A reduced-form model for level-1 limit order books

Abstract.

One popular approach to model the limit order books dynamics of the best bid and ask at level-1 is to use the reduced-form diffusion approximations. It is well known that the biggest contributing factor to the price movement is the imbalance of the best bid and ask. We investigate the data of the level-1 limit order books of a basket of stocks and study the numerical evidence of drift, correlation, volatility and their dependence on the imbalance. Based on the numerical discoveries, we develop a nonparametric discrete model for the dynamics of the best bid and ask, which can be approximated by a reduced-form model that incorporates the empirical data of correlation and volatilities with analytical tractability that can fit the empirical data of the probability of price movement.

Key words and phrases:

Limit order books, data analysis, reduced form models, diffusion approximations2010 Mathematics Subject Classification:

91G99, 62P051. Introduction

The traditional human traders have largely been replaced by the automatic and electronic traders in today’s financial world. The role and the controversy of those high frequency traders have caught public’s attention ever since the infamous flash crash on May 6, 2010 and the long-standing debate over the fairness of equity markets briefly became salient with the recent publication of the book “Flash Boys” by Michael Lewis, who argued that the trading has become unfair and skewed by the high-frequency trading and dampened the opportunities of the regular investors.

In automatic and electronic order-driven trading platforms, orders arrive at the exchange and wait in the limit order book. There are two types of orders in the limit order book: market orders and limit orders. Cancellation is also allowed. One of the key research areas in limit order books has been centered around modeling the limit order book dynamics. In this paper, we only consider the limit order book model at level-1, that is, we only study the dynamics of the volumes at the best bid and the best ask.

The limit order book is a discrete queuing system and many of the works in the literature model study the dynamics of the limit order book in a discrete setting directly, see e.g. Cont et al. [5], Abergel and Jedidi [1]. Another popular approach, is to study the reduced-form of the discrete model. In the sense of heavy traffic limits, various authors, see e.g. Cont and de Larrard [3, 4], Avellaneda et al. [2], Guo et al. [8] considered the diffusion limit as an approximation of the discrete model. The diffusion approximation is valid if the average queue sizes are much larger than the typical quantity of shares traded and the frequency of orders per unit time is high, see e.g. the discussions in Avellaneda et al. [2]. With the empirical finding of approximate scale invariance, Bouchaud et al. [7] derive a two dimensional Fokker-Planck equation describing the statistical behavior of the queue dynamic. In the recent work by Huang et al. [10], they introduced a model which accommodates the empirical properties of the full order book and the stylized facts of lower frequency financial data. In their model, the order flows have state-dependent intensities. We refer to the recent book [12] for more details.

One research area of great interests is the dynamics of the limit order books and how it influences the stock price movement, see e.g. Avellaneda et al. [2], Cont et al. [5], Huang and Kercheval [9] etc. There is strong empirical evidence to suggest the biggest factor that drives the movement for the stock price to the next level is the imbalance of the best bid and the best ask, see e.g. Avellaneda et al. [2], which is defined as the ratio of the volume at the best bid and total volume at the best bid and ask:

| (1.1) |

In the limit order book, the stock price will move up when the best ask queue is depleted and the price will move down when the best bid queue is depleted. The empirical data suggests that the probability that the stock price will move up increases as the imbalance increases. One can think the probability of price moving up as a monotonically increasing function of the current imbalance. One may expect that the probability of the stock price moving up is a monotonic function from to as the imbalance increases from to . But empirical evidence suggests otherwise. In Avellaneda et al. [2], they discovered that even though the probability of the stock price moving up is indeed an increasing function of the imbalance, it increases from a positive value to a value less than one. One explanation is the hidden liquidity, that is, the sizes that are not shown in the limit order book, see [2]. As it is hypothesized in [2], there can be two explanations for hidden liquidity. First, markets are fragmented and it can happen that once the best ask on an exchange is depleted, the price will not necessarily go up since an ask order at that price may still be available on another market and a new bid cannot arrive until that price is cleared on all markets. Second, there exist so-called iceberg orders, the trading algorithms that split large orders into smaller ones that refill the best quotes as soon as they are depleted.

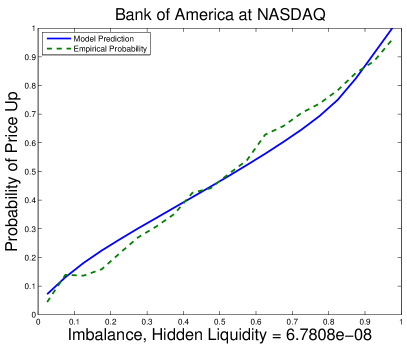

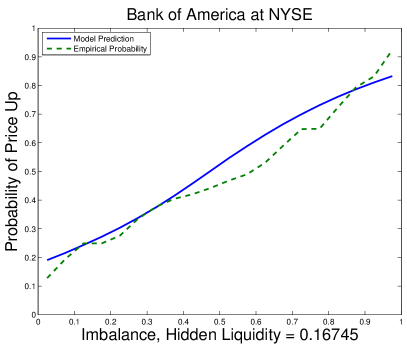

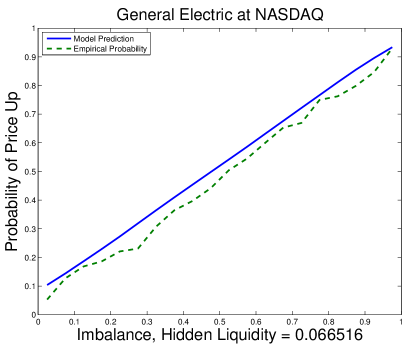

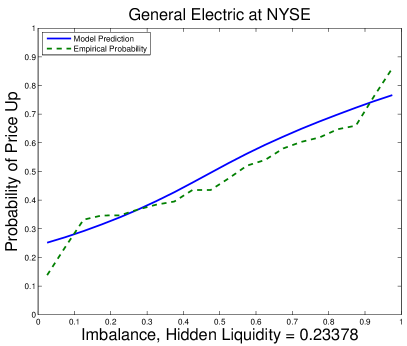

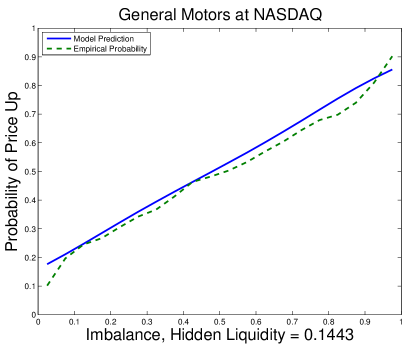

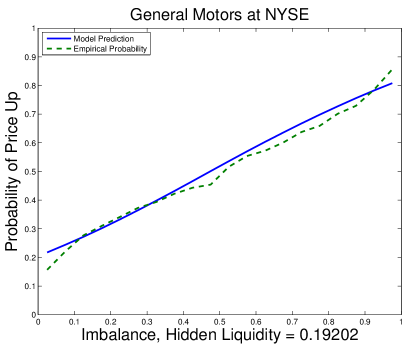

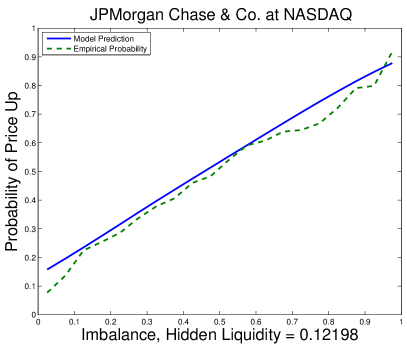

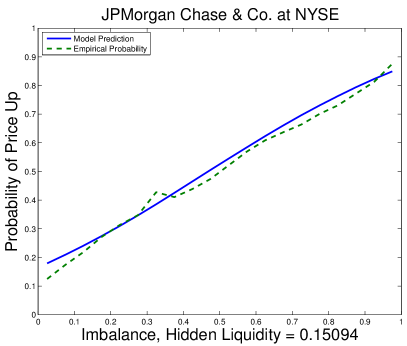

Indeed, we also discover the hidden liquidity in our numerical analysis and we use the idea of the hidden liquidity to better fit the model. The numerical evidence suggests that empirical probability of price moving up depends linearly on the imbalance, with hidden liquidity at the very small and large imbalance levels, see Figures 10, 11, 12, 13. In [2], correlated Brownian motions are used as a reduced-form model to describe the dynamics at the best bid and ask queues. The linear dependence of the empirical probability of price moving up on the imbalance level suggests that in the correlated Brownian motions model, the correlation should be exactly . However, we carried out numerical analysis to study the correlation and volatilities of the best bid and ask sizes and their dependence on the imbalance, and found out that the correlation is negative, but far away from and it is also dependent on the level of the imbalance. Therefore, the correlated Brownian motions might be too simplistic explaining the dynamics of the best bid and ask queues. In this paper, we will build up a non-parametric model that can fit the data of the empirical correlation, empirical volatilities of the best bid and ask sizes and the empirical probability of price moving up simultaneously.

In this paper, we will use data to study the level-1 limit order books for a basket of stocks, to further understand the dependence on the imbalance of the best bid and ask sizes. We will look at a basket of stocks and also compare the results amongst different exchanges, in particular, NASDAQ and NYSE because our empirical data suggest that the stocks we selected have the largest trading volumes in these two stock exchanges. We discover that the micro structure and the dynamics of the limit order books depend on their exchanges, in the sense, that the key statistics like correlation between the best bid and ask, and the drift effect at the best bid and ask queues can differ across the exchanges. The discrepancy amongst the exchanges has caught a lot of attention lately. As noted in a recent article on Wall Street Journal [13]:

“There is no question that U.S. equity markets are fragmented. The New York Stock Exchange’s share of trading in its listed stocks has dropped to 32% of its volume from 77% a decade ago… This fragmentation… also creates arbitrage opportunities that did not exist when trading markets were unified.”

In our empirical study, we discover the evidence of discrepancy amongst different exchanges and also across different stocks. This has two possible implications. First, the discrepancy can possibly be explained by the different trading patterns of different algorithmic traders. Say we have two high frequency traders A and B, who are trading two different baskets of stocks. Then the different behavior of the dynamics of the limit order books of the stocks may be due to the different trading strategies and patterns of these two different players. As we will see later from our empirical studies, different stocks are concentrated in different exchanges. Hence the different trading strategies of the traders behind different stocks can result in the discrepancy across the different exchanges. Second, the fragmentation of the stock exchanges may intrinsically cause the difference of the dynamics of the limit order books on different exchanges, especially when the imbalance of the best bid and ask is either small or large, that is when the queues at the best bid and ask are near depletion. In these cases, new orders may be directed to a different exchange when liquidity is still available. Thus the fragmentation of the stock exchanges and the discrepancy of the limit order books dynamics across different exchanges may create arbitrage opportunities. As the same article on WSJ pointed out,

“Transparency disappears behind a shroud of complex order types executed on vaguely sinister dark pools, trading venues that sometimes are used to disadvantage long-term investors… The remedy is to create multiple trading venues and then limit trading in a particular security to one of them.”

The paper is organized as follows. In Section 2, we carry out the data analysis to study the empirical evidence of the dependence of the dynamics at the best bid and ask on the imbalance. Based on the empirical evidence, we build a nonparametric reduced-form model in Section 3 with analytical tractability, hence extending the existing reduced-form and diffusion approximation approach of the level-1 limit order book dynamics in the literature. The conclusion of the paper is in Section 4. Finally, the technical proofs are in Appendix A and the tables are in Appendix B.

2. Data Analysis

For our data analysis, we use the consolidated quotes of the NYSE-TAQ data set from the Wharton Research Data Services (WRDS). We look at the level-1 data, that is, the best bid price, best ask price, best bid size and best ask size for a basket of stocks traded on different exchanges. The time window of the data set we selected is the first five trading days of 2014, that is, January 2nd, 3rd, 6th, 7th and 8th. We only consider the trades happened between 10am and 4pm of the trading days. We exclude the pre-market and after-market data as well as the data from the first half an hour of each trading day, i.e., 9:30-10am since these data are usually quite noisy. We concentrate on the studies of the following stocks: Bank of America (BAC), General Electric (GE), General Motors (GM) and JP Morgan & Chase (JPM). These blue-chip stocks have large market capitalization, are highly liquid and have large trading volumes. Moreover, the average prices of these stocks are reasonably small and the bid-ask spreads are narrow (one tick size most of time), so that the data sets are not too noisy. A sample table of the raw data we are using is given in Table 1 as an illustration. In Table 1, the units of best bid and ask prices are US Dollars and the units of the best bid and ask sizes are 100.

Out empirical observation from the raw data, shows that for most of time, there is only one size of the bid and ask queues changes, while the other size remains the same. Such a pattern would not be an appropriate approximation of a diffusion process that we consider in Section 3 and the empirical correlation between the bid and ask queue sizes is almost zero. We therefore average the consecutive data when there is only one queue size varying while the other one remains the same. In this way, the data would have a better approximation to a diffusion process.

| Ticker | Date | Time | Bid | Ask | Bid Size | Ask Size | Exchange |

|---|---|---|---|---|---|---|---|

| GM | 20140102 | 10:12:44 | 40.55 | 40.57 | 9 | 33 | N |

| GM | 20140102 | 10:12:44 | 40.55 | 40.57 | 7 | 33 | N |

| GM | 20140102 | 10:12:44 | 40.56 | 40.57 | 4 | 4 | T |

| GM | 20140102 | 10:12:44 | 40.56 | 40.57 | 4 | 6 | T |

| GM | 20140102 | 10:12:44 | 40.56 | 40.57 | 1 | 2 | P |

| GM | 20140102 | 10:12:44 | 40.56 | 40.57 | 3 | 6 | T |

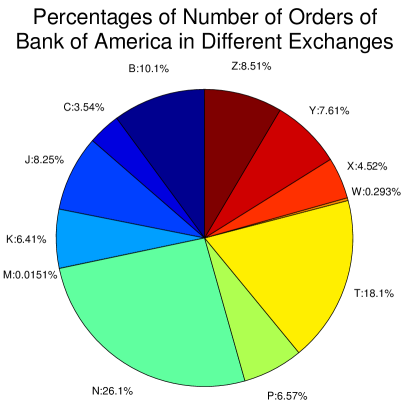

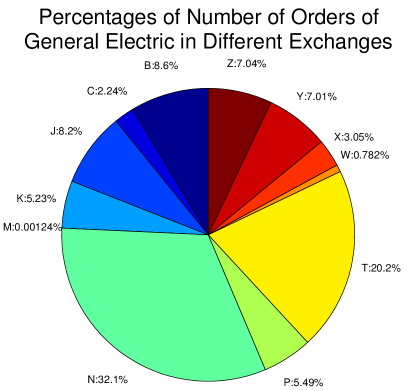

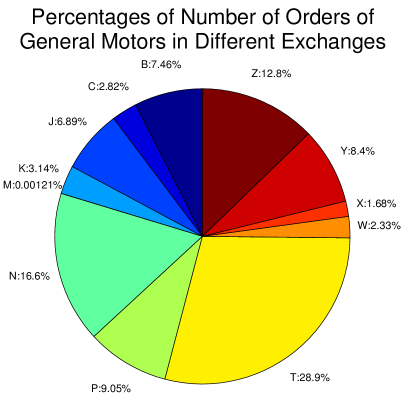

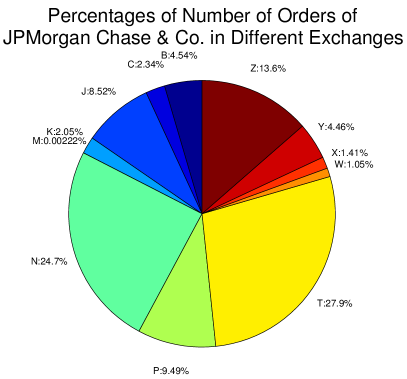

We found out that the largest volumes for these stocks we studied are traded on NASDAQ (T) and NYSE (N)111That is not always the case. For example, for the first five trading days of 2014, the exchanges that trade the largest volumes of Walmart (WMT) are NYSE (N) and BATS (Z) and the exchanges that trade the largest volumes of Microsoft (MSFT) are NASDAQ (T) and BATS (Z). For the comparison purposes, we only study those stocks with top two exchanges being NASDAQ and NYSE., see Figure 1. The symbols in Figure 1 stand for the exchanges that the stocks are traded at and the details are given in Table 2.

| Code | Exchange | Code | Exchange |

|---|---|---|---|

| B | NASDAQ OMX BX | P | NYSE Arca SM |

| C | National Stock Exchange | T | NASDAQ OMX |

| J | Direct Edge A Stock Exchange | W | CBOE Stock Exchange |

| K | Direct Edge X Stock Exchange | X | NASDAQ OMX PSX |

| M | Chicago Stock Exchange | Y | BATS Y-Exchange |

| N | New York Stock Exchange | Z | BATS Exchange |

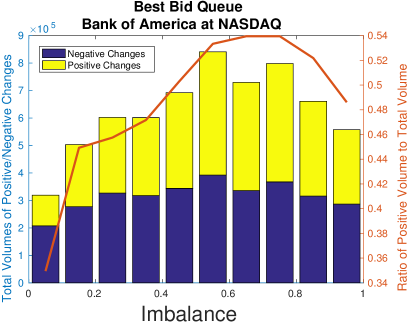

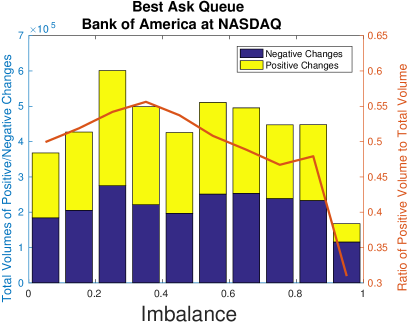

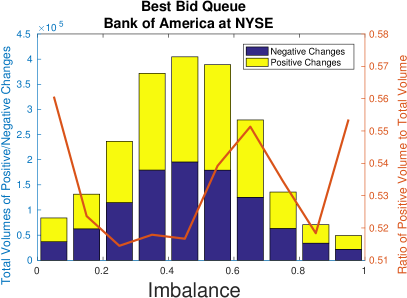

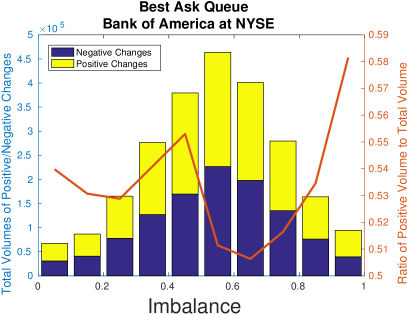

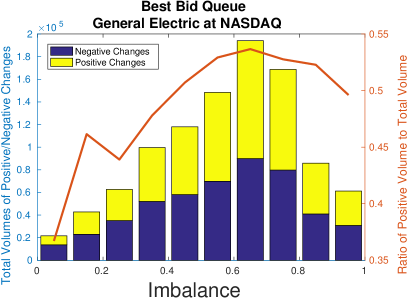

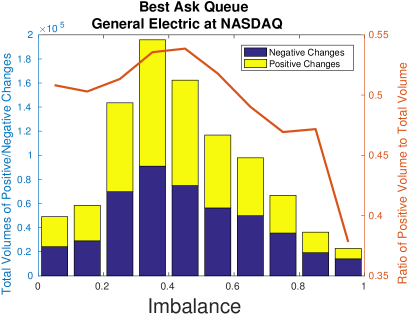

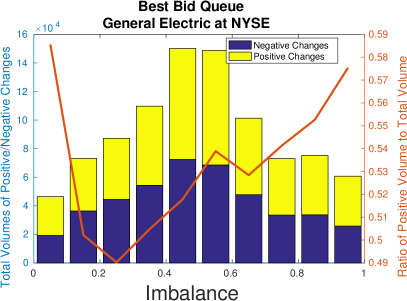

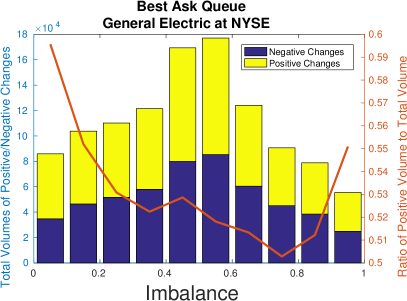

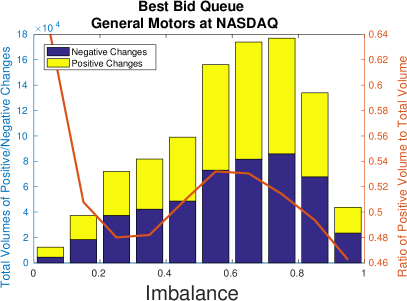

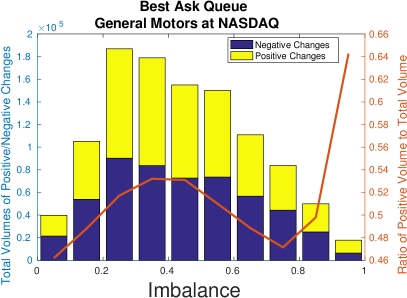

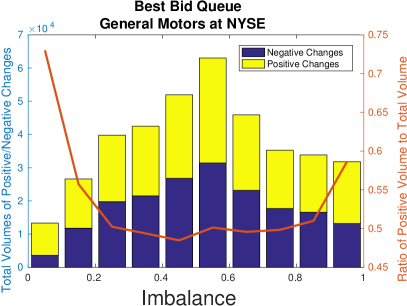

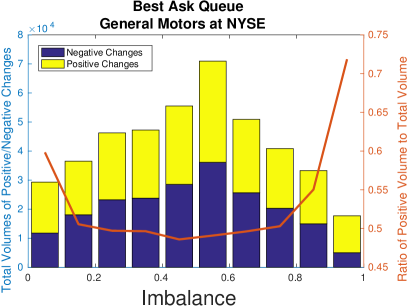

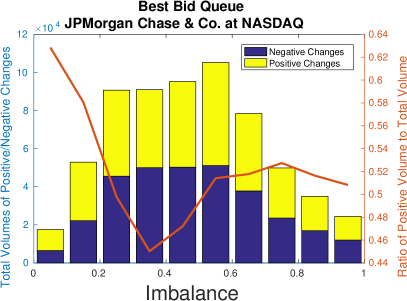

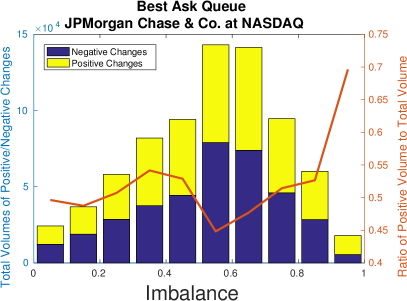

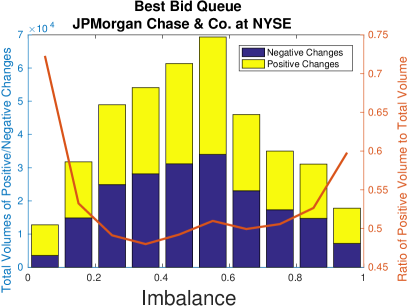

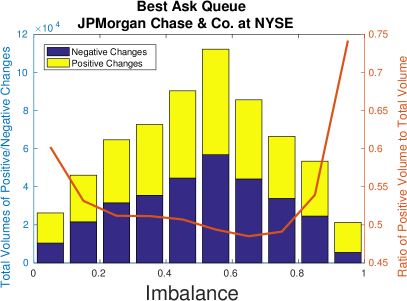

First, we investigate the drift effect of the best bid and ask queue lengths. People have used both driftless diffusions, see e.g. [2] and diffusions with constant drift, see e.g. [4, 8] to model the dynamics of the best bid and ask queues. Therefore, we are interested in seeing from the data set if there is indeed any evidence of the drift in the dynamics of the best and bid queues. If there is any evidence of drift, is the drift a constant, or a function depending on the queue lengths and the imbalance of the best bid and ask? Our studies are summarized in Figure 2 for Bank of America, Figure 3 for General Electric, Figure 4 for General Motors and Figure 5 for JP Morgan & Chase. For example, in Figure 2, we study the total volumes for the positive changes and the negative changes at the best bid queues, best ask queues for both NASDAQ and NYSE for the Bank of America stock. In all these plots, the purple bars stand for the total volume of the negative changes at a particular imbalance level and the yellow bars stand for the total volume of the positive changes at a particular imbalance level. The red lines denote the ratio of the total volume of the positive changes to the total volume of all the changes.

We can see that when the imbalance is neither too small or too large, there is little evidence of the drift in the best bid and ask queues.

On the other hand, when the imbalance is very small or very large, we do observe drifts. From the top left picture in Figure 2, it is clear that there is evidence of negative drift at the best bid queue when the imbalance is small (and hence the queue length is short) and little evidence of drift otherwise. From the top right picture in Figure 2, it is clear that there is evidence of negative drift at the best ask queue when the imbalance is small (and hence the queue length is short) and little evidence of drift otherwise. On the other hand, from the bottom two pictures in Figure 2, we observe that exactly the opposite is true for the Bank of America stock traded on NYSE, that is, there is positive drift at the best bid queue when the imbalance is small and at the best ask queue when the imbalance is large, although the drift effect is weak. One possible explanation is that there can be different scenarios when the queue lengths are short. For example, it can happen that the queue length is short when the traded stock is about to move to the next price level. There is the clustering effect of market orders and cancellations of the limit orders that can explain the negative drift we observed in the top two pictures in Figure 2. On the other hand, it is also possible that the queue length is short because it is a new queue and there is clustering effect of the arrivals of new limit orders at the new queue, which results in the positive drift we observed in the bottom two pictures in Figure 2. Similar patterns are also observed for the General Electric stock, see Figure 3. On the other hand, we see in Figure 4 that for the General Motors stock, for both NASDAQ and NYSE, there is positive drift at the best bid queue when the imbalance is small and at the best ask queue when the imbalance is large and there is little drift otherwise. Similar patterns also hold for the JP Morgan & Chase stock, see Figure 5.

The statistics are summarized in Table 3 and Table 4. BAC b and BAC a stand for the best bid and the best ask queues for BAC respectively. The number in each cell is obtained by computing

From Table 3 and Table 4, we can see that except when the imbalance is small or large, there is little evidence of the drift in the best bid and ask queues. In terms of modeling, this suggests that we can build up a model with no drift effect when the imbalance is neither too small or too large. With the small and large imbalance, instead of modeling the drift effect by adding a drift term in the dynamics, we use the idea of the hidden liquidity from [2] to better fit the model and explain the dynamics at the best bid and ask queues.

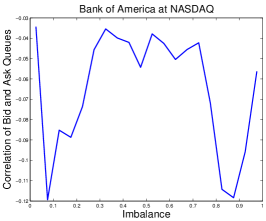

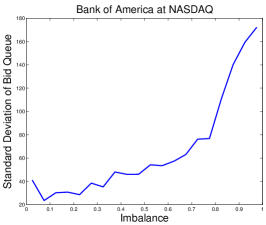

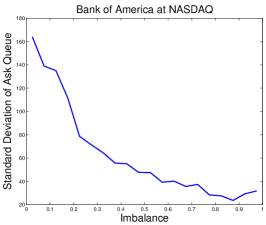

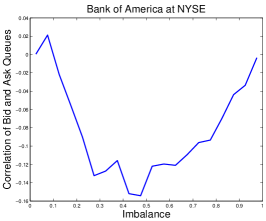

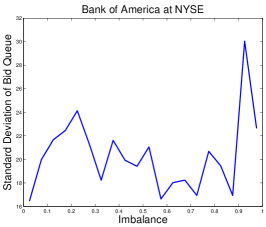

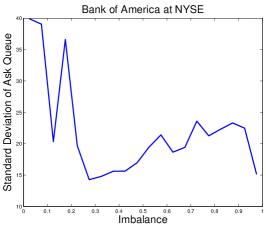

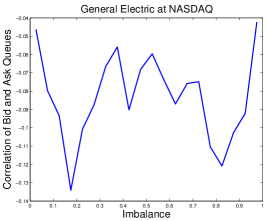

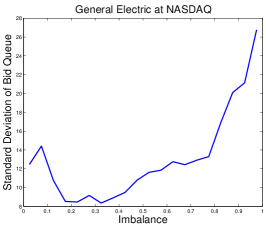

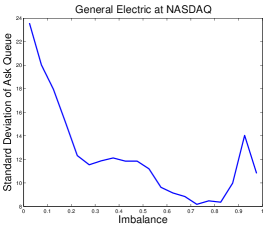

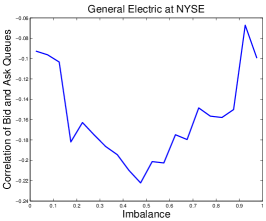

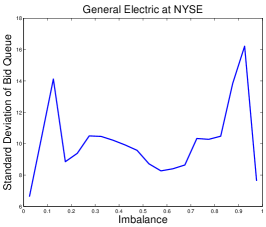

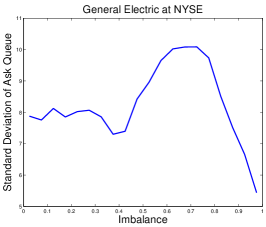

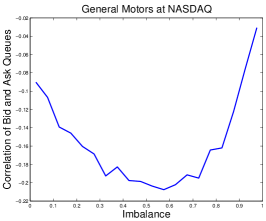

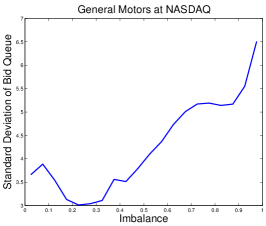

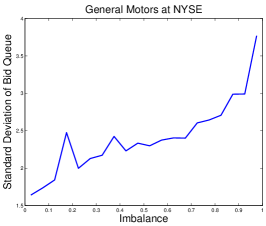

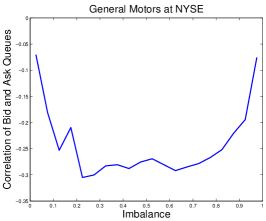

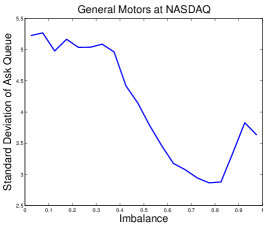

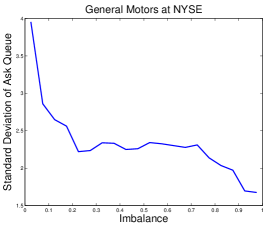

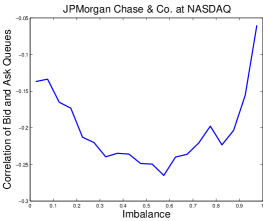

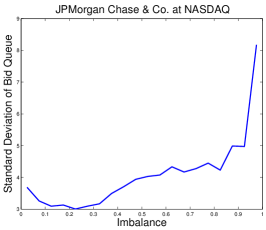

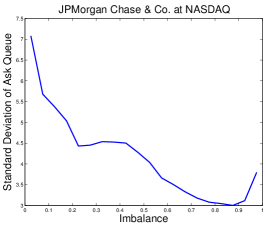

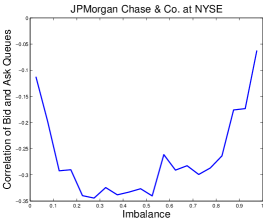

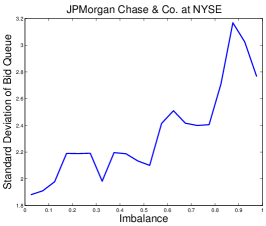

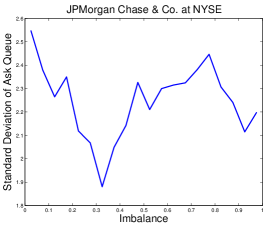

Next, we investigate the correlation between the best bid and ask dynamics, the volatilities at the best bid and ask queues, and their dependence on the imbalance. We summarized our observations for the Bank of America stock in Figure 6, the General Electric stock in Figure 7, the General Motors stock in Figure 8, and the JP Morgan & Chase stock in Figure 9. For example, let us take a look at the summary for the Bank of America stock in Figure 6. The top row in Figure 6 stands for the correlation between the size changes at the best bid and the best ask (top left), the standard deviation of size changes at the best bid (top middle), and the standard deviation of size changes at the best ask (top right) for the Bank of America stock traded in NASDAQ. Similar statistics for the Bank of America stock traded in NYSE are summarized in the bottom row in Figure 6. As we can see from the top left picture, the correlation as a function of the imbalance, is a -shaped curve for the Bank of America stock traded in NASDAQ and from the bottom left picture a -shaped curve for the Bank of America stock traded in NYSE. Similar pattern is observed also for the General Electric stock traded in NASDAQ and NYSE, see Figure 7. The -shaped curve is observed for General Motors and JP Morgan & Chase traded in both NASDAQ and NYSE, see Figure 8 and Figure 9. Indeed, we studied some other stocks as well in the WRDS database and empirical studies suggest that -shape curves and -shaped curves are universal for the correlation between the size changes at the best bid and ask for most stocks. It also holds that the correlation in general is negative but is far away from . It is curious why a typical relation of the correlation between the size changes at the best bid and ask and the imbalance of the best bid and ask can be represented by either a -shaped curve or a -shaped curve. It is also worth noting that sometimes we get different shaped curves for different exchanges (Figure 6, Figure 7) and sometimes we get the same shaped curves for different exchanges (Figure 8, Figure 9). That can probably be explained by the fact that some high frequency and algorithmic trading firms apply their trading strategies to a particular stock exchange only and the different trading strategies result in the different patterns of the best bid and ask dynamics we observed from the data. Figures 6, 7, 8, 9 also contain the information about the standard deviations of the size changes at the best bid and best ask queues on NASDAQ and NYSE. The general observation is that most of the time, the standard deviation increases as the imbalance increases at the best bid queues and decreases as the imbalance increases at the best ask queues. Note that best bid size increases as imbalance increases and best ask size decreases as imbalance increases. Hence, what we observed is that the standard deviations increases as the queue lengths increases. This is not surprising at all. But what’s interesting is that in many cases, it is not exactly monotone and we see a sudden increase of the standard deviation when the imbalance is small for the best bid and large for the best ask, that is, when the queue length is short. That suggests that when the queue length is short, that is when the queue is about to get deleted, or when there is a new queue created, the volatilities tend to be large. In general, the volatilities of the empirical data tend to be noisier than the correlations, which is either a -shaped or a -shaped curve. Nevertheless, it is quite often to observe the skewed -shaped curves. For example, in top middle and top right pictures in Figure 6, Figure 7, Figure 8 and Figure 9, we have the skewed -shaped curves. For the best bid queues, it is skewed towards the left and for the best ask queues, it is skewed towards the right. It is curious that for the stocks traded on NASDAQ, we have this universal skewed -shapes for the volatilities. But the data for the NYSE tend to be noisier and the pattern is not very clear. This once again indicates the very different natures of the level-1 limit order dynamics across different exchanges.

We summarize the statistics of the correlations in Table 5. As we can see, the correlation is almost always negative. In terms of the numbers, the strongest correlation is achieved by the Bank of America stock traded on NYSE with imbalance between and . The most negative correlation is achieved by JP Morgan traded on NYSE, which is , that is far away from . One interesting observation is that when the imbalance is between and , from Table 5, we can see that the correlation of the stock traded on NYSE is always more negative than the correlation of the same stock traded on NASDAQ222with the exception of JP Morgan when the imbalance is between 0.55 and 0.60. As we mentioned earlier, the fragmentation and discrepancy of the stock exchanges is well documented in the literature. For example, we can ask the question why the correlation of stocks traded on NYSE is more negative than that of NASDAQ.

3. A Reduced-Form Model

The simplest continuous time diffusion model to describe the dynamics of the level-1 limit order book is the correlated Brownian motions, where and are the queue lengths at the best bid and the best ask normalized by the median size of the queues, see e.g. Avellaneda et al. [2]:

| (3.1) | ||||

| (3.2) |

where and are two correlated standard Brownian motions with correlation .

We are interested in the probability of the price movement. The probability that the price moves up and down are given respectively by

| (3.3) |

where

| (3.4) |

Let the probability of price moving up be:

| (3.5) |

It is known that, see e.g. Avellaneda et al. [2]:

| (3.6) |

When there is no correlation, i.e., :

| (3.7) |

When the correlation is perfectly negative , i.e., :

| (3.8) |

From (3.6), we can see that the probability of price moving up can be written as a function depending only on the imbalance:

| (3.9) |

where . Moreover, is monotonically increasing in the imbalance .

Remark 1.

More generally, we can assume that the diffusion processes are correlated Brownian motions with constant drifts:

| (3.10) | ||||

| (3.11) |

Based on the results in Iyengar [11] and Metzler [14], we have

| (3.12) |

where

| (3.13) |

and , where is the modified Bessel function of the first kind and

In particular, when ,

| (3.14) |

In Avellaneda et al. [2], the authors fitted the empirical probability of mid-price moving up by the correlated Brownian motion model when the correlation is , that is, (3.8). From Figures 10-13 and Table 4-5 the empirical probability of mid-price moving up is indeed linearly dependent on the imbalance. However, as we have already seen in Figures 6, 7, 8, 9 that the correlation is negative, but far away from , and it also depends on the level of the imbalance. Therefore, a perfect negatively correlated Brownian motions model might not fit both the empirical probability and the empirical correlation. We will propose a non-parametric diffusion model that can fit the empirical correlation, empirical volatilities, and empirical probability of price movement simultaneously.

The correlated Brownian motion is simple yet still captures the phenomenon that the price movement is mainly driven by the imbalance at the best bid and ask level. We are interested to investigate further the relation of the dynamics of the volumes at the best bid and ask level and the imbalance. The assumption in the model (3.6) that the correlation and volatility of the volumes at the best bid and ask levels are constant might be oversimplified and not consistent with the real data. Indeed, the empirical studies we did in Section 2 suggests that the correlation of the movements of the volumes at the best bid and ask level is non-trivially dependent on the imbalance. Two universal shapes for the correlation as a function of the imbalance are the -shaped curve and -shaped curve. For a -shaped correlation function of the imbalance, the correlation is negative and it is close to zero when the imbalance is close to and and it is the most negative when the imbalance is close to . Similarly we also observe -shaped correlation curves. The correlations are consistently negative though far away from . We also observe that the volatilities of the volumes at the best bid and ask levels also depend non-trivially on the imbalance. The volatility is in general large when the imbalance is small or large and the volatility is small when the imbalance is moderate. The difference here is that instead of a symmetric -shaped or -shaped curve, we often get two skewed -shaped curves, depending on whether we consider the best bid or the best ask. Therefore, our goal is to improve the model (3.6) to allow the correlation and volatilities to be non-constant and depend on the level of the imbalance.

In a very loose analogy, in the literature of the pricing of derivative securities, it is well known that the stock price has the so-called leverage effect, that is, the volatility of a stock tends to increase when the stock price drops, which is one of the key reasons that people have used the CEV models and other local volatility models as an alternative to the Black-Scholes model in which the volatility is always constant.

We are interested to build up a model for the dynamics of the level-1 limit order books, that can capture the empirical evidence that we observed from the data.

Let us build a discrete model and find its diffusion approximation. Let be the queue lengths at the best bid and the best ask at time and be the imbalance. Let us assume that

-

•

The limit orders that arrive at the best bid is a simple point process with intensity at time ;

-

•

The market orders or cancellations that arrive at the best bid is a simple point process with intensity at time ;

-

•

The limit orders that arrive at the best ask is a simple point process with intensity at time ;

-

•

The market orders or cancellations that arrive at the best ask is a simple point process with intensity at time ;

-

•

There are simultaneous cancellations at the best ask and limit orders at the best bid that is a simple point process with intensity at time ;

-

•

There are simultaneous cancellations at the best bid and limit orders at the best ask that is a simple point process with intensity at time ;

The last two assumptions above are made due to the observation that the empirical correlation between the best bid and ask queues are always negative. Note that is the arrival rate for the idiosyncratic limit orders at the best bid, so the total arrival rate for the limit orders at the best bid is . Similarly, the total arrival rate for the limit orders at the best ask is . For , we assume that are continuous and bounded (there is singularity when and we assume analytic continuation of at the singularity). Finally, for simplicity, we assume that the order size has unit size . Note that all the following arguments work if we assume constant order sizes for different types of orders. Therefore, the dynamics at the best bid and ask are given by:

| (3.15) | ||||

Since empirically, we do not observe strong evidence for the drift effect, we assume the driftless condition:

| (3.16) |

so that and are driftless, in the sense that

where for any , is a martingale. For the high frequency trading, the number of orders is large and the trading frequency is high, so we can rescale time and space to get a diffusion approximation to the discrete model. Let us define the rescaled process for ,

| (3.17) |

The discrete model (3.15) describes the dynamics of the best bid and ask queues at the micro level, but may not be easy to work with when we are interested to compute the probability of mid-price movement. So, next, let us find a diffusion approximation to the discrete model (3.15).

Let us assume that

| (3.18) | ||||

where and are two standard Brownian motions with correlation at time . We assume that , are bounded and continuous from to , and is bounded and continuous333Note that can be singular, and are defined as the analytic continuation at the singular points . from to , so that there exists a unique solution to (3.18), see e.g. [16]. If in addition, we assume that are Lipschitz, then the solution is guaranteed to be strong, see e.g. [15].

Note that the discrete process and should both live in the first quadrant. But to avoid the well-definedness after the process hitting the boundary of the first quadrant, we make the processes well-defined on . Since our goal is to compute the probability of mid-price movement, which is about the first hitting time of the boundary of the first quadrant, the extension from the first quadrant to will not alter the results, and it is just for the sake of convenience.

Theorem 2.

Given that is the discrete model of the best bid and ask queues in (3.15), assume that for , are continuous and bounded functions and the driftless condition (3.16) holds. Also assume that . Then the rescaled process in (3.17) converges weakly in as to in (3.18), where is the space of càdlàg processes equipped with Skorohod topology. In addition, the diffusion and correlation coefficients are the explicit functions of the intensities :

The probability of mid-price movement for the diffusion model (3.18) can be computed in the closed-form as follows.

Theorem 3.

Remark 4.

What we are really interested to compute is the probability of mid-price movement for the discrete model, and this can be approximated by the probability of mid-price movement for the diffusion model which has closed-form formula, that is given in Theorem 3. For any , we have

as . Note that the approximation requires that and and this is still reasonable since the formula in Theorem 3 only depends on the ratio of and so we can rescale the initial condition.

Remark 5.

Remark 6.

When , we have and . And thus . By using the assumption 3.16, we can check that the probability of mid-price moving up satisfies (A.4) and thus this is the probability of mid-price movement for the reduced-form model. Indeed, for the original unscaled discrete model (3.15), satisfies the equation

| (3.21) |

for with boundary condition and . It is easy to see that . Indeed, this result is true for perfectly negatively correlated queues model-free. To see this, notice that and are perfectly negatively correlated martingales and we can write and , where is a martingale. Therefore, the probability that hits before does is the same as the probability that hits before . By optional stopping theorem for martingales, this probability can be easily computed as .

As we can see from Figures 10, 11, 12, 13, the empirical probability of mid-price moving up (dotted lines) is linearly dependent on the imbalance. Except the BAC at NASDAQ and the GE at NASDAQ, there is also a strong numerical evidence of the hidden liquidity, that is, the probability of moving up is bigger than zero when the imbalance is near zero and less than one when the imbalance is near one. To better fit the data, we introduce the hidden liquidity , so that the theoretical probability of mid-price moving up is for imbalance at zero and for imbalance at one444This is slightly different from the definition of hidden liquidity in Avellaneda et al. [2]. Our definition of can be interpreted as a probability, a free parameter that helps get closer to the empirical data in the least-square sense rather than a real liquidity as in Avellaneda et al. [2]. We choose this definition to keep the analytical tractability of the model and also our definition is simpler in the sense that we only need to bucket the data and discretize our analytical formula according to the imbalance level rather than the best bid and ask queue sizes as in [2]. That is, satisfies the boundary condition and . Following the proofs of Theorem 3, we get the following result (the proof will be given in Appendix A).

Theorem 7.

To fit the data, we use the empirical data for , and to plug into the formula (3.22) and obtain , the theoretical probability of mid-price moving up at imbalance level and then use the least square method

| (3.23) |

to find the best fitting hidden liquidity . The solid lines in Figures 10, 11, 12, 13 are the model predictions. Remarkably, the solid lines are almost linear in imbalance even though the correlation is a complicated function of imbalance and far away from being . Hence, we have built up a model with the empirical correlation and volatilities as the input that can produce an analytical formula for the price movement probability that can be used to fit to the empirical probability data

4. Conclusions

We did numerical studies of the drift effect, correlation and volatility of the best bid and ask queues and how they depend on the imbalance of the volumes at the best bid and ask queues from the level-1 limit order books data from the WRDS. We discovered that there is little evidence for the drift except when the imbalance is small or large. The correlation as a function of the imbalance exhibits universal behaviors, which is either a -shaped or a -shaped curve, and it is almost always negative though far away from . The volatility is much more noisy and in general lacks a clear pattern though very often exhibit skewed -shapes. All the empirical results are highly stock and also exchange dependent, which suggests that the dynamics of the limit order books are very sensitive to their particular stock and also exchanges. Based on our empirical discoveries, we built up a discrete model for the dynamics of the best bid and ask queues and showed that it can be approximated by a reduced-form diffusion model with functional dependence of the drift, correlation and volatility on the imbalance, which therefore generalizes the correlated Brownian motion model that is commonly used in the limit order books literature. Our reduced-form model still keeps analytical tractability, and it is self-consistent when it is fit to the data of both the empirical probability of mid-price movement and the empirical correlation/volatility.

Acknowledgments

The authors are very grateful to two anonymous referees and the editor whose suggestions have greatly improved the presentation and the quality of the paper. The authors would also like to thank Jean-Philippe Bouchaud, Yuanda Chen, Arash Fahim, Xuefeng Gao and Alec Kercheval for their invaluable comments. Lingjiong Zhu is partially supported by NSF Grant DMS-1613164.

Appendix A Proofs

Proof of Theorem 2.

Notice that are martingales with predictable quadratic variation , where is bounded, i.e. . For any , , we have

| (A.1) |

for some constant . By Burkholder-Davis-Gundy inequality, for any ,

| (A.2) |

for some constant . Therefore, by applying Kolmogorov’s tightness criterion, we can show that is tight.

The infinitesimal generator for the rescaled process is given by

where and is a twice continuously differentiable test function.

By using the driftless assumption (3.16), we get

As , , where

Also notice that by our assumption, the initial condition satisfies . The tightness gives the relative compactness of the sequence and and the convergence of infinitesimal generators gives convergence in distribution for finite fixed time point, which guarantees the weak convergence on , see e.g. Theorem 7.8(b) of Chapter 3 in Ethier and Kurtz [6]. Hence on . ∎

Proof of Theorem 3.

Recall that the price moves up is:

| (A.3) |

Then, satisfies the PDE:

| (A.4) |

with the boundary condition: and , where is the imbalance.

Assuming that is a function of so that , by the chain rule,

| (A.5) | |||

| (A.6) | |||

| (A.7) | |||

| (A.8) |

Hence, the PDE reduces to:

which can be further reduced to the ODE:

with the boundary condition and , which can be rewritten as

| (A.9) |

where

and . This is a first-order linear equation with solution

| (A.10) |

and hence

| (A.11) |

where are two constants to be determined. By using the boundary conditions and , we conclude that

| (A.12) |

∎

Appendix B Tables

| Imbalance | BAC b | BAC a | GE b | GE a | GM b | GM a | JPM b | JPM a |

|---|---|---|---|---|---|---|---|---|

| 0.0-0.1 | 0.349 | 0.499 | 0.367 | 0.508 | 0.640 | 0.462 | 0.628 | 0.496 |

| 0.1-0.2 | 0.449 | 0.519 | 0.461 | 0.503 | 0.508 | 0.488 | 0.580 | 0.487 |

| 0.2-0.3 | 0.458 | 0.542 | 0.439 | 0.513 | 0.480 | 0.517 | 0.498 | 0.507 |

| 0.3-0.4 | 0.472 | 0.556 | 0.478 | 0.536 | 0.482 | 0.532 | 0.450 | 0.542 |

| 0.4-0.5 | 0.503 | 0.537 | 0.507 | 0.539 | 0.508 | 0.531 | 0.472 | 0.529 |

| 0.5-0.6 | 0.533 | 0.508 | 0.529 | 0.518 | 0.532 | 0.510 | 0.514 | 0.448 |

| 0.6-0.7 | 0.540 | 0.488 | 0.537 | 0.490 | 0.530 | 0.489 | 0.518 | 0.477 |

| 0.7-0.8 | 0.540 | 0.467 | 0.528 | 0.469 | 0.514 | 0.471 | 0.527 | 0.514 |

| 0.8-0.9 | 0.522 | 0.479 | 0.523 | 0.472 | 0.494 | 0.498 | 0.516 | 0.527 |

| 0.9-1.0 | 0.486 | 0.310 | 0.496 | 0.378 | 0.463 | 0.643 | 0.508 | 0.696 |

| Imbalance | BAC b | BAC a | GE b | GE a | GM b | GM a | JPM b | JPM a |

|---|---|---|---|---|---|---|---|---|

| 0.0-0.1 | 0.561 | 0.540 | 0.586 | 0.596 | 0.730 | 0.598 | 0.723 | 0.602 |

| 0.1-0.2 | 0.524 | 0.531 | 0.502 | 0.552 | 0.557 | 0.506 | 0.532 | 0.531 |

| 0.2-0.3 | 0.514 | 0.529 | 0.490 | 0.531 | 0.502 | 0.497 | 0.491 | 0.512 |

| 0.3-0.4 | 0.518 | 0.541 | 0.505 | 0.522 | 0.494 | 0.497 | 0.480 | 0.511 |

| 0.4-0.5 | 0.517 | 0.553 | 0.518 | 0.529 | 0.485 | 0.486 | 0.492 | 0.507 |

| 0.5-0.6 | 0.539 | 0.511 | 0.539 | 0.518 | 0.501 | 0.491 | 0.510 | 0.494 |

| 0.6-0.7 | 0.551 | 0.506 | 0.528 | 0.513 | 0.496 | 0.496 | 0.499 | 0.485 |

| 0.7-0.8 | 0.534 | 0.516 | 0.541 | 0.503 | 0.498 | 0.503 | 0.506 | 0.491 |

| 0.8-0.9 | 0.518 | 0.535 | 0.553 | 0.512 | 0.510 | 0.550 | 0.527 | 0.539 |

| 0.9-1.0 | 0.554 | 0.582 | 0.575 | 0.551 | 0.586 | 0.718 | 0.598 | 0.742 |

| Imbalance | BAC(T) | BAC(N) | GE(T) | GE(N) | GM(T) | GM(N) | JPM(T) | JPM(N) |

|---|---|---|---|---|---|---|---|---|

| 0.00-0.05 | -0.03 | 0.00 | -0.05 | -0.09 | -0.09 | -0.07 | -0.14 | -0.11 |

| 0.05-0.10 | -0.12 | 0.02 | -0.08 | -0.10 | -0.11 | -0.18 | -0.13 | -0.20 |

| 0.10-0.15 | -0.09 | -0.02 | -0.09 | -0.10 | -0.14 | -0.25 | -0.17 | -0.29 |

| 0.15-0.20 | -0.09 | -0.06 | -0.13 | -0.18 | -0.15 | -0.21 | -0.17 | -0.29 |

| 0.20-0.25 | -0.07 | -0.09 | -0.10 | -0.16 | -0.16 | -0.31 | -0.21 | -0.34 |

| 0.25-0.30 | -0.05 | -0.13 | -0.09 | -0.17 | -0.17 | -0.30 | -0.22 | -0.34 |

| 0.30-0.35 | -0.04 | -0.13 | -0.07 | -0.19 | -0.19 | -0.28 | -0.24 | -0.32 |

| 0.35-0.40 | -0.04 | -0.12 | -0.06 | -0.19 | -0.18 | -0.28 | -0.23 | -0.34 |

| 0.40-0.45 | -0.04 | -0.15 | -0.09 | -0.21 | -0.20 | -0.29 | -0.24 | -0.33 |

| 0.45-0.50 | -0.05 | -0.15 | -0.07 | -0.22 | -0.20 | -0.28 | -0.25 | -0.33 |

| 0.50-0.55 | -0.04 | -0.12 | -0.06 | -0.20 | -0.20 | -0.27 | -0.25 | -0.34 |

| 0.55-0.60 | -0.04 | -0.12 | -0.07 | -0.20 | -0.21 | -0.28 | -0.27 | -0.26 |

| 0.60-0.65 | -0.05 | -0.12 | -0.09 | -0.17 | -0.20 | -0.29 | -0.24 | -0.29 |

| 0.65-0.70 | -0.05 | -0.11 | -0.08 | -0.18 | -0.19 | -0.28 | -0.24 | -0.28 |

| 0.70-0.75 | -0.04 | -0.10 | -0.07 | -0.15 | -0.19 | -0.28 | -0.22 | -0.30 |

| 0.75-0.80 | -0.07 | -0.09 | -0.11 | -0.16 | -0.16 | -0.27 | -0.20 | -0.29 |

| 0.80-0.85 | -0.11 | -0.07 | -0.12 | -0.16 | -0.16 | -0.25 | -0.22 | -0.26 |

| 0.85-0.90 | -0.12 | -0.04 | -0.10 | -0.15 | -0.12 | -0.22 | -0.20 | -0.18 |

| 0.90-0.95 | -0.10 | -0.03 | -0.09 | -0.07 | -0.08 | -0.19 | -0.16 | -0.17 |

| 0.95-1.00 | -0.06 | 0.00 | -0.04 | -0.10 | -0.03 | -0.08 | -0.06 | -0.06 |

| Imbalance | BAC(E) | BAC(P) | GE(E) | GE(P) | GM(E) | GM(P) | JPM(E) | JPM(P) |

|---|---|---|---|---|---|---|---|---|

| 0.00-0.05 | 0.044 | 0.072 | 0.053 | 0.104 | 0.102 | 0.176 | 0.077 | 0.158 |

| 0.05-0.10 | 0.139 | 0.131 | 0.127 | 0.144 | 0.197 | 0.211 | 0.137 | 0.196 |

| 0.10-0.15 | 0.136 | 0.181 | 0.168 | 0.186 | 0.245 | 0.247 | 0.225 | 0.235 |

| 0.15-0.20 | 0.159 | 0.224 | 0.186 | 0.229 | 0.267 | 0.285 | 0.254 | 0.275 |

| 0.20-0.25 | 0.215 | 0.263 | 0.221 | 0.273 | 0.306 | 0.322 | 0.285 | 0.315 |

| 0.25-0.30 | 0.270 | 0.301 | 0.231 | 0.319 | 0.342 | 0.359 | 0.336 | 0.356 |

| 0.30-0.35 | 0.307 | 0.337 | 0.308 | 0.364 | 0.367 | 0.394 | 0.378 | 0.396 |

| 0.35-0.40 | 0.351 | 0.374 | 0.364 | 0.409 | 0.412 | 0.429 | 0.406 | 0.436 |

| 0.40-0.45 | 0.426 | 0.410 | 0.397 | 0.454 | 0.463 | 0.463 | 0.460 | 0.475 |

| 0.45-0.50 | 0.441 | 0.447 | 0.441 | 0.498 | 0.482 | 0.497 | 0.484 | 0.514 |

| 0.50-0.55 | 0.492 | 0.484 | 0.504 | 0.542 | 0.503 | 0.531 | 0.540 | 0.553 |

| 0.55-0.60 | 0.539 | 0.523 | 0.545 | 0.586 | 0.533 | 0.566 | 0.591 | 0.591 |

| 0.60-0.65 | 0.628 | 0.562 | 0.600 | 0.631 | 0.570 | 0.602 | 0.607 | 0.630 |

| 0.65-0.70 | 0.658 | 0.603 | 0.653 | 0.676 | 0.604 | 0.639 | 0.639 | 0.668 |

| 0.70-0.75 | 0.704 | 0.646 | 0.669 | 0.722 | 0.644 | 0.677 | 0.645 | 0.706 |

| 0.75-0.80 | 0.737 | 0.693 | 0.749 | 0.766 | 0.679 | 0.716 | 0.668 | 0.744 |

| 0.80-0.85 | 0.783 | 0.750 | 0.762 | 0.811 | 0.698 | 0.754 | 0.722 | 0.780 |

| 0.85-0.90 | 0.844 | 0.825 | 0.799 | 0.855 | 0.740 | 0.791 | 0.791 | 0.815 |

| 0.90-0.95 | 0.885 | 0.912 | 0.846 | 0.896 | 0.810 | 0.825 | 0.799 | 0.848 |

| 0.95-1.00 | 0.960 | 1.000 | 0.930 | 0.933 | 0.902 | 0.856 | 0.918 | 0.878 |

| Imbalance | BAC(E) | BAC(P) | GE(E) | GE(P) | GM(E) | GM(P) | JPM(E) | JPM(P) |

|---|---|---|---|---|---|---|---|---|

| 0.00-0.05 | 0.128 | 0.191 | 0.138 | 0.251 | 0.157 | 0.217 | 0.125 | 0.179 |

| 0.05-0.10 | 0.194 | 0.216 | 0.237 | 0.271 | 0.221 | 0.244 | 0.174 | 0.209 |

| 0.10-0.15 | 0.249 | 0.243 | 0.332 | 0.292 | 0.277 | 0.272 | 0.219 | 0.241 |

| 0.15-0.20 | 0.249 | 0.272 | 0.346 | 0.315 | 0.310 | 0.302 | 0.272 | 0.275 |

| 0.20-0.25 | 0.276 | 0.303 | 0.347 | 0.340 | 0.341 | 0.333 | 0.313 | 0.310 |

| 0.25-0.30 | 0.335 | 0.338 | 0.367 | 0.367 | 0.373 | 0.365 | 0.348 | 0.347 |

| 0.30-0.35 | 0.377 | 0.375 | 0.384 | 0.396 | 0.393 | 0.398 | 0.428 | 0.385 |

| 0.35-0.40 | 0.405 | 0.415 | 0.395 | 0.428 | 0.422 | 0.432 | 0.411 | 0.425 |

| 0.40-0.45 | 0.420 | 0.458 | 0.435 | 0.461 | 0.443 | 0.466 | 0.439 | 0.465 |

| 0.45-0.50 | 0.442 | 0.502 | 0.435 | 0.495 | 0.454 | 0.501 | 0.474 | 0.506 |

| 0.50-0.55 | 0.468 | 0.546 | 0.476 | 0.529 | 0.516 | 0.536 | 0.522 | 0.545 |

| 0.55-0.60 | 0.490 | 0.588 | 0.520 | 0.562 | 0.554 | 0.570 | 0.569 | 0.584 |

| 0.60-0.65 | 0.530 | 0.628 | 0.540 | 0.593 | 0.572 | 0.603 | 0.608 | 0.623 |

| 0.65-0.70 | 0.590 | 0.665 | 0.580 | 0.622 | 0.601 | 0.636 | 0.637 | 0.661 |

| 0.70-0.75 | 0.648 | 0.700 | 0.603 | 0.649 | 0.638 | 0.667 | 0.664 | 0.696 |

| 0.75-0.80 | 0.649 | 0.731 | 0.619 | 0.675 | 0.659 | 0.698 | 0.701 | 0.730 |

| 0.80-0.85 | 0.723 | 0.760 | 0.647 | 0.699 | 0.701 | 0.727 | 0.730 | 0.763 |

| 0.85-0.90 | 0.793 | 0.787 | 0.660 | 0.723 | 0.729 | 0.756 | 0.771 | 0.794 |

| 0.90-0.95 | 0.832 | 0.811 | 0.763 | 0.745 | 0.785 | 0.783 | 0.812 | 0.823 |

| 0.95-1.00 | 0.924 | 0.833 | 0.860 | 0.766 | 0.856 | 0.808 | 0.875 | 0.849 |

References

- [1] Frédéric Abergel and Aymen Jedidi. A mathematical approach to order book modeling. International Journal of Theoretical and Applied Finance, 16(05):1350025, 2013.

- [2] Marco Avellaneda, Josh Reed, and Sasha Stoikov. Forecasting prices from level-I quotes in the presence of hidden liquidity. Algorithmic Finance, 1(1), 2011.

- [3] Rama Cont and Adrien De Larrard. Order book dynamics in liquid markets: limit theorems and diffusion approximations. Available at SSRN 1757861, 2012.

- [4] Rama Cont and Adrien de Larrard. Price dynamics in a Markovian limit order market. SIAM Journal on Financial Mathematics, 4(1):1–25, 2013.

- [5] Rama Cont, Sasha Stoikov, and Rishi Talreja. A stochastic model for order book dynamics. Operations Research, 58(3):549–563, 2010.

- [6] S. N. Ethier and T. G. Kurtz. Markov Processes: Characterization and Convergence. Wiley-Interscience, New Jersey, second edition, 2005.

- [7] A. Garèche, G. Disdier, J. Kockelkoren, and J.-P. Bouchaud. Fokker-Planck description for the queue dynamics of large tick stocks. Phys. Rev. E, 88:032809, Sep 2013.

- [8] Xin Guo, Zhao Ruan, and Lingjiong Zhu. Dynamics of order positions and related queues in a limit order book. arXiv preprint arXiv:1505.04810, 2015.

- [9] He Huang and Alec N. Kercheval. A generalized birth-death stochastic model for high-frequency order book dynamics. Quantitative Finance, 12(4):547–557, 2012.

- [10] Weibing Huang, Charles-Albert Lehalle, and Mathieu Rosenbaum. Simulating and analyzing order book data: The queue-reactive model. Journal of the American Statistical Association, 110:107–122, 2015.

- [11] Satish Iyengar. Hitting lines with two-dimensional Brownian motion. SIAM Journal on Applied Mathematics, 45(6):983–989, 1985.

- [12] Charles-Albert Lehalle and Sophie Laruelle. Market Microstructure in Practice. World Scientific, Singapore, first edition, 2013.

- [13] Jonathan Macey and David Swensen. The cure for stock-market fragmentation: More exchanges. The Wall Street Journal, May 31 2015.

- [14] Adam Metzler. On the first passage problem for correlated Brownian motion. Statistics & Probability Letters, 80(5-6):277–284, 2010.

- [15] Bernt Øksendal. Stochastic differential equations. Universitext. Springer-Verlag, Berlin, sixth edition, 2003. An introduction with applications.

- [16] D. W. Stroock and S. R. S. Varadhan. Multidimensional diffusion processes. Springer-Verlag, Berlin, 1979.