Tight MIQP Reformulations for Semi-Continuous Quadratic Programming:

Lift-and-Convexification Approach

Baiyi Wu

Department of Systems Engineering and Engineering Management, The

Chinese University of Hong Kong, Shatin, N. T., Hong Kong,

bywu@se.cuhk.edu.hk

Xiaoling Sun

Department of Management Science,

School of Management, Fudan University, Shanghai 200433, P. R. China

Duan Li

Department of Systems Engineering and Engineering Management, The

Chinese University of Hong Kong, Shatin, N. T., Hong Kong,

dli@se.cuhk.edu.hk

Xiaojin Zheng

School of Economics and Management,

Tongji University, Shanghai 200092, P. R. China.

Abstract

We consider in this paper a class of semi-continuous quadratic programming problems which arises in many real-world applications such as production planning, portfolio selection and subset selection in regression. We propose a lift-and-convexification approach to derive an equivalent reformulation of the original problem. This lift-and-convexification approach lifts the quadratic term involving only in the original objective function to a quadratic function of both and and convexifies this equivalent objective function. While the continuous relaxation of our new reformulation attains the same tight bound as achieved by the continuous relaxation of the well known perspective reformulation, the new reformulation also retains the linearly constrained quadratic programming structure of the original mix-integer problem. This prominent feature improves the performance of branch-and-bound algorithms by providing the same tightness at the root node as the state-of-the-art perspective reformulation and offering much faster processing time at children nodes. We further combine the lift-and-convexification approach and the quadratic convex reformulation approach in the literature to form an even tighter reformulation. Promising results from our computational tests in both portfolio selection and subset selection problems numerically verify the benefits from these theoretical features of our new reformulations.

1 Introduction

We consider in this paper the following mixed-integer quadratic programming (MIQP) problem:

| (1) |

where is an positive semidefinite symmetric matrix, , , and .

Problem (P) is in general NP-hard (see bienstock96 ). Its difficulty arises from the discrete structure induced by the constraint in (1). This constraint is used to model the situation where must rest inside an interval if it is not zero, that is, . These variables are termed semi-continuous variables. We assume in our study . We also assume that the feasible region of problem (P) is nonempty. A recent review on problem (P) and its solution methods can be found in sun2013 .

Semi-continuous variables appear in many real-world optimization problems. For instance, in production planning, the semi-continuous variables are used to describe the state of a production process that is either turned off (inactive), hence nothing is produced, or turned on (active) such that the production level has to lie in certain interval (frangioni2006or , frangioni2008power , frangioni2009ieee ). Other typical applications of semi-continuous variables include portfolio selection with minimum buy-in threshold (jobst01 , frangioni06mp , cui2013 , sun2013 ) and lot-sizing with minimum order quantity (anderson1993 , park2013lot ).

An important instance of (P) involves optimization models with a cardinality constraint:

| (2) |

where and is an integer with . The cardinality constraint is often encountered when the number of nonzero variables has to be limited. The cardinality constraint in (2) can be easily incorporated into problem (P) by introducing an additional linear constraint .

A well-known application of semi-continuous variables and cardinality constraint is the cardinality constrained mean-variance portfolio selection in financial optimization. The classical mean-variance model of Markowitz is a quadratic programming problem that minimizes the variance subject to linear constraints on expected return and budget availabilities. In real-world applications of portfolio selection models, however, most investors would invest in only a limited number of assets due to market frictions such as management and transaction fees. Moreover, the minimum buy-in threshold is often a mandate trading constraint. Suppose that there are risky assets in a financial market with a random return vector . Furthermore, the expected return vector and the covariance matrix of are assumed to be given as and , respectively. The portfolio selection model with cardinality and minimum buy-in threshold constraints can be then expressed as:

where represents the proportion of the total capital invested in the th asset, and is a prescribed expected return level set by the investor. Portfolio selection problems with cardinality and/or minimum threshold constraints have been studied extensively in recent literature. For exact solution methods, please see, e.g., bienstock96 , li06 , shawa08 , bonami09 , bertsimas09 , cui2013 , gaoli2013b . For inexact solution methods, such as heuristics, local search methods and randomized techniques, please see, e.g., jacob74 , blog83 , chang00 , jobst01 , schaerf02 , maringer03 , crama03 , mitra07 , fernandez07 , zhang08 .

Another application of (P) with cardinality constraint is the subset selection problem in multivariate linear regression. Given observed data points with and , we need to minimize the least square measure of with only a subset of the prediction variables in (see, e.g., arthanari93 , miller02 , bertsimas09 ). This problem can be formally formulated as:

where , , and is an integer with . When we convert this problem to problem (P), lower bounds and upper bounds on , i.e. , can be imposed for a sufficiently large positive number and a sufficiently small negative number .

Cardinality constrained linear-quadratic optimal control was investigated in GaoLi2011 . Furthermore, a polynomially solvable case of the cardinality-constrained quadratic optimization problem was identified in gaoli2013a .

We focus in this paper on exact solution methods for problem (P). Standard MIQP solvers that are based on branch-and-bound frameworks can be applied to (P) directly. However, the lower bound generated from the continuous relaxation of (P) by relaxing to is often quite loose. Equivalent reformulations with tighter continuous relaxation, i.e., a larger lower bound, have been proposed in the literature frangioni06mp , frangioni2007letter , frangioni2009letter , zheng2013 . These reformulations are more efficient when solved in MIQP solvers. We propose a lift-and-convexification approach to construct a tight reformulation for problem (P). This lift-and-convexification approach lifts the quadratic term involving only in the original objective function to a quadratic function of both and and convexifies this equivalent objective function in a quadratic form of . The new reformulation retains the linearly constrained structure of the MIQP form so that its continuous relaxations can be solved efficiently. At the same time, the lower bound achieved by the continuous relaxation of this newly proposed reformulation is the same as the lower bound obtained from the state-of-the-art perspective reformulation. Thus it improves the performance of branch-and-bound algorithms by providing the same tightness at the root node as the state-of-the-art perspective reformulation and much faster processing time at children nodes. We then further combine our lift-and-convexification approach and the quadratic convex reformulation (QCR) billionnet2008 , billionnet2009qcr approach in the literature to form an even tighter reformulation. The QCR approach has been applied to zero-one quadratic programs billionnet2009qcr and integer quadratic programs billionnet2012qcrExtended . While the QCR approach cannot be directly applied to problem (P), it can be successfully applied on top of our new lift-and-convexification reformulation. This further reduces the duality gap as we will show in our numerical tests.

The paper is organized as follows: In §2, we review the current state-of-the-art reformulation and exact solution methods for problem (P). In §3, we propose a lift-and-convexification approach to obtain a tight reformulation. We show that this new reformulation is as tight as the state-of-the-art reformulation in terms of the lower bound from its continuous relaxation. As the continuous relaxation of the new reformulation is a quadratic program, it can be thus solved efficiently. In §4, we conduct numerical experiments to demonstrate the effectiveness of our new lift-and-convexification reformulation. In §5, we review the QCR approach in the literature for the binary and integer quadratic programs. We then combine lift-and-convexification approach and the QCR approach to form an even tighter reformulation. We conclude our paper in §6.

Notation: Throughout this paper, we denote by the optimal value of problem , and the nonnegative orthant of . For any , we denote by the diagonal matrix with being its th diagonal element. We denote by the all-one vector.

2 Literature review and related work

One efficient solution method for (P) is the perspective reformulation proposed by frangioni06mp , frangioni2007letter , in which problem (P) is transformed into the following equivalent form:

where is chosen such that

with an assumption .

The perspective reformulation is very tight, i.e., the lower bound generated from the continuous relaxation of this reformulation is usually much higher than the lower bound generated directly from the continuous relaxation of (P). To deal with the fractional terms in the objective function of , two tractable reformulations of were proposed in the literature.

The first reformulation is a second-order cone programming (SOCP) reformulation akturk2009strong , gunluk2010perspective . For each , introducing an additional variable and then rewriting the constraint as an SOCP constraint yields the following SOCP reformulation:

However, as the problem size grows, the time needed to solve the above SOCP relaxation becomes a critical factor. When interior point methods are used, the corresponding branch-and-bound algorithm may converge very slowly.

The second reformulation is the perspective cut (PC) reformulation frangioni06mp , frangioni2007letter . Representing the value of by the supremum of a set of infinitely many hyperplanes, which are called perspective cuts, gives rise to the following PC reformulation:

| (3) |

The perspective cuts in (3) can be added dynamically when is solved in a branch-and-cut framework (see frangioni2009letter ). With the help of warm start and dual methods, quadratic programming relaxations in the perspective cut algorithm can be solved efficiently.

Let , and

denote the continuous relaxations of

, and

, respectively, by relaxing to .

It is easy to see that the objective values of these continuous relaxations form the same

lower bound for .

A key issue is how to choose the vector such that this lower bound is as large as possible.

One natural way is to set every component of to be the smallest eigenvalue of .

Frangioni and Gentile frangioni2007letter proposed a better heuristic and set to be

the optimal solution to the following SDP problem:

| (4) |

Ideally, the best parameter that maximizes the lower bound can be found by solving the following problem:

| (5) |

Recently, Zheng et al. zheng2013 established the following interesting result.

Theorem 1

Problem is equivalent to the following semi-definite programming (SDP) problem:

| (8) | ||||

| (11) | ||||

Zheng et al. zheng2013 showed that the perspective cut approach for with obtained from is most efficient for solving problem (P) to its optimality.

When in the constraint , Frangioni et al. frangioni2011or developed an equivalent MIQP reformulation of , whose continuous relaxation becomes a quadratic programming problem. Frangioni et al. frangioni2013 also proposed an MIQP reformulation of the original problem (P). But the continuous relaxation of this MIQP reformulation is in general not as tight as that of the perspective reformulation.

3 Lift-and-convexification approach

In this section, we derive a tight

MIQP reformulation of (P)

by proposing

a lift-and-convexification approach.

This approach lifts the quadratic term involving only in the original objective function

to an equivalent quadratic function of both and and convexifies this equivalent objective function in a quadratic form of .

Contrast to the the perspective reformulation which involves fractional terms, our new reformulation is a quadratic programming problem whose continuous relaxations can be solved efficiently. At the same time, the lower bound achieved by the continuous relaxation of this new reformulation can be proved to achieve the same lower bound obtained from or with calculated from . To construct the new reformulation, we only need to solve an additional SOCP problem, given the solution for .

Let us determine first what kind of quadratic functions in the -space we need to add to achieve the above mentioned goals.

Theorem 2

Let be a quadratic function of and . If for all , , , where , then must take the following form:

| (12) |

where

| (13) |

is a quadratic function of parameterized by

Proof. If , , , then for any , if , then must be .

Let be of the following general form:

parameterized by . Let be a vector with a non-zero component only in its th position and be a vector with a non-zero component (which is set at one) only in its th position. It is clear that , , . If for all , , then

| (14) | ||||

| (15) |

for any . (14) implies

| (16) |

Because (16) must hold for any and , we have

| (17) | ||||

| (18) | ||||

| (19) |

Furthermore, (15) leads to

which can be simplified to the following equality by using (17)-(19),

As the above equality holds for any with and , we must have Combining the above equality with (17)-(19) yields the following form of ,

which is of the same form as (13).

We propose the following reformulation of (P):

where is defined in (13). It is easy to see that problem is equivalent to (P) and the continuous relaxation of is a quadratic program.

The difference among equivalent formulations (P), , and lies in their objective functions. The following example shows the relative relationship among these three objective functions.

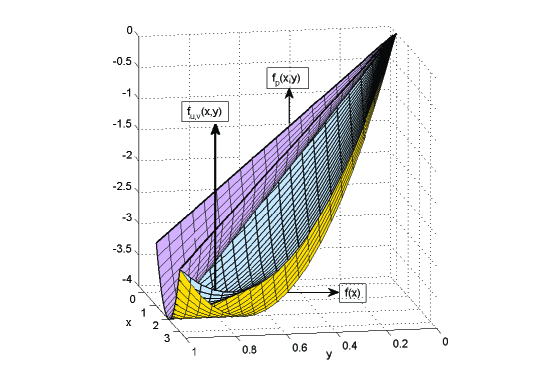

Example 1

Consider a univariate function , where . Let . Then, is zero at the region . Figure 1 illustrates the original function , the lifted quadratic function and the perspective function . While the three functions has the same value when , we can see that always lies between and in the region . This can be numerically verified since for all . We can also verify that for all .

Example 1 shows that the objective function of our new reformulation could lie below that of the perspective reformulation. This indicates that our new reformulation may not attain a lower bound that is tighter than the perspective reformulation. However, we will show that our new reformulation can achieve the same lower bound as the perspective reformulation.

Let and . Now, one critical question is “What is the best parameter vector of ?” Let denote the continuous relaxation of by relaxing to . It is desirable to choose such that the continuous relaxation of is as tight as possible. This clear goal motivates us to consider the following problem:

| (20) |

Theorem 3

Problem is equivalent to the following SDP problem:

| (24) | ||||

| (25) | ||||

where

| (26) | ||||

| (27) |

Proof. We first express by its dual form. Associate the following multipliers to the constraints in :

-

•

for ;

-

•

and for and , respectively, ; and

-

•

and for and , respectively, .

Let , , and . Let denote the vector formed by and . The Lagrangian function of is then given by

Furthermore, the Lagrangian dual problem of can be expressed as

| (28) |

Introducing an additional variable , we can rewrite (28) as

| (29) | ||||

| (30) | ||||

| (31) |

We see that the constraint in (30) is equivalent to for all , which is further equivalent to

| (32) |

Multiplying both sides of (32) by yields a homogeneous quadratic form of in the left-hand side of (32). Thus, the constraint in (30) is equivalent to the following semidefinite constraint:

| (36) |

where and are defined by (26) and (27), respectively. Consequently, the problem in (29)-(31) can be expressed as

| (37) |

If is convex, by the strong duality of convex quadratic programming (see, e.g., Proposition 6.5.6 in bertsekas2003 ), the optimal values of and (37) are equal. Thus, we have shown that problem is equivalent to an SDP problem in the form of .

Let be the optimal parameters for our new reformulation by solving the SDP program . Let be the optimal parameters for by solving the SDP program . It is necessary to compare the tightness of and , i.e., the bounds from the continuous relaxation of the “best” reformulation proposed in this paper and the “best” perspective reformulation. We will show in the following that these two bounds are the same using constructive proofs.

Theorem 4

Define as

| (38) |

Then,

- (a)

-

is feasible for problem ,

- (b)

-

.

Proof. (a)

From the proof of Theorem 3, we know that there exists

such that

is optimal to .

The constraint in (24) implies that

For any , we define with

We then have

Hence and is feasible to problem .

(b) As and have the same feasible region, for any feasible , we can compare their objective values as follows,

| (39) | |||

The above deduction is valid because if , then due to (24). Thus .

The following corollary is a direct result of Theorem 4.

Corollary 1

.

Next we show the other way around.

Theorem 5

Suppose that is optimal to problem , the continuous relaxation of . Define with

| (40) | ||||

| (41) |

Then,

- (a)

-

is feasible to problem ,

- (b)

-

.

Proof. (a) For any , we have

Hence is feasible to problem .

(b) We first show that is also an optimal solution for , we compare the gradients of and at the point . For we have

and

So . As is assumed to be optimal to problem , the directional derivative of at along any feasible direction should be non-negative. Since the feasible regions of and are the same, the directional derivative of at along any feasible direction is also non-negative. So must also be optimal for because of the convexity of . (See e.g., Chapter 2.1 of borwein2006 .)

The following corollary is a direct result of Theorem 5.

Corollary 2

.

Theorem 6

.

Thus the bound from our new reformulation is as good as the bound from the perspective reformulation. However, to find , we need to solve which is an SDP program that has a much larger size than . Our numerical tests show that could consume ten times of the computation time of . Fortunately, based on Theorems 4 and 5, the following corollary becomes evident which reveals the nonnecessity in using in the calculation.

Corollary 3

4 Computational results

In this section, we conduct computational experiments to compare the performance of the perspective cut reformulation and our new reformulation . To be specific, we compare the performance of standard MIQP solvers between solving the following two reformulations of problem :

-

•

: the perspective reformulation with , where is computed by solving .

- •

Although the continuous relaxation of (LCR) is as tight as that of (PC) at the root node of the branch-and-bound tree, the relaxations in (LCR) are in general looser than those in (PC) at children nodes. The advantage of (LCR) is that its continuous relaxations are quadratic programs and thus can be solved much faster than the continuous relaxations of (PC). We would like to test if this advantage of (LCR) would dominate (at least verifying itself as a competitive and useful reformulation).

The time difference between finding and is the time needed to solve one SOCP programming problem . We will count this amount of time into the computational time for (LCR) in the comparison, although this amount of time is quite small in general.

The two reformulations and are all solved in 64-bit IBM ILOG CPLEX Optimization Studio 12.3 (Hereinafter referred to as CPLEX) through its C interface. The perspective cut reformulation is implemented by means of user cut callbacks and lazy constraint callbacks in CPLEX. Although frangioni06mp suggested to apply the separation procedure only once at each node, we do not limit the times of separation because we find that in our numerical tests, if we allow CPLEX to actively generate mixed integer cuts, the computation would be much faster if the times of separation are unlimited at each node. is solved using sedumi interfaced by CVX 1.21 (cvx , gb08 ) on Matlab R2012b.

All the computation is conducted on a Linux machine (64-bit CentOS Release 5.5) with 48 GB of RAM. All the tests are confined on one single thread (2.99 GHz).

We consider two types of test problems from the cardinality constrained mean-variance portfolio selection (MV) and the subset selection problem (SSP) in our computational experiments.

4.1 Cardinality constrained portfolio selection problem

In this subsection, we compare (PC) and (LCR) for the cardinality constrained mean-variance portfolio selection problem (MV) introduced in the introduction section.

Frangioni and Gentile frangioni2007letter tested 90 instances of (MV) in their paper, instances each for , and . The instances for each are divided further into three subsets denoted by , and , in each subset, with different diagonal dominance in the matrix . We use these 90 instances created in frangioni2007letter in our test. While Frangioni and Gentile frangioni2007letter did not consider the cardinality constraint in their models, we add the cardinality constraint to these instances in our numerical experiments. Testing each instance without the cardinality constraint and with , , , and , we have 450 instances of (MV). The data files of these instances can be downloaded at: http://www.di.unipi.it/optimize/Data/MV.html.

| (MV) | |||||||||

| time | nodes | time | nodes | ||||||

| 6 | 27.92 | 2.30 | 19.68 | 65 | 4.10 | 26 | |||

| 8 | 27.02 | 2.13 | 11.20 | 55 | 2.29 | 19 | |||

| 10 | 26.19 | 2.06 | 6.18 | 50 | 2.86 | 42 | |||

| 12 | 26.29 | 2.05 | 10.40 | 111 | 4.28 | 95 | |||

| nonK | 32.60 | 2.17 | 13.31 | 148 | 8.66 | 147 | |||

| 6 | 26.66 | 2.54 | 18.03 | 86 | 7.07 | 65 | |||

| 8 | 27.20 | 2.05 | 16.02 | 96 | 7.59 | 73 | |||

| 10 | 23.83 | 2.21 | 9.38 | 126 | 4.16 | 120 | |||

| 12 | 24.88 | 2.10 | 30.73 | 256 | 24.44 | 217 | |||

| nonK | 30.64 | 2.00 | 33.76 | 291 | 27.42 | 281 | |||

| 6 | 26.00 | 2.39 | 26.16 | 204 | 18.49 | 248 | |||

| 8 | 25.53 | 2.16 | 22.49 | 235 | 19.96 | 287 | |||

| 10 | 24.67 | 2.03 | 19.88 | 328 | 11.00 | 350 | |||

| 12 | 25.23 | 2.11 | 287.60 | 3306 | 329.02 | 1964 | |||

| nonK | 28.47 | 1.85 | 152.45 | 1935 | 219.22 | 1380 | |||

| 6 | 62.05 | 5.91 | 82.11 | 127 | 14.25 | 26 | |||

| 8 | 65.26 | 5.54 | 48.48 | 133 | 8.43 | 25 | |||

| 10 | 55.55 | 5.47 | 16.85 | 76 | 4.20 | 30 | |||

| 12 | 60.31 | 6.89 | 18.43 | 128 | 10.27 | 119 | |||

| nonK | 87.59 | 16.23 | 108.44 | 446 | 26.60 | 241 | |||

| 6 | 60.45 | 5.43 | 43.53 | 118 | 28.42 | 105 | |||

| 8 | 54.63 | 5.14 | 51.06 | 190 | 32.20 | 123 | |||

| 10 | 57.15 | 5.04 | 22.00 | 148 | 11.96 | 129 | |||

| 12 | 61.08 | 5.14 | 75.97 | 238 | 80.78 | 249 | |||

| nonK | 63.26 | 4.80 | 101.63 | 371 | 95.79 | 323 | |||

| 6 | 63.27 | 5.10 | 55.05 | 236 | 48.85 | 237 | |||

| 8 | 62.77 | 5.72 | 99.03 | 399 | 62.47 | 328 | |||

| 10 | 60.52 | 6.40 | 47.20 | 471 | 40.47 | 609 | |||

| 12 | 62.08 | 4.92 | 35.73 | 312 | 48.94 | 341 | |||

| nonK | 68.22 | 4.56 | 137.15 | 493 | 117.96 | 506 | |||

| 6 | 126.97 | 22.32 | 70.89 | 186 | 22.73 | 39 | |||

| 8 | 122.96 | 14.19 | 196.76 | 587 | 22.25 | 38 | |||

| 10 | 122.70 | 12.02 | 28.43 | 95 | 14.23 | 47 | |||

| 12 | 139.76 | 27.78 | 38.70 | 181 | 14.37 | 105 | |||

| nonK | 100.40 | 25.47 | 562.95 | 849 | 364.24 | 613 | |||

| 6 | 104.11 | 11.74 | 105.06 | 236 | 88.21 | 197 | |||

| 8 | 124.41 | 10.54 | 149.88 | 435 | 82.51 | 170 | |||

| 10 | 119.51 | 10.47 | 54.55 | 276 | 49.06 | 287 | |||

| 12 | 128.22 | 10.73 | 71.52 | 376 | 40.67 | 287 | |||

| nonK | 125.80 | 13.20 | 542.91 | 1132 | 227.31 | 846 | |||

| 6 | 104.30 | 11.77 | 115.01 | 393 | 216.02 | 566 | |||

| 8 | 116.33 | 10.08 | 341.40 | 1053 | 239.26 | 599 | |||

| 10 | 110.30 | 10.08 | 83.77 | 515 | 95.99 | 564 | |||

| 12 | 118.64 | 10.60 | 149.93 | 495 | 29.41 | 343 | |||

| nonK | 123.05 | 10.14 | 750.27 | 1448 | 715.51 | 1373 | |||

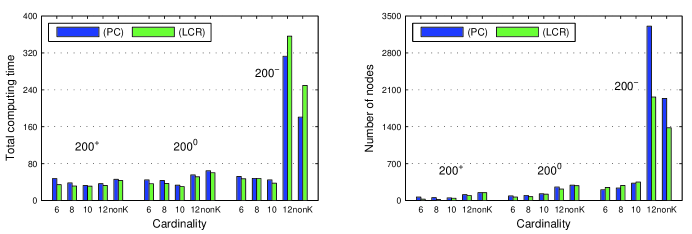

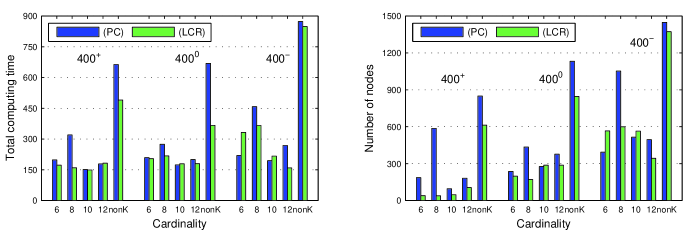

Table 1 summarizes the numerical results for the 450 instances of (MV) when the time limit is set at seconds. Each line reports the average results for the instances in a subset. The notations in the table are given as follows: The column “” is the computation time for solving and the column “” is the computation time for solving . The termination threshold of the relative gap (in percentage) between the objective value of the incumbent solution and the best lower bound is set to be . (The exact value of the relative gap when CPLEX terminates could range between and . Rounding this number would make it or ). Because all our instances terminated with a relative gap smaller than , the relative gap is not reported here. The columns “time” and “nodes” are the computing time (in seconds) and the number of nodes explored by CPLEX respectively. The “nonK” refers to the instances with no cardinality constraints.

Figure 2 displays the total computing time and nodes of the two reformulations for (MV). The total computing time for (PC) is the sum of “” and the “time” for (PC), and the total computing time for (LCR) is the sum of “”, “” and the “time” for (LCR).

From Figure 2, we can see that, in terms of the total computing time, (LCR) performs better than (PC) for 25 out of the total 45 cases. If we omit the time for solving the SDP and SOCP and only compare the time of the MIQP solver CPLEX, (LCR) performs better than (PC) for 41 out of the total 45 cases. As the perspective cut approach represents the state-of-the-art, the test result for this (MV) data set confirms that using (LCR) reformulation to solve (P) is also efficient. We need to emphasize that, we have tried our best in our numerical tests to optimize the implementation of the perspective cut approach, as the efficiency of the perspective cut approach depends heavily on its implementation details and also on selected parameters of the MIQP solvers.

For the number of nodes explored in (LCR) and (PC), they closely match each other. We might think that because the relaxations in (LCR) are in general looser than the ones in (PC) at children nodes, the number of nodes explored by (LCR) should be larger than (PC) all the time. However, this might not always be the case because the branching schemes, feasible solution heuristics and the branch-and-bound tree inside CPLEX could be quite different for (PC) and (LCR) and the number of nodes explored could demonstrate a more random pattern.

4.2 Subset selection problem

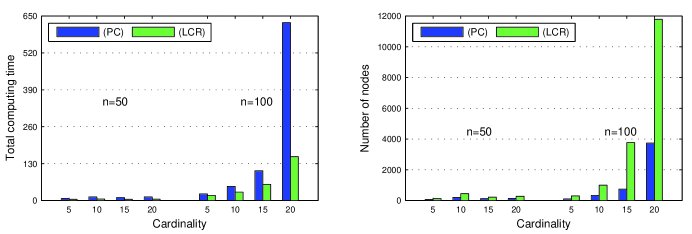

In this subsection, we compare (PC) and (LCR) for the subset selection problem (SSP) introduced in the introduction section.

We use the instances of the subset selection problem from zheng2013 with and , instances for each pair. In those instances, we set . The elements of are generated from the standard normal distribution and where the elements of are generated from the standard normal distribution and the elements of are generated uniformly form . The lower and upper bounds for the solution , are set, respectively, at and , which are sufficiently large for those instances.

| time | nodes | time | nodes | ||||||

| 5 | 3.86 | 0.14 | 2.90 | 61 | 0.35 | 115 | |||

| 10 | 3.58 | 0.21 | 9.17 | 205 | 1.29 | 445 | |||

| 15 | 3.24 | 0.20 | 6.82 | 119 | 0.71 | 218 | |||

| 20 | 3.44 | 0.25 | 9.20 | 136 | 0.77 | 276 | |||

| 5 | 14.39 | 0.48 | 8.69 | 99 | 3.35 | 295 | |||

| 10 | 14.90 | 0.37 | 34.65 | 334 | 14.11 | 993 | |||

| 15 | 14.95 | 0.49 | 89.46 | 739 | 41.38 | 3767 | |||

| 20 | 13.36 | 0.38 | 613.27 | 3737 | 140.76 | 11789 | |||

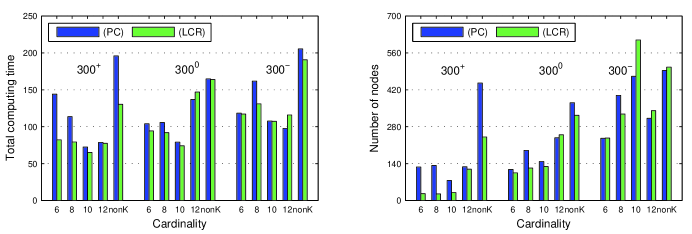

Table 2 summarizes the numerical results for the 40 instances of (SSP). Each line reports the average results for instances for each pair. The notations in the table are the same as those in Table 1.

Figure 3 displays the total computing time and nodes of the two reformulations for (SSP). The total computing time for (PC) is the sum of “” and the “time” for (PC), and the total computing time for (LCR) is the sum of “”, “” and the “time” for (LCR).

From Figure 3, we can see that although (LCR) explores more nodes than (PC), the total computing time for (LCR) is smaller than that of (PC) in all cases and this advantage of (LCR) over (PC) becomes more apparent as the problem size grows and/or as the cardinality increases. Here for the (SSP) data set, trading off tighter children-node bounds with faster processing time indeed has a good payoff. We also remark again that the efficiency of the perspective cut approach depends heavily on its implementation details and also on the selected parameters of the MIQP solvers. We, however, believe that our new reformulation derived from the lift-and-convexification approach provides a good supplement to the current state-of-the-art approaches.

5 Combination of lift-and-convexification and QCR

In this section, we further combine our lift-and-convexification approach and the QCR approach to derive an even tighter reformulation for (P).

Hammer and Rubin hammer1970 pioneered the QCR approach in the following binary quadratic programs:

where is indefinite. In the proposed QCR, they added to the objective function a term , where is a scaler and is chosen to be the negative value of the smallest eigenvalue of . Billionnet and Elloumi billionnet2007 improved this method by adding the term with being the optimal dual variables of a certain semi-definite program (SDP). Plateauplateau2006reformulations and Billionnet et al.billionnet2008 , billionnet2009qcr also utilized the equality in QCR and added the term to the objective, where and are chosen to be the dual variables of an enlarged SDP program. Ahlatçıoğlu et al. ahlatcciouglu2012combining proposed to combine QCR and the convex hull relaxation to solve problem (BQP). The geometric investigation in Li et al. li2012 for binary quadratic programs provides some theoretical support for QCR from another angle. Billionnet et al.billionnet2012qcrExtended extended the QCR approach to general mixed-integer programs by using binary decomposition.

To make our discussion more general, we add equality constraints to (P) and consider the following variant of (P):

where , and .

QCR would become beneficial when being applied to the equality and inequality constraints in (P’) on a top of our lift-and-convexification reformulation. Let us consider now the following equivalent reformulation of :

where is defined in (13).

The best parameter set can be found by solving the following problem:

where is the continuous relaxation of .

Using the same technique in the proof for Theorem 3, we can convert the problem to an SDP problem.

Theorem 7

The problem is equivalent to the following SDP problem:

| (46) | ||||

where

Proof. We first express by its dual form. Associate the following multipliers to the constraints in :

-

•

for ;

-

•

for ;

-

•

for ;

-

•

and for and , respectively, ;

-

•

and for and , respectively, .

Let , , and . Let denote the vector formed by and . The Lagrangian function of is then given by

Furthermore, the Lagrangian dual problem of can be expressed as

| (47) |

Introducing an additional variable , we can rewrite (47) as

| (48) | ||||

| (49) | ||||

| (50) |

We see that the constraint in (49) is equivalent to for all ,s, which is further equivalent to

| (51) |

Multiplying both sides of (51) by yields a homogeneous quadratic form of in the left-hand side of (51). Thus, the constraint in (49) is equivalent to the semidefinite constraint (46). Consequently, the problem in (48)-(50) can be expressed as

| (52) |

If the objective function of is convex, by the strong duality of convex quadratic programming (see, e.g., Proposition 6.5.6 in bertsekas2003 ), the optimal values of and (52) are equal. Thus, we have shown that problem is equivalent to an SDP problem in the form of .

Although this SDP problem is very large and takes time to solve, it only needs to be solved once to get the new reformulation. When the original problem is very difficult to solve, solving this SDP to get a better reformulation can gain overall computational advantage.

To test the effectiveness of the new reformulation, we compare the bounds of and on the portfolio selection problem data set introduced in §4. We use the 30 instances with the least diagonal dominance. For each instance, we impose additional equality constraints by dividing the stocks into 10 sections and demanding only one stock to be invested from each section. Such an additional constraint is a very practical one, as in real life applications portfolios are often constructed by choosing investment opportunities from different industries and sections. We use the following measure for bound improvement,

Table 3 shows the bound improvement for the 30 instances, which ranges from to , resulting an average bound improvement around . This numerical experiment confirms that combining the lift-and-convexification approach and QCR generates a much tighter reformulation on average.

| n | inst. | impr. | n | inst. | impr. | n | inst. | impr. |

| 1 | 17.0% | 1 | 47.1% | 1 | 15.1% | |||

| 2 | 28.0% | 2 | 12.7% | 2 | 21.8% | |||

| 3 | 31.8% | 3 | 25.9% | 3 | 6.5% | |||

| 4 | 18.1% | 4 | 17.6% | 4 | 10.1% | |||

| 5 | 12.7% | 5 | 26.1% | 5 | 16.5% | |||

| 6 | 17.7% | 6 | 22.0% | 6 | 17.9% | |||

| 7 | 31.1% | 7 | 22.8% | 7 | 42.1% | |||

| 8 | 29.2% | 8 | 15.6% | 8 | 22.5% | |||

| 9 | 30.4% | 9 | 2.5% | 9 | 11.5% | |||

| 10 | 33.0% | 10 | 30.2% | 10 | 20.1% | |||

| average | 24.9% | 22.2% | 18.4% |

6 Concluding remarks

We have developed in this paper the lift-and-

convexification approach to construct a

parameterized set of MIQP reformulations for convex quadratic programs with semi-continuous variables.

The primary idea behind this approach is to lift the quadratic term in the objective function from

the -space to the -space and to convexify the resulting quadratic function of .

We have proposed an SDP formulation to identify the best MIQP reformulation from among this parameterized

set and have proved that the identified best reformulation has a continuous relaxation that is as tight as

the continuous relaxation of the well known perspective reformulation.

By revealing the relationship between our new reformulation and the perspective reformulation,

we further reduce the computational effort required to construct our new reformulation and show that

we only need little extra effort to solve an additional SOCP problem when compared to the perspective reformulation. Most importantly, our new reformulation

retains the linearly constrained quadratic programming structure of the original mix-integer problem, which facilitates more effective utilization of commercial mixed integer programming solvers and ensures much faster computational time

at children nodes in the branch-and-bound searching process.

Our preliminary comparison results indicate that the performance

of our new reformulation solved in general MIQP solvers

is, at least, competitive to the state-of-the-art perspective

cut approach in many cases and provides a good

supplement to the state-of-the-art approaches.

We further combine our lift-and-convexification approach

and the quadratic convex reformulation approach in the literature

to obtain an even tighter reformulation.

In a broader picture, the lift-and-convexification approach offers an efficient solution

framework of tight MIQP reformulation which improves the existing literature on the trade-off between the bound quality and computational complexity.

References

- [1] A. Ahlatçıoğlu, M. Bussieck, M. Esen, M. Guignard, J.H. Jagla, and A. Meeraus, Combining QCR and CHR for convex quadratic pure 0–1 programming problems with linear constraints, Annals of operations research, 199 (2012), pp. 33–49.

- [2] M.S. AktüRk, A. Atamtürk, and S. GüRel, A strong conic quadratic reformulation for machine-job assignment with controllable processing times, Operations Research Letters, 37 (2009), pp. 187–191.

- [3] E.J. Anderson and B.S. Cheah, Capacitated lot-sizing with minimum batch sizes and setup times, International Journal of Production Economics, 30 (1993), pp. 137–152.

- [4] T.S. Arthanari and Y. Dodge, Mathematical Programming in Statistics, John Wiley & Sons, New York, 1993.

- [5] D.P. Bertsekas, A. Nedić, and A.E. Ozdaglar, Convex Analysis and Optimization, Athena Scientific Belmont, Mass, 2003.

- [6] D. Bertsimas and R. Shioda, Algorithm for cardinality-constrained quadratic optimization, Computational Optimization and Applications, 43 (2009), pp. 1–22.

- [7] D. Bienstock, Computational study of a family of mixed-integer quadratic programming problems, Mathematical Programming, 74 (1996), pp. 121–140.

- [8] A. Billionnet and S. Elloumi, Using a mixed integer quadratic programming solver for the unconstrained quadratic 0-1 problem, Mathematical Programming, 109 (2007), pp. 55–68.

- [9] A. Billionnet, S. Elloumi, and A. Lambert, Extending the QCR method to general mixed-integer programs, Mathematical programming, 131 (2012), pp. 381–401.

- [10] A. Billionnet, S. Elloumi, and M.C. Plateau, Quadratic 0–1 programming: tightening linear or quadratic convex reformulation by use of relaxations, RAIRO-Operations Research, 42 (2008), pp. 103–121.

- [11] , Improving the performance of standard solvers for quadratic 0-1 programs by a tight convex reformulation: The QCR method, Discrete Applied Mathematics, 157 (2009), pp. 1185–1197.

- [12] B. Blog, G. Van der Hoek, A.H.G. Rinnooy Kan, and G.T. Timmer, The optimal selection of small portfolios, Management Science, 29 (1983), pp. 792–798.

- [13] P. Bonami and M.A. Lejeune, An exact solution approach for portfolio optimization problems under stochastic and integer constraints, Operations Research, 57 (2009), pp. 650–670.

- [14] J. Borwein and A. Lewis, Convex Analysis and Nonlinear Optimization: Theory and Examples, Springer, 2006.

- [15] T.J. Chang, N. Meade, J.E. Beasley, and Y.M. Sharaiha, Heuristics for cardinality constrained portfolio optimisation, Computer & Operations Research, 27 (2000), pp. 1271–1302.

- [16] Y. Crama and M. Schyns, Simulated annealing for complex portfolio selection problems, European Journal of Operational Research, 150 (2003), pp. 546–571.

- [17] X.T. Cui, X.J. Zheng, S.S. Zhu, and X.L. Sun, Convex relaxations and MIQCQP reformulations for a class of cardinality-constrained portfolio selection problems, Journal of Global Optimization, 56 (2013), pp. 1409–1423.

- [18] Inc. CVX Research, CVX: Matlab software for disciplined convex programming, version 2.0. http://cvxr.com/cvx, Aug. 2012.

- [19] A. Fernández and S. Gómez, Portfolio selection using neural networks, Computers & Operations Research, 34 (2007), pp. 1177–1191.

- [20] A. Frangioni, F. Furini, and C. Gentile, Approximated perspective relaxations: A project and lift approach, tech. report, 2013. TR-13-04. Avialable at: http://compass2.di.unipi.it/TR/Files/TR-13-04.pdf.gz.

- [21] A. Frangioni and C. Gentile, Perspective cuts for a class of convex 0–1 mixed integer programs, Mathematical Programming, 106 (2006), pp. 225–236.

- [22] , Solving nonlinear single-unit commitment problems with ramping constraints, Operations Research, 54 (2006), pp. 767–775.

- [23] , SDP diagonalizations and perspective cuts for a class of nonseparable MIQP, Operations Research Letters, 35 (2007), pp. 181–185.

- [24] , A computational comparison of reformulations of the perspective relaxation: SOCP vs. cutting planes, Operations Research Letters, 37 (2009), pp. 206–210.

- [25] A. Frangioni, C. Gentile, E. Grande, and A. Pacifici, Projected perspective reformulations with applications in design problems, Operations Research, 59 (2011), pp. 1225–1232.

- [26] A. Frangioni, C. Gentile, and F. Lacalandra, Solving unit commitment problems with general ramp constraints, International Journal of Electrical Power & Energy Systems, 30 (2008), pp. 316–326.

- [27] , Tighter approximated MILP formulations for unit commitment problems, IEEE Transactions on Power Systems, 24 (2009), pp. 105–113.

- [28] J.J. Gao and D. Li, Cardinality constrained linear-quadratic optimal control, IEEE Transations on Automatical Control, 56 (2011), pp. 1936–1941.

- [29] , Optimal cardinality constrained portfolio selection, Operations Research, 61 (2013), pp. 745–761.

- [30] , A polynomial case of the cardinality-constrained quadratic optimization problem, Journal of Global Optimization, 56 (2013), pp. 1441–1455.

- [31] M. Grant and S. Boyd, Graph implementations for nonsmooth convex programs, in Recent Advances in Learning and Control, V. Blondel, S. Boyd, and H. Kimura, eds., Lecture Notes in Control and Information Sciences, Springer-Verlag Limited, 2008, pp. 95–110. http://stanford.edu/~boyd/graph_dcp.html.

- [32] O. Günlük and J. Linderoth, Perspective reformulations of mixed integer nonlinear programs with indicator variables, Mathematical programming, 124 (2010), pp. 183–205.

- [33] P.L. Hammer and A.A. Rubin, Some remarks on quadratic programming with 0-1 variables, RAIRO-Operations Research-Recherche Opérationnelle, 4 (1970), pp. 67–79.

- [34] N.L. Jacob, A limited-diversification portfolio selection model for the small investor, Journal of Finance, 29 (1974), pp. 847–856.

- [35] N.J. Jobst, M.D. Horniman, C.A. Lucas, and G. Mitra, Computational aspects of alternative portfolio selection models in the presence of discrete asset choice constraints, Quantitative Finance, 1 (2001), pp. 489–501.

- [36] D. Li, X.L. Sun, and C.L. Liu, An exact solution method for unconstrained quadratic 0–1 programming: a geometric approach, Journal of Global Optimization, 52 (2012), pp. 797–829.

- [37] D. Li, X.L. Sun, and J. Wang, Optimal lot solution to cardinality constrained mean-variance formulation for portfolio selection, Mathematical Finance, 16 (2006), pp. 83–101.

- [38] D. Maringer and H. Kellerer, Optimization of cardinality constrained portfolios with a hybrid local search algorithm, OR Spectrum, 25 (2003), pp. 481–495.

- [39] A.J. Miller, Subset Selection in Regression, Chapman and Hall, 2002. Second edition.

- [40] G. Mitra, F. Ellison, and A. Scowcroft, Quadratic programming for portfolio planning: Insights into algorithmic and computational issues. part ii: Processing of portfolio planning models with discrete constraints, Journal of Asset Management, 8 (2007), pp. 249–258.

- [41] Y.W. Park and D. Klabjan, Lot sizing with minimum order quantity, Discrete Applied Mathematics, 181 (2015), pp. 235–254.

- [42] M.C. Plateau, Reformulations quadratiques convexes pour la programmation quadratique en variables 0-1, PhD thesis, Ph. D. thesis, Conservatoire National d Arts et Métiers, 2006.

- [43] A. Schaerf, Local search techniques for constrained portfolio selection problems, Computational Economics, 20 (2002), pp. 177–190.

- [44] D.X. Shaw, S. Liu, and L. Kopman, Lagrangian relaxation procedure for cardinality-constrained portfolio optimization, Optimization Methods and Software, 23 (2008), pp. 411–420.

- [45] X.L. Sun, X.J. Zheng, and D. Li, Recent advances in mathematical programming with semi-continuous variables and cardinality constraint, Journal of the Operations Research Society of China, 1 (2013), pp. 55–77.

- [46] J. Xie, S. He, and S. Zhang, Randomized portfolio selection, with constraints, Pacific Jorunal of Optimization, 4 (2008), pp. 89–112.

- [47] X.J. Zheng, X.L. Sun, and D. Li, Improving the performance of MIQP solvers for quadratic programs with cardinality and minimum threshold constraints: A semidefinite program approach, INFORMS Journal on Computing, 26 (2014), pp. 690–703.