and

t1Supported in part by the Austrian Science Fund (FWF) under grant P25815 and P28661 and by the Vienna Science and Technology Fund (WWTF) under grant MA14-008. t2Supported in part by the Austrian Science Fund (FWF) under grants P26736 and Y782-N25.

The Sharp Constant for the Burkholder-Davis-Gundy Inequality and Non-Smooth Pasting

Abstract

We revisit the celebrated family of BDG-inequalities introduced by Burkholder, Gundy [8] and Davis [10] for continuous martingales. For the inequalities with we propose a connection of the optimal constant with an ordinary integro-differential equation which gives rise to a numerical method of finding this constant. Based on numerical evidence we are able to calculate, for , the explicit value of the optimal constant , namely . In the course of our analysis, we find a remarkable appearance of ”non-smooth pasting“ for a solution of a related ordinary integro-differential equation.

keywords:

[class=MSC]keywords:

1 Introduction

Theorem 1.1.

There is a constant such that, for every bounded stopping time , we have

| (1) |

Here denotes a standard Brownian motion, starting at By we denote the corresponding running maximum of the absolute value

It is obvious that the set of constants which satisfy inequality (1) is a closed, unbounded interval in . By the results of [5] it is known that is contained in this set. To the best of our knowledge, this is the smallest constant known in the previous literature. In the present paper we establish the optimal value for this constant.

Theorem 1.2.

The paper is organised as follows. As usual in stochastic control theory, we first introduce the value function of the optimal stopping problem which corresponds to the inequality (1). After some structural facts about the stopping problem we turn to some analytic properties of the value function in Section 3. We deduce the OIDE (ordinary integro-differential equation) which is referred to in Theorem 1.2. The subsequent section is devoted to properties of solutions to the fundamental OIDE (30) which are needed to identify these solutions with the value function of the stopping problem in Section 5.

The critical associated to the optimal constant via (30) below also turns out to be of somewhat independent interest: if denotes the first moment, say after , when is bigger than , then is finite or infinite depending on whether is smaller or bigger than (Proposition 5.6 and 5.7). In Section 6 we state a pointwise version of the BDG inequalities and in Section 7 we briefly discuss the case of general without entering into a numerical analysis. Finally, in Section 8 we discuss the fact why the constant which was established by D. Burkholder [7] as the optimal constant for (1) in the case of martingales which are not necessarily continuous, is different from the present constant which holds true for continuous processes. We relate this discrepancy with a certain lack of concavity of the value function.

2 The Value Function of an Optimal Stopping Problem

Fix a constant Following a well-known path in optimal control theory we define the value function

| (2) |

where denotes the set of bounded stopping times and denotes the expectation conditionally on starting the Brownian motion at time with the values The domain of definition of is

| (3) |

Equivalently we can write

| (4) |

which follows from the strong Markov property and stationarity of increments of Brownian motion.

Denote by the infimum of such that (1) holds true. Clearly still satisfies (1). If then , otherwise we have:

Lemma 2.1.

Let then defined via (2) is

-

(i)

continuous,

-

(ii)

finite-valued, and

-

(iii)

is decreasing for fixed .

In particular (ii) follows from the bounds

| (5) |

Proof.

The lower bound of follows from choosing the stopping time . For the upper bound observe that we can estimate for an arbitrary

Taking expectations we get the upper bound for from the representation in (4).

Next observe that for we have for

by concavity of the square root. Now (iii) follows by taking expectations suprema.

For (i), please refer to Sections 7 and 9.2 in [14]. ∎

To exclude the trivial case, we assume in the sequel that

For fixed , the stopping region and the non-stopping region are defined by

| (6) |

To characterize the stopping region first note that it is certainly not a good idea to stop when .

Lemma 2.2.

Let with Then

Proof.

Consider the first exit time of the interval . ∎

Next we observe a useful scaling property of (compare Burkholder [7]).

Lemma 2.3.

For and , we have

| (7) |

Proof.

This follows directly from the scaling property of Brownian motion: if is a standard Brownian motion, then again is a standard Brownian motion. Also, a random time is a stopping time for the first process if and only if is a stopping time for the second process. ∎

This allows us to derive the following Lemma where the first part is a direct consequence of Lemmas 2.1 (iii) and 2.3 and the second part is technical and deferred to the appendix in Lemma B.3.

Lemma 2.4.

Let and . Then implies .

Hence, for fixed there is a smallest such that if and only if

| (8) |

In fact, we have

The next result is a standard result in optimal control theory and also intuitively rather obvious. Again, the proof is deferred to the appendix.

Lemma 2.5.

Suppose and let be in the non-stop region . Consider a Brownian motion starting at time conditionally on and Let be the first hitting time of the stopping region , i.e.

| (9) |

Then the value process stopped at time

| (10) |

is a martingale.

The unstopped value process

| (11) |

still is a supermartingale.

We conclude this section with a minor technical remark. In the above statement, as well as in most of the paper, we follow the usual language of optimal control theory to condition on the event . As this is a null set under this procedure needs some proper interpretation in order to make it rigorous.

Let us now introduce some notation to make this a bit clearer.

We denote by the (right-continuous, saturated) filtration generated by the Brownian motion . Of course, in definition (2) the stopping time is understood with respect to this filtration. But it is clear from the Markov property that, for fixed , we may assume that depends only on the behavior of the Brownian motion after time and not on the previous behavior of (except for the requirements and ).

To formalize this fact, we denote by the (right-continuous, saturated) filtration generated by . A stopping time (i.e., with respect to the filtration ) then may also be considered as a randomized stopping time with respect to the filtration , the randomization given by the trajectories of . As is independent of the filtration , we conclude that the value of (2) does not change whether we optimize over the randomized or the non-randomized stopping times with respect to the filtration . For an introduction to the notion of randomized stopping times, please refer to [3]

The bottom line of these considerations is that we may assume w.l.o.g. in (2) that is a stopping time with respect to the filtration .

Now, the statement Lemma 2.5 could be rephrased without referring to conditioning on a null set, by noting that is a stopping time with respect to the filtration .

All other statements in the paper referring to conditioning on the values and could be made rigorous in an analogous way if the reader insists, but we do not further elaborate on these technicalities.

3 The Value Function from an Analytic Perspective

Again fix . Differentiating the scaling equation (7) with respect to and setting we obtain, at least formally, the PDE

| (12) |

The optimal constant for inequality (1) will be determined by analyzing whether this PDE has a reasonable solution for given or not.

We need some preparation. For we denote by the density of the distribution of the stopping time where is a Brownian motion starting at

Define

It is well-known (e.g. [11, Exercise 2.2.8.11]) that there is an explicit representation of as an infinite sum. By differentiation of each summand we obtain an explicit infinite sum representation also for (see the appendix below).

The function appears in the formulation of the subsequent lemma which will turn out to be of crucial relevance for our analysis.

Lemma 3.1.

Let be a continuous function such that

-

(a)

is Lipschitz continuous and

-

(b)

is decreasing.

Furthermore let be defined by for some fixed . Consider a standard Brownian Motion and define to be the first hitting time of . Suppose that is a supermartingale and is a martingale. Further assume that the process is uniformly integrable where is given by .

Then,

-

(i)

(13) -

(ii)

(14)

Observe that (i) in the above Lemma would follow directly from Ito’s formula if we assume that is sufficiently differentiable by considering

| (15) |

which is the increment of a martingale. The process is non-decreasing and its variation is a.s. singular with respect to Lebesgue measure. A necessary condition for to be a martingale therefore is that vanishes a.s. with respect to the variation measure of . This indicates that should hold true whenever and is in the non-stop region . In particular, we should have , for

Proof of 3.1.

(i) For as in (13) define, conditionally on and the stopping times

| (16) | ||||

| (17) |

Recall that the random variable is a stopping time with respect to the filtration . Note that the process , starting at and , also remains in up to the stopping time . To see this, we distinguish two cases:

-

(i)

: Here we have and thus .

-

(ii)

: In this case is the same for and .

As we have that is a.s. strictly positive. This implies that

| (18) |

as , almost surely.

We may write

| (19) | ||||

Here we use that conditionally on as by definition. Furthermore we make use of the martingale property of and the optional stopping theorem. For the use of the latter we need the assumption that is uniformly integrable.

On the set we have for both initial conditions and . Therefore, the value is the same under both initial conditions. It follows that

On the remaining set we have . Because is Lipschitz continuous in the variable with some constant we may estimate

(ii) As is a martingale before hitting we have for as above that

where the density is given by

| (20) |

We can use this relation to calculate the derivative w.r.t. the second component:

We split this integral into two parts at some point and observe that is continuous and for pointwise at and thus by Dini’s Theorem also uniformly (monotone) on any interval , for . Therefore we have

| (21) | ||||

for given by

As before, because is decreasing and is concave, we have . Therefore the integrand is dominated by .

For we can then estimate

This probability tends to uniformly in , thus the integrals over can be neglected and we can replace by in (21).

For the other part of the integral we first observe that

The last integral converges to for by monotone convergence.

We conclude by setting for , making the estimate

and then taking the limit for . ∎

We can now apply this technical Lemma to our value function by checking that the assumptions of the previous Lemma are satisfied by the value function :

Lemma 3.2.

Let be the value function for (2). Then,

-

(i)

(22) -

(ii)

(23)

Proof.

is continuous by Lemma 2.1 and Lipschitz-continuous in by definition. We also have is decreasing by Lemma 2.1. Furthermore is a martingale up to hitting by Lemma 2.5. Thus, setting , and , it remains to check the required uniform integrability condition. We have

where the first estimate follows because the function is decreasing in . The second inequality is due to the fact that is decreasing in and increasing in as well as . Now, and has exponential moments and is therefore integrable which yields the desired uniform integrability.

Observe that is smaller than the first hitting time of the non-stop region no matter whether we condition on or which warrants the use of Lemma 2.5. ∎

The subsequent lemma shows that, for , the behavior of and follows a different pattern than the one given by Lemma 3.2. We find that

| (24) |

where we have to interpret this equation properly.

Lemma 3.3.

For we have

| (25) |

Proof.

For we have

for in a neighbourhood of . ∎

To abbreviate notation we shall sometimes denote by the function (recall that we keep and the corresponding fixed). We thus obtain the following integro-differential equation for

Lemma 3.4.

The function satisfies the following equations

| (26) | ||||

| (27) |

Proof.

The first assertion is obvious, as we have

| (28) |

Let us discuss the behaviour of the function at . As observed in the previous section, is continuous so that we must have “continuous pasting” at It is the immediate reflex – at least it was so for the present authors – to expect smooth pasting of at i.e. By (26) and (27) this would result in determining by equating with To our big surprise this turned out not to be the case; after some time of reconsidering we had to conclude that there is little reason why the smooth pasting principle should prevail in the present context. Here is one intuitive reason: for a fixed number we have that for almost all trajectories of a Brownian motion , starting at , there is no such that the two equalities are simultaneously verified. By Lemma 2.4 we conclude that a discontinuity of the derivatives of can only take place where these two equations are simultaneously satisfied. Roughly speaking: the Brownian motion “does not see” a kink of the function at

As a matter of fact, this natural example of a case of non-smooth pasting in the case of continuous martingales seems to us a remarkable feature of the present paper. The literature on non-smooth pasting is generally revolving around non-continuous processes. Some examples of non-smooth pasting for processes with jumps can be found in [1], [2], [6], [9] and [14].

4 The Integro-Differential-Equation

Fix the parameters and . We consider the ordinary integro-differential equation for the function

| (29) | |||||

| (30) |

where is given by (3).

Here the fixed behaviour (29) of , for , is considered as the initial condition, and subsequently the OIDE (ordinary integro-differential equation) (30) is solved by letting decrease from to . For , the derivative in (30) is understood as the left limit of when increases to

It is standard to verify that, for and the solution of (29) is well-defined for and depends smoothly on the parameters and On the other hand, the term on the left hand side of (30) indicates that only for special cases of and this solution can be extended to a continuous and finitely valued function defined for all .

The evidence resulting from our numerical analysis of the solutions , in dependence of and , can be resumed as follows:

Numerical Evidence 4.1.

For , the solutions of the OIDE (30) tend to , for , while, for , the solutions tend to , for . We have and .

The functions and are monotone increasing and

| (31) |

Finally, we find the numerical values

| (32) |

We have not been able to provide a mathematically rigorous proof of the above assertions and only rely on the numerical evidence (which is based on Euler-type simulations in Python with variable step sizes). We therefore consider the above statements rather as hypotheses underlying our subsequent results and we shall carefully point out in the subsequent statements where we rely on this evidence.

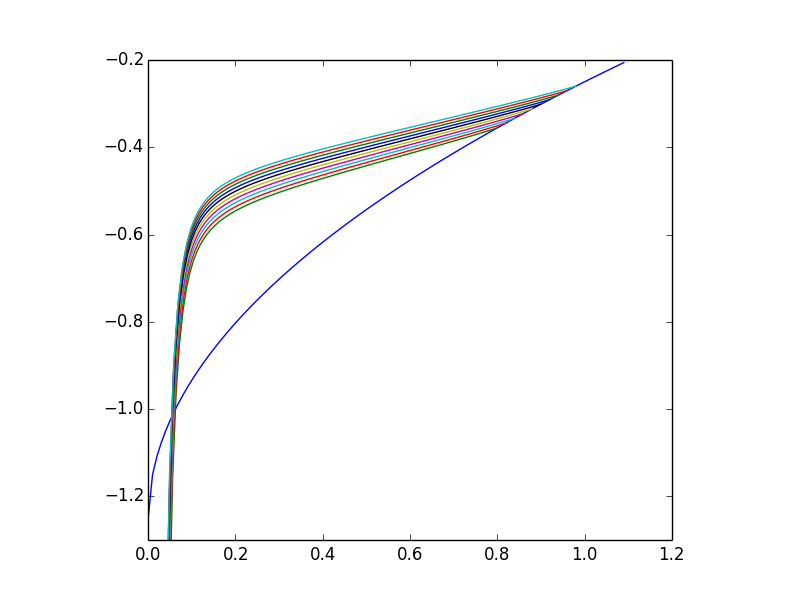

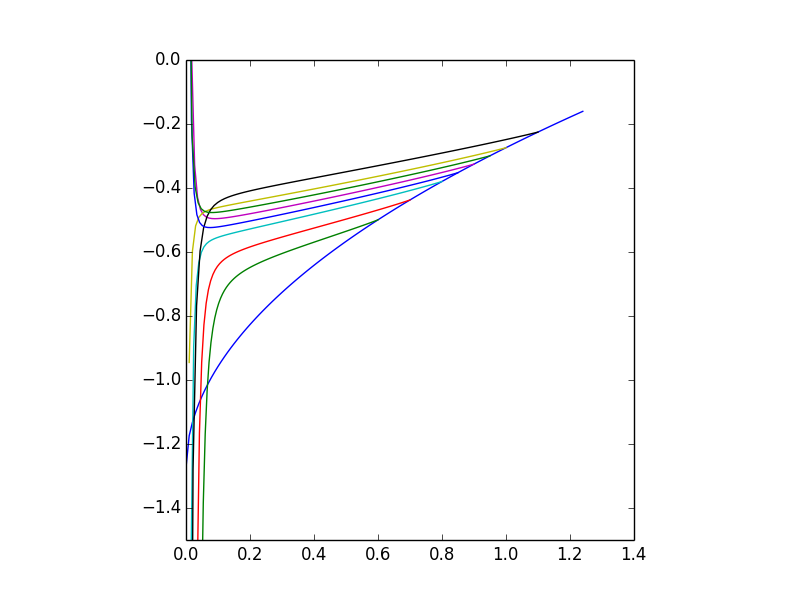

For example, for which is case (ii) above we illustrate the situation by Figure 1.

For , which is case (iii) above, we find and as illustrated in Figure 2.

When decreases to the critical value the numerics suggest that the length of the intervals decreases to zero and that these intervals shrink to a single point for which we find . It is convincing from the numerics that the limiting solution then is well-defined for all by letting This function is monotone increasing and such that lies above the function Clearly we expect that must be the “right” solution, which may be identified with the value function defined in (2) for the optimal constant and, in particular, that equals the optimal constant in the Burkholder-Davis-Gundy inequality (1). We shall subsequently deduce this result more formally.

5 Identifying the Value-Function

Admitting the Numerical Evidence 4.1 we shall show that the function , obtained above from the analysis of the OIDE (30), indeed determines the value function as defined in (2) for the constant and that this constant is indeed the optimal Burkholder-Davis-Gundy constant in inequality (1).

Starting from a solution of the OIDE (30) for parameters and such that extends continuously to a finite value we may extend this solution (by slight abuse of notation) to a function , defined on , by first letting

| (33) |

where is defined in Section 3. For general we use (7) to define

| (34) |

For later reference, we note that implies

| (35) |

Lemma 5.1.

Fix and such that extends continuously to a finite and admit the Numerical Evidence 4.1 (i) and (iii). Let be a Brownian motion starting at some time at and . The process is then a local super-martingale. It is a local martingale up to entering the stopping area .

For the proof we need the following Lemma to justify the use of Ito’s formula for a function that is not smooth everywhere but where the Brownian Motion hardly ever touches the set where it is not differentiable.

Lemma 5.2.

Let be a continuous function and such that

-

(a)

the derivatives and exist and are continuous on the interior of , and

-

(b)

,

-

(c)

, and

-

(d)

for .

Define . For a standard Brownian Motion let be the first hitting time of for . Then,

-

(i)

is a local supermartingale, and

-

(ii)

is a local martingale.

Proof.

This follows at least formally from the assumptions and Ito’s formula

| (36) |

To address this in a more formal way, let and define the stopping times by and

We also denote by the union which is a predictable subset of Denoting by the set simply equals Fixing the Lebesgue-measure of tends to zero, for almost all

Fix a bounded stopping time such that remains bounded. It follows that as well as also remain bounded on so that

is a martingale and is the complement of Indeed, it suffices to reason on the stochastic intervals and to observe that remains constant on these intervals.

Turning to the remaining part

we shall show that along a sequence these processes tend almost surely to the non-increasing process

Indeed, the dominated convergence theorem for Ito-Integrals yields convergence in probability and thus subsequence convergence almost surely. Fixing this sequence of ’s we can take the process to the appropriate limit. ∎

Proof of Lemma 5.1.

On the boundary, for , we can apply the definition of to obtain

The last equality is exactly the OIDE (30). Applying Lemma 3.1 (ii) one obtains that the last expression is equal to

where all the assumptions of this Lemma are easily checked. Clearly the left and right derivatives of agree. It follows that and more generally that for . For we can derive as in Lemma 3.3 that

This expression is monotone decreasing in , and is necessarily non-positive at so that holds. We conclude that, for arbitrary , .

Having established that and for we may derive, at least formally, the assertion of the present lemma from (56) and Ito’s formula as in (15).

Now, we can conclude using Lemma 5.2 ∎

Let us now observe the following relations between value functions to the optimal stopping problem and solutions to the OIDE (30).

Lemma 5.3.

Proof.

For , we have .

For denote by the stopping time as in (17) above, conditionally on Note that then is a uniformly integrable martingale. To see this, we make a distinction for and where is the stopping time :

-

1.

: The domain of is bounded by and . Clearly is bounded on this domain.

-

2.

: Here the properties of given in Lemma 2.5 allow us to see that one can rewrite the process as

where is again the first time where holds. Note that this holds because is now constant for , and it is clearly the definition of a uniformly integrable martingale, provided the conditional expectation is well defined, which it is by the estimate

Proposition 5.4.

Proof.

To show suppose that is a constant satisfying the Burkholder-Davis-Gundy inequality (1), i.e. suppose that . Then by Lemma 5.3 we have that satifies the OIDE (30) for this choice of and the corresponding separating from .

As is increasing in and satisfies we conclude from the Numerical Evidence 4.1 (i) and (ii) that . This yields

To show conversely that consider the function By Lemma 5.1 the process is a local supermartingale. Hence we have, conditionally on and for each bounded stopping time and localizing sequence .

We can finally summarize these results to proof the main theorem.

Proof of Theorem 1.2.

Suppose that is the optimal constant for (1) and let the corresponding critical value given by Lemma 2.4. Then satisfies the OIDE (29) and this solution is increasing in and satisfies

As shown in the previous section there is a minimal allowing for such a solution, for an appropriately chosen This value of therefore must coincide with the optimal value for the Burkholder-Davis-Gundy inequality (1).

Remark 5.5.

It is interesting to consider, for a fixed constant , the relation between the value-function defined in (2) and the corresponding solutions of the OIDE (30). In this case the numerical evidence 4.1 (iii) indicates that there are two bounded solutions and Which of the two is the “good one”, i.e. which one equals the value function ?

To answer this question, first note that, for , we clearly have the monotonicity relation . It is also easy to see that , where is associated to the value function via Lemma 2.4. In other words, the stopping region for the function in (2) is bigger than the stopping region for the function

It follows from the numerical evidence that the value for which we have is the only candidate for the “good” solution while for for which we have we cannot have We can conclude from Lemma 5.3 that the value function indeed equals the solution of the OIDE (30).

The fact that cannot be the “good” solution has the following consequence which is interesting in its own right (compare [15]).

Proposition 5.6.

Proof.

Define the stopping time by

| (39) |

Clearly , as we may equivalently define

| (40) |

We claim that if and only if . Indeed, it follows from (40) that the law of , conditionally on , is that of the first hitting time of the level by the absolute value of a Brownian motion starting at . We may (very crudely) estimate .

Noting that at time we have we may estimate

Hence we obtain

which readily shows that . This implies that .

So let us suppose that and work towards a contradiction.

Define the stopping region relative to as

and the corresponding non-stopping region by .

We condition on some fixed . Note that is the first time when leaves .

Admitting the Numerical Evidence 4.1 (iii), associate to the constant such that is a solution of the OIDE (30) which remains bounded as We write for its extension defined in (34). In contrast, we denote by the value function as defined in (2) for the constant .

The process is a local martingale by Lemma 5.1, where the present corresponds to in the statement of this lemma.

In addition we show that this local martingale is a uniformly integrable martingale up to time , i.e. the family of random variables , where ranges in the stopping times , is uniformly integrable. Recall the scaling relation

and note that remains in the interval so that, by compactness, the term remains bounded by some constant . Therefore

If we infer from the Burkholder-Davis-Gundy inequality (this time the reverse inequality to (1)) that the random variable is integrable. Hence the family of random variables is dominated by the integrable random variable which shows that the local martingale is of class D and is thus a uniformly integrable martingale.

Hence, conditionally on we obtain

| (41) |

We now pass to the process again conditionally on . By Lemma 2.5 we know that this process is a supermartingale. Repeating the above argument, we obtain that this supermartingale is uniformly integrable up to time . Hence

| (42) |

The above result is complemented by the following estimate in the reverse direction.

Proposition 5.7.

Admitting the Numerical Evidence 4.1 (iii), we have, for , that the stopping time

| (43) |

satisfies

| (44) |

Proof.

Similarly as in the proof of the previous proposition, we define

We shall show that

| (45) |

which will imply (44).

We condition on in the non-stop region defined as in the preceding proof, and will show

| (46) |

for some constant , which will imply (45) by integrating over the values and .

We associate to the corresponding such that the solution of the OIDE (30) remains bounded (Numerical Evidence 4.1 (iii)).

Using the Numerical Evidence 4.1 (iii) there is some such that the solutions of the OIDE (30) and the value function for the optimal constant are separated by some , i.e.

| (47) |

Indeed, for we have and . For we have by (31) so that by compactness we obtain a separating constant .

More generally, we obtain from (33)

| (48) |

Similarly as in the above proof we consider, conditionally on , the processes

Both are local martingales up to time . Let be a sequence of localizing, bounded stopping times, , increasing to .

Hence, letting , for each

Using the scaling relation again, we get

| (49) |

Remark 5.8.

As regards the limiting case when we define in (43) by replacing by the critical value we conjecture that we obtain But we were not able to prove this result.

6 A pointwise version of one of Davis’ inequalities

The value function allows to derive a pointwise version of the Burkholder-Davis-Gundy inequality (1), which holds true in an almost sure sense rather than in expectation as stated in (1). This line of argument, inspired by the idea of robust superhedging from mathematical finance, is well-known (see e.g. [5] and [4]).

Theorem 6.1.

Denote by the value function (2) associated to the optimal constant and consider the Brownian motion with its (right continuous, saturated) natural filtration .

There is a predictable process satisfying , for each , given a.s. by

| (50) |

for Lebesgue almost all , such that, for every bounded stopping time ,

| (51) |

Before giving the proof we observe the well-known fact that (51) trivially implies (2) by taking expectations on both sides of (51).

Proof.

Lemma 2.5 states that the continuous process

is a super-martingale, starting at . sBy Doob-Meyer we may decompose as

| (52) |

where is a continuous local martingale and is a continuous non-decreasing predictable process, and .

In fact, is a square integrable martingale as we will show in Lemma A.1 in the appendix.

By martingale representation we may find a predictable process with , for each such that

7 BDG-Inequalities for general

The above procedure can be easily modified to obtain similar results for the inequalities with . Lemma 2.2 and 2.4 stay essentially the same, with a different scaling given by

This leads to the PDE

and the OIDE

for and the starting condition for .

In principle a similar analysis as in the present paper should provide explicit numerical values and , in dependence of . We leave this task to future research.

On the other hand, for the present method does not seem to apply and some new idea is needed.

8 Relation to the Burkholder constant

In this section we consider martingales also allowing for jumps and we focus (w.l.o.g.) on martingales defined on a finite probability space (see Lemma 8.2 below). The BDG inequality (1) reads in this context as

| (53) |

where denotes the quadratic variation process. It was shown by D. Burkholder [7] that in this context the sharp constant equals .

One may ask for a deeper reason why we obtain a different sharp constant in (1) for continuous martingales as for martingales also having jumps. One reason is that the value function fails to have a certain concavity property.

Fix a point as well as . Define the points by

We also define and .

Proposition 8.1.

There exist as well as , such that

| (54) |

Of course, we could verify the above proposition in a trivial way by numerically analyzing the function and detecting explicitly some and . It is also clear where we should search for such a “bad” triple , namely in a neighborhood of the “kink” related to the “non-smooth pasting” (Figure 1 and 2) which displays a strong form of non-concavity.

But this is not our point. The purpose of the above statement is to show how the non-concavity (54) of the value function is related to the difference between the case of continuous martingales and the case of martingales with jumps.

Also note that the equations in the interior of and on the non-stopping boundary of (i.e. (22) and (15) above), imply that in the (properly interpreted) case of infinitesimal increments and we do have a “” in (54) above. This is the message of Lemma 2.5.

Proof of Proposition 8.1.

Admitting the subsequent lemma, we consider a dyadic martingale starting at .

Let us fix some notation: The underlying probability space is given by

and the filtration is given by . Consider the process

where is the value function (2) associated to the optimal constant for continuous processes.

It may happen that is a super-martingale. In this case

so that we obtain the inequality

However, we know that is smaller than the sharp constant for martingales with jumps so that there must exist some dyadic martingale such that the corresponding process fails to be a supermartingale.

This means that there is some and such that – with slight abuse of notation – we find

as well as

such that inequality (54) holds true. ∎

For the following Lemma recall that a martingale is dyadic if the increment can attain at most two values, conditionally on ,.

Lemma 8.2.

Proof.

The equivalence (ii) (iii) is standard but for the convenience of the reader we will recall the argument for the non-trivial implication (ii) (iii).

First, we can reduce the problem to discrete -martingales: Fix an -bounded martingale , based on a filtered probability space and consider the martingales for . If they fulfill (53), then letting yields that satisfies (53).

Now, fix an -bounded martingale on a filtered probability space . Consider the net of finite subfiltrations of this filtration and their associated martingales (i.e. ). By (ii), every satisfies (53). The limit of is and (iii) follows.

The implication (ii) (i) is trivial.

To show (i) (ii) first observe that without loss of generality we can assume to be deterministic. First, we can translate the martingale such that it has mean . Second, if is random, then define a martingale with and for . Then and .

Now, suppose first that is just a one step martingale on a finite probability space with . We then have that is a finitely valued random variable with .

By possibly passing to a bigger (still finite) we may find a partition of such that takes at most values on each and

We now define a dyadic martingale by and

Clearly the variables and are equal in law. This shows that, at least for , we may associate to every finitely values martingale a dyadic martingale such that (53) holds true for if and only if it does so for .

It is rather obvious how to continue the above construction in an inductive way so that we may associate to each finitely valued martingale a dyadic martingale such that and are equal in law. This readily shows (i) (ii). ∎

Appendix A The Martingale Property of the Value Process and Square Integrability

Proof of Lemma 2.5.

We denote the function appearing on the right side of (5) by :

For fixed and we denote by the value function defined similarly as in (2), but where we only allow for stopping times which are bounded by . Clearly increases to as , pointwise for Also note that Fix and a bounded stopping time . We have to show that

| (55) |

By the monotone convergence theorem it will suffice to show that

| (56) |

for where is the stopping time defined conditionally on by

We then have that is bounded by and increases a.s. to . The crucial property is

and, more generally, for any stopping time

This classical result can be found in [13, Theorem 2.2]. Putting this together and taking , we obtain (56).

The proof of the supermartingale property which still holds true, after time is identical with an inequality instead of an equality.

∎

We can even show that the value process is bounded in up to some fixed time :

Lemma A.1.

The supermartingale given by

is uniformly bounded from above and bounded in . Furthermore the martingale component of its Doob-Meyer decomposition is also bounded in and we obtain the following quantitative estimates for every stopping times with :

-

(i)

-

(ii)

,

-

(iii)

.

Proof.

We first observe that holds as a consequence of the proof of Lemma 2.4 which gives us the estimate . Letting this also imples and we can show (i) by

is monotone increasing in and monotone decreasing in and . So we can observe for the positive part of that

For the negative part we can use and estimate

In summary we have

To show the last assertion, we now split into a sum of bounded processes in the following way. Define the stopping times by

and define the processes , obtained by starting at time and stopping it at time :

Of course, we have and the trajectories of are only different from zero on the set .

The probability of these events can be estimated by

| (57) |

for some constants and .

Using a classical inequality on uniformly bounded supermartingales (apparently due to P. Meyer [12]) we obtain that each is a square integrable martingale whose norm can be estimated by

| (58) |

for some constants depending only on .

For the convenience of the reader we spell out the message of Meyer’s Theorem [12, Theorem 46] in the present context.

Theorem A.2 (Meyer).

Let be a uniformly bounded supermartingale

Denoting by its Doob-Meyer decomposition we get that is a square integrable martingale whose norm can be estimated by

Proof.

By standard approximation results it will suffice to show the result for a super-martingale in finite discrete time. Note that in this case we have and

so that

We may telescope to obtain

By taking expectations we get

The final term is uniformly bounded as

This yields

To obtain a bound for we use the relation and to get

∎

Appendix B Some facts on the stopping time of first leaving a corridor

We discuss the first exit time of the interval for some for a standard Brownian motion started at .

This stopping time has a well-known density and a well-known Laplace-Transform (see e.g. [11, Section 2.2.8.C] given by

One can calculate the expected value of the stopping time by noting that so that . The Jensen-inequality directly implies that the fractional moments of order less than also exist and one has the estimate . This motivates to conjecture that for . We can get an expression for this moment using the Laplace-transform above by the formula , which we can evaluate to

where a substitution was used. It can be shown that both of these integrals are in fact finite for positive , but we are only interested in the above limiting behavior of this expression. To see this first note that the integrands of both integrals are always positive. Furthermore the hyperbolic tangent converges to . Therefore we can fix a constant such that for we have that for . Putting this together we make the following estimate:

The last expression now obviously diverges for . The following Lemma which we will need later on uses the above observations:

Lemma B.1.

Let be an arbitrary constant. There exist such that

Proof.

By the above observations we can choose small enough to obtain . We also have for small enough by monotone convergence of to for . ∎

We can now proceed to show the following facts about to prove the final statement of Lemma 2.4.

Lemma B.2.

Let and the corresponding value function. The map is decreasing and if it follows that .

Proof.

We need a quantitative version of Lemma 2.1 (ii) which already shows that is decreasing. First choose some to be a bounded stopping time which achieves

| (59) |

such that

| (60) |

for arbitrary . It is clear by definition of that there exists a stopping time which satisfies (59). Suppose there is no appropriate stopping time such that (60) is satisfied, then there is an optimizing sequence of bounded stopping times which converge to in probability and thus a subsequence which converges almost surely. This would imply that which contradicts the assumptions of the Lemma.

Now, we can consider the stopping time as a randomized stopping time with respect to the filtration . The shifted stopping time is then a randomized stopping time with respect to . We can now estimate

To get from the second to the third line, we used that by definition and . We dropped the superscript to emphasize that we now view as a stopping time with respect to the filtration . To obtain the fourth and the fifth line in the derivation, we observe that the map is non-negative and non-decreasing, and use (60). The sixth line can be derived by noting that is concave and thus lies completely under its tangent at . The last inequality holds for small enough. In the same way one can actually show that as long as the spread is strictly positive, it is also strictly decreasing. ∎

Lemma B.3.

Let and the critical point separating from . Then

-

1.

and

-

2.

.

Proof.

(1): Assume . This means that we actually have

for all . We then obtain for arbitrary that

by the supermartingale property of the value-process. This is a contradiction to Lemma B.1 for small enough and .

(2): Assume . This means that everywhere. As we also have . By Lemma B.2 we can set . Now fix some and . We can then make the following estimate, where we use twice the fact that the function is decreasing and is defined as before:

Now we can eliminate on both sides and note that , and do not depend on . The last term however goes to for by dominated convergence (since and ). This leads to the desired contradiction. ∎

Acknowledgements

Thanks go to an extremely helpful referee who provided a very careful report. The paper in its present form owes much to his suggestions. We also thank Mathias Beiglböck for his insight and advice in the course of many discussions on the present paper and Josef Teichmann for pointing out to us Meyer’s inequality (Theorem A.2).

References

- [1] L. Alili and A. E. Kyprianou. Some remarks on first passage of Lévy processes, the American put and pasting principles. Ann. Appl. Probab., 15(3):2062–2080, 2005.

- [2] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and american put options under exponential phase-type Lévy models. Stochastic Processes and their Applications, 109(1):79–111, 2004.

- [3] J. R. Baxter and R. V. Chacon. Compactness of stopping times. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 40(3):169–181, 1977.

- [4] M. Beiglböck and M. Nutz. Martingale inequalities and deterministic counterparts. Electron. J. Probab., 2014.

- [5] M. Beiglböck and P. Siorpaes. Pathwise versions of the Burkholder-Davis-Gundy inequality. Bernoulli, 21(1):360–373, 2015.

- [6] S. I. Boyarchenko and S. Z. Levendorskii. Perpetual american options under lévy processes. SIAM Journal on Control and Optimization, 40(6):1663–1696, 2002.

- [7] D. Burkholder. The best constant in the Davis inequality for the expectation of the martingale square function. Transactions of the American Mathematical Society, 354(1):91–105, 2002.

- [8] D. L. Burkholder and R. F. Gundy. Extrapolation and interpolation of quasi-linear operators on martingales. Acta Math., 124:249–304, 1970.

- [9] R. C. Dalang and M.-O. Hongler. The right time to sell a stock whose price is driven by markovian noise. Annals of Applied Probability, pages 2176–2201, 2004.

- [10] B. Davis. On the intergrability of the martingale square function. Israel Journal of Mathematics, 8(2):187–190, 1970.

- [11] I. Karatzas and S. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1988.

- [12] P.-A. Meyer. Martingales and Stochastic Integrals I. Springer-Verlag, Berlin, 1972.

- [13] G. Peskir and A. Shiryaev. Optimal stopping and free-boundary problems. Springer, 2006.

- [14] G. Peskir and A. N. Shiryaev. Sequential testing problems for Poisson processes. Annals of Statistics, pages 837–859, 2000.

- [15] L. Shepp. A first passage problem for the Wiener process. The Annals of Mathematical Statistics, pages 1912–1914, 1967.