Why is GDP growth linear?

Abstract

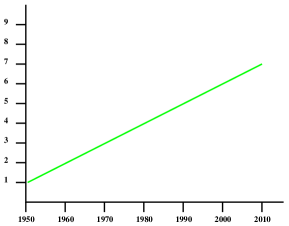

In many European countries the growth of the real GDP per capita has been linear since 1950. An explanation for this linearity is still missing. We propose that in artificial intelligence we may find models for a linear growth of performance. We also discuss possible consequences of the fact that in systems with linear growth the percentage growth goes to zero.

In Babylonia the real GDP per capita has shown a linear growth from 1950 up to now (2015), as in practically all European countries (up to fluctuations) [1,2,3,4,5]. In the USA growth has indeed been exponential, but this is due to the exponential growth of the population: More people eat more and work more. There, the real per capita GDP has grown linearly, too. Of course, linear growth may break down due to a particular incidence, as it happened to Russia in 1989.

How could such a linear growth process start? And what is the mechanism behind it?

For a physicist, among all possible types of lines - exponential, logarithmic, logistic, wavelike, chaotic, stochastic - a straight line is indeed something very special and thus calls for an explanation.

So far I don’t know any answer to this question. Some economists say that it is exponential but the second term is so small that we don’t see it yet; others say that this linearity is purely accidental; still others say that linear growth cannot occur, so we need not talk about it.

Sure, there are systems with an exponential growth: compound interest, bacteria in a Petri dish, Moore’s Law; others start with an exponential growth and then run into saturation (logistic growth): the number of Gothic cathedrals in Europe, the number of burned witches in Scotland, and the concentration in the atmosphere [6,7,8,11]. These two types are related to mathematical models: The equation leads to exponential growth, and leads to logistic growth (with and system specific parameters).

For a linear growth we may take the bathtub as an example, with a constant flow of water, which could be modeled by the equation . However, I find it hard to believe that economy could be seen as a system just nourished by a constant flow of something.

Something more sophisticated may be needed for an explanation. An example is the use of thermodynamic models in economics, but as far as I know also this approach cannot reproduce a linear growth of the GDP.

However, in artificial intelligence one could possibly meet systems with such a behaviour, like in some Pseudo-Monte-Carlo systems. Here, in a complex learning system, at a random spot some change is applied, and if the performance of the system is increased the change will be kept, otherwise it will be reversed; and this proceedure will be repeated at some other spot etc. In such a system the performance may grow linearly.

This could serve as a possible model for economics: For instance, at some spot an engineer modifies a diesel engine, and if this leads to a better performance the modification will be kept; or if a company brings to market a visual telephone, and this turns out to be a flop, then the company will stop producing these devices. (Later on the idea of a visual telephone may successfully be implemented in a different way.) Actually, if progress in economy is based on many single logistic processes taking place in time, the sum of these may have a linear line as an evelope; but this is purely speculative.

In artificial intelligence there are other processes which are linear in time. In “sane” artificial evolution the pragmatic information grows linearly in time (up to fluctuations), but in this case the information is the logarithm of the performance which itself is exponential. Now we could turn the argument around and say that there is some economic quantitiy X which grows exponentially, and the GDP is just its logarithm. However, this would somehow contradict the fact that the pragmatic information contained in a quantity of money is proportional to its logarithm [11].

Let us now consider more closely some systems with logistic growth [6,7,8]. The construction of Gothic cathedrals is an example. In those times the population in the cities was growing very fast, so there was a need for larger churches, and we may call this a technical reason for growth. On the other hand, Gothic cathedrals were in fashion, which can be seen as a “cultural program”, a term which (in this context) has been coined by Cesare Marchetti.

In the case of burning witches we can hardly speak of a technical process, because at that time the technology of stakes was well developed; so this seems to have been a purely cultural program. (See also [9].)

It is often difficult to distinguish between technical and cultural processes. Consider for example Moore’s Law which says that the number of transistors on a chip doubles every 18 months. Thus the relative growth rate is a constant leading to an exponential growth. Is this a technical or a cultural process? At first we may say that there are technical reasons for this growth behaviour, like the development of technology or the money available for R&D; but we may also suspect that it is a cultural program or even a cultural pressure such that the protagonists - physicists, engineers, managers - act in a way to fulfill the program.

In the case of GDP growth we are faced with the same question: Is there a technical reason for linear growth, or is this a cultural process such that the protagonists - engineers, managers, politicians, jurists - act in a way to fulfill the program of linear growth? In the latter case we may say that somewhere there is some kind of information in the system which is preserved and determines the process.

Another amazing fact is that economic growth has been remarkably stable against the political direction of the government, against the social policy, against several tax reforms, against the distribution of wealth, against external disturbances (the influence of the two oil crises, e.g., was very small indeed), with the gobalisation, with innovations like the internet, etc.

An unavoidable consequence of linear growth is that the relative growth rate itself decreases. Clearly if grows linearly, , the growth rate is a constant, the relative growth rate goes to zero like , and the same of course applies to the percentage growth rate which is just . So, for instance, globalization did not lead to a faster growth of economy; but we cannot exclude that it was a measure to keep the slope of growth constant.

Thus, whereas in the decade from 1950 to 1960 the GDP increased by 100 %, the percentage growth went down to an increase of 17 % between 2000 and 2010, corresponding to an average annual percentage growth rate of 1.7 %; now, in 2015, the percentage growth rate is reported to be around 1.3 % (with fluctuations, of course).

In the seventies people thought that a stable economy without growth was not possible. Now we have an experimental proof that a (nearly) steady-state economy is indeed possible (unless you claim that it is not stable).

Is there a connection between the growth rate and the level of interest? And is the presently low interest rate necessarily smaller than the percentage growth rate? We may assume that interest can only be generated by a surplus in the production. Then it cannot be larger than the growth rate of economy. Actually we see that the interest produced by a life insurance can no longer reach values of 4% or larger; and one of the problems connected to the Euro Stability Pact may be due to the assumption that the percentage growth rate of the debts may achieve up to (a number connected to the Holy Trinity), whereas now the percentage growth rate of the GDP has become much smaller. So we might suspect that the decline of the relative growth rate like was not taken into account when the Euro Stability Pact was closed. We also have to keep this in mind when talking about the crisis connected to Greece, and the interest rates they have to pay for their debts.

Finally we may ask why investigations remain low in spite of the fact that loans are cheap. Could it be that also industry does not believe in a larger growth rate in demand? And how could we possibly start a new cycle of growth (linear or other)? Or is this unnessecary?

Remark: Some if these questions have already been discussed in references [10,11].

Acknowledgment:

It is a pleasure to thank Dr. Kay Bourcarde for his hint to ref. [3].

References:

[1] Horst Afheld (1997), Wohlstand für Niemand? Die Marktwirtschaft entläßt ihre Kinder. Rohwolt Tb. ISBN: 978-3499604720

[2] Kernaussage des Instituts für Wachstumsstudien (Edition 2013). Dr. Kay Bourcarde, Institut für Wachstumsstudien, Postfach 11 12 31, D-35357 Gießen

[3] Sören Wibe, Ola Carlén, Is Post-War Economic Growth Exponential? Australian Economic Review, Vol. 39, No. 2, pp. 147-156, June 2006

[4] Carlén Ola, Wibe Sören (2012), A Note on Post-War Economic Growth. The Empirical Economics Letters, 11 (2)

[5] http://antipropaganda.eu/USSRGrowth.html

[6] Cesare Marchetti (1996), Looking Forward – Looking

Backward. A Very Simple Mathematical Model for Very Complex Social

Systems. To be found in:

http://cesaremarchetti.org/publist.php

[7] Cesare Marchetti, A Personal Memoir: From Terawatts to Witches. My Life with Logistics at IIASA. Technonlogical Forecasting and Social Change 37, 409-414 (1990)

[8] John Casti, Reality Rules, The Fundamentals; in particular: p. 131. Wiley Interscience (1990) ISBN: 978-0471570219

[9] Christopher Fry, The Lady’s Not for Burning. Dramatist’s Play Service (January 1998). ISBN: 0-8222-1431-8

[10] J.D.Becker (Hrsg), Wirtschaftsphysik (2 Bände). Proceedings eines Workshops, München, September 2008. Universität der Bundeswehr München 2008

[11] Jörg D. Becker (2014), Information Theory - A Tool for Thinking. Shaker Verlag. ISBN: 978-3-8440-2719-8