Large Covariance Estimation through Elliptical Factor Models

Abstract

We proposed a general Principal Orthogonal complEment Thresholding (POET) framework for large-scale covariance matrix estimation based on an approximate factor model. A set of high level sufficient conditions for the procedure to achieve optimal rates of convergence under different matrix norms were brought up to better understand how POET works. Such a framework allows us to recover the results for sub-Gaussian in a more transparent way that only depends on the concentration properties of the sample covariance matrix. As a new theoretical contribution, for the first time, such a framework allows us to exploit conditional sparsity covariance structure for the heavy-tailed data. In particular, for the elliptical data, we proposed a robust estimator based on marginal and multivariate Kendall’s tau to satisfy these conditions. In addition, conditional graphical model was also studied under the same framework. The technical tools developed in this paper are of general interest to high dimensional principal component analysis. Thorough numerical results were also provided to back up the developed theory.

Keywords: principal component analysis; approximate factor model; sub-Gaussian family; elliptical distribution; conditional graphical model; robust estimation.

1 Introduction

This paper considers large factor model based covariance matrix estimation for heavy-tailed data. Factor model is a powerful tool for dimension reduction and latent factor extraction, which gained its popularity in various applications from finance to biology. When applied to covariance matrix estimation, it assumes a conditional sparse covariance structure, i.e., conditioning on the low dimensional spiked factors, the covariance matrix of the idiosyncratic errors is sparse. To be specific, consider the approximate factor model in Bai and Ng (2002):

| (1.1) |

where is the observed data for the th () dimension at time ; is an unknown -dimensional vector of common factors, and is the factor loading for the th variable; is the idiosyncratic error, uncorrelated with the common factors. Previous works are limited by only considering Gaussian or sub-Gaussian factors and noises. In this paper we aim to extend this limitation and consider heavy-tailed distributions. More specifically, we will consider the case where factors and noises are elliptically distributed. Under this broader class of heavy tailed distributions, we aim to understand how to estimate covariance matrix accurately.

Covariance matrix estimation has been pioneered by Bickel and Levina (2008a, b) and Fan et al. (2008). After that, substantial amount of work has focused on the inference of high-dimensional covariance matrices under unconditional sparsity (Cai and Liu, 2011; Cai et al., 2013c, 2010; Karoui, 2008; Lam and Fan, 2009; Ravikumar et al., 2011) or conditional sparsity (Amini and Wainwright, 2008; Berthet and Rigollet, 2013b, a; Birnbaum et al., 2013; Cai et al., 2013b, a; Johnstone and Lu, 2009; Levina and Vershynin, 2012; Rothman et al., 2009; Ma, 2013; Shen et al., 2013; Paul and Johnstone, 2012; Vu and Lei, 2012; Zou et al., 2006). This research area is very active, and as a result, this list of references is illustrative rather than comprehensive. To emphasize, Fan and his collaborators proposed to use factor model or conditional sparsity structure for covariance matrix estimation (Fan et al., 2008, 2011, 2013, 2014c). The model encompasses the situation of unconditional sparse covariance by setting the number of factors to zero. Thus it is more general and realistic given the fact that the observed data are usually driven by some common factors.

Another line of research on robust covariance estimation also receives significant attention from the literature. The idea of robust estimation dates back to Huber (1964) and had been extended in regression problems with different types of loss function; see for example Fan et al. (2014b) and Catoni (2012). Recently, Han and Liu (2013b, 2014) introduce robust covariance matrix estimation to high-dimensional elliptical and transelliptical (or elliptical copula) distribution family. In those papers, they proposed a robust procedure using the marginal Kendall’s tau statistics and proved its optimality for covariance matrix estimation under elliptical distributions. In addition, multivariate Kendall’s tau was also considered by Han and Liu (2013a) to estimate eigenspaces of covariance matrices in high dimensions. Those methods, applied to PCA or sparse PCA, can be potentially useful for dealing with factor models with heavy-tailed factors and noises. The goal of the current paper is to develop a unified theory that allows us to extend these robust rank-based covariance estimation procedures to handle heavy-tailed data with conditional covariance sparsity.

1.1 Background on approximate factor model

To illustrate how to use factor model as a dimension reduction tool for covariance matrix estimation, let us write model (1.1) in its vector form:

| (1.2) |

where contains all observed individuals at time and is the factor loading matrix. The matrix form of (1.1) is

| (1.3) |

where , , , are matrices from observed data, factor loadings, factors, and errors with , and . Here we consider the case where the dimension is larger than sample size and for simplicity we assume samples are independent and identically distributed in the sequel (An extension to the dependent setting is straightforward, but tedious.). We assume factor matrix is observable. To make the model (1.1) identifiable, we impose the following conditions as in Bai and Ng (2013) and Bai and Li (2012):

| (1.4) |

The conditions in (1.4) are common in the factor model literature. But we will point out in Section 2 that these conditions are sufficient only for asymptotic identifiability up to an error of order rather than exact identifiability. Under the conditions in (1.4), the covariance matrix of is

| (1.5) |

where is the covariance matrix of the idiosyncratic error .

1.2 Major contributions of this paper

Under model (1.2), Fan et al. (2013) proposed the Principal Orthogonal complEment Thresholding (POET) estimator for under the assumption that factors and noises are sub-Gaussian. By imposing the condition that the leading eigenvalues of diverges at the rate of order from their pervasiveness condition, Fan et al. (2013) proved the consistency of the POET estimator and showed its rates of convergence. However, their proofs are mathematically involved and do not transparently explain why POET works in estimating large covariance matrices. It has been pointed out by Fan and Wang (2015) how pervasive factors help in estimating the low-rank part in (1.5). The idea is further explored in this paper. A surprising result is that the diverging signal of spiked eigenvalues excludes the necessity of the sparse principal component assumption in sparse PCA literature, comparing with for example Cai et al. (2013b).

The main contributions of the paper are two folds. On one hand, we summarize a unified generic framework in Section 2.2 for applying POET to various potentially heavy-tailed distributions. The key Theorem 2.1 provides a set of high level interface conditions (1.6) explaining how to design a POET covariance estimator according to factor and error distributions. POET regularization needs the following three components: initial pilot estimators for covariance matrix , its leading eigenvalues and their corresponding leading eigenvectors . With these compoents, a generic POET estimator can be constructed. We will show that such a POET procedure attains desired rates of convergence as long as

| (1.6) | ||||

These conditions are relatively easy to verify, as they involve only the componentwise maximums. Through those sufficient conditions, we are able to separate the deterministic analysis of the estimation procedure and the probabilistic guarantee of the design of initial estimators.

For two specific factor and error distributions, we provide methods to construct those initial estimators. For sub-Gaussian, it is natural to employ sample covariance matrix and its eigenvalues and eigenvectors as the estimates for , and . We show the natural idea indeed achieves the above conditions for sub-Gaussian data, which gives an explanation why POET in previous literature works. However, for elliptical distributions, constructing estimators with the desired rates are highly nontrivial. We use the marginal Kendall’s tau to obtain and while a different method multivariate Kendall’s tau is applied to construct . Notice an interesting fact that the generic POET procedure allows separately estimating the eigenvectors and eigenvalues using different methods. Robust estimators are constructed for the first time for elliptical factor models.

1.3 Notations

Here are some useful notations. If is a general matrix, we denote its matrix entry-wise maximum value as and define the quantities (or for short), , and to be its spectral, Frobenius, induced and element-wise norms. If furthermore is symmetric, we define to be the th largest eigenvalue of and , to be the maximal and minimal eigenvalues respectively. We denote to be the trace of . For any vector , its norm is represented by while norm is written as . We denote to be the diagonal matrix with the same diagonal entries as . For two random matrices of the same size, we say if and if . Similarly for two random vectors of the same length, if and if . We denote if random vectors and have the same distribution. In the sequel, is a generic constant that may differ from line to line.

1.4 Paper organization

In Section 2, we present a generic POET estimating procedure and a high-level theoretical interface which secures the consistency of the generic procedure for factor-based conditional sparsity mdoels. We verify that the conditions in Section 3 hold with high probability for sub-Gaussian data, which provides a transparent understanding of the mechanism of the POET methodology. In Section 4, we propose a new method using a combination of marginal and multivariate Kendall’s tau and prove its theoretical properties under elliptical factor models. Thorough numerical simulations are conducted illustrate the merits of our proposed method in Section 5. In Section 6, we conclude the paper with a short discussion. The technical proofs are relegated to the appendix.

2 A High-level theoretical interface

In this section, we summarize a generic POET procedure and provide a set of high level sufficient conditions for consistent covariance estimation when . Before doing that, let us review what has been achieved in the existing literature where both the factors and noises are assumed to be sub-Gaussian.

2.1 Spiked covariance model

Assume the observed random variables have zero mean and covariance matrix where the eigenvalues of are ordered in descending order. We consider the spiked population model as suggested by the approximate factor structure (1.5). Specifically we have the following assumption on the eigvenvalues.

Assumption 2.1 (Spiked covariance model).

Let be a fixed constant that does not change with and . As , , where the spiked eigenvalues are linearly proportional to dimension while the non-spiked eigenvalues are bounded, i.e., for constants . In addition, the non-spiked eigenvalue average .

Assumption 2.1 requires the eigenvalues be divided into the diverging and bounded ones. For simplicity, we only consider distinguishable eigenvalues (multiplicity 1) for the largest eigenvalues. This assumption is typically satisfied by the factor model (1.1) with pervasive factors. More specifically, if the factor loadings (the transpose of the rows of ) are an i.i.d. sample from a population with finite second moments, then by the strong law of large numbers, almost surely, where . In other words, the eigenvalues of are approximately

where is the th eigenvalue of . If we further assume that is bounded, by Weyl’s theorem, we conclude

| (2.1) |

and the remaining are bounded.

2.2 A generic POET procedure for covariance estimation

We see from (1.5) that the population covariance of the factor model (1.1) exhibits a low-rank plus sparse structure, if is sparse, whose sparsity level is measured by

for some is small. In particular, with , corresponds to the maximum number of nonzero elements in each row of .

To estimate the covariance matrix with the approximate factor structure (1.5), Fan et al. (2013) proposed the POET method to recover the factor matrix as well as the factor loadings. The idea is to first decompose the sample covariance matrix into the spike and non-spike parts,

| (2.2) |

where is called the principal orthogonal complement. Then by employing adaptive thresholding on to get (Cai and Liu, 2011), they obtain a final covariance estimator defined as

| (2.3) |

The above procedure can be equivalently viewed as a least-squares approach. That is, the factor and loading matrices can be estimated by solving the following nonconvex minimization problem:

| (2.4) |

It is shown that the columns of are the eigenvectors corresponding to the largest eigenvalues of the matrix and . Note that the estimator given by minimizing (2.4), after normalization, is actually the first empirical eigenvectors of . Given , we define and . Finally adaptive thresholding is applied to to obtain with

| (2.5) |

where is the generalized shrinkage function (Antoniadis and Fan, 2001; Rothman et al., 2009) and is an entry-dependent threshold. The above adaptive threshold operator corresponds to applying thresholding with parameter to the correlation matrix of . The positive parameter will be determined based on theoretical analysis.

Let . Fan et al. (2013) claimed that under some technical assumptions, with , if ,

| (2.6) |

and

| (2.7) | ||||

where is the relative Frobenius norm. The scaling is exploited to ensure . The term in is the price we need to pay for estimating the unknown factors. But in the high dimensional regime so that , the rate is optimal. The original proofs for getting the above rates are mathematically involved and is not clear why the optimal rates can be attained, especially when no sparsity assumption for eigenvectors was imposed as in sparse PCA literature.

We propose a generic POET procedure here: (1) given three initial pilot estimators for true covariance matrix , leading eigenvalues and leading eigenvectors respectively, the principal orthogonal complement can be computed by subtracting out the leading low-rank part, i.e.,

(2) The adaptive thresholding (2.5) is applied to to obtain , and (3) the low-rank structure is added back to obtain . Note for sub-Gaussian distributions, is the diagonal matrix constructed by the first leading empirical eigenvalues of the sample covariance matrix while is the matrix of corresponding leading empirical eigenvectors. But in general, and do not have to come from the sample covariance matrix. In fact, they can even be separately estimated.

So our question is: why such a simple POET procedure works under the piked covariance assumption (2.1)? Can we replace the sample covariance matrix by other pilot estimators as a starting point for the eigen-strucuture if other family of distributions, such as elliptical distributions or other more general heavy-tailed distributions, are considered?

2.3 A high level theoretical interface

A high level explanation is provided to understand the generic POET procedure. Sufficient conditions are brought up for and to achieve the desired rates of convergence in (2.6) and (2.7). Our vital conclusion is stated in the following theorem.

Theorem 2.1.

The proof given in the appendix to obtain (A.1) provides insights on how the generic POET procedure works. Note that the max norm of low rank matrix estimation is bounded by and . The former quantifies the estimation error of leading empirical eigen-structure for its population counterpart, while the latter measures the error of identifying the low rank matrix by from the true matrix . The identification of low-rank and sparse matrices under pervasive condition is asymptotically unique with identification error . Additionally, the estimation contributes an error term of order .

2.4 Conditional graphical model

In Section 2.2, measures the sparsity of , but its inverse is not necessarily sparse. Sometimes, the sparsity structure on reveals more interesting structure than . For example, If , the sparsity of encodes the conditional uncorrelatedness relationships between all variables in the dimensional vector . More specifically, for nodes , each corresponding to one element of , and are connected if and only if , meaning that and are uncorrelated conditioning on all the other and . If the number of factors is zero, this reduces to the classical elliptical graphical model, exhaustively studied by Vogel and Fried (2011) and Liu et al. (2012).

In many applications, the conditional graphical model (or conditional sparse inverse covariance model) appears more natural compared to the conditional sparse covariance model. For example, in understanding the dependence of financial returns, the interest lies in the graphical model of the idiosyncratic components after taking the common market risk factors away; in genomic studies, the graphs after taking the confounding factors such as age and environment exposure are of better interest. The factors can be interpreted as covariates that need to be adjusted before focusing on the analysis of correlatedness of the residual part (Fan et al., 2011). Cai et al. (2012) adopted the same idea of adjusting the factors in genomics application, but they do not assume the factors are pervasive so that they need to impose the constraint of a sparse factor loading matrix . The sparsity was put on and measured by the quantity

The generic POET procedure could also be modified to estimate conditional graphical model. The first step is still recovering by removing the effect of low-rank dominating factors. Then the method “constrained -minimization for inverse matrix estimation” (CLIME) proposed by Cai et al. (2011) can be applied to obtain . Specifically, CLIME solves the following constrained minimization problem:

| (2.8) |

where and is a tuning parameter so that . A further symmetrization step can be carried out to guarantee a symmetric estimator where

| (2.9) |

Note that the optimization in (2.8) can be solved column by column using linear programming. Other possible methods can also be considered including graphical Lasso, graphical SCAD, graphical Dantzig selector, and graphical neighborhood selection (Friedman et al., 2008; Yuan and Lin, 2007; Fan et al., 2009; Lam and Fan, 2009; Ravikumar et al., 2011; Yuan, 2010; Meinshausen and Bühlmann, 2006). Though substantial amount of efforts have been made to understand the graphical model, little has been done for estimating conditional graphical model, which is again more general and realistic.

Once we have , the original inverse covariance matrix can also be estimated using the Sherman-Morrison-Woodbury formula as follows:

| (2.10) |

The following theorem gives the rates of convergence for and provided good pilot estimators , and are given. Its proof is in Appendix A.

Theorem 2.2.

Note the assumption of bounded is stronger than the case of estimating covariance matrix. This condition might be relaxed if other methods instead of CLIME was applied. But we do not pursue the weakest possible conditions here. Many potential applications are only involved with the estimation of inverse covariance matrix , for instance classification and discriminant analyses and optimal portfolio allocation in finance.

2.5 Positive semi-definite projection under max norm

There is an additional issue that requires careful consideration. In the generic POET procedure, if and are not estimated from the same positive semi-definite (PSD) matrix , the residual may not be PSD for a given sample. Thus, the following optimization should be considered to find the nearest PSD matrix of in terms of the max norm:

| (2.12) |

The minimizer preserves the max norm error bound since

and everything else in the POET procedure works with replaced by . The same problem occurs in conditional graphical model estimation. Although is PSD with high probability, in practice we may reach a non-PSD estimator for . So we need to explicitly perform the PSD projection of onto the PSD cone as in (2.12).

Minimization (2.12) is challenging due to its non-smoothness. An effective smooth surrogate for the max norm objective was proposed by Zhao et al. (2014) which can be solved efficiently. Specifically, they considered minimizing subject to where

where . More details can be found in Zhao et al. (2014). Another possibility to ease computation burden is solving the dual problem of graphical lasso, that is,

By choosing , the optimal solution is a PSD matrix satisfying the max norm bound. Such a projection is still valid for the generic POET procedure to get the desired convergence rates under max norm.

3 Sub-Gaussian factor models

We have established sufficient conditions in (1.6) for optimal estimation of covariance matrices as well as conditional graphical models. The next natural question is whether these conditions hold for sub-Gaussian factor models. In this subsection, we validate the conditions for sample covariance matrix under sub-Gaussian conditions.

By the spectral decomposition, where and is constructed by all the corresponding eigenvectors of . We use subscript to explicitly denote the dependence of and on all eigenvalues or eigenvectors rather than just spiked ones. Let . So has mean zero and diagonal covariance matrix . Since under orthonormal transformations of the data, the empirical eigenvalues of sample covariance are invariant and the empirical eigenvectors are equivariant, the analysis will be done on ’s which naturally extends to our original data ’s by a simple affine transformation. The following assumption on is imposed.

Assumption 3.1 (Sub-Gaussian distribution).

Let be the standardized version of the transformed data . ’s are iid samples of sub-Gaussian isotropic random vector , i.e., for some constant where the sub-Gaussian norm is defined as . Furthermore, we assume such that for ,

| (3.1) |

The above lemma require a slightly stronger condition than the classical sub-Gaussian condition for . It has to satisfy (3.1) for technical reasons discussed in Lemma D.2 in Appendix D. This assumption is clearly satisfied if has independent elements of sub-Gaussian variables (Vershynin, 2010) although it could also hold for weakly dependent sub-Gaussian vectors.

Under this assumption, trivially the first condition in (1.6) holds for the sample covariance matrix of , i.e., . We present two theoretical properties next respectively on leading empirical eigenvalues and eigenvectors of the sample covariance matrix of ’s. These properties are useful for us to verify the remaining conditions of the high level theoretical interface described in (1.6).

Consider the empirical eigenvectors of for . Each is divided into two parts , where is of length corresponding to the spike component and corresponds to the noise component.

Theorem 3.2.

The theorems state that under the pervasive condition that spiked eigenvalues are of order , we are able to approximately recover the true leading eigenvalues and eigenvectors. In Fan and Wang (2015), the same phenomenon is observed when ’s are sub-Gaussian vector with independent elements. But here we do not require element-wise independence and relax the condition to any sub-Gaussian isotropic random vectors satisfying (3.1). The proofs of the above two theorems can be found in Appendix B.

Given the above two theorems, let us validate the second and third conditions in (1.6). Define where is short for sub-Gaussian. The second condition holds for according to Theorems 3.1. Note that and share the same set of empirical eigenvalues. To check the third one, let be the matrix consists of the top leading eigenvectors of . If the whole eigen-space of is written as , then . Therefore and

| (3.2) | ||||

which is due to Theorem 3.2 and the fact shown in Theorem 2.1. Hence, we have shown that the sample covariance based estimators and satisfy the sufficient conditions (1.6). Together with Theorem 2.1, this explains why POET achieves all the desired rates (2.6) and (2.7).

We finally devote a remark to the assumption of zero mean of the observed data implied by Assumption 3.1. This condition is only made to simplify the presentation of proofs. In practice, we first center the data by . All the conclusions of this section hold for the centered data as well.

4 Elliptical factor models

In the previous section, we assume to be a sub-Gaussian random vector, which is a strong distributional assumption for many applications. In this section, we replace the sub-Gaussian assumption 3.1 by elliptical distribution assumption 4.1 and propose a novel robust estimator for the analysis of factor models.

We first briefly review the elliptical distribution family, which generalize the multivariate normal distribution and multivariate t-distribution. Compared to the sub-Gaussian setting, it is more challenging to design pilot estimators to simultaneously satisfy the three requirements in (1.6). To handle this challenge, we separately construct two estimators and . and its leading eigenvalues satisfies the first two requirements in (1.6) while the eigenvectors of satisfies the last condition of (1.6).

4.1 Elliptical distribution

We define the elliptical distribution as follows. Let and with . A -dimensional random vector has an elliptical distribution, denoted by , if it has a stochastic representation

| (4.1) |

where is a uniform random vector on the unit sphere in , is a scalar random variable independent of , is a deterministic matrix satisfying . Here is called the scatter matrix. Note that the representation in (4.1) is not identifiable since we can rescale and . To make the model identifiable, we require so that . In addition, we assume is non-singular, i.e., . If , as long as they are of the same order, all results in the following still hold. In this paper, we only consider continuous elliptical distributions with .

An equivalent definition of an elliptical distribution is through its characteristic function, which admits the form , where is a properly defined characteristic function and . and are mutually determined by each other. In this setting, we denote by . The marginal and conditional distributions of an elliptical distribution are also elliptical. Therefore, in factor model (1.1), if and are uncorrelated and jointly elliptical, i.e., , then we have .

Compared to the Gaussian family, the elliptical family provides more flexibility in modeling complex data. The main advantage of the elliptical family is its ability to model heavy-tail data and the tail dependence between variables (Hult and Lindskog, 2002), which makes it useful for modeling many modern datasets, including financial data (Rachev, 2003; Cizek et al., 2005), genomics data (Liu et al., 2003; Posekany et al., 2011), and fMRI brain-imaging data (Ruttimann et al., 1998).

The following assumption is considered in this section.

Assumption 4.1 (Elliptical distribution).

The data ’s are elliptically distributed, i.e., or with uniformly distributed on the unit sphere and the random variable independent from . Additionally, we assume due to identifiability and is bounded.

The above assumption is implied by imposing a joint elliptical model of the factors and noises, i.e., . Obviously, the elliptical family is more general than Gaussian assumption and contains heavy tail distributions. One typical example is multivariate t-distribution with degrees of freedom . The moment condition is imposed only for the sake of estimating marginal variances by methods discussed in Section 4.2. This assumption may be relaxed if other methods are applied.

4.2 Robust estimation of variances

Let where is the correlation matrix and is the diagonal matrix consists of standard deviations for each dimension. Our construction of is based on separately estimating and . In this subsection, we first introduce a robust estimator to estimate .

Since exhibits heavy tails, we need a method to robustly estimate in order to center the data and estimate the covariance matrix. Substantial amount of research has been conducted on this subject in both low dimensional setting (Huber, 1964; Zou and Yuan, 2008; Wu and Liu, 2009) and high dimensional setting (Belloni et al., 2011; Fan et al., 2014a). In addition, Koenker (2005) has considered problem from a quantile regression perspective. In this section, we introduce two M-estimator methods proposed by Fan et al. (2014b) and Catoni (2012), who borrow the original idea from Huber (1964). The methods are also useful for robust estimation of variances.

Let us denote and for . We estimate each using the data . The M-estimator of Fan et al. (2014b) is obtained by solving

| (4.2) |

for each , where is the derivative function of the Huber loss satisfying if , if and if . The above estimator can be equivalently obtained by minimizing the Huber loss

According to Fan et al. (2014b), choosing for such that , where is an upper bound of , we have

| (4.3) |

Catoni (2012) proposed another M-estimator by solving (4.2) with a different strictly increasing such that . For a value such that , let

where is again an upper bound of . Catoni (2012) showed that the solution of (4.2) satisfies

| (4.4) |

Therefore, by taking , with probability at least for both methods. We implement Catoni’s estimator in the simulation by taking . For the choice of , we simply take , where are the sample covariance of the th dimension.

To estimate , we apply the above M-estimation methods on the squared data. Note that . We have estimated above. To estimate , we employ the M-estimator (4.2) on the squared data , denoted by . This works as the fourth moment of is assumed finite. The robust variance estimator is then defined as

| (4.5) |

where is a small constant (). If , let , we have

| (4.6) |

Additionaly, due to the structure of , where and , it is easy to see and .

4.3 Marginal Kendall’s tau estimator

We now provide a pilot estimator to robustly estimate the correlation matrix when data follow elliptical distributions. The idea of Kendall’s tau statistic was introduced by Kendall (1948) for estimating pairwise comovement correlation. Kendall’s tau correlation coefficient is defined as

| (4.7) |

whose population counterpart is

| (4.8) |

Note that the estimator does not depend on the location . So without loss of generality, we assume . Then with independent and identically distributed samples .

Denote by and . For elliptical family, it is known that the nonlinear relationship holds for the Pearson correlation and Kendall’s correlation (Fang et al., 1990; Han and Liu, 2014). Therefore, a natural estimator for is where

| (4.9) |

By Theorem 3.2 of Han and Liu (2013b), with probability larger than for any ,

Using the fact , we know since all the eigenvalues of are bounded away from infinity and zero. This is true because and as derived in Section 4.2. This implies

| (4.10) |

Combining the rates in (4.6) and (4.10), we conclude

Define . The estimator , which consists the first eigenvalues of , satisfies

| (4.11) |

Here is short for elliptical distribution. This makes the second sufficient condition in (1.6) hold. Furthermore, we can easily check that the first sufficient condition holds for using the concentration of U-statistics, i.e.

| (4.12) |

Although the marginal Kendall’s tau based estimator has good properties for eigenvalues, it is hard to prove the third sufficient condition for eigenvectors in (1.6) due to the complicated nonlinear transformation. Luckily, we do not require and in (1.6) to come from the same covariance estimator. In the next section, we propose another covariance estimator whose eigenvectors satisfy the third sufficient condition in (1.6).

4.4 Multivariate Kendall’s tau estimator

To find an estimator that satisfies the third condition in (1.6), we resort to the multivariate Kendall’s tau estimator. We focus our analysis again on the transformed data . The population multivariate Kendall’s tau matrix is defined as

| (4.13) |

The sample version of the multivariate Kendall’s tau estimator is a second-order U-statsitc:

| (4.14) |

where

Several important properties of the above estimator is worth mentioning. First this estimator is location invariant, which allows us to assume without generality, i.e., . Secondly, the eigenvectors of the estimator is equivariant to orthogonal transformation. So if we define the multivariate Kendall’s tau estimator based on the observed data as

we have , where and are the empirical eigenvector of and , respectively.

The most important feature of the U-statistic estimator in (4.14) is that its kernel is distribution-free. To see this, we have

where is an independent copy of and the characteristic function of is determined by that of . See Hult and Lindskog (2002) for the detailed expression of the characteristic function. Thus,

which depends only on the multivariate standard normal vector . The last equality is due to . Thus defined by (4.13) is a diagonal matrix by the symmetry of .

Write , where is defined as

which is a multiple of . Obviously, shares the same eigenvalue ordering as that of , and thus the same eigenspaces as those of . So estimating the leading eigenvectors of is equivalent to estimating those of . In sum, particularly fits the goal of estimating the eigenvectors of .

The above multivariate Kendall’s tau statistic is first introduced in Choi and Marden (1998) and has been used for low dimensional covariance estimation (Visuri et al., 2000) and principal component estimation (Marden, 1999; Croux et al., 2002). Many testing literature based on rank statistics is also related to the estimator, for example Tyler (1982); Hallin and Paindaveine (2006). The literature listed here is only illustrative rather than complete.

We now consider the theoretical properties of the eigenvectors of . As before, is divided into the spiked part and noise part .

Theorem 4.1.

The proof for Theorem 4.1 is relegated to Appendix C. Define as the multivariate Kendall’s tau estimator of the observed data ’s and as the leading eigenvectors of . Theorem 4.1 implies

following the same argument (3.2) in Section 3. So the third sufficient condition in (1.6) holds for . Together with the estimators and defined in Section 4.3, we are ready to apply the general POET procedure for the heavy tail factor model and achieve all the desired estimation convergence rates for both covariance and precision matrices.

5 Simulations

Simulations are carried out in this section to demonstrate the effectiveness of the proposed method for elliptical factor models. The robust estimators , , proposed in Section 4 will be compared with the original POET estimator based on the sample covariance, or , , discussed in Section 3. We put the two sets of estimators into the general POET framework described in Section 2 for estimating both conditional sparsity covariance and conditional graphical models.

5.1 Conditional sparse covariance estimation

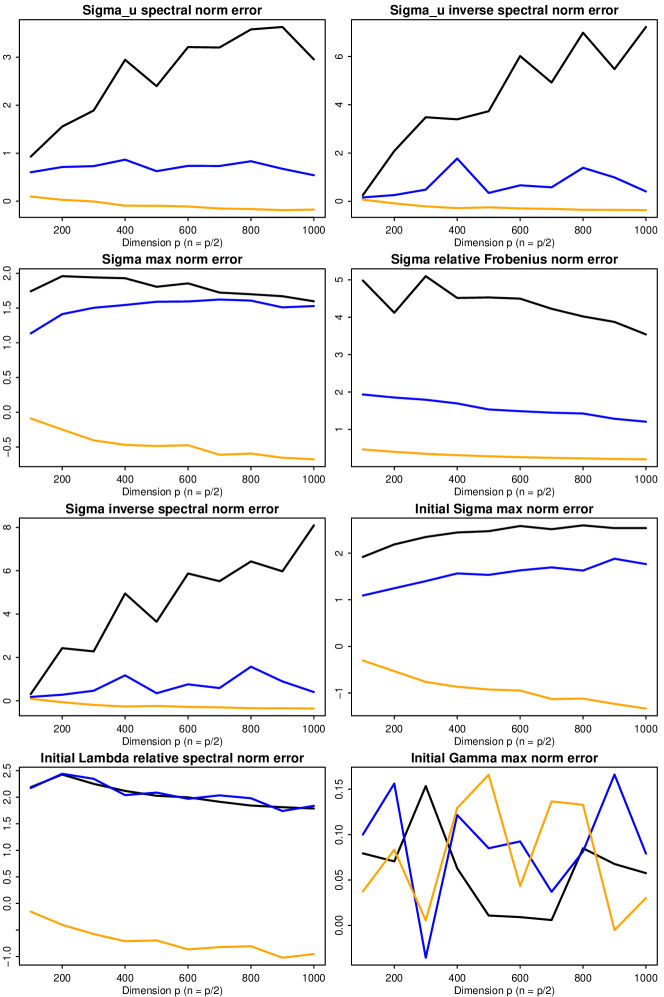

In this section, we consider the factor model (1.1) with jointly follow a multivariate t-distribution with degrees of freedom . Larger corresponds to lighter tail and corresponds to a multivariate normal distribution. We simulated independent samples of from multivariate t-distribution with covariance matrix and each row of from . The observed data is formed as and the true covariance is . We vary from to with sample size , and fixed number of factors in this simulation.

For each triple , both the original POET estimator (, , ) and the proposed robust POET estimator (, , ) were employed to estimate and . simulations were conducted for each case. The log-ratio (base 2) of the average estimation errors using the two methods were reported in Figure 1, measured under different norms ( and for ; and for ; and for initial pilot estimators). In addition, three different degrees of freedom were chosen, representing respectively heavy tail, moderate heavy tail, and normal situations.

From Figure 1, when factors and noises are heavy-tailed from (black), the original POET estimators are poorly behaved while the robust method works well as we expected. (blue) typically fits financial or biological data better than normal in practice. In this case, we also observe a significant advantage of the robust POET estimators. The error is roughly reduced by a magnitude of two if the rank based estimation is applied. However, when the distribution is indeed normal or (orange), the original POET estimators based on sub-Gaussian data performs better, though the robust POET also achieves comparable performance.

5.2 Conditional graphical model estimation

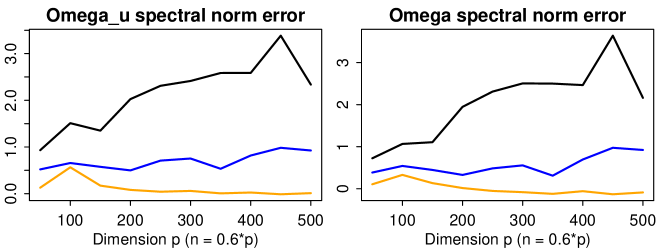

In this section, we consider the conditional graphical model described in Section 2.4. In particular, we compare the accuracy of different methods for estimating the precision matrices and . Here we assume a block diagonal precision error matrix where is by correlation matrix with off-diagonal element equals . Then we simulate again from multivariate t-distribution with covariance . We set the dimension to range from to , sample size and a fixed number of factors .

For each configuration of , after applying POET with the original and robust pilot estimators, we estimate and as proposed in Section 2.4 using the CLIME procedure. To efficiently solve large-scale CLIME optimization (2.8), we used the R package “fastclime” developed by Pang et al. (2014). simulations were conducted for each case. The log-ratio (base 2) of the average errors of the two methods were reported in Figure 2, measured under spectral norms and . Three different degrees of freedom (black), (blue), (orange) were used as in Section 5.1. Clearly, the robust estimators outperform non-robust ones for and , and maintains competitive for the normal case.

6 Discussions

We provide a fundamental understanding of high dimensional factor models under the pervasive condition. In particular, we extend the POET estimator in Fan et al. (2013) to be a generic procedure which could take any pilot covariance matrix estimators as initial inputs, as long as they satisfy a set of sufficient conditions specified in (1.6). Transparent theoretical results are then developed. The main challenge is to check the high level conditions hold for certain estimators. When the observed data is sub-Gaussian random vector, we are able to simply use sample covariance matrix to construct initial estimators. However, if we encounter heavy-tailed elliptical distributions, robust estimators for eigen-structure should be considered. The paper provides an example of separately estimating leading eigenvalues and eigenvectors under elliptical factor models. But the results could possibly be generated to other richer family of distributions.

Based on recent work of Fan and Wang (2015), it is possible to relax the spiked eigenvalue condition from order to weaker signal level. But bounded eigenvalues are obviously not enough for consistent estimation as has been pointed out by Johnstone and Lu (2009), and as a result more structural assumptions are needed. Agarwal et al. (2012) considered a similar type of low-rank plus sparse decomposition, but their work is based on optimization technique and does not leverage pervasiveness. In addition, they only analyze the obtained estimator using Frobenius norm errors. Consequently, their lower bound results are not applicable to our setting. The lower bound for the rates in (2.6) and (2.7) will be pursued in a separate work. By all means, the similarity and difference between optimization thinking and pervasiveness thinking should be studied in further details.

Appendix A Proofs in Section 2

Proof of Theorem 2.1.

We establish (2.6) here and defer the details of the proof of (2.7) to Appendix A.. To obtain the rates of convergence in (2.6), it suffices to prove . Once the max error of sparse matrix is controlled, it is not hard to show the adaptive procedure discussed in (2.5) gives such that the spectral error (Fan et al., 2011; Cai and Liu, 2011; Rothman et al., 2009). Furthermore, . So is also due to the lower boundedness of .

According to first condition in (1.6), . Therefore to show , we only need to prove the low rank part of concentrates at a desired rate under max norm. So our goal is to prove

| (A.1) |

Let where and the th column of is . To obtain (A.1), we bound and separately. Four useful rates of convergence are listed in the following:

The first one is due to Weyl’s inequality since while the second follows from trivial bound , which is further bounded by according to the theorem of Davis and Kahan (1970). The third and fourth rates are by assumption. Next we show and derive the rates for and .

Note that

Since , we have and . Using this fact, the following argument implies and . More specifically,

Combining the rates of and , we prove (A.1). Thus (2.6) follows.

Now let us prove (2.7). The first result follows from when is chosen as the same order and

We now prove the remaining two results. Suppose the SVD decomposition of where and . Then obviously

| (A.2) | ||||

and

| (A.3) |

It is easy to show

| (A.4) | ||||

where , and . In order to characterize the rate of convergence under relative Frobenius norm, we analyze the terms and separately.

According to Theorem 4.1 of Fan and Wang (2015), . is bounded by

where

because by assumption and . Similarly, as by the Theorem (Davis and Kahan, 1970). Finally, . Following similar arguments, is dominated by and . Combining the terms , , and together, we complete the proof for the relative Frobenius norm.

We now turn to analyze the spectral norm error of the inverse covariance matrix. By the Sherman-Morrison-Woodbury formula, we have

| (A.5) |

where

| (A.6) |

where and . The right hand side can be bounded by the terms representing the differences of the “hat” part , , and the “tilde” part , , :

The first term is ; the second term is ; and the third term is . Thus, , which implies . Therefore, we finish the proof of the remaining parts of (2.7) in Theorem 2.1. ∎

Proof of Theorem 2.2.

From (A.1), we have . Next we prove that the CLIME estimator will give such that . Choose so that the true is within the region of the constraint of (2.8). So

where the first term is bounded by since is a feasible solution of (2.8), and the second term is bounded by due to the optimality of over . Therefore with , we have . It is easy to see the symmetrization step does not change the rate of . By similar arguments as in Cai et al. (2011), we obtain .

Appendix B Proofs in Section 3

Proof of Theorem 3.1.

Define where , with and , . In order to prove the theorem, we first define two auxillary quantities as follows and analyze them separately. Let

In addition we define

which share the same nonzero eigenvalues with the sample covariance matrix .

We first prove satisfy . Note that has the same eigenvalues as matrix , where is an matrix with independent and identically distributed rows. Each row is a sub-Gaussian random vector with mean and variance . Therefore, we are in the low dimensional situation with fixed dimension , although eigenvalues diverge. By central limit theorem, the diagonal element of is of order and the off-diagonal elements are of order . Therefore, and furthermore

Since dimension is fixed, we have .

Secondly, we have . By the definition of , where is a random matrix with independent rows of zero mean and identity covariance and . Since each row of is independent sub-Gaussian isotropic vector of dimension , by Lemma D.1, choose , for any ,

Therefore, for ,

By Wely’s Theorem, Therefore, combining results for and , we conclude . ∎

Proof of Theorem 3.2.

(i) We start by proving the rate for in the simple case of . In this case, by Lemma B.1, we indeed have since . In the following, we consider . Denote as before. Recall are eigenvectors of . Let be the eigenvectors of . It is well known that for ,

| (B.1) |

Using (B.1), we have

| (B.2) |

Since is the eigenvector of , that is, . Plugging in , we obtain

where we denote , . We then left-multiply the above equation by and employ the relationship (B.2) to replace by and as follows:

| (B.3) | ||||

Further, we define

where is well defined because . Then we have . Left multiplying to (B.3), we have

where . Dividing both sides by , we get

| (B.4) |

where

| (B.5) | ||||

Following Fan and Wang (2015), together with Lemma D.1, we can show . Further note that , we obtain

| (B.6) |

According to the definition of , as ,

where exists. So . We claim , so the right hand side of (B.6) is . To prove the rate of , note first by Lemma D.1, , so we have

Therefore, . From Lemma B.1, , so (i) holds.

(ii) Now we prove the second conclusion of the theorem on the non-spiked part . Again we consider the case and separately. When , by definition of eigenvector, we can easily see that

Plug the former equation into the latter one, we have

where . Therefore, let , is bounded by

which is due to the facts that , , according to Lemma B.1 and three claims yet to be shown:

| (B.7) | ||||

Now we turn to the case . Similar as derivations above, by definition, we have

The former equation implies

where . Note that this definition of degenerates to when and . Left multiply this equation by defined in (i) and plug it into the previous equation, we obtain

Carefully bounding each term of the right hand side by (B.7) and Lemma B.1, we find the dominating term is the third term, which has rate . Thus .

It remains to prove (B.7). Firstly, . Thus the third result holds. To show the other two rates, denote . Then each element of is iid sub-Gaussian with bounded variance proxy. Hence and for . So we have

and

Now the proof is complete.

∎

Lemma B.1.

For , and .

Proof.

Recall that . Let , then

where and . Further define and consider the eigenvalue of the matrix . The diagonal element of the matrix must lie in between its minimum and maximum eigenvalues. That is

where is the -th element of the empirical eigenvector for . Note that converges to , and decided by both the left and right hand side converge in probability to by Lemma D.1, thus to . So . Also, by definition, for while the ratio is 1 for . Hence, , which implies that and . ∎

Appendix C Proofs in Section 4

Let us introduce some additional notations and two lemmas in order to prove Theorem 4.1. Assume is even, otherwise we can drop one sample without affecting the asymptotics. Let . For any permutation of , let . For , we define and :

| (C.1) |

| (C.2) |

where is the permutation group of . For each fixed permutation , we have the following two conclusions on empirical eigenvalues and eigenvectors of similar to the sample covariance for sub-Gaussian factor models.

Lemma C.1.

Now consider the leading empirical eigenvectors of , . Each is divided into two parts where is of length .

With the above two lemmas, we prove Theorem 4.1.

Proof of Theorem 4.1.

(i) First, we have the simple fact that

Now let us derive the rate of . Write

where and . From Lemma C.1, we have and . From Lemma C.2, we have . Therefore, the following two bounds hold:

which is ; in addition,

where . Therefore, for any fixed permutation , which implies that . This further implies conclusion (i) by Weyl’s inequality and .

(ii) We first prove the following conclusion: there exists diagonal scaling random matrix and random vector such that where is uniformly distributed over the centered sphere of dimension and radius .

To this end, we need to employ rescaled data where . Here superscript denotes rescaled data by . Recall that follows . After rescaling, follows . Let and define a matrix such that , which corresponds to each pair of samples. Clearly . Let , and correspondingly so that and , where

Other quantities are also defined for the rescaled data. For example, and are eigenvectors of and . Let .

Since the estimator is invariant to orthogonal transformation of the data, similar to Paul (2007), we can show is distributed uniformly over the unit sphere. Define . From the proof of (i), we know . So is uniformly distributed over a centered ball of radius . Hence it only remains to bound the difference of and to validate the claim.

Note that

It is not hard to show , which is in the same order as the first term. The second term is dominated by plus

where . Using the notations defined in the proof of Lemma C.1, we have

where and

The right hand side is of order by Lemma D.1. This implies . Thus by the theorem of Davis and Kahan (1970), we get . With (B.1), we have

The right hand side is since from above , , converges to and , which is true because

where the last equality can be seen from the proof of Lemma C.1. Hence we conclude, if ,

We are done proving the claim.

Now let us come back to our goal of bounding for any by matrix such that . Obviously,

Let . Then,

where the second inequality is due to for , and . Thus to bound the elementwise sup-norm , it suffices to show .

Let be standard normal distributed. Obviously, where is uniform over unit sphere of dimension . Provided , we only need to show . It follows from and

since is normally distributed with bounded variance. This completes the proof for (ii).

∎

Proof of Lemma C.1.

Recall that

For ease of notation, let us assume is the identity permutation and ignore the index in the following. Define where , with

and

Then, . Exchanging and , we further define , which share the same nonzero eigenvalues as . Now in order to prove the lemma, let us decompose where

We deal with first. Note that has the same eigenvalues as matrix , where is an matrix with iid rows. Therefore, we are in the low dimensional situation with fixed dimension . It is easy to see that

and thus by the central limit theorem, the diagonal element of is and the off-diagonal elements are of order . Therefore, write , we have with . By Weyl’s inequality,

By the definition of , , where the row of is . Let where . Therefore

Since each row of is Gaussian, by Lemma D.1 with , for any ,

In addition, we have . This is because

Therefore, . By Wely’s Theorem, Therefore, we conclude that for and for . ∎

Proof of Lemma C.2.

Similar to Lemma B.1, we can prove as well as . If , obviously the conclusion holds. So in the following we assume .

Appendix D A Technical Lemma

Recall that is the standardized version of the transformed data . We have the following theorem for , which will be useful for the proofs in Section 3 and 4.

Lemma D.1.

Let be the matrix () with rows . Assume to be iid sub-Gaussian random vector with for some constant . Condition (3.1) holds for . The columns of are denoted by of length . Then for , let , we have

| (D.1) |

with probability at least , where depend on . Here, is bounded from above for all and .

Proof.

Without loss of generality, let us assume all the ’s are non-negative and bounded away from zero. Otherwise, we subtract the minimal one from all the ’s. Let the new non-negative weights to be . Since all the eigenvalues concentrate to the same number, it is easy to separately consider the concentration for and , which both have nonnegative lower bounded weights.

Let , so . Assume without loss of generality that is decreasing and . First we have

Since is sub-Gaussian, by Theorem 5.39 of Vershynin (2010), we have with probability at least ,

If , without loss of generality we assume . Then since , the minimum eigenvalue of satisfies the conclusion. It remains to validate the conclusion for the maximal eigenvalue. According to the above, is bounded by

Thus the theorem holds for .

We only need to consider the case . This corresponds to conditioning on the event where . Obviously, with probability at least , the event holds. To prove (D.1), it suffices to show that with high probability

where is the -net covering the unit sphere and (Vershynin, 2010). Due to the following decomposition,

we have

Therefore,

| (D.2) | ||||

We need to separately bound the two terms on the right hand side.

Since ,

| (D.3) |

For a fixed and , we now bound . By Lemma D.2, choosing , since satisfies (3.1), we have

where is defined in Lemma D.2 and is bounded since is bounded. Choose so that and , which implies . So is bounded by . Therefore, from (D.3), we have

by choosing in the definition of large enough. This proves the first term in (D.2).

For the second term in (D.2), we apply the decoupling technique. By Lemma 5.60 of Vershynin (2010),

So we have

| (D.4) |

For each fixed and , we first consider the above probability conditioning on for . Let where is constructed by columns for and contains the coordinates of corresponding to . We know is sub-Gaussian since

where the last inequality is due to conditioning on the event . So there exists a constant independent of such that . Furthermore, the weighted sum of ’s is also sub-Gaussian distributed with . Hence, from (D.4),

where the right hand side is bounded by

by choosing a large enough in the definition of . So we bounded the second term.

Lemma D.2.

Let be a by matrix and . Suppose is an isotropic sub-Gaussian random vector, that is,

for all . For all ,

| (D.5) |

if furthermore the SVD decomposition of where is a by diagonal matrix and consist of left and right orthogonal singular vectors and (3.1) holds for , we have,

| (D.6) |

where and is the condition number of .

The above lemma is an extension of the exponential inequality for iid one dimensional sub-Gaussian variables proved by Laurent and Massart (2000). It is the Hanson-Wright inequality for the quadratic functional of a sub-Gaussian random vector. Rudelson and Vershynin (2013) showed this inequality for independent sub-Gaussian elements. Hsu et al. (2012) obtained the upper tail bound (D.5) under a much weaker assumption of general sub-Gaussian vector with dependency. However, they did not provide result for the lower tail bound. Note that quadratic functionals are different from linear functionals in that changing the sign of does not naturally give the lower tail bound. In the following, we prove (D.6) under (3.1). This bound is used for proving Lamma D.1.

Proof.

Denote so that . Write with decreasing diagonal elements. Since (3.1) holds for , we have for ,

Choose which is smaller than if while choose if . In any case, we can show that the right hand side is bounded by . Define an event . Then . Futhermore, we define

So (D.6) is equivalent to . Obviously . We bound as follows:

where the first inequality is a summation of the inequalities defined in events and ; the second inequality is due to the fact where and the last inequality is by (D.5). Thus we have proved . ∎

References

- Agarwal et al. (2012) Agarwal, A., Negahban, S. and Wainwright, M. J. (2012). Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions. The Annals of Statistics 40 1171–1197.

- Amini and Wainwright (2008) Amini, A. A. and Wainwright, M. J. (2008). High-dimensional analysis of semidefinite relaxations for sparse principal components. In Information Theory, 2008. ISIT 2008. IEEE International Symposium on. IEEE.

- Antoniadis and Fan (2001) Antoniadis, A. and Fan, J. (2001). Regularization of wavelet approximations. Journal of the American Statistical Association 96.

- Bai and Li (2012) Bai, J. and Li, K. (2012). Statistical analysis of factor models of high dimension. The Annals of Statistics 40 436–465.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica 70 191–221.

- Bai and Ng (2013) Bai, J. and Ng, S. (2013). Principal components estimation and identification of static factors. Journal of Econometrics 176 18–29.

- Belloni et al. (2011) Belloni, A., Chernozhukov, V. et al. (2011). -penalized quantile regression in high-dimensional sparse models. The Annals of Statistics 39 82–130.

- Berthet and Rigollet (2013a) Berthet, Q. and Rigollet, P. (2013a). Complexity theoretic lower bounds for sparse principal component detection. In Conference on Learning Theory.

- Berthet and Rigollet (2013b) Berthet, Q. and Rigollet, P. (2013b). Optimal detection of sparse principal components in high dimension. The Annals of Statistics 41 1780–1815.

- Bickel and Levina (2008a) Bickel, P. J. and Levina, E. (2008a). Covariance regularization by thresholding. The Annals of Statistics 2577–2604.

- Bickel and Levina (2008b) Bickel, P. J. and Levina, E. (2008b). Regularized estimation of large covariance matrices. The Annals of Statistics 199–227.

- Birnbaum et al. (2013) Birnbaum, A., Johnstone, I. M., Nadler, B. and Paul, D. (2013). Minimax bounds for sparse PCA with noisy high-dimensional data. Annals of statistics 41 1055.

- Cai and Liu (2011) Cai, T. and Liu, W. (2011). Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association 106 672–684.

- Cai et al. (2011) Cai, T., Liu, W. and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association 106 594–607.

- Cai et al. (2013a) Cai, T., Ma, Z. and Wu, Y. (2013a). Optimal estimation and rank detection for sparse spiked covariance matrices. Probability Theory and Related Fields 1–35.

- Cai et al. (2012) Cai, T. T., Li, H., Liu, W. and Xie, J. (2012). Covariate-adjusted precision matrix estimation with an application in genetical genomics. Biometrika ass058.

- Cai et al. (2013b) Cai, T. T., Ma, Z. and Wu, Y. (2013b). Sparse PCA: Optimal rates and adaptive estimation. The Annals of Statistics 41 3074–3110.

- Cai et al. (2013c) Cai, T. T., Ren, Z. and Zhou, H. H. (2013c). Optimal rates of convergence for estimating toeplitz covariance matrices. Probability Theory and Related Fields 156 101–143.

- Cai et al. (2010) Cai, T. T., Zhang, C.-H. and Zhou, H. H. (2010). Optimal rates of convergence for covariance matrix estimation. The Annals of Statistics 38 2118–2144.

- Catoni (2012) Catoni, O. (2012). Challenging the empirical mean and empirical variance: a deviation study. In Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, vol. 48. Institut Henri Poincaré.

- Choi and Marden (1998) Choi, K. and Marden, J. (1998). A multivariate version of kendall’s . Journal of Nonparametric Statistics 9 261–293.

- Cizek et al. (2005) Cizek, P., Härdle, W. K. and Weron, R. (2005). Statistical tools for finance and insurance. Springer Science & Business Media.

- Croux et al. (2002) Croux, C., Ollila, E. and Oja, H. (2002). Sign and rank covariance matrices: statistical properties and application to principal components analysis. In Statistical data analysis based on the L1-norm and related methods. Springer, 257–269.

- Davis and Kahan (1970) Davis, C. and Kahan, W. M. (1970). The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis 7 1–46.

- Fan et al. (2014a) Fan, J., Fan, Y. and Barut, E. (2014a). Adaptive robust variable selection. Annals of statistics 42 324.

- Fan et al. (2008) Fan, J., Fan, Y. and Lv, J. (2008). High dimensional covariance matrix estimation using a factor model. Journal of Econometrics 147 186–197.

- Fan et al. (2009) Fan, J., Feng, Y. and Wu, Y. (2009). Network exploration via the adaptive lasso and scad penalties. Annals of Applied statistics 3 521–541.

- Fan et al. (2014b) Fan, J., Li, Q. and Wang, Y. (2014b). Robust estimation of high-dimensional mean regression. arXiv preprint arXiv:1410.2150 .

- Fan et al. (2011) Fan, J., Liao, Y. and Mincheva, M. (2011). High dimensional covariance matrix estimation in approximate factor models. Annals of statistics 39 3320.

- Fan et al. (2013) Fan, J., Liao, Y. and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B 75 1–44.

- Fan et al. (2014c) Fan, J., Liao, Y. and Wang, W. (2014c). Projected principal component analysis in factor models. arXiv preprint arXiv:1406.3836 .

- Fan and Wang (2015) Fan, J. and Wang, W. (2015). Asymptotics of empirical eigen-structure for ultra-high dimensional spiked covariance model. arXiv preprint arXiv:1502.04733 .

- Fang et al. (1990) Fang, K.-T., Kotz, S. and Ng, K. W. (1990). Symmetric multivariate and related distributions. Chapman and Hall.

- Friedman et al. (2008) Friedman, J., Hastie, T. and Tibshirani, R. (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9 432–441.

- Hallin and Paindaveine (2006) Hallin, M. and Paindaveine, D. (2006). Semiparametrically efficient rank-based inference for shape. i. optimal rank-based tests for sphericity. The Annals of Statistics 34 2707–2756.

- Han and Liu (2013a) Han, F. and Liu, H. (2013a). ECA: High dimensional elliptical component analysis in non-gaussian distributions. arXiv preprint arXiv:1310.3561 .

- Han and Liu (2013b) Han, F. and Liu, H. (2013b). Optimal rates of convergence for latent generalized correlation matrix estimation in transelliptical distribution. arXiv preprint arXiv:1305.6916 .

- Han and Liu (2014) Han, F. and Liu, H. (2014). Scale-invariant sparse PCA on high-dimensional meta-elliptical data. Journal of the American Statistical Association 109 275–287.

- Hsu et al. (2012) Hsu, D., Kakade, S. M. and Zhang, T. (2012). A tail inequality for quadratic forms of subgaussian random vectors. Electronic Communications in Probability 17 1–6.

- Huber (1964) Huber, P. J. (1964). Robust estimation of a location parameter. The Annals of Mathematical Statistics 35 73–101.

- Hult and Lindskog (2002) Hult, H. and Lindskog, F. (2002). Multivariate extremes, aggregation and dependence in elliptical distributions. Advances in Applied probability 34 587–608.

-

Johnstone and Lu (2009)

Johnstone, I. M. and Lu, A. Y. (2009).

On consistency and sparsity for principal components analysis in high

dimensions.

Journal of the American Statistical Association 104

682–693.

URL http://amstat.tandfonline.com/doi/abs/10.1198/jasa.2009.0121 - Karoui (2008) Karoui, N. E. (2008). Operator norm consistent estimation of large-dimensional sparse covariance matrices. The Annals of Statistics 2717–2756.

- Kendall (1948) Kendall, M. G. (1948). Rank correlation methods. .

- Koenker (2005) Koenker, R. (2005). Quantile regression. 38, Cambridge university press.

- Lam and Fan (2009) Lam, C. and Fan, J. (2009). Sparsistency and rates of convergence in large covariance matrix estimation. Annals of statistics 37 4254.

- Laurent and Massart (2000) Laurent, B. and Massart, P. (2000). Adaptive estimation of a quadratic functional by model selection. Annals of Statistics 1302–1338.

- Levina and Vershynin (2012) Levina, E. and Vershynin, R. (2012). Partial estimation of covariance matrices. Probability Theory and Related Fields 153 405–419.

- Liu et al. (2012) Liu, H., Han, F. and Zhang, C.-h. (2012). Transelliptical graphical models. In Advances in Neural Information Processing Systems.

- Liu et al. (2003) Liu, L., Hawkins, D. M., Ghosh, S. and Young, S. S. (2003). Robust singular value decomposition analysis of microarray data. Proceedings of the National Academy of Sciences 100 13167–13172.

- Ma (2013) Ma, Z. (2013). Sparse principal component analysis and iterative thresholding. The Annals of Statistics 41 772–801.

- Marden (1999) Marden, J. I. (1999). Some robust estimates of principal components. Statistics & Probability Letters 43 349–359.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. The Annals of Statistics 1436–1462.

- Pang et al. (2014) Pang, H., Liu, H. and Vanderbei, R. (2014). The fastclime package for linear programming and large-scale precision matrix estimation in r. The Journal of Machine Learning Research 15 489–493.

- Paul (2007) Paul, D. (2007). Asymptotics of sample eigenstructure for a large dimensional spiked covariance model. Statistica Sinica 17 1617–1642.

- Paul and Johnstone (2012) Paul, D. and Johnstone, I. M. (2012). Augmented sparse principal component analysis for high dimensional data. arXiv preprint arXiv:1202.1242 .

- Posekany et al. (2011) Posekany, A., Felsenstein, K. and Sykacek, P. (2011). Biological assessment of robust noise models in microarray data analysis. Bioinformatics 27 807–814.

- Rachev (2003) Rachev, S. T. (2003). Handbook of Heavy Tailed Distributions in Finance: Handbooks in Finance, vol. 1. Elsevier.

- Ravikumar et al. (2011) Ravikumar, P., Wainwright, M. J., Raskutti, G. and Yu, B. (2011). High-dimensional covariance estimation by minimizing -penalized log-determinant divergence. Electronic Journal of Statistics 5 935–980.

- Rothman et al. (2009) Rothman, A. J., Levina, E. and Zhu, J. (2009). Generalized thresholding of large covariance matrices. Journal of the American Statistical Association 104 177–186.

- Rudelson and Vershynin (2013) Rudelson, M. and Vershynin, R. (2013). Hanson-wright inequality and sub-gaussian concentration. arXiv preprint arXiv:1306.2872 .

- Ruttimann et al. (1998) Ruttimann, U. E., Unser, M., Rawlings, R. R., Rio, D., Ramsey, N. F., Mattay, V. S., Hommer, D. W., Frank, J. A. and Weinberger, D. R. (1998). Statistical analysis of functional mri data in the wavelet domain. Medical Imaging, IEEE Transactions on 17 142–154.

- Shen et al. (2013) Shen, D., Shen, H. and Marron, J. (2013). Consistency of sparse PCA in high dimension, low sample size contexts. Journal of Multivariate Analysis 115 317–333.

- Tyler (1982) Tyler, D. E. (1982). Radial estimates and the test for sphericity. Biometrika 69 429–436.

- Vershynin (2010) Vershynin, R. (2010). Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027 .

- Visuri et al. (2000) Visuri, S., Koivunen, V. and Oja, H. (2000). Sign and rank covariance matrices. Journal of Statistical Planning and Inference 91 557–575.

- Vogel and Fried (2011) Vogel, D. and Fried, R. (2011). Elliptical graphical modelling. Biometrika 98 935–951.

- Vu and Lei (2012) Vu, V. Q. and Lei, J. (2012). Minimax rates of estimation for sparse PCA in high dimensions. arXiv preprint arXiv:1202.0786 .

- Wu and Liu (2009) Wu, Y. and Liu, Y. (2009). Variable selection in quantile regression. Statistica Sinica 19 801.

- Yuan (2010) Yuan, M. (2010). High dimensional inverse covariance matrix estimation via linear programming. The Journal of Machine Learning Research 11 2261–2286.

- Yuan and Lin (2007) Yuan, M. and Lin, Y. (2007). Model selection and estimation in the gaussian graphical model. Biometrika 94 19–35.

- Zhao et al. (2014) Zhao, T., Roeder, K. and Liu, H. (2014). Positive semidefinite rank-based correlation matrix estimation with application to semiparametric graph estimation. Journal of Computational and Graphical Statistics 23 895–922.

- Zou et al. (2006) Zou, H., Hastie, T. and Tibshirani, R. (2006). Sparse principal component analysis. Journal of computational and graphical statistics 15 265–286.

- Zou and Yuan (2008) Zou, H. and Yuan, M. (2008). Composite quantile regression and the oracle model selection theory. The Annals of Statistics 1108–1126.