A permutation Information Theory tour through different interest rate maturities:

the Libor case

Abstract

This paper analyzes Libor interest rates for seven different maturities and referred to operations in British Pounds, Euro, Swiss Francs and Japanese Yen, during the period years 2001 to 2015. The analysis is performed by means of two quantifiers derived from Information Theory: the permutation Shannon entropy and the permutation Fisher information measure. An anomalous behavior in the Libor is detected in all currencies except Euro during the years 2006–2012. The stochastic switch is more severe in 1, 2 and 3 months maturities. Given the special mechanism of Libor setting, we conjecture that the behavior could have been produced by the manipulation that was uncovered by financial authorities. We argue that our methodology is pertinent as a market overseeing instrument.

PACS: 89.65.Gh Econophysics; 74.40.De noise and chaos

1 Introduction

Since the seminal work of Bachelier [1], prices in a competitive market have been modeled as a memoryless stochastic process. In fact, according to the Efficient Market Hypothesis (EMH), prices fully reflect all available information [2]. This property was duly proved by Samuelson [3]. It is known that informational efficiency can vary over time. This may be due to several reasons. For example, Cajueiro and Tabak [4] studied the Chinese stock market and found that liquidity plays a role in explaining the evolution of the long term memory; Bariviera [5] argued that informational efficiency in the Thai stock market is influenced by liquidity constraints; while Bariviera et al. [6] detailed the influence of the 2008 financial crisis on the memory endowment of the European fixed income market. However, changes in informational efficiency are essentially unpredictable, under the EMH framework.

The problem addressed in this paper stems from a newspaper. Mollenkamp and Whitehouse [7] published a disruptive article in the Wall Street Journal: they suggested that the Libor rate did not reflect what it was expected, i.e., the cost of funding of prime banks. The British Bankers Association (BBA) defines Libor as “…the rate at which an individual Contributor Panel bank could borrow funds, were it to do so by asking for and then accepting inter-bank offers in reasonable market size, just prior to 11:00 [a.m.] London time”. Every London business day, each bank in the Contributor Panel (selected banks from BBA) makes a blind submission such that each banker does not know the quotes of the other bankers. A compiler, Thomson Reuters, then averages the second and third quartiles. This average is published and represents the Libor rate on a given day. In other words, Libor is a trimmed average of the expected borrowing rates of leading banks. Libor rates has been published for ten currencies and fifteen maturities. As it is defined, Libor is expected to be the best self estimate of leading banks borrowing cost at different maturities. Several publications in newspapers [8, 9] casting doubts on Libor integrity triggered investigations by several surveillance authorities such as the US Department of Justice, the UK Financial Services Authority or the European Commission. All these offices found several traces of misconduct, which resulted in severe fines to leading banks.

There are a few papers dealing with this topic in academic journals. Most of them are focused, once the manipulation is known, on verifying or discarding its existence, by means of statistical tests. Taylor and Williams [10] documented the detachment of the Libor rate from other market rates such as Overnight Interest Swap (OIS), Effective Federal Fund (EFF), Certificate of Deposits (CDs), Credit Default Swaps (CDS), and Repo rates. Snider and Youle [11] studied individual quotes in the Libor bank panel and found that Libor quotes in the US were not strongly related to other bank borrowing cost proxies. Abrantes-Metz et al. [12] analyzed the distribution of the Second Digits (SDs) of daily Libor rates between 1987 and 2008 and, compared it with uniform and Benford’s distributions. If we take into account the whole period, the null hypothesis that the empirical distribution follows either the uniform or Benford’s distribution cannot be rejected. However, if we take into account only the period after the subprime crisis, the null hypothesis is rejected. This result calls into question the “aseptic” setting of Libor. Monticini and Thornton [13] found evidence of Libor under-reporting after analyzing the spread between 1-month and 3-month Libor and the rate of Certificate of Deposits using the Bai and Perron [14] test for multiple structural breaks. For a historical overview of the Libor case from a regulator’ point of view, see the Federal Reserve Staff Report [15].

Recently, Bariviera et al. [16, 17] present preliminary results about 3-month UK Libor manipulation. They performed a symbolic time series analysis using the Complexity Entropy Causality Plane (CECP). Our approach goes deeper in two aspects. First, we study the behavior of the Libor for several maturities and currencies. Second, we introduce a local information theory quantifier, which is able to detect tiny perturbations in the probability density function. Consequently, instead of analyzing our results with global vs. global quantifiers, as in the CECP, we study the time series by means of global vs. local quantifiers, defined in the Shannon-Fisher plane.

Interest rates have broad and wide economic impact on our daily life. The lack of integrity of Libor as an information signal gives market participants a wrong proxy of borrowing costs, thus providing a bad rate for pricing financial products. Many mortgages as well as sovereign bonds have Libor-linked interest rates. Therefore, the wrong setting of the interest rates produces a cascade effect throughout the whole economy. Consequently, Libor reliability is crucial to private and public borrowers around the world.

Our approach is somewhat different to the previous literature. The aim of this paper is to propose a quantitative technique based on Information Theory quantifiers, in order to detect changes in the stochastic/chaotic underlying dynamics of the Libor time series. We claim that our methodology is able to capture changes in the process dynamics on an ongoing basis. In other words, our method allows periodic monitoring of interest time series. This market audit, done at regular intervals, can detect unusual mutation in the statistical properties of a time series. It is clear that not only manipulation can shift signal features. Other external forces, such as increasing noise or special economic situations influence on signal observation and measurement. Therefore, results should be read with care. A change in the stochastic dynamics should not be read exclusively as produced by manipulation. It could be due to spurious contamination of the signal, or liquidity constraints, etc. However, our method acts as an early warning mechanism to detect some kind of “market distress”. This study is relevant no only for researchers, but also for surveillance authorities who need an efficient market watch device in order to detect strange movements in key economic variables such as the Libor.

2 Methodology

Financial markets are complex, dynamic systems in which unobservable hidden structures govern their behavior. Usually, we can only observe an output, e.g. an equilibrium price, an interest rate fixing, etc. As a consequence, the researcher should study the behavior of that output in order to infer the characteristics of the underlying dynamical phenomenon.

Time series should be carefully analyzed in order to extract relevant information for simulation and forecasting purposes. Information Theory derived quantifiers can be considered good candidates for this task because they are able to characterize some properties of the probability distribution associated with the observable or measurable quantity.

If the Libor rates were somewhat manipulated (as suggested in Ref. [7]), some change in the stochastic behavior should appear. To be more precise, according to the EMH, interest rate time series should behave approximately as an standard Brownian motion. Manipulation is, by definition, the introduction of an strange deterministic device into the time series. According to Wold [18] a time series can be split into two components, one purely random and other deterministic. If manipulation is successful, the deterministic induced behavior should offset the random behavior. This process results in an reduction of the natural stochastic character of the interest rates. We argue that the selected Information Theory quantifiers are able to detect such reduction and its temporal duration.

We use two specific quantifiers: permutation Shannon entropy and permutation Fisher information measure. These quantifiers are evaluated in pairs, displaying them in -planar representation. This causal Shannon–Fisher Plane gives an insight on global versus local perturbations on the behavior of a time series of the underlying dynamics of a physical process under analysis.

2.1 The Shannon entropy

The Shannon entropy is usually regarded as a natural measure of the quantity of information in a physical process. Given a continuous probability distribution function (PDF) with and , its associated Shannon Entropy [19] is

| (1) |

a measure of “global character” that it is not too sensitive to strong changes in the distribution taking place on a small-sized region. Let now be a discrete probability distribution, with the number of possible states of the system under study. In the discrete case, we define a “normalized” Shannon entropy, , as

| (2) |

where the denominator is that attained by a uniform probability distribution .

2.2 The Fisher information measure

The Fisher’s Information Measure (FIM) [20, 21], constitutes a measure of the gradient content of the distribution , thus being quite sensitive even to tiny localized perturbations. It reads

| (3) |

FIM can be variously interpreted as a measure of the ability to estimate a parameter, as the amount of information that can be extracted from a set of measurements, and also as a measure of the state of disorder of a system or phenomenon [21]. In the previous definition of FIM (Eq. (3)) the division by is not convenient if at certain values. We avoid this if we work with a real probability amplitudes [20, 21], which is a simpler form (no divisors) and shows that simply measures the gradient content in . The gradient operator significantly influences the contribution of minute local variations to FIM’s value. Accordingly, this quantifier is called a “local” one [21].

Let be a discrete probability distribution, with the number of possible states of the system under study. The concomitant problem of information-loss due to discretization has been thoroughly studied and, in particular, it entails the loss of FIM’s shift-invariance, which is of no importance for our present purposes [22, 23]. For the FIM we take the expression in term of real probability amplitudes as starting point, then a discrete normalized FIM, , convenient for our present purposes, is given by

| (4) |

It has been extensively discussed that this discretization is the best behaved in a discrete environment [24]. Here the normalization constant reads

| (5) |

If our system lies in a very ordered state, which occurs when almost all the – values are zeros except for a particular state with , we have a normalized Shannon entropy and a normalized Fisher’s information measure . On the other hand, when the system under study is represented by a very disordered state, that is when all the – values oscillate around the same value we obtain while . One can state that the general FIM–behavior of the present discrete version (Eq. (4)), is opposite to that of the Shannon entropy, except for periodic motions [22, 23]. The local sensitivity of FIM for discrete–PDFs is reflected in the fact that the specific “ordering” of the discrete values must be seriously taken into account in evaluating the sum in Eq. (4). This point was extensively discussed by Rosso et al. in previous works [22, 23]. The summands can be regarded as a kind of “distance” between two contiguous probabilities. Thus, a different ordering of the pertinent summands would lead to a different FIM-value, hereby its local nature. In the present work, we follow the lexicographic order described by Lehmer [25] in the generation of Bandt-Pompe PDF (see next section). Given the local character of FIM, when combined with a global quantifier as the Shannon entropy, conforms the Shannon–Fisher plane, , introduced by Vignat and Bercher [26]. These authors showed that this plane is able to characterize the non-stationary behavior of a complex signal.

2.3 The Bandt Pompe method for PDF evaluation

Time series (TS) analysis, i.e. temporal measurements of variables, is a very important area of economic science. In particular, it is very important to extract information in order to unveil the underlying dynamics of irregular and apparently unpredictable behavior in a given market. The starting point of TS analysis is to determine the most appropriate probability density function associated with the TS. Several methods compete for its proper estimation. For example Rosso et al. [27] propose the frequency of occurrence; De Micco et al. [28] propose amplitude-based procedures; Mischaikow et al. [29] prefer binary symbolic dynamics; Powell et al. [30] recommend Fourier analysis and; Rosso et al. [31] introduce wavelets transformation, among others. The suitability of each of the proposed methodologies depends on the peculiarity of data, such as stationarity, length of the series, the variation of the parameters, the level of noise contamination, etc. In all these cases, global aspects of the dynamics can be somehow captured, but the different approaches are not equivalent in their ability to discern all relevant physical details. Bandt and Pompe [32] introduced a simple and robust symbolic method that takes into account time order of the TS.

The pertinent symbolic data are: (i) created by ranking the values of the series; and (ii) defined by reordering the embedded data in ascending order, which is tantamount to a phase space reconstruction with embedding dimension (pattern length) and time lag . In this way, it is possible to quantify the diversity of the ordering symbols (patterns) derived from a scalar time series. Note that the appropriate symbol sequence arises naturally from the time series, and no model-based assumptions are needed. In fact, the necessary “partitions” are devised by comparing the order of neighboring relative values rather than by apportioning amplitudes according to different levels. This technique, as opposed to most of those in current practice, takes into account the temporal structure of the time series generated by the physical process under study. This feature allows us to uncover important details concerning the ordinal structure of the time series [23, 33, 34] and can also yield information about temporal correlation [35, 36].

It is clear that this type of analysis of a time series entails losing some details of the original series’ amplitude information. Nevertheless, by just referring to the series’ intrinsic structure, a meaningful difficulty reduction has indeed been achieved by Bandt and Pompe with regard to the description of complex systems. The symbolic representation of time series by recourse to a comparison of consecutive () or nonconsecutive () values allows for an accurate empirical reconstruction of the underlying phase-space, even in the presence of weak (observational and dynamic) noise [32]. Furthermore, the ordinal patterns associated with the PDF is invariant with respect to nonlinear monotonous transformations. Accordingly, nonlinear drifts or scaling artificially introduced by a measurement device will not modify the estimation of quantifiers, a nice property if one deals with experimental data (see, e.g., [37]). These advantages make the Bandt and Pompe methodology more convenient than conventional methods based on range partitioning (i.e., PDF based on histograms).

To use the Bandt and Pompe [32] methodology for evaluating the PDF, , associated with the time series (dynamical system) under study, one starts by considering partitions of the pertinent -dimensional space that will hopefully “reveal” relevant details of the ordinal structure of a given one-dimensional time series with embedding dimension () and embedding time delay (). We are interested in “ordinal patterns” of order (length) generated by

| (6) |

which assigns to each time the -dimensional vector of values at times . Clearly, the greater the value, the more information on the past is incorporated into our vectors. By “ordinal pattern” related to the time , we mean the permutation of defined by

| (7) |

In order to get a unique result, we set if . This is justified if the values of have a continuous distribution, so that equal values are very unusual.

For all the possible orderings (permutations) when embedding dimension is , their associated relative frequencies can be naturally computed according to the number of times this particular order sequence is found in the time series, divided by the total number of sequences,

| (8) |

In the last expression the symbol stands for “number”. Thus, an ordinal pattern probability distribution is obtained from the time series.

Consequently, it is possible to quantify the diversity of the ordering symbols (patterns of length ) derived from a scalar time series, by evaluating the so-called permutation entropy (Shannon entropy) and permutation Fisher information measure. Of course, the embedding dimension plays an important role in the evaluation of the appropriate probability distribution, because determines the number of accessible states and also conditions the minimum acceptable length of the time series that one needs in order to work with reliable statistics [33].

Regarding the selection of the parameters, Bandt and Pompe suggested working with and specifically considered an embedding delay in their cornerstone paper [32]. Nevertheless, it is clear that other values of could provide additional information. It has been recently shown that this parameter is strongly related, if it is relevant, to the intrinsic time scales of the system under analysis [38, 39, 40].

Additional advantages of the method reside in i) its simplicity (we need few parameters: the pattern length/embedding dimension and the embedding delay ) and ii) the extremely fast nature of the pertinent calculation-process [41]. The BP methodology can be applied not only to time series representative of low dimensional dynamical systems but also to any type of time series (regular, chaotic, noisy, or reality based). In fact, the existence of an attractor in the -dimensional phase space in not assumed. The only condition for the applicability of the BP method is a very weak stationary assumption: for , the probability for should not depend on . For a review of BP’s methodology and its applications to physics, biomedical and econophysics signals see Zanin et al. [42]. Rosso [33] show that the above mentioned quantifiers produce better descriptions of the process associated dynamics when the PDF is computed using BP rather than using the usual histogram methodology.

The Bandt and Pompe proposal for associating probability distributions to time series (of an underlying symbolic nature) constitutes a significant advance in the study of nonlinear dynamical systems [32]. The method provides univocal prescription for ordinary, global entropic quantifiers of the Shannon-kind. However, as was shown by Rosso and coworkers [22, 23], ambiguities arise in applying the Bandt and Pompe technique with reference to the permutation of ordinal patterns. This happens if one wishes to employ the BP-probability density to construct local entropic quantifiers, like the Fisher information measure, which would characterize time series generated by nonlinear dynamical systems.

The local sensitivity of the Fisher Information measure for discrete PDFs is reflected in the fact that the specific “-ordering” of the discrete values must be seriously taken into account in evaluating the sum in Eq. (4). The pertinent numerator can be regarded as a kind of “distance” between two contiguous probabilities. Thus, a different ordering of the pertinent summands would lead to a different Fisher information value. In fact, if we have a discrete PDF given by , we will have possibilities for the -ordering.

The question is, which is the arrangement that one could regard as the “proper” ordering? The answer is straightforward in some cases, the histogram-based PDF constituting a conspicuous example. For such a procedure, one first divides the interval (with and the minimum and maximum amplitude values in the time series) into a finite number on non-overlapping sub-intervals (bins). Thus, the division procedure of the interval provides the natural order sequence for the evaluation of the PDF gradient involved in the Fisher information measure. In our current paper, we chosen for the Bandt–Pompe PDF the lexicographic ordering given by the algorithm of Lehmer [25], amongst other possibilities, due to it provide a better distinction of different dynamics in the Shannon–Fisher plane, (see [22, 23]).

3 Data

We analize the Libor rates in British Pounds (GBP), Euro (EUR), Swiss Franc (CHF) and Japanese Yen (JPY), for the following seven maturities: overnight (O/N), one week (1W), one month (1M), two months (2M), three months (3M), six months (6M) and twelve months (12M). The data coverage is from 02/01/2001 until 24/03/2015, for a total of 3711 data points. All data were retrieved from Datastream.

4 Results

We analyze each time series using the methodology described in Section 2. The PDF was computed following the BP recipe, because it is the single method to introduce time-causality in PDF building. Although we have performed our analysis using embedding dimensions and 5 with time lag , we present the results only for , because it exhibits the best clarity for our explanations. The other embedding dimensions results are similar.

We would like to know if the underlying generating process changes during the observation period. In order to evaluate such change, we construct sliding windows. The sliding windows work as follows: We consider the first data points and evaluate the two quantifiers, and . Then we move data points forward and compute the quantifiers of the new window with the following data points. We continue this process until the end of the time series. After doing so, we obtain 170 estimation windows. Each window spans approximately one year, and the window step is approximately one month.

The initial and final dates of each estimation window is displayed in the electronic supplementary material ESM-Table 1.

We also present in the electronic supplementary material the graphs corresponding to -plane for the Libor rates in GBP (ESM-Fig. 1), Euro (ESM-Fig. 2), CHF (ESM-Fig. 3), JPY (ESM-Fig. 4) for the seven considered maturities: O/N, 1W, 2M, 3M, 6M and 12M, when they are evaluated on the 170 estimation windows respectively, given in this way a representation of the time evolution of them. From these figures, it can be observed that 1M, 2M and 3M maturities have similar shape. It can also noted that 6M and 12M are very similar to each other and their localization points are more concentrated. We can summarize these results as: two distinct dynamics are detected. On one side, 1M, 2M and 3M maturities scatters throughout the plane. On the other side, O/N, 1W, 6M and 12M graphs are less disperse and their points are more concentrated on the low right corner. In the financial economics vocabulary, we can say that the latter maturities are more informationally efficient: their time series are closer to a random walk. The middle maturities (1M, 2M, 3M) occupy places in the –plane that are consistent with fractional Brownian motion or with chaotic dynamics.

This is the first evidence that we are dealing with a single interest rate but with distinct generating processes. In order to highlight the unequal behavior between the two groups of maturities, we count the number of points of the –plane that are closer to the low right corner and the number of points that are away from that corner. We divide the points into two regions. One, the most informational efficient region comprises the points where and . The other is the complement of the –plane. We display the results of the point counting in Tables 1 to 4. These tables confirm the ocular inspection of the –plane (see figures ESM-Fig. 1 to ESM-Fig. 4). Whereas for 1M, 2M and 3M maturities only between 33% to 39% of the points are in the efficient area, the percentages for the other maturities ranges 55% to 63%. We recall that each point reflects the estimation of the quantifiers at a given moving window.

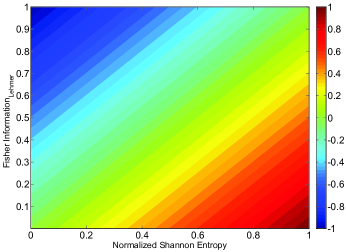

We would like to enquire if the aforementioned characteristics changed in an ordered way through time. Taking into account that we are studying the changes across time in the degree of informational efficiency of financial time series, we propose the following efficiency index, :

| (9) |

Given that both quantifiers, and , are bounded between 0 and 1, and that their behavior is expected opposite, the maximum value of our efficiency index is , when and and when and The most informational efficient behavior (i.e. the most random behavior) is when Shannon entropy is maximized and Fisher information minimized. Consequently, our efficiency index lies in the interval. Accordingly, our efficiency index can be represented in a color map as in Fig. 1

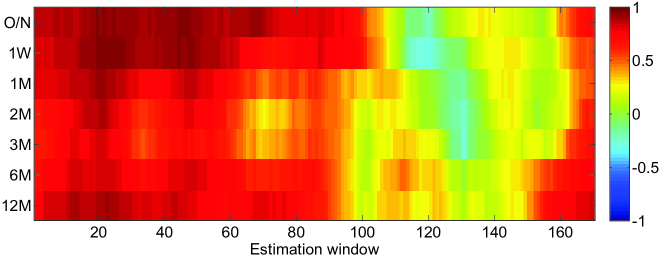

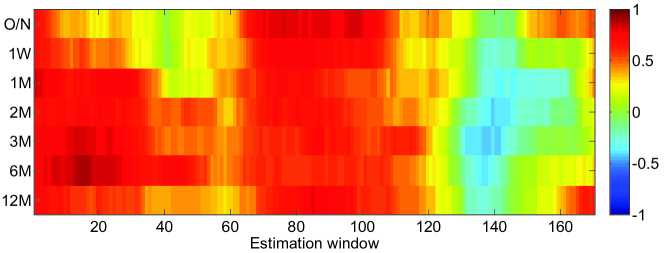

We aim to assess the evolution of the efficiency through time. In order to do so, we display the result for each currency in a color map where the -axis is the temporal dimension (i.e. the estimation windows) and the -axis are the different currencies. The colors of the map reflects a degree of efficiency according to the color scale on the right of each graph and coincides with the color scale of Fig. 1.

The map corresponding GBP (see Fig. 2(a)) clearly reflects two features. First that O/N, 1W, 6M and 12M maturities has been behaving better that the middle maturities. Even more, 6M and 12M has been globally the most efficient during all the period. On contrary, 1M, 2M, 3M were informationally efficient until window 100 (05/08/2008 to 31/08/2009) and suffered a sudden shift in its stochastic behavior, that returns to its previous path around window 160 (12/03/2013 to 05/05/2014). Additionally we can observe a yellow area around windows 65–80, that roughly correspond to years 2006 and 2007. The behavior detected by this color map is consistent with the alleged manipulation of Libor rates reported in the press [7]. According to our results, Libor rates suffered from some kind of inefficient behavior (coherent with manipulation) during the period 2006–2012. In year 2013 the levels of informational efficiency recovered to levels similar to periods previous to the financial crisis.

| Points within | Points outside | Percentage of | Series |

|---|---|---|---|

| efficiency bounds | efficiency bounds | efficient windows | |

| 107 | 63 | 63% | GBP Libor O/N |

| 103 | 67 | 61% | GBP Libor 1W |

| 67 | 103 | 39% | GBP Libor 1M |

| 56 | 114 | 33% | GBP Libor 2M |

| 58 | 112 | 34% | GBP Libor 3M |

| 93 | 77 | 55% | GBP Libor 6M |

| 106 | 64 | 62% | GBP Libor 12M |

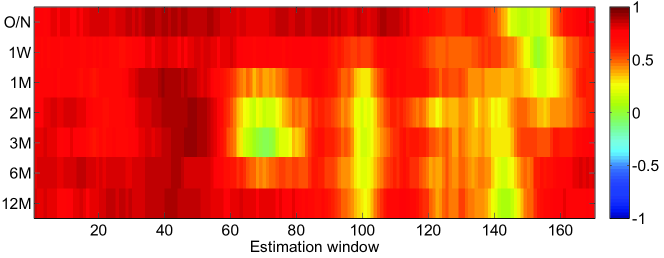

The Euro market exhibits a similar pattern with respect to the two groups of maturities. However, the loss of efficiency is was less severe. This can be observed in the Fig. 2(b), where there is a prevalence of orange and red colors.

| Points within | Points outside | Percentage of | Series |

|---|---|---|---|

| efficiency bounds | efficiency bounds | efficient windows | |

| 145 | 25 | 85% | EUR Libor O/N |

| 113 | 57 | 66% | EUR Libor 1W |

| 87 | 83 | 51% | EUR Libor 1M |

| 68 | 102 | 40% | EUR Libor 2M |

| 84 | 86 | 49% | EUR Libor 3M |

| 90 | 80 | 53% | EUR Libor 6M |

| 121 | 49 | 71% | EUR Libor 12M |

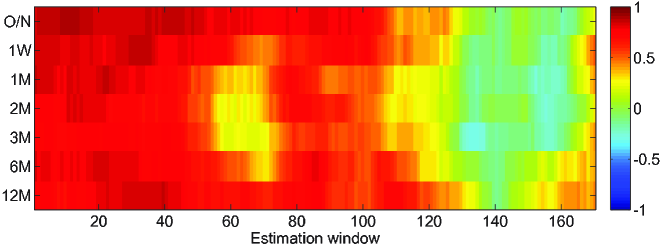

The Swiss Franc market behavior (see Fig. 2(c)) is more similar to the British Pound market (see Fig. 2(a)) The region that comprises windows 120 until 160 reflects an eroded informational efficiency, that was slowly recovered at the final of the observation period. Additionally there is a yellow spot around windows 60–70 exclusively in 1M, 2M and 3M maturities.

| Points within | Points outside | Percentage of | Series |

|---|---|---|---|

| efficiency bounds | efficiency bounds | efficient windows | |

| 107 | 63 | 63% | CHF Libor O/N |

| 95 | 75 | 56% | CHF Libor 1W |

| 59 | 111 | 35% | CHF Libor 1M |

| 66 | 104 | 39% | CHF Libor 2M |

| 58 | 112 | 34% | CHF Libor 3M |

| 78 | 92 | 46% | CHF Libor 6M |

| 102 | 68 | 60% | CHF Libor 12M |

The Japanese Yen market (see Fig. 2(d)) was also affected in the degree of efficiency. In general, we can observe in the color map that this is a less informational efficient market: light orange, yellow and light blue are dominant. There is also a severe erosion of the informational efficiency between windows 120 to 160, recovered at the end of the observation period mainly in O/N and 12M maturities.

| Points within | Points outside | Percentage of | Series |

|---|---|---|---|

| efficiency bounds | efficiency bounds | efficient windows | |

| 49 | 121 | 29% | JPY Libor S/N |

| 50 | 120 | 29% | JPY Libor 1W |

| 59 | 111 | 35% | JPY Libor 1M |

| 64 | 106 | 38% | JPY Libor 2M |

| 64 | 106 | 38% | JPY Libor 3M |

| 82 | 88 | 48% | JPY Libor 6M |

| 68 | 102 | 40% | JPY Libor 12M |

5 Conclusion

The first finding that we can extract from our data analysis is that the Libor for all currencies and for maturities 1M, 2M and 3M is governed by a different process than the other maturities. The mentioned maturities usually reflect a lower level of informational efficiency than the other maturities. The second important finding is that during the years 2007-2012 (windows 120-160) there was a significant reduction in the informational efficiency of all markets, except the Euro market. This behavior seems to be contemporary to the uncovered manipulation announced in the newspapers [7]. We would like to highlight that our method is not intended to find manipulation, but rather to uncover changes in the hidden stochastic structure of data. However, it is able to clearly discriminate areas of more deterministic behavior in the time series, which could be consistent with the alleged interest rate rigging.

References

- [1] Bachelier L, 1900 Thérie de la spéculation. Annales scientifiques de l’École Normale Supérieure; Paris, 17 21–86.

- [2] Fama EF, 1976 Foundations of finance: portfolio decisions and securities prices. New York: Basic Books. .

- [3] Samuelson, 1965 Proof that properly anticipated prices fluctuate randomly. Industrial Management Review 6 41–49.

- [4] Cajueiro DO, Tabak BM, 2006 The long-range dependence phenomena in asset returns: the Chinese case. Applied Economics Letters 13 131–133.

- [5] Bariviera AF, 2011 The influence of liquidity on informational efficiency: The case of the Thai Stock Market. Physica A 390 4426–4432.

- [6] Bariviera AF, Guercio MB, Martinez LB, 2012 A comparative analysis of the informational efficiency of the fixed income market in seven European countries. Economics Letters 116 426–428.

- [7] Mollenkamp C, Whitehouse M, 2008 Study casts doubt on key rate: WSJ analysis suggests banks may have reported flawed interest data for Libor. The Wall Street Journal, Thursday, 29 May, p.1.

- [8] Saigol L. Libor: The email trail; 2013. The Financial Services, http://www.ft.com/cms/s/0/cefd67a0-25df-11e3-aee8-00144feab7de.html#axzz3FNK2XAFe.

- [9] Reuters, 2012 New York Federal Reserve knew about Libor rate-fixing issues as far back as 2007 and proposed changes but were ignored. The Daily Mail, July 10.

- [10] Taylor JB, Williams JC, 2009 A black swan in the money market. American Economic Journal: Macroeconomics. 1 58–83.

- [11] Snider CA, Youle T, 2010 Does the Libor reflect banks’ borrowing costs?. Available at Social Sicence Research Network (SSRN): http://ssrn.com/abstract=1569603 or http://dx.doi.org/10.2139/ssrn.1569603.

- [12] Abrantes-Metz RM, Villas-Boas SB, Judge G, 2011 Tracking the Libor rate. Applied Economics Letters. 18 893–899.

- [13] Monticini A, Thornton DL, 2013 The effect of underreporting on Libor rates. Journal of Macroeconomics 37 345–348.

- [14] Bai J, Perron P, 1998 Estimating and testing linear models with multiple structural changes. Econometrica 66 47–78.

- [15] Hou D, Skeie DR, 2014 Libor: Origins, Economics, Crisis, Scandal, and Reform. Federal Reserve Bank of New York Staff Report No. 667, March 1 .

- [16] Bariviera AF, Guercio MB, Martinez LB, 2015 Data manipulation detection via permutation information theory quantifiers. ArXiv preprint, arXiv:1501.04123.

- [17] Bariviera AF, Guercio MB, Martinez LB, Rosso OA,2015 The (in)visible hand in the Libor market: an Information Theory approach The European Physics Journal B, 88 208.

- [18] Wold H, 1938 A study in the analysis of stationary time series. Almqvist and Wiksell, Upsala, Sweeden.

- [19] Shannon C, Weaver W, 1949 The Mathematical Theory of Communication. University of Illinois Press, Champaign, USA.

- [20] Fisher RA, 1922 On the mathematical foundations of theoretical statistics, Philos. Trans. R. Soc. Lond. Ser. A 222 309–368.

- [21] Frieden BR, 2004 Science from Fisher information: A Unification. Cambridge University Press, Cambridge, UK.

- [22] Olivares F, Plastino A, Rosso OA, 2012 Ambiguities in BandtPompe’s methodology for local entropic quantifiers. Physica A 391 2518–2526.

- [23] Olivares F, Plastino A, Rosso OA, 2012 Contrasting chaos with noise via local versus global information quantifiers. Phys. Lett A 376 1577–1583.

- [24] Sánchez-Moreno P, Yáñez RJ, Dehesa JS, 2009 Discrete Densities and Fisher Information. In Proceedings of the 14th International Conference on Difference Equations and Applications. Difference Equations and Applications. Istanbul, Turkey: Uğur Bahçeşehir University Publishing Company, 291–298.

- [25] http://www.keithschwarz.com/interesting/code/factoradicpermutation/ FactoradicPermutation.hh.html

- [26] Vignat C, Bercher JF, 2003 Analysis of signals in the Fisher x Shannon information plane. Physics Letters A 312 27–33.

- [27] Rosso OA, Craig H, Moscato P, 2009 Shakespeare and other English Renaissance authors as characterized by Information Theory complexity quantifiers. Physica A 388 916–-926.

- [28] De Micco L, Gonzalez CM, Larrondo HA, Martín MT, Plastino A, Rosso OA, 2008 Randomizing nonlinear maps via symbolic dynamics. Physica A 387 3373–3383.

- [29] Mischaikow K, Mrozek M, Reiss J, Szymczak A, 1999 Construction of symbolic dynamics from experimental time series. Phys. Rev. Lett. 82 1144–1147.

- [30] Powell GE, Percival IC, 1979 A spectral entropy method for distinguishing regular and irregular motion of Hamiltonian systems. J. Phys. A: Math. Gen. 12 2053–2071.

- [31] Rosso OA, Blanco S, Jordanova J, Kolev V, Figliola A, Schürmann M, Başar E, 2001 Wavelet entropy: a new tool for analysis of short duration brain electrical signals. J. Neurosci. Methods. 105 65–75.

- [32] Bandt C, Pompe B, Permutation Entropy: A Natural Complexity Measure for Time Series. Phys. Rev. Lett. 88 174102.

- [33] Rosso OA, Larrondo HA., Martín MT, Plastino A, Fuentes MA, 2007 Distinguishing noise from chaos. Phys. Rev. Lett. 99 154102.

- [34] Rosso OA, Olivares F, Zunino L, De Micco L, Aquino ALL, Plastino A, Larrondo HA, 2012 Characterization of chaotic maps using the permutation Bandt-Pompe probability distribution. Eur. Phys. J. B 86 116–129.

- [35] Rosso OA, Masoller C, 2009 Detecting and quantifying stochastic and coherence resonances via information-theory complexity measurements. Phys. Rev. E 79 040106(R).

- [36] Rosso OA, Masoller C, 2009 Detecting and quantifying temporal correlations in stochastic resonance via information theory measures. Eur. Phys. J. B 69 37–43.

- [37] Saco PM, Carpi LC, Figliola A, Serrano E, Rosso OA, 2010 Entropy analysis of the dynamics of El Niño/Southern Oscillation during the Holocene. Physica A 389 5022–5027

- [38] Zuninov L, Soriano MC, Fischer I, Rosso OA, Mirasso CR, 2010 Permutation information-theory approach to unveil delay dynamics from time-series analysis. Phys. Rev. E 82 046212.

- [39] Soriano MC, Zunino L, Rosso, OA, Fischer I, Mirasso CR, 2011 Time scales of a chaotic semiconductor laser with optical feedback under the lens of a permutation information analysis. IEEE J. Quantum Electron. 47 252-–261.

- [40] Zunino L, Soriano MC, Rosso OA, 2012 Distinguishing chaotic and stochastic dynamics from time series by using a multiscale symbolic approach. Phys. Rev. E 86 046210.

- [41] Keller K, Sinn M, 2005 Ordinal analysis of time series. Physica A 356 114–120.

- [42] Zanin M, Zunino L, Rosso OA, Papo D, 2012 Permutation entropy and its main biomedical and econophysics applications: A review. Entropy 14 1553–1577.