Random mappings designed for commercial search engines

Abstract

We give a practical random mapping that takes any set of documents represented as vectors in Euclidean space and then maps them to a sparse subset of the Hamming cube while retaining ordering of inter-vector inner products. Once represented in the sparse space, it is natural to index documents using commercial text-based search engines which are specialized to take advantage of this sparse and discrete structure for large-scale document retrieval. We give a theoretical analysis of the mapping scheme, characterizing exact asymptotic behavior and also giving non-asymptotic bounds which we verify through numerical simulations. We balance the theoretical treatment with several practical considerations; these allow substantial speed up of the method. We further illustrate the use of this method on search over two real data sets: a corpus of images represented by their color histograms, and a corpus of daily stock market index values.

1 Introduction

Rapid document retrieval is a basic problem in modern large-scale computation. One is given a corpus of documents and a query, and the goal is to find documents in the corpus that nearly match the query. We consider the case where the query is itself a document and thus our problem is closely related to approximate nearest neighbor search. While this problem becomes challenging in the high-dimensional setting, in the special case of text documents it has been addressed, in practice, with success. Text documents may be represented as “bags of words” in which each document is represented as a vector, whose length is the size of the dictionary, and whose -th entry contains the number of times word appears.111For example, the first sentence of the introduction would be represented as a vector with 12 entries equal to one and all other entries equal to zero. Commercial search engines have been built to take advantage of this sparse and discrete structure for large scale search.

However, many documents of interest are best represented as vectors in , which are not amenable to large scale search in their original form. A small set of examples includes images, video, and audio; biometric data such as fingerprints and iris scans; and bioinformatic data such as gene expressions, enzyme activities, and protein libraries. Given the high degree to which text-based search has been implemented, including the consequential familiarity of software engineers for text-based search infrastructure, we give a way to adapt this familiar infrastructure to search in .

Naive search for objects in for is prohibitively slow when the corpus is large. Indeed, as stated in [1], “Despite decades of intensive effort, the current solutions suffer from either space, or query time, that is exponential in dimension ”. See [21] for an overview. A typical solution is to apply a dimension-reduction technique, such as that espoused by Johnson Lindenstrauss Lemma [11], which maps the data into a lower dimensional Euclidean space. While this has a beautiful theoretical backing, in practice Euclidean space is not ideally suited for search. Many other mapping strategies have been invented, in particular the locality-sensitive hashing used in approximate nearest neighbour search [9, 6]. These give theoretically appealing low-complexity and low-storage guarantees, but are typically dissimilar in operation to text-based search, so cannot leverage existing search infrastructure, nor be naturally combined with text-based search. In this paper, we give an easy to use practical mapping which puts the data precisely in the form used by commercial text search engines, namely in high-dimensional but sparse subsets of or even of . Mapping real valued vectors to discrete measurements is also the approach of locality sensitive hashing. However, in this paper we emphasize mapping to a sparse set to put the data into the same representation as a text document. We believe this falls outside of the perspective considered in prior literature.

1.1 Random mapping scheme

Although proving that our random mapping scheme works is involved, the scheme is remarkably simple. Our corpus is a finite collection of vectors in , normalized to have unit norm. To transform each vector in , multiply each vector by a random matrix, then threshold each element. We now formalize this procedure.

Introducing notation we will use throughout, let be standard normal random vectors of length . Fix . Map to the Hamming cube as follows

| (1.1) |

Above, is equal to if and otherwise. Note that is mapped to a sparse vector provided is large enough.

After indexing each document in this manner, we search by performing the same transformation to query vector . We then take inner products in the Hamming cube to determine the best match. Thus, we return to the user in decreasing order of score,

| (1.2) |

The bulk of this paper is devoted to proving and demonstrating that with appropriate choices for parameters and , this procedure returns closest, or nearly closest, to query with high probability.

The astute reader will already observe that the transformation itself is : Although the theory is straightforward to introduce with Gaussian, we elaborate in the section on practical considerations, Section 4, on an alternate choice for the random transformation that is . We show through simulations that this alternate strategy gives identical performance to that observed with a Gaussian transform.

The particular case where , correponding with measurements of the form sign(), was introduced as a method for locality-sensitive hashing in [5], and is well studied in general. Similarly, other authors [10, 13] threshold to , but replace with an inner product with respect to a kernel tailored to the corpus in order to gain greater fidelity in the hashed (transformed) space. Assuming , the vanilla sign mapping has been shown to be a near isometry from the sphere with geodesic distance to the Hamming cube, even in the case when has an infinite collection of elements [20]. Thus, it is a very effective locality-sensitive hash. Further, this near-isometric property is pivotal in 1-bit compressed sensing [3, 19]. In contrast, we focus on the case when is much greater than 0. We show that, while the mapping is not a near isometry, it still does preserve ordering of inner products, i.e., if then, with high probability, . This relationship is sufficient for effective document search and by relaxing the need for near-isometry we gain sparsity and thus improve search speed. As it happens, our choice of also provides increased sensitivity to distinguishing the nearly-similar items we in practice expect to find among the top search results.

1.2 Notation

refers to the Euclidean sphere in dimensions; the corpus is a set of documents to be indexed (we assume each document has been normalized); , always refer to a corpus document, and a user query, respectively; is the expected score of query against document given their true similarity as their inner product ; the vocabulary size is a large parameter that we control.

is the cumulative distribution function of a standard normal random variable; are standard normal vectors, each of length ; the threshold value is parameterized by a scalar so that .

For two sequences of numbers, and , we say that is asymptotically equivalent to , denoted , if and only if

where as . If for each , then if and only if

Note that this (standard) equivalence relationship is preserved under addition, multiplication, and division.

2 Problem definition

As previously noted, there exists a great body of literature addressing nearest neighbor and approximate nearest neighbor search. We broaden this perspective slightly to address the more practical problem of producing a list of results, ordered by decreasing relevance. We therefore introduce notions of relevance, retrieval, and errors in order to use standard information retrieval performance metrics (see [15] for an overview).

Recall that provided . Thus, with a goal of retrieving documents whose inner product with is at least , we will return any document whose score exceeds .

Definition 2.1 (Document sets).

Fix , , and . We call the document retrieved if and only if . We call the document relevant if and only if ; a document that is not relevant is irrelevant.

While purely relevant documents are appealing, in practice the mapping will cause some (small) error. Thus, we replace the notion of relevant with -relevant.

Definition 2.2 (Document sets with small error).

Fix , , and . We call the document -relevant if and only if ; we call the document -irrelevant if and only if .

Borrowing notions from hypothesis testing, we identify two important events:

Definition 2.3 (Error events).

We define two types of events: If an -irrelevant document is retrieved this is called a type I error. If an -relevant document is not retrieved this is called a type II error.

See Figure 1 for an illustration.

.

The practitioner will have two main goals:

-

1.

Minimize the complexity of retrieval in space (precomputation, also called indexing) and time (search) by making the mapping as sparse as possible; and

-

2.

Minimize while still controlling the probability of type I errors and type II errors.

Not surprisingly, there is a tradeoff between those two goals. Our main theoretical contribution, given in the next section, is to precisely characterize the sparsity and the size of as a function of adjustable parameters and given the desired bound on type 1 errors and type II errors.

3 Theoretical results

This section states results concerning sparsity of our mapping and asymptotic and non-asymptotic statements of its accuracy. These results anticipate the roles of parameters and in the tradeoff between accuracy and sparsity (hence, complexity) elucidated in Section 4.

3.1 Sparsity of the map

We begin by controlling the expected sparsity of mapped vectors. Recall that each vector is mapped to the sequence . Observe that is standard normal, and thus the expected number of non-zero components of a mapped vector is Recall that . For large , which implies large , one may use the classic [7] approximation

| (3.1) |

Note that the right-hand side is not only asymptotically accurate, but is also a non-asymptotic upper bound on [7].

To conclude, let be the number of non-zero entries in a mapped vector. Then satisfies

| (3.2) |

Thus, one sees that after ignoring logarithmic factors there are roughly non-zero entries. In fact, it is for this simple expression, and similar expressions below, that we parameterize as . Indeed, in Lemma 3.1 below, we see that naturally characterizes a phase transition.

We now proceed to the more significant part of the theory: characterizing the size of the error. This will come from controlling the concentration of the score around its mean. We begin in the asymptotic regime to give an exact result and a useful intuition.

3.2 Asymptotic characterization of the score

We begin with the following lemma, concerning the asymptotic normality of .

Lemma 3.1.

Fix with . Let and be, respectively, the expectation and variance of . Depending on , there are two cases to consider.

Case 1: .

Then

Case 2: .

The normalized score

| (3.3) |

convergences to a standard normal random variable in distribution as .

The phase transition at can be intuited by the following observations. When , the expected number of non-zero summands in converges to 0. When , the expected number of non-zero summands converges to infinity, and the score exhibits Gaussian behaviour. Let us derive this precisely. To ease notation, here and below let and . Let be standard normal with covariance so that are independent copies of . Consider , that is, the expected number of non-zero summands in the score. To control this quantity, we need the following bivariate normal tail approximation, which can be derived from [22],

| (3.4) |

Thus, the expected number of non-zero summands is

| (3.5) |

It is now clear that this quantity converges to infinity for and converges to 0 for . This latter observation, combined with Markov’s inequality, already completes the proof of the lemma in Case 1. Indeed, Markov’s inequality shows that

| (3.6) |

The Gaussian behaviour of Case 2 does not follow from the vanilla central limit theorem since the summands depend on (through ), but nevertheless is proven as an application of a Berry-Esseen approximation. We state this approximation, and complete the proof, in Appendix A.1 below.

3.3 Main theoretical results

We now leverage Lemma 3.1 to determine the efficacy of search via the sparsifying transformation of this paper. In the following theorem we give a precise asymptotic characterization of , which vanishes as increases. Below, is a parameter which controls the expected number of errors.

Theorem 3.2 (Main theorem, asymptotic version).

Fix also satisfying and . Let

| (3.7) |

Then,

Thus, by taking , we have

The last inequality follows from the Gaussian tail bound (3.1). Note that the last inequality combined with Markov’s inequality implies that, with probability at least , there are no type I errors or type II errors.

It may be helpful to write this in a different way. Define the (good) event := {For every , if , then ; if , then .} Then the theorem, combined with Markov’s inequality, implies that

We pause to remark on how this result falls into the framework of approximate nearest neighbour search. Note that vanishes as and thus, asymptotically, the search returns precisely the documents with the desired level of inner product with . However, for large, but finite , exact recovery is not expected. Instead, there is a small interval around , and if a document falls into this interval, we cannot predict whether it will be correctly returned (or not returned). Outside the interval, documents are returned precisely as desired with high probability. Our main result above characterizes the size of this interval. This is a version of an approximate nearest neighbours solution [2].

In order to give a more traditional treatment of the nearest neighbor problem, one may be interested in just keeping the document with highest score, rather than keeping all documents whose scores exceed a certain threshold. The theorem may be leveraged to describe the accuracy of this method. Let be the vector in which is closest to , and let . While the document with highest score is not guaranteed to be , it is guaranteed to have inner product with nearly as high as . The easiest way to see this is to make a slight change in the definition of by switching with . Thus, let be defined as in Equation (3.7) and define the event := {For every , if , then ; if , then .} One can see, by tweaking the proof, that the theory still holds with replaced by . If the event holds, then , and, for any with , one has . Thus, under this event, which holds with high probability, the document with highest score must have inner product with at least , i.e., it is an approximate nearest neighbour.

In the above theorem, we focus on asymptotics in order to give a rule of thumb; in particular, note that the main term quantifying the rate at which of decreases is . However, we find in numerical simulations that must be quite large to realize the expected asymptotic behaviour. Thus, we present the following non-asymptotic version of this theorem, with a more complex expression to quantify the interval, but one that may be verified in numerical simulations even for modestly large .

For use in this theorem, we make a slight change in the definition of errors, allowing a different value of for type I errors versus type II errors.

Definition 3.3 (Error events).

We define two types of events: If an -irrelevant document is retrieved this is called a type I error. If an -relevant document is not retrieved this is called a type II error.

Theorem 3.4 (Main theorem, non-asymptotic version).

Fix and . Define and to satisfy

| (3.8) |

provided there are solutions.

If there are solutions, then

Remark 3.5 (Understanding the accuracy of the Gaussian approximation).

The bound on the accuracy of the approximation has an intuitive meaning, which is further verified in simulations. Indeed, note that is roughly the expected number of non-zero summands in the score when (see Equation (3.5)). If this value is very small, one expects the score to be approximated by a discrete Poisson distribution, rather than the continuous Gaussian distribution given in the theorem. In this sparser regime, we find that the accuracy oscillates above and below what is expected by the Gaussian approximation as is increased. This effect is well studied in [4].

4 Practical considerations

Practitioners implementing our sparse mapping scheme need to consider tradeoffs between complexity and accuracy. In this section, we not only illustrate how the results of the previous section inform practical design decisions that must be made when incorporating sparse mapping into existing infrastructure, but we also address the cost of performing the mapping itself, proposing the use of a structured random matrix over the Gaussian random matrix used in our analysis thus far. Although the principal advantage of our approach is that it can be implemented on standard search engine infrastructure, we also illustrate here the marked improvement in complexity over an exhaustive search. Nevertheless, we emphasize that optimizing the precise complexity-accuracy tradeoff is not our main goal in this paper; instead the goal is to map to a space utilizable by commercial search engines.

4.1 Complexity-accuracy tradeoffs

Previous sections point to the tradeoff between search complexity and accuracy. Search complexity is determined by the amount of data provided to the two processes – indexing and searching – undertaken by the search engine. Accuracy is determined by the loss of fidelity in our random transform of documents and queries. Here we make explicit the relationship between parameters and and their combined effect on complexity and accuracy.

Indexing cost

In the indexing step, the search engine pre-processes the documents into a data structure suitable for efficient searching. The indexer creates a posting list for each term it encounters, and appends to each posting list the pointers to documents containing that term. In our case, each term is an element of the -dimensional output of the random projection; documents exceeding our threshold in a dimension are added to its respective posting list222Readers familiar with search technology will note that a posting list can furthermore store the number of times the term appears in each document. For simplicity, we do not exploit this capacity, instead preferring to increase , hence the number of terms we index. .

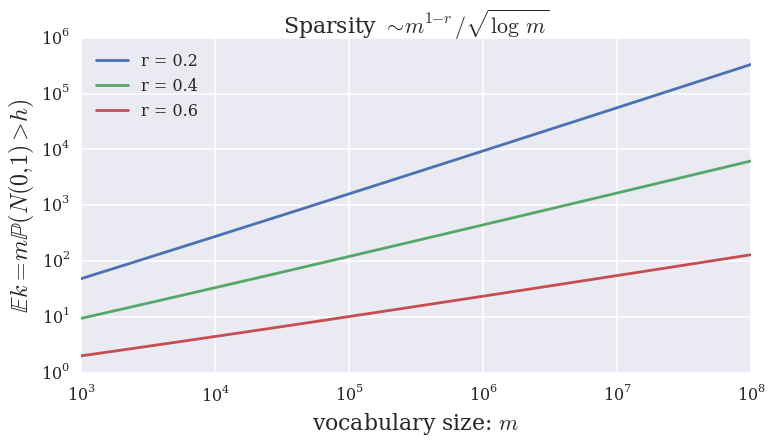

The cost of storing the search index is dominated by the number elements appearing in each of the term posting lists. Equivalently, this is the number of unique terms in each document multiplied by the number of documents. After our transformation, sparsity estimates (3.1) indicate that indexing the entire corpus, size , has an expected storage cost of

| (4.1) |

That is, determines the rate at which indexing complexity increases with . Figure 2(a) is a plot of the relationship between and for various .

Search cost

Sparsity in the transformed space also determines search time complexity. We first bound worst-case complexity. The search engine must expect to examine the posting lists indicated by the query vector (in transformed space). Each of these lists has length bounded by , and hence each search must examine

documents. However, in practice one would not expect each mapped vector in the corpus to have precisely the same support as the mapped query vector, and thus each list size would be much smaller.

We now give a rough average-case complexity. In practice, we find most data sets are clustered, i.e., there are a cluster of corpus elements close to the query, and the rest are nearly orthogonal to the query. Indeed, in image search, most images in a data base have nothing to do with the query, and unrelated (random), high-dimensional, vectors tend to be nearly orthogonal333The inner product between random high dimensional vectors concentrates very close to zero [14].. Thus, as an approximation, consider the case when of the corpus elements are near to the query, and corpus elements are orthogonal to the query. Further, note that when the query vector and the corpus vector are orthogonal, the random mappings are independent. Thus, for each of the corpus elements orthogonal to the query, the probability that this element contributes to a posting list is bounded by . It follows that each posting list has an expected length bounded by . If , the first term dominates. Then, since there are posting lists, each search must examine an expected

| (4.2) |

documents. Here is where we see an advantage over the exhaustive comparison of the query against each of documents, an procedure.

Finally, to speed up search, we suggest using a larger value of to generate queries than that used to index the corpus. This makes query vectors sparser than the calculated above. This modification leverages engineering design choices consequential to an asymmetry in text-based search, where queries tend to have many fewer terms than the text documents they retrieve. For simplicity, we do not address this scenario in our section on theory (although we believe it would be straightforward to adjust our theory to this setting). However, our search experiments of Section 5 use larger for search query transformation than for indexing with no loss of fidelity, with significant improvements in search-time performance.

Of course, the costs of indexing and search are determined not only by transformed document sparsity, but also by the cost of doing the transformation. In the case of our transformation by a dense Gaussian matrix, this is the cost of a matrix multiplication, . We can make this cost sublinear in if we use a structured random matrix to transform our corpus vectors: see Section 4.2, below.

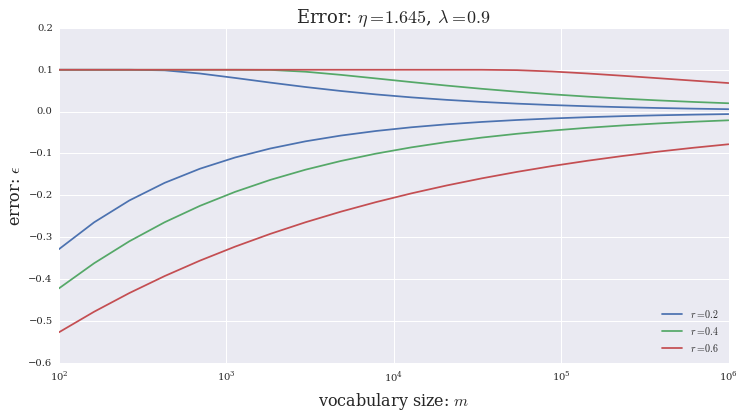

Accuracy

We focus our discussion of accuracy on the rate at which we erroneously return documents that do not match the query. The essential result is that the interval shrinks as increases at a rate that depends on . Although given implicity by (3.8), the relationship between this confidence interval and is approximately . (Up to logarithmic factors, this heuristic matches the asymptotic theoretical rate of decay of given in Theorem 3.2 for approaching 1.) Figure 3 gives an example relationship between and for . Naturally, accuracy in this sense increases with , although contrary to cost estimates, does so more rapidly with decreasing .

4.2 Fast mappings using structured matrices

Because a Gaussian random matrix is dense and unstructured, transforming each corpus document and each query is . To speed this up, we take advantage of the growing literature on structured random mappings, which suggests that structured random matrices, which allow fast transforms, behave similarly to Gaussian matrices. In particular, [12] shows that the metric-preserving property of the Johnson-Lindenstrauss Lemma can be achieved via multiplication by a random diagonal matrix followed by a (fast) discrete Fourier transform. Thus, we try a similar fast, structured mapping, and show through numerical simulations that it behaves much the same as a Gaussian matrix, provided that is large enough, and the documents are not overly sparse.

The structured mapping we propose is in two steps. First, we apply a random but fast linear mapping of our vector to an intermediary . Then, we perform a discrete cosine transform on , thresholding each element of the output by , just as we did for the Gaussian transform.

In our experiments, the specific transform we choose to expand creates copies of , then randomly changes the sign of each element. That is, we may represent this operation as multiplication by matrix

| (4.3) |

where each block is a diagonal matrix of random . We have restricted such that is a divisor of .

To intermediary , we apply a normalized type 2 discrete cosine transform (DCT-II), which we can represent as , or specifically,

| (4.4) |

This is an transform, just as is the complex discrete Fourier transform. The normalization factor we choose for in (4.4) ensures that , just as where is the Gaussian matrix we chose previously. With this choice, we can use the same threshold that we used in the Gaussian analysis.

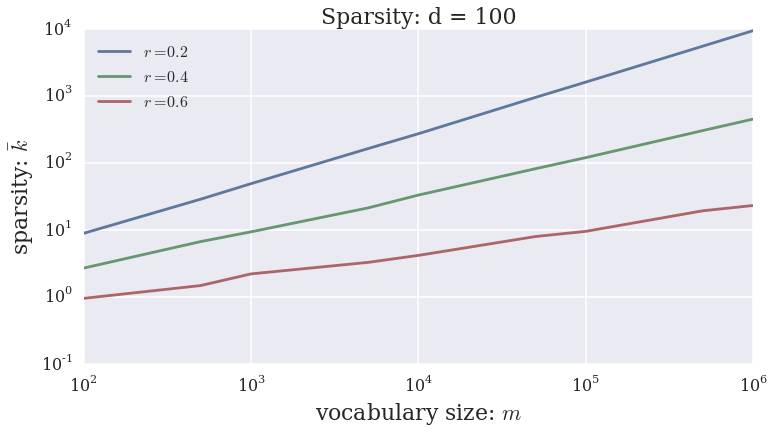

Computer experiments suggest that our proposed structured mapping approximates the behaviour of the Gaussian mapping that we prove in our main theorems. Figure 2(b) illustrates not only that sparsity grows at a rate comparable to the rate realized by the Gaussian mapping, but bears the same absolute values.

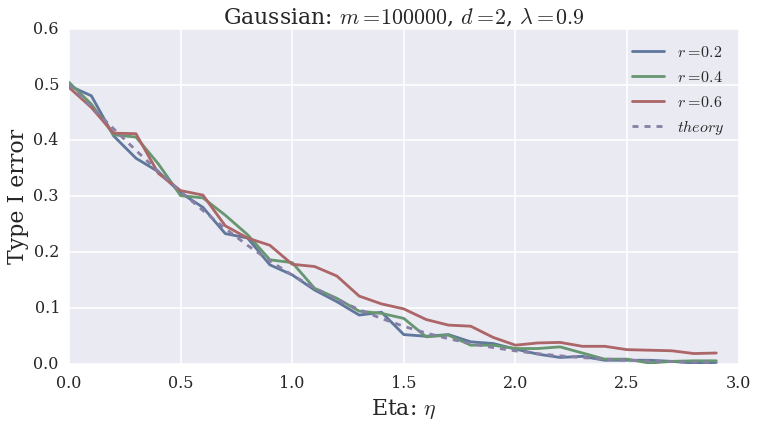

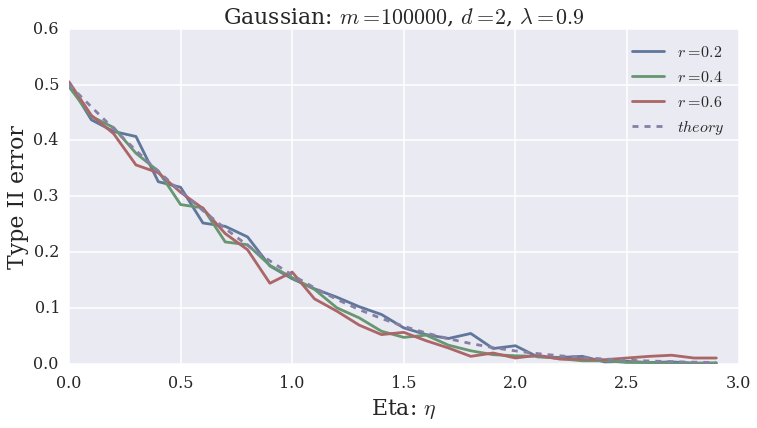

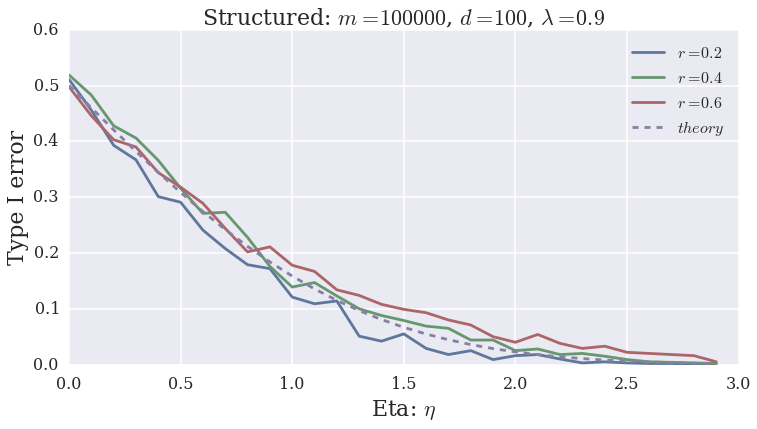

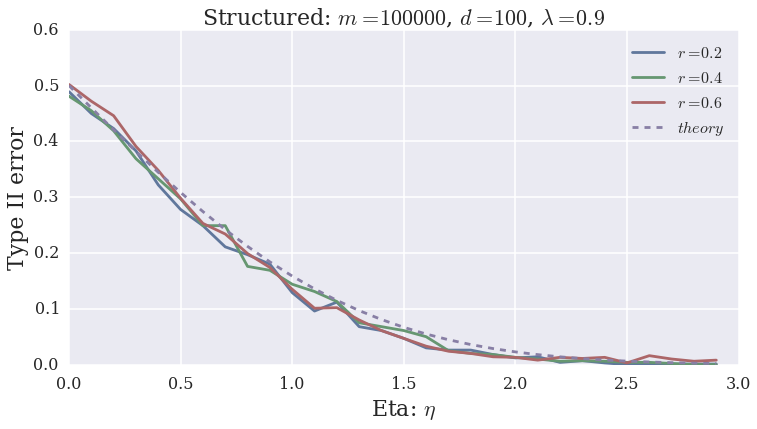

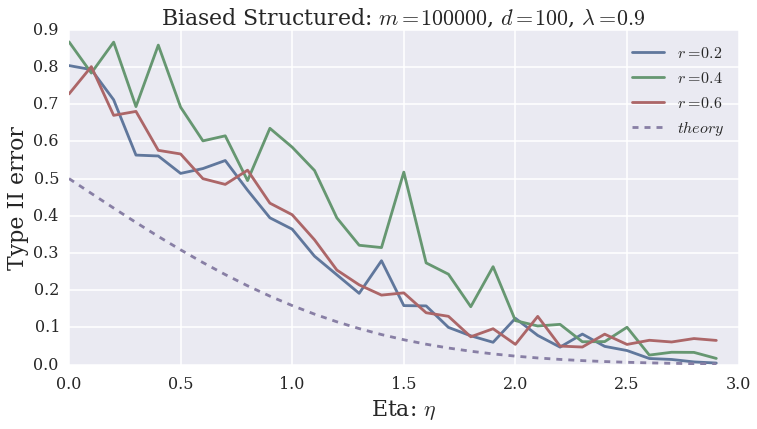

Figures 4 demonstrate similar behaviour of our Gaussian and structured mappings in the model case where we have a corpus of a single document. We query using vector , setting to examine type I error and when examining type II error. Queries are iterated over many random transforms (as opposed to many random ) to measure error rates.

Note that choosing in simulating the Gaussian mapping gives the same result as larger : all that we require for this mapping is that each mapped element . For testing the structured mapping, we select dense of modest dimension .

We do not believe that the particular we choose to construct our structured random mapping are the only possibilities. In particular, we imagine that the speed of at least the Fourier transform step can be increased by leveraging recent work in randomized Fourier transforms that realize complexity of determining the larges entries of the Fourier transform [8].

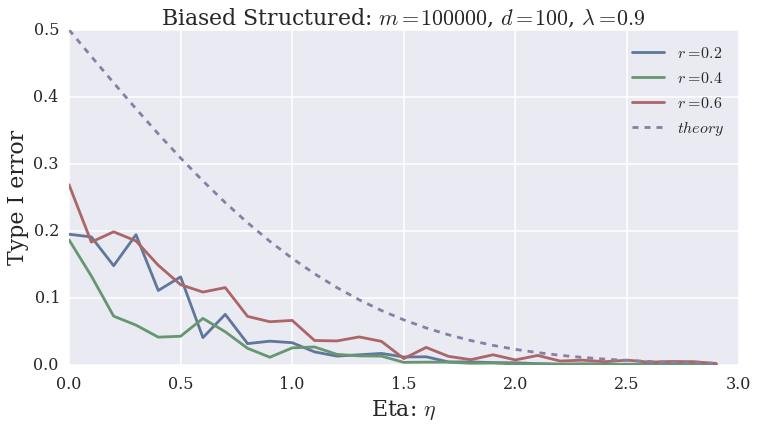

However, we caution the reader that even if normalized correctly, the expansion cannot be arbitrary: In one of our early attempts, we chose a matrix with exactly one random in each column and at most one non-zero in each row. Although the sparsity of the resulting map (not illustrated) is comparable to the sparsity of the Gaussian map, the asymmetry between simulated type I and type II errors shown in Figures 4(e) and 4(f) indicate output biased towards moving relevant documents apart from each other. We conjecture that for an unbiased transform, the vector we input to the Fourier transform must be dense with elements having mean zero. However, a study of the class of structured random mappings which approximate the behaviour proven in our main theorems remains, for the time being, future work.

5 Experiments

We now evaluate the performance of the random mapping approach using two different datasets: search based on the color of Wikipedia images, and Dow Industrial market data based on closing value percentage differences going back to the inception of this index. Searches take a seed item as a query, and attempt to find other items having similar features. We note that our two examples are from remarkably different areas of study: all that is required is that corpus documents be represented by vectors in . In both cases, we evaluate recall and precision as well as ranking of top search results. Below, relevant is the set of all relevant documents in the corpus and retrieved is the set of all retrieved documents in the corpus. Precision and recall scores are calculated as:

| (5.1) |

5.1 ImageCLEF Wikipedia image corpus

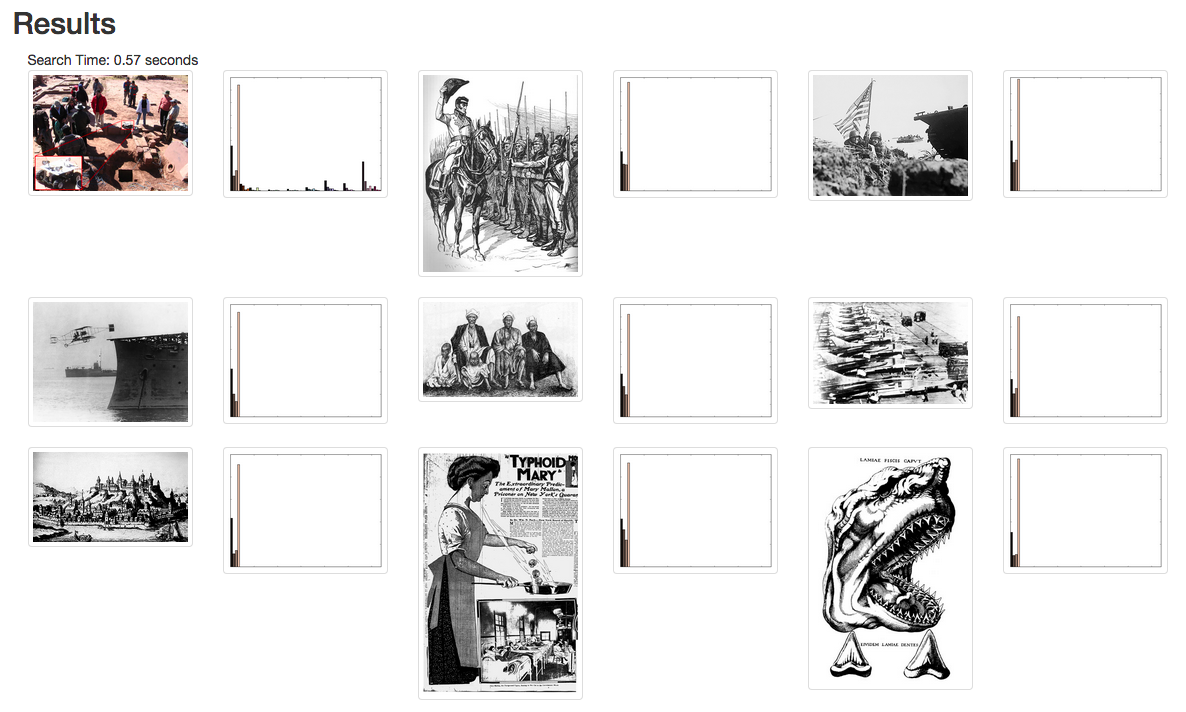

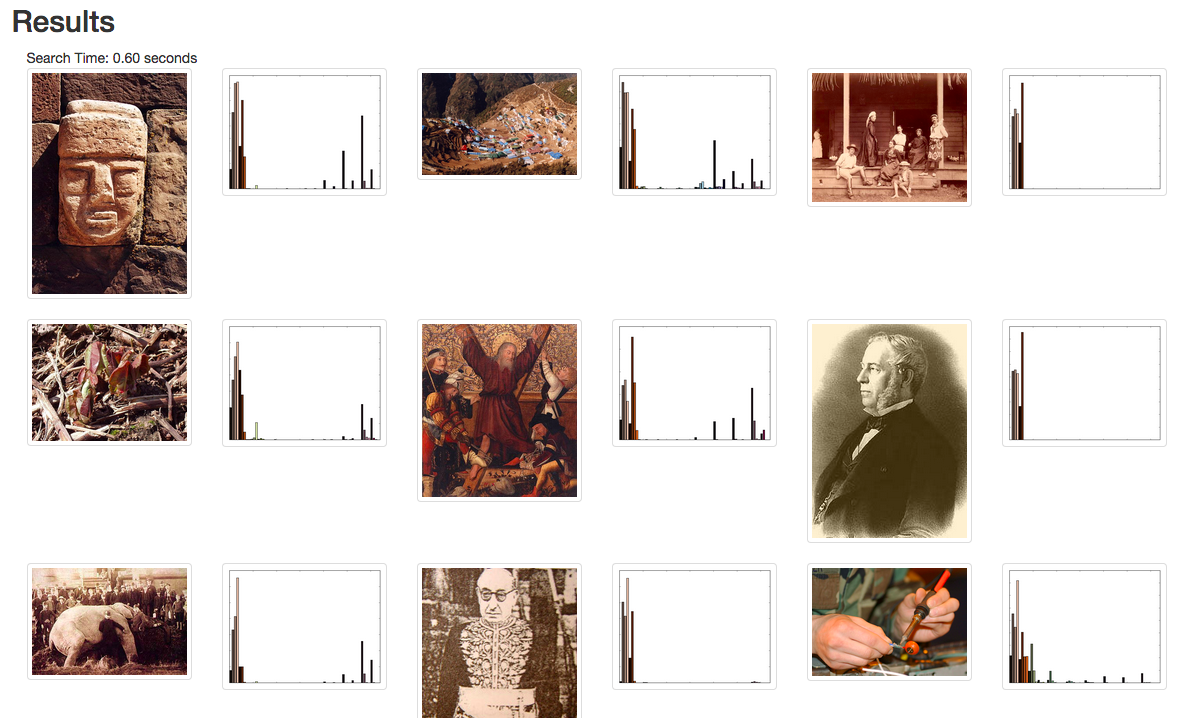

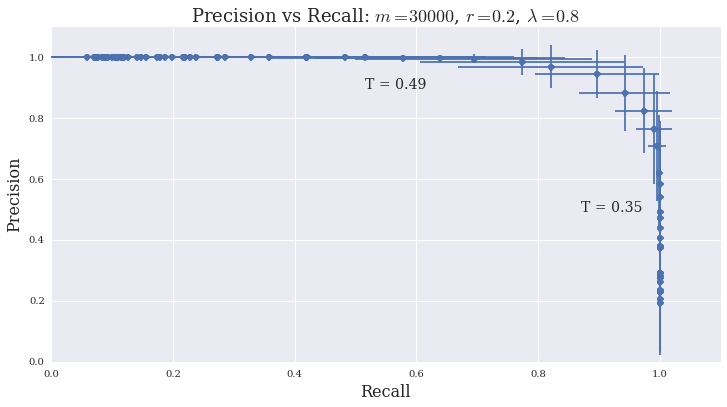

For its intuitive evaluation and ubiquity, our first test is a search of images of common color in the ImageCLEF 2010 Wikipedia Collection [16]. We process each image by transforming images to HSV colorspace, and binning the pixels of each image into histograms. Two example searches are shown in Figure 5. For these searches, we use other images as the queries, and so the first step in each search is to extract the color histogram from the query image before transforming it.

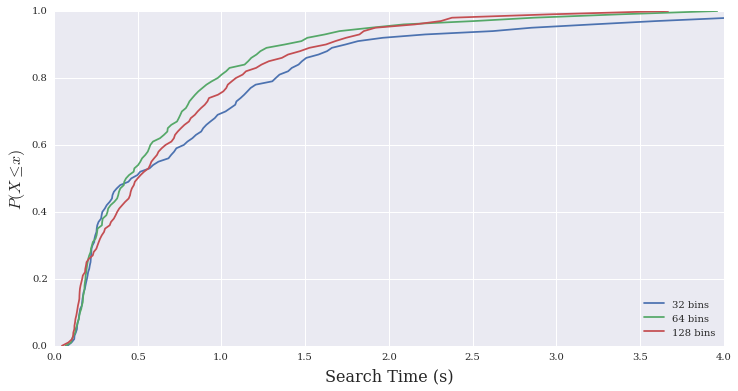

Results for histograms of 128 color bins are shown. We achieve good results with corpora represented by 32 and 64 bins. However, as shown by the search-time comparison in Figure 6, our method does not penalize large document vectors, and we choose the higher-resolution histograms. We also choose our structured random embedding over the Gaussian transformation at no loss in functionality. Note that the histograms accompany each image in Figure 5 so that errors due to our transform may be distinguished from quantization error due to color histogram binning.

Figure 7 gives a more quantitative representation of performance as the precision-recall curve. To generate each point on these curves, we fix our threshold for relevant documents, and our threshold for returned documents. Error bars representing the standard error of precision and recall are generated for each point by sampling over may query images.

Naturally, precision increases with , but most importantly, the area under the mean precision-recall curve is nearly 1, showing that our method tends to preserve the ordering of ranked results.

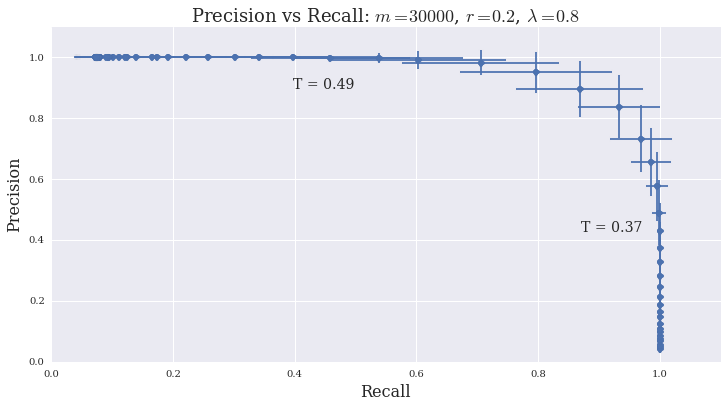

5.2 Dow Industrial corpus

Inspired by the finance literature employing nearest neighbour estimates for forecasting markets, the second test of our method draws on the Dow Jones Industrial Average [17]. Each vector of this corpus is a 10-element vector of relative differences between closing index values for each of preceeding 5 and succeeding 5 trading days. “Bullish” elements are characterized by large positive differences, while “bearish” differences are characterized by large negative differences. A search, thus, takes a single day as query and finds days with similar time-local trading patterns. Example results of two searches, queried by each of a bearish and bullish day, are shown in Table 2 and Table 2.

| Date | % Change | True score | Vector |

|---|---|---|---|

| 1907-03-14 | -8.289 | 1.0 | |

| 1957-05-28 | -0.298 | 0.916 | |

| 1945-08-08 | 0.173 | 0.934 | |

| 1943-11-18 | 0.422 | 0.917 | |

| 1972-09-26 | 0.089 | 0.935 | |

| 1898-01-05 | 1.268 | 0.917 | |

| 1971-11-02 | 0.257 | 0.863 | |

| 1901-05-09 | -6.051 | 0.881 | |

| 1975-03-25 | 0.6 | 0.843 | |

| 1985-08-19 | -0.017 | 0.868 | |

| 1929-10-29 | -11.729 | 0.865 | |

| 1896-07-21 | 0.59 | 0.844 | |

| 1979-09-19 | 0.263 | 0.858 | |

| 1968-01-31 | -0.477 | 0.905 |

| Date | % Change | True Score | Vector |

|---|---|---|---|

| 2008-10-28 | 10.878 | 1.0 | |

| 1980-12-12 | 0.958 | 0.939 | |

| 1898-07-18 | -0.191 | 0.873 | |

| 1930-02-26 | 2.382 | 0.901 | |

| 1927-03-07 | -0.383 | 0.883 | |

| 1909-11-11 | -0.01 | 0.822 | |

| 1962-09-28 | 0.847 | 0.872 | |

| 1939-02-11 | 0.647 | 0.818 | |

| 1900-09-25 | 0.321 | 0.839 | |

| 1913-05-16 | 0.408 | 0.889 | |

| 1973-05-01 | -0.024 | 0.76 | |

| 1938-04-30 | -0.34 | 0.884 | |

| 1980-04-22 | 4.047 | 0.869 | |

| 1979-02-06 | -0.137 | 0.9 |

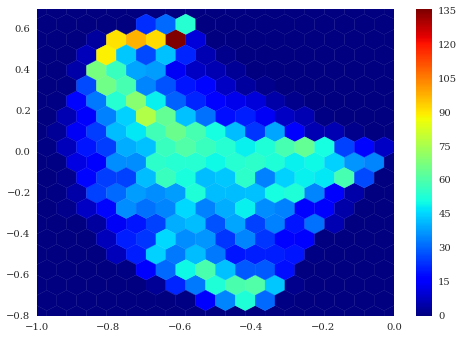

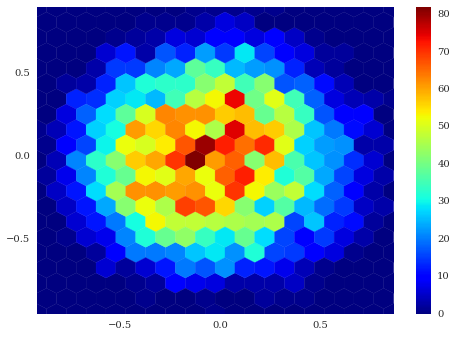

This second example has two appealing features: First, it is not an image corpus, illustrating that our method is not an image search method (though it may find application there), but is a search for any data well-represented by vectors in . Second, as shown in Figure 9, the statistics of these Dow data differ significantly from those of the image data. Despite these different statistics, the precision-recall curve for the Dow Industrial data, Figure 8, shows the ranked search performance to be comparable to that for the image data.

5.3 Online resources

See https://gitlab.com/dgpr-sparse-search/code for code for the simulations in Section 4 and the search demonstrations. The code for this project is written in Python, with simulations appearing as IPython notebooks. Whereever possible, custom code is avoided in favour of off-the-shelf open-source projects. Search examples use the Django web framework, and are powered by the Whoosh search package. As evidenced by the long search times (median for our set of 270K images), Whoosh is not the fastest off-the-shelf search engine. Rather, we select it for its ease of configuration and structural similarity to compiled off-the-shelf search engines such as Apache Lucene and ElasticSearch.

References

- [1] Alexandr Andoni and Piotr Indyk. Near-optimal hashing algorithms for approximate nearest neighbor in high dimensions. Communications of the ACM, 51(1):117–122, Jan 2008.

- [2] Marshall Bern. Approximate closest-point queries in high dimensions. Information Processing Letters, 45(2):95–99, 1993.

- [3] Petros T Boufounos and Richard G Baraniuk. 1-bit compressive sensing. In Information Sciences and Systems, 2008. CISS 2008. 42nd Annual Conference on, pages 16–21. IEEE, 2008.

- [4] Lawrence D Brown, T Tony Cai, and Anirban DasGupta. Confidence intervals for a binomial proportion and asymptotic expansions. Annals of Statistics, 30(1):160–201, 2002.

- [5] Moses S Charikar. Similarity estimation techniques from rounding algorithms. In Proceedings of the Thiry-Fourth Annual ACM Symposium on Theory of Computing, pages 380–388, 2002.

- [6] Aristides Gionis, Piotr Indyk, and Rajeev Motwani. Similarity search in high dimensions via hashing. In Proceedings of the 25th International Conference on Very Large Data Bases, pages 518–529, 1999.

- [7] Robert D Gordon. Values of Mills’ ratio of area to bounding ordinate and of the normal probability integral for large values of the argument. The Annals of Mathematical Statistics, 12(3):364–366, 1941.

- [8] Haitham Hassanieh, Piotr Indyk, Dina Katabi, and Eric Price. Simple and practical algorithm for sparse Fourier transform. In Proceedings of the Twenty-Third Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1183–1194. SIAM, 2012.

- [9] Piotr Indyk and Rajeev Motwani. Approximate nearest neighbors: towards removing the curse of dimensionality. In Proceedings of the Thirtieth Annual ACM Symposium on Theory of Computing, pages 604–613, 1998.

- [10] Ke Jiang, Qichao Que, and Brian Kulis. Revisiting kernelized locality-sensitive hashing for improved large-scale image retrieval. In IEEE Computer Vision and Pattern Recognition, pages 4933–4941, 2015.

- [11] William B Johnson and Joram Lindenstrauss. Extensions of Lipschitz mappings into a Hilbert space. Contemporary Mathematics, 26(1):189–206, 1984.

- [12] Felix Krahmer and Rachel Ward. New and improved Johnson-Lindenstrauss embeddings via the restricted isometry property. SIAM Journal on Mathematical Analysis, 43(3):1269–1281, 2011.

- [13] Brian Kulis and Kristen Grauman. Kernelized locality-sensitive hashing for scalable image search. In Proceedings of the IEEE International Conference on Computer Vision, pages 2130–2137, 2009.

- [14] Michel Ledoux and Michel Talagrand. Probability in Banach Spaces: isoperimetry and processes, volume 23. Springer Science & Business Media, 2013.

- [15] Christopher D Manning, Prabhakar Raghavan, and Hinrich Schütze. Introduction to Information Retrieval. Cambridge University Press, Cambridge, 2008.

- [16] Henning Müller, Paul Clough, Thomas Deselaers, Barbara Caputo, and Image CLEF. Experimental evaluation in visual information retrieval. The Information Retrieval Series, 32, 2010.

- [17] Central Bank of Brazil. Dow Jones Industrial Average. www.quandl.com/data/BCB/UDJIAD1-Dow-Jones-Industrial-Average. Accessed: 2015-06-25.

- [18] Robin L Plackett. A reduction formula for normal multivariate integrals. Biometrika, 41(3-4):351–360, 1954.

- [19] Yaniv Plan and Roman Vershynin. Robust 1-bit compressed sensing and sparse logistic regression: A convex programming approach. Information Theory, IEEE Transactions on, 59(1):482–494, 2013.

- [20] Yaniv Plan and Roman Vershynin. Dimension reduction by random hyperplane tessellations. Discrete & Computational Geometry, 51(2):438–461, 2014.

- [21] Hanan Samet. Foundations of Multidimensional and Metric Data Structures. The Morgan Kaufmann Series in Computer Graphics and Geometric Modeling. Morgan Kaufmann, San Francisco, 2005.

- [22] I Richard Savage. Mills’ ratio for multivariate normal distributions. Journal of Research of the National Bureau of Standards Section B, 66:93–96, 1962.

- [23] I Shevtsova. On the absolute constants in the Berry-Esseen-type inequalities. In Doklady Mathematics, volume 3, pages 378–381, 2014.

Appendix A Proofs

A.1 Proof of Lemma 3.1

We will need the following non-asymptotic version of the Central Limit Theorem [23].

Theorem A.1 (Berry-Esseen Central Limit Theorem).

Let be independent, identically distributed, mean-zero, random variables satisfying . Set

Let be the cumulative distribution function of . Then for all and ,

| (A.1) |

where .

We may leverage Theorem A.1 to characterize the rate at which converges to a standard normal random variable.

Lemma A.2.

Let everything be as in Lemma 3.1, but with no restriction on (aside from ). Note that the distribution of depends only on and , and define to be the corresponding cumulative distribution function. Then,

| (A.2) |

Proof.

We apply Theorem A.1 to . Thus, let , and note that the normalized score satisfies

It is not hard to bound as follows

Thus, the right-hand side of the Berry-Esseen bound Equation (A.1) is less than . Further, and thus, .

Then Theorem A.1 implies that for all and , the cumulative distribution function of satisfies

This result quickly translates into a proof of Lemma 3.1.

A.2 Proof of non-asymptotic main theorem: Theorem 3.4

We begin with a few lemmas, which determine the behaviour of the image search procedure non-asymptotically, and in the simple case when .

Lemma A.3.

Fix , and let . Fix .

The probability that (i.e., the event that we return ) satisfies the following bound:

| (A.3) |

We may synthesize this result to give an interval around outside of which one would expect to return (and not return) precisely the desired documents.

Lemma A.4.

Fix and . Define and as in Theorem 3.4. Consider the (good) event {if , then ; if , then .} Then

Proof.

We begin with the following observation about the behaviour of the score. Fix and with and . Suppose that . Then probabilistically dominates , i.e., for any

| (A.4) |

The above is a simple consequence of the fact that and are both binomially distributed, with respective means of and , and .

We will use this observation below, but first fix with . Then, by Lemma A.3,

| (A.5) |

We will now show that for any other vector

which will complete the proof. Thus, fix with .

There are four cases to consider:

Case 1: . Since probabilistically dominates , we have

as desired.

Case 2: . Then, clearly,

Case 3: If , then clearly since is always bounded by 1. Thus, suppose . Then, by Lemma A.3,

since is monotonically increasing.

Case 4: By the probabilistic domination of Equation (A.4), we may reduce to the situation of Case 3.

Our main non-asymptotic theorem follows directly.

Proof of Theorem 3.4.

Note that

The proof then follows by taking the expectation and then the supremum and then dividing by .

A.3 Proof of asymptotic main theorem: Theorem 3.2

Once again, this will come from manipulating the result of Lemma A.3. We have the following asymptotic characterization of the parameters of this Lemma.

Remark A.6 (A note regarding parameters in Theorem 3.4).

In passing, we note that the asymptotic equivalence , combined with the fact that is proportional to , may be manipulated to show that , where are defined in Theorem 3.4. Thus, since , we also have .

Proof.

We write to emphasize dependence on . We will show that . The argument that is quite similar. We control the numerator of via the first order Taylor approximation in

| (A.7) |

Note, while , it is not apriori obvious that the first term dominates asymptotically since also depends on . However, this will become apparent with a bit of calculus.

We begin with the observation that

which may be found in [18]. A bit of calculus then gives the second derivative

Note that this is positive for , and thus the first derivative is increasing. Further, for large, since by assumption and . We use these observations to develop the above equation into a bound on the supremum of the second derivative

The first-order Taylor approximation (A.7) then becomes

Thus, since , we have

| (A.8) |

Thus the numerator of is asymptotically equivalent to the right-hand side of the above expression, multiplied by . Let us also note that Equation (A.8) combined with Equation (3.5) imply that

| (A.9) |

We now move to the denominator of , that is, . It is not hard to show that , and thus .

Thus, by Equation (A.9), we have

| (A.10) |

Now we have shown that the right-hand side of Equation (A.8), multiplied by , is asymptotically equivalent to the numerator of and the right-hand side of Equation (A.10) is asymptotically equivalent to the denominator. If you divide the former by the latter, you get , thus showing that as desired.

The above lemma implies the following result when .

Lemma A.7.

Fix and . Let satisfy Equation (3.7). Consider the (good) event {if , then ; if , then .} Then

Proof.

We are now in position to prove our main non-asymptotic theorem.