional setting by Konno (2009). The second concern is the estimation of the Moore-Penrose pseudo-inverse of the covariance matrix, also known as the precision matrix, under the Frobenius loss. This problem was first considered in the full rank case by Haff (1977, 1979a) and in the high-dimensional setting by Kubokawa and Srivastava (2008).

Finally, we consider the problem of estimating the discriminant coefficient that arise in Linear Discriminant Analysis (LDA) under the squared loss, a problem first considered in the full rank case by Haff (1986) and Dey and Srinivasan (1991). LDA is a standard method for classification when the number of observations is much larger than the number of features . If data follows -variate normal distribution with the same covariance structure across the groups, it provides an asymptotically optimal classification rule, meaning that its misclassification error converges to Bayes risk. However, it was noted by Dudoit et al. (2002) that a naive implementation of LDA for high-dimensional data provides poor classification results in comparison to alternative methods. A rigorous proof of this phenomenon in the case is given by Bickel and Levina (2004). There are two main reasons for this. First, standard LDA uses the sample covariance matrix to estimate the covariance structure, and in high dimensional settings this results in a singular estimator. Secondly, by using all features in classification, interpretation of the results becomes challenging. One of the popular approaches to deal with the singularity is to use the independence rule which overcomes the singularity problem of the sample covariance but ignores the dependency structure. This approach is very appealing because of its simplicity and was encouraged by the work of Bickel and Levina (2004), who showed it performs better than the standard LDA in a setting when the population matrix is full rank. Unfortunately, independence is only an approximation and it is unrealistic in most applications: for instance, in a genomic context, gene interactions and low dimensional network structure are crucial for the understanding of biological processes. In this situation, one should aim for better estimators of the covariance matrix rather than relying on an independence structure that assumes a full rank population covariance matrix. Indeed, we will see in Section 3 that using the diagonal of the sample covariance matrix is a poor strategy if the true covariance matrix is rank deficient.

The presentation of our approach to these three estimation problems is divided as follows. The decision-theoretic results are described in Section 2. For each of the three problems, we construct an appropriate unbiased estimator of the risk (URE) using Stein’s and Haff’s lemmas (Stein, 1986; Haff, 1979b; Tsukuma and Kubokawa, 2015). We then consider the class of estimator given by constant multiples of a naive estimator, and minimize an upper bound on the difference in risk to obtain estimators that dominate the naive estimator. Finally, we consider a larger class given by the sum of this estimator and an appropriate trace, and again minimize an upper bound on the risk to obtain a dominating estimator.

2 Estimation Results

2.1 Model

Our setting is similar to the one used in Tsukuma and Kubokawa (2015). We observe an -sample identically and independently distributed from a -dimensional multivariate normal distribution , where and are unknown. However, the -dimensional covariance matrix is rank-deficient with respect to the dimension and the sample size, in the sense that

| (2.1) |

The resulting singular multivariate normal distribution does not have a density with respect to the Lebesgue measure on , but lives in the -dimensional linear subspace spanned by the columns of . More details can be found, for example, in Srivastava and Khatri (1979, Section 2.1).

Define the data matrix . The sample covariance matrix then follows a Wishart distribution with degrees of freedom. Since is rank-deficient, it is singular in the terminology of Srivastava and Khatri (1979, Section 3.1). We warn the reader that the expression “singular Wishart” has also been used in the literature to describe the different situation where the covariance is positive-definite and the dimension exceeds the degrees of freedom, as in Srivastava (2003). Let denote the reduced spectral decomposition of , where denote the non-zero eigenvalues and is semi-orthogonal.

In this situation, neither nor are invertible. Since inverses of covariance matrix are of considerable interest in multivariate statistical analysis, some generalized inverse of these quantities is desirable. In this article, we will focus on the Moore-Penrose pseudoinverse, which will be denoted for a matrix . Definitions and theoretical properties can be found in Harville (1997, Chapter 20).

The singular multivariate normal model is amenable to decision-theoretic analysis through a key insight of Tsukuma and Kubokawa (2015, Section 2.2). The authors proved that when (2.1) holds, the subspace spanned by the sample covariance matrix is almost surely constant and matches the subspace spanned the true covariance matrix, in the sense that the remarkable identity holds

| (2.2) |

This fact will be repeatedly used in the Section 5 proofs and is essential to our derivations.

Let us now turn our attention to the three problems we wish to solve. In terms of the notation introduced above, these are:

-

Covariance matrix estimation. The estimation of under the invariant squared loss .

-

Precision matrix estimation. The estimation of under the Frobenius loss .

-

Discriminant coefficient estimation. The estimation of under the square loss .

The traditional estimators for and are the sample mean and covariance , which suggests the corresponding naive estimators , and for each respective problem. In the next three subsections we will see traditional estimators are not admissible and improved estimators will be developed.

2.2 Covariance matrix estimation

The standard estimator for a covariance matrix is the sample covariance matrix . An alternative is the unbiased estimator , which corrects for the loss in degrees of freedom from not knowing . We will look for estimators that improve over these benchmarks and study their performance.

We first show that an unbiased estimator of the risk holds for orthogonally invariant estimators, that is, estimators of the form with twice-differentiable functions of .

Theorem 1 (Unbiased risk estimation for singular covariance matrices).

Let and define

Assume the regularity conditions

| (2.3) |

We then have

| (2.4) |

Let us now consider estimators that are proportional to the sample covariance matrix, that is, of the form for constant. The following result provides the optimal proportionality factor.

Proposition 1.

Let . The optimal estimator of of the form for a deterministic constant is , with risk

In particular dominates , which itself dominates .

Thus and are inadmissible. We can further extend this result by considering a larger class of estimators of the form for constant. Estimators of this shape were first considered by Haff (1980). Although computing the exact risk of these estimators is difficult, it is possible to bound the difference in risk with the one of as follows.

Proposition 2.

Let . Then the risk of estimators of the form for can be bounded by

| (2.5) |

The constant that minimizes this upper bound is . When , the estimator dominates .

Thus is itself inadmissible for . Although this result does not show optimal within the class, the estimator is likely to have good overall risk properties.

2.3 Precision matrix estimation

A standard estimator for a singular precision matrix is the Moore-Penrose pseudoinverse of the sample covariance matrix . Note that by Muirhead (1982, Page 97, Equation (12)) we have

for . Thus in this case an alternative could be the unbiased estimator . We will look for estimators that improve over these benchmarks and study their performance.

We first show that an unbiased estimator of the risk holds for orthogonally invariant estimators, that is, estimators of the form with twice-differentiable functions of .

Theorem 2 (Unbiased risk estimation for singular precision matrices).

Let . Assume the regularity condition

Then

Let us now consider estimators that are proportional to the Moore-Penrose inverse of the sample covariance matrix, that is, of the form for constant. The following optimality result holds over this class.

Proposition 3.

Let . The risk of estimators of the form for can be bounded in terms of the risk of by

| (2.6) |

The constant that minimizes this upper bound is , and the corresponding estimator dominates , which itself dominates .

Thus and are inadmissible. Note that our bound on the risk only holds for : presumably, estimators with do not dominate , but we have not been able to prove this hypothesis.

In any case, we can further extend this result by considering a larger class of estimators of the form for constant. Estimators of this form were first considered by Efron and Morris (1976). It is possible to bound the difference in risk with the one of as follows.

Proposition 4.

Let . The risk of estimators of the form for can be bounded in terms of the risk of through

| (2.7) |

The constant that minimizes this upper bound is , and the corresponding estimator dominates .

Thus is itself inadmissible. Again, although these results do not show and optimal within their classes, they are likely to possess good overall risk properties.

2.4 Discriminant coefficients estimation

A standard estimator for a singular discriminant coefficient is . Note that since and are independent, we have

for . Thus in this case an alternative could be the unbiased estimator . We will look for estimators that improve over these benchmarks and study their performance.

We first show that an unbiased estimator of the risk holds for estimators of the form with twice-differentiable functions of .

Theorem 3 (Unbiased risk estimation for singular discriminant coefficients).

Let with

Assume the regularity conditions

Then

Let us now consider estimators that are proportional to the naive estimator, that is, of the form for constant. The following optimality result holds over this class.

Proposition 5.

Let . The risk of estimators of the form for can be bounded in terms of the risk of by

| (2.8) |

The constant that minimizes this upper bound is , and the corresponding estimator dominates , which itself dominates .

Thus and are inadmissible. Again, note that our bound on the risk only holds on the subset . Presumably, estimators with do not dominate , but we have not been able to prove this result.

We can further extend this result by considering a larger class of estimators of the form for constant. Estimators of this form were first considered by Dey and Srinivasan (1991). It is possible to bound the difference in risk with the one of as follows.

Proposition 6.

Let . The risk of estimators of the form for can be bounded in terms of the risk of through

| (2.9) |

The constant that minimizes this upper bound is , and the corresponding estimator dominates .

Thus is itself inadmissible. One again, although these results do not show and optimal within their classes, they are likely to have good overall risk properties.

3 Numerical study

In this section we investigate the risk performance of the proposed estimator for covariance, precision and discriminant coefficients estimation through two simulation studies. We also consider the performance of the diagonal of the sample covariance matrix, . In various applications, using this estimator is a popular approach to overcome the singularity problem of the sample covariance. Although it ignores the dependency structure, this estimator is appealing because of its simplicity, and was suggested by the results of Bickel and Levina (2004).

3.1 Autoregressive simulation

We let be , , and . For each from to , we constructed the true covariance matrix from an autoregressive structure with coefficient and set its smallest eigenvalues to zero to create a rank matrix, as described in Algorithm 1. We then randomly generated replications from a multivariate normal distribution with mean and singularized autoregressive covariance , and computed the resulting sample covariance matrix .

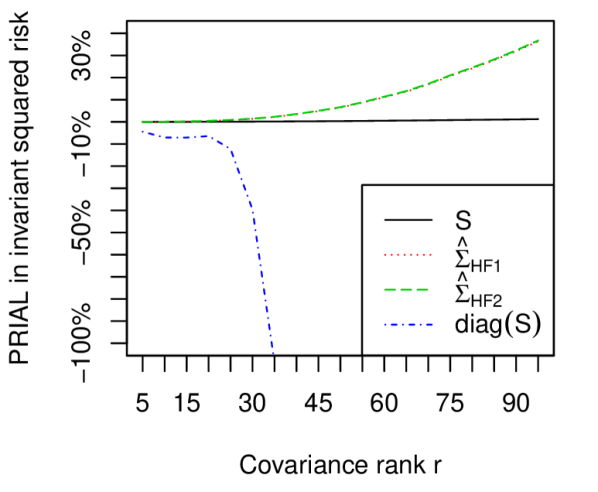

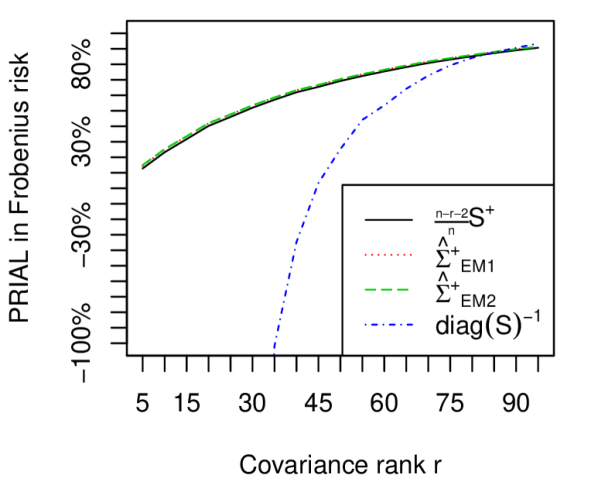

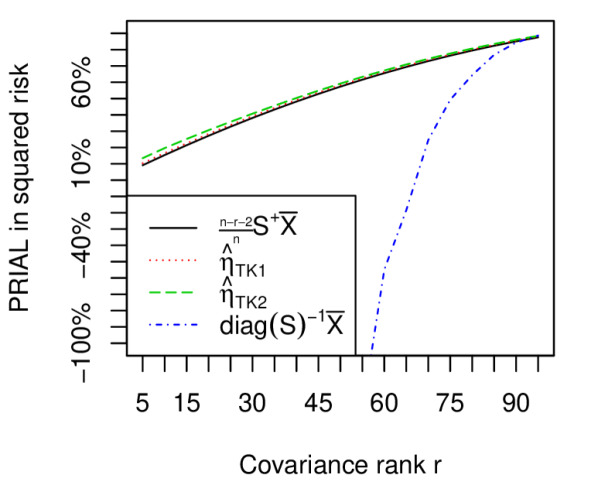

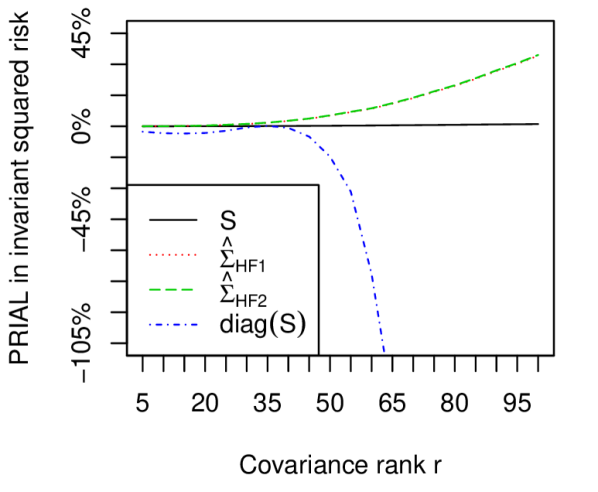

For the covariance matrix estimation problem, we computed the Percentage Reduction In Average Loss (PRIAL) with respect to in invariant squared loss for four estimators. The first three are the estimators , and considered in Subsection 2.2. We also included as fourth estimator the diagonal of the sample covariance matrix . The simulation results are given in Figure 1. We notice that and behave similarly, and both improve substantially on , while the diagonal estimator does much worse.

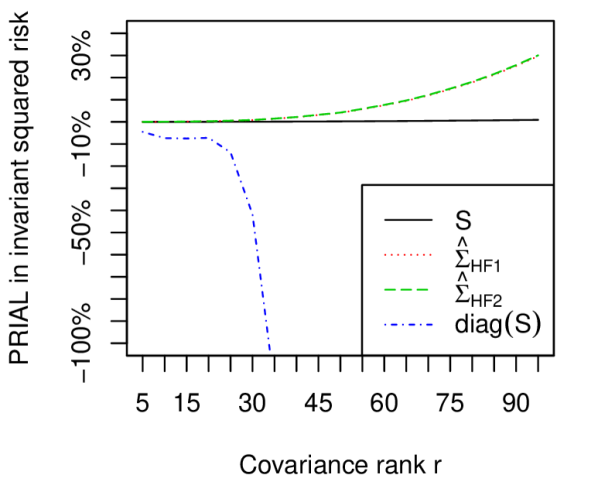

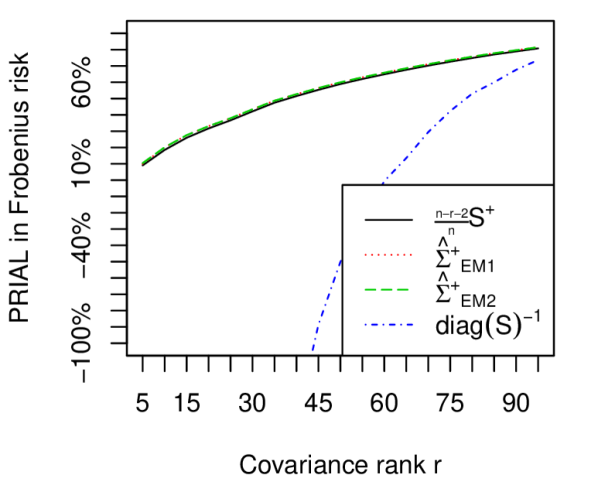

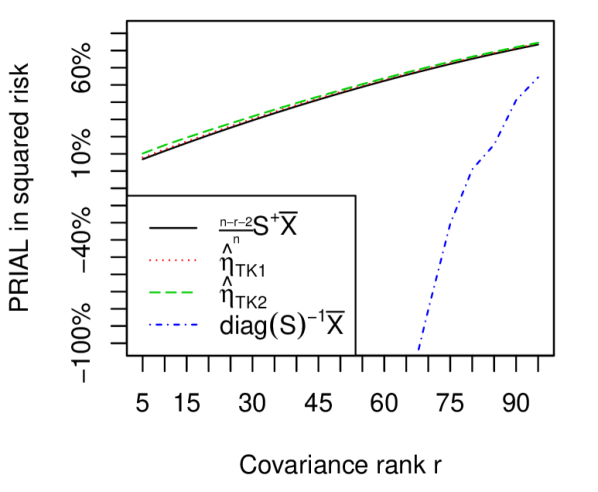

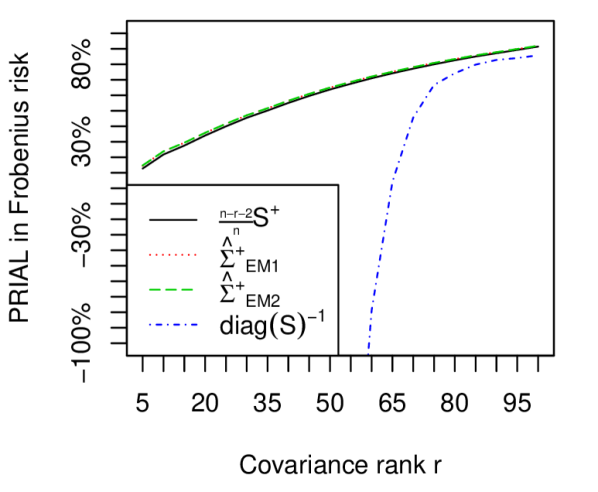

Similarly, for the precision matrix estimation problem, we estimated the PRIAL with respect to in the Frobenius loss for four estimators. The first three are the estimators , and from Subsection 2.3. The fourth one is the inverse of the diagonal of the sample covariance matrix, . The simulation results are given in Figure 2. We can see that all first three estimators improve substantially over , but do not differ significantly in risk. In contrast, the diagonal estimator performs well when the true matrix is almost full rank, but becomes worse and worse for smaller covariance ranks.

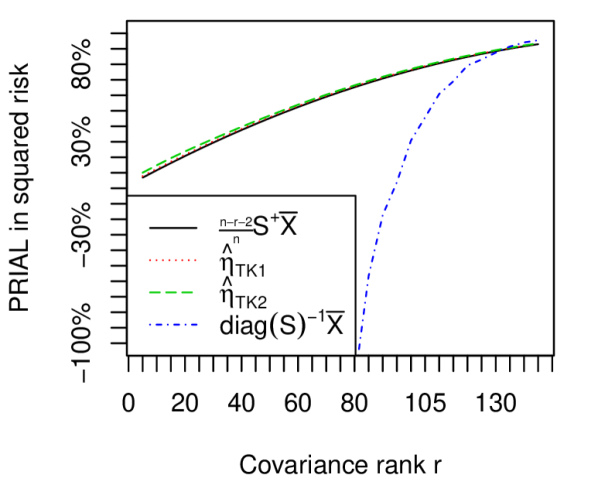

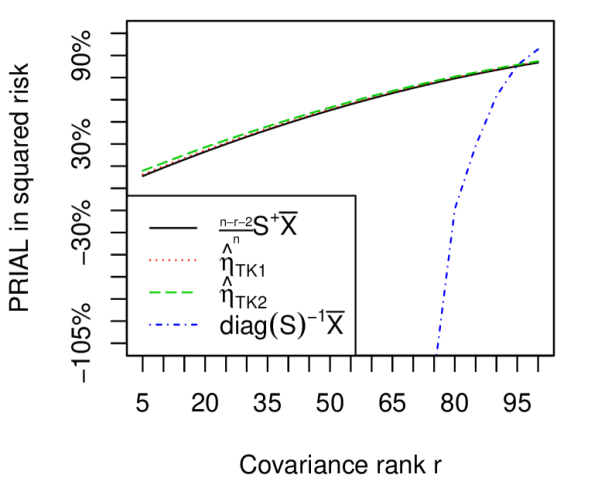

Finally, for the discriminant coefficient estimation problem, we estimated the PRIAL with respect to in the square loss for four estimators. The first three estimators are , and , which were considered in Subsection 2.4. The fourth one is the estimator , which has been considered in linear discriminant analysis when . The simulation results are given in Figure 3. In this case again, all first three estimators have similar risk and substantially improve on the naive estimator, , while the diagonal estimator is acceptable only when the true covariance matrix is almost full rank and quite bad otherwise.

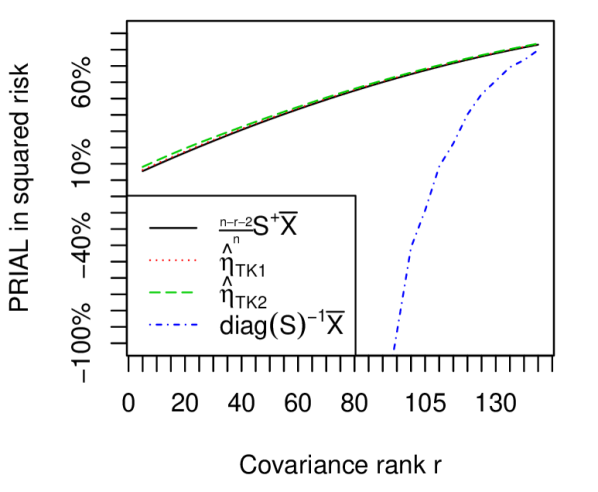

3.2 NASDAQ-100 simulation

To explore more realistic designs than an autoregressive covariance matrix, we also considered a setting where the true covariance matrix was constructed from real data.

The NASDAQ-100 is a stock market index composed of the hundred largest non-financial companies on the NASDAQ. As of 2015, this is composed of 107 securities, since some companies offer several classes of stock. We computed the net daily returns of these assets up to March 6, 2015. The newest security is Liberty Media Corp Series C (LMCK), which was issued to series A and B shareholders as dividend on July 7, 2014. To avoid missing data issues, we took this date as the initial time point. This yielded a sample size of 167 trading days. From this data we computed a sample covariance matrix of the NASDAQ-100 returns.

We then proceeded with the risk simulation as follows. For every from 1 to , the true covariance matrix was defined as the NASDAQ-100 sample covariance matrix with its smallest eigenvalues set to zero. We then randomly generated replications from a multivariate normal distribution with mean and singular covariance , and computed the resulting sample covariance matrix .

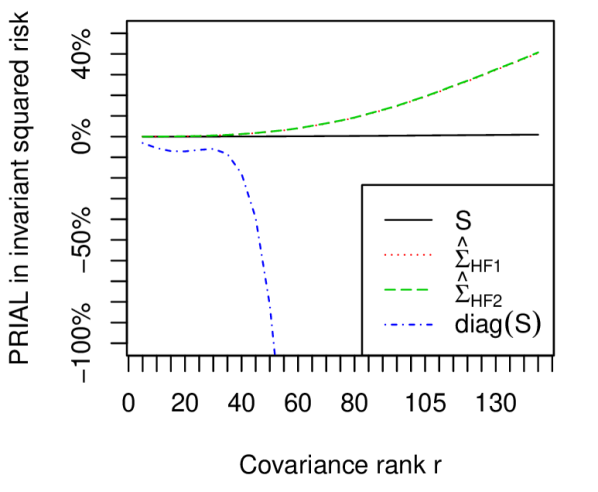

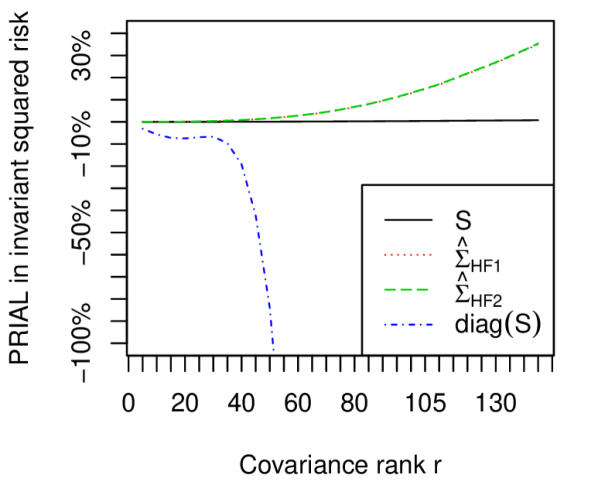

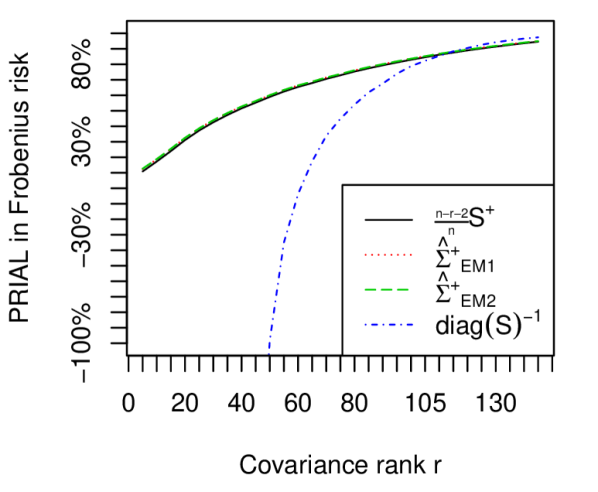

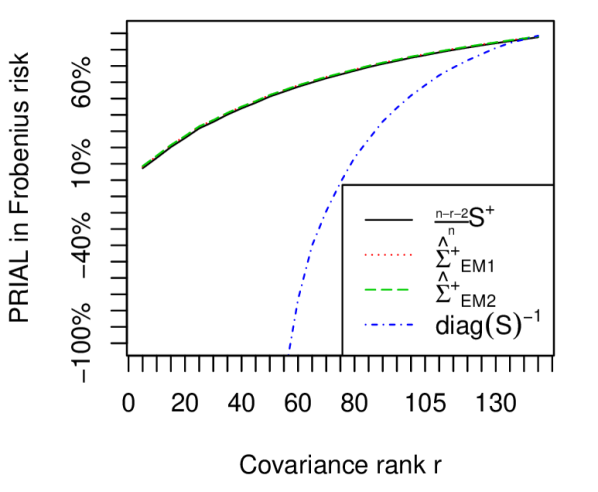

For each of the three estimation problems, we computed the PRIAL as in Subsection 3.1. The simulation results are given in Figure 4. The results appear similar to the singularized autoregressive setting.

4 Discussion

An application of the Tsukuma and Kubokawa (2015) technique developed in Subsection 2.1 allows in essence to reduce the dimension from to . Since , this in effect turns the problem into a classical setting where the sample size is greater than the dimension, and allows for classical proof techniques to be applied.

An interesting extension is the setting where . In that case, an adaptation of the method would yield a high-dimensional context where the true covariance matrix is full rank, but the sample size is still smaller than the dimension . Recent work, for example by Konno (2009), could allow the construction of improved estimators analogous to the ones presented in this article.

Recent attention has been given to the notion of the effective rank of a matrix , developed by Vershynin (2010)and applied in the study of spiked covariance matrices in Bunea and Xiao (2015). Singular covariance matrices can be regarded as a boundary case of spiked matrices where the noise equals zero. In that regard, it is interesting to notice that the quantity that appear in inequality (2.5) is related to the effective rank of through the inequality

The presence of this quantity is likely connected to the orthogonal invariance of the loss function.

The some of the key results in Bickel and Levina (2004) can be extended to the case where . Suppose is known and let and equal the limiting Bayes risk of the classification rule using and , respectively. By an application of an extended Kantorovich inequality for generalized inverses, developed by Liu and Neudecker (1997), it can be shown that , where is the Gaussian survival function and with the non-zero eigenvalues of . In the setting of Bickel and Levina (2004), is assumed to be full rank so that the limiting Bayes risk of the classification rule using is close to optimal. However, in the rank deficient case for , which implies that the diagonal rule give rise to a procedure that is no better than random guessing, that is with . This behavior is evident from Figures 3 and 4. In the case where the rank is close to , the risk of the diagonal based discriminant estimator is close to the improved estimates, however, as the rank of declines from the risk properties of the diagonal based discriminant estimator become inferior.

Finally, in applications where a singular covariance matrix is unlikely but a low-dimensional approximation is desired, it might be beneficial to use one of the estimators proposed in this article and cross-validate the rank on the task to accomplish. For example, a mean-variance portfolio optimization problem could use as precision matrix estimate, with rank cross-validated on some validation set. To the best of our knowledge, this methodology has no theoretical grounding but might nevertheless prove useful in some high-dimensional problems.

5 Proofs

5.1 Preliminaries

Before presenting the proofs of the statements from Section 2, we explain the techniques employed by Tsukuma and Kubokawa (2015) to work around the singularity of the covariates in the model. Define the sample mean and covariance matrix to be

Since has rank , we can factorize it as for some full rank matrix . Let and - then is semi-orthogonal and , is invertible, and . Since is rank deficient, there must be a such that , and therefore we can write for . Define then

Notice how is full rank, since , in contrast with . Using , we can see that these constructions are related to and through

Recall that almost surely, from Equation (2.2). Since has rank , there must be a semi-orthogonal matrix such that , almost surely and for . The matrix is easily seen to be orthogonal, and so by , we see that and must share the same non-zero eigenvalues, i.e. .

These constructions and facts form the basis of our risk estimation procedures and the notation will be repeatedly used in the following subsections.

5.2 Proofs of Subsection 2.2

Proof of Theorem 1.

Since and share the same non-zero eigenvalues, we can regard as a function of only. Since and is full rank, we can apply Lemma 1 and 2 of Chételat and Wells (2014) to . On that result, one can also consult Sheena (1995, Theorem 4.1), and in the singular case Kubokawa and Srivastava (2008, Proposition 2.1) and Konno (2009, Theorem 2.4). In any case, we get

under the regularity conditions

But these are satisfied by Inequalities (2.3). This concludes the proof. ∎

Proof of Proposition 1.

Proof of Proposition 2.

Again, let us apply the results of Theorem 1. Here , so using that we find

Let us now compute the terms in the URE. We find for the first term:

Next, using the fact that and that , we find

Finally, using that and we can bound

Hence the URE (2.4) equals

Now note that and . Then since and we can write

| (5.1) |

Now, using that we find

and by (5.1)

Thus all the regularity conditions of Theorem 1 are satisfied, and we find

which proves inequality (2.5). To minimize this upper bound, notice that since , it is enough to minimize the quadratic coefficient . This is achieved precisely when . When , this makes this quadratic coefficient strictly negative, which in view of Proposition 1 guarantees

Thus in this case dominates , as desired. ∎

5.3 Proofs of Subsection 2.3

Proof of Theorem 2.

Since and share the same non-zero eigenvalues, we can regard as a function of only. Since and is full rank we can apply Lemma 2.1 from Dey (1987). However, the proposition is given without proof and, more importantly, without the implied regularity conditions that inevitably come from using Stein’s and Haff’s lemmas. For completeness, we therefore derive again this result in our context. First, we can write

By Lemma 3 of Chételat and Wells (2014), this equals

under the regularity condition

The result follows from the fact that . ∎

Proof of Proposition 3.

We have , so

Summing everything, we get the URE

Now notice that

Since , by Theorem 2.4.14 (viii) from Kollo and von Rosen (2006) we have the bound

| (5.2) |

when , which holds since . Therefore, the regularity condition hold and we can apply Theorem 2 to conclude that

for any . Thus, in particular, the risk of the unbiased estimator must equal . When we can bound

which shows inequality 2.6. This upper bound has a minimum at , which yields

Thus dominates , as desired. Moreover, the URE of is and so

so dominates , as claimed. ∎

Proof of Proposition 4.

We have , so

Summing everything, we get the URE

Now note, using and that

since by equation (5.2). Therefore, we can apply Theorem 2 to obtain

for all . Using that and again, we can bound the difference in risk as

which proves inequality (2.7). There is a minimum in since , which is . In this case the quadratic coefficient and thus the difference in risk is strictly negative, so the corresponding estimator dominates , as desired. ∎

5.4 Proofs of Subsection 2.4

Proof of Theorem 3.

Since and share the same non-zero eigenvalues, we can regard as a function of only. Moreover, . Using that almost surely, we find

Define and notice it is independent of since and are independent. Then

The first term can be handled as follows. By independence of and , and Stein’s lemma (Fourdrinier and Strawderman, 2003, Lemma A.1), we get

under the condition

For the second term, we will make use of the fact that

| (5.3) |

where is defined as the statement. This is the result of a non-singular analogue of Theorem 2.2 from Konno (2009), or alternatively of a matrix analogue of Lemma 3 from Chételat and Wells (2014). By appropriate modifications to the latter result and the underlying Lemma 3 from Chételat and Wells (2012) on which it depends, it can be seen that sufficient conditions for equation 5.3 to hold are

A sufficient condition for this to happen is

Then, using the independence of and , we can conclude

Thus

But and . Hence

This proves the result. ∎

Proof of Proposition 5.

We have , so

We can bound

so by inequality (5.2) and the fact that these two expressions are finite. Therefore, we can apply the results of Theorem 3 to obtain

for any . Therefore, for we can bound the difference in risk by

which proves inequality (2.8). The quadratic coefficient is minimized at , at which point we have

Thus dominates , as desired. Moreover,

so dominates , as claimed. ∎

Proof of Proposition 6.

We will apply 2, and we have here for , so

Therefore,

We can bound

so by , inequality (5.2) and the fact that these two expressions are finite. Therefore, we can apply the results of Theorem 3 to obtain

for any . Therefore, the difference in risk can be written

But , so we can bound

Next, write the reduced singular value decomposition of as with semi-orthogonal, . Then

Therefore, we can bound by

which proves (2.9). Since , the quadratic coefficient has a minimum, at . In this case we have

Thus dominates , as desired. ∎

References

- Tsukuma and Kubokawa (2015) H. Tsukuma, T. Kubokawa, Estimation of the mean vector in a singular multivariate normal distribution, Journal of Multivariate Analysis 140 (2015) 245 – 258.

- Haff (1980) L. Haff, Empirical Bayes estimation of the multivariate normal covariance matrix, Annals of Statistics 8 (1980) 586–597.

- Konno (2009) Y. Konno, Shrinkage estimators for large covariance matrices in multivariate real and complex normal distributions under an invariant quadratic loss, Journal of Multivariate Analysis 100 (2009) 2237–2253.

- Haff (1977) L. Haff, Minimax estimators for a multinormal precision matrix, Journal of Multivariate Analysis 7 (1977) 374–385.

- Haff (1979a) L. Haff, Estimation of the inverse covariance matrix: random mixtures of the inverse Wishart matrix and the identity, Annals of Statistics 7 (1979a) 1264–1276.

- Kubokawa and Srivastava (2008) T. Kubokawa, M. Srivastava, Estimation of the precision matrix of a singular Wishart distribution and its application in high-dimensional data, Journal of Multivariate Analysis 99 (2008) 1906–1928.

- Haff (1986) L. Haff, On linear log-odds and estimation of discriminant coefficients, Communications in Statistics-Theory and Methods 15 (1986) 2131–2144.

- Dey and Srinivasan (1991) D. Dey, C. Srinivasan, On estimation of discriminant coefficients, Statistics & Probability Letters 11 (1991) 189–193.

- Dudoit et al. (2002) S. Dudoit, J. Fridlyand, T. P. Speed, Comparison of discrimination methods for the classification of tumors using gene expression data, Journal of the American Statistical Association 97 (2002) 77–87.

- Bickel and Levina (2004) P. Bickel, E. Levina, Some theory for Fisher’s linear discriminant function, ‘naive Bayes’, and some alternatives when there are many more variables than observations, Bernoulli 10 (2004) 989–1010.

- Stein (1986) C. Stein, Lectures on the theory of estimation of many parameters, Journal of Soviet Mathematics 34 (1986) 1373–1403.

- Haff (1979b) L. Haff, An identity for the Wishart distribution with applications, Journal of Multivariate Analysis 9 (1979b) 531–544.

- Srivastava and Khatri (1979) M. Srivastava, C. Khatri, An Introduction to Multivariate Statistics, North-Holland, New York, 1979.

- Srivastava (2003) M. Srivastava, Singular Wishart and multivariate beta distributions, Annals of Statistics 31 (2003) 1537–1560.

- Harville (1997) D. Harville, Matrix Algebra from a Statistician’s Perspective, vol. 157, Springer, 1997.

- Muirhead (1982) R. Muirhead, Aspects of Multivariate Statistical Theory, Wiley, New York, 1982.

- Efron and Morris (1976) B. Efron, C. Morris, Multivariate empirical Bayes and estimation of covariance matrices, Annals of Statistics (1976) 22–32.

- Vershynin (2010) R. Vershynin, Introduction to the non-asymptotic analysis of random matrices, arXiv preprint arXiv:1011.3027 .

- Bunea and Xiao (2015) F. Bunea, L. Xiao, On the sample covariance matrix estimator of reduced effective rank population matrices, with applications to fPCA, Bernoulli 21 (2015) 1200– 1230.

- Liu and Neudecker (1997) S. Liu, H. Neudecker, Kantorovich inequalities and efficiency comparisons for several classes of estimators in linear models, Statistica Neerlandica 51 (1997) 345–355.

- Chételat and Wells (2014) D. Chételat, M. Wells, Noise Estimation in the Spiked Covariance Model, arXiv preprint arXiv:1408.6440 .

- Sheena (1995) Y. Sheena, Unbiased estimator of risk for an orthogonally invariant estimator of a covariance matrix, Journal of the Japanese Statistical Society 25 (1995) 35–48.

- Dey (1987) D. Dey, Improved estimation of a multinormal precision matrix, Statistics & Probability Letters 6 (1987) 125–128.

- Kollo and von Rosen (2006) T. Kollo, D. von Rosen, Advanced Multivariate Statistics with Matrices, vol. 579, Springer Science & Business Media, 2006.

- Fourdrinier and Strawderman (2003) D. Fourdrinier, W. Strawderman, On Bayes and unbiased estimators of loss, Annals of the Institute of Statistical Mathematics 55 (4) (2003) 803–816.

- Chételat and Wells (2012) D. Chételat, M. Wells, Improved multivariate normal mean estimation with unknown covariance when is greater than , Annals of Statistics 40 (2012) 3137–3160.