∎

Georgia Institute of Technology, Atlanta, Georgia, USA.

22email: {caoyang, yao.xie, nagi}@gatech.edu

Multi-Sensor Slope Change Detection

Abstract

We develop a mixture procedure for multi-sensor systems to monitor data streams for a change-point that causes a gradual degradation to a subset of the streams. Observations are assumed to be initially normal random variables with known constant means and variances. After the change-point, observations in the subset will have increasing or decreasing means. The subset and the rate-of-changes are unknown. Our procedure uses a mixture statistics, which assumes that each sensor is affected by the change-point with probability . Analytic expressions are obtained for the average run length (ARL) and the expected detection delay (EDD) of the mixture procedure, which are demonstrated to be quite accurate numerically. We establish the asymptotic optimality of the mixture procedure. Numerical examples demonstrate the good performance of the proposed procedure. We also discuss an adaptive mixture procedure using empirical Bayes. This paper extends our earlier work on detecting an abrupt change-point that causes a mean-shift, by tackling the challenges posed by the non-stationarity of the slope-change problem.

Keywords:

statistical quality control change-point detection intelligent systems1 Introduction

As an enabling component for modern intelligent systems, multi-sensory monitoring has been widely deployed for large scale systems, such as manufacturing systems fang2015adaptive , 6496166 , power systems VVV-IWSM-2015 , and biological and chemical threat detection systems threat_CSL_2015 . The sensors acquire a stream of observations, whose distribution changes when the state of the network is shifted due to an abnormality or threat. We would like to detect the change online as soon as possible after it occurs, while controlling the false alarm rate. When the change happens, typically only a small subset of sensors are affected by the change, which is a form of sparsity. A mixture statistic which utilizes this sparsity structure of this problem is presented in xie2013sequential . The asymptotic optimality of a related mixture statistic is established in optmal_mix_procedure . Extensions and modifications of the mixture statistic that lead to optimal detection are considered in ChanOptimal2015 .

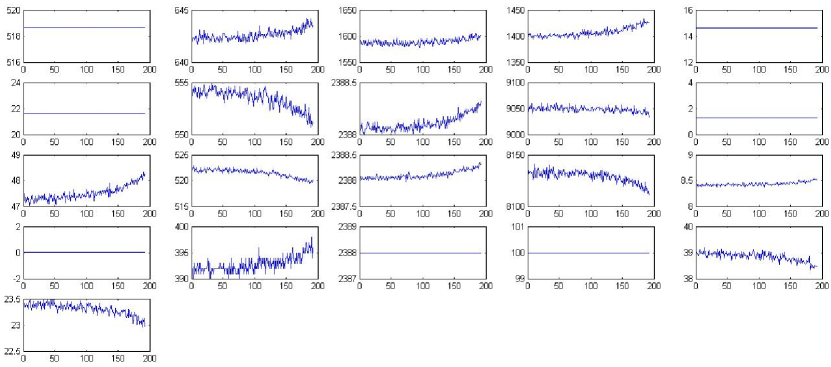

In the above references xie2013sequential ; ChanOptimal2015 , the change-point is assumed to cause a shift in the means of the observations by the affected sensors, which is good for modeling an abrupt change. However, in many applications above, the change-point is an onset of system degradation, which causes a gradual change to the sensor observations. Often such a gradual change can be well approximated by a slope change in the means of the observations. One such example is shown in Fig. 1, where multiple sensors monitor an aircraft engine and each panel of figure shows the readings of one sensor. At some time a degradation initiates and causes decreasing or increasing in the means of the observations. Another example comes from power networks, where there are thousands of sensors monitoring hundreds of transformers in the network. We would like to detect the onset of any degradation in real-time and predict the residual life time of a transformer before it breaks down and causes a major power failure.

In this paper, we present a mixture procedure that detects a change-point causing a slope change to the means of the observations, which can be a model for gradual degradations. Assume the observations at each sensor are normal random variables with constant means. After the change, observations at the sensors affected by the change-point become normal distributed with increasing or decreasing means. The subset of sensors that are affected are unknown. Moreover, their rate-of-changes are also unknown. Our mixture procedure assumes that each sensor is affected with probability independently, which is a guess for the true fraction of sensors affected. When is small, this captures an empirical fact that typically only a small fraction of sensors are affected. With such a model, we derive the log-likelihood ratio statistic, which becomes applying a soft-thresholding to the local statistic at each sensor and then combining the results. The mixture procedure fires an alarm whenever the statistic exceeds a prescribed threshold. We consider two versions of the mixture procedure that compute the local sensor statistic differently: the mixture CUSUM procedure , which assumes some nominal values for the unknown rate-of-change parameters, and the mixture generalized likelihood ration (GLR) procedure , which uses the maximum likelihood estimates for these parameters. To characterize the performance of the mixture procedure, we present theoretical approximations for two commonly used performance metrics, the average run length (ARL) and the expected detection delay (EDD). Our approximations are shown to be highly accurate numerically and this is useful in choosing a threshold of the procedure. We also establish the asymptotic optimality of the mixture procedures. Good performance of the mixture procedure is demonstrated via real-data examples, including: (1) detecting a change in the trends of financial time series; (2) predicting the life of air-craft engines using the Turbofan engine degradation simulation dataset.

The mixture procedure here can be viewed as an extension of our earlier work on multi-sensor mixture procedure for detecting mean shifts xie2013sequential . The extensions of theoretical approximations to EDD and especially to ARL are highly non-trivial, because of the non-i.i.d. distributions in the slope change problem. Moreover, we also establish some new optimality results which were omitted from xie2013sequential , by extending the results in lai1998information and tartakovsky2014sequential to handle non- distributions in our setting. In particular, we generalize the theory to a scenario where the log likelihood ratio grows polynomially as a result of linear increase or decrease of the mean values, whereas in xie2013sequential , the log-likelihood ratio grows linearly. A related recent work optmal_mix_procedure studies optimality of the multi-sensor mixture procedure for observations, but the results therein do not apply to the slope change case here.

The rest of this paper is organized as follows. Section 2 sets up the formalism of the problem. Section 3 presents our mixture procedures for slope change detection, and Section 4 presents theoretical approximations to its ARL and EDD, which are validated by numerical examples. Section 5 establishes the first order asymptotic optimality. Section 6 shows real-data examples. Finally, Section 7 presents an extension of the mixture procedure that adaptively chooses . All proofs are delegated to the appendix.

2 Assumptions and formulation

Given sensors. For the th sensor , denote the sequence of observations by , . Under the hypothesis of no change, the observations at the th sensor have a known mean and a known variance . Probability and expectation in this case are denoted by and , respectively. Alternatively, there exists an unknown change-point that occurs at time , , and it affects an unknown subset of sensors simultaneously. The fraction of affected sensors is given by . For each affected sensor , the mean of the observations changes linearly from the change-point time and is given by for all , and the variance remains . For each unaffected sensor, the distribution stays the same. Here the unknown rate-of-change can differ across sensors and it can be either positive or negative. The probability and expectation in this case are denoted by and , respectively. In particular, denotes an immediate change occurring at the initial time. The above setting can formulate as the following hypothesis testing problem:

| (1) |

Our goal is to establish a stopping rule that stops as soon as possible after a change-point occurs and avoids raising false alarms when there is no change. We will make these statements more rigorous in Section 4 and Section 5. Here, for simplicity, we assume that all sensors are affected by the change simultaneously. This ignores the fact that there can be delays across sensors. For asynchronous sensors, one possible approach is to adopt the scheme in hadjiliadis2009one , which claims a change-point whenever the any sensor detects a change. We plan investigate the issue of delays in our future work.

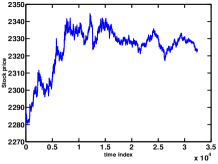

A related problem is to detect a change in a linear regression model. One such example is a change-point in the trend of the stock price illustrated in Fig. 7(a). This can be casted into a slope change detection problem, if we fit a linear regression model under (e.g., using historical data) and subtract it from the sequence. The residuals after the subtraction will have zero means before the change-point, and their means will increase or decrease linearly after the change-point.

Remark 1 (Reason for not differencing the signal.)

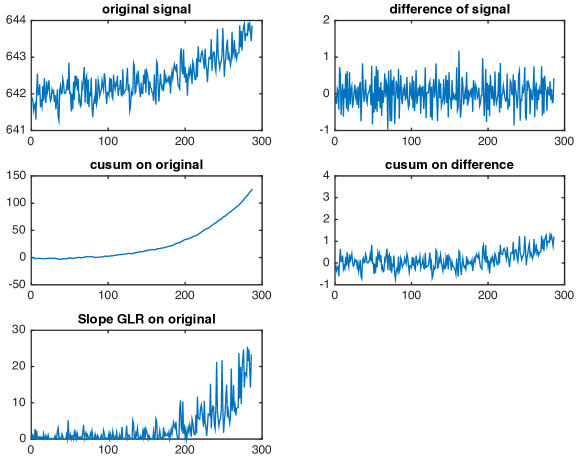

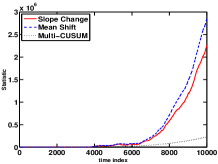

One legitimate question is that why not de-trending the signal at each sensor by difference, which may turn the slope change into a mean change problem and we can apply the standard CUSUM procedure designed for detecting the mean shift. Indeed, for the affected sensors after the change-point, . However, differencing will also increase the variance, as . Hence, differencing reduces the signal-to-noise ratio and this is particularly bad for weak signals and makes them even non-detectable. This is validated by real data as well. Consider the engine data displayed in Fig. 1. The first panel in Fig. 2 corresponds to observations of one sensor that is affected by noise, which clearly has the “signal” as the mean is increasing. However, after we difference the signal, the change is almost invisible, as illustrated. We then try applying CUSUM on the difference, where the statistic either rises slowly which means it cannot detect quickly. We also try applying CUSUM (designed for mean change detection) directly on the original signal. Although the statistics rises reasonably fast; however, clearly this statistic cannot estimate the change-point location accurately due to its model mismatch. The last panel in Fig. 2 shows our proposed statistic, which can detect the change fairly quickly, and it can also accurately estimate the change-point location.

3 Detection procedures

Since the observations are independent, for an assumed change-point location and an affected sensor , the log-likelihood for observations up to time is given by

| (2) |

Motived by the mixture procedure in xie2013sequential and siegmund2011detecting to exploit an empirical fact that typically only a subset of sensors are affected by the change-point, we assume that each sensor is affected with probability independently. In this setting, the log likelihood of all sensors is given by

| (3) |

Using (3), we may derive several change-point detection rules.

Since the rate-of-change is unknown, One possibility is to set equal to some nominal post-change value and define the stopping rule, referred to as the mixture CUSUM procedure:

| (4) |

where is a threshold typically prescribed to satisfy the average run length (ARL) requirement (formal definition of ARL is given in Section 4).

Another possibility is to replace by its maximum likelihood estimator. Given the current number of observations and a putative change-point location , by setting the derivative of the log likelihood function (2) to 0, we may solve for the maximum likelihood estimator:

| (5) |

Define to be the number of samples after the change-point . Denote the sum of squares from to , and the weighted sum of data as, respectively,

Let

| (6) |

Substitution of (5) into (2) gives the log generalized likelihood ratio (GLR) statistic at each sensor:

| (7) |

and we define the mixture GLR procedure as

| (8) |

where is a prescribed threshold.

Remark 2 (Window limited procedures.)

In the following we use window limited versions of and , where the maximum for the statistic is restricted to a window for suitable choices of window size and . In the following, we use to denote a window-limited version of a procedure . By searching only over a window of the past samples, this reduces the memory requirements to implement the stopping rule, and it also sets a minimum level of change that we want to detect. The choice of may depend on and sometimes we need make additional assumptions on for the purpose of establishing the asymptotic results below. More discussions about the choice of can be found in lai1995sequential and lai1998information . The other parameter is the minimum number of observations needed for computing the maximum likelihood estimator for parameters. In the following, we set .

Remark 3 (Relation to mean shift.)

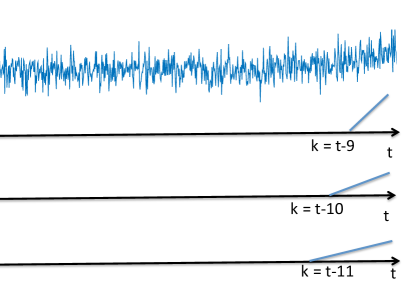

For the mean-shift multi-sensor change-point detection xie2013sequential , the detection statistic depends on a key quantify, which is the average of the samples in the time window . Note that in the slope change case, the detection statistic has a similar structure, except that the key quantity is replaced by a weighted average of the samples in the window: . This has an interpretation of “matched filtering”, as illustrated in Fig. 3: each data stream is matched with a triangle shaped signal starting at a potential change-point time that represents a possible slope change.

Remark 4 (Recursive computation.)

The quantity involved in the detection statistic for (8) can be calculated recursively,

where . This facilitates online implementation of the detection procedure. The quantity can be pre-computed since it is data-independent.

Remark 5 (Extension to correlated sensors.)

The mixture procedure (8) can be easily extended to the case where sensors are correlated with a known covariance matrix. Define a vector of observations for all sensors at time . When there is no change, follows a normal distribution with a mean vector and a covariance matrix . Alternatively, there may exist a change-point at time such that after the change, the observation vectors are normally distributed with mean vector , and the covariance matrix remains for all . We can whiten the signal vector by , where is the square-root of the positive definite covariance matrix that may be computed via its eigen-decomposition. The coordinates of are independent and the problem then becomes the original hypothesis testing problem (1) with all sensors being affected simultaneously by the change-point, the rate-of-change vector is , the mean vector is zero before the change, and the covariance remains an identity matrix before and after the change. Hence, after the transform, we may apply the mixture procedure with on .

4 Theoretical properties of the detection procedures

In this section we develop theoretical properties of the mixture procedure. We use two standard performance metrics (1) the expected value of the stopping time when there is no change, the average run length (ARL); (2) the expected detection delay (EDD), defined to be the expected stopping time in the extreme case where a change occurs immediately at . Since the observations are i.i.d. under the null, the EDD provides an upper bound on the expected delay after a change-point until detection occurs when the change occurs later in the sequence of observations (this is also a commonly used fact in change-point detection work xie2013sequential ). An efficient detection procedure should have a large ARL and meanwhile a small EDD. Our approximation to the ARL is shown below to be accurate. In practice, we usually fix ARL to be a large constant, and set the threshold in (8) accordingly. The accurate approximation here can be used to find the threshold analytically. Approximation for EDD shows its dependence on a quantity that plays a role of the Kullback-Leibler (KL) divergence, which links to the optimality results in Section 5.

Average run length (ARL). We present an accurate approximation for ARL of a window limited version of the stopping rule in (8), which we denote as . Let

| (9) |

and

where has a standard normal distribution. Also let

and

where the dot and double-dot denote the first-order and second-order derivatives of a function , respectively. Denote by and the standard normal density function and its distribution function, respectively. Also define a special function . For numerical purposes an accurate approximation is given by Segimundbook2007

Theorem 4.1 (ARL of .)

Assume that and with fixed. Let be defined by . For a window limited stopping rule of (8) with for some positive integer , we have

| (10) |

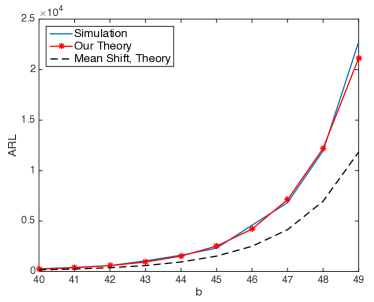

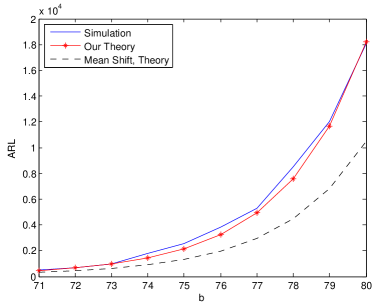

The proof of Theorem 10 is an extension of the proofs in xie2013sequential and yakir2013extremes using the change of measure techniques. To illustrate the accuracy of approximation given in Theorem 10, we perform Monte Carlo trials with , and . Figs. 4(a) and (b) compare the simulated and theoretical approximation of ARL given in Theorem 10 when and , respectively. Note that expression (10) takes a similar form as the ARL approximation obtained in xie2013sequential for the multi-sensor mean-shift case, and only differs in the upper and lower limits in the integration. In Figs. 4(a) and (b) we also plot the approximate ARL for the mean shift case in xie2013sequential , which shows the importance of having the corrected integration upper and lower limits in our approximation. In practice, ARL is usually set to and . Table 1 compares the thresholds obtained theoretically and from simulation at these two ARL levels, which demonstrates the accuracy of our approximation.

|

|

| (a) | (b) |

| ARL | Theory | Simulated ARL | Simulated | |

|---|---|---|---|---|

| 5000 | 46.34 | 5024 | 46.31 | |

| 10000 | 47.64 | 10037 | 47.60 | |

| 5000 | 77.04 | 5035 | 76.89 | |

| 10000 | 78.66 | 10058 | 78.59 |

Expected detection delay (EDD). After a change-point occurs, we are interested in the expected number of additional observations required for detection. In this section we establish an approximation upper bound to the expected detection delay. Define a quantity

| (11) |

which roughly captures the total signal-to-noise ratio of all affected sensors.

Theorem 4.2 (EDD of .)

Suppose , with other parameters held fixed. Let be a standard normal random variable. If the window length is sufficiently large and greater than , then

| (12) |

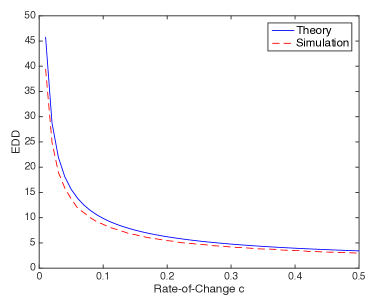

where is defined at the beginning of Section 2. To demonstrate the accuracy of (12), we perform 500 Monte Carlo trials. In each trial, we let the change-point happen at the initial time and randomly select sensors affected by the change and set the rate-of-change for a constant , . The thresholds for each procedure are set so that their ARLs are equal to 5000. Fig. 5 shows EDD versus , where our upper bound turns out to be an accurate approximation to EDD.

5 Optimality

In this section, we prove that our detection procedures: and the window limited versions and are asymptotically first order optimal. The optimality proofs here extends the results in tartakovsky2014sequential , lai1998information , for our multi-sensor non-i.i.d. data setting. The non-i.i.d.ness is due to the fact that under the alternative, the means of the samples change linearly as the number of post-change samples grows. Following the classic setup, we consider a class of detection procedures with their ARL greater than some constant , and then find an optimal procedure within such a class to minimize the detection delay. Since it is difficult to establish an uniformly optimal procedure for any given , we consider the asymptotic optimality when tends to infinity.

We first study a general setup with non- distributions for the multi-sensor problem, and establish optimality of two general procedures related to and . Then we specialize the results to the multi-sensor slope-change detection problem. In particular, we generalize the lower bound for the detection delay from the single sensor case (Theorem 8.2.2 in tartakovsky2014sequential and Theorem 1 in lai1998information ) to our multi-sensor case. We also generalize the result therein to our setting where the log-likelihood ratio grows polynomially on the order of for as the number of post-change observations grows (in the classic setting ); this is used to account for the non-stationarity in our problem.

Setup for general non- case. Consider a setup for the multi-sensor problem with non- data. Assume there are sensors that are independent (or with known covariance matrix so the observations can be whitened across sensors), and that the change-point affects all sensors simultaneously. Observations at the th sensor are denoted by over time . If there is no change, are distributed according to conditional densities , where = (this allows the distributions at time to be dependent on the previous observations). Alternatively, if a change-point occurs at time and the th sensor is affected, are distributed according to conditional densities for , and are according to for . Note that the post-change densities are allowed to be dependent on the change-point . Define a filtration at time by . Again, assume a subset of sensors are affected by the change-point. Similar to Section 2, with a slight abuse of notation, we denote , , and as the probability and expectation when there is no change, or when a change occurs at time and a set of sensors are affected by the change, with the understanding that here the probability measures are defined using the conditional densities.

Optimality criteria. We adopt two commonly used minimax criteria to establish the optimality of a detection procedure . Similar to Chapter 8.2.5 of tartakovsky2014sequential , we consider two criterions associated with the -th moment of the detection delay for . The first criterion is motivated by Lorden’s work lorden1971procedures , which minimizes the worst-case delay

| (13) |

where “esssup” denotes the measure theoretic supremum that excluded points of measure zero. In other words, the definition (13) first maximizes over all possible trajectories of observations up to the change-point and then over the change-point time. The second criterion is motivated by Pollak’s work pollak1985optimal , which minimizes the maximal conditional average detection delay

| (14) |

The extended Pollak’s criterion (14) is not as strict as the extended Lorden’s criterion in the sense that SM, and we prefer (14) since it is connected to the conventional decision theoretic approach and the resulted optimization problem can possibly be solved by a least favorable prior approach. The EDD defined earlier in Section 4 can be viewed as ESMm and SMm for , and the supremum over happens when .

Define to be a class of detection procedures with their ARL greater than :

A procedure is optimal, if it belongs to and minimizes or .

Optimality for general non- setup. Under the above assumptions, the log-likelihood ratio for each sensor is given by

For any set of affected sensors, the log-likelihood ratio is given by

| (15) |

We first establish an lower bound for any detection procedure. The constant below can be understood intuitively as a surrogate for the Kullback-Leibler (KL) divergence in the hypothesis problem. When the observations are , is precisely the KL divergence lai1998information .

Theorem 5.1 (General lower bound.)

For any such that there exists some , converges in probability to a positive constant under ,

| (16) |

and in addition, for all , for an arbitrary

| (17) |

Then,

-

(i)

for all , there exists some such that

(18) -

(ii)

for all ,

(19)

Consider a general mixture CUSUM procedure related to , which has also been studied in siegmund2011detecting and xie2013sequential :

| (20) |

where is a prescribed threshold. The following lemma shows that for an appropriate choice of the threshold , has an ARL lower bounded by and, hence, for such thresholds it belongs to .

Lemma 1

For any , , provided .

Theorem 5.2 (Optimality of .)

For any such that there exists some and a finite positive number for which (17) holds, and for all and ,

| (21) |

If and , then is asymptotically minimax in the class in the sense of minimizing and for all to the first order as .

We can also prove that the window-limited version is asymptotically optimal. Since the window length affects ARL and the detection delay, in the following we denote this dependence more explicitly by .

Corollary 1 (Optimality of .)

Assume the conditions in Theorem 5.2 hold and in addition,

| (22) |

If and , then is asymptotically minimax in the class in the sense of minimizing and for all to the first order as .

Intuitively, this means that the window length should be greater than the first order approximation to the detection delay . Note that our earlier result (12) for the expected detection delay of the multi-sensor case is of this form for and .

Similarly, we may consider a general mixture GLR procedure related to as in xie2013sequential . Denote the log-likelihood (15) as to emphasize its dependence on an unknown parameter . The mixture GLR procedure maximizes over a parameter space before combining them across all sensors. Unfortunately, we are unable to establish the asymptotic optimality for the general GLR procedure and its window limited version, due to a lack of martingale property.

Optimality for multi-sensor slope change. Note that and correspond to special cases of , , so we can use Theorem 5.2 and Corollary 1 to show their optimality by checking conditions. Although we are not able to establish optimality of the general mixture GLR procedure as mentioned above, we can prove the optimality for by exploiting the structure of the problem.

Lemma 2 (Lower bound.)

The following lemma plays a similar role as the general version Lemma 1 in our multi-sensor case in (1), and it shows that for a properly chosen threshold , ARL of is lower bounded by and, hence, for such threshold it belongs to .

Lemma 3

For any , , provided

Remark 6 (Implication on window length.)

Lemma 3 shows that to have , we need .

Theorem 5.3 (Asymptotical optimality of , and .)

Consider the multi-sensor slope change detection problem (1).

-

(i)

If and , then is asymptotically minimax in class in the sense of minimizing expected moments and for all to the first order as .

-

(ii)

In addition to conditions in (i), if the window length satisfies

(23) then is asymptotically minimax in class in the sense of minimizing expected moments and for all to first order as .

-

(iii)

If , , the window length satisfies and (23) holds, then is asymptotically minimax in class in the sense of minimizing and for to first order as .

Remark 7

Above we prove the optimality of and for . However, we can only prove the optimality of for a special case , due to a lack of martingale properties here.

6 Numerical Examples

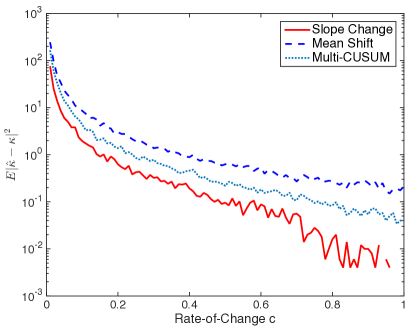

Comparison with mean-shift GLR procedures. We compare the mixture procedure for slope change detection, with the classic multivariate CUSUM multivariate_CUSUM and the mixture procedure for mean shift detection xie2013sequential . The multivariate CUSUM essentially forms a CUSUM statistic at each sensor, and raises an alarm whenever a single sensor statistic hits the threshold. As commented earlier in Remark 3, the only difference between and the mixture procedure for mean shift in xie2013sequential is how is defined. Following the steps for deriving (32), we can show that the mean shift mixture procedure is also asymptotically optimal for the slope change detection problem. Here, our numerical example verifies this, and show that the improvement of EDD by using versus the multi-variate CUSUM and the mean-shift mixture procedure is not significant. However, the mean-shift mixture procedure fails to estimate the change-point time accurately due to model mismatch. Fig. 6 shows the mean square error for estimating the change-point time , using the multi-chart CUSUM, the mean-shift mixture procedure, and , respectively. Note that has a significant improvement.

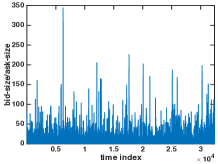

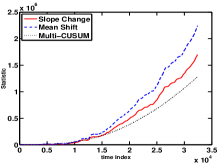

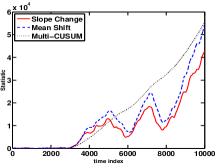

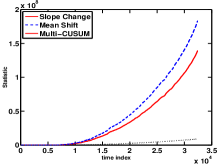

Financial time series. In the earlier example illustrated in Fig. 7(a), the goal is to detect a trend change online. Clearly a change-point occurs at time 8000 in the stock price, and such a change-point is verifiable. Fig. 7(b) shows that there is a peak in the bid size versus the ask size, which usually indicates a change in the trend of the price (possible with some delay). To illustrate the performance of our method in this financial dataset, we plot the detection statistics by using a “single-sensor”, i.e., using only one data stream, and by using “multi-sensor” scheme, i.e. using data from multiple streams, which in this case correspond to factors (e.g, stock price, total volume, bid size and bid price, as well ask size and ask price). In fact, only 4 factors out of 8 factors contain the change-point. Fig. 7(c) plots the statistic if we use only a single-sensor. Fig. 7(d) illustrates the statistic when we use all the 8 factors and preprocess by whitening with the covariance of the factors as described in Section 5. The statistics all rise around time 8000 with the multi-sensor statistic to be smoother and indicates a lower false detection rate. Looking at Fig. 7(d), after the major trend change (around sample index 8000), the multi-chart CUSUM statistic rises the slowest. Although it appears, the slope-change mixture procedure rises a bit slower than the mean-shift mixture procedure, we demonstrate in simulation that for fixed ARL these two procedures have similar EDD s, and also in Fig. 5 that the slope-change mixture procedure has a better performance in estimating than the mean-shift mixture procedure. Therefore, the slope-change mixture procedure is still preferrable.

|

|

| (a) Stock price data. | (b) ask-size/bid-size |

|

|

| (c) Single-sensor. | (d) Zoom-in of (c). |

|

|

| (e) Multi-sensor, correlation. | (f) Zoom-in of (e). |

Aircraft engine multi-sensor prognostic. We present an engine prognostic example using the aircraft turbofan engine dataset simulated by NASA111Data can be downloaded from http://ti.arc.nasa.gov/tech/dash/pcoe/prognostic-data-repository/. In the dataset, multiple sensors measure different physical properties of the aircraft engine to detect a faulty condition and to predict the whole life time. The dataset contains training systems and testing systems. Each system is monitored by sensors. In the training dataset, we have a complete sample path from the initial time to failure for each of the sensors of each training system. In the testing dataset, we only have partial sample paths (i.e., the system fails eventually but we have not observed that yet and it still has a remaining life). Our goal is to predict the whole life for the test systems using available observations. The dataset also provides ground truth, i.e., the actual failure times (or equivalently the whole life) of the testing systems.

We first apply our mixture procedures to each training system , , to estimate a change-point location (which corresponds to the maximizer of in the definition of when the procedure stops), and the rate-of-change at th sensor for the th system using (5). Then fit a simple survival model using and as regressors in determining the remaining life. We build a model for the Time-To-Failure (TTF) of system based a log location-normal model, which is commonly used in reliability theory fang2015adaptive : where is a user specified scale parameter that is assumed to be the same for each system, is the location parameter that is assumed to be a linear function of the rate-of-change: where is a vector of the regression coefficients that are estimated by maximum likelihood. Next, we apply the mixture procedure on the th testing system to estimate the change-point time and the rate-of-change , and substitute them into the fitted models to determine a TTF using the mean value. The whole life of the th system is estimated as plus its mean TTF.

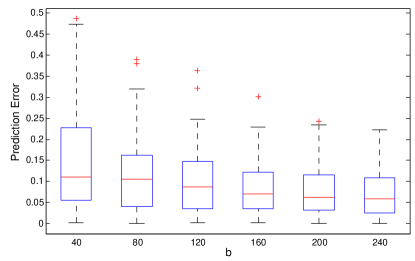

We use the relative prediction error as performance metric, which is the absolute difference between the estimated life and the actual whole life, divided by the actual whole life. Fig. 8 shows the box-plot of the relative prediction error versus threshold . Our method based on change-point detection works well and it has a mean relative prediction error around 10%. Here the choice of the threshold has a tradeoff: the relative prediction error decreases with a larger ; however, a larger also causes a longer detection delay.

|

7 Discussion: adaptive choice of

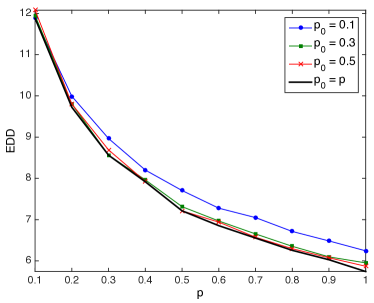

The mixture procedure assumes that a fraction of the sensors are affected by the change. In practice, can be different from which is the actual fraction of sensors affected. The performance of the procedure is fairly robust to the choice of . Fig. 9 compares the simulated EDD of a mixture procedure with a fixed value, versus a mixture procedure when setting if we know the true fraction of affected sensors. Again, thresholds are chosen such that ARL for all cases are 5000. Note that the detection delay is the smallest if matches ; however, EDD in these two settings are fairly close when .

Still, we may improve the performance of the mixture procedure by adapting the parameter using a method based on empirical Bayes. Assume each sensor is affected with probability , but now itself is a random variable with Beta distribution . This also allows the probability of being affected to be different at each sensor. With sequential data, we may update by computing a posterior distribution of using data in the following way. Choosing a constant , we believe that the th sensor is likely to be affected by the change-point if is larger than . Let denote an indicator function. For each , assume is a Bernoulli random variable with parameter . Due to conjugacy, the posterior of at the th sensor, given up to time , is also a Beta distribution with parameters . An adaptive mixture procedure can be formed using the posterior mean of , which is given by :

| (24) |

where is a prescribed threshold.

We compare the performance of with its non-adaptive counterpart by numerical simulations. Assume and there are 10 sensors affected from the initial time with a rate-of-change . The parameters for are and . Again, the thresholds are set so that the simulated ARL for both procedures are 5000. Table 2 shows that has a much smaller EDD than when signal is weak with a relative improvement around . However, it is more difficult to analyze ARL of the adaptive method theoretically.

| Rate-of-change | 0.01 | 0.03 | 0.05 | 0.07 | 0.09 |

|---|---|---|---|---|---|

| Non-Adaptive | 54.15 | 26.24 | 18.75 | 14.98 | 12.74 |

| Adaptive | 38.56 | 20.28 | 14.42 | 12.17 | 10.13 |

Acknowledgement

Authors would like to thank Professor Shi-Jie Deng at Georgia Tech for providing the financial time series data. This work is partially supported by NSF grant CCF-1442635 and CMMI-1538746.

References

- (1) Chan, H.: Optimal detection in multi-stream data. arXiv:1506.08504 (2015)

- (2) Fang, X., Zhou, R., Gebraeel, N.: An adaptive functional regression-based prognostic model for applications with missing data. Reliability Engineering & System Safety 133, 266–274 (2015)

- (3) Fellouris, G., Sokolov, G.: Multisensor quickest detection. arXiv:1410.3815 (2014)

- (4) Hadjiliadis, O., Zhang, H., Poor, H.V.: One shot schemes for decentralized quickest change detection. Information Theory, IEEE Transactions on 55(7), 3346–3359 (2009)

- (5) King, E.: Veeravalli to develop sensor networks for chemical, biological threat detection (2012). URL http://csl.illinois.edu/news/veeravalli-develop-sensor-networks-chemical-biological-threat-detection

- (6) Lai, T.L.: Sequential changepoint detection in quality control and dynamical systems. Journal of the Royal Statistical Society. Series B (Methodological) pp. 613–658 (1995)

- (7) Lai, T.L.: Information bounds and quick detection of parameter changes in stochastic systems. Information Theory, IEEE Transactions on 44(7), 2917–2929 (1998)

- (8) Liu, K., Gebraeel, N., Shi, J.: A data-level fusion model for developing composite health indices for degradation modeling and prognostic analysis. Automation Science and Engineering, IEEE Transactions on 10(3), 652–664 (2013). DOI 10.1109/TASE.2013.2250282

- (9) Lorden, G.: Procedures for reacting to a change in distribution. The Annals of Mathematical Statistics pp. 1897–1908 (1971)

- (10) Pollak, M.: Optimal detection of a change in distribution. The Annals of Statistics pp. 206–227 (1985)

- (11) Saxena, A., Goebel, K., Simon, D., Eklund, N.: Damage propation modeling for aircraft engine run-to-failure simulation. In: Int. Conf. Prognostics and Health Management (PHM) (2008)

- (12) Siegmund, D.: Sequential Analysis: Tests and Confidence Intervals. Springer (1985)

- (13) Siegmund, D., Yakir, B.: The Statistics of Gene Mapping. Springer (2007)

- (14) Siegmund, D., Yakir, B., Zhang, N.R., et al.: Detecting simultaneous variant intervals in aligned sequences. The Annals of Applied Statistics 5(2A), 645–668 (2011)

- (15) Tartakovsky, A., Nikiforov, I., Basseville, M.: Sequential analysis: Hypothesis testing and changepoint detection. CRC Press (2014)

- (16) Veeravalli, V.: Quickest detection and isolation of line outages in power systems. In: International Workshop on Sequential Methods (IWSM) (2015)

- (17) Woodall, W.H., Ncube, M.M.: Multivariate CUSUM qualify control procedures. Technometrics 27(3) (1985)

- (18) Xie, Y., Siegmund, D.: Sequential multi-sensor change-point detection. The Annals of Statistics 41(2), 670–692 (2013)

- (19) Yakir, B.: Extremes in random fields: a theory and its applications. John Wiley & Sons (2013)

Appendix A An informal derivation of Theorem 10: ARL

We first obtain an approximation to the probability that the stopping time is greater than some big constant . Such an approximation is obtained using a general method for computing first passing probabilities first introduced in yakir2013extremes and developed in siegmund2011detecting . The method relies on measure transformations that shift the distribution of each sensor over a window that contains the hypothesized post-change samples. More technical details to make the proofs more rigorous are omitted. These details have been described and proved in siegmund2011detecting .

In the following, let . Define the log moment-generating-function . Recall that is a generic standardized sum over all observations within a window of size in one sensor, and the parameter is selected by solving the equation

Since is a standardized weighted sum of independent random variables, converges to a limit as , and converges to a limiting value. We denote this limiting value by .

Denote the density function under the null as . The transformed distribution for all sequences at a fixed current time and at a hypothesized change-point time (and hence there are hypothesized post-change samples) is denoted by and is defined via

Let

Let the region

be the set of all possible change-point times and time up to a horizon . Let

be the event of interest. Hence, we have

| (25) |

where

As explained in siegmund2011detecting , under certain verifiable assumptions, a “localization lemma” allows simplifying the quantities of the form in into a much simpler expression of the form

where is the standard deviation of and is the limit of as . This reduction relies on the fact that, for large and , the “local” processes and are approximately independent of the “global” process . This allows the expectation to be decomposed into the expectation of times the expectation involving , treating as a constant.

Let , and denote by which are i.i.d. normal random variables, . Note that, use Taylor expansion up to the first order, we obtain

| (26) |

Note that in the above expression, the first term has two weighted data sequences running backwards from and when and both tends to infinity they tend to cancel with each other. Hence, asymptotically we need to consider the second term. Observe that one may let and for in the definition of the increments and still maintain the required level of accuracy. When the first term in the above expression, and the second term consists of two terms that are highly correlated. The second term can be rewritten as

| (27) |

Since all sensors are assumed to be independent (or has been whitened by a known covariance matrix so the transformed coordinates are independent), so the covariance between the two terms is given by

| (28) |

For each , let and , and define and . We have

By choosing , we know that the expression above is approximately on the order of

Let . Hence, by summarizing the derivations above and applying the law of large number, we have that when and , the covariance between the two terms become

This shows that the two-dimensional random walk decouples in the change-point time and the time index and the variance of the increments in these two directions are the same and are both equal to . Hence, the random walk along these two coordiates are asymptotically independent and it becomes similar to the case studied in siegmund2011detecting . Compare this with (the equation following equation (A.4) in siegmund2011detecting ), note that the only difference is that here the variance of the increment is proportional to instead of , so we may follow a similar chains of calculation as in the proof in Chapter of yakir2013extremes , siegmund2011detecting xie2013sequential , the final result corresponds to modifying the upper and lower limit by changing the window length expression to be and .

Appendix B An informal derivation of Theorem 4.2: EDD

Recall that is defined in (6), let . Then for , are i.i.d. normal random variables with mean and unit variance, and for , are i.i.d. standard normal random variables. Since we may write

| (29) |

For any time and , we have

| (30) |

which grows cubically with respect to time. For the unaffected sensors, , . Hence, the value of the detection statistic will be dominated by those affected sensors.

On the other hand, note that when is large,

Then the expectation of the statistic in (8) can be computed if is sufficiently large (at least larger than the expected detection delay), as follows:

At the stopping time, if we ignore of the overshoot of the threshold over , the value statistic is . Use Wald’s identify Siegmund1985 and if we ignore the overshoot of the statistic over the threshold , we may obtain a first order approximation as , by solving

| (31) |

From Jensen’s inequality, we know that . Therefore, a first-order approximation for the expected detection delay is given by

| (32) |

Appendix C Proof for Optimality

Proof (Proof of Theorem 5.1)

The proof starts by a change of measure from to . For any stopping time , we have that for any , and ,

| (33) |

where is the indicator function of any event , the first equality is Wald’s likelihood ratio identity and the last inequality uses the fact that for any event and and probability measure , .

From (33) we have for any

| (34) |

where

Next, we want to show that both and converge to zero for any and any as goes to infinity.

Second, by Lemma 6.3.1 in tartakovsky2014sequential , we know that for any there exists a , possibly depending on , such that

Choosing , then we have

and therefore,

| (37) |

where the last convergence holds since for any and we have . Therefore, for every and for any we have that for some ,

which proves (18).

Next, to prove (19), since

it is suffice to show that for any ,

| (38) |

where the residual term does not depend on . Using the result (18) just proved, we can have that for any , there exists some such that

Therefore, by also Chebyshev inequality, for any and , there exist some such that

| (39) |

where the residual term does not depend on . Since we can arbitrarily choose such that the (39) holds, so we have (38), which completes the proof.

Proof (Proof of Lemma 1)

Rewrite as

| (40) |

and define an extended Shiryaev-Roberts (SR) procedure as follows:

| (41) |

where

Clearly, . Therefore, it is sufficient to show that if .

Noticing the martingale properties of the likelihood ratios, we have

| (42) |

for all , and . Moreover, noticing that

| (43) |

then combining (42) we have for all ,

| (44) |

Therefore, the statistic is a -martingale with zero mean. If then the theorem is naturally correct, so we only suppose that and thus exists. Next, since on the event , we have

Now we can apply the optional sampling theorem to have . By the definition of stopping time , we have . Thus, we have , which shows that if .

Proof (Proof of Theorem 5.2)

First, we notice that if

Therefore, by Theorem 5.1, it is sufficient to show that if and , then

| (45) |

Equivalently, it is sufficient to prove that

| (46) |

To start with, we consider a special case when in and denote it by

Next, we will prove an asymptotical upper bound for the detection delay of .

Let

| (47) |

and then . Noticing that under , we have almost surely since the the log-likelihood ratios are for the sensors that are not affected. Therefore, by (21) we can have that for any , and some sufficiently large ,

| (48) |

Then, for any and integer , we can use (48) times by conditioning on for in succession (see lai1998information ) to have

| (49) |

Therefore, for sufficiently large and any , we have

| (50) |

where the first inequality can be known directly from the geometric interpretation of expectation of discrete nonnegative random variables and the last equality holds since for any given , as so that the radius of convergence is . Using the fact that we prove (46) for the case .

Next, we will deal with the case when . Rewrite as

then

Clearly, , and thus

| (51) |

Therefore, we can claim that (46) holds for any fixed since and are constants. If and , belongs to and achieves its lower bound.

Proof (Proof of Corollary 1)

Proof (Proof of Lemma 2)

Consider testing problem (1), then for any and ,

We define, for each and for all ,

Then we have

where we define .

Under probability measure , we easily know that are independent variables which follow normal distribution . Other simple computation tells us that

and under probability measure ,

where denotes the variance of random variable . Therefore, combining Kronecker s lemma with the Kolmogorov convergence criteria, we have immediately a strong law of large numbers which tells us that

Finally, we complete the proof by using the fact that all the observations are independent.

Proof (Proof of Lemma 3)

First, define , then

| (52) |

where is a random variable with distribution. Then, since is a non-negative discrete random variable, we have

| (53) |

Then if we can choose some so that

we can claim that and thus . To choose appropriate threshold , we need use the tail bound for the distribution. Since is sub-exponential with parameter , it is well known that if . If we set

then .

Proof (Proof of Theorem 5.3)

By Lemma 2, we can use Theorem 5.1 to obtain a lower bound for the detection delays of arbitrary procedures in . Specifically, for all ,

| (54) |

(i) Since is a specified mixture CUSUM procedure for testing problem (1) and the observations are independent, the optimality is an immediate corollary from Theorem 5.2.