Strong convergence of the symmetrized Milstein scheme for some CEV-like SDEs

Abstract

In this paper we study the rate of convergence of a symmetrized version of the Milstein scheme applied to the solution of the one dimensional SDE

Assuming big enough, and smooth, we prove a strong rate of convergence of order one, recovering the classical result of Milstein for SDEs with smooth diffusion coefficient. In contrast with other recent results, our proof does not relies on Lamperti transformation, and it can be applied to a wide class of drift functions. On the downside, our hypothesis on the critical parameter value is more restrictive than others available in the literature. Some numerical experiments and comparison with various other schemes complement our theoretical analysis that also applies for the simple projected Milstein scheme with same convergence rate.

1 Introduction and main result

The Milstein scheme was introduced by Milstein in [16] for one dimensional Stochastic Differential Equations (SDEs) having smooth diffusion coefficient. Introducing an appropriated correction term, this scheme has better convergence rate for the strong error than the classical Euler-Maruyama scheme. Typically, when the drift and diffusion coefficient of one dimensional SDE are twice continuously differentiable with bounded derivatives, the Milstein scheme is of order one for strong error (see eg. Talay [20]) instead of one-half for the Euler-Maruyama scheme. This well-know fact produces remarks on blogs, internet forums, and software packages that sometimes recommend to use the Milstein scheme for constant elasticity of variance (CEV) models in finance, or its extension with stochastic volatility as SABR model, (see e.g Delbaen and Shirakawa [8] and Lions and Musiela [15] for a discussion on the (weak) existence of such models); CEV are popular stochastic volatility models of the form

with . But the interesting fact in this story is that the rate of convergence of the Milstein scheme, for such family of processes with is not yet well studied, to the best of our knowledge.

In this paper we establish a rate of convergence result for a symmetrized version of the Milstein scheme applied to the solution of the one dimensional SDE

| (1.1) |

where , and . Of course Equation (1.1) does not satisfies the hypothesis to apply the classical result of Milstein [16]. In particular, the diffusion coefficient is only Hölder continuous whereas the classical hypothesis is to have a diffusion coefficient.

The main picture of our convergence rate result is that Milstein scheme stays of order one in the case of Equation (1.1), but some attention must be paid to the values of , and .

There exist in the literature other strategies for the discretization of the solution to (1.1). There are some results based on the Lamperti transformation of the equation, for example, by Alfonsi [1, 2], and by Chassagneux, Jacquier and Mihaylov [6]. And also, there some are results where the equation (1.1) is discretized directly, as in Berkaoui, Bossy and Diop [3] or in Kahl and Jackël [12]. In the numerical experiments section, we compare the symmetrized Milstein scheme with a selection of schemes proposed in the aforementioned references. We also experiment the symmetrized Milstein scheme in a multilevel Monte Carlo application and we compare with other schemes.

In the whole paper, we work under the following basis-hypothesis:

Hypothesis 1.1.

The power parameter in the diffusion coefficient of Equation (1.1) belongs to . The drift coefficient is Lipschitz with constant , and is such that .

Hypothesis 1.1 is a classical assumption to ensure a unique strong solution valued in . We assume it in all the forthcoming results of the paper, without recall it explicitly. To state the convergence result (see Theorem 1.6), another Hypothesis 1.5 will be added and discussed, that in particular constrains the values , and .

1.1 The symmetrized Milstein scheme

To complete our task we follow the ideas of Berkaoui, Bossy and Diop in [3] who analyze the rate of convergence of the strong error for the symmetrized Euler scheme applied to Equation (1.1). Although, whereas they utilize an argument of change of time, we consider first a weighted -error for which we prove a convergence result, and then we utilize this result to prove the convergence of the actual -error.

We consider , , and . We define the constant step size and . Over this discretization of the interval we define the Symmetrized Milstein Scheme (SMS) by

In the following, we use the time continuous version of the SMS, satisfying

| (1.2) |

where . We also introduce the increment process defined by

| (1.3) |

so that . Thanks to Tanaka’s Formula, the semi-martingale decomposition of is given by

| (1.4) |

where .

Moment upper bound estimations for and

We summarize some facts about the process , the proofs of which can be found in Bossy and Diop [5].

Lemma 1.2.

For any , there exists a positive constant depending on , but also on the parameters , , , and such that, for any ,

| (1.5) |

When , for any ,

| (1.6) |

When , for any such that ,

| (1.7) |

Lemma 1.3.

Notice that the condition is also imposed by the Feller test in the case for the strict positivity of , that allows to rewrite Equation (1.1) as

Using the semimartingale representation (1.4), we prove the following Lemma regarding the existence of moments of any order for .

Lemma 1.4.

For any , there exists a positive constant depending on , but also on the parameters , , , and such that for any ,

The proof of this lemma is based on the Lipschitz property of and classical combination of Itô formula and Young Inequality. For the sake of completeness, we give a short proof in the Appendix.

1.2 Strong rate of convergence

The main result of this works is the strong convergence at rate one of the SMS to the exact process . The convergence holds in for . To state it, we add to Hypothesis 1.1 the following.

For any in , we denote the rounded up integer.

Hypothesis 1.5.

(i) Let . To control the -norm of the error, if we assume . Whereas for we assume .

(ii) The drift coefficient is of class , and has polynomial growth.

We now state our main theorem. To lighten the notation, we consider for

| (1.9) |

and we extend this definitions to taking limits. So, , and . Notice that , and since is continuous on , we have that is bounded. This is especially important in the definition of bellow, because tells us that is strictly positive and bounded on .

Theorem 1.6.

About Hypothesis 1.5.

Notice that for , Assumption does not depend on and becomes easier to fulfill as increases. On the other hand, for , Assumption depends on in a unpleasant manner. However, as we will see later in Section 4 (see Table 1), this kind of dependence in is expected, and similar conditions are asked in the literature for other approximation schemes in order to obtain similar rate of convergence results.

Also, notice that is a sufficient condition: in the numerical experiments we still observe a rate of convergence of order one for parameters that do not satisfy it, but we also observe that for parameters such that , although the convergence occurs, it does in a sublinear fashion.

On the other hand, Assumption is the classical requirement for the strong convergence of the Milstein scheme. As we will see later in the proof of the main theorem, with the help of the Itô formula, this hypothesis let us conclude that

instead of

which is the classical bound obtained for the Euler-Maruyama scheme under a Lipschitz condition for a drift .

The rest of the paper is organized as follow. In Section 2 we state some preliminary results on the scheme which will be building blocks in the proof of Theorem 1.6. Section 3 is devoted to the proof of the convergence rate. The main idea is first to introduce a weight process in the -error. Wet get the rate of convergence for this weighted error process, and we use this intermediate bound to control the -error, from where we finally control the -error. Also, as a byproduct we obtain the order one convergence of the Projected Milstein Scheme (see 3.3). In section 4, we display some numerical experiments to show the effectiveness of the theoretical rate of convergence of the scheme, but also to test Hypotheses 1.5- on a set of parameters. In this section we also shows how the inclusion of the SMS in a Multilevel Monte Carlo framework could help to optimize the computational time of weak approximation of assets valuation. In Section 5 we present the proof of the preliminary results on the scheme. Finally we have included in a small appendix a couple of proofs to make this paper self contained.

2 Some preliminary results for

This short section is devoted to state some results about the behavior of , their proofs are postponed to Section 5. All these results hold under Hypothesis 1.5- which is in fact stronger than what we need here. So, we present the next lemmas with their minimal hypotheses (still assuming Hypothesis 1.1).

Lemma 2.1 (Local error).

For any , for any , there exists a positive constant , depending on , , the parameters of the model , , , , but not on such that

By construction the scheme is nonnegative, but a key point of the convergence proof resides in the analysis of the behavior of or visiting the point 0. The next Lemma shows that although is not always positive, the probability of being negative is actually very small under suitable hypotheses.

Lemma 2.2.

For , if , and , then there exists a positive constant , depending on the parameters of the model, but not on , such that

| (2.1) |

In particular,

| (2.2) |

To prove Lemma 2.2, it is necessary to establish before the following one, which although technical, gives some intuition about the difference between the SMS and the Symmetrized Euler scheme presented in [3].

Lemma 2.3.

For , if , we set . Then for all , and for all ,

Roughly speaking, from this lemma we see that when , becomes negative only when

But observe that only the left-hand side of this inequality depends on , and its expectation decreases to zero proportionally to , according to Lemma 2.1.

Now imposing small enough, we prove an explicit bound for the local time moment of .

Lemma 2.4.

For , if and , then there exist positive constants and depending on , , , and but not in such that

We end this section with another key preliminary result, which is the convergence rate of order 1 for the corrected local error. Although the classical local error is of order 1/2, as stated in Lemma 2.1, the local error seen by the diffusion coefficient function, corrected with the Milstein term stays of order 1.

Lemma 2.5 (Corrected local error process).

Let us fix , and . For , assume , whereas for , assume Then, there exists , depending on the parameters of the model but not in , such that for all , the Corrected Local Error satisfies

3 Proof of the main Theorem 1.6

The proof of Theorem 1.6 is built in several steps. First, we work with the -norm of the error, for , then at the last step of the proof we go back to the -norm for .

In what follows we denote

and

so that

Also, to make the notation lighter, we will denote the Corrected Local Error by

3.1 The Weighted Error

Before to prove the main theorem, we establish in the Proposition 3.1 the convergence of a weighted error. For , let us consider , defined by

| (3.1) |

and the Weight Process defined by

| (3.2) |

The Weight Process is adapted, almost surely positive, and bounded by . Its paths are non increasing and hence has bounded variation, and also satisfies

The process can be seen as an integrating factor in the sense of linear first order ODE (see for example [19]). When we apply the Itô’s Lemma to , instead of alone, we can remove a very annoying term that appears in the righthand side bound (see the proof of Lemma 3.3). The exponential weight in a -norm is a useful tool to obtain a priori bound (as an example, for the existence and uniqueness of the solution of a Backward SDE, it is introduced a norm with exponential weight, such that the operator associated to the BSDE is contractive under this new norm (see proof of Theorem 1.2 in [17]). In the same way, here we introduce this exponential weight to get the following a priori error-bound, which will allow us to prove Theorem 1.6.

Proposition 3.1 (Weighted Error).

Under the hypotheses of Theorem 1.6, for and , there exists a constant not depending on such that for all

| (3.3) |

Remark 3.2.

(i) Since we are going to work first with the -norm of the error, when , Hypothesis 1.5- becomes

in particular

| (3.4) |

(ii) From Lemma 1.2, the process has polynomial moments of any order for , and when , there exists such that for all . From the previous point in this Remark, it follows that the process has moments at least up to order .

We cut the proof of Proposition 3.1 in two technical lemmas.

Lemma 3.3.

Under the hypotheses of Theorem 1.6, for and , there exists a constant not depending on such that for all

| (3.5) |

Lemma 3.4.

Under the hypotheses of Theorem 1.6, for and , there exists a constant not depending on such that for all , and for any

| (3.6) |

As we will see soon, we prove (3.6) with the help of the Itô’s formula applied to , and here is where we need of class required in Hypotheses 1.5-.

Proof of Proposition 3.1.

Now we present the proof of the technical lemmas.

Proof of Lemma 3.3.

By the integration by parts formula,

Thanks to Lemma 2.4 and the control in the moments of the exact process in Lemma 1.2 we have

On the other hand, with , calling , we get for all

where we put aside all the terms multiplied by in

So, from the previous computations, the Lipschitz property of , and Young’s Inequality, we conclude

where , and from Lemma 2.2 we have

Since and Remark 3.2-, we can apply Lemma 2.5 so . Introducing these estimations in the previous computations, we have

Now we use the particular form of the weight process. Since for all , for all , ,

| (3.7) |

we have

and then, from the definition of in (3.1), we conclude

from where

∎

Proof of Lemma 3.4.

By integration by parts

| (3.8) | ||||

Applying Hölder’s Inequality to the first term in the right-hand side we have

Recalling the Remark 3.2-, we have that is finite, so applying Lemma 2.1,

Then,

Applying the Itô’s Formula to the second term in the right-hand side of (3.8), and taking expectation we get

| (3.9) |

By the finiteness of the moment of , the linear growth of , and the polynomial growth of , applying Holder’s inequality, we have

For the bound of , since is Lipschitz, and , we have

Where again, all the terms multiplied by are putted in the rest , and the expectation of the product is bounded with Lemma 2.2.

In a similar way for the bound of , decomposing with ,

For the first term in the right-hand side we have

due to the bound for the increments of the exact process and Lemma 2.5. For the second term, applying (3.7), and noting that from Remark 3.2-, the exact process has negative moments up to of order

We control the third term in the right-hand side in the bound for using again Lemma 2.2, so

Now we bound .

We control the first term in the right-hand side using Hölder’s inequality, Lemma 2.5 and the control in the moments of the exact process for all

For the second term in the right-hand side of the bound for , we use one more time (3.7), and the existence of negative moments of the exact process , and then

To control the third term in the right-hand side of the bound for we use Lemma 2.2 just as before. So

Finally,

Remark 3.5.

Proceeding as in the Proof of Lemma 3.4, if or , is not difficult to prove

| (3.10) |

Notice that (3.10) is similar to (3.6) with the process . The restriction on comes from the following observation. Applying the Itô’s Lemma to the function for , with the couple of processes , in the analogous of the identity (3.9) with , it will appear a term of the form

The restriction avoids the situation where is negative.

3.2 Proof of Theorem 1.6

We start by controlling the -error. First, assume or . By the Itô’s formula we have

As we have seen before, and , so

| (3.11) |

where If we use the Lipschitz property of , and Young’s inequality in the first term in the right of (3.11), Lemma 2.5 in the fourth one, and Lemma 2.2 in the fifth one, we have

| (3.12) |

And, according to Remark 3.5, we have

On the other hand, using again (3.7), we have

and applying Cauchy-Schwartz inequality,

The first term in the right-hand side is the weight error controlled by Proposition 3.1. To control the second one, let us recall Remark 3.2. For , the exact process and the weight process have negative moments of any order, therefore the second term in the last inequality is bounded by a constant. On the other hand, for we need a finer analysis. From the second point in Remark 3.2, the -th negative moment of the exact process is finite, and since

according with the third point of Remark 3.2, the -th negative moment of the weight process is also finite. Therefore, when ,

and then in any case

Introducing all the last computations in (3.12) we get

Since the right-hand side is increasing, thanks to Gronwall’s Inequality we have, for or ,

We extend to , thanks to Jensen’s inequality

and we conclude that for all satisfying Remark 3.2-.

Now we control the -error. For and , denoting ,

Hypothesis 1.5- gives

Since (3.4) in Remark 3.2 is satisfied, we can control the -norm of the error and then

If , Hypothesis 1.5- is , which is enough to bound the -norm of the error, and then from Jensen’s inequality

The case is easier. Since the Hypothesis in the parameters for this case does not depend on , we can conclude for any from Jensen’s inequality and the control for the -norm of the error.

Remark 3.6.

Let us mention an example of extension of our convergence result, based on simple transformation method: consider the -model, namely the solution of

Applying the Itô’s Formula to , with , we have

where is a Brownian motion. We can approximate with the SMS , and then define . Then we can deduce the strong convergence with rate one of to from our previous results.

Transformation methods can be used in a more exhaustive manner, in the context of CEV-like SDEs and we refer to [6] for approximation results and examples, using this approach.

3.3 Strong Convergence of the Projected Milstein Scheme

The Projected Milstein Scheme (PMS) is defined by

where for all , . The continuous time version of the (PMS) is given by

| (3.13) |

Notice that for all , , then the positive moments of the PMS are bounded (see Lemma 1.4).

To obtain a strong convergence rate for the PMS, we first show that the PMS and the SMS coincide with a large probability.

Lemma 3.7.

Let us consider the stopping time . Assume that and . Then for any ,

Proof.

Notice that is almost surely strictly positive because both schemes start from the same deterministic initial condition . On the other hand

and according to Lemma 2.2

So,

Since for any , there exists a constant such that , we have

∎

Corollary 3.8.

Assume Hypotheses 1.1 and 1.5. Consider a maximum step size defined in (1.10). Let be the process defined on (1.1) and the Projecter Milstein scheme given in (3.13). Then for any that allows Hypotheses 1.5, there exists a constant depending on , , , , , , and , but not on , such that for all ,

| (3.14) |

4 Numerical Experiments and Conclusion

We start this section with the analysis of two numerical experiments. The first one aims to study empirically the strong rate of convergence of the SMS in comparison with other schemes proposed the literature. The second one aims to study the impact of including the SMS in a Multilevel Monte Carlo application.

4.1 Empirical study of the strong rate of converge

In this experiment we compute the error of the schemes as a function of the step size for different values of the parameters and .

For we compare the SMS with the Symmetrized Euler Scheme (SES) introduced in [3], and with the Balanced Milstein Scheme (BMS) presented in [13]. Whereas for , in addition to the aforementioned schemes, we will also compare SMS with the Modified Euler Scheme (MES) proposed in [6], and with the Alfonsi Implicit Scheme (AIS) proposed in [1].

Let us first, shortly review those different schemes.

Alfonsi Implicit Scheme (AIS).

Proposed in [1], the AIS can be applied to equation (1.1) when the drift is a linear function. A priori, the AIS can be applied for , but is relevant to observe that only when , the AIS is in fact an explicit scheme (also know as drift-implicit square-root Euler approximations ) whereas in any other case is not. This implies that in order to compute the AIS for , at each time step it is necessary to solve numerically a non linear equation. This extra step in the implementation of the scheme brings questions about the impact of the error of this subroutine in the error of the scheme, and about the computing performance of the scheme. Since this questions are beyond the scope of the present work, we include the AIS in the comparison only in the Cox–Ingersol–Ross (CIR) case (linear drift and ). In this context, the AIS can be use only if , for other values of the parameters the AIS is not defined. In terms of convergence, when , according to Theorem 2 in Alfonsi [2], the AIS converges in the -norm, for , at rate when . When , the AIS (see Section 3 of [2]) converge as soon as , at rate to the exact solution.

Balanced Milstein Scheme (BMS).

The BMS was introduced by Kahl and Schurz in [13], and although its convergence it is not proven for Equation (1.1) (see Remark 5.12 in [13]), numerical experiments shows a competitive behavior (see [12]). Also, the BMS can be easily implemented for , so we decide to include it in our numerical comparison.

Modified Euler Scheme (MES).

Introduced in [6], the MES can be applied to the Equation (1.1) for when the drift has the form for and suitables functions. The rate of convergence in the -norm of the MES depends on the parameters. For the rate is 1 if is big enough compared with , and it is in other case. When , the MES converges at rate 1 as soon as (see Proposition 4.1 in [6]). When , the implementation of the MES requires some extra tuning which is not explicitly given in [6] (see Remark 5.1), so we implement the MES only for .

Symmetryzed Euler Scheme (SES).

The SES, introduced in [3], is an explicit scheme which can be apply to the equation (1.1) for and any Lipschitz drift function . It has the weakest hypothesis over of all the schemes discussed in this paper. If , according to Theorem 2.2 in [3], the rate of convergence of the SES is under suitable conditions for , and . When the SES converge at rate as soon as (see Theorem 2.2 in [3]).

| Scheme | Norm | Drift | Convergence’s Condition |

|

|||

| SMS | Lipschitz, | 1 | |||||

| with polynomial growth | |||||||

| AIS [2] | 1 | ||||||

| BMS | undetermined | ||||||

| MES [6] | |||||||

| SES [3] | Lipschitz |

|

| Scheme | Norm | Drift | Convergence’s Condition |

|

||

| SMS |

|

1 | ||||

| AIS | 1 | |||||

| BMS | undetermined | |||||

| MES | ||||||

| SES | Lipschitz |

Simulation setup

In our simulations we consider a time horizon , and . In order to include as many schemes as possible we consider for all simulations a linear drift

To measure the error of each scheme, we estimate its -norm for which a theoretical rate is proposed for all the selected schemes.

Let , , , , and be the -norm of the error for the SMS, BMS, SES, MES and AIS respectively. To estimate these quantities, we consider as a reference solution the AIS approximation for when , and the SMS for when . Then for each

we estimate by computing trajectories of the corresponding scheme, and comparing them with the reference solution. The results of these simulations are reported in Figures 1 () and 2 (). The graphs plot the in terms of the , and we have added the plot of the identity map to serve as reference for rate of order 1. The schemes with a slope smaller than the slope of the reference line have an order of convergence smaller than one. To obtain a more quantitative comparison of the schemes, we also perform a regression analysis on the model

Notice that the estimated value for , corresponds to the empirical rate of convergence of the different schemes. We present the result of this regression analysis in Tables 3 and 4.

Empirical results for .

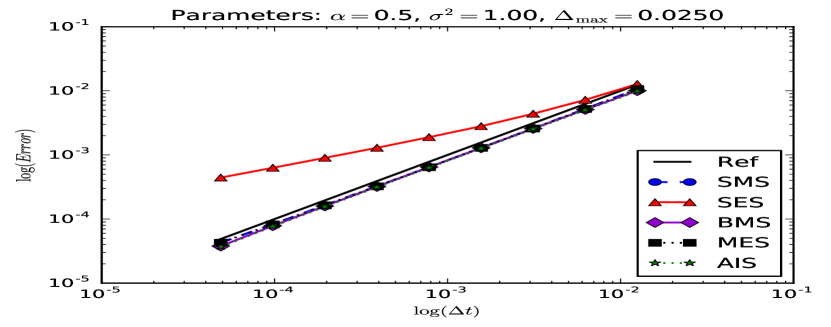

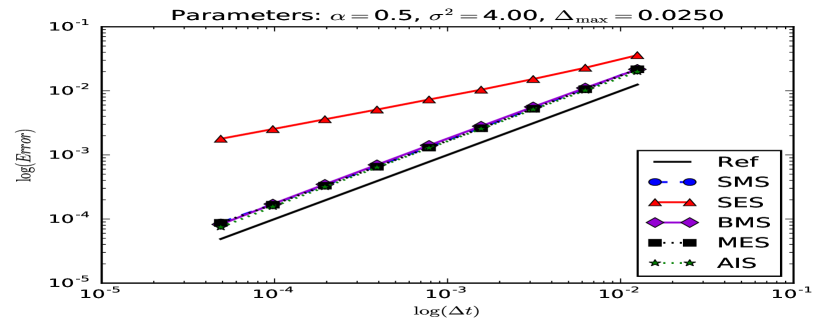

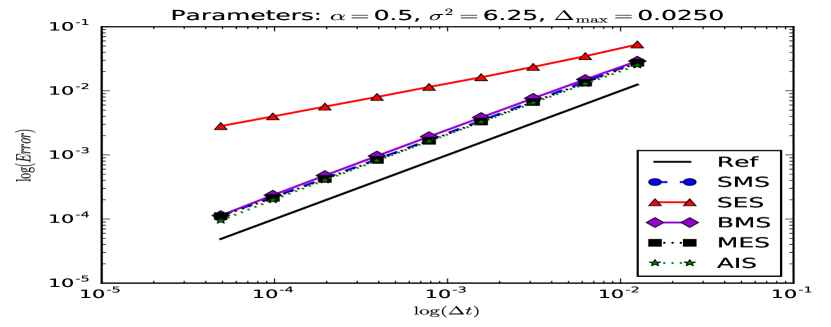

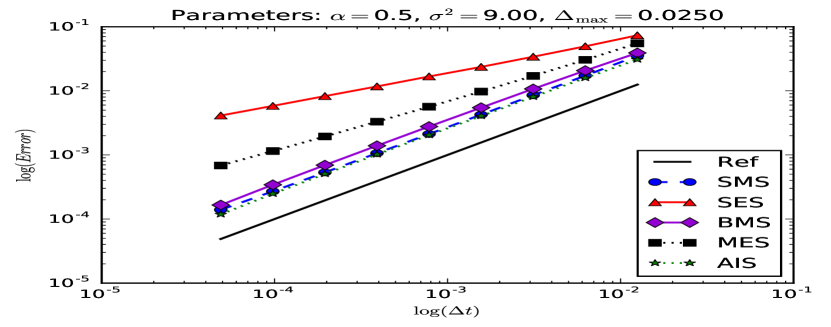

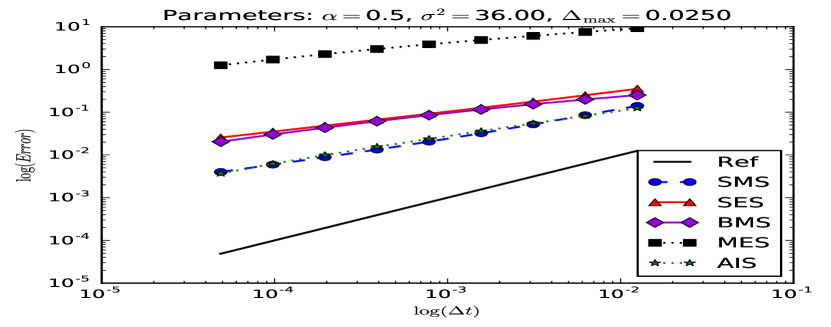

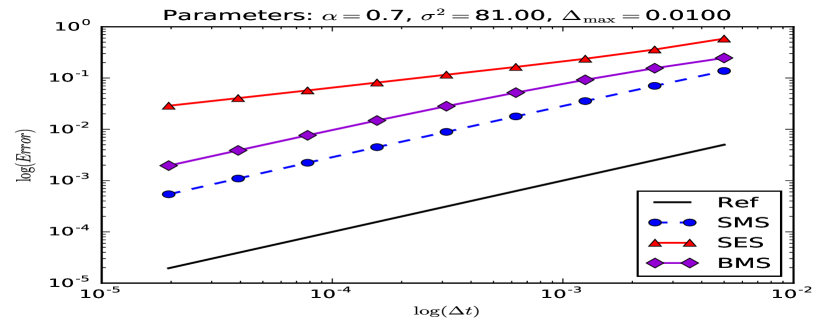

Figure 1 and Table 3 present the result for the CIR case. From Table 1, we observe that we can distinguish five cases for the parameters.

The first case is such that : the SMS, the AIS, and the MES have a theoretical rate of convergence equal to , whereas the SES has a theoretical rate of convergence equal to . In Figure 1(a), we observe that the graphs of the SMS, the AIS, the BMS, and the MES seem parallel to the reference line, which is expected, while the SES has a smaller slope. This is also confirms in the first line of the Table 3, where we observe that the empirical rates of convergence are close to the theoretical ones. Notice that the BMS has a competitive empirical rate of convergence, although the theoretical one is not known.

| Observed convergence rate (and its value) | ||||||||||

| SMS | AIS | BMS | MES | SES | ||||||

| () | () | () | () | () | ||||||

| 1 | 0.9956 | (99.9%) | 1.0060 | (99.9%) | 1.0055 | (99.9%) | 0.9955 | (99.9%) | 0.5941 | (99.3%) |

| 4 | 0.9969 | (99.9%) | 1.0054 | (99.9%) | 1.0037 | (99.9%) | 0.9961 | (99.9%) | 0.5344 | (99.8%) |

| 6.25 | 0.9976 | (99.9%) | 1.0043 | (99.9%) | 1.0002 | (99.9%) | 0.9941 | (99.9%) | 0.5237 | (99.9%) |

| 9 | 0.9984 | (99.9%) | 1.0015 | (99.9%) | 0.9859 | (99.9%) | 0.7891 | (99.9%) | 0.5164 | (99.9%) |

| 36 | 0.6410 | (99.7%) | 0.6282 | (99.8%) | 0.4538 | (99.3%) | 0.3575 | (99.4%) | 0.4718 | (99.9%) |

The second case is such that , now only the AIS and the MES have a theoretical rate of convergence equal to . However, how we can see in Figure 1(b) the SMS still shows a linear behavior in this case. Recall that the condition over the parameters is a sufficient condition and we believe that could be improved. Notice that also the BMS shows a linear behavior. In the second line of Table 3, we can observe that empirical rates of convergence are close to one for all the scheme but the SES.

In Figure 1(c), we illustrate the third case and then . In this case, only the AIS has a theoretical rate of convergence equal to one. For the MES is , but in the graphics we still observe a linear behavior for the MES, and also for the SMS and the BMS. This is confirm in the third line of Table 3.

The fourth case is and , which we display in Figure 1(d). For this values of the parameters the theoretical rate of convergence is known only for the AIS and the MES. Nevertheless, we observe in the graphs and in the fourth line of Table 3 that all the schemes seems to reach their optimal convergence rates.

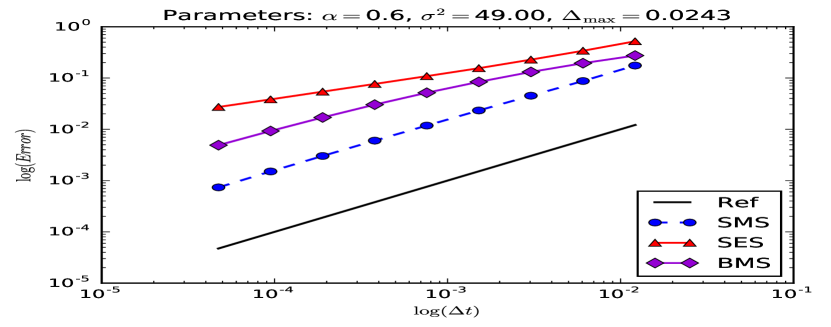

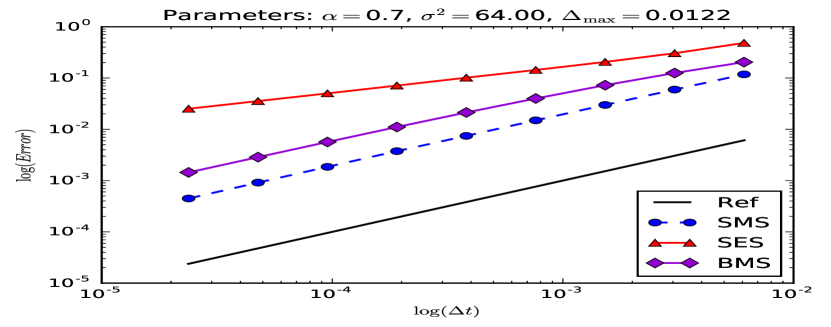

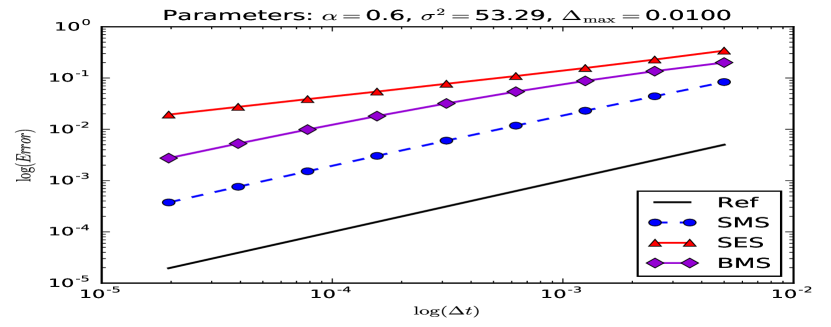

Empirical results for .

In these cases, it can be observed in numerical experiments that the MES needs smaller to achieve its theoretical order one convergence rate, unless one tunes the projection operator in the manner of Remark 5.1 in [6]. Since this tuning is not explicitly given we do not include the MES in these simulations.

| Parameters | Observed convergence rate (and its value) | ||||||

| SMS | BMS | SES | |||||

| () | () | () | |||||

| 49 | 0.9819 | (99.9%) | 0.7296 | (99.1%) | 0.5273 | (99.8%) | |

| 53.29 | 0.9766 | (99.9%) | 0.7788 | (99.3%) | 0.5133 | (99.9%) | |

| 144 | 0.6609 | (98.9%) | 0.4336 | (97.3%) | 0.5074 | (99.9%) | |

| 64 | 1.004 | (99.9%) | 0.9022 | (99.7%) | 0.5242 | (99.8%) | |

| 81 | 0.9991 | (99.9%) | 0.8813 | (99.7%) | 0.5327 | (99.7%) | |

| 225 | 0.9146 | (99.7%) | 0.6497 | (97.6%) | 0.6410 | (99.2%) | |

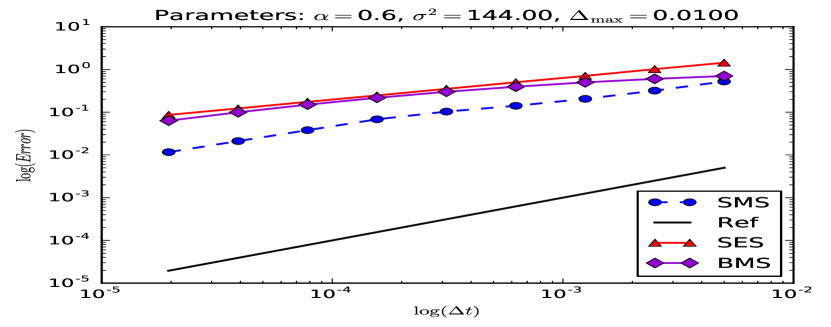

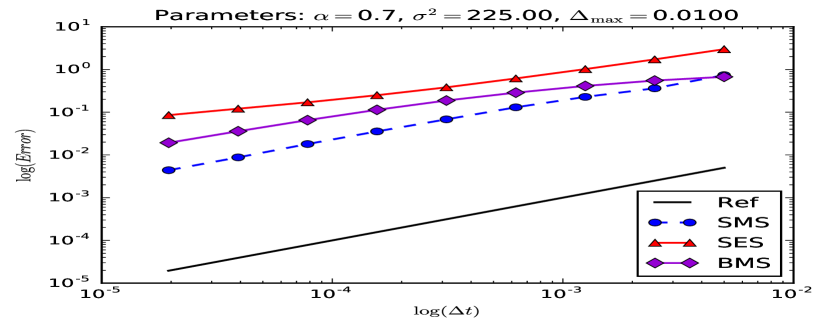

We have observed in the numerical experiments three cases for the parameters. The first one is when ( and ). In this case, Theorem 1.6 holds and we observe the order one convergence (see Figures 2(a), 2(b), and first and fourth row in Table 4). The second case is when the parameters do not satisfy ( and ), and then we can not apply Theorem 1.6, but in the numerical simulations we still observe the order one convergence (see Figures 2(c), 2(d), and second and fifth row in Table 4). Finally the third case, is when , and then we do not observe a linear convergence anymore (see Figures 2(e), 2(f), and third and six row in Table 4). Notice that in the three cases the SMS performs better than the BMS, specially when grows. (see Table 4).

The second and third case show us that some restriction has to be impose on the parameters to observe the convergence of order one. But our restriction, although sufficient, it seems to be too strong, specially for close to one.

4.2 Application of the SMS in Multilevel Monte Carlo

We continue this section by testing the SMS in the context of a multilevel Monte Carlo application widely used nowadays in computational finance (see e.g. [11] and references therein). Multilevel Monte Carlo is an efficient technique introduced by Giles [9] to decrease the computational complexity of an estimator combining Monte Carlo simulation and time discretisation scheme for a given threshold in the accuracy. For details we refer to [9, 10, 11].

For this experiment, we consider the classical but non trivial test-case of the Zero Coupon Bound (ZCB) pricing of maturity ,

under the hypothesis that the short interest rate dynamics is modeled with a CIR process ( and ) :

In this context, the price of the ZCB admits a wellknown closed-form solution given by (see e.g [7, 14])

where is the initial value of the interest rate, and . Let a discrete-time weak approximation of with the time step . We consider the -level Monte Carlo estimator :

For a targeted mean-square error on the computation of the quantity

one can choose the following a priori parametrization of the MLMC method in order to minimize the computational time (complexity) (see [9, 10, 11]): we use the estimation ; from one level to the next one the time step is divided by , ; the number of trajectories to simulate is estimated with Giles formula [9]

with . As an estimator for the bias variance, the strong rate of convergence of the discretisation scheme enters as a key ingredient in the a priori estimation. A scheme with a reduced strong bias will then allow a smaller . We apply the MLMC computation for the SMS, the PMS, the AIS and the BMS.

We summarize the results of the performance comparison between the four schemes in Table 5. The computation have been run using a initial interest rate , the maturity of the bond , the drift parameters , the volatility . For the MLMC simulation, we fix a minimum number of trajectories equal to , and a minimal number of levels equal to .

In Table 5, we give the measures of the CPU time for a set of three decreasing targeted errors, as long as the effective measured error and the total number of simulated trajectories. As expected, the required threshold error has been reached by the MLMC strategy. As also expected (see Giles [10]), Milstein schemes perform better than their Euler versions. Finally, as decreases, the SMS clearly performs better than his PMS version.

|

SMS | PMS | AIS | BMS | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|

SMS | PMS | AIS | BMS | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|

SMS | PMS | AIS | BMS | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

4.3 Conclusion

In this paper we have recovered the classical rate of convergence of the Milstein scheme in a context of non smooth diffusion coefficient, although we have to impose some restrictions over the parameters of the SDE (1.1) to ensure the theoretical order one of convergence. Typically, if the quotient is big enough we will observe the optimal convergence rate.

In the numerical simulations we have observed that, despite the fact it is necessary to impose some restriction over the parameters of SDE (1.1) to obtain the order one convergence, Hypothesis 1.5 seems to be not optimal, specially for . Also, through numerical simulations, we have observed that the use of SMS could improve the computation times in a Multilevel Monte Carlo framework, at least as well as the (CIR specialized) one-order schemes.

Although our result seems more restrictive in term of hypotheses on the set of parameters, in particular if we compare SMS with Lamperti’s transformation-based schemes (see the recent works in [2] and [6], the SMS can be applied to a more general class of drifts functions and in various contexts. It is thus a useful complement of the existing literature.

5 Proofs for preliminary lemmas

5.1 On the Local Error of the SMS

5.2 On the Probability of SMS being close to zero

From and defined in (1.9), let us recall the notation

introduced in Lemma 2.3. As under Hypothesis 1.5-, is bounded away from . In particular,

Proof of Lemma 2.3.

Denoting , and , we have for all ,

From the Lipschitz property of and the following bound for any

| (5.1) |

we have

| (5.2) |

So,

From the independence of with respect to , if we denote by a standard Gaussian variable, we have

Notice that in the right-hand side we have a quadratic polynomial of a standard Gaussian random variable. Let us compute its discriminant:

Since , we have for all , and . So, for all we have

taking we conclude on the Lemma. ∎

Proof of Lemma 2.2.

We have

| (5.3) |

We start with the second term in the right hand of the last inequality. By continuity of the path of and Lemma 2.3, we have

On the other hand, from 5.2 we have

| (5.4) |

Then

where the last equality holds thanks to the Markov Property of the Brownian motion, for

where denotes a Brownian Motion independent of .

If is a Brownian motion with drift , starting at , then for all , we have (see [4]):

| (5.5) |

where for , In our case , , and . Then

Since , for any , the arguments in the function in the last equality are both positives, and then recalling that for all , we obtain

So, for all

Then

and finally, choosing , we get

∎

5.3 On the Local Time of the SMS at Zero

The Stopping Times

In what follows, we consider

| (5.6) |

Lemma 5.1.

Assume , and . Then there exists a positive constant depending on , , and but not on such that

| (5.7) |

Proof.

First, notice that the condition ensures that the stopping time is almost surely strictly positive.

To enlighten the notation along this proof, let us call , and . We split the proof in three steps.

Step 1.

Let us prove that for a suitable function and the set :

| (5.8) |

Indeed,

But, for each

Since we have

thanks to Lemma 2.3. On the other hand, we have

where the inequality comes from (5.2), and the last equality holds thanks to the Markov Property of the Brownian motion, for

where denotes a Brownian Motion independent of . Summarizing

and we have (5.8) for .

Step 2.

Let us prove that for all :

| (5.9) |

Step 3.

5.4 On the negative moments of the stopped increment process

To prove Lemma 2.5 (see section 5.5 below), we need to control the negative moments of the stopped increment process . This is the object of the following lemmas, that can be summarize in the following

Lemma 5.2.

Let . Let be the stopping time defined in (5.6). Let us assume . Moreover, let us assume when , and when . Then there exists a constant depending on , , , and but not on , such that

Existence of Negative Moments. Case

The proof of the existence of Negative Moments of has two parts. First we study the quotient , and then we proof the main result of the section.

Lemma 5.3.

For , and we have

| (5.10) |

To prove this lemma, we need the following auxiliary result, the proof of which is postponed in Appendix A as a straightforward adaptation of the Lemma 3.6 in [5].

Lemma 5.4.

Assume Hypothesis 1.1 holds, and . Assume also that . Then, for any there exists a constant depending on the parameters , , , , , and also on , such that

Proof of Lemma 5.3.

Lemma 5.5.

Let be the stopping time defined in (5.6), and . If , and

| (5.12) |

Then there exists a constant depending on , , , and but not on , such that

Proof.

Let us call , and . By Ito’s formula

| (5.13) |

But,

| (5.14) |

Indeed,

But, thanks to the Lipschitz property of ,

since , and . So we have (5.14). Introducing (5.14) in (5.13), and using , we have

| (5.15) |

Since

and applying Hölder’s Inequality for some , we have

Since , we have , so choosing , and applying Lemma 5.3 we have

and then

Since from the Hypotheses, the third term in the right-hand side is negative, we can conclude thanks to Gronwall’s Lemma. ∎

Existence of Negative Moments. Case

Lemma 5.6.

For , if and , there exists such that

| (5.16) |

Proof.

Let us call , , and

Notice that for fix , is a quadratic polynomial. Using (5.2), we have

where recall, . But

where stands for a standard Gaussian random variable. As in the Lemma 2.3, we have a quadratic polynomial in , its discriminant is

so if , and the quadratic form in has not real roots, and in particular is non negative almost surely. Then

On the other hand,

and since we can apply the exponential bound for Gaussian tails and get

We conclude by taking . ∎

Lemma 5.7.

Let be the stopping time defined in (5.6). Let us assume for , , and , then for all , there exists a constant depending on , , , and but not on , such that

Proof.

Let us call . By Ito’s formula and the Lipschitz property of ,

| (5.17) |

Following the same ideas to prove (5.14), for all we can easily prove that almost surely

Introducing this bound in the previous inequality, we have

| (5.18) |

since for ,

we get

The last term in the previous inequality is bounded because of the definition of and the Lemma 5.6. Indeed,

So, (5.18) becomes

| (5.19) |

But, for any , the mapping is bounded, and (5.19) becomes

from where we can conclude applying Gronwall’s Lemma. ∎

5.5 On the corrected local error process

Proof of Lemma 2.5.

Let us recall the notation in the proof of the main Theorem

| (5.20) |

and also introduce

and .

Using Lemma 5.1, and the finiteness of the moments of , is easy to prove

Then we only have to prove

| (5.21) |

Notice that , so

Then applying Itô’s Formula to the function which is for , we have

| (5.22) |

Notice that on the event we have , and then

By the Burkholder-Davis-Gundy inequality, there exists a constant depending only on such that

observing that the integrand in the right-hand side is positive. And we have

But for , and it holds , so

Let . Thanks to Hölder’s inequality we have

We use Lemma 2.1 to bound the Local Error of the scheme

On the other hand, when , we have control of any negative moment of , so

whereas when , we choose , such that so we have control of the -th negative moment of . And then

So, in any case we have

And then we can conclude

Using the same arguments for , we have

To bound we proceed as follows

Finally for we consider first . In this case we have control of any negative moment of . So proceeding as before

The case is a little more delicate. Let us recall the identity used in the proof of (5.14)

so, we have from the definition of

Then

So for every , , from where we conclude on the Lemma. ∎

Acknowledgements.

The authors are grateful to the anonymous Referees for their useful suggestions and comments on the early version of this work.

The second author acknowledges the following institutions for their financial support: Proyecto Mecesup UCH0607, the Dirección de Postgrado y Postítulo de la Vicerrectoría de Asuntos Académicos de la Universidad de Chile, the Instituto Francés de Chile - Embajada de Francia en Chile, and the Center for Mathematical Modeling CMM.

Appendix A Appendix

Proof of Lemma 1.4.

Let us recall the notations , and . Let us define . Then by Itô’s Formula, Young’s inequality and the Lipschitz property of , we have

| (A.1) |

From the definition of , a straightforward computation shows that for all almost surely

Putting this in (A.1), we have

Since we have and then, using Young’s Inequality and the finiteness of the moments of Gaussian random variables, we conclude

Since the right-hand side is increasing, we can take supremum in the left-hand side and from here, applying Gronwall’s inequality, and taking we get

From here, following standard argument using Burkholder-Davis-Gundy inequality we can conclude on Lemma 1.4. ∎

Proof of lemma 5.4..

First, from the definition of we have

then

where . From here, just as in Lemma 3.6 in [5], we conclude

| (A.2) |

Then if we introduce the same sequence of Lemma 3.6 in [5], given by

We can repeat the proof in [5] and find out that if then, the sequence is nonnegative, decreasing and satisfies the following bound

On the other hand making the same calculations to obtain (A.2) we can get for any ,

from where, by an induction argument we have

From here, and the bound for the sequence , we have

From where we see immediately

References

- [1] A. Alfonsi. On the discretization schemes for the CIR (and Bessel squared) processes. Monte Carlo Methods and Applications, 11:355–384, December 2005.

- [2] A. Alfonsi. Strong order one convergence of a drift implicit Euler Scheme: Application to CIR process. Statistic and Probability Letters, (83):602–607, 2013.

- [3] A. Berkaoui, M. Bossy, and A. Diop. Euler sheme for SDEs with non-Lipschitz diffusion coeffcient : strong convergence. ESAIM Probability and Statistics, 12:1–11, 2008.

- [4] A.N. Borodin and P. Salminen. Handbook of Brownian Motion: Facts and Formulae. Operator Theory, Advances and Applications. Birkhäuser, 2002.

- [5] M. Bossy and A. Diop. Euler sheme for one dimensional SDEs with a diffusion coeffcient function of the form , in . Preprint arXiv:1508.04573, 2004.

- [6] J.-F. Chassagneux, A. Jacquier, and I. Mihaylov. An explicit Euler scheme with strong rate of convergence for financial SDEs with non-Lipschitz coefficients. Preprint, 2015.

- [7] J. Cox, J. Ingersoll, and S. Ross. A theory of the Term Structure of Interest Rates. Econometrica, 53(2):385–407, Mar. 1985.

- [8] F. Delbaen and H. Shirakawa. A Note on Option Pricing for the Constant Elasticity of Variance Model. Asia-Pacific Financial Markets, 9(2):85–99, 2002.

- [9] M. B. Giles. Multilevel Monte Carlo Path Simulation. Operations Research, 56(3):607–617, 2008.

- [10] Mike Giles. Improved Multilevel Monte Carlo Convergence using the Milstein Scheme. In Alexander Keller, Stefan Heinrich, and Harald Niederreiter, editors, Monte Carlo and Quasi-Monte Carlo Methods 2006, pages 343–358. Springer Berlin Heidelberg, Berlin, Heidelberg, 2008.

- [11] D.J. Higham. An Introduction to Multilevel Monte Carlo for Option Valuation. Preprint, 2015.

- [12] C. Kahl and P. Jäckel. Fast strong approximation Monte Carlo schemes for stochastic volatility models. Quantitative Finance, 6(6):513–536, 2006.

- [13] C. Kahl and H. Schurz. Balanced Milstein methods for ordinary SDEs. Monte Carlo Methods and Applications, 12(2):143–170, 2006.

- [14] D. Lamberton and B. Lapeyre. Introduction to Stochastic Calculus Applied to Finance, Second Edition. Chapman & Hall/CRC Financial Mathematics Series. Taylor & Francis, 1996.

- [15] P.-L. Lions and M. Musiela. Correlations and bounds for stochastic volatility models. Annales de l’Institut Henri Poincare (C) Non Linear Analysis, 24(1):1 – 16, 2007.

- [16] G. N. Milstein. Approximate Integration of Stochastic Differential Equations. Theory of Probability & Its Applications, 19:557–562, 1974.

- [17] E. Pardoux. Backward Stochastic Differential Equations and Viscosity Solutions of Systems of Semilinear Parabolic and Elliptic PDEs of Second Order. In Laurent Decreusefond, Bernt Øksendal, Jon Gjerde, and Ali Süleyman Üstünel, editors, Stochastic Analysis and Related Topics VI: Proceedings of the Sixth Oslo—Silivri Workshop Geilo 1996, pages 79–127. Birkhäuser Boston, Boston, MA, 1998.

- [18] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion. Grundlehren der mathematischen Wissenschaften. Springer-Verlag Berlin Heidelberg, 1st edition, 1991.

- [19] G.F. Simmons. Differential equations: with applications and historical notes. International series in pure and applied mathematics. McGraw-Hill, 1972.

- [20] D. Talay. Probabilistic numerical methods for partial differential equations: elements of analysis. In D. Talay and L. Tubaro, editors, Probabilistic Models for Nonlinear Partial Differential Equations, volume 1627 of Lecture Notes in Mathematics, pages 148–196. Springer-Verlag, CIME Lectures, 1996.