Extending the square root method

to account for additive forecast noise in ensemble methods

Abstract

A square root approach is considered for the problem of accounting for model noise in the forecast step of the ensemble Kalman filter (EnKF) and related algorithms. The primary aim is to replace the method of simulated, pseudo-random, additive noise so as to eliminate the associated sampling errors. The core method is based on the analysis step of ensemble square root filters, and consists in the deterministic computation of a transform matrix. The theoretical advantages regarding dynamical consistency are surveyed, applying equally well to the square root method in the analysis step. A fundamental problem due to the limited size of the ensemble subspace is discussed, and novel solutions that complement the core method are suggested and studied. Benchmarks from twin experiments with simple, low-order dynamics indicate improved performance over standard approaches such as additive, simulated noise and multiplicative inflation.

Permission to place a copy of this work on this server has been provided by the AMS. The AMS does not guarantee that the copy provided here is an accurate copy of the published work.

1 Introduction

The EnKF is a popular method for doing data assimilation (DA) in the geosciences. This study is concerned with the treatment of model noise in the EnKF forecast step.

1.1 Relevance and scope

While uncertainty quantification is an important end product of any estimation procedure, it is paramount in DA due to the sequentiality and the need to correctly weight the observations at the next time step. The two main sources of uncertainty in a forecast are the initial conditions and model error (Slingo and Palmer, 2011). Accounting for model error is therefore essential in DA.

Model error, the discrepancy between nature and computational model, can be due to incomplete understanding, linearisation, truncation, sub-grid-scale processes, and numerical imprecision (Nicolis, 2004; Li et al., 2009). For the purposes of DA, however, model error is frequently described as a stochastic, additive, stationary, zero-centred, spatially correlated, Gaussian white noise process. This is highly unrealistic, yet defensible in view of the multitude of unknown error sources, the central limit theorem, and tractability (Jazwinski, 1970, §3.8). Another issue is that the size and complexity of geoscientific models makes it infeasible to estimate the model error statistics to a high degree of detail and accuracy, necessitating further reduction of its parameterisations (Dee, 1995).

The model error in this study adheres to all of the above assumptions. This, however, renders it indistinguishable from a noise process, even from our omniscient point of view. Thus, this study effectively also pertains to natural noises not generally classified as model error, such as inherent stochasticity (e.g. quantum mechanics) and stochastic, external forcings (e.g. cosmic microwave radiation). Therefore, while model error remains the primary motivation, model noise is henceforth the designation most used. It is left to future studies to recuperate more generality by scaling back on the assumptions.

Several studies in the literature are concerned with the estimation of model error, as well as its treatment in a DA scheme (Daley, 1992; Zupanski and Zupanski, 2006; Mitchell and Carrassi, 2014). The scope of this study is more restricted, addressing the treatment only. To that end, it is functional to assume that the noise statistics, namely the mean and covariance, are perfectly known. This unrealistic assumption is therefore made, allowing us to focus solely on the problem of incorporating or accounting for model noise in the EnKF.

1.2 Model noise treatment in the EnKF

From its inception, the EnKF has explicitly considered model noise and accounted for it in a Monte-Carlo way: adding simulated, pseudo-random noise to the state realisations (Evensen, 1994). A popular alternative technique is multiplicative inflation, where the spread of the ensemble is increased by some “inflation factor”. Several comparisons of these techniques exist in the literature (e.g. Hamill and Whitaker, 2005; Whitaker et al., 2008; Deng et al., 2011).

Quite frequently, however, model noise is not explicitly accounted for, but treated simultaneously with other system errors, notably sampling error and errors in the specification of the noise statistics (Whitaker et al., 2004; Hunt et al., 2004; Houtekamer et al., 2005; Anderson, 2009). This is because (a) inflation can be used to compensate for these system errors too, and (b) tuning separate inflation factors seems wasteful or even infeasible. Nevertheless, even in realistic settings, it can be rewarding to treat model error explicitly. For example, Whitaker and Hamill (2012) show evidence that, in the presence of multiple sources of error, a tuned combination of a multiplicative technique and additive noise is superior to either technique used alone.

Section 5 discusses the EnKF model noise incorporation techniques most relevant to this manuscript. However, the scope of this manuscript is not to provide a full comparison of all of the alternative under all relevant circumstances, but to focus on the square root approach. Techniques not considered any further here include using more complicated stochastic parameterisations (Arnold et al., 2013; Berry and Harlim, 2014), physics-based forcings such as stochastic kinetic energy backscatter (Shutts, 2005), relaxation (Zhang et al., 2004), and boundary condition forcings.

1.3 Framework

Suppose the state and observation, and respectively, are generated by:

| (1) | |||||

| (2) |

where the Gaussian white noise processes and , and the initial condition, , are specified by:

| (3) |

The observation operator, , has been assumed linear because that is how it will effectively be treated anyway (through the augmentation trick of e.g. Anderson, 2001). The parameter is assumed known, as are the symmetric, positive-definite (SPD) covariance matrices and . Generalisation to time-dependent , and is straightforward.

Consider , the Bayesian probability distribution of conditioned on all of the previous observations, , where the colon indicates an integer sequence. The recursive filtering process is usually broken into two steps: the forecast step, whose output is denoted by the superscript , and the analysis step, whose output is denoted using the superscript . Accordingly, the first and second moments of the distributions are denoted

| (4) | ||||||

| (5) |

where and are the (multivariate) expectation and variance operators. In the linear-Gaussian case, these characterise and , and are given, recursively in time for sequentially increasing indices, , by the Kalman filter equations.

The EnKF is an algorithm to approximately sample ensembles, , from these distributions. Note that the positive integer is used to denote ensemble size, while and have been used to denote state and observation vector lengths. For convenience, all of the state realisations are assembled into the “ensemble matrix”:

| (6) |

A related matrix is that of the “anomalies”:

| (7) |

where is the column vector of ones, is its transpose, and the matrix is the -by- identity. The conventional estimators serve as ensemble counterparts to the exact first and second order moments of eqns. 5 and 4,

| (8) | ||||||

| (9) |

where, again, the superscripts indicate the conditioning. Furthermore, (without any superscript) is henceforth used to refer to the anomalies at an intermediate stage in the forecast step, before model noise incorporation. In summary, the superscript usage of the EnKF cycle is illustrated by

Although the first of the diagram is associated with the time step before that of , , and the latter , this ambiguity becomes moot by focusing on the analysis step and the forecast step separately.

1.4 Layout

The proposed methods to account for model noise builds on the square root method of the analysis step, which is described in section 2. The core of the proposed methods is then set forth in section 3. Properties of both methods are analysed in section 4. Alternative techniques, against which the proposed method is compared, are outlined in section 5. Based on these alternatives, section 6 introduces methods to account for the residual noise resulting from the core method. It therefore connects to, and completes, section 3. The set-up and results of numerical experiments are given in section 7 and section 8. A summary is provided, along with final discussions, in section 9. The appendices provide additional details on the properties of the proposed square root methods.

2 The square root method in the analysis step

Before introducing the square root method for the EnKF forecast step, which accounts for model noise, we here briefly discuss the square root method in the analysis step.

2.1 Motivation

It is desirable that and throughout the DA process. This means that the Kalman filter equations, with the ensemble estimates swapped in,

| (10) | ||||

| (11) | ||||

| (12) |

should be satisfied by from the analysis update.

2.2 Method

On the other hand, the square root analysis update satisfies eqn. 12 exactly. Originally introduced to the EnKF by Bishop et al. (2001), the square root analysis approach was soon connected to classic square root Kalman filters (Tippett et al., 2003). But while the primary intention of classic square root Kalman filters was to improve on the numerical stability of the Kalman filter (Anderson and Moore, 1979), the main purpose of the square root EnKF was rather to eliminate the stochasticity and the accompanying sampling errors of the perturbed-observations analysis update (13).

Assume that , or that is diagonal, or that is readily computed. Then, both for notational and computational (Hunt et al., 2007) simplicity, let

| (15) | |||||

| (16) |

denote the “normalised” anomalies and mean innovation of the ensemble of observations. Recalling eqn. 9 it can then be shown that eqns. 10, 11 and 12 are satisfied if:

| (17) | ||||

| (18) |

where the two forms of ,

| (19) | ||||

| (20) |

are linked through the Woodbury identity (e.g. Wunsch, 2006). Therefore, if is computed by

| (21) |

with being a matrix square root of , then satisfies eqn. 12 exactly. Moreover, “square root update” is henceforth the term used to refer to any update of the anomalies through the right-multiplication of a transform matrix, as in eqn. 21. The ensemble is obtained by recombining the anomalies and the mean:

| (22) |

2.3 The symmetric square root

Equation 20 implies that is SPD. The matrix is a square root of if it satisfies

| (23) |

However, by substitution into eqn. 23 it is clear that is also a square root of , for any orthogonal matrix . There are therefore infinitely many square roots. Nevertheless, some have properties that make them unique. For example, the Cholesky factor is unique as the only triangular square root with positive diagonal entries.

Here, however, the square root of most interest is the symmetric one, . Here, is an eigendecomposition of , and is defined as the entry-wise positive square root of (Horn and Johnson, 2013, Th. 7.2.6). Its existence follows from the spectral theorem, and its uniqueness from that of the eigendecomposition. Note its distinction by the subscript.

It has been gradually discovered that the symmetric square root choice has several advantageous properties for its use in eqn. 21, one of which is that the it does not affect the ensemble mean (e.g. Wang and Bishop, 2003; Evensen, 2009), which is updated by eqn. 17 apart from the anomalies. Further advantages are surveyed in section 4, providing strong justification for choosing the symmetric square root, and strong motivation to extend the square root approach to the forecast step.

3 The square root method in the forecast step

Section 2 reviewed the square root update method for the analysis step of the EnKF. In view of its improvements over the Monte-Carlo method, it is expected that a similar scheme for incorporating the model noise into the forecast ensemble, , would be beneficial. Section 3.2 derives such a scheme: Sqrt-Core. First, however, section 3.1 illuminates the motivation: forecast step sampling error.

3.1 Forecast sampling errors in the classic EnKF

Assume linear dynamics, , for ease of illustration. The Monte-Carlo simulation of eqn. 1 can be written

| (24) |

where the columns of are drawn from by

| (25) |

where , and each is independently drawn from . Note that different choices of the square root, say and , yield equally-distributed random variables, and . Therefore the choice does not matter, and is left unspecified. It is typical to eliminate sampling error of the first order by centering the model noise perturbations so that . This introduces dependence between the samples and reduces the variance. The latter is compensated for by rescaling by a factor of . The result is that

| (26) | ||||

as per eqn. 8, where . But, for the same reasons as for the analysis step, ideally:

| (27) |

Thus, the second line of eqn. 26 constitutes a stochastic discrepancy from the desired relations (27).

3.2 The square root method for model noise – Sqrt-Core

As illustrated in section 1.3, define as the anomalies of the propagated ensemble before noise incorporation:

| (28) |

where is applied column-wise to . Then the desired relation (27) is satisfied if satisfies:

| (29) |

However, can only have columns. Thus, the problem of finding an that satisfies eqn. 29 is ill-posed, since the right hand side of eqn. 29 is of rank for arbitrary, full-rank , while the left hand side is of rank or less.

Therefore, let be the Moore-Penrose pseudoinverse of , denote the orthogonal projector onto the column space of , and define the “two-sided” projection of . Note that the orthogonality of the projector, , induces its symmetry. Instead of eqn. 29, the core square root model noise incorporation method proposed here, Sqrt-Core, only aims to satisfy

| (30) |

By virtue of the projection, eqn. 30 can be written as

| (31) | ||||

| (32) |

Thus, with being a square root of , the update

| (33) |

accounts for the component of the noise quantified by . The difference between the right hand sides of eqns. 29 and 30, , is henceforth referred to as the “residual noise” covariance matrix. Accounting for it is not trivial. This discussion is resumed in section 6.

As for the analysis step, we choose to use the symmetric square root, , of . Note that two SVDs are required to perform this step: one to calculate , and one to calculate the symmetric square root of . Fortunately, both are relatively computationally inexpensive, needing only to calculate singular values and vectors. For later use, define the square root “additive equivalent”:

| (34) |

3.3 Preservation of the mean

The square root update is a deterministic scheme that satisfies the covariance update relations exactly (in the space of ). But in updating the anomalies, the mean should remain the same. For Sqrt-Core, this can be shown to hold true in the same way as Livings et al. (2008) did for the analysis step, with the addition of eqn. 36.

Theorem 1 – Mean preservation.

If , then

| (35) |

I.e. the symmetric square root choice for the model noise transform matrix preserves the ensemble mean.

4 Dynamical consistency of square root updates

Many dynamical systems embody “balances” or constraints on the state space (van Leeuwen, 2009). For reasons of complexity and efficiency these concerns are often not encoded in the prior (Wang et al., 2015). They are therefore not considered by the statistical updates, resulting in state realisations that are inadmissible because of a lack of dynamical consistency or physical feasibility. Typical consequence of breaking such constraints include unbounded growth (“blow up”), exemplified by the quasi-geostrophic model of Sakov and Oke (2008a), or failure of the model to converge, exemplified by reservoir simulators (Chen and Oliver, 2013).

This section provides a formal review of the properties of the square root update as regards dynamical consistency, presenting theoretical support for the square root method. The discussion concerns any square root update, and is therefore relevant for the square root method in the analysis step as well as for Sqrt-Core.

4.1 Affine subspace confinement

The fact that the square root update is a right-multiplication means that each column of the updated anomalies is a linear combination of the original anomalies. On the other hand, itself depends on . In recognition of these two aspects, Evensen (2003) called such an update a “weakly nonlinear combination”. However, our preference is to describe the update as confined to the affine subspace of the original ensemble, that is the affine space .

4.2 Satisfying equality constraints

It seems reasonable to assume that the updated ensemble, being in the space of the original one, stands a fair chance of being dynamically consistent. However, if consistency can be described as equality constraints, then discussions thereof can be made much more formal and specific, as is the purpose of this subsection. In so doing, it uncovers a couple of interesting, hitherto unnoticed advantage of the symmetric square root choice.

Suppose the original ensemble, , or , satisfies for all , i.e.

| (38) |

One example is conservation of mass, in which case the state, , would contain grid-block densities, while the constraint coefficients, , would be a row vector of the corresponding volumes, and would be the total mass. Another example is geostrophic balance (e.g. Hoang et al., 2005), in which case would hold horizontal velocity components and sea surface heights, while would concatenate the identity and a discretised horizontal differentiation operator, and would be zero.

The constraints (38) should hold also after the update. Visibly, if is zero, any right-multiplication of , i.e. any combination of its columns, will also satisfy the constraints. This provides formal justification for the proposition of Evensen (2003), that the “linearity” of the EnKF update implicitly ensures respecting linear constraints.

One can also write

| (39) | ||||

| (40) |

implying (38) provided holds. Equations 39 and 40 show that the ensemble mean and anomalies can be thought of as particular and homogeneous solutions to the constraints. They also indicate that in a square root update, even if is not zero, one only needs to ensure that the mean constraints are satisfied, because the homogeneity of eqn. 40 means that any right-multiplying update to will satisfy the anomaly constraints. However, as mentioned above, unless it preserves the mean, it might perturb eqn. 39. A corollary of Theorem 1 is therefore that the symmetric choice for the square root update also satisfies inhomogeneous constraints.

Finally, in the case of nonlinear constraints, e.g. , truncating the Taylor expansion of yields

| (41) |

where . Contrary to eqn. 40, the approximate constraints of eqn. 41, are not homogeneous, and therefore not satisfied by any right-multiplying update. Again, however, by Theorem 1, the symmetric square root appears an advantageous choice, because it has as an eigenvector with eigenvalue 1, and therefore satisfies the (approximate) constraints.

4.3 Optimality of the symmetric choice

A number of related properties on the optimality of the symmetric square root exist scattered in the literature. However, to the best of our knowledge, these have yet to be reunited into a unified discussion. Similarly, considerations on their implications on DA have so far not been collected. These are the aims of this subsection.

Theorem 2 – Minimal ensemble displacement.

Consider the ensemble anomalies with ensemble covariance matrix , and let be column of : the displacement of the -th anomaly through a square root update. The symmetric square root, , minimises

| (42) | ||||

| (43) |

among all such that , for some SPD matrix . Equation 43 coincides with eqn. 42 if exists, but is also valid if not.

Theorem 2 was proven by Ott et al. (2004), and later restated by Hunt et al. (2007) as the constrained optimum of the Frobenius norm of . Another interesting and desirable property of the symmetric square root is the fact that the updated ensemble members are all equally likely realisations of the estimated posterior (Wang et al., 2004; McLay et al., 2008). More recently, the choice of mapping between the original and the updated ensembles has been formulated through optimal transport theory (Cotter and Reich, 2012; Oliver, 2014). However, the cost functions therein typically use a different weighting on the norm than , in one case yielding an optimum that is the symmetric left-multiplying transform matrix – not to be confused with the right-multiplying one of Theorem 2.

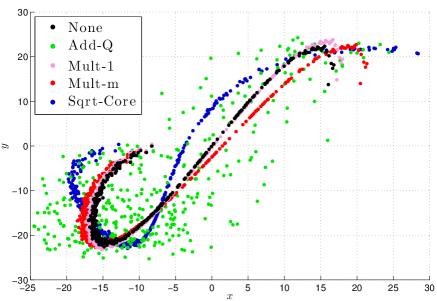

Theorem 2 and the related properties should benefit the performance of filters employing the square root update, whether for the analysis step, the model noise incorporation, or both. In part, this is conjectured because minimising the displacement of an update means that the ensemble cloud should retain some of its shape, and with it higher-order, non-Gaussian information, as illustrated in Fig. 1.

A different set of reasons to expect strong performance from the symmetric square root choice is that it should promote dynamical consistency, particularly regarding inequality constraints, such as the inherent positivity of concentration variables, as well as non-linear equality constraints, initially discussed in section 4.2. In either case it stands to reason that smaller displacements are less likely to break the constraints, and therefore that their minimisation should inhibit it. Additionally, it is important when using “local analysis” localisation that the ensemble is updated similarly at nearby grid points. Statistically, this is ensured by employing smoothly decaying localisation functions, so that does not jump too much from one grid point to the next. But, as pointed out by Hunt et al. (2007), in order to translate this smoothness to dynamical consistency, it is also crucial that the square root is continuous in . Furthermore, even if does jump from one grid point to the next, it still seems plausible that the minimisation of displacement might restrain the creation of dynamical inconsistencies.

5 Alternative approaches

| Description | Label | where | thus satisfying | ||

|---|---|---|---|---|---|

| Additive, simulated noise | Add-Q | is a centred sample from | |||

| Scalar inflation | Mult- | ||||

| Multivariate inflation | Mult- | ||||

| Core square root method | Sqrt-Core |

This section describes the model noise incorporation methods most relevant methods to this study. Table 1 summarises the methods that will be used in numerical comparison experiments. Add-Q is the classic method detailed in section 3.1. Mult- and Mult- are multiplicative inflation methods. The rightmost column relates the different methods to each other by succinctly expressing the degree to which they satisfy eqn. 29; it can also be used as a starting point for their derivation. Note that Mult- only satisfies one degree of freedom of eqn. 29, while Mult- satisfies degrees, and would therefore be expected to perform better in general. It is clear that Mult- and Mult- will generally not provide an exact statistical update, no matter how big is, while Add-Q reproduces all of the moments almost surely as . By comparison, Sqrt-Core guarantees obtaining the correct first two moments for any , but does not guarantee higher order moments.

Using a large ensemble size, Fig. 1 illustrates the different techniques. Notably, the cloud of Add-Q is clearly more dispersed than any of the other methods. Furthermore, in comparison to Mult- and Mult-, Sqrt-Core significantly skewers the distribution in order to satisfy the off-diagonal conditions.

Continuing from section 1.2, the following details other pertinent alternatives, some of them sharing some similarity with the square root methods proposed here.

One alternative is to resample the ensemble fully from . However, this incurs larger sampling errors than Add-Q, and is more likely to cause dynamical inconsistencies.

Second-order exact sampling (Pham, 2001) attempts to sample noise under the restriction that all of the terms on the second line of eqn. 27 be zero. It requires a very large ensemble size (), and is therefore typically not applicable, though recent work indicate that this might be circumvented (Hoteit et al., 2015).

The singular evolutive interpolated Kalman (SEIK) filter (Hoteit et al., 2002) has a slightly less primitive and intuitive formalism than the EnKF, typically working with matrices of size . Moreover, it does not have a separate step to deal with model noise, treating it instead implicitly, as part of the analysis step. This lack of modularity has the drawback that the frequency of model noise incorporation is not controllable: in case of multiple model integration steps between observations, the noise should be incorporated at each step in order to evolve with the dynamics; under different circumstances, skipping the treatment of noise for a few steps can be cost efficient (Evensen and van Leeuwen, 1996). Nevertheless, a stand-alone model noise step can be distilled from the SEIK algorithm as a whole. Its forecast covariance matrix, , would equal to that of Sqrt-Core: . However, unlike Sqrt-Core, which uses the symmetric square root, the SEIK uses random rotation matrices to update the ensemble. Also, the SEIK filter uses a “forgetting factor”. Among other system errors, this is intended to account for the residual noise covariance, . As outlined in section 1.2, however, this factor is not explicitly a function of ; it is instead obtained from manual tuning. Moreover, it is only applied in the update of the ensemble mean.

Another method is to include only the largest eigenvalue components of , as in reduced-rank square root filters (Verlaan and Heemink, 1997), and some versions of the unscented Kalman filter (Chandrasekar et al., 2008). This method can be referred to as T-SVD because the update can be effectuated through a truncated SVD of , where the choices of square roots do not matter. It captures more of the total variance than Sqrt-Core, but also changes the ensemble subspace. Moreover, it is not clear how to choose the updated ensemble. For example, one would suspect dynamical inconsistencies to arise from using the ordered sequence of the truncated SVD. Right-multiplying by random rotation matrices, as in the SEIK, might be a good solution. Or, if computed in terms of a left-multiplying transform matrix, the symmetric choice is likely a good one. Building on T-SVD, the “partially orthogonal” EnKF and the COFFEE algorithm of (Heemink et al., 2001; Hanea et al., 2007) also recognise the issue of the residual noise. In contrasts with the treatments proposed in this study, these methods introduce a complementary ensemble to account for it.

6 Improving Sqrt-Core: Accounting for the residual noise

As explained in section 4.1, Sqrt-Core can only incorporate noise components that are in the span (range) of . This leaves a residual noise component unaccounted for, orthogonal to the span of , with posing as its covariance matrix.

First consider why there is no such residual of for the square root methods in the analysis step: because the analysis step subtracts uncertainty, unlike the forecast step which adds it. Therefore the presence or absence of components of outside of the span of the observation ensemble makes no difference to the analysis covariance update because the ensemble effectively already assumes zero uncertainty in these directions.

In the rest of this section the question addressed is how to deal with the residual noise. It is assumed that Sqrt-Core, eqn. 33, has already been performed. The techniques proposed thus complement Sqrt-Core, but do not themselves possess the beneficial properties of Sqrt-Core discussed in section 4. Also, the notation of the previous section is reused. Thus, the aim of this section is to find an that satisfies, in some limited sense

| (44) |

6.1 Complementary, additive sampling – Sqrt-Add-Z

Let be a any square root of , and define

| (45) | ||||

| (46) |

the orthogonal projection of onto the column space of , and the complement, respectively.

A first suggestion to account for the residual noise is to use one of the techniques of section 5, with taking the place of the full in their formulae. In particular, with Add-Q in mind, the fact that

| (47) |

motivates sampling the residual noise using . That is, in addition to of Sqrt-Core, which accounts for , one also adds to the ensemble, where the columns of are drawn independently from . We call this technique Sqrt-Add-Z.

Note that , defined by eqn. 45, is a square root of . By contrast, multiplying eqn. 47 with its own transpose yields

| (48) |

and reveals that is not a square root of . Therefore, with expectation over , Sqrt-Add-Z does not respect , as one would hope.

Thus, Sqrt-Add-Z has a bias equal to the cross term sum, . Notwithstanding this problem, Corollary 1 of appendix A shows that the cross terms sum, has a spectrum symmetric around 0, and thus zero trace. To some extent, this exonerates Sqrt-Add-Z, since it means that the expected total variance is unbiased.

6.2 The underlying problem: replacing a single draw with two independent draws

Since any element of is smaller than the corresponding element in , either one of the multiplicative inflation techniques can be applied to account for without second thoughts. Using Mult- would satisfy , while Mult- would satisfy . However, the problem highlighted for Sqrt-Add-Z is not just a technicality. In fact, as shown in appendix A section A.2, has negative eigenvalues because of the cross terms. It is therefore not a valid covariance matrix in the sense that it has no real square root: samples with covariance will necessarily be complex numbers; this would generally be physically unrealisable and therefore inadmissible. This underlying problem seems to question the validity of the whole approach of splitting up and dealing with the parts and separately.

Let use emphasise the word independently, because that is, to a first approximation, what we are attempting to do: replacing a single draw from by one from plus another, independent draw from . Rather than considering anomalies, let us now focus on a single one, and drop the index. Define the two random variables,

| (49) | ||||

| (50) |

where are random variables independently drawn from . By eqn. 47, and design, can be identified with any of the columns of of eqn. 25 and, furthermore, . On the other hand, while originates in a single random draw, is the sum of two independent draws.

The dependence between the terms of , and the lack thereof for , yields the following discrepancy between the variances:

| (51) | ||||

| (52) |

Formally, this is the same problem that was identified with eqn. 48, namely that of finding a real square root of , or eliminating the cross terms. But eqns. 51 and 52 show that the problem arises from the more primal problem of trying to emulate by . Vice versa, would imply that the ostentatiously dependent terms, and , are independent, and thus is emulated by .

6.3 Reintroducing dependence – Sqrt-Dep

As already noted, though, making the cross terms zero is not possible for general and . However, the perspective of and hints at another approach: reintroducing dependence between the draws. In this section we will reintroduce dependence by making the residual sampling depend on the square root equivalent, of eqn. 34.

The trouble with the cross terms is that “gets in the way” between and , whose product would otherwise be zero. Although less ambitious than emulating with , it is possible to emulate a single draw from , e.g. , with two independent draws:

| (53) |

where, as before, and are independent random variables with law , and is some orthogonal projection matrix. Then, as the cross terms cancel,

| (54) |

and thus .

We can take advantage of this emulation possibility by choosing as the orthogonal projector onto the rows of . Instead of eqn. 49, redefine as

| (55) |

Then, since ,

| (56) |

as desired. But also

| (57) | ||||

| (58) |

The point is that, while maintaining , and despite the reintroduction of dependence between the two terms in eqn. 58, the influence of has been confined to . The above reflections yield the following algorithm, labelled Sqrt-Dep:

-

1.

Perform the core square root update for , eqn. 33;

-

2.

Find such that of eqn. 34. Components in the kernel of are inconsequential;

-

3.

Sample by drawing each column independently from ;

-

4.

Compute the residual noise, , and add it to the ensemble anomalies;

(59)

Unfortunately, this algorithm requires the additional SVD of in order to compute and . Also, despite the reintroduction of dependence, Sqrt-Dep is not fully consistent, as discussed in appendix B.

7 Experimental set-up

The model noise incorporation methods detailed in sections 3 and 6 are benchmarked using “twin experiments”, where a “truth” trajectory is generated and subsequently estimated by the ensemble DA systems. As indicated by eqns. 1 and 2, stochastic noise is added to the truth trajectory and observations, respectively. As defined in eqn. 1, implicitly includes a scaling by the model time step, , which is the duration between successive time indices. Observations are not taken at every time index, but after a duration, , called the DA window, which is a multiple of .

The noise realisations excepted, the observation process, eqn. 2, given by , , and , and the forecast process, eqn. 1, given by , , and , are both perfectly known to the DA system. The analysis update is performed using the symmetric square root update of section 2 for all of the methods under comparison. Thus, the only difference between the ensemble DA systems is their model noise incorporation method.

Performance is measured by the root-mean-square error of the ensemble mean, given by:

| (60) |

for a particular time index . By convention, the RMSE is measured only immediately following each analysis update. In any case, there was little qualitative difference to “forecast” RMSE averages, which are measured right before the analysis update. The score is averaged for all analysis times after an initial transitory period whose duration is estimated beforehand by studying the RMSE time series. Each experiment is repeated 16 times with different initial random seeds. The empirical variances of the RMSEs are checked to ensure satisfying convergence.

Covariance localisation is not used. Following each analysis update, the ensemble anomalies are rescaled by a scalar inflation factor intended to compensate for the consequences of sampling error in the analysis (e.g. Anderson and Anderson, 1999; Bocquet, 2011). This factor, listed in Table 2, was approximately optimally tuned prior to each experiment. In this tuning process the Add-Q method was used for the forecast noise incorporation, putting it at a slight advantage relative to the other methods.

In addition to the EnKF with different model incorporation methods, the twin experiments are also run with the standard methods of Table 1 for comparison, as well as three further baselines: (a) the climatology, estimated from several long, free runs of the system, (b) 3D-Var (optimal interpolation) with the background from the climatology, and (c) the extended Kalman filter (Rodgers, 2000).

7.1 The linear advection model

The linear advection model evolves according to

| (61) |

for , , with , and periodic boundary conditions. The dissipative factor is there to counteract amplitude growth due to model noise. Direct observations of the truth are taken at equidistant locations, with , every fifth time step.

The initial ensemble members, , as well as the truth, , are generated as a sum of 25 sinusoids of random amplitude and phase,

| (62) |

where and is drawn independently and uniformly from the interval for each and , and the normalisation constant, , is such that the standard deviation of each is 1. Note that the spatial mean of each realisation of eqn. 62 is zero. The model noise is given by

| (63) |

7.2 The Lorenz-96 model

The Lorenz-96 model evolves according to

| (64) |

for , and , with periodic boundary conditions. It is a nonlinear, chaotic model that mimics the atmosphere at a certain latitude circle. We use the parameter settings of Lorenz and Emanuel (1998), with a system size of , a forcing of , and the fourth-order Runge-Kutta numerical time stepping scheme with a time step of . Unless otherwise stated, direct observations of the entire state vector are taken a duration of apart, with .

The model noise is spatially homogeneous, generated using a Gaussian autocovariance function,

| (65) |

where the Kronecker delta, , has been added for numerical stability issues.

8 Experimental results

Each figure contains the results from a set of experiments run for a range of some control variable.

8.1 Linear advection

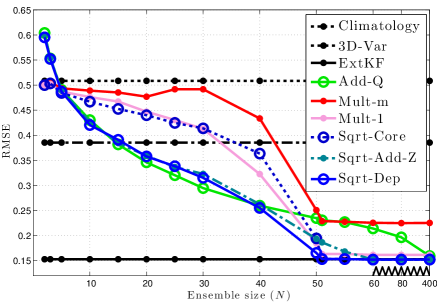

Figure 2 shows the RMSE versus the ensemble size for different model noise incorporation schemes. The maximum wavenumber of eqn. 62 is . Thus, by the design of and , the dynamics will take place in a subspace of rank 50, even though . This is clearly reflected in the curves of the square root methods, which all converge to the optimal performance of the Kalman filter (0.15) as approaches , and goes to zero. Sqrt-Add-Z takes a little longer to converge because of numerical error. The multiplicative inflation curves are also constant for , but they do not achieve the same level of performance. As one would expect, Add-Q also attains the performance of the Kalman filter as .

Interestingly, despite Mult- satisfying eqn. 29 to a higher degree than Mult-, the latter performs distinctly better across the whole range of . This can likely be blamed on the fact that Mult- has the adverse effect of changing the subspace of the ensemble, though it is unclear why its worst performance occurs near .

Add-Q clearly outperforms Mult- in the intermediate range of , indicating that the loss of nuance in the covariance matrices of Mult- is more harmful than the sampling error incurred by Add-Q. But, for , Mult- beats Add-Q. It is not clear why this reversal happens.

Sqrt-Core performs quite similar to Mult-. In the intermediate range, it is clearly deficient compared to the square root methods that account for residual noise, illustrating the importance of doing so. The performance of Sqrt-Dep is almost uniformly superior to all of the other methods. The only exception is around , where Add-Q slightly outperforms it. The computationally cheaper Sqrt-Add-Z is beaten by Add-Q for , but has a surprisingly robust performance nevertheless.

8.2 Lorenz-96

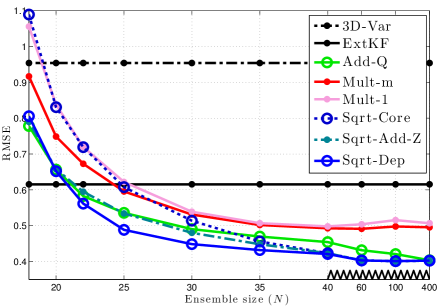

Figure 3 shows the RMSE versus ensemble size. As with the linear advection model, the curves of the square root schemes are coincident when , which here happens for . In contrast to the linear advection system, however, the square root methods still improve as increases beyond , and noticeably so until . This is because a larger enable is better able to characterise the non-Gaussianity of the distributions and the non-linearity of the models. On the other hand, the performance of the multiplicative inflation methods stagnates around , and even slightly deteriorates for larger . This can probably be attributed to the effects observed by Sakov and Oke (2008b).

Unlike the more ambiguous results of the linear advection model, here Add-Q uniformly beats the multiplicative inflation methods. Again, the importance of accounting for the residual noise is highlighted by the poor performance of Sqrt-Core for . However, even though Sqrt-Add-Z is biased, it outperforms Add-Q for , and approximately equals it for smaller .

The performance of Sqrt-Dep is nearly uniformly the best, the exception being at , where it is marginally beaten by Add-Q and Sqrt-Add-Z. The existence of this occurrence can probably be attributed to the slight suboptimality discussed in Appendix B, as well as the advantage gained by Add-Q from using it to tune the analysis inflation. Note, though, that this region is hardly interesting, since results lie above the baseline of the extended KF.

Add-Q asymptotically attains the performance of the square root methods. In fact, though it would have been imperceptible if added to Fig. 3, experiments show that Add-Q beats Sqrt-Dep by an average RMSE difference of 0.005 at , as predicted in section 5.

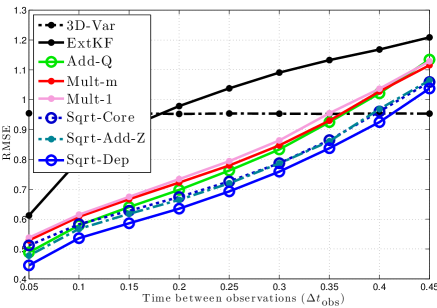

Figure 4 shows the RMSE versus the DA window. The performance of Add-Q clearly deteriorates more than that of all of the deterministic methods as increases. Indeed, the curves of Sqrt-Core and Add-Q cross at , beyond which Sqrt-Core outperforms Add-Q. Sqrt-Core even gradually attains the performance of Sqrt-Add-Z, though this happens in a regime where all of the EnKF methods are beaten by 3D-Var. Again, however, Sqrt-Dep is uniformly superior, while Sqrt-Add-Z is uniformly the second best. Similar tendencies were observed in experiments (not shown) with .

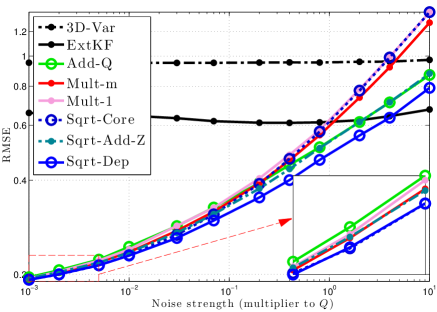

Figure 5 shows the RMSE versus the amplitude of the noise. Towards the left, the curves converge to the same value as the noise approaches zero. At the higher end of the range, the curves of Mult- and Sqrt-Core are approximately twice as steep as that of Sqrt-Dep. Again, Sqrt-Dep performs uniformly superior to the rest, with Sqrt-Add-Z performing second best. In contrasts, Add-Q performs worse than Mult- for a noise strength multiplier smaller than 0.2, but better as the noise gets stronger.

9 Summary and discussion

The main effort of this study has been to extend the square root approach of the EnKF analysis step to the forecast step in order to account for model noise. Although the primary motivation is to eliminate the need for simulated, stochastic perturbations, the core method, Sqrt-Core, was also found to possess several other desirable properties, which it shares with the analysis square root update. In particular, a formal survey on these features revealed that the symmetric square root choice for the transform matrix can be beneficial in regards to dynamical consistency.

Yet, since it does not account for the residual noise, Sqrt-Core was found to be deficient in case the noise is strong and the dynamics relatively linear. In dealing with the residual noise, cursory experiments (not shown) suggested that an additive approach works better than a multiplicative approach, similar to the forgetting factor of the SEIK. This is likely a reflection of the relative performances of Add-Q and Mult-, as well as the findings of Whitaker and Hamill (2012), which indicate that the additive approach is better suited to account for model error. Therefore, two additive techniques were proposed to complement Sqrt-Core, namely Sqrt-Add-Z and Sqrt-Dep. Adding simulated noise with no components in the ensemble subspace, Sqrt-Add-Z is computationally relatively cheap as well as intuitive. However, it was shown to yield biased covariance updates due to the presence of cross terms. By reintroducing dependence between the Sqrt-Core update and the sampled, residual noise, Sqrt-Dep remedies this deficiency at the cost of an additional SVD.

The utility of the noise integration methods proposed will depend on the properties of the system under consideration. However, Sqrt-Dep was found to perform robustly (nearly uniformly) better than all of the other methods. Moreover, the computationally less expensive method Sqrt-Add-Z was also found to have robust performance. These findings are further supported by omitted experiments using fewer observations, larger observation error, and different models.

Future directions

The model noise square root approach has shown significant promise on low-order models, but has not yet been tested on realistic systems. It is also not clear how this approach performs with more realistic forms of model error.

As discussed in Appendix B, a more shrewd choice of might improve Sqrt-Dep. This choice impacts , but not the core method, as shown in Appendix A section A.3, and should not be confused with the choice of . While the Cholesky factor yielded worse performance than the symmetric choice, other options should be contemplated.

Nakano (2013) proposed a method that is distinct, yet quite similar to Sqrt-Core, this should be explored further, in particular with regards to the residual noise.

Acknowledgments.

The authors thank Marc Bocquet for many perspectives and ideas, some of which are considered for ongoing and future research. Additionally, Chris Farmer and Irene Moroz have been very helpful in improving the numerics. The work has been funded by Statoil Petroleum AS, with co-funding by the European FP7 project SANGOMA (grant no. 283580).

Appendix A The residual noise

A.1 The cross terms

Let be the sum of the two cross terms:

| (66) | ||||

| (67) |

Note that , and therefore (and its transpose) only has the eigenvalue 0. Alternatively one can show that it is nilpotent of degree 2. By contrast, the nature of the eigenvalues of is quite different.

Theorem 3 – Properties of .

The symmetry of implies, by the spectral theorem, that its spectrum is real. Suppose that is a non-zero eigenvalue of , with eigenvector , where and . Then (a) is also an eigenvector, (b) its eigenvalue is , and (c) neither nor are zero.

Proof.

Note that

| (68) | |||||

| (69) |

As , eqns. 68 and 69 imply that

| (70) | ||||

| (71) |

Therefore,

| (72) |

Equations 70 and 71 can also be seen to imply (c).

Corollary 1.

. This follows from the fact that the trace of a matrix equals the sum of its eigenvalues.

Corollary 2.

. This follows from the fact that should be zero by the spectral theorem.

Interestingly, imaginary, skew-symmetric matrices also have the property that their eigenvalues, all of which are real, come in positive/negative pairs. These matrices can all be written for some , which is very reminiscent of . However, it is not clear if these parallels can be used to prove Theorem 3 because only has zeros on the diagonal, while generally does not (by symmetry, it can be seen that this would imply ). Also, Theorem 3 depends on the fact that the cross terms are “flanked” by orthogonal projection matrices, whereas there are no requirements on .

A.2 The residual covariance matrix

The residual, , differs from the symmetric, positive matrix by the cross terms, . The following theorem establishes a problematic consequence.

Theorem 4 – is not a covariance matrix.

Provided , the residual “covariance” matrix, , has negative eigenvalues.

Proof.

Since is symmetric, and thus orthogonally diagonalisable, the assumption that implies that has non-zero eigenvalues. Let be the eigenvector of a non-zero eigenvalue, and write , with and . Then . Define . Then:

| (73) | ||||

| (74) |

The second term can always be made negative, but larger in magnitude than the first, simply by choosing the sign of and making it sufficiently large. ∎

A.3 Eliminating the cross terms

Can the cross terms be entirely eliminated in some way? section 6.2 already answered this question in the negative: there is no particular choice of the square root of , inducing a choice of and through eqns. 45 and 46, that eliminates the cross terms, .

But suppose we allow changing the ensemble subspace. For example, suppose the partition uses the projector onto the largest-eigenvalue eigenvectors of instead of . It can then be shown that the cross terms are eliminated: , and hence and . A similar situation arises in the case of the COFFEE algorithm (section 5), explaining why it does not have the cross term problem. Another particular rank- square root that yields is the lower-triangular Cholesky factor of with the last columns set to zero.

Unfortunately, for general and , the ensemble subspace will not be that of the rank- truncated Cholesky or eigenvalue subspace. Therefore neither of these options can be carried out using a right-multiplying square root.

Appendix B Consistency of Sqrt-Dep

Sqrt-Core ensures that eqn. 30 is satisfied, i.e. that

| (75) |

where . However, this does not imply that . Therefore, in reference to Sqrt-Dep, . Instead, the magnitudes of and are minimised as much as possible, as per Theorem 2.

However, Sqrt-Dep is designed assuming that is stochastic, with its columns drawn independently from . If this were the case, then Sqrt-Dep would be consistent in the sense of

| (76) |

where the expectation is with respect to and . This follows from the consistency of as defined in eqn. 55, which has , because each column of is sampled in the same manner as .

The fact that is in fact not stochastic, as Sqrt-Dep assumes, but typically of a much smaller magnitude, suggests a few possible venues for future improvement. For example we speculate that inflating by a factor larger than one, possibly estimated in a similar fashion to Dee (1995). The value of also depends on the choice of square root for . It may therefore be a good idea to choose somewhat randomly, so as to induce more randomness in the square root “noise”, . One way of doing so is to apply a right-multiplying rotation matrix to . Cursory experiments indicate that there may be improvements using either of the above two suggestions.

Appendix C Left-multiplying formulation of Sqrt-Core

Lemma 1.

The row (and column) space of is the row space of .

Proof.

Let be the SVD of . Then:

| (77) | ||||

| (78) |

In view of Lemma 1 it seems reasonable that there should be a left-multiplying update, , such that it equals the right-multiplying update, . Although in most applications of the EnKF, the left-multiplying update would be a lot less costly to compute than the right-multiplying one in such cases if . The following derivation of an explicit formula for is very close to that of Sakov and Oke (2008b), except for the addition of eqn. 36. Lemma 2 will also be of use.

Lemma 2.

For any matrices, , , and any positive integer, ,

| (79) |

Theorem 5 – Left-multiplying transformation.

For any ensemble anomaly matrix, , and any SPD matrix ,

| (80) |

where

| (81) | ||||

| (82) |

In case , eqn. 82 reduces to

| (83) |

Note that is not a symmetric matrix. We can nevertheless define its square root as the square root obtained from its eigendecomposition, as was done for the symmetric square root in section 2.3.

Proof.

Note that the existence of a left-multiplying formulation of the right multiplying operation could be used as a proof for Theorem 1, because by the definition (28) of . Finally, Theorem 6 provides an indirect formula for .

Theorem 6 – Indirect left-multiplying formula.

If we have already calculated the right-multiplying transform matrix , then the we can obtain a corresponding left-multiplying matrix, , from:

| (84) |

Proof.

We need to show that . Note that is the orthogonal (and hence symmetric) projector onto the row space of , which Lemma 1 showed is also the row and column space of . Therefore , and . ∎

References

- Anderson and Moore (1979) Anderson, B. D. O., and J. B. Moore, 1979: Optimal Filtering. Prentice-Hall, Englewood Cliffs, NJ.

- Anderson (2001) Anderson, J. L., 2001: An ensemble adjustment Kalman filter for data assimilation. Monthly Weather Review, 129 (12), 2884–2903.

- Anderson (2009) Anderson, J. L., 2009: Spatially and temporally varying adaptive covariance inflation for ensemble filters. Tellus A, 61 (1), 72–83.

- Anderson and Anderson (1999) Anderson, J. L., and S. L. Anderson, 1999: A Monte Carlo implementation of the nonlinear filtering problem to produce ensemble assimilations and forecasts. Monthly Weather Review, 127 (12), 2741–2758.

- Arnold et al. (2013) Arnold, H. M., I. M. Moroz, and T. N. Palmer, 2013: Stochastic parametrizations and model uncertainty in the Lorenz’96 system. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 371 (1991), 20110 479.

- Ben-Israel and Greville (2003) Ben-Israel, A., and T. N. E. Greville, 2003: Generalized Inverses. Theory and Applications. 2nd ed., CMS Books in Mathematics/Ouvrages de Mathématiques de la SMC, 15, Springer-Verlag, New York, xvi+420 pp.

- Berry and Harlim (2014) Berry, T., and J. Harlim, 2014: Linear theory for filtering nonlinear multiscale systems with model error. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Science, 470 (2167), 20140 168.

- Bishop et al. (2001) Bishop, C. H., B. J. Etherton, and S. J. Majumdar, 2001: Adaptive sampling with the ensemble transform Kalman filter. Part I: Theoretical aspects. Monthly Weather Review, 129 (3), 420–436.

- Bocquet (2011) Bocquet, M., 2011: Ensemble Kalman filtering without the intrinsic need for inflation. Nonlinear Processes in Geophysics, 18 (5), 735–750.

- Burgers et al. (1998) Burgers, G., P. Jan van Leeuwen, and G. Evensen, 1998: Analysis scheme in the ensemble Kalman filter. Monthly Weather Review, 126 (6), 1719–1724.

- Chandrasekar et al. (2008) Chandrasekar, J., I. S. Kim, D. S. Bernstein, and A. J. Ridley, 2008: Reduced-rank unscented Kalman filtering using Cholesky-based decomposition. International Journal of Control, 81 (11), 1779–1792.

- Chen and Oliver (2013) Chen, Y., and D. S. Oliver, 2013: Levenberg–Marquardt forms of the iterative ensemble smoother for efficient history matching and uncertainty quantification. Computational Geosciences, 17 (4), 689–703.

- Cotter and Reich (2012) Cotter, C. J., and S. Reich, 2012: Ensemble filter techniques for intermittent data assimilation – a survey. arXiv preprint arXiv:1208.6572.

- Daley (1992) Daley, R., 1992: Estimating model-error covariances for application to atmospheric data assimilation. Monthly Weather Review, 120 (8), 1735–1746.

- Dee (1995) Dee, D. P., 1995: On-line estimation of error covariance parameters for atmospheric data assimilation. Monthly Weather Review, 123 (4), 1128–1145.

- Deng et al. (2011) Deng, Z., Y. Tang, and H. J. Freeland, 2011: Evaluation of several model error schemes in the EnKF assimilation: Applied to Argo profiles in the Pacific Ocean. Journal of Geophysical Research: Oceans (1978–2012), 116 (C9).

- Evensen (1994) Evensen, G., 1994: Sequential data assimilation with a nonlinear quasi-geostrophic model using Monte Carlo methods to forecast error statistics. Journal of Geophysical Research, 99, 10–10.

- Evensen (2003) Evensen, G., 2003: The ensemble Kalman filter: Theoretical formulation and practical implementation. Ocean Dynamics, 53 (4), 343–367.

- Evensen (2009) Evensen, G., 2009: The ensemble Kalman filter for combined state and parameter estimation. Control Systems, IEEE, 29 (3), 83–104.

- Evensen and van Leeuwen (1996) Evensen, G., and P. J. van Leeuwen, 1996: Assimilation of Geosat altimeter data for the Agulhas current using the ensemble Kalman filter with a quasigeostrophic model. Monthly Weather Review, 124 (1), 85–96.

- Golub and Van Loan (1996) Golub, G. H., and C. F. Van Loan, 1996: Matrix Computations. 1996. 3rd ed., Johns Hopkins University, Press, Baltimore, MD, USA.

- Hamill and Whitaker (2005) Hamill, T. M., and J. S. Whitaker, 2005: Accounting for the error due to unresolved scales in ensemble data assimilation: A comparison of different approaches. Monthly Weather Review, 133 (11), 3132–3147.

- Hanea et al. (2007) Hanea, R. G., G. J. M. Velders, A. J. Segers, M. Verlaan, and A. W. Heemink, 2007: A hybrid Kalman filter algorithm for large-scale atmospheric chemistry data assimilation. Monthly Weather Review, 135 (1), 140–151.

- Heemink et al. (2001) Heemink, A. W., M. Verlaan, and A. J. Segers, 2001: Variance reduced ensemble Kalman filtering. Monthly Weather Review, 129 (7), 1718–1728.

- Hoang et al. (2005) Hoang, H. S., R. Baraille, and O. Talagrand, 2005: On an adaptive filter for altimetric data assimilation and its application to a primitive equation model, MICOM. Tellus A, 57 (2), 153–170.

- Horn and Johnson (2013) Horn, R. A., and C. R. Johnson, 2013: Matrix analysis. 2nd ed., Cambridge University Press, Cambridge, xviii+643 pp.

- Hoteit et al. (2002) Hoteit, I., D.-T. Pham, and J. Blum, 2002: A simplified reduced order kalman filtering and application to altimetric data assimilation in tropical pacific. Journal of Marine systems, 36 (1), 101–127.

- Hoteit et al. (2015) Hoteit, I., D.-T. Pham, M. Gharamti, and X. Luo, 2015: Mitigating observation perturbation sampling errors in the stochastic EnKF. Monthly Weather Review, in review.

- Houtekamer et al. (2005) Houtekamer, P. L., H. L. Mitchell, G. Pellerin, M. Buehner, M. Charron, L. Spacek, and B. Hansen, 2005: Atmospheric data assimilation with an ensemble Kalman filter: Results with real observations. Monthly Weather Review, 133 (3), 604–620.

- Hunt et al. (2007) Hunt, B. R., E. J. Kostelich, and I. Szunyogh, 2007: Efficient data assimilation for spatiotemporal chaos: A local ensemble transform Kalman filter. Physica D: Nonlinear Phenomena, 230 (1), 112–126.

- Hunt et al. (2004) Hunt, B. R., and Coauthors, 2004: Four-dimensional ensemble Kalman filtering. Tellus A, 56 (4), 273–277.

- Jazwinski (1970) Jazwinski, A. H., 1970: Stochastic Processes and Filtering Theory, Vol. 63. Academic Press.

- Li et al. (2009) Li, H., E. Kalnay, T. Miyoshi, and C. M. Danforth, 2009: Accounting for model errors in ensemble data assimilation. Monthly Weather Review, 137 (10), 3407–3419.

- Livings et al. (2008) Livings, D. M., S. L. Dance, and N. K. Nichols, 2008: Unbiased ensemble square root filters. Physica D: Nonlinear Phenomena, 237 (8), 1021–1028.

- Lorenz (1963) Lorenz, E. N., 1963: Deterministic nonperiodic flow. Journal of the Atmospheric Sciences, 20 (2), 130–141.

- Lorenz and Emanuel (1998) Lorenz, E. N., and K. A. Emanuel, 1998: Optimal sites for supplementary weather observations: Simulation with a small model. Journal of the Atmospheric Sciences, 55 (3), 399–414.

- McLay et al. (2008) McLay, J. G., C. H. Bishop, and C. A. Reynolds, 2008: Evaluation of the ensemble transform analysis perturbation scheme at nrl. Monthly Weather Review, 136 (3), 1093–1108.

- Mitchell and Carrassi (2014) Mitchell, L., and A. Carrassi, 2014: Accounting for model error due to unresolved scales within ensemble Kalman filtering. Quarterly Journal of the Royal Meteorological Society, DOI: 10.1002/qj.2451.

- Nakano (2013) Nakano, S., 2013: A prediction algorithm with a limited number of particles for state estimation of high-dimensional systems. Information Fusion (FUSION), 2013 16th International Conference on, IEEE, 1356–1363.

- Nicolis (2004) Nicolis, C., 2004: Dynamics of model error: The role of unresolved scales revisited. Journal of the Atmospheric Sciences, 61 (14), 1740–1753.

- Oliver (2014) Oliver, D. S., 2014: Minimization for conditional simulation: Relationship to optimal transport. Journal of Computational Physics, 265, 1–15.

- Ott et al. (2004) Ott, E., and Coauthors, 2004: A local ensemble Kalman filter for atmospheric data assimilation. Tellus A, 56 (5), 415–428.

- Pham (2001) Pham, D. T., 2001: Stochastic methods for sequential data assimilation in strongly nonlinear systems. Monthly Weather Review, 129 (5), 1194–1207.

- Rodgers (2000) Rodgers, C. D., 2000: Inverse Methods for Atmospheric Sounding. World Scientific.

- Sakov and Oke (2008a) Sakov, P., and P. R. Oke, 2008a: A deterministic formulation of the ensemble Kalman filter: an alternative to ensemble square root filters. Tellus A, 60 (2), 361–371.

- Sakov and Oke (2008b) Sakov, P., and P. R. Oke, 2008b: Implications of the form of the ensemble transformation in the ensemble square root filters. Monthly Weather Review, 136 (3), 1042–1053.

- Shutts (2005) Shutts, G., 2005: A kinetic energy backscatter algorithm for use in ensemble prediction systems. Quarterly Journal of the Royal Meteorological Society, 131 (612), 3079–3102.

- Slingo and Palmer (2011) Slingo, J., and T. Palmer, 2011: Uncertainty in weather and climate prediction. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 369 (1956), 4751–4767.

- Tippett et al. (2003) Tippett, M. K., J. L. Anderson, C. H. Bishop, T. M. Hamill, and J. S. Whitaker, 2003: Ensemble square root filters. Monthly Weather Review, 131 (7), 1485–1490.

- van Leeuwen (2009) van Leeuwen, P. J., 2009: Particle filtering in geophysical systems. Monthly Weather Review, 137 (12), 4089–4114.

- Verlaan and Heemink (1997) Verlaan, M., and A. W. Heemink, 1997: Tidal flow forecasting using reduced rank square root filters. Stochastic Hydrology and Hydraulics, 11 (5), 349–368.

- Wang and Bishop (2003) Wang, X., and C. H. Bishop, 2003: A comparison of breeding and ensemble transform Kalman filter ensemble forecast schemes. Journal of the Atmospheric Sciences, 60 (9).

- Wang et al. (2004) Wang, X., C. H. Bishop, and S. J. Julier, 2004: Which is better, an ensemble of positive-negative pairs or a centered spherical simplex ensemble? Monthly Weather Review, 132 (7), 1590–1605.

- Wang et al. (2015) Wang, Y., F. Counillon, and L. Bertino, 2015: Alleviating the bias induced by the linear analysis update with an isopycnal ocean model. Quarterly Journal of the Royal Meteorological Society, in review.

- Whitaker et al. (2004) Whitaker, J. S., G. P. Compo, X. Wei, and T. M. Hamill, 2004: Reanalysis without radiosondes using ensemble data assimilation. Monthly Weather Review, 132 (5), 1190–1200.

- Whitaker and Hamill (2012) Whitaker, J. S., and T. M. Hamill, 2012: Evaluating methods to account for system errors in ensemble data assimilation. Monthly Weather Review, 140 (9), 3078–3089.

- Whitaker et al. (2008) Whitaker, J. S., T. M. Hamill, X. Wei, Y. Song, and Z. Toth, 2008: Ensemble data assimilation with the NCEP global forecast system. Monthly Weather Review, 136 (2), 463–482.

- Wunsch (2006) Wunsch, C., 2006: Discrete Inverse and State Estimation Problems: With Geophysical Fluid Applications. Cambridge University Press.

- Zhang et al. (2004) Zhang, F., C. Snyder, and J. Sun, 2004: Impacts of initial estimate and observation availability on convective-scale data assimilation with an ensemble Kalman filter. Monthly Weather Review, 132 (5), 1238–1253.

- Zupanski and Zupanski (2006) Zupanski, D., and M. Zupanski, 2006: Model error estimation employing an ensemble data assimilation approach. Monthly Weather Review, 134 (5), 1337–1354.

| Fig. | Post-analysis inflation | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 2 | None | |||||||||

| 3 | 1.25 | 1.22 | 1.19 | 1.15 | 1.13 | 1.12 | 1.10 | 1.03 | 1.00 | 1.00 |

| 4 | 1.13 | 1.25 | 1.30 | 1.35 | 1.43 | 1.50 | 1.57 | 1.65 | 1.70 | |

| 5 | 1.02 | 1.02 | 1.02 | 1.03 | 1.04 | 1.05 | 1.07 | 1.09 | 1.13 | … |

| 1.17 | 1.21 | 1.31 | ||||||||