Asymptotic Theory for Estimating the Singular Vectors and

Values of a Partially-observed Low Rank Matrix with Noise

Juhee Cho, Donggyu Kim, and Karl Rohe111This research is supported by NSF grant DMS-1309998 and ARO grant W911NF-15-1-0423.

University of Wisconsin-Madison

Abstract: Matrix completion algorithms recover a low rank matrix from a small fraction of the entries, each entry contaminated with additive errors. In practice, the singular vectors and singular values of the low rank matrix play a pivotal role for statistical analyses and inferences. This paper proposes estimators of these quantities and studies their asymptotic behavior. Under the setting where the dimensions of the matrix increase to infinity and the probability of observing each entry is identical, Theorem 1 gives the rate of convergence for the estimated singular vectors; Theorem 3 gives a multivariate central limit theorem for the estimated singular values. Even though the estimators use only a partially observed matrix, they achieve the same rates of convergence as the fully observed case. These estimators combine to form a consistent estimator of the full low rank matrix that is computed with a non-iterative algorithm. In the cases studied in this paper, this estimator achieves the minimax lower bound in Koltchinskii et al. (2011a). The numerical experiments corroborate our theoretical results.

Key words and phrases: Matrix completion, low rank matrices, singular value decomposition, matrix estimation

1 Introduction

The matrix completion problem arises in several different machine learning and engineering applications, ranging from collaborative filtering (Rennie and Srebro (2005)), to computer vision (Weinberger and Saul (2006)), to positioning (Montanari and Oh (2010)), and to recommender systems (Bennett and Lanning (2007)). The literature has established a sizable body of algorithmic research (Rennie and Srebro (2005); Keshavan et al. (2009); Cai et al. (2010); Mazumder et al. (2010); Hastie et al. (2014); Cho et al. (2015)) and theoretical results (Fazel (2002); Srebro et al. (2004); Candès and Recht (2009); Candès and Plan (2010); Keshavan et al. (2010); Recht (2011); Gross (2011); Negahban et al. (2011); Koltchinskii et al. (2011a); Rohde et al. (2011); Koltchinskii et al. (2011b); Candès and Plan (2011); Negahban and Wainwright (2012); Cai and Zhou (2013); Davenport et al. (2014); Chatterjee (2014)). This extant literature is primarily focused on estimating the unobserved entries of the matrix. In several of these previous estimation techniques, the algorithms first estimate the singular vectors and singular values of the low rank matrix. Also, based upon classical multivariate statistics, these singular vectors and singular values can serve various types of statistical analyses and inferences. For example, the overarching aim in the Netflix problem was to predict the unobserved film ratings and the previous algorithms and theories served this purpose. However, if one wishes to interpret the resulting model predictions, then the estimated singular vectors and singular values can provide insights on (i) the main latent factors of film preferences and (ii) their relative strengths, respectively. In the Netflix example,

“The first factor has on one side lowbrow comedies and horror movies, aimed at a male or adolescent audience (Half Baked, Freddy vs. Jason), while the other side contains drama or comedy with serious undertones and strong female leads (Sophie’s Choice, Moonstruck). The second factor has independent, critically acclaimed, quirky films (Punch-Drunk Love, I Heart Huckabees) on one side, and mainstream formulaic films (Armageddon, Runaway Bride) on the other side.” (Koren et al. (2009))

This inference is based upon the leading singular vectors of the estimated matrix. To the best of our knowledge, no previous research has studied the statistical properties of the estimated singular vectors and singular values.

This paper proposes estimators of the singular vectors and singular values of the low rank matrix as well as an estimator of the low rank matrix itself. First, Lemma 1 studies the singular vectors and singular values of a partially observed matrix that simply substitutes zeros for the unobserved entries; the resulting estimators are biased. The proposed estimators adjust for this bias. Theorem 1 finds the convergence rate for the bias-adjusted singular vector estimators and Theorem 3 gives a multivariate central limit theorem for the bias-adjusted singular value estimators. Despite the fact that the proposed estimators are built upon a partially observed matrix, they converge at the same rate as the standard estimators built from a fully observed matrix up to a constant factor which depends on the probability of observing each entry. Combining the proposed singular vector and value estimators, Section 4.2 gives a one-step consistent estimator of the low rank matrix which does not iterate over several singular value decompositions or eigenvalue decompositions. The mean squared error of this estimator achieves the minimax lower bound in Theorems 5-7 (Koltchinskii et al. (2011a)).

The rest of this paper is organized as follows. Section 2 describes the model setup. Section 3 shows that the singular vectors and singular values of a partially observed matrix are biased and suggests a bias-adjusted alternative. Section 4.1 finds (1) the convergence rates of the estimated singular vectors and (2) the asymptotic distribution of the estimated singular values. Section 4.2 proposes and studies a one-step consistent estimator of the full matrix. Section 5 corroborates the theoretical findings with numerical experiments. Finally, Section 6 provides the proofs of our main theoretical results. The proofs of the other results are collected in the Appendix.

2 Model setup

The underlying matrix that we wish to estimate is an matrix with rank . By singular value decomposition (SVD),

| (1) |

for orthonormal matrices containing the left and right singular vectors, and a diagonal matrix containing the singular values. is corrupted by noise , where the entries of are i.i.d. sub-Gaussian random variables with mean zero and variance . Let be such that if the -th entry of is observed and otherwise. The entries of are i.i.d. Bernoulli() and independent of the entries of . Thus, the total number of observed entries in is a Binomial() random variable. We observe and the partially observed matrix , where

for and . Throughout the paper, it is presumed that . Moreover, the entries of are bounded in absolute value by a constant .

Remark 1.

Depending on the case, the noise can be related to the measurement system so that assuming that there exist errors for unobserved entries does not make sense. Hence, assume a hierarchical model as follows;

In this setting, the results obtained in this paper would still hold although it may require more techniques or minor changes in the proof. For simplicity of the paper, we only focus on the original setting.

3 Estimation of singular values and vectors of

The vast majority of previous estimators of have been initialized with , in effect imputing the missing values with zero. In this section, we study the properties of singular vectors and values of . This suggests alternative estimators of the singular vectors and values of .

3.1 Properties of singular values and vectors of

Define

Then, the eigenvectors of and are the same as the right and left singular vectors of , respectively, and the squared root of eigenvalues of are the same as the singular values of . The following lemma shows that and are biased estimators of and , respectively.

Lemma 1.

Under the model setup in Section 2, we have

| (2) |

and similarly,

| (3) |

where and are and identity matrices, respectively.

The proof of this lemma is in Appendix A.1. The right-hand side of (2) contains terms beyond and they make the singular vectors and singular values of biased estimators of the singular vectors and values of . While the bias coming from is manageable222This term does not change the singular vectors of ; it merely increases each singular value by ., the bias coming from is not. The same applies to in (3).

To get rid of the terms producing unmanageable biases, we define and and their eigenvectors and eigenvalues as follows,

| (4) | ||||

where

The following proposition shows that and adjust the bias.

Proposition 1.

Proposition 1 shows that the top eigenvectors of and are the same as the right and left singular vectors of , respectively. Also, the top eigenvalues of are easily adjusted to match the singular values of as follows,

3.2 Estimators of singular values and vectors of

The results in Proposition 1 suggest plug-in estimators using the leading eigenvectors and eigenvalues of and the leading eigenvectors of as estimators of , , and , respectively. However, since is an unknown parameter in practice, the proposed estimators use instead of the proportion of observed entries in , , which is defined as

| (5) |

Using , define and as

| (6) |

By eigendecomposition,

| (7) |

where , , , , , and . Then, estimate the left and right singular vectors, and , of by and , respectively. Also, estimate the singular values, , of by

| (8) |

where

For any , let the -th left singular vector of be denoted by , the -th right singular vector of by , and the top -th singular value of by for . Then, Algorithm 1 summarizes the steps to compute the proposed estimators of the singular values and vectors of .

4 Asymptotic theory

4.1 Convergence rate of the estimated singular vectors and asymptotic distribution of the estimated singular values

Let be a -dimensional vector and a matrix. Then, the -norm is defined as follows,

The spectral norm is a square root of the largest eigenvalue of ,

The squared Frobenius norm is defined by , the trace of . We denote by and generic constants that are free of , , and , and different from appearance to appearance.

To measure how close the proposed estimator is to (or, to ), we introduce a classical notion of distance between subspaces. Let denote a column space spanned by and by . Then, to measure the dissimilarity between and , consider the following loss function

where is a diagonal matrix of singular values (canonical angles) of with orthogonal projections and of and , respectively. Here . The canonical angles generalize the notion of angles between lines and are often used to define the distance between subspaces. If the columns of and are singular vectors, and have projections and , respectively, and . Proposition 2.2 in Vu and Lei (2013) relates this subspace distance to the Frobenius distance

| (9) |

where and denotes the Stiefel manifold of orthonormal matrices. In other words, the distance between two subspaces corresponds to the minimal distance between their orthonormal bases.

Assumption 1.

-

(1)

, where for a constant ;

-

(2)

there exists a constant such that , where ;

-

(3)

for a constant free of , , and .

Remark 2.

To motivate Assumption 1 (1), suppose that a non-vanishing proportion of entries of contains non-vanishing signals (i.e. for some constant ) and that the rank of is fixed. Then,

for some constant . Because the squared Frobenius norm is also the sum of the squared singular values of , the order of the singular values of should be (see also Fan et al. (2013)). Assumption 1(1) may seem uncommon in the matrix completion literature, but consider the widely-used assumption (II.2) in Candès and Plan (2010),

for and a constant , which prevents spiky singular vectors. Under the model setup in Section 2 where the entries of are bounded in absolute value by a constant , this implies Assumption 1(1).

The following theorem shows the convergence of to and to .

Theorem 1.

The proof of this theorem is in Section 6.1.

Remark 3.

Remark 4.

Despite the fact that is built on a partially observed matrix , Theorem 1 gives the convergence rate which is the standard convergence rate for eigenvectors (Anderson et al. (1958)). The effect of the partial observations appears in the denominator of the right-hand side of (10) as . A similar discussion applies to in (11).

The next theorem shows the asymptotic distribution of centered around .

Theorem 2.

The proof of this theorem is in Section 6.2.

Remark 5.

Remark 6.

Theorem 2 shows that the convergence rate of is . Considering Assumption 1(1), it is an optimal rate. However, since the results are based on partially observed entries, the asymptotic variance, , increases with the rate . For example, when we have a fully-observed matrix, simply becomes which is a lower bound for .

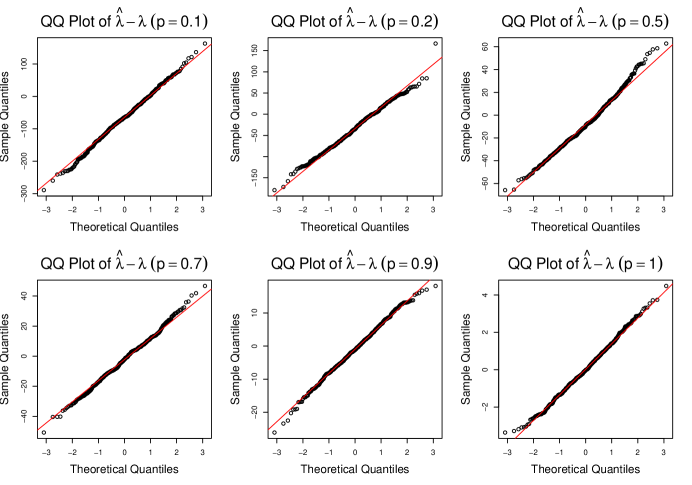

One of the main purposes of this paper is to investigate asymptotic behaviors of the estimators of the singular values of . An application of the proof of Theorem 2 and the delta method provides a multivariate central limit theorem for .

Theorem 3.

Remark 7.

As in case of Theorem 2 (see Remark 5), as long as and , the asymptotic normality result in Theorem 3 will hold. Note that Theorems 2 and 3 require an additional condition, , to the condition required for Theorem 1, . Under the setting where is a constant, this additional condition implies that has to go to zero. The rationale behind this is as follows. In Theorems 2 and 3, we find the limiting distribution on the singular values of from a matrix , while the total number of observations is . That is, the size of our parameter space is and the total amount of information we can use to find asymptotic properties on the parameters is . Since our observations are even noisy, we need an enough number of observations to achieve our goal. When , we can make the approximation errors in the singular values of negligible and find the limiting distribution on the singular values of .

Remark 8.

4.2 A consistent estimator of

Suppose that for all . Theorem 1 and (9) imply that and can estimate and up to constant factors and , respectively. Let be

| (13) |

Then, becomes a consistent estimator of . However, since is an unknown parameter in practice, we employ as an estimator of ;

| (14) |

where contains indices of the observed entries, , and for any denotes the projection of onto ,

Hence, the proposed estimator of is

| (15) |

Remark 9.

In the following we show that is a consistent estimator of under certain conditions. The steps to compute using from Algorithm 1 are summarized in Algorithm 2.

Assumption 2.

-

(1)

;

-

(2)

for all .

Remark 10.

When the rank is 1, it is more straightforward to understand Assumption 2(1). Assuming that , it means that

That is, the probability that picks a different sign than the true sign goes to zero with the dimensionality. Given the asymptotic properties of our estimators , and , this is not an unreasonable assumption to make.

Theorem 4.

The proof of this theorem is in Section 6.3.

Remark 11.

As in case of Theorem 1 (see Remark 3), as long as , the convergence rates in Theorem 4 will hold. If we let so that represents the number of observed entries in the population sense, this condition implies that . Therefore, for to be consistent, the number of observed entries should increase at a faster rate than . This is a comparable result to Theorem 1 in Candès and Plan (2010).

Remark 12.

Remark 13.

Theorem 4 shows that is bounded by for some constant . Under the setting where the rank of is fixed as in this paper, this is matched to the minimax lower bound in Theorems 5-7 (Koltchinskii et al. (2011a)). The previous estimators that obtain the minimax rate are computed via semidefinite programs that require iterating over several SVDs. However, the proposed estimator is a non-iterative algorithm.

Remark 14.

Chatterjee (2014) established the minimax error rate for estimators of a general class of noisy incomplete matrices which extend beyond low rank matrix completion. In the regime studied herein, the convergence rate of our estimator of is faster than the convergence rate in Theorem 2.1 (Chatterjee (2014)). This is likely because we consider a smaller class of matrices, where the singular values of a low rank matrix have the divergence rate (Assumption 1(1)). Remark 2 justifies this assumption in the setting of low rank matrix completion.

Throughout this paper, we have assumed that the rank, , of is known. However, it is an unknown parameter and needs to be estimated. The following lemma proposes an estimator of and shows its consistency.

Lemma 2.

Let such that and , for example, for any . Also, let where is defined in (7). Then, for any given , we have

The proof of this lemma is in Appendix A.5.

Remark 15.

Remark 16.

As long as satisfies , consistency of in Lemma 2 will hold. However, in the finite sample case, if the noise level is larger than , it can be difficult to observe a singular-value gap and determine using the scree plot of the singular values of .

5 Numerical experiments

5.1 Simulations

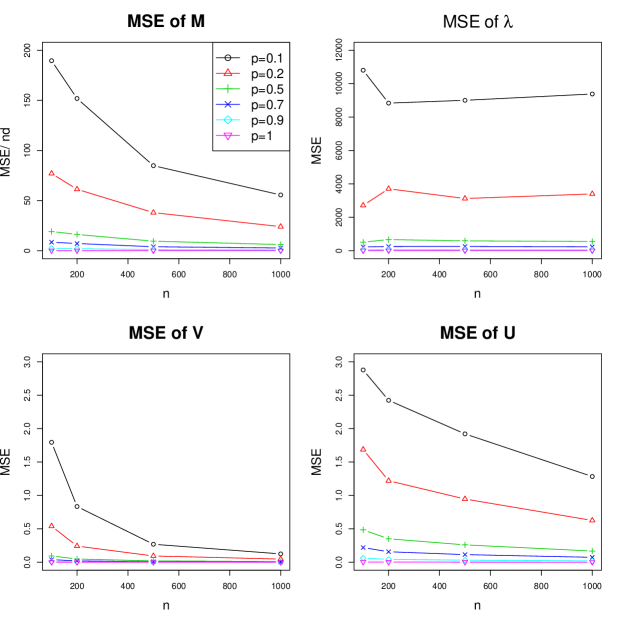

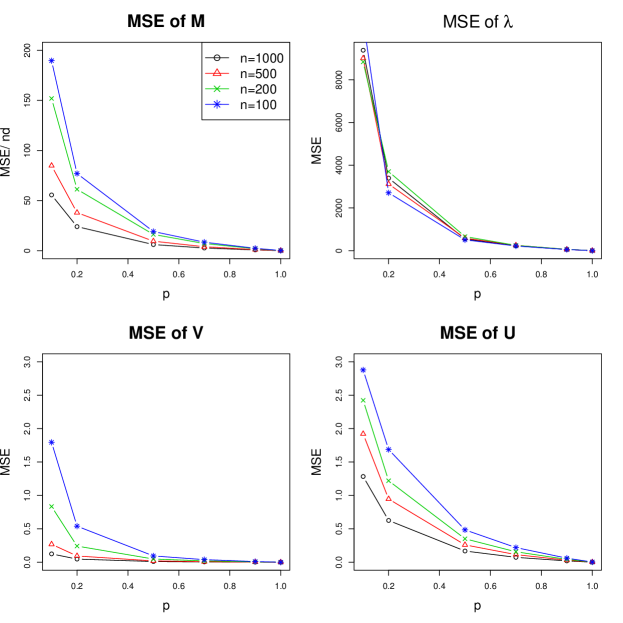

This section studies the performance of the proposed estimators using several values of the dimension and the probability .

To simulate , generate , to contain i.i.d. Uniform random variables and define

Each entry of is observed with probability and unobserved with probability . The observed entries of are corrupted by noise as defined in Section 2, where are i.i.d. . The dimension varies from 100 to 1000 and from 0.1 to 1, while . Each simulation was repeated 500 times and the errors were averaged.

Figures 1 and 2 summarize the resulting mean squared errors calculated by , , , and , when and increase along the -axis, respectively. The MSE for decreases more rapidly than the MSE for and both MSEs decrease when increases; this is consistent with the results in Theorem 1. The MSE of decreases with the increase of and . The MSE of stays stable over the changes of since it is measured on instead of (see Theorem 3), but decreases with the increase of .

5.2 A data example

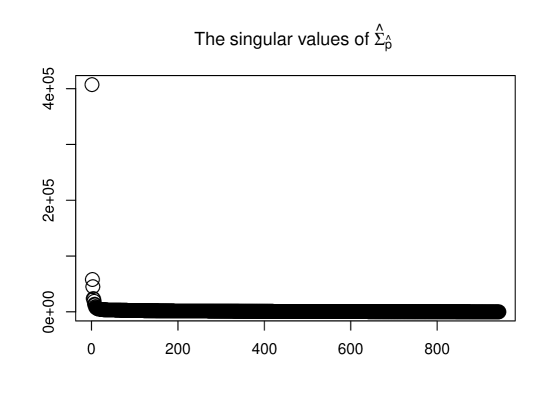

To illustrate the proposed estimation methods, this section analyzes the MovieLens 100k data (GroupLens (2015)). The data set consists of 100,000 ratings from 943 users and 1682 movies and each user has rated at least 20 movies. Taking this partially observed data matrix as , we computed as in (6) and plotted the scree plot of the singular values of to determine . Figure 4 shows the result.

Since there exists a singular value gap between the 3rd and 4th singular values, we chose . Then, we computed the estimators of the singular vectors and values and the estimator of the full low rank matrix as illustrated in Algorithms 1 and 2.

The estimated singular vectors help us understand what the main factors of movie preferences are. Table 1 shows lists of movies that characterize the top 3 singular vectors (factors of movie preferences). Particularly, it presents 5 movies that correspond to the largest values in each singular vector and 5 movies that correspond to the smallest values.

| 1st singular vector |

|

|

||||

|---|---|---|---|---|---|---|

|

|

|||||

| 2nd singular vector |

|

|

||||

|

|

|||||

| 3rd singular vector |

|

|

||||

|

|

The 1st factor has well-known and top-rated movies on one side and unknown and poorly-rated movies on the other side. The 2nd factor has box-office hit movies in 1990’s on one side and memorable classic movies in 1940’s-1960’s on the other side. The 3rd factor has action and thriller movies on one side and quieter and drama movies on the other side.

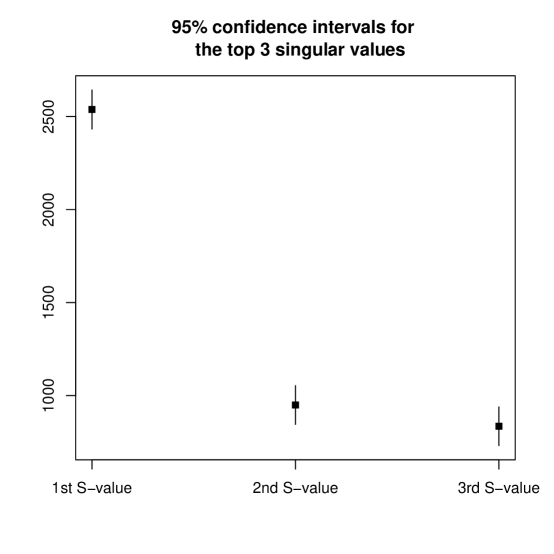

The estimated singular values help us see how influential the main factors of movie preferences are. Particularly, Figure 5 shows the estimated singular values and their confidence intervals. For the standard deviation used in the confidence intervals, we used from (12) in Theorem 4. Computing requires information on the values of the parameters , and , but we replaced these with the estimated values , and . From Figure 5, we observe that all 3 factors of movie preferences are significant.

To find the RMSE of our estimator of the full low rank matrix, , we used 5 training and 5 test data sets from 5-fold cross validation which is publicly provided in GroupLens (2015). The RMSE was computed by

where contains indices of observed entries that belong to the test set, for a matrix denotes the projection of onto , and denotes the cardinality of . The average of the resulting RMSEs was 1.656.

6 Proofs

6.1 Proofs for Theorem 1

The proof of the following proposition and lemmas are in Appendix A.2.

Proposition 2.

Lemma 3.

Lemma 4.

Under the model setup in Section 2 and Assumption 1, for any given , there exists a large constant such that

| (18) |

with probability at least , where and are defined in (6) and (4), respectively. Similarly, for any given , there exists a large constant such that

with probability at least , where and are defined in (6) and (4), respectively.

Lemma 5.

Proof of Theorem 1.

By triangle inequality and Proposition 2, we have

| (20) | |||

| (21) | |||

| (22) |

Now, consider . Let

where , and

where . Then, by Weyl’s theorem (Li (1998a)), Lemma 3, and Lemma 4, we have for large constants , and ,

Thus, for large and ,

| (29) | |||||

where is an indicator function of an event , the first inequality holds by the fact that and Davis-Kahan theorem (Theorem 3.1 in Li (1998b)), and the last inequality is due to Lemma 5.

6.2 Proofs for Theorem 2

The proof of the following propositions are in Appendix A.3.

Proposition 3.

Proposition 4.

Proof of Theorem 2.

We have

First, consider the term . We have

| (30) | |||||

| (33) | |||||

| (34) |

By (9), there is such that

where is the -th column of . Then, the term is

| (36) | |||||

| (38) | |||||

| (39) |

where the last equality holds by the fact that

| (40) | |||

| (41) | |||

| (42) | |||

| (43) | |||

| (44) | |||

| (45) |

where the last equality is due to (9), (29), and (46) below; by the application of Weyl’s theorem (Li (1998a)) and Lemma 3, we can show

| (46) |

The term is

| (47) | |||||

| (48) | |||||

| (49) | |||||

| (50) | |||||

| (51) | |||||

| (52) |

where the second inequality is due to Hölder’s inequality and the last equality holds by the fact that

The term in (30) is

| (54) | |||||

| (58) | |||||

| (60) | |||||

| (61) |

where the third equality is due to (47), (40), Proposition 3, and the fact that

| (62) |

by CLT and Delta method. From (36), (47), and (54), we have

| (63) | |||

| (64) |

Second, the term is

| (65) | |||||

| (66) | |||||

| (67) | |||||

| (68) |

where the third equality is due to Proposition 4 and (62), and the last equality holds by the fact that there is by (9) such that

where is the -th column of , and that

where the second inequality can be derived similarly to (40), the second equality holds similarly to (47), and the last equality is due to (29) and (46).

6.3 Proofs for Theorem 4

The proof of the following Proposition is in Appendix A.4.

Proposition 5.

Appendix A Appendix

A.1 Proofs for Lemma 1

A.2 Proofs for Section 6.1

Proof of Proposition 2.

We only show the result (16), since the other result can be shown similarly.

Let

where . Note that . By Weyl’s theorem (Li (1998a)) and Lemma 3, we have for large constants ,

Thus, for large ,

| (A.3) | |||

| (A.4) | |||

| (A.5) | |||

| (A.6) | |||

| (A.7) | |||

| (A.8) |

where is an indicator function of an event , the first inequality is due to the fact that and Davis-Kahan theorem (Theorem 3.1 in Li (1998b)), and the last inequality holds by Lemma 6 below. ∎

Lemma 6.

Proof of Lemma 6.

We only show the result (A.9) because the other result holds similarly.

From (A.2), (4), Proposition 1, and triangle inequality, we have

| (A.10) | |||

| (A.11) | |||

| (A.12) | |||

| (A.13) | |||

| (A.14) | |||

| (A.15) | |||

| (A.16) | |||

| (A.17) | |||

| (A.18) | |||

| (A.19) |

We examine the convergence rates of the above terms, -.

First, consider the term (A) in (A.10). Then, we have

| (A.20) | |||

| (A.21) | |||

| (A.22) | |||

| (A.23) | |||

| (A.24) | |||

| (A.25) | |||

| (A.26) | |||

| (A.27) | |||

| (A.28) | |||

| (A.29) |

Similarly to (A.20), we can show that the expected values of the terms , and squared are bounded by .

Second, consider the term (C) in (A.10). Then, we have

| (A.30) | |||

| (A.31) | |||

| (A.32) | |||

| (A.33) | |||

| (A.34) | |||

| (A.35) | |||

| (A.36) |

where the last inequality holds due to Cauchy-Schwarz inequality.

Lastly, for the term (E) in (A.10),

| (A.37) | |||

| (A.38) | |||

| (A.39) | |||

| (A.40) | |||

| (A.41) | |||

| (A.42) |

where last inequality holds due to Cauchy-Schwarz inequality.

Lemma 7.

Proof of Lemma 7.

Let be such that

Then,

, and for all and . Also, we have

| (A.43) | |||

| (A.44) |

Thus, by Proposition 1 in Koltchinskii et al. (2011a), we have

with probability at least .

In a similar way together with Proposition 2 in Koltchinskii et al. (2011a), we can show that with probability at least .

∎

Proof of Lemma 3.

We only show the result (17) because the other result holds similarly.

From (A.2), Proposition 1 and triangle inequality, we have

| (A.45) | |||

| (A.46) | |||

| (A.47) | |||

| (A.48) | |||

| (A.49) | |||

| (A.50) | |||

| (A.51) |

Because of similarity, we provide arguments only for and .

Consider the term in (A.45). First, we have by Lemma 7

| (A.52) |

with probability at least . Also, we have with probability at least ,

| (A.53) | |||

| (A.54) | |||

| (A.55) | |||

| (A.56) | |||

| (A.57) | |||

| (A.58) | |||

| (A.59) |

where the second inequality holds by (A.60) below. Take for some large constant . Then, by Bernstein’s inequality,

| (A.60) | |||

| (A.61) | |||

| (A.62) | |||

| (A.63) |

| (A.64) |

with probability at least . Similarly, we can show that and are bounded by with probability at least .

Consider the term in (A.45). We have

where and hence are centered sub-Gaussian random variables under the model setup in Section 2. Then, we have for any and for all , and ,

Take for some large constant and . Then, by Markov’s inequality,

| (A.65) | |||||

| (A.66) | |||||

| (A.67) | |||||

| (A.68) | |||||

| (A.69) |

Similarly,

| (A.70) |

By (A.65) and (A.70), with probability at least ,

| (A.71) |

Similarly, we can show that is bounded by with probability at least .

Proof of Lemma 4.

We only show the result (18) because the other result holds similarly.

By triangle inequality, we have

| (A.72) | |||

| (A.73) | |||

| (A.74) |

We will look at the terms in (A.72) one by one.

By Bernstein’s inequality, we have for large constant ,

| (A.75) | |||

| (A.76) | |||

| (A.77) | |||

| (A.78) |

Take for some large constant . Then, since , are independent centered sub-exponential random variables, we have by Proposition 5.16 in Vershynin (2010),

| (A.79) | |||

| (A.80) | |||

| (A.81) | |||

| (A.82) | |||

| (A.83) |

Also, note that

| (A.84) | |||||

| (A.85) |

Proof of Lemma 5.

We only show the result (19) because the other result holds similarly.

We have

| (A.87) | |||

| (A.88) | |||

| (A.89) | |||

| (A.90) | |||

| (A.91) | |||

| (A.92) | |||

| (A.93) | |||

| (A.94) |

where the fourth inequality holds by Hölder’s inequality and the fifth inequality is due to the fact that

| (A.95) | |||

| (A.96) | |||

| (A.97) | |||

| (A.98) | |||

| (A.99) | |||

| (A.100) |

∎

A.3 Proofs for Section 6.2

Lemma 8.

Proof of Lemma 8.

We have

| (A.101) | |||

| (A.102) | |||

| (A.103) | |||

| (A.104) | |||

| (A.105) | |||

| (A.106) | |||

| (A.107) | |||

| (A.108) | |||

| (A.109) | |||

| (A.110) | |||

| (A.111) | |||

| (A.112) | |||

| (A.113) | |||

| (A.114) | |||

| (A.115) | |||

| (A.116) | |||

| (A.117) | |||

| (A.118) |

where is a solution to and the fourth equality holds by (4) and (A.2). Below, we examine the six terms - one by one.

The term in (A.101) is

| (A.119) | |||||

| (A.122) | |||||

| (A.124) | |||||

Note that the two terms in (A.119) are centered and uncorrelated with each other. So, the variance is

| (A.126) | |||||

| (A.128) | |||||

| (A.130) | |||||

| (A.131) |

where the first inequality is due to Jensen’s inequality. This shows that the term is . Similarly, we can show that the terms and are .

The term (c) in (A.101) is

Then, its variance is

where the last inequality is due to Assumption 1(1) and the fact that

| (A.132) | |||

| (A.133) | |||

| (A.134) | |||

| (A.135) | |||

| (A.136) | |||

| (A.137) | |||

| (A.138) | |||

| (A.139) |

The term (d) in (A.101) is

Then, its variance is

where the last inequality is due to Assumption 1(1) and the fact that

| (A.140) | |||

| (A.141) | |||

| (A.142) | |||

| (A.143) | |||

| (A.144) |

Proof of Proposition 3.

By Cramèr-Wold device, it is enough to show that for any given ,

where . When , this can be directly showed by CLT. Thus, we only consider the case where .

We have

| (A.154) | |||

| (A.155) | |||

| (A.156) | |||

| (A.157) | |||

| (A.158) | |||

| (A.159) | |||

| (A.160) | |||

| (A.161) | |||

| (A.162) | |||

| (A.163) | |||

| (A.164) |

where the second equality holds by Lemma 8. Since the terms and are centered and not correlated with each other under the model setup in Section 2, we have

| (A.165) | |||

| (A.166) | |||

| (A.167) | |||

| (A.168) | |||

| (A.169) | |||

| (A.170) | |||

| (A.171) | |||

| (A.172) | |||

| (A.173) | |||

| (A.174) | |||

| (A.175) |

where the third equality is due to (A.132), (A.140) and Assumption 1(1). Note that

| (A.176) |

Thus, Liapunov’s condition is satisfied with because we have

| (A.177) | |||

| (A.178) | |||

| (A.179) | |||

| (A.180) | |||

| (A.181) | |||

| (A.182) | |||

| (A.183) | |||

| (A.184) | |||

| (A.185) | |||

| (A.186) | |||

| (A.187) | |||

| (A.188) |

where the first inequality holds by Assumption 1(1), and the last two lines are due to Cauchy-Schwarz inequality.

Proof of Proposition 4.

Similarly to the proof of (A.101), we have

where is a solution to , and the third equality is due to the fact that . We will show that - are .

Since the first five terms, -, are centered, we only need to check their variances to find their rates. The variances of the terms and are , which can be shown similarly to the proof of (A.126). The variance of the term is

where the inequality is due to Jensen’s inequality. Similarly, the variance of the term is .

A.4 Proofs for Section 6.3

A.5 Proofs for Lemma 2

References

- Anderson et al. (1958) T.W. Anderson. An introduction to multivariate statistical analysis, volume 2. Wiley New York, 1958.

- Bennett and Lanning (2007) J. Bennett and S. Lanning. The netflix prize. In Proceedings of KDD cup and workshop, volume 2007, page 35, 2007.

- Cai et al. (2010) J.-F. Cai, E. J. Candès, and Z. Shen. A singular value thresholding algorithm for matrix completion. SIAM Journal on Optimization, 20(4):1956–1982, 2010.

- Cai and Zhou (2013) T. T. Cai and W.-X. Zhou. Matrix completion via max-norm constrained optimization. arXiv preprint arXiv:1303.0341, 2013.

- Candès and Plan (2010) E. J. Candès and Y. Plan. Matrix completion with noise. Proceedings of the IEEE, 98(6):925–936, 2010.

- Candès and Plan (2011) E. J. Candès and Y. Plan. Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. Information Theory, IEEE Transactions on, 57(4):2342–2359, 2011.

- Candès and Recht (2009) E. J. Candès and B. Recht. Exact matrix completion via convex optimization. Foundations of Computational mathematics, 9(6):717–772, 2009.

- Chatterjee (2014) S. Chatterjee. Matrix estimation by universal singular value thresholding. The Annals of Statistics, 43(1):177–214, 2014.

- Cho et al. (2015) J. Cho, D. Kim, and K. Rohe. Intelligent initialization and adaptive thresholding for iterative matrix completion; some statistical and algorithmic theory for adaptive-impute, 2015.

- Davenport et al. (2014) M. A. Davenport, Y. Plan, E. van den Berg, and M. Wootters. 1-bit matrix completion. Information and Inference, 3(3):189–223, 2014.

- Fan et al. (2013) J. Fan, Y. Liao, and M. Mincheva. Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(4):603–680, 2013.

- Fazel (2002) M. Fazel. Matrix rank minimization with applications. PhD thesis, PhD thesis, Stanford University, 2002.

- GroupLens (2015) GroupLens (2015). Movielens100k @MISC. http://grouplens.org/datasets/movielens/.

- Gross (2011) D. Gross. Recovering low-rank matrices from few coefficients in any basis. Information Theory, IEEE Transactions on, 57(3):1548–1566, 2011.

- Hastie et al. (2014) T. Hastie, R. Mazumder, J. Lee, and R. Zadeh. Matrix completion and low-rank svd via fast alternating least squares. arXiv preprint arXiv:1410.2596, 2014.

- Keshavan et al. (2009) R. Keshavan, A. Montanari, and S. Oh. Matrix completion from noisy entries. In Advances in Neural Information Processing Systems, pages 952–960, 2009.

- Keshavan et al. (2010) R. H. Keshavan, A. Montanari, and S. Oh. Matrix completion from a few entries. Information Theory, IEEE Transactions on, 56(6):2980–2998, 2010.

- Koltchinskii et al. (2011a) V. Koltchinskii, K. Lounici, A. B. Tsybakov, et al. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. The Annals of Statistics, 39(5):2302–2329, 2011a.

- Koltchinskii et al. (2011b) V. Koltchinskii et al. Von neumann entropy penalization and low-rank matrix estimation. The Annals of Statistics, 39(6):2936–2973, 2011b.

- Koren et al. (2009) Y. Koren, R. Bell, and C. Volinsky. Matrix factorization techniques for recommender systems. Computer, 42(8):30–37, 2009.

- Li (1998a) R.-C. Li. Relative perturbation theory: I. eigenvalue and singular value variations. SIAM Journal on Matrix Analysis and Applications, 19(4):956–982, 1998a.

- Li (1998b) R.-C. Li. Relative perturbation theory: II. eigenspace and singular subspace variations. SIAM Journal on Matrix Analysis and Applications, 20(2):471–492, 1998b.

- Mazumder et al. (2010) R. Mazumder, T. Hastie, and R. Tibshirani. Spectral regularization algorithms for learning large incomplete matrices. The Journal of Machine Learning Research, 11:2287–2322, 2010.

- Montanari and Oh (2010) A. Montanari and S. Oh. On positioning via distributed matrix completion. In Sensor Array and Multichannel Signal Processing Workshop (SAM), 2010 IEEE, pages 197–200. IEEE, 2010.

- Negahban and Wainwright (2012) S. Negahban and M. J. Wainwright. Restricted strong convexity and weighted matrix completion: Optimal bounds with noise. The Journal of Machine Learning Research, 13(1):1665–1697, 2012.

- Negahban et al. (2011) S. Negahban, M. J. Wainwright, et al. Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, 39(2):1069–1097, 2011.

- Recht (2011) B. Recht. A simpler approach to matrix completion. The Journal of Machine Learning Research, 12:3413–3430, 2011.

- Rennie and Srebro (2005) J. D. Rennie and N. Srebro. Fast maximum margin matrix factorization for collaborative prediction. In Proceedings of the 22nd international conference on Machine learning, pages 713–719. ACM, 2005.

- Rohde et al. (2011) A. Rohde, A. B. Tsybakov, et al. Estimation of high-dimensional low-rank matrices. The Annals of Statistics, 39(2):887–930, 2011.

- Srebro et al. (2004) N. Srebro, J. Rennie, and T. S. Jaakkola. Maximum-margin matrix factorization. In Advances in neural information processing systems, pages 1329–1336, 2004.

- Vershynin (2010) R. Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- Vu and Lei (2013) V. Q. Vu and J. Lei. Minimax sparse principal subspace estimation in high dimensions. The Annals of Statistics, 41(6):2905–2947, 2013.

- Weinberger and Saul (2006) K. Q. Weinberger and L. K. Saul. Unsupervised learning of image manifolds by semidefinite programming. International Journal of Computer Vision, 70(1):77–90, 2006.

Department of Statistics, University of Wisconsin, Madison, WI 53706, U.S.A E-mail: chojuhee@stat.wisc.edu

Department of Statistics, University of Wisconsin, Madison, WI 53706, U.S.A E-mail: kimd@stat.wisc.edu

Department of Statistics, University of Wisconsin, Madison, WI 53706, U.S.A E-mail: karlrohe@stat.wisc.edu