Distributed SDDM Solvers: Theory & Applications

Abstract

In this paper, we propose distributed solvers for systems of linear equations given by symmetric diagonally dominant M-matrices based on the parallel solver of Spielman and Peng. We propose two versions of the solvers, where in the first, full communication in the network is required, while in the second communication is restricted to the R-Hop neighborhood between nodes for some . We rigorously analyze the convergence and convergence rates of our solvers, showing that our methods are capable of outperforming state-of-the-art techniques.

Having developed such solvers, we then contribute by proposing an accurate distributed Newton method for network flow optimization. Exploiting the sparsity pattern of the dual Hessian, we propose a Newton method for network flow optimization that is both faster and more accurate than state-of-the-art techniques. Our method utilizes the distributed SDDM solvers for determining the Newton direction up to any arbitrary precision . We analyze the properties of our algorithm and show superlinear convergence within a neighborhood of the optimal. Finally, in a set of experiments conducted on randomly generated and barbell networks, we demonstrate that our approach is capable of significantly outperforming state-of-the-art techniques.

1 Introduction

Solving systems of linear equations given by symmetric diagonally matrices (SDD) is of interest to researchers in a variety of fields. Such constructs, for example, are used to determine solutions to partial differential equations [18] and computations of maximum flows in graphs [19, 20]. Other application domains include machine learning [21, 22], and computer vision [34]111This research is supported in parts by by ONR grant Number N00014-12-1-0997 and AFOSR grant FA9550-13-1-0097..

Much interest has been devoted to determining fast algorithms for solving SDD systems. Recently, Spielman and Teng [24], utilized the multi-level framework of [25], pre-conditioners [26], and spectral graph sparsifiers [27], to propose a nearly linear-time algorithm for solving SDD systems. Further exploiting these ingredients, Koutis et. al [28, 29] developed an even faster algorithm for acquiring -close solutions to SDD linear systems. Further improvements have been discovered by Kelner et. al [30], where their algorithm relied on only spanning-trees and eliminated the need for graph sparsifiers and the multi-level framework.

Motivated by applications, much progress has been made in developing parallel versions of these algorithms. Koutis and Miller [31] proposed an algorithm requiring nearly-linear work (i.e., total number of operations executed by a computation) and depth (i.e., longest chain of sequential dependencies in the computation) for planar graphs. This was then extended to general graphs in [32] leading to depth close to . Since then, Peng and Spielman [11] have proposed an efficient parallel solver requiring nearly-linear work and poly-logarithmic depth without the need for low-stretch spanning trees. Their algorithm, which we provide a distribute construction for, requires sparse approximate inverse chains [11] which facilitates the solution of the SDD system.

Less progress, on the other hand, has been made on the distributed version of these solvers. Contrary to the parallel setting, memory is not shared and is rather distributed in the sense that each unit abides by its own memory restrictions. Furthermore, communication in a distributed setting fundamentally relies on message passing through communication links. Current methods, e.g., Jacobi iteration [16, 17], can be used for such distributed solutions but require substantial complexity. In [33], the authors propose a gossiping framework for acquiring a solution to SDDM systems in a distributed fashion. Recent work [34] considers a local and asynchronous solution for solving systems of linear equations, where they acquire a bound on the number of needed multiplication proportional to the degree and condition number of the graph for one component of the solution vector.

Contributions: In this paper, we propose a fast distributed solver for linear equations given by symmetric diagonally dominant M-Matrices. Our approach distributes the parallel solver in [11] by considering a specific approximated inverse chain which can be computed efficiently in a distributed fashion. We develop two versions of the solver. The first, requires full communication in the network, while the second is restricted to R-Hop neighborhood of nodes for some . Similar to the work in [11], our algorithms operate in two phases. In the first, a “crude” solution to the system of equations is retuned, while in the second a distributed R-Hop restricted pre-conditioner is proposed to drive the “crude” solution to an -approximate one for any . Due to the distributed nature of the setting considered, the direct application of the sparsfier and pre-conditioner of Peng and Spielman [11] is difficult due to the need of global information. Consequently, we propose a new sparse inverse chain which can be computed in a decentralized fashion for determining the solution to the SDDM system.

Interestingly, due to the involvement of powers of matrices with eigenvalues less than one, our inverse chain is substantially shorter compared to that in [11]. This leads us to a distributed SDDM solver with lower computational complexity compared to state-of-the-art methods. Specifically, our algorithm’s complexity is given by

with being the number of nodes in graph , and denoting the largest and smaller weights of the edges in , respectively, representing the upper bound on the size of the R-Hop neighborhood , and being the precision parameter. Furthermore, our approach improves current linear methods by a factor of and by a factor of the degree compared to [34] for each component of the solution vector.

Having developed such distributed solvers, we next contribute by proposing an accurate distributed Newton method for network flow optimization. Exploiting the sparsity pattern of the dual Hessian, we propose a Newton method for network optimization that is both faster and more accurate than state-of-the-art techniques. Our method utilizes the proposed SDDM distributed solvers to approximate the Newton direction up to any arbitrary . The resulting algorithm is an efficient and accurate distributed second-order method which performs almost identically to exact Newton. We analyze the properties of the proposed algorithm and show that, similar to conventional Newton methods, superlinear convergence within a neighborhood of the optimal value is attained. We finally demonstrate the effectiveness of the approach in a set of experiments on randomly generated and Barbell networks.

2 The parallel SDDM Solver

We now review the parallel solver for symmetric diagonally dominant (SDD) linear systems [11].

2.1 Problem Setting

As detailed in [11], SDDM solvers consider the following system of linear equations:

| (1) |

where is a Symmetric Diagonally Dominant M-Matrix (SDDM). Namely, is symmetric positive definite with non-positive off diagonal elements, such that for all :

The system of Equations in 1 can be interpreted as representing an undirected weighted graph, , with being its Laplacian. Namely, , with representing the set of nodes, denoting the edges, and representing the weighted graph adjacency. Nodes and are connected with an edge iff , where:

Following [11], we seek -approximate solutions to , being the exact solution of , defined as:

-

Approximate Solution

Let be the solution of . A vector is called an approximate solution, if:

(2)

The R-hop neighbourhood of node is defined as . We also make use of the diameter of a graph, , defined as .

-

Sparsity Pattern

We say that a matrix has a sparsity pattern corresponding to the R-hop neighborhood if for all and for all such that .

We will denote the spectral radius of a matrix by , where represents an eigenvalue of the matrix . Furthermore, we will make use of the condition number222Please note that in the case of the graph Laplacian, the condition number is defined as the ratio of the largest to the smallest nonzero eigenvalues., of a matrix defined as . In [11] it is shown that the condition number of the graph Laplacian is at most

where and represent the largest and the smallest edge weights in . Finally, the condition number of a sub-matrix of the Laplacian is at most , see [11].

2.2 Standard Splittings & Approximations

Our first contribution is a distributed version of the parallel solver for SDDM systems of equations previously proposed in [11]. Before detailing our solver, however, we next introduce basic mathematical machinery needed for developing the parallel solver of [11]. The parallel solver commences by considering the standard splitting of the symmetric matrix :

-

Definition

The standard splitting of a symmetric matrix is:

(3)

Here, is a diagonal matrix consisting of the diagonal elements in such that:

Furthermore, is a non-negative symmetric matrix such that:

To quantify the quality of the acquired solutions, we define two additional mathematical constructs. First, the Loewner ordering is defined as:

-

Definition

Let be the space of -symmetric matrices. The Loewner ordering is a partial order on such that if and only if is positive semidefinite.

Having defined the Loewner order, we next define the notion of approximation for matrices “”:

-

Definition

Let and be positive semidefinite symmetric matrices. Then if and only iff

(4) with meaning is positive semidefinite.

Based on the above definitions, the following lemma represents the basic characteristics of the operator:

Lemma 1.

[11] Let and, be symmetric positive semi definite matrices. Then

-

(1) If , then ,

-

(2) If and , then ,

-

(3) If and , then

-

(4) If , and are non singular and , then ,

-

(5) If and is a matrix, then .

Since the parallel solver returns an approximation, , to (see Section 2), the following lemma shows that “good” approximations to guarantee “good” approximate solutions to .

Lemma 2.

Let , and , then is approximate solution to .

Proof.

The proof can be found in the appendix. ∎

2.3 The Solver

The parallel SDDM solver proposed in [11] is a parallelized technique for solving the problem of Section 2.1. It makes use of inverse approximated chains (see Definition 2.3) to determine and can be split in two steps. In the first, Algorithm 1, a “crude” approximation, , of is returned. is driven to the -close solution, , using Richardson Preconditioning in Algorithm 2. Before we proceed, we start with the following two Lemmas which enable the definition of inverse chain approximation.

Lemma 3.

[11] If is an SDDM matrix, with being positive diagonal, and denoting a non-negative symmetric matrix, then is also SDDM.

Lemma 4.

[11] Let be an SDDM matrix, where is positive diagonal and a symmetric matrix. Then

| (5) |

Given the results in Lemmas 3 and 4, we now can consider inverse approximated chains of :

-

Definition

Let be a collection of SDDM matrices such that , with a positive diagonal matrix, and denoting a non-negative symmetric matrix. Then is an inverse approximated chain if there exists positive real numbers such that:

-

(1) ,

-

(2) , and

-

(3) .

-

It is shown in [11] that an approximate inverse chain allows for “crude” solutions to the system of linear equations in in time proportional to the number of non-zeros entries in the matrices in the inverse chain. Such a procedure is summarized in the following algorithm:

On a high level, Algorithm 1 operates in two phases. In the first (i.e., lines 3-5) a forward loop (up-to the length of the inverse chain ) computes intermediate vectors as:

| (6) |

for . These can then be used to compute the “crude” solution using a “backward” loop (i.e., lines 7-9). Consequently, the crude solution is computed iteratively backwards as:

with and as defined in Equation 6. The quality of the “crude” solution returned by the Algorithm is quantified in the following lemma:

Lemma 5.

[11] Let be the inverse approximated chain and denote be the operator defined by , namely, . Then

| (7) |

Having returned a “crude” solution to , the authors in [11] obtain arbitrary close solutions using the preconditioned Richardson iterative scheme. The first step in the exact solver is the usage of Algorithm 1 to obtain the “crude” solution . This is then updated through the loop in lines 4-8 to obtain an -close solution to , see Algorithm 2.

Following the analysis in [11], Lemma 6 provides the iteration count needed by Algorithm 2 to arrive at :

Lemma 6.

[11] Let be an inverse approximated chain such that . Then requires iterations to arrive at an close solution of with: .

3 Distributed SDDM Solvers

Having introduced the parallel solver, next we detail our first contribution by proposing a distributed solver for SDDM linear systems. In particular, we develop two versions. The first, requires full communication in the network, while the second restricts communication to the R-Hop neighborhood increasing its applicability. Not only our solver improves the computational complexity of distributed methods for system of equations represented by an SDDM matrix, but can also be applied to a variety of fields including distributed Newton methods, computer vision, among others.

To compute the solution of SDDM systems in a distributed fashion, we follow a similar strategy to that of [11] with major differences. Our distributed solver requires two steps to arrive at an -close approximation to . Similar to [11], the first step adopts an inverse approximated chain to determine a “crude” solution to . The inverse chain proposed in [11] can not be computed in a distributed fashion rendering its immediate application to our setting difficult. Hence, we par-ways with [11] by proposing an inverse chain which can be computed in a distributed fashion. This chain, defined in Section 3.1.1, enables the distributed computation of both a crude and exact solution to . Interestingly, due to the involvement of matrices with eigenvalues less than 1, the length, , of our inverse chain is substantially shorter compared to that of [11], allowing for fast and efficient distributed solvers. Given the crude solution, the second step computes an -close approximation to . This is achieved by proposing a distributed version of the Richardson pre-conditioning scheme. Definitely, this step is also similar in spirit to that in [11], but generalizes the aforementioned authors’ work into a distributed setting and allows for -close approximation to for any arbitrary . Main results on the full communication version of the solver are summarized in the following theorem:

Theorem 1.

There exists a distributed algorithm,

that computes -close approximations to the solution of in time steps, with the number of nodes in , the condition number of , and the row of , as well as representing the precision parameter.

The above distributed algorithms require no knowledge of the graph’s topology, but do require the information from all other nodes (i.e., full communication) for computing solutions to . In a variety of real-world applications (e.g., smart-grids, transportation) load, capacity, money and resource restrictions pose problems for such a requirement. Consequently, we extend the previous solvers to an R-Hop version in which communication is restricted to the R-Hop neighborhood between nodes for some . Again we follow a two-step strategy, where in the first we compute the crude solution and in the second an -close approximation to is determined using an “R-Hop restricted” Richardson pre-conditioner. These results are captured in the following theorem:

Theorem 2.

There is a decentralized algorithm,

that uses only -Hop communication between the nodes and computes -close solutions to in

time steps, with being the number of nodes in , denoting the maximal degree, the condition number of , and representing the upper bound on the size of the R-hop neighborhood , and being the precision parameter.

The remainder of the section details the above distributed solvers and provides rigorous theoretical guarantees on the convergence and convergence rates of each of the algorithms. We start by describing solvers requiring full network communication and then detail the R-Hop restricted versions.

3.1 Full Communication Distributed Solvers

As mentioned previously, our strategy for a distributed implementation of the parallel solver in [11] requires two steps. In the first a “crude” solution is returned, while in the second an -close approximation (for any arbitrary ) to is computed.

3.1.1 “Crude” Distributed SDDM Solvers

The distributed crude solver, represented in Algorithm 3, resembles similarities to the parallel one of [11] with major differences. On a high level, Algorithm 3 operates in two distributed phases. In the first, a forward loop computes intermediate vectors which are then used to update the crude solution of . The crucial difference to [11], however, is the distributed nature of these computations. Precisely, the algorithm is responsible for determining the crude solution for each node . Due to such distributed nature, the inverse approximated chain used in [11] is inapplicable to our setting. Therefore, the second crucial difference to the parallel SDDM solver is the introduction of a new chain which can be computed in a distributed fashion. Starting from , our “crude” distributed solver makes use of the following collection as the inverse approximated chain:

| (8) |

where , and , for with being the length of the inverse chain. Note that since the magnitude of the eigenvalues of is strictly less than 1, tends to zero as increases which reduces the length of the chain needed. This length is explicitly computed in Section 3.1.3 for attaining -close approximations to .

It is relatively easy to verify that is an inverse approximated chain, since:

-

(1) with for ,

-

(2) with for , and

-

(3) .

Algorithm 3 returns the component of the approximate solution vector, . As inputs it requires the inverse chain of Equation 8, the component of , and the length of the inverse chain. Namely, each node, , receives the row of , the value of (i.e., ), and the length of the inverse approximated chain and then operates in two parts. In the first (i.e., lines 1-8) a forward loop computes the component of exploiting the distributed inverse chain, while in the second a backward loop (lines 9-17) is responsible for computing the component of the“crude” solution which is then returned. Essentially, in both the forward and backward loops each of the and vectors are computed in a distributed fashion based on the relevant components of the matrices, explaining the usage of loops in Algorithm 3.

Theoretical Guarantees of Algorithm 3: Due to the modifications made to the original parallel solver, new theoretical analysis quantifying convergence and accuracy of the returned “crude” solution is needed. We show that DistrRSolve computes the component of the “crude” approximation of and provide time complexity analysis. These results are summarized in the following lemma333For ease of presentation, we leave the proof of the lemma to the appendix.:

Lemma 7.

Let be the standard splitting of . Let be the operator defined by (i.e., ). Then

Moreover, Algorithm 3 requires time steps.

In words, Lemma 7 states that Algorithm 3 requires to arrive at an approximation to the real inverse , where this approximation is quantified using Definition 2.2:

can then be used to compute the crude solution as . Note that the accuracy of approximating is limited to motivating the need for an “exact” distributed solver reducing the error to any .

3.1.2 “Exact” Distributed SDDM Solvers

Having introduced DistrRSolve, we are now ready to present a distributed version of Algorithm 2 which enables the computation of close solutions for . Contrary to the work of [11], our algorithm is capable of acquiring solutions up to any arbitrary . Similar to DistrRSolve, each node receives the row of , , and a precision parameter as inputs. Node then computes the component of the close approximation of by using DistrRSolve as a sub-routine and updates the solution iteratively as shown in lines 2-6 in Algorithm 4.

Analysis of Algorithm 4: Here, we again provide the theoretical analysis needed for quantifying the convergence and computational time of the exact algorithm for returning -close approximation to . The following lemma shows that DistrESolve computes the component of the -close approximation of :

Lemma 8.

Let be the standard splitting. Further, let in the nverse approximated chain . Then requires iterations to return the component of the close approximation for .

The above lemma proofs that the algorithm requires iterations for attaining for returning the of the -close approximation to . Consequently, the overall complexity can be summarized as:

Lemma 9.

Let be the standard splitting. Further, let in the inverse approximated chain . Then, requires time steps.

3.1.3 Length of the Inverse Chain

Both introduced algorithms depend on the length of the inverse approximated chain, . Here, we provide an analysis to determine the value of which guarantees in :

Lemma 10.

Let be the standard splitting and denote the condition number of . Consider the inverse approximated chain

with , then with .

Proof.

The proof will be given as a collection of claims:

Claim: Let be the condition number of , and denote the eigenvalues of . Then, , for all

Proof.

See Appendix. ∎

Notice that if represented an eigenvalue of , then is an eigenvalue of for all . Therefore, we have

| (9) |

Claim: Let be an SDDM matrix and consider the splitting , with being non negative diagonal and being symmetric non negative. Further, assume that the eigenvalues of lie between and . Then,

Proof.

See Appendix. ∎

Combining the above results, gives

Hence, to guarantee that , the following system must be satisfied:

Introducing for , we arrive at:

Hence, . Now, notice that if then, . Hence, . This gives , implying . ∎

Using the above results the time complexity of DistrESolve with is times steps, which concludes the proof of Theorem 1.

3.2 R-Hop Distributed Solvers

The above version of the distributed solver requires no knowledge of the graph’s topology, but does require the information from all other nodes. Next, we will outline an R-Hop version of the algorithm in which communication is restricted to the R-Hop neighborhood between nodes. Due to such communication constraints, the R-Hop solver is general enough to be applied in a variety of fields including but not limited to, network flow problems (see Section 4). Along with Theorem 2, the following corollary summarizes the results of the R-Hop distributed solver:

Corollary 1.

Let be the weighted Laplacian of . There exists a decentralized algorithm that uses only -hop communication between nodes and computes close solutions of in time steps, with being the number of nodes in , denoting the largest and the smallest weights of edges in , respectively, representing the upper bound on the size of the R-hop neighborhood , and being the precision parameter.

Similar to development of the full communication solver, the R-Hop version also requires two steps to attain the -close approximation to , i.e., the “crude R-Hop” and the “exact R-Hop” solutions.

3.2.1 “Crude” R-Hop Distributed Solver

The “crude R-Hop” solver uses the same inverse approximated chain as that of the full communication version (see Equation 8) to acquire a “crude” approximation for the component while only requiring R-Hop communication between the nodes. Algorithm 5 represents the “crude” R-Hop solver requiring the inverse chain, component of , length of the inverse chain , and the communication bound as inputs. Namely, each node receives the row of , component, , of , the length of the inverse chain, , and the local communication bound444For simplicity, is assumed to be in the order of powers of 2, i.e., . as inputs to output the component of the “crude” approximation to . Algorithm 5 operates in three major parts. Due to the need of the R-powers of and , the first step is to compute such matrices in a distributed manner.

Given the inverse chain and the communication bound, R, and serve this cause as detailed in Algorithms 6 and 7, respectively. Essentially, these algorithms execute multiplications needed for determining and in a distributed fashion looping over the relevant hops of the network. For a node, , the component of these powers are returned to Algorithm 5 as and for ; see Part One in Algorithm 5.

Similar to the full communication version, the second two parts of the “crude R-Hop” solver run two loops. In the first, the component of is computed by looping forward through the inverse chain, while in the second the component of the crude solution is determined by looping backwards.

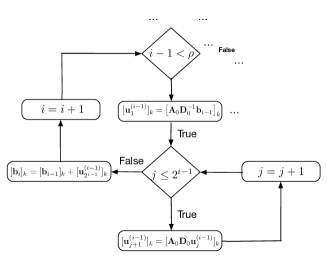

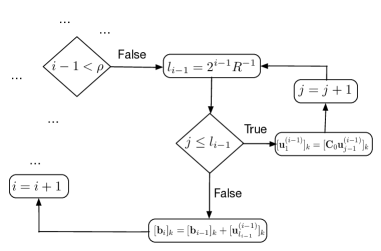

The second part of the solver is better depicted in the flow diagrams of Figures 1 and 1. Within the first loop running through the length of the inverse chain, the condition is checked. In case this condition is true, , , and the previous iteration vector are used to update as shown in Figure 1.

This is performed using another loop constructing a series of vectors for , used to update the component of at the iteration: At the next iteration, the condition is checked again. In case this condition is met, the previous computations are executed again. Otherwise, the commands depicted in Figure 1 run. Here, a temporary variable denoting the fraction to the communication bound , , is used to determine the upper iterate bound in . Again throughout this loop, a series of vectors used to update are constructed.

Having terminated the forward loop, the component of the “crude” solution is computed by looping backward through the inverse approximated chain (see part three in Algorithm 5). For running backwards to , an R-Hop condition, , is checked. In case , the following update is performed:

for , , and

The role of are backward intermediate solutions needed for updating the “crude” solution to :

for a node . In case a similar set of computations are executed for updating the crude solution using:

Analysis of Algorithm 5 Similar to the previous section, we next provide the theoretical analysis needed for quantifying the performance of the crude R-Hop solver. The following Lemma shows that RDistRSolve computes the component of the “crude” approximation of and provides the algorithm’s time complexity:

Lemma 11.

Let be the standard splitting and let be the operator defined by RDistRSolve, namely, , then . Furthermore, RDistRSolve requires

where to arrive at .

Proof.

The proof of the above Lemma can be obtained by proving a collection of claims:

Claim: Matrices and have sparsity patterns corresponding to the -Hop neighborhood for any .

The above claim is proved by induction on . We start with the base case: for ,

Therefore, has a sparsity pattern corresponding to the -Hop neighborhood. Assume that for all , has a sparsity pattern corresponding to the neighborhood. Consider,

| (10) |

Since is non negative, then iff there exists such that and , namely, . The proof can be done in a similar fashion for . ∎

The next claim provides complexity guarantees for and described in Algorithms 6 and 7, respectively.

Claim: Algorithms 6 and 7 use only the R-hop information to compute the row of and , respectively, in time steps, where .

Proof.

The proof will be given for described in Algorithm 6 as that for can be performed similarly. Due to Claim 3.2.1, we have

| (11) |

Therefore at iteration , computes the row of using:

-

(1) the row of , and

-

(2) the column of .

Node , however, can only send the row of making non-symmetric. Noting that , since is symmetric, leads to . To prove the time complexity guarantee, at each iteration computes at most values, where is the upper bound on the size of the R-hop neighborhood . Each such computation requires at most operations. Thus, the overall time complexity is given by . ∎

We are now ready to provide the proof of Lemma 11.

Proof.

From Parts Two and Three of Algorithm 5, it is clear that node computes and , respectively. These are determined using the inverse approximated chain as follows

| (12) | ||||

Considering the computation of for , we have

with for . Since has a sparsity pattern corresponding to 1-hop neighborhood (see Claim 3.2.1), node computes , based on , acquired from its 1-Hop neighbors. It is easy to see that the computation of requires time steps. Thus, the computation of requires . Now, consider the computation of but for

with , , and for . Since has a sparsity pattern corresponding to R-hop neighborhood (see Claim 3.2.1), node computes based on the components of attained from its R-hop neighbors. For each such that the computing requires time steps, where being the upper bound on the number of nodes in the hop neighborhood . Therefore, the overall computation of is achieved in time steps. Finally, the time complexity for the computation of all of the values is . Similar analysis can be applied to determine the computational complexity of , i.e., Part Three of Algorithm 5. We arrive at . Finally, using Claim 11, the time complexity of RDistRSolve (Algorithm 5) is . ∎

3.2.2 “Exact” R-Hop Distributed Solver

Having developed an R-hop version which computes a “crude” approximation to the solution of , now we provide an exact R-hop solver presented in Algorithm 8. Similar to RDistRSolve, each node receives the row , , , , and a precision parameter as inputs, and outputs the component of the close approximation of vector .

Analysis of Algorithm 8: The following Lemma shows that EDistRSolve computes the component of the close approximation to and provides the time complexity analysis.

Lemma 12.

Let be the standard splitting. Further, let . Then Algorithm 8 requires iterations to return the component of the close approximation to .

The following Lemma provides the time complexity analysis of EDistRSolve:

Lemma 13.

Let be the standard splitting and let , then EDistRSolve requires time steps. Moreover, for each node , EDistRSolve only uses information from the R-hop neighbors.

Length of the Inverse Chain: Again these introduced algorithms depend on the length of the inverse approximated chain, . The analysis in Section 3.1.3 can be applied again to determine the as the length of the inverse chain.

3.3 Comparison to Existing Literature

As mentioned before, the proposed solver is a distributed version of the parallel SDDM solver of [11]. Our approach is capable of acquiring -close solutions for arbitrary in , with the number of nodes in graph , and denoting the largest and smaller weights of the edges in , respectively, representing the upper bound on the size of the R-Hop neighborhood , and as the precision parameter. After developing the full communication version, we proposed a generalization to the R-Hop case where communication is restricted.

Our method is faster than state-of-the-art methods for iteratively solving linear systems. Typical linear methods, such as Jacobi iteration [16], are guaranteed to converge if the matrix is strictly diagonally dominant. We proposed a distributed algorithm that generalizes this setting, where it is guaranteed to converge in the SDD/SDDM scenario. Furthermore, the time complexity of linear techniques is , hence, a case of strictly diagonally dominant matrix can be easily constructed to lead to a complexity of . Consequently, our approach not only generalizes the assumptions made by linear methods, but is also faster by a factor of . Furthermore, such algorithms require average consensus to decentralize vector norm computations. Contrary to these methods which lead to additional approximation errors to the real solution, our approach resolves these issues by eliminating the need for such a consensus framework.

In centralized solvers, nonlinear methods (e.g., conjugate gradient descent [37, 36], etc.) typically offer computational advantages over linear methods (e.g., Jacobi Iteration) for iteratively solving linear systems. These techniques, however, can not be easily decentralized. For instance, the stopping criteria for nonlinear methods require the computation of weighted norms of residuals (e.g., with being the search direction at iteration ). To the best of our knowledge, the distributed computation of weighted norms is difficult. Namely using the approach in [38], this requires the calculation of the top singular value of which amounts to a power iteration on leading to the loss of sparsity. Furthermore, conjugate gradient methods require global computations of inner products.

Another existing method which we compare our results to is the recent work of the authors [34] where a local and asynchronous solution for solving systems of linear equations is considered. In their work, the authors derive a complexity bound, for one component of the solution vector, of , with being the precision parameter, a constant bound on the maximal degree of , and is defined as which can be directly mapped to . The relevant scenario to our work is when is PSD and is symmetric. Here, the bound on the number of multiplications is given by , with being the condition number of . In the general case, when the degree depends on the number of nodes (i.e., ), the minimum in the above bound will be the result of the second term ( ) leading to . Consequently, in such a general setting, our approach outperforms [34] by a factor of .

Special Cases: To better understand the complexity of the proposed SDDM solvers, next we detail the complexity for three specific graph structures. Before deriving these special cases, however, we first note the following simple yet useful connection between weighted and unweighted Laplacians of a graph . Denoting by the incidence matrix of and a diagonal matrix with edge weights as diagonal elements, we can write:

Hence, we can easily establish:

This implies that the condition number of the weighted Laplacian satisfies:

with and are the minimal and maximal edge weights of . Using the above, we now consider four different graph topologies:

3.3.1 Path Graph

Similar to the hitting time of a Markov chain on a path graph which is given by , the time complexity of the R-Hop SDDM solver is given by555Due to space constraints, the proofs can be found in the appendix.:

Corollary 2.

Given a path graph with nodes, the time complexity of the R-Hop SDDM solver is given by:

for any and for .

3.3.2 Grid Graph

Recognizing that a grid graph can be represented as a product of two path graphs, , our solver’s computational time can be summarized by:

Corollary 3.

Given a grid graph, , the time complexity of the distributed SDDM-solver can be bounded by:

for any .

3.3.3 Scale-Free Networks (Polya-Urn Graphs)

Using the results developed in [39, 40] the total time complexity of the distributed R-Hop solver is bounded by:

Corollary 4.

Given a scale-free network, , the time complexity of the R-Hop SDD solver for R=1 is given by:

3.3.4 - Regular Ramanujan Expanders

For regular Ramanujan expanders in which does not depend on , we have and . Hence, the time complexity of the SDD-solver is given by constant time.

The developed R-Hop distributed SDDM solver is a fundamental contribution with wide ranging applicability. Next, we develop one such application from. We apply our solver for proposing an efficient and accurate distributed Newton method for network flow optimization. Namely, the distributed SDDM solver is used for computing the Newton direction in a distributed fashion up-to any arbitrary . This results in a novel distributed Newton method outperforming state-of-the-art techniques in both computational complexity and accuracy.

4 Distributed Newton Method for Network Flow Optimization

Conventional methods for distributed network optimization are based on sub-gradient descent in either the primal or dual domains, see. For a large class of problems, these techniques yield iterations that can be implemented in a distributed fashion using only local information. Their applicability, however, is limited by increasingly slow convergence rates. Second order Newton methods [4] are known to overcome this limitation leading to improved convergence rates.

Unfortunately, computing exact Newton directions based only on local information is challenging. Specifically, to determine the Newton direction, the inverse of the dual Hessian is needed. Determining this inverse, however, requires global information. Consequently, authors in [5, 6, 7] proposed approximate algorithms for determining these Newton iterates in a distributed fashion. Accelerated Dual Descent (ADD) [5], for instance, exploits the fact that the dual Hessian is the weighted Laplacian of the network and performs a truncated Neumann expansion of the inverse to determine a local approximate to the exact direction. ADD allows for a tradeoff between accurate Hessian approximations and communication costs through the N-Hop design, where increased N allows for more accurate inverse approximations arriving at increased cost, and lower values of N reduce accuracy but improve computational times. Though successful, the effectiveness of these approaches highly depend on the accuracy of the truncated Hessian inverse which is used to approximate the Newton direction. As shown later, the approximated iterate can resemble high variation to the real Newton direction, decreasing the applicability of these techniques.

Contributions: Exploiting the sparsity pattern of the dual Hessian, here we tackle the above problem and propose a Newton method for network optimization that is both faster and more accurate. Using the above developed solvers for SDDM linear equations, we approximate the Newton direction up-to any arbitrary precision . This leads to a distributed second-order method which performs almost identically the exact Newton method. Contrary to current distributed Newton methods, our algorithm is the first which is capable of attaining an -close approximation to the Newton direction up to any arbitrary . We analyze the properties of the proposed algorithm and show that, similar to conventional Newton methods, superlinear convergence within a neighborhood of the optimal value is attained.

We finally demonstrate the effectiveness of the approach in a set of experiments on randomly generated and Barbell networks. Namely, we show that our method is capable of significantly outperforming state-of-the-art methods in both the convergence speeds and in the accuracy of approximating the Newton direction.

4.1 Network Flow Optimization

We consider a network represented by a directed graph with node set and edge set . The flow vector is denoted by , with representing the flow on edge . The flow conservation conditions at nodes can be compactly represented as

where is the node-edge incidence matrix of defined as

and the vector denotes the external source, i.e., (or ) indicates units of external flow enters (or leaves) node . A cost function is associated with each edge . Namely, denotes the cost on edge as a function of the edge flow . We assume that the cost functions are strictly convex and twice differentiable. Consequently, the minimum cost network optimization problem can be written as

| (13) | ||||

| s.t. |

Our goal is to investigate Newton type methods for solving the problem in 13 in a distributed fashion. Before diving into these details, however, we next present basic ingredients needed for the remainder of the paper.

4.2 Dual Subgradient Method

The dual subgradient method optimizes the problem in Equation 13 by descending in the dual domain. The Lagrangian, , is given by

The dual function is then derived as

Hence, it can be clearly seen that the evaluation of the dual function decomposes into E one-dimensional optimization problems. We assume that each of these optimization problems have an optimal solution, which is unique by the strict convexity of the functions . Denoting the solutions by and using the first order optimality conditions, it can be seen that for each edge, e, is given by666Note that if the dual is not continuously differentiable, the a generalized Hessian can be used.

| (14) |

where and denote the source and destining nodes of edge , respectively (see [6] for details). Therefore, for an edge , the evaluation of can be performed based on local information about the edge’s cost function and the dual variables of the incident nodes, and .

The dual problem is defined as . Since the dual function is convex, the optimization problem can be solved using gradient descent according to

| (15) |

with being the iteration index, and denoting the gradient of the dual function evaluated at . Importantly, the computation of the gradient can be performed as , with being a vector composed of as determined by Equation 14. Further, due to the sparsity pattern of the incidence matrix , the element, , of the gradient can be computed as

| (16) |

Clearly, the algorithm in Equation 15 can be implemented in a distributed fashion, where each node, , maintains information about its dual, , and primal, , iterates of the outgoing edges . Gradient components can then be evaluated as per 16 using only local information. Dual variables can then be updated using 15. Given the updated dual variables, the primal variables can be computed using 14.

Although the distributed implementation avoids the cost and fragility of collecting all information at centralized location, practical applicability of gradient descent is hindered by slow convergence rates. This motivates the consideration of Newton methods discussed next.

4.3 Newton’s Method for Dual Descent

Newton’s method is a descent algorithm along a scaled version of the gradient. Its iterates are typically given by

| (17) |

with being the Newton direction at iteration , and denoting the step size. The Newton direction satisfies

| (18) |

with being the Hessian of the dual function at the current iteration .

4.3.1 Properties of the Dual and Assumptions

Here, we detail some assumptions needed by our approach. We also derive essential Lemmas quantifying properties of the dual Hessian.

Assumption 1.

The graph, , is connected, non-bipartite and has algebraic connectivity lower bound by a constant .

Assumption 2.

The cost functions, , in Equation 13 are

-

1.

twice continuously differentiable satisfying

with and are constants; and

-

2.

Lipschitz Hessian invertible for all edges

The following two lemmas [5, 6] quantify essential properties of the dual Hessian which we exploit through our algorithm to determine the approximate Newton direction.

Lemma 14.

The dual objective abides by the following two properties [5, 6]:

-

1.

The dual Hessian, , is a weighted Laplacian of :

-

2.

The dual Hessian is Lispshitz continuous with respect to the Laplacian norm (i.e., ) where is the unweighted laplacian satisfying with being the incidence matrix of . Namely, :

with where and denote the largest and second smallest eigenvalues of the Laplacian .

Proof.

See Appendix. ∎

The following lemma follows from the above and is needed in the analysis later:

Lemma 15.

If the dual Hessian is Lipschitz continuous with respect to the Laplacian norm (i.e., Lemma 14), then for any and we have

Proof.

See Appendix. ∎

As detailed in [6], the exact computation of the inverse of the Hessian needed for determining the Newton direction can not be attained exactly in a distributed fashion. Authors in [5, 6] proposed approximation techniques for computing this direction. The effectiveness of these algorithms, however, highly depends on the accuracy of such an approximation. In this work, we propose a distributed approximator for the Newton direction capable of acquiring -close solutions for any arbitrary . Our results show that this new algorithm is capable of significantly surpassing others in literature where its performance accurately traces that of the standard centralized Newton approach.

4.4 Accurate Distributed Newton Methods

Using the results of the distributed R-Hop solver, we propose a novel technique requiring only R-Hop communication for the distributed approximation of the Newton direction. Given the results of Lemma 14, we can determine the approximate Newton direction by solving a system of linear equations represented by an SDD matrix777For ease of presentation, we refrain some of the proofs to the appendix. with .

Formally, we consider the following iteration scheme:

| (19) |

with representing the iteration number, the step-size, and denoting the approximate Newton direction. We determine by solving using Algorithm 8. It is easy to see that our approximation of the Newton direction, , satisfies

where approximates according to the routine of Algorithm 8. The accuracy of this approximation is quantified in the following Lemma

Lemma 16.

Let be the Hessian of the dual function, then for any arbitrary we have

Proof.

See Appendix. ∎

4.4.1 Convergence Guarantees

Given such an accurate approximation, next we analyze the iteration scheme of our proposed method showing that similar to standard Newton methods, we achieve superlinear convergence within a neighborhood of the optimal value. We start by analyzing the change in the Laplacian norm of the gradient between two successive iterations

Lemma 17.

Consider the following iteration scheme with , then, for any arbitrary , the Laplacian norm of the gradient, , follows:

| (20) |

with and being the largest and second smallest eigenvalues of , and denoting the upper and lower bounds on the dual’s Hessian, and is defined in Lemma 15.

Proof.

See Appendix. ∎

At this stage, we are ready to present the main results quantifying the convergence phases exhibited by our approach:

Theorem 3.

Let , , be the constants defined in Assumption 2 and Lemma 14, and representing the largest and second smallest eigenvalues of the normalized laplacian , the precision parameter for the SDDM solver, and letting the optimal step-size parameter . Then the proposed algorithm given by the exhibits the following three phases of convergence:

-

1.

Strict Decreases Phase: While :

-

2.

Quadratic Decrease Phase: While :

-

3.

Terminal Phase: When :

where and , with

| (21) |

Proof.

We will proof the above theorem by handling each of the cases separately. We start by considering the case when (i.e., Strict Decrease Phase). We have:

where the last steps holds since . Noticing that (see Appendix), the only remaining step needed is to evaluate . Knowing that , we recognize

where the last step follows from the fact that . Therefore, we can write

It is easy to see that minimizes the right-hand-side of the above equation. Using gives the constant decrement in the dual function between two successive iterations as

Considering the case when (i.e., Quadratic Decrease Phase), Equation 20 can be rewritten as

with and defined as in Equation 21. Further, noticing that since then . Consequently the quadratic decrease phase is finalized by

Finally, we handle the case where (i.e., Terminal Phase). Since , it is easy to see that

∎

4.4.2 Iteration Count and Message Complexity

Having proved the three convergence phases of our algorithm, we next analyze the number of iterations needed by each phase. These results are summarized in the following lemma:

Lemma 18.

Consider the algorithm given by the following iteration protocol: . Let be the initial value of the dual variable, and be the optimal value of the dual function. Then, the number of iterations needed by each of the three phases satisfy:

-

1.

The strict decrease phase requires the following number of iterations to achieve the quadratic phase:

where .

-

2.

The quadratic decrease phase requires the following number of iterations to terminate:

where , with being the first iteration of the quadratic decrease phase.

-

3.

The radius of the terminal phase is characterized by:

Proof.

See Appendix. ∎

Given the above result, the total message complexity can then be derived as:

4.4.3 Comparison to Existing Literature

Recent progress towards distributed second-order methods applied to network flow optimization adopt an approximation scheme based on the properties of the Hessian. Most of these methods (e.g., [7]) handle the simpler consensus setting and thus are not directly applicable to our more general setting. Closest to this work is that proposed in [5], where the authors approximate the Newton direction by truncating the Neumann expansion of the pseudo-inverse of the Hessian. This truncation, however, introduces additional error to the computation of the Newton direction leading to inaccurate results especially on large networks. The primary contrast to this work is that our method is capable of acquiring -close (for any arbitrary ) approximation to the Newton direction. In fact, the proposed method is almost identical to the exact Newton direction computed in a centralized manner (see Section 4.5).

Next, we formally derive the iteration counts for our method on four-special cases as benchmark comparisons. Since the main contribution (due to the presence of term in ) in the iteration count is given by the strict decrease phase (see Lemma 18), we develop these results in terms of . Also note that the corollaries provided below are substantially harder to acquire when compared to the standard Newton analysis due to the dependence of some constants, e.g, and on the graph structure. Opposed to the analysis performed by other methods, our analysis explicitly handles such dependencies leading to more realistic and accurate mathematical insights. This explains the relatively high dependency on in some cases. Note, that in such case where these relations (i.e., parameter dependency on the graph structure) were not taken into account, substantial decrease in the complexity can be achieved at the compensate of accurate mathematical description.

Path Graph:

Corollary 5.

Given a path graph with nodes, the strict-decrease phase of the distributed Newton method is given by:

Grid Graph:

Corollary 6.

For a grid graph the strict-decrease phase of the distributed Newton method is given by:

Scale-Free Graph:

Corollary 7.

For a scale free grid graph with , the strict-decrease phase is given by:

d-Regular Ramanujan Expanders: For such expanders the iteration count for the strict-decrease phase can be bounded by a constant.

4.5 Experiments and Results

We evaluated the proposed distributed second-order method in three sets of experiments on randomly generated and Barbell networks. The goal was to assess the performance on networks exhibiting good and bad mixing times. We compared our algorithm’s performance to: 1) exact-newton computed in a centralized fashion, 2) Accelerated Dual Descent (ADD) with two different splittings [5, 6], 3) dual sub-gradients, and 4) the fully distributed algorithms for convex optimization [41] (FDA). An of , a feasibility threshold of , and an R-Hop of 1 were provided to our SDDM solver for determining the approximate Newton direction. For all other methods free parameters were chosen as specified by the relevant papers. Feasibility and objective values were used as performance measures.

4.5.1 Experiments & Results on Random Graphs

Two experiments on small (20 nodes, 60 edges) and large (50 nodes, 150 edges) random graphs were conducted. The random graphs were constructed in such a way that edges were drawn uniformly at random. The flow vectors, , were chosen to place source and sink nodes apart.

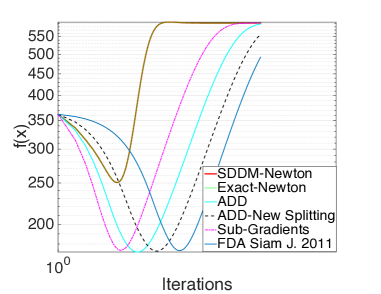

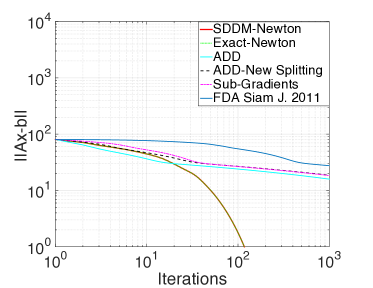

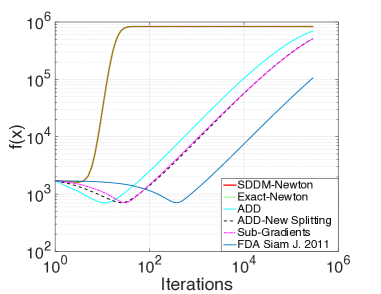

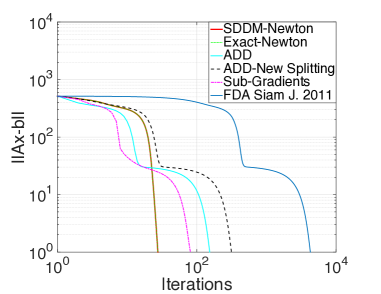

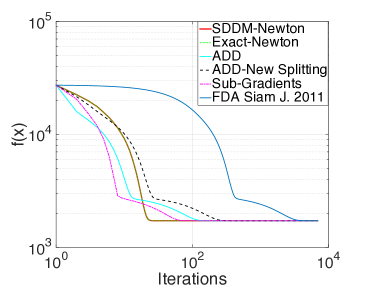

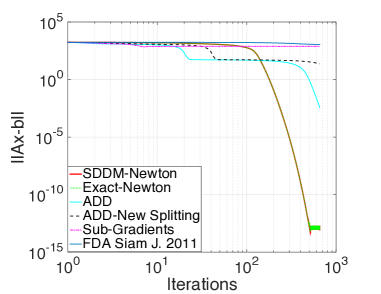

Results summarizing the primal objective value, , and feasibility, , on both networks are shown in Figure 3. On small networks (i.e., 20 nodes and 60 edges), all algorithms perform relatively well. Clearly, our proposed approach (titled SDDM-Newton in the figures) outperforms, ADD, Sub-gradients, and the approach in [41] with about an order of magnitude. Another interesting realization is that SDDM-Newton accurately tracks the exact Newton method with its direction computed in a centralized fashion. The reason for such positive results, is that our algorithm is capable of approximating the Newton direction up-to-any arbitrary while abiding by the R-Hop constraint. For larger networks, Figures 2 and 2, SDDM-Newton is highly superior compared to other approaches. Here, our algorithm is capable of converging in about 3-5 orders of magnitude faster, i.e., we converge in about 3000 iterations as opposed to 6000 for ADD which showed the best performance among the other techniques. It is worth noting that we are again capable of tracing exact Newton due to the accuracy of our approximation.

4.5.2 Experiments & Results on Bar Bell Graphs

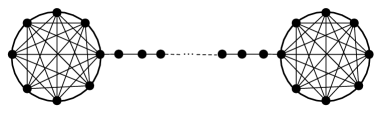

In the second set of experiments we assessed the performance of SDDM-Newton on a barbell graph, Figure 3, of 60 nodes. The graph consisted of two 20 node cliques connected by a 20 nodes line graph is depicted in. We assign directed edges on the graph arbitrary and solve the network flow optimization problem with a cost of .

Results in Figure 4 and 4 demonstrate the superiority of our algorithm to state-of-the-art methods. Here, again we are capable of converting faster than other techniques in about 2 magnitudes faster. It is worth noting that the second-best performing algorithm is ADD which is capable of converging in almost 3000 iterations.

Finally, we repeated the same experiments on a larger bar bell network formed of 120 nodes (two cliques with 40 nodes connected by a 40 node line graph). These results, demonstrated in Figures 5 and 5, again validate the previous performance measures showing even better performance in both the objective value and feasibility.

4.5.3 Measuring Message Complexity

Though successful, the experiments performed in the previous section show accuracy improvements without demonstrating per-iteration message complexities needed. To have a fair comparison to state-of-the-art methods, in this section we report such results on four different network topologies. Here, we show that our method requires a relatively slight increase in message complexity to trace the exact Newton direction.

These per-iteration values were determined by deriving bounds to each of the benchmark algorithms. For all methods except SDDM-Newton and that in [5], such complexity can be bounded by with being the maximal degree. As for SDDM-Newton, the per-iteration complexity is upper-bounded by , with being the condition number of the graph Laplacian. For the algorithm in [5] the message complexity satisfies with being the total number of nodes in . Immediately, we recognize that our algorithm is faster by a factor of compared to that in [5]. Compared to other techniques, however, our method is slower by a factor of .

To better quantify such a difference, we perform four sets of experiments on two randomly generated and two barbell networks with varying size. The random networks consisted of 20 nodes, 60 edges, and 120 nodes and 500 edges, respectively. Moreover, the barbell graphs followed the same construction of the previous section with sizes varying from 60 to 120 nodes. Comparison results showing the logarithm of the message complexity are reported in the bar graph of Figure 6. These demonstrate that SDDM-Newton requires a slight increase in the message complexity to trace the exact Newton direction.

5 Conclusion

In this paper we proposed a distributed solver for linear systems described by SDDM matrices. Our approach distributes that in [11] by proposing the usage of an inverse approximated chain which can be computed in a distributed fashion. Precisely, two solvers were proposed. The first required full communication in the network, while the second restricts communication to the R-Hop neighborhood between the nodes.

We applied our solver to network flow optimization. This resulted in an efficient and accurate distributed second-order method capable of tracing exact Newton computed in a centralized fashion. We showed that similar to standard Newton, our methods are capable of achieving superlinear convergence in a neighborhood of the optimal solution. We extensively evaluated the proposed method on both randomly generated and barbell graphs. Results demonstrate that our method outperforms state-of-the-art techniques.

References

- [1] S. Authuraliya and S. H. Low, Optimization flow control with newton-like algorithm, Telecommunications Systems 15 (200), 345-358.

- [2] D.P. Bertsekas, Nonlinear programming, Athena Scientific, Cambridge, Massachusetts, 1999.

- [3] D.P. Bertsekas, A. Nedic, and A.E. Ozdaglar, Convex analysis and optimization, Athena Scientific, Cambridge, Massachusetts, 2003.

- [4] S. Boyd and L. Vandenberghe, Convex optimization, Cambridge University Press, Cambridge, UK, 2004.

- [5] A. Jadbabaie, A. Ozdaglar, and M. Zargham, A distributed newton method for network optimization, Proceedings of IEEE CDC, 2009.

- [6] M. Zargham, A. Ribeiro, A. Ozdaglar, and A. Jadbabaie, Accelerated Dual Descent for Network Optimization, Proceedings of IEEE, 2011.

- [7] E. Wei, A. Ozdaglar, and A. Jadbabaie, A distributed newton method for network utility maximization, LIDS Technical Report 2823 (2010).

- [8] J. Sun and H. Kuo, Applying a newton method to strictly convex separable network quadratic programs, SIAM Journal of Optimization, 8, 1998.

- [9] R. Tyrrell Rockafellar, Network Flows and Monotropic Optimization, J. Wiley & Sons, Inc., 1984.

- [10] E. Gafni and D. P. Bertsekas, Projected Newton Methods and Optimization of Multicommodity Flows, IEEE Conference on Decision and Control (CDC), Orlando, Fla., Dec. 1982.

- [11] R. Peng, and D. A. Spielman, An efficient parallel solver for SDD linear systems, The 46th Annual ACM Symposium on Theory of Computing2014.

- [12] A. Nedic and A. Ozdaglar, Approximate primal solutions and rate analysis for dual subgradient methods, SIAM Journal on Optimization, forthcoming (2008).

- [13] S. Low and D.E. Lapsley, Optimization flow control, I: Basic algorithm and convergence, IEEE/ACM Transactions on Networking 7 (1999), no. 6, 861-874.

- [14] A. Ribeiro and G. B. Giannakis, Separation theorems of wireless networking, IEEE Transactions on Information Theory (2007).

- [15] A. Ribeiro, Ergodic stochastic optimization algorithms for wireless communication and networking, IEEE Transactions on Signal Processing (2009).

- [16] O. Axelsson, Iterative Solution Methods, Cambridge University Press, New York, NY, USA, 1994.

- [17] D. P. Bertsekas and J. N. Tsitsiklis, Parallel and Distributed Computation: Numerical Methods, Prentice Hall, Inc., Upper Saddle River, NJ, USA, 1989.

- [18] E. G. Boman, B. Hendrickson, and S. A. Vavasis, Solving elliptic finite element systems in near-linear time support preconditioners, SIAM Journal on Numerical Analysis, 2008.

- [19] S. I. Daitch, and D. A. Spielman, Faster Approximate Lossy Generalized Flow via Interior Point Algorithms, In Proceedings of the Annual ACM Symposium on Theory of Computing, 2008.

- [20] A. Madry, Navigating Central Path with Electrical Flows: From Flows to Matching and Back, In Proceedings of the Annual IEEE Symposium On the Theory Of Computing (STOC), 2012.

- [21] X. Zhu, Z. Ghahramani, and J. D. Lafferty, Semi-supervised Learning Using Gaussian Fields and Harmonic Functions, In Proceedings of the International Conference on Machine Learning, 2003.

- [22] D. Zhou, and B. Schoelkopf, A Regularization Framework For Learning from Graph Data, In the Statistical Relation Learning and Its Connections to Other Fields Workshop held at the International Conference on Machine Learning, 2004.

- [23] J.A. Kelner, and A. Madry, Faster Generation of Random Spanning Trees, In Foundations of Computer Science (FOCS), 2009.

- [24] D. A. Spielman, and S.-H. Teng, Nearly-Linear Time Algorithm for Preconditioning and Solving Symmetric Diagonally Dominant Linear Systems, CoPR, 2008.

- [25] A. Joshi, Topics in Optimization and Sparse Linear Systems, University of Illinois at Urbana-Champaign, 1996.

- [26] E. Boman, and B. Hendrickson, Support Theory for Preconditioning, SIAM Journal on Matrix Analysis and Applications, 2003.

- [27] D. A. Spielman, and S.-H. Teng, Spectral Sparsification of Graphs, CoPR, 2008.

- [28] I. Koutis, G. L. Miller, and R. Pend, Approaching optimality for solving SDD systems, CoPR, 2010.

- [29] I. Koutis, G. L. Miller, and R. Pend, Solving SDD linear systems in time , CoPR, 2011.

- [30] J. A. Kelner, and A. Madry, Faster Generation of Random Spanning Trees, CoPR, 2009.

- [31] I. Koutis, and G. L. Miller, A Linear Work, Time, Parallel Algorithm for Solving Planar Laplacians, SODA, 2007.

- [32] G. Belloch, A. Gupta, I. Koutis, G. L. Miller, R. Peng, and K. Tandwongsan, Near Linear-Work Parallel SDD Solvers, Low-Diameter Decomposition, and Low-Stretch Subgraphs, CoPR, 2011.

- [33] J. Liu, S. Mou, and S. A. Morse, An Asynchronous Distributed Algorithm for Solving a Linear Algebraic Equation, In Proceedings of the Annual Conference on Decision and Control (CDC), 2013.

- [34] C. E. Lee, A. Ozdaglar, and D. Shah, Solving Systems of Linear Equations: Locally and Asynchronously, CoPR, 2014.

- [35] W. Casaca, G. Nonato, G. Taubin, Laplacian Coordinates for Seeded Image Segmentation, IEEE Conference on Computer Vision and Pattern Recognition (CVPR), 2014.

- [36] J. Nocedal, and S. J. Wright, Numerical Optimization, Springer, New York, 2006.

- [37] E.F. Kaasschieter, Preconditioned Conjugate Gradients for Solving Singular Systems, Journal of Computational and Applied Mathematics, 1988.

- [38] A. Olshevsky, Linear Time Average Consensus on Fixed Graphs and Implications for Decentralized Optimization and Multi-Agent Control, ArXiv e-prints, 2014.

- [39] Béla Bollobás, Oliver Riordan, Joel Spencer, and Gábor Tusnády, The Degree Sequence of Scale-Free Random Graph Process, Random Structures and Algorithms, 2001.

- [40] Rasul Tutunov, Haitham Bou-Ammar, Ali Jadbabaie, and Eric Eaton On the Degree Distribution of Pólya Urn Graphical Processes, ArXiv e-prints, 2014.

- [41] D. Mosk-Aoyama, T. Roughgarden, and D. Shah, Fully Distributed Algorithms For Convex Optimization Problems, Siam Journal on Optimization 2010.

- [42] C. Couprie, L. Grady, L. Najman, and H. Talbot, Power Watershed: A Unifying Graph-Based Optimization Framework, IEEE Transactions on Pattern Analysis and Machine Intelligence, 2011.

- [43] C. Rother, V. Kolmogorov, A. Blake, GrabCut-Interactive Foreground Extraction using Iterated Graph Cuts, ACM Transactions on Graphics (SIGGRAPH), 2004.

- [44] Y. Boykov, M.-P. Jolly, Interactive Graph Cuts for Optimal Boundary Amp; Region Segmentation of Objects in N-D Images, IEEE International Conference on Computer Vision, 2001.

- [45] L. Grady, Random Walks for Image Segmentation, IEEE Transactions on Pattern Analysis and Machine Intelligence, 2006.

- [46] J. Cousty, G. Bertrand, L. Najman, and M. Couprie, Watershed Cuts: Minimum Spanning Forests and the Drop of Water Principle, IEEE Transactions on Pattern Analysis and Machine Intelligence 2009.

- [47] O. Sorkine, Differential Representations for Mesh Processing, Computer Graphics Forum (Eurographics), 2006.

- [48] K. Xu, H. Zhang, D. Cohen-Or, and Y. Xiong, Dynamic Harmonic Fields for Surface Processing, IEEE International Conference on Shape Modelling and Applications, 2009.

- [49] F. Estrada, A. Jepson, Benchmarking Image Segmentation Algorithms, International Journal of Computer Vision, 2009.

- [50] P. Arbelaez, M. Maire, C. Fowlkes, J. Malik, Contour Detection and Hierarchical Image Segmentation, IEEE Transactions on Pattern Analysis and Machine Intelligence, 2011.

- [51] K. Gremban, Combinatorial Preconditioners for Sparse, Symmetric, Diagonally Dominant Linear Systems, PhD Thesis, Carnegie Mellon University, 1996.

6 SDDM Solver Proofs

In this appendix, we provide the complete and comprehensive proofs specific for the distributed SDDM solver.

Lemma 19.

Let , and . Then is approximate solution of .

Proof.

Lemma 20.

Let be the standard splitting of . Let be the operator defined by (i.e., ). Then

Moreover, Algorithm 3 requires time steps.

Proof.

The proof commences by showing that and have a sparsity pattern corresponding to the r-hop neighborhood for any . This case be shown using induction as follows

-

1.

If , we have

Therefore, has sparsity pattern corresponding to the 1-Hop neighborhood.

-

2.

Assume that has a sparsity patter corresponding to the p-hop neighborhood for all .

-

3.

Now, consider , where

(24) Since is non negative then it is easy to see that if and only if there exists such that and (i.e., ).

For , the same results can be derived similarly.

Please notice that in Part One of DistrRSolve algorithm node computes (in a distributed fashion) the components to using the inverse approximated chain . Formally,

Clearly, at the iteration node requires the row of (i.e., the row from the previous iteration) in addition to the row of from all nodes to compute the row of .

For computing , node requires the row and column of . The problem, however, is that node can only send the row of which can be easily seen not to be see that symmetric. To overcome this issue, node has to compute the column of based on its row. The fact that is symmetric, manifests that for

Hence, for all

| (25) |

Now, lets analyze the time complexity of computing components .

Time Complexity Analysis: At each iteration , node receives the row of from all nodes . using Equation 25, node computes the corresponding columns as well as the product of these columns with the row of . Therefore, the time complexity at the iteration is , where is responsible for the row computation, and represents the communication cost between the nodes. Using the fact that , the total complexity of Part One in DistrRSolve algorithm is .

In Part Two, node computes (in a distributed fashion) using the same inverse approximated chain .

| (26) | ||||

for . Thus,

Similar to the analysis of Part One of DistrRSolve algorithm the time complexity of Part Two as well as the time complexity of the whole algorithm is .

Finally, using Lemma 5 for the inverse approximated chain yields:

∎

Lemma 21.

Let be the standard splitting. Further, let in the nverse approximated chain . Then requires iterations to return the component of the close approximation for .

Proof.

Lemma 22.

Let be the standard splitting. Further, let in the inverse approximated chain . Then, requires time steps.

Proof.

Each iteration of DistrESolve algorithm calls DistRSolve routine, therefore, using the above the total time complexity of f DistrESolve algorithm is time steps ∎

Lemma 23.

Let be the standard splitting. Further, let . Then Algorithm 8 requires iterations to return the component of the close approximation to .

Proof.

Please note that the iterations of EDistRSolve correspond to a distributed version of the preconditioned Richardson iteration scheme

with and being the operator defined by RDistRSolve. From Lemma 3.8 it is clear that . Applying Lemma 2.12, provides that EDistRSolve requires iterations to return the component of the close approximation to . Finally, since EDistRSolve uses procedure RDistRSolve as a subroutine, it follows that for each node only communication between the R-hope neighbors is allowed. ∎

Lemma 24.

Let be the standard splitting and let , then EDistRSolve requires time steps. Moreover, for each node , EDistRSolve only uses information from the R-Hop neighbors.

Proof.

Notice that at each iteration EDistRSolve calls RDistRSolve as a subroutine, therefore, for each node only R-hop communication is allowed. Lemma 3.8 gives that the time complexity of each iteration is , and using Lemma 3.9 immediately gives that the time complexity of . ∎

7 Distributed Newton Lemmas

Lemma 25.

The dual objective abides by the following two properties [6]:

-

1.

The dual Hessian, , is a weighted Laplacian of :

-

2.

The dual Hessian is Lispshitz continuous with respect to the Laplacian norm (i.e., ) where is the unweighted laplacian satisfying with being the incidence matrix of . Namely, :

with where and denote the largest and second smallest eigenvalues of the Laplacian .

Proof.

For the first part see Lemma 1 in [6]. So, lets prove the second part:

Lets denote , then:

| (27) |

Using that lets fix some and consider the expression :

We used in step (1) , and in step (2) we used that . Therefore, we have:

| (28) |

Now, we upper bound the expression :

| (29) | ||||

In the last transition we used Assumption 2. Now, using formulae for the derivative of the inverse function we have:

| (30) |

Hence, is bounded, and therefore is Lipshittz continuous with constant . Now, because , we have that is Lipshitz continuous with corresponding constant . Hence, :

| (31) |

Now we are ready to prove the following

Claim: For all and for any :

| (32) |

Proof.

Consider three cases:

-

1.

. In this case, using that

in (31): - 2.

-

3.

, where . In this case , and . Notice that the same expression for will be in the case when . Hence, using the first case which proves the claim:

∎

Lemma 26.

If the dual Hessian is Lipschitz continuous with respect to the Laplacian norm (i.e., Lemma 7), then for any and we have

Proof.

We apply the result of Fundamental Theorem of Calculus for the gradient which implies for any vectors and in we can write

| (34) |

We proceed by adding and subtracting to the integral in the right hand side of (34). It follows that

| (35) | ||||

we can separate the integral in (35) into two integrals as

| (36) | ||||

The second integral in the right hand side of (36) does not depend on and we can simplify the integral as . This simplification implies that we can rewrite (36) as

| (37) | ||||

By rearranging terms in (37) and taking the norm of both sides we obtain

| (38) | ||||

Now we are ready to prove the following

Claim: Let be the Hessian of the dual function . Then, for any :

| (39) |

Proof.

Applying the above claim to (38) gives:

where in step (1) we used the fact that is Lipshitz continuous with respect to the laplacian norm . ∎

Lemma 27.

Let be the Hessian of the dual function, then for any arbitrary we have

Proof.

Lets be the collection of eigenvalues of and are corresponding eigenvectors. Then

| (40) |

where we use and . Now lets fix some and consider the matrix . The corresponding linear system will have the form:

| (41) |

and the operator defined by by EDistRSolve routine for (41) satisfies:

| (42) |

Notice that . Hence, taking in (42):

| (43) |

The last step is to take the limit in (43) and notice that :

∎

Lemma 28.

Consider the following iteration scheme with , then, for any arbitrary , the Laplacian norm of the gradient, , follows:

| (44) |

with and being the largest and second smallest eigenvalues of , and are constants from Assumption 2, and is defined previously.

Proof.

Because the dual function has Hessian which is Lipschitz continuous with respect to the laplacian norm , we can write:

| (45) |

Using can be rewritten as:

| (46) |

Therefore,

| (47) |

Since . Let , then:

| (48) |

and

| (49) | ||||

Therefore, we need to evaluate :

Hence,

| (50) |

Combining the above gives:

| (51) |

Therefore, we have:

∎

Lemma 29.

Consider the algorithm given by the following iteration protocol: . Let be the initial value of the dual variable, and be the optimal value of the dual function. Then, the number of iterations needed by each of the three phases satisfy:

-

1.

The strict decrease phase requires the following number iterations to achieve the quadratic phase:

where .

-

2.

The quadratic decrease phase requires the following number of iterations to terminate:

where , with being the first iteration of the quadratic decrease phase.

-

3.

The radius of the terminal phase is characterized by:

Proof.

We will start with strict decrease phase. From Theorem 1:

| (52) |

where , with:

Hence:

| (53) | |||

Now, notice that:

Moreover, because , therefore:

| (54) |

Therefore, we can write:

| (55) | ||||

| (56) | ||||

Denote

then from (55) we have:

Hence, the number of iterations required by the algorithm for the strict decrease phase is upper-bounded by:

where - optimal value of dual function.

Now, lets analyze the quadratic decrease phase. We have, for :

Hence,

| (57) |

Now, denote be the first iteration when quadratic phase is achieved, i.e , therefore, for iteration:

where we use notation . Hence, the number or iterations ADD-SDDM algorithm requires to reach terminal phase is given by the following condition:

which immediately gives:

Hence,

Finally lets consider the radius of the terminal phase:

∎