Risk aggregation with empirical margins: Latin hypercubes, empirical copulas, and convergence of sum distributions

Abstract

This paper studies convergence properties of multivariate distributions

constructed by endowing empirical margins with a copula.

This setting includes

Latin Hypercube Sampling with dependence, also

known as the Iman–Conover method.

The primary question addressed here is the convergence of the component sum,

which is relevant to risk aggregation in insurance and finance.

This paper shows that a CLT for the aggregated risk

distribution is not available, so that the underlying mathematical problem

goes beyond classic functional CLTs for empirical copulas.

This issue is relevant to Monte-Carlo based risk aggregation in

all multivariate models generated by plugging empirical margins into

a copula.

Instead of a functional CLT,

this paper establishes strong uniform consistency of

the estimated sum distribution function and provides a sufficient criterion

for the convergence rate in probability.

These convergence results hold for all copulas with bounded densities.

Examples with unbounded densities

include bivariate Clayton and Gauss copulas.

The convergence results are not specific to the component

sum and hold also for any other componentwise non-decreasing aggregation

function.

On the other hand, convergence of estimates for the joint distribution

is much easier to prove, including CLTs.

Beyond Iman–Conover estimates, the results of this paper

apply to multivariate distributions obtained by

plugging empirical margins into

an exact copula or by plugging exact margins into an empirical copula.

Key words: Risk aggregation, empirical marginal distributions, empirical copula, functional CLT, Iman–Conover method, Latin hypercube sampling

1 Introduction

In various real-world applications, multivariate stochastic models are constructed upon empirical marginal data and an assumption on the dependence structure between the margins. This dependence assumption is often formulated in terms of copulas. The major reason for this set-up is the lack of multivariate data sets, as it is often the case in insurance and finance. This approach may appear artificial from the statistical point of view, but it arises naturally in the context of stress testing. In addition to finance and insurance, relevant application areas include engineering and environmental studies. Sometimes the marginal data is not even based on observations, but is generated by a univariate model that is considered reliable. Many of these models are so complex that the resulting distributions cannot be expressed analytically. In such cases exact marginal distributions are replaced by empirical distributions of simulated univariate samples. These empirical margins are endowed with some dependence structure to obtain a multivariate distribution. The computation of aggregated risk or other characteristics of this multivariate model is typically based on Monte-Carlo techniques.

Iman–Conover: dependence “injection” by sample reordering

Related methods include generation of synthetic multivariate samples from univariate data sets. Whilst the margins of such a synthetic sample accord with the univariate data, its dependence structure is modified to fit the application’s needs. The most basic example is the classic Latin Hypercube Sampling method, which mimics independent margins. It is a popular tool for removing spurious correlations from multivariate data sets. This method is also applied to variance reduction in the simulation of independent random variables (cf. McKay et al., 1979; Stein, 1987; Owen, 1992; Iman, 2008). Similar applications to dependent random variables include variance reduction in Monte-Carlo methods (Packham and Schmidt, 2010) and in copula estimation (Genest and Segers, 2010).

An extension of Latin Hypercube Sampling that brings dependence into the samples was proposed by Iman and Conover (1982). The original description of the Iman–Conover method uses random reordering of marginal samples, and the intention there was to control the rank correlations in the synthetic multivariate sample. The reordering is performed according to the vectors of marginal ranks in an i.i.d. sample of some multivariate distribution, say, , with continuous margins. Thus rank correlations of are “injected” into the synthetic sample. This procedure is equivalent to plugging empirical margins (obtained from asynchronous observations) into the rank based empirical copula of a sample of (Arbenz et al., 2012). Moreover, it turned out that the Iman–Conover method allows to introduce not only the rank correlations of into the synthetic samples, but the entire copula of (cf. Arbenz et al., 2012; Mildenhall, 2005). In somewhat weaker sense, these results are related to the approximation of stochastic dependence by deterministic functions and to the pioneering result by Kimeldorf and Sampson (1978). Further developments in that area include measure preserving transformations (Vitale, 1990) and shuffles of (Durante et al., 2009). In statistical optimization, reordering techniques were also used by Rüschendorf (1983). A very recent, related application in quantitative risk management is a rearrangement algorithm that computes worst-case bounds for the aggregated loss quantiles in a portfolio with given marginal distributions (cf. Embrechts et al., 2013, and references therein).

Using explicit reorderings of univariate marginal samples, the Iman–Conover method has a unique algorithmic tractability. It is implemented in various software packages, and it serves as a standard tool in dependence modelling and uncertainty analysis. The reordering algorithm allows even to construct synthetic samples with hierarchical dependence structures that meet the needs of risk aggregation in insurance and reinsurance companies (Arbenz et al., 2012). The distribution of the aggregated risk is estimated by the empirical distribution of the component sums of the synthetic samples for . This Monte-Carlo approach has computational advantages. The resulting convergence rate of (or even faster with Quasi-Monte-Carlo using special sequences) allows to outperform explicit calculation of sum distributions already for moderate dimensions (cf. Arbenz et al., 2011).

Challenge and contribution: convergence proofs

Despite its popularity, some applications of the Iman–Conover method have been justified by simulations rather than by mathematical proofs. The original publication (Iman and Conover, 1982) derives its conclusions from promising simulation results for the distribution of the following function of a -dimensional random vector: . Yet a rigorous proof is still missing. The present paper provides a convergence proof for Iman–Conover estimates of the component sum distribution. It also includes a proof sketch for the much simpler case of the estimated joint distribution. Both problems have been open until now.

The solutions given in this paper are derived from the empirical process theory as presented in van der Vaart and Wellner (1996). Under appropriate regularity assumptions, Iman–Conover estimates of the sum distribution are strongly uniformly consistent with convergence rate (see Theorems 4.1 and 4.2). The convergence of Iman–Conover estimates for the joint distribution is discussed in cf. Remark 4.8. All these findings are not specific to the component sum and extend immediately to all componentwise non-decreasing functions (see Corollary 4.10). Moreover, Theorems 4.1 and 4.2 also cover the convergence of aggregated risk distributions obtained by Monte-Carlo sampling of a multivariate model constructed by plugging empirical margins into a copula (see Remark 4.9). In fact, both sampling methods (reordering by Iman–Conover and classic top-down sampling with empirical margins instead of the exact ones) lead to the same mathematical problem. This is discussed in Remark 3.2(d).

The regularity assumptions used here to establish the convergence rate for Iman–Conover estimates of sum distributions are satisfied for all copulas with bounded densities. This case includes the independence copula in arbitrary dimension . The assumptions are also satisfied for all bivariate Clayton copulas and for bivariate Gauss copulas with correlation parameter . The convergence rate for is, if at all, only slightly weaker. The best bound that is currently available for is .

The regularity assumptions for the marginal distributions involved in the Iman–Conover method are absolutely natural, and they are always satisfied by empirical distribution of i.i.d. samples: Strong uniform consistency of Iman–Conover estimates needs strong uniform consistency of consistency of empirical margins, whereas the uniform convergence rate of Iman–Conover requires the same uniform convergence rate of in the margins.

Why a precise CLT remains elusive

The convergence results obtained here are related to standard convergence results for empirical copulas (cf. Rüschendorf, 1976; Deheuvels, 1979; Fermanian et al., 2004; Segers, 2012). However, the mathematical problem for the sum distribution goes beyond the standard setting, where empirical measures are evaluated on rectangular sets. In the case of sum distributions, the usage of empirical margins in the construction of the multivariate model significantly extends the class of sets on which the empirical process of the copula sample should converge. As shown in Section 3, the canonical way to prove asymptotic normality for the Iman–Conover estimator of the sum distribution would need a uniform CLT for the copula sample on the collection of so-called lower layers in . However, this class is too complex for a uniform CLT (cf. Dudley, 1999, Theorems 8.3.2, 12.4.1, and 12.4.2). For this reason the proofs of consistency and convergence rate presented here sacrifice the precise asymptotic variance and use approximations that allow to simplify the problem. This technical difficulty is not specific to the Iman–Conover method. It also arises in any other application where multivariate samples are generated from a simulated copula sample and empirical marginal distributions. As mentioned above, this approach is very popular in practice, especially for computational reasons. Similar problems also arise in applications that combine exact marginal distributions with empirical copulas.

Structure of the paper

The paper is organized as follows. Section 2 introduces the reordering method and highlights the relations between sample reordering and empirical copulas. The complexity issues are discussed in Section 3. The convergence results are established in Section 4. The underlying regularity assumptions are discussed in Section 5, including examples of copula families that satisfy them. Conclusions are stated in Section 6.

2 Empirical copulas and sample reordering

Let be a random vector in with joint distribution function , marginal distribution functions , and copula . That is,

| (1) |

where is a probability distribution function on with uniform margins. By Sklar’s Theorem, any multivariate distribution function admits this representation.

We assume throughout the following that are unknown and that we have some uniform approximations , . The true margins need not be continuous. In this case the representation (1) is not unique, but it is not an issue in our application, which is rather computational than statistical. As sketched in the Introduction, we consider the case where only univariate, asynchronous observations of the components are available, and the copula is set by expert judgement to compute the resulting distribution of the component sum. In practice, the choice of the copula aims at dependence characteristics that are known or assumed for the random vector . This choice also depends on the ability to sample or any other multivariate distribution with continuous margins and copula .

To keep the presentation simple, we assume that are empirical distribution functions of some univariate samples for :

| (2) |

These samples need not be i.i.d. We will only assume that , either -a.s. or in probability. Extensions to the general case will be given later on.

Let denote the order statistics of the -th component for , and let denote the probability measure with distribution function . The Iman–Conover method approximates by the empirical measure of the following synthetic multivariate sample:

| (3) |

where for are the marginal ranks of a simulated i.i.d. sample :

It is easy to verify (cf. Arbenz et al., 2012, Theorem 3.2) that the empirical distribution function of the synthetic sample (3) is equal to

| (4) |

where is the rank based empirical copula of :

| (5) |

This links the convergence of the Iman–Conover method to the convergence of to , and hence to the convergence of to .

Remark 2.1.

-

(a)

The central application of the Iman–Conover method discussed in the present paper is the computation of the aggregated risk distribution. The most common risk aggregation function is the sum. In this case one must compute the probability distribution of the random variable for with defined in (1). Iman–Conover involves two approximations: replacing the unknown margins by their empirical versions , and replacing the known (or treated as known) copula by its empirical version .

-

(b)

Using may appear unnecessary because one can also compute the sum distribution for a random vector with margins and exact copula . However, computation of sum distributions from margins and copulas is quite difficult in practice. It involves numeric integration on non-rectangular sets, which cannot be reduced to taking the value of for a few points . Implementations of this kind are exposed to the curse of dimensions. Monte-Carlo methods, which Iman–Conover belongs to, have the convergence rate of , and Quasi-Monte-Carlo methods using special sequences may even allow to achieve the rate . According to Arbenz et al. (2011), explicit computation of sum distributions is outperformed by Monte-Carlo already for .

-

(c)

Another motivation of the Iman–Conover method is its flexibility and algorithmic tractability. It only includes reordering of samples and works in the same way for any dimension. Moreover, sample reordering is compatible with hierarchical dependence structures that can be described as trees with univariate distributions in leaves and copulas in branching nodes (cf. Arbenz et al., 2012). In each branching node, the marginal distributions are aggregated according to the node’s copula and the resulting aggregated (typically, sum) distribution is propagated to the next aggregation level. As shown in Arbenz et al. (2012), sample reordering can be implemented for a whole tree. The setting with one copula and margins discussed in the present paper is the basic element of such aggregation trees. The results presented here allow to prove the convergence of the aggregated (say, sum) distribution in every tree node, including the total sum.

Now let us return to the technical details of the Iman–Conover estimator for the aggregated sum distribution. As the random variables are continuously distributed, they have no ties -a.s. Thus consists -a.s. of atoms of size . Moreover, these atoms build a Latin hypercube on the -variate grid , i.e., each section for and contains precisely one atom. Therefore the Iman–Conover method is also called Latin Hypercube Sampling with dependence.

For , let denote the distribution function of the component sum: , . The relation between and can be expressed as follows.

Lemma 2.2.

| (6) |

where , , and

The notation refers to the closed -dimensional interval between and : .

Proof.

Let and denote

for , where is the quantile function of . It is well known that . Hence

and it suffices to show that is equivalent to .

If , then . Due to for all this implies that .

If , then (componentwise) for some . Since for all , this yields . As the function is componentwise non-decreasing, we obtain that . ∎

Remark 2.3.

-

(a)

The measurability of follows from the equivalence of and .

-

(b)

The purpose of the operator is to guarantee that for and the componentwise ordering implies . This immediately yields . Consistently with Dudley (1999), we will call the lower layer of . This set class is also mentioned in the context of nonparametric regression (cf. Wright, 1981, and references therein).

-

(c)

The sets are closed if the marginal distributions have bounded domains, but not necessarily in the general case. If, for instance, are standard normal distributions, then . This example with punctured corners is quite prototypical. It is easy to show that if a sequence in converges to , then is on the boundary of . Indeed, if , then for sufficiently large . This allows to construct a sequence such that and for all . For any there exists such that . As is non-decreasing and for all , we have and hence for all . Since all are left continuous on , we obtain and . As for all , we obtain . Thus is only possible for .

By construction, includes all points such that for some unit vector , , and . Thus the area where the set does not include its boundary points is very small.

Let us now return to the estimation of the sum distribution . The empirical distribution of the component sum in the synthetic sample (3) is nothing else than the empirical multivariate distribution of this sample evaluated at the sets :

| (7) | ||||

Analogously to (6), can be written in terms of the empirical copula defined in (5) and, as next step, in terms of the empirical distribution of the i.i.d. copula sample :

Let denote the margins of , and let denote the corresponding quantile functions. To avoid technicalities, we consider as mappings from to :

Denote and , where . Then we can state the following result.

Corollary 2.4.

| (8) |

and, with probability ,

| (9) |

Proof.

It is easy to see that the synthetic sample (3) can be written as

where and . This yields

| (10) |

According to the proof of Lemma 2.2, is equivalent to . Hence (10) implies

which is the same as (8) because is the empirical distribution function of .

Being continuously distributed, have different values -a.s. for each . Hence the mapping is componentwise -a.s. strictly increasing on with probability , and therefore

Thus (9) follows from and . ∎

Remark 2.5.

Uniform consistency of and implies in .

3 Complexity of the problem

The representation (9) translates the asymptotic normality of into a CLT for uniformly on the random set sequence . The canonical way to prove results of this kind is to establish a uniform CLT on the set class of all possible and . This is the natural set class to work with if are unknown and estimated empirically. The index in the notation highlights the dimension. Since need not be continuous, the set of all includes all , so that is simply the collection of all possible . Furthermore, if each unknown margin has a positive density on entire , then the resulting empirical distributions can take any value in the class of all possible stair functions on with steps of size going from to . In this case the class of all possible is dense (w.r.t. Hausdorff metric) in the class of all possible . Thus, even though there is only one limit transformation that really matters to us, considering the class of all possible does not add more complexity to the problem.

It is also easy to see that even pointwise asymptotic normality of in some would require a uniform CLT on . Shifting the unknown margins , one can easily generate all possible sets from a single . Thus the complexity of the problem is the same for the uniform and for the pointwise asymptotic normality of .

There are various functional CLTs for empirical copulas (cf. Rüschendorf, 1976; Deheuvels, 1979; Fermanian et al., 2004; Segers, 2012, and references therein). However, empirical copula estimates are empirical measures evaluated on the set class of rectangle cells for . This set class is simple enough to be universally Donsker. A set class is called -Donsker if the empirical measure of an i.i.d. sample satisfies

| (11) |

as a mapping in , where is the so-called Brownian bridge “with time” . That is, is a centred Gaussian process with index and covariance structure

The Donsker property of is called universal if it holds for any probability measure on the sample space.

The symbol in (11) refers to the extended notion of weak convergence for non-measurable mappings in as used in van der Vaart and Wellner (1996). See Remark 4.5 for further details.

Sufficient conditions for a set class to be Donsker can be obtained from the entropy of this set class. Entropy conditions can be formulated in terms of covering numbers or bracketing numbers (cf. van der Vaart and Wellner, 1996, Sections 2.1 and 2.2). Entropy bounds that do not depend on the underlying probability measure are called uniform. The most common sufficient criterion for uniform entropy bounds guaranteeing that a set class is universally Donsker is the Vapnik–C̆ervonenkis (VC) property. A set class is VC if it does not shatter any -point set for sufficiently large . The set is shattered by if every subset can be obtained as with some . The smallest such that no -point set is shattered by is called VC-index of .

It is well known that the set class is VC with index (cf. van der Vaart and Wellner, 1996, Example 2.6.1). This yields asymptotic normality of uniformly in . The asymptotic normality of empirical copulas follows then by functional Delta method. These functional CLTs allow to prove asymptotic normality for the estimators of the multivariate distribution function that are derived from or .

Unfortunately, the problem for is much more difficult. As shown above, a functional CLT for is closely related to a uniform CLT for on the set class . The complexity of is much higher than that of . Lemma 3.1 stated below implies that is not VC, and Remark 3.2(c) shows that the complexity of this set class is even so high that a uniform CLT on does not hold.

Let denote the collection of all lower layers in :

and denote . Analogously, denote . According to Remark 2.3(c), implies that , which is a -null set for any copula . Thus, for empirical processes constructed from copula samples, uniform convergence on is equivalent to uniform convergence on .

It is obvious that . The following result shows that for these set classes are almost identical.

Lemma 3.1.

If , then , where is the union of lower faces of .

Proof.

Denote . It suffices to find probability distribution functions such that with . Denote

and

Since , the function is non-decreasing in . Indeed, if , then for any , and hence . The maximal value of is , and is right continuous because is closed. Thus is a probability distribution function.

As and are non-decreasing, we have

where is the boundary of . Now observe that

Hence is the area enclosed between the zero line and the graph of for . This is precisely . ∎

Remark 3.2.

-

(a)

Since is a -null set for any copula , the modification of into in Lemma 3.1 has no influence on the uniform convergence of empirical processes obtained from copula samples.

-

(b)

The set classes and are not VC. For instance, they shatter all sets for . Any subset of this hyperplane in can be picked out by . Similar arguments apply to the modified set class . Hence Lemma 3.1 implies that is not VC. This rules out the canonical usage of VC criteria in convergence proofs for .

-

(c)

The problem is even more difficult, and also more remarkable. In fact, the set classes and for are not Donsker with respect to the Lebesgue measure on (cf. Dudley, 1999, Theorems 8.3.2, 12.4.1, and 12.4.2). Thus Lemma 3.1 implies that a uniform CLT on does not hold in the most basic case, when is the independence copula. Therefore one cannot prove asymptotic normality of via uniform CLT on , and precise asymptotic variance of also seems out of reach.

-

(d)

The complexity issues are not specific to the estimator obtained by plugging empirical margins into the rank based empirical copula . They also affect models generated by plugging directly into the “exact” copula . Top-down simulation of such models means marginal transformation of copula samples by . The resulting estimate of the component sum distribution can be written as where . The sets feature the same stair shape as the sets . Asymptotic normality of leads us again to a uniform CLT on .

-

(e)

It is not yet clear whether Lemma 3.1 can be extended to for . However, the complexity of can only increase for greater . It is easy to embed in for by identifying with the following subclass:

Setting for in the proof of Lemma 3.1, the result obtained there can be extended to for . This allows to extend the conclusions in (b,c,d) to all dimensions .

Remark 3.3.

-

(a)

The results of this section can be summarized as follows: The true target set class is simple (it will be shown in Remark 4.12 that is VC with index 2), but unknown. Replacing these unknown margins by the empirical ones, we obtain random elements of the set class , which is too complex for a uniform CLT. This is the reason why the convergence proofs presented below sacrifice precise asymptotic variance. The resulting loss of precision can be considered as the price one is forced to be pay for using empirical margins instead of the true ones.

-

(b)

Similar issues can also arise when the margins are known, but the copula is not. The implicit use of transformations in (cf. proof of Corollary 2.4) entails deformations of target sets that are very similar to the ones caused by or . Thus, depending on the application, loss of precision may also be caused by the use of an empirical copula. In particular, a uniform CLT for on the set class is still an open problem, and the foregoing results suggest a plausible explanation why this problem is so hard.

-

(c)

A deeper reason behind these complexity issues is the typical shape of the target sets . If the margins or the copula are estimated empirically, corresponding random transformations of ( and in Corollary 2.4) significantly increase the complexity of the problem. Depending on the application, the resulting loss of precision can be attributed to empirical margins, empirical copulas, or both.

4 Convergence results

The major problem studied in this paper is the uniform convergence of the Iman–Conover estimator introduced in (7). Strong consistency in is established in Theorem 4.1. A sufficient condition for the convergence rate to be is given in Theorem 4.2. These results are stated below and followed by some corollaries, remarks, and auxiliary results needed in the proofs. The technical proofs of the auxiliary results are provided in Section 4.1.

Theorem 4.1.

As discussed in Remark 3.2(c), a CLT for seems out of reach, so that the convergence rate is established as an bound. This notation is related to tightness: means that is tight, and is equivalent to . In particular, if and , then .

The regularity assumptions also need some additional notation. In the following, let denote the “upper” boundary of :

and let denote the closed -neighbourhood of in Euclidean distance:

| (13) |

One of the regularity assumptions in Theorem 4.2 specifies the probability mass that the copula assigns to . The other one involves the Lebesgue density of . For , we denote

The growth of for specifies the behaviour of near the boundary of .

Theorem 4.2.

Remark 4.3.

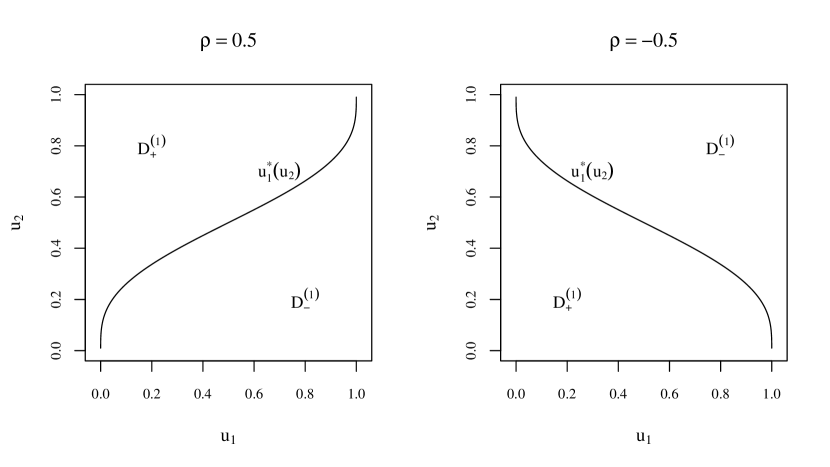

The shapes of the sets strongly depend on the marginal distributions . Two examples of set families are given in Figure 1. The verification of (15) for some copula families is discussed in Section 5. The examples presented there suggest that this condition is non-trivial, and that it depends on the interplay between the copula and the true, unknown margins .

We proceed with an auxiliary result that gives us an upper bound for the volume of . It follows from the componentwise monotonicity of the transformation . The general idea behind this result is that the “surface area” of is bounded by the sum of its projections on the lower faces of the unit square , and the “thickness” of is roughly . The proof is given in Section 4.1.

Lemma 4.4.

Let denote the Lebesgue measure on . Then .

The next lemma provides the Glivenko–Cantelli and Donsker properties for two set classes involved in the proofs of Theorems 4.1 and 4.2. The Donsker property is defined in (11). A set class is called -Glivenko–Cantelli if the empirical measure of an i.i.d. sample satisfies

| (17) |

This notation emphasizes that the convergence also depends on the true distribution that is sampled to construct .

Remark 4.5.

One technical aspect of (17) and (11) needs an additional comment. These statements regard and as mappings from the probability space to . However, need not be measurable with respect to the Borel -field on (cf. Billingsley, 1968, Chapter 18). This issue can be solved by extended versions of almost sure and weak convergence as presented in van der Vaart and Wellner (1996). In the following, and are understood according to that monograph. In case of measurability these extended notions coincide with the standard ones.

Lemma 4.6.

-

(a)

The set class

for a fixed is universally Glivenko–Cantelli and Donsker.

-

(b)

If is Lebesgue absolutely continuous, then the set class

is -Glivenko–Cantelli for any .

-

(c)

If is Lebesgue absolutely continuous and satisfies (16), then is -Donsker for any .

The proof of this auxiliary result is given in Section 4.1. Now we proceed with the proofs of Theorems 4.1 and 4.2.

Proof of Theorem 4.1.

For the sake of simplicity, we will write instead of for any measure on . According to (9), we have to show that uniformly in . It is easy to see that

| (18) |

where denotes the symmetric difference: . According to Lemma 4.6(a), the set class is -Glivenko–Cantelli. Hence the second term in (18) converges to -a.s. uniformly in .

Now consider the first term in (18) and denote

| (19) |

As the transformations and are componentwise non-decreasing, is a measurable random variable. Furthermore, symmetry arguments give us , where for . Hence (12) and the classic Glivenko-Cantelli theorem for yield in . This implies that .

Proof of Theorem 4.2.

According to (18) and (20), we have that

| (22) |

The second term in (22) is uniformly in due to Lemma 4.6(a).

The following corollary allows to replace the empirical marginal distributions in Theorems 4.1 and 4.2 by any other consistent approximations of the true, unknown margins .

Corollary 4.7.

Proof.

Remark 4.8.

-

(a)

Compared to , the multivariate distribution function obtained by plugging into is much easier to handle. The deeper reason here is that can be written as the empirical measure indexed with random elements of the rectangle set class . In particular, if are defined according to (2), then, analogously to (9), we have

(26) As mentioned above, is VC, and hence universally Donsker and Glivenko–Cantelli. Thus, due to , we can apply standard results to .

-

(b)

To prove strong consistency of , recall that any copula is a Lipschitz function with Lipschitz constant (cf. Nelsen, 2006, Theorem 2.2.4). Therefore (26) yields

(27) As mentioned below (19), assumption (12) implies that . Hence -a.s. due to the classic Glivenko–Cantelli Theorem for empirical distribution functions. The extension to general is analogous to Corollary 4.7(a).

- (c)

-

(d)

If satisfy a functional CLT, then the functional Delta method yields a functional CLT for , with precise asymptotic variance – see van der Vaart and Wellner (1996, Lemma 3.9.28) and Segers (2012) for further details. Unfortunately, this does not imply a functional CLT for , as is obtained by indexing with a totally different set class.

Remark 4.9.

Theorems 4.1 and 4.2, along with all their extensions and corollaries, also apply to multivariate models generated by plugging empirical margins directly into the copula . According to Remark 3.2(d), the resulting estimator of can be written as with . Since , extension of convergence results to is straightforward. A closer look at the proof of Corollary 2.4 suggests that same is true for the convergence of uniformly in , where and . This setting corresponds to the combination of exact margins with the empirical copula .

The final result in this section generalizes all foregoing results to a broader class of aggregation functions. Revising the proofs above, it is easy to see that the only property of the component sum used there is that it is componentwise non-decreasing. This immediately yields the following extension.

Corollary 4.10.

Let a function satisfy

Then all results stated above for the sum distribution also hold for the distribution function of the aggregated random variable . In particular, the estimator converges -a.s. to in under the assumptions of Theorem 4.1 and has convergence rate under the assumptions of Theorem 4.2.

Remark 4.11.

-

(a)

It depends on the aggregation function whether the generalization stated above is advantageous. In some special cases even stronger results are possible. If, for instance, , then the convergence of in is related to the uniform convergence of the empirical measure on the rectangle set class . As the latter set class is VC, one can derive a Donsker Theorem for with a precise asymptotic variance.

-

(b)

Another remarkable example is the Kendall process, which is obtained by taking the joint distribution function as aggregating function . The resulting aggregated distribution function is . Using the notation from above, this means for . The aggregated distribution function can be estimated by the empirical distribution , where are the Iman–Conover synthetic variables defined in (3) and is their empirical distribution function (cf. (4)). If the margins are continuous, then has the same distribution as for . Moreover, can always be written as for . Thus the distribution of the process does not depend on the margins . In this case asymptotic normality is also available (cf. van der Vaart and Wellner, 2007; Ghoudi and Rémillard, 1998; Barbe et al., 1996).

- (c)

4.1 Proofs of auxiliary results

Proof of Lemma 4.4.

Denote

and, subsequently,

The notation for and represents a shift of the set , i.e., . Further, denote

The boundaries of are Lebesgue null sets, because any for is Lebesgue-boundary-less. Indeed, the construction of guarantees that if and , then (componentwise) implies . Analogously, if and with , then . This monotonicity property allows to cover the boundary by -dimensional cubes with edge length for any . The total volume of this coverage is , so that sending we obtain . This implies that all sets and are Lebesgue-boundary-less.

It is obvious that . Moreover, the construction of entails that

and for all . This yields . ∎

Proof of Lemma 4.6.

According to van der Vaart and Wellner (1996, Theorem 2.4.1), a set class is -Glivenko–Cantelli if the bracketing number is finite for any . The number is the minimal amount of so-called -brackets needed to cover . An -bracket with respect to is a pair of sets satisfying and . A set class is covered by brackets , , if each satisfies for some . The criterion cited above is stated in terms of function classes, but it easily applies to set classes by identifying sets with their indicator functions.

A sufficient condition for to be -Donsker is

| (28) |

(cf. van der Vaart and Wellner, 1996, Section 2.5.2). The distance of two sets and in is related to their distance in via

Hence the bracketing entropy condition (28) is equivalent to

| (29) |

Part (a). The set class is the collection of all for with a fixed . Since the sets are increasing in , and is componentwise non-decreasing, we have for . Consequently, can be covered by brackets of size with respect to for any probability measure on . The brackets can be chosen as , with an appropriate finite sequence . If has jumps, then it may be difficult to choose such that for all . In this case we may have for some , but the total number of brackets is still . Thus we have

and is universally Glivenko–Cantelli. If the maximal bracket size is , then one needs brackets to cover . This is sufficient for (29), and hence is universally Donsker.

Remark 4.12.

It is also easy to show that the set class is VC with index . As the sets are increasing in , they cannot shatter any two-point set. Let , and let be such that for is equivalent to . Without loss of generality let . Then cannot pick out , and hence is VC. From here, universal Glivenko–Cantelli and Donsker properties follow if we verify -measurability of for any probability measure on (cf. van der Vaart and Wellner, 1996, Definition 2.3.3). This can also be done.

Part (c). Fix . As is a bracket of size in covering any subset of , we can assume that . For this we define

and

Given an arbitrary and , consider the following sets:

The bracket covers all for and . The size of this bracket in equals

Denote for , and let be the Lebesgue measure on . Then

| (30) |

As is a copula and has uniform marginal distributions, the first term on the right hand side satisfies

To obtain an upper bound for , observe that

where is the upper layer of in . Moreover, analogously to Lemma 4.4, one can obtain that

Same bound holds for . Thus (30) yields

| (31) |

Consequently, as is absolutely continuous, we can choose such that either and or and . If , then (31) implies that

| (32) |

Proceeding in the same way as above, we obtain an increasing sequence that eventually terminates at . Technical difficulties related to possible jumps of for can be handled analogously to the proof of Part (a). A similar construction yields a decreasing sequence that eventually terminates at .

We still have to show that the sequence is always finite, i.e., that indeed assumes for some . Consider the sets and . As are disjoint for different , we have and, analogously, . It is obvious that

Furthermore, monotonicity of implies that

This immediately yields . Applying (32), we obtain that if and are finite. As the sum is bounded by , the length of the sequence is bounded by . Possible discontinuities of may increase this number at most additional steps (cf. proof of Part (a)).

Thus we have shown that the set class can be covered by brackets of size in . Defining for , we reach after steps. As the arguments above apply to any interval , we obtain a coverage for the set class and hence an upper bound for the bracketing number:

According to (29), we need to verify that

| (33) |

Changing the upper integral bound from to is justified by the fact that any set class can be covered by a single bracket of size .

5 Examples

In this section we discuss the regularity assumptions of Theorems 4.1 and 4.2. The main results are stated in Propositions 5.2 and 5.3, verifying all regularity assumptions for bivariate Clayton copulas and bivariate Gauss copulas with correlation parameter . The case is treated in Proposition 5.3(c), which guarantees the convergence rate . This is almost as good as .

We start the discussion with a remark covering the mild integrability condition (16) and copulas with bounded densities.

Remark 5.1.

-

(a)

It is easy to see that for with some implies (16). In particular, any polynomial bound for is sufficient.

-

(b)

An immediate consequence of Lemma 4.4 is that all copulas with bounded densities satisfy all regularity conditions of Theorems 4.1 and 4.2. A particularly important copula example with a bounded density is the independence copula . The Iman–Conover method with independence copula is a standard tool in applications with empirically margins based on real data. It is applied to generate multivariate samples with margins that are close to independent or to remove spurious correlations from multivariate data sets.

Unfortunately, many popular copulas, such as Gauss, Clayton, Gumbel, or copulas, have unbounded densities. In particular, a bounded copula density implies that all tail dependence coefficients are zero. Thus applications related to dependence of rare events demand a deeper study of copulas with unbounded densities. The present paper provides two bivariate examples: the Clayton and the Gauss copula.

The bivariate Clayton copula with parameter is defined as

The density can be obtained by differentiation:

| (34) |

The next result states that this copula family satisfies all regularity assumptions of Theorem 4.2.

Proof.

To verify (16), it suffices to show that is polynomial (cf. Remark 5.1(a)). The density is given in (34). It is easy to see that for . Hence the order of magnitude of is determined by , which is clearly polynomial.

To verify (15), recall that the proof of Lemma 4.4 used the following coverage of the set :

Hence, for , we have

| (35) |

The arguments that yield bounds for are symmetric in , so that it suffices to consider . For , denote

and

It is easy to see that

Moreover, the construction of implies that

Partial differentiation of yields

Hence is equivalent to

and for fixed the copula density attains its maximum at

Furthermore, is increasing in for and decreasing in for . Let and denote the corresponding sub-domains of :

An exemplary plot of the function with resulting sets , is given in Figure 2. Note that the function is non-decreasing for any .

We will show that and are bounded by . Denote

where is the projection on the second coordinate: . Further denote and . It is easy to see that . Hence we can write

| (36) |

Denote . This definition implies that for all . Moreover, it is easy to see that . As is non-decreasing, this yields for . This gives us

and, as a consequence, . If , then the uniform margins of the copula immediately yield . Hence, without loss of generality, we assume that .

As is increasing in on and -a.s., we obtain that

| (37) |

Moreover, it is easy to see that if and , then . This yields

| (38) |

Combining (37), (38), and (36), we obtain that

| (39) |

The latter equality is due to the uniform margins of the copula .

The proof of (37) formalizes the idea of slicing the set along for every and shifting each slice upwards along until this slice touches the point as illustrated in Figure 2. Since is increasing in on , the transformed set has a larger probability under .

The next example is the bivariate Gauss copula , defined as the copula of a bivariate normal distribution with correlation parameter . The parameter value yields the independence copula, which is the uniform distribution on the unit square . In this case all regularity conditions are satisfied (cf. Remark 5.1(b)).

Let denote the distribution function of the univariate standard normal distribution, and for let denote the corresponding standard normal quantiles. Further, let denote the correlation matrix corresponding to . Then the bivariate Gauss copula for can be written as

where is considered as a bivariate column vector and is the transposed of . The copula density can be obtained by differentiation:

where and is the identity matrix.

Proposition 5.3.

Proof.

As mentioned above, the case is trivial. Hence we assume .

Part (a) It is easy to verify that for any fixed with some constant . Hence, for ,

Let denote the standard normal density: . It is obvious that for . This yields

| (41) |

for sufficiently small . Hence we obtain that

Part (b). The verification of (15) for is analogous to Proposition 5.2. Due to

| (44) |

partial differentiation of in yields

Hence is equivalent to

| (45) |

Moreover, it is easy to see that with is increasing in if and decreasing in if . This is illustrated in Figure 3. As is increasing, the slicing and shifting argument used in the proof of Proposition 5.2 applies here, and we obtain that . Due to the symmetry of in and , partial differentiation in and the slicing and shifting method yield . Hence (35) gives us .

Part (c). The situation for is different. The copula density is still increasing in for and decreasing in for , but the function is decreasing (cf. Figure 3). Thus (37) does not hold here. Instead of shifting each slice as in the proof of Proposition 5.2, one can shift it until it touches the point . If , no shift is needed. That is, we replace the interval by the interval , where

It is easy to see that

Integrating over , we obtain that

where . It is easy to see that

Hence, as is a copula and has uniform margins, we obtain that

Denote the remaining part of by :

As maximizes for fixed , we have that

Applying (44) and (45) we obtain that

Thus we need an upper bound for the integral

The substitution yields

Finally, applying (41), we obtain that

for . This implies that

| (46) |

Symmetry arguments yield the same order of magnitude for and, as a consequence, for .

Remark 5.4.

-

(a)

It is currently an open question whether the weaker result of Proposition 5.3(c) reflects the reality or simply arises from the approximations used in the proof. However, it should be noted that the case is indeed more difficult than . For the curve may be much closer to the set , and hence may be substantially larger than for . In particular, if and , then

That is, for one can be confronted with the worst case when some entirely falls into the area where the copula density is at its largest. A graphic example to this issue is given on the left hand side of Figure 1. The set in that plot coincides with the set from the right hand side of Figure 3 (. Such coincidence is not possible for or for the Clayton copula.

-

(b)

Intuitively speaking, this problem originates from the negative dependence for , where large values of tend to be associated with small values of and vice versa. As a consequence, the probability is influenced by tail events. This effect is much weaker for Gauss copulas with and, analogously, for many other copulas with positive dependence.

-

(c)

The margins may also influence the convergence of the estimated sum distribution function . In insurance and reinsurance applications the components are often non-negative. In this case implies that for , so that the tail events have no influence on for moderately large . The resulting sets for do not contain any internal points of the unit square that are close to the upper left or to the lower right vertex. That is, and with a small implies , and implies . These avoid the areas where the density of the Gauss copula with is at its highest. Thus non-negative margins simplify the estimation of the function for the Gauss copula with and, analogously, for many other copulas with negative dependence. An illustration to the different types of sets is given in Figure 1.

6 Conclusions

This paper proves that Iman–Conover based estimates for the distribution function of the component sum are strongly uniformly consistent, and it provides sufficient conditions for the convergence rate . Besides the component sum, these results hold for any other componentwise non-decreasing function. The underlying mathematical problem goes beyond the classic uniform convergence results for empirical copulas. In the context of the Iman–Conover method, the primary cause for this technical difficulty is the implicit usage of empirical marginal distributions. Similar issues also arise in all multivariate models generated by plugging empirical margins into an exact copula or by plugging exact marginal distributions into an empirical copula. The marginal transformations involved in these applications complicate the resulting estimation problem in a way that does not allow to establish asymptotic normality of the estimated sum distribution. Therefore the weaker statement is quite the best result one can achieve.

The results proved here for the Iman–Conover method extend to all models generated by plugging empirical margins into an exact copula or by plugging exact margins into an empirical copula. The regularity conditions needed for the convergence rate are satisfied for all copulas with bounded densities, all bivariate Clayton copulas, and bivariate Gauss copulas with correlation parameter . The best convergence rate that could be established for the bivariate Gauss copulas with is . This result suggests that negative dependence may slow down the convergence of estimates. On the other hand, non-negative components , as typical in insurance applications, may simplify the problem. The proof technique used for the bivariate Clayton copula applies to bivariate Gauss copulas with and may also work for other bivariate copulas with positive dependence. A straightforward generalization of this method to higher dimensions is, however, not feasible. Thus the question for the convergence rate in the -variate case with and an unbounded copula density is currently open.

Acknowledgements

The author would like to thank RiskLab, ETH Zurich, for financial support. Further thanks for helpful discussions and comments are due to Philipp Arbenz, Sara van de Geer, Jan Beran, Fabrizio Durante, and Paul Embrechts. Last but not least, the author thanks the anonymous referees, whose valuable comments and suggestions helped to improve this paper.

References

- Arbenz et al. (2011) P. Arbenz, P. Embrechts, and G. Puccetti. The AEP algorithm for the fast computation of the distribution of the sum of dependent random variables. Bernoulli, 17(2):562–591, 2011. doi:10.3150/10-BEJ284.

- Arbenz et al. (2012) P. Arbenz, C. Hummel, and G. Mainik. Copula based risk aggregation through sample reordering. Insurance: Mathematics and Economics, 51(1):122 – 133, 2012. doi:10.1016/j.insmatheco.2012.03.009.

- Barbe et al. (1996) P. Barbe, C. Genest, K. Ghoudi, and B. Rémillard. On Kendall’s process. Journal of Multivariate Analysis, 58(2):197 – 229, 1996. doi:10.1006/jmva.1996.0048.

- Billingsley (1968) P. Billingsley. Convergence of Probability Measures. John Wiley & Sons Inc., New York, 1968.

- Deheuvels (1979) P. Deheuvels. La fonction de dépendance empirique et ses propriétés. Un test non paramétrique d’indépendance. Acad. Roy. Belg. Bull. Cl. Sci. (5), 65(6):274–292, 1979.

- Dudley (1999) R. M. Dudley. Uniform Central Limit Theorems. Cambridge University Press, 1999.

- Durante et al. (2009) F. Durante, P. Sarkoci, and C. Sempi. Shuffles of copulas. Journal of Mathematical Analysis and Applications, 352(2):914 – 921, 2009. doi:10.1016/j.jmaa.2008.11.064.

- Embrechts et al. (2013) P. Embrechts, G. Puccetti, and L. Rüschendorf. Model uncertainty and var aggregation. Journal of Banking & Finance, 37(8):2750 – 2764, 2013. doi:10.1016/j.jbankfin.2013.03.014.

- Fermanian et al. (2004) J.-D. Fermanian, D. Radulović, and M. Wegkamp. Weak convergence of empirical copula processes. Bernoulli, 10(5):847–860, 2004. doi:10.3150/bj/1099579158.

- Genest and Segers (2010) C. Genest and J. Segers. On the covariance of the asymptotic empirical copula process. Journal of Multivariate Analysis, 101(8):1837 – 1845, 2010. doi:10.1016/j.jmva.2010.03.018.

- Ghoudi and Rémillard (1998) K. Ghoudi and B. Rémillard. Emprical processes based on pseudo-observations. In Asymptotic Methods in Probability and Statistics, pages 171 – 197. North-Holland, Amsterdam, 1998. doi:10.1016/B978-044450083-0/50012-5.

- Iman and Conover (1982) R. Iman and W. Conover. A Distribution-Free Approach to Inducing Rank Correlation Among Input Variables. Communications in Statistics - Simulation and Computation, 11(3):311–334, 1982.

- Iman (2008) R. L. Iman. Latin Hypercube Sampling. John Wiley & Sons, Ltd, 2008. doi:10.1002/9780470061596.risk0299.

- Kimeldorf and Sampson (1978) G. Kimeldorf and A. R. Sampson. Monotone dependence. The Annals of Statistics, 6(4), 1978. URL http://www.jstor.org/stable/2958865.

- McKay et al. (1979) M. D. McKay, R. J. Beckman, and W. J. Conover. A comparison of three methods for selecting values of input variables in the analysis of output from a computer code. Technometrics, Chemical and Engineering Sciences, 21(2):239–245, 1979.

- Mildenhall (2005) S. Mildenhall. Correlation and aggregate loss distributions with an emphasis on the Iman-Conover Method. In The Report of the Research Working Party on Correlations and Dependencies Among All Risk Sources, pages 103–204. Casualty Actuarial Society Forum, 2005. URL http://mynl.com/wp/ic.pdf.

- Nelsen (2006) R. B. Nelsen. An introduction to copulas. Springer, New York, second edition, 2006.

- Owen (1992) A. B. Owen. A central limit theorem for Latin hypercube sampling. J. Roy. Statist. Soc. Ser. B, 54(2):541–551, 1992.

- Packham and Schmidt (2010) N. Packham and W. M. Schmidt. Latin hypercube sampling with dependence and applications in finance. Journal of Computational Finance, 13(3), 2010.

- Rüschendorf (1976) L. Rüschendorf. Asymptotic distributions of multivariate rank order statistics. Ann. Statist., 4(5):912–923, 1976.

- Rüschendorf (1983) L. Rüschendorf. Solution of a statistical optimization problem by rearrangement methods. Metrika, 30(1):55–61, 1983. doi:10.1007/BF02056901.

- Segers (2012) J. Segers. Asymptotics of empirical copula processes under nonrestrictive smoothness assumptions. Bernoulli, 18(3):764–782, 2012. doi:10.3150/11-BEJ387.

- Stein (1987) M. Stein. Large sample properties of simulations using Latin hypercube sampling. Technometrics, 29(2):143–151, 1987. doi:10.2307/1269769.

- van der Vaart and Wellner (1996) A. W. van der Vaart and J. A. Wellner. Weak Convergence and Empirical Processes. Springer, New York, 1996. Corrected 2nd printing 2000.

- van der Vaart and Wellner (2007) A. W. van der Vaart and J. A. Wellner. Empirical processes indexed by estimated functions. In Asymptotics: Particles, Processes and Inverse Problems, IMS Lecture Notes – Monograph Series, pages 234–252. Institute of Mathematical Statistics, Beachwood, Ohio, 2007.

- Vitale (1990) R. Vitale. On stochastic dependence and a class of degenerate distributions. In H. Block, A. Sampson, and T. Savits, editors, Topics in statistical dependence, IMS Lecture Notes Monograph Series volume 16, pages 459–469. Institute of Mathematical Statistics, Hayward, 1990.

- Wright (1981) F. T. Wright. The empirical discrepancy over lower layers and a related law of large numbers. The Annals of Probability, 1981.