Duality and stationary distributions of the

“Immediate Exchange Model” and its generalizations.

Abstract

We prove that the “Immediate Exchange Model” of [5] has a discrete dual, where the duality functions are

natural polynomials assocaited to the Gamma distribution with shape parameter and are exactly

those connecting the and the models in [1], [9].

As a consequence, we recover invariance of products of Gamma distributions with shape parameter 2, and obtain ergodicity results.

Next we show similar properties for a more general model, where the exchange fraction is distributed, and product measures with

marginals are invariant.

We also show that the discrete dual model is itself self-dual and has a similar continuous model as its scaling limit.

We show that the self-duality is linked with an underlying symmetry, similar to the one found before for

the and related processes.

1 Introduction

Kinetic wealth exchange models (KWEMs) constitute a popular class of econophysical models in which agents exchange their wealth according to some stochastic rules, always preserving the total amount of wealth in the economy. The aim is to understand some important properties of the dynamics of wealth distribution, such as wealth concentration, stationary distributions and time dependent correlation functions. For a recent review about KWEMs, we refer to [3].

The apparently economically strong assumption of wealth conservation - which also rules out the possibility of (endogenous) growth - is justifiable by choosing the appropriate time scale (or time unit) for the economy.

An interesting feature of KWEMs is their similarity with another family of models, known as KMP [1]. Introduced in [7], KMP models are microscopic models of heat conduction and are meant to provide a microscopic foundation of the Fourier law; in those models the exchanged quantity represents energy.

As shown in [1], duality is a powerful tool to study the properties of KMP models. Thanks to duality it is possible to investigate invariant measures, ergodic results, and important macroscopic properties such as hydrodynamic limits, the propagation of local equilibrium, and the local equilibrium of boundary-driven non-equilibrium states.

In [4], the authors show that duality can also be fruitfully applied to kinetic wealth exchange models, obtaining relevant information about the stationary distributions of a model with saving propensities.

In this paper we aim to extend the use of duality techniques in the field of KWEMs, by focusing our attention on a recent model, the so-called “Immediate Exchange Model”.

The model has been first proposed in [5], where it is studied via simulations, and it has been later analytically explored in [6]. In that model, upon exchange, each agent gives a fraction of his/her wealth to the other. In [6] it is proved that, if this fraction is a uniformly distributed random variable with support , then the exchange process is characterized by an invariant measure, which can be expressed as the product of distributions.

It is now worth noticing that an invariant measure which is a product of Gammas also occur in the redistribution models presented in [1]. In these models duality is characterized by duality polynomials that are naturally associated with the Gamma distribution and it is shown that these polynomials are also the duality functions linking a discrete particle system, the symmetric inclusion process , with a diffusion process, the Brownian energy process .

It is therefore natural to conjecture that these polynomials also occur as duality functions in the Immediate Exchange Model of [5], relating this model to a simpler discrete dual model.

In this paper we show that this is indeed the case, and we generalize the Immediate Exchange Model to the case in which the random fraction of wealth the agents exchange is distributed. In this more general setting, the invariant measure shows to be a product of distributions. As in [4], using duality we are able to directly infer basic properties of the time-dependent expected wealth, together with an ergodic result.

The rest of our paper is organized as follows: in Section 2 we describe the Immediate Exchange Model when the economy is just made up of two agents and prove duality with a discrete two-agent model. In Section 3 we extend the model to the case of many agents and we give some relevant consequences of duality. In Section 4 a further generalization is proposed, by assuming -distributed exchanged fractions of wealth; also for this generalized model we obtain duality with a discrete model and stationary product measures which are Gamma with shape parameter . In Section 5 we study various properties of the discrete dual process, which is an interesting model in itself. We characterize its reversible product measures and prove that in an appropriate scaling limit it scales to a simple variation of the original continuum model. Finally, in section 6 we show self-duality of the discrete model for the general case via a Lie algebraic approach, where we actually obtain the full symmetry of the discrete model, and, as a further consequence, of the continuous model, too. Self-duality then follows by acting with an appropriate symmetry on the so-called cheap duality function obtained from the reversible product measure [2].

2 The Immediate Exchange model with two agents and its dual

2.1 Definition of the model

We start by considering a toy economy with just two agents, as given in [5] and [6]. More complex models can be built by addition of two-agent generators along the edges of a graph. Most properties such as duality and self-duality transfer immediately from the two-agent model to the many agent models.

More formally, we write , with . With we indicate the total wealth in the economy.

Then the dynamics of two agents is described as follows, starting from an initial state ,

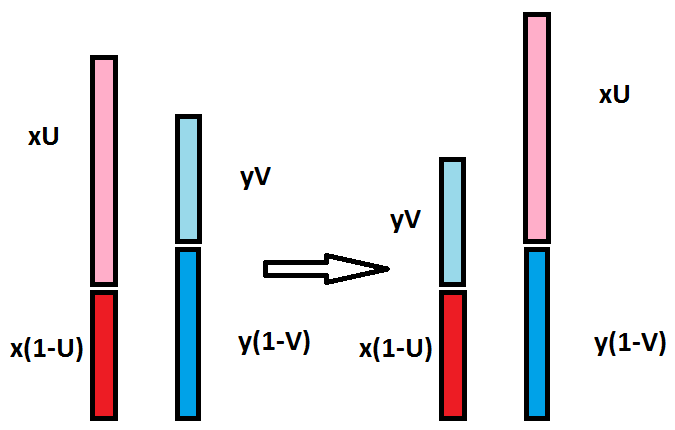

after an exponential waiting time (with mean one), an exchange of wealth occurs, whereby the wealth configuration is updated towards , with

| (1) |

where and are two i.i.d. random variables. This gives a continuous-time Markov jump process for which the total wealth is conserved.

The infinitesimal generator of this exchange process is defined on bounded continuous functions via

| (2) | |||||

Notice that can be rewritten as , where is the discrete-time Markov transition operator

and is the identity.

We denote to be the initial wealth configuration of the two agents, and indicates the wealth of the two agents at time .

2.2 Duality for the two-agent model

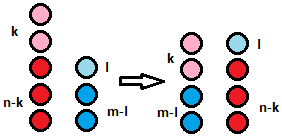

We will now first define a discrete wealth distribution model, i.e., where wealth can only be a nonnegative integer quantity. See the figure for the continuous model and its discrete dual. This model will be related to the original one via a duality relation.

Hence, in the discrete model the couple is replaced by a couple , where denotes the set of non-negative integers (including zero).

On this couple we define a continuous-time Markov process with generator

| (3) |

In this process, when initiated at , for a given with , the wealth configuration changes from to

at rate .

We denote this discrete state space continuous-time Markov process by , with .

We will then show that the processes and are related via duality. To introduce this, we need some further notation.

Define, for , the polynomial

| (4) |

and

| (5) |

The polynomials are naturally associated to the distribution with shape parameter and scale parameter , i.e.

by

for all .

With a slight abuse of notation, we will denote by the product measure with marginals

.

We are now ready to state the first main result.

THEOREM 2.1.

The processes and are each others dual with duality function given by

(5).

More precisely, for all , and for

all , we have

| (6) |

where and are the expectations in the path-space measures started from and respectively.

PROOF.

To prove (6) it is sufficient to show the same relation at the level of the generators. In other words, we have to show that

| (7) |

for all and , and where works on , and on .

We compute

Now we have

| (8) |

Therefore, we indeed find that

| (9) | |||||

As a consequence of duality, and thanks to the relation between the duality functions and the measure , we obtain relevant information about the invariant measures. Let us denote by the set of probability measures on with finite moments of all order and which are such that their finite moments determine the probability measure uniquely. I.e., two measures in with identical moments are equal. We say that such a measure satisfies the “finite moments condition”. Similarly for a probability measure on we say that it satisfies the “finite moments condition” if it has finite moments of all order and which are such that these finite moments determine the probability measure uniquely. This is e.g. assured by the Carleman’s moment growth condition. We will focus from now on only probability measures in this set .

THEOREM 2.2.

A probability measure is invariant if and only if its -transform

is harmonic for the dual process, i.e., if and only if

for all . In particular the product measures are invariant for the process .

PROOF. To have invariance of , for all , it is sufficient to have

| (10) |

Combining this with duality and Fubini’s theorem we obtain

As a result, we find that is invariant if and only if

To show the invariance of the measures, just notice that

and recall that in the process the sum is conserved.

Another consequence of duality is the ergodicity of the process . i.e., starting from any initial condition the process converges to a unique stationary distribution determined by the conserved sum . Indeed, the dual process starting from is an irreducible continuous-time Markov chain on the finite set and therefore converges to a unique stationary distribution denoted by , given by

| (11) |

where

| (12) |

For all we can therefore observe that

| (13) | |||||

It then follows from an easy computation using (11) that

| (14) |

where is given by (12) i.e., the limit in the r.h.s. of (13) only depends on . On the other hand, in the process we know that is conserved. Therefore, the conditional measure obtained by conditioning the stationary product measure on the sum being equal to is an invariant measure concentrating on the set . This measure is exactly the distribution of , with being . If we combine this fact with (13), we obtain the following ergodic theorem and complete characterization of the set of invariant measures satisfying the finite moment condition.

THEOREM 2.3.

-

a)

The process is ergodic, i.e., converges in distribution to , with and .

-

b)

The set of invariant measures contained in is given by the distributions of the form where is an arbitrary distribution on satisfying the finite moments condition and .

3 Generalization to many agents

Consider now an economy populated by many agents.

Let us assume that the economy can be represented as a graph , where each vertex represents an agent.

Consider now an irreducible symmetric random walk kernel on , i.e., such that , and

for all there exists with .

In this setting, the wealth configuration of the economy is an element of the set . For (from now on simply ), we denote with the wealth of the agent , that is of vertex .

We then define the generator of the model via

| (15) |

with

where

Accordingly, the dual process has state space and the elements of this state space are denoted by (from now on just ), where is the number of “dual units” at vertex . A configuration is called finite if is finite.

The generator of the dual process is then

| (16) |

with

where

Now, for and , define

| (17) |

The relation between these duality polynomials and the product measure is

| (18) |

with

the number of dual particles.

In the many agents economy model, the duality relation between both processes is then given by the following theorem. Its proof is direct from the two agents case, because the generator is a sum of two agents generators.

THEOREM 3.1.

Let be a finite configuration. For all and for all , we have

| (19) |

As a consequence, the product measures are invariant.

Notice that when is finite, the product measures can never be ergodic because the total wealth is conserved. However, for infinite , we have ergodicity under an additional condition. Let us denote by the probability to go from the finite configuration to the finite configuration in time , in the dual process with generator (15). Assume that

| (20) |

for all . As an example we have and symmetric nearest neighbor random walk.

PROPOSITION 3.1.

Let be infinite and let be such that (20) holds. Then the product measure is ergodic

PROOF. Abbreviate . Because ergodicity is implied by mixing, it suffices to show that

| (21) |

because linear combinations of the polynomials are dense in . To prove (21) denote if the support of and are disjoint, i.e., if there are no vertices which contain both particles from and . If then under the measure , the polynomials and are independent. Because of (20) it then follows, using duality and conservation of the total number of particles in the dual process:

Notice that, for a single dual particle, that is to say when , we have

In the dual process, the motion of single dual particle is a continuous-time random walk

jumping with rate from to .

If we denote by the

time transition probability of this walk, then duality with a single dual particle implies the following

“random walk” spread of the expected wealth at time .

PROPOSITION 3.2.

In the model with generator (15), for all and we have

4 Generalized immediate exchange model

Consider the update rule (2.1) and assume that and are now independent and distributed (the original model is then recovered for ). In other words, we consider the generator

| (22) |

where

is the probability density of two independent distributed random variables.

As before, the generator can be rewritten as , where is the identity and the discrete Markov transition operator

In this generalized setting, the polynomials which we need for duality are now given by

| (23) |

and

| (24) |

These polynomials are associated to the distribution with shape parameter ,

via

| (25) |

As before, with a slight abuse of notation we also denote the product measure with marginals .

The same computation as the one following (7) now yields that for a given with , the dual process will jump from towards , at rate

| (26) |

where the factorials are to be interpreted as , when is non-integer. Notice that as before in (8) we have that the rates sum up to one

| (27) |

This follows via rewriting

with

and recognizing the probability mass function of the Beta binomial distribution with parameters , given by

as a consequence one has

We can then state the generalized duality result, and its consequences, as in theorem 2.1. The dual process when initiated at is once more an irreducible continuous-time Markov chain on the finite set which converges to unique stationary distribution which we denote by denote and is given by

| (28) |

where

| (29) |

Notice now that we have the analogue of (14), i.e., if we the product measure conditioned on then

| (30) |

is only a function of . As a consequence, we obtain the following result in the generalized model.

THEOREM 4.1.

- 1.

-

2.

As a consequence, the product measure is invariant.

-

3.

Moreover, starting from any initial state , the process converges in distribution to where is -distributed, and .

-

4.

The invariant measures with finite moments are of the form , with is -distributed.

We can then build the analogue of this model for many agents associated to the vertices of a graph , as in equations (15) and (16). First notice that for a single dual particle, when , we get

Just as before, the motion of single dual particle in the dual process is a continuous-time random walk, jumping with rate from to . If we denote by the time transition probability of this walk, we then have the following result.

PROPOSITION 4.1.

In the model with generator (15), for all , we have, for all

5 Properties of the discrete dual process

The discrete dual process is a redistribution model of independent interest. It is a discrete redistribution model of the same type as the original continuous model in the spirit of the KMP process and its analogues of [1], where also a similar discrete process is the dual of the original continuous redistribution model. It is therefore useful to understand better the discrete dual process and its connection to the original process.

5.1 Reversible measures

Define the discrete Gamma distribution with shape parameter and scale parameter as the probability measure on with probability mass function

| (31) |

where is the normalizing factor. We first recall that the dual process has generator

| (32) |

where the rates are given by (26). It is important to notice here that this generator can be rewritten as follows

| (33) |

where is Beta binomial distributed with parameters and independent Beta binomial with parameters , and is expectation w.r.t. these variables.

PROPOSITION 5.1.

For all , the product probability measures with marginals are reversible for the process with generator (32).

PROOF. The reversibility of for the generator follows from a standard detailed balance computation. Indeed, fix two configurations and with ; now, for any and such that and , it trivially follows that and and , . In other words, for each redistribution of according to , we can find a ”reverse” redistribution of according to . Furthermore, these two redistributions are indeed reversible, as one may see by explicit computation, combining (26) and (31) that

which implies detailed balance and thus reversibility.

5.2 Scaling limit

The fact that the rescaled Beta Binomial converges to the Beta distribution (by the law of large numbers) provides a connection between the discrete dual process and the continuous process. The continuous process arises as a limit of the discrete dual process where the number of initial “coins” is suitably rescaled to infinity. This is expressed in the following result.

THEOREM 5.1.

PROOF. Define a number . Because convergence of generators on a core implies convergence of the processes, it suffices to show that for smooth

| (34) |

where , is given by (32), and by (22). Consider Beta binomial with parameters , and independent Beta binomial with parameters . By the law of large numbers it follows that

with , being independent distributed. Therefore, by smoothness of and dominated convergence, as we have

which shows (34).

6 Self duality and symmetry of the dual process

In this section we show self-duality with the self-duality polynomials which are naturally associated to the reversible discrete Gamma distributions. More precisely, we define the following discrete polynomials:

| (35) |

where negative factorials are defined to be infinite. These polynomials are naturally connected to the discrete reversible Gamma distribution via

| (36) |

with . Next we have the associated polynomial in two variables:

| (37) |

Notice that in the case , divided by , and in the limit , these discrete polymials converge to the duality polynomials (24). We recall that the dual process has a generator of the form

where the discrete transition operator

is indeed a Markov transition operator because, as we showed before,

To prove self-duality of the process with generator (32), we show that it commutes with a raising operator , from which we can generate the self-duality function via the strategy described in [2], namely by acting with on a cheap self-duality function coming from the reversible product measure.

In order to proceed with this, we introduce the raising operators [9],

| (38) |

For a function of two discrete variables, we denote , resp. the operator defined in (38) working on the first (resp. second) variable. Similarly we have the lowering and diagonal operators

| (39) |

Together, the generate a discrete (left) representation of ; i.e. they satisfy the commutation relations

| (40) |

where denotes the commutator. We will show in this subsection that the generator defined in (32) has symmetry and that the self-duality follows as a consequence, in the spirit of [9], [1]. We start by noticing that by reversibility of the measure , the function

is a “cheap” self-duality function [9], [2]. Furthermore, we remark that the claimed self-duality polynomials can be obtained via

where the operator is working on the , variables. Therefore, in order to prove that self-duality holds with the claimed polynomials (35), (37), it suffices to prove that commutes with the generator. Indeed, then from the general theory developed in [9], see also [2], it follows that , which arises from the action of a symmetry (an operator commuting with the generator) on a self-duality function, is again a self-duality function.

THEOREM 6.1.

The generator in (32) and the operator commute, i.e., for all we have

| (41) |

REMARK 6.1 (Hypergeometric Functions).

We briefly recall some definitions and properties about hypergeometric functions we will need in the proof of Theorem 6.1. On a suitable subdomain of , the hypergeometric function is defined via the following series expansion

Note that for all and ,

and

Moreover, as a particular case of Gauss’s summation theorem ([8], Theorem 2), we can state that

Some useful formulas are listed below:

PROOF. Let us prove that for all functions and

| (42) |

By straightforward computations and substitutions, if we adopt the notation

the l.h.s. rewrites ()

while the r.h.s

Let us introduce another shortcut:

As it is enough to show the identity only for the functions in the form

we can recast (42) as follows:

Since

we can further simplify

Now, by noting that

and by using the shortcuts

and similarly for and , we can continue with

| (43) | ||||

Note that, as in Remark 6.1, we can rewrite these quantities , etc., in terms of hypergeometric functions as follows

and

Therefore, the expression

simplifies to

| (44) |

By some standard manipulations of hypergeometric functions, the expression

reduces to

In conclusion, if we go back and plug the latter expression into (44), we can rewrite the l.h.s. in (43) as

By simply replacing by , by etc. and exchanging the sign in the latter expression, one simply obtains the explicit form of the r.h.s. in (43), which indeed proves identity (42).

We extend now the commutation of the generator with to full symmetry of both the discrete and the continuous model. For this we need some additional notation. Denoting the operators working on functions

| (45) | |||||

| (46) | |||||

| (47) |

we have that the algebra generated by forms a (right) representation of , i.e., satisfy the commutation relations (40) with opposite sign. Moreover, this continuous right representation is linked with the discrete left representation used before via the duality polynomials (23), i.e.,

| (48) |

where works on , and on (see e.g. [2] for the proof).

We now first formulate a simple lemma, showing that is the adjoint of in .

LEMMA 6.1.

PROOF. Let be functions with compact support, then we compute

We are now ready to prove the full symmetry of both the original continuous process and the discrete dual process. To explain this, we denote the coproduct

which is defined on the generators as and extended to the algebra as a homomorphism. We then say that the process with generator has full symmetry if it commutes with every element of the form , . This in turn follows if it holds for the generators , by the bilinearity of the commutator.

THEOREM 6.2.

PROOF. We start with the discrete process. Because the sum of the wealths is conserved, trivially commutes with . We showed in (41) that it commutes with . To show that it commutes with we use lemma 6.1 and the fact that is self-adjoint in by the reversibility of .

We then turn to the continuous model, using (48). We show the commutation with , the other cases are similar. We consider , the duality polynomial defined in (24), (25), and abbreviate it simply by , where in what follows we tacitly understand that operators of the form are working on and of the form on . In this notation, remark that operators working on different variables always commute (e.g. commutes with , etc.). We can then proceed as follows, using duality which reads .

On the other hand, via (48)

where in the third equality we used the commutation of with . Combination of these computations then gives indeed

on the functions , and then by standard arguments on all in .

Acknowledgement

We thank Gioia Carinci, Pasquale Cirillo and Wioletta Ruszel for useful discussions and comments.

References

- [1] G. Carinci, C. Giardinà, C. Giberti, F. Redig (2013) Duality for stochastic models of transport. Journal of Statistical Physics 152, 657-697.

- [2] G. Carinci, C. Giardinà, C. Giberti, F. Redig Dualities in population genetics: A fresh look with new dualities, Stochastic Processes and their Applications 125 (3), 941-969.

- [3] B.K. Chakrabarti, A. Chakraborti, S.R. Chakravarty, A. Chatterjee (2013). Econophysics of Income and Wealth Distributions. Cambridge University Press, Cambridge.

- [4] P. Cirillo, F. Redig, W. Ruszel (2014). Duality and stationary distributions of wealth distribution models. Journal of Physics A 47, 085203.

- [5] E. Heinsalu, M. Patriarca (2014). Kinetic models of immediate exchange. European Physical Journal B 87: 170.

- [6] G. Katriel (2014). The Immediate Exchange model: an analytical investigation. Preprint at http://arxiv.org/abs/1409.6646.

- [7] C. Kipnis, C. Marchioro, E. Presutti (1982). Heat flow in an exactly solvable model. Journal of Statistical Physics 27, 65-74.

- [8] R. Koekoek, Hypergeometric Functions. Lecture notes available at http://homepage.tudelft.nl/11r49/documents/wi4006/hyper.pdf.

- [9] C. Giardinà, J. Kurchan, F. Redig, K. Vafayi, Duality and hidden symmetries in interacting particle systems, Journal of Statistical Physics 135 (1), 25-55.

- [10] C. Giardinà, F. Redig, K. Vafayi, Correlation inequalities for interacting particle systems with duality, Journal of Statistical Physics 141 (2), 242-263.