DIV=last

[1]yannick.armenti@gmail.com \eMail[2]stephane.crepey@univ-evry.fr \eMail[3]sdrapeau@saif.sjtu.edu.cn \eMail[4]papapan@math.tu-berlin.de

[t1]Financial support from the EIF grant “Collateral management in centrally cleared trading”, from the Chair “Markets in Transition”, Fédération Bancaire Française, and from the ANR 11-LABX-0019. \myThanks[t2]Financial support from LCH.Clearnet Paris. \myThanks[t3]Financial support from the EIF grant “Post-crisis models for interest rate markets”. \myThanks[t4]Financial support from the DAAD PROCOPE project “Financial markets in transition: mathematical models and challenges”. \myThanks[t5]Financial support from the National Science Foundation of China, “Research Fund for International Young Scientists”, Grant number 11550110184.

Multivariate Shortfall Risk Allocation and Systemic Risk

Abstract

The ongoing concern about systemic risk since the outburst of the global financial crisis has highlighted the need for risk measures at the level of sets of interconnected financial components, such as portfolios, institutions or members of clearing houses. The two main issues in systemic risk measurement are the computation of an overall reserve level and its allocation to the different components according to their systemic relevance. We develop here a pragmatic approach to systemic risk measurement and allocation based on multivariate shortfall risk measures, where acceptable allocations are first computed and then aggregated so as to minimize costs. We analyze the sensitivity of the risk allocations to various factors and highlight its relevance as an indicator of systemic risk. In particular, we study the interplay between the loss function and the dependence structure of the components. Moreover, we address the computational aspects of risk allocation. Finally, we apply this methodology to the allocation of the default fund of a CCP on real data.

Systemic risk, risk allocation, multivariate shortfall risk, sensitivities, numerical methods, CCP, Default Fund.

1507.05351 \keyAMSClassification91G, 91B30, 91G60

1 Introduction

The ongoing concern about systemic risk since the onset of the global financial crisis has prompted intensive research on the design and properties of multivariate risk measures. In this paper, we study the risk assessment for financial systems with interconnected risky components, focusing on two major aspects, namely:

-

•

The quantification of a monetary risk measure corresponding to an overall reserve of liquidity such that the whole system can overcome unexpected stress or default scenarios;

-

•

The allocation of this overall amount between the different risk components in a way that reflects the systemic risk of each one.

Our goal is fourfold. First, we introduce a theoretically sound but numerically tractable class of systemic risk measures. Second, we study the impact of the intrinsic dependence on the risk allocation and it sensitivity. Third, we address the computational aspect and challenges of systemic risk allocation. Finally, we present empirical results, based on real data provided by LCH S.A., on the risk allocation of the default fund of a CCP.

Review of the Literature:

Monetary risk measures have been the subject of intensive research since the seminal paper of Artzner et al. [6], which was further extended by Föllmer and Schied [31] and Frittelli and Rosazza Gianin [32], among others. The corresponding risk measures, including conditional value-at-risk by Artzner et al. [6], shortfall risk measures by Föllmer and Schied [31] or optimized certainty equivalents by Ben-Tal and Teboulle [9], can be applied in a multivariate framework that models the dependence of several financial risk components. Multivariate market data-based risk measures include the marginal expected shortfall of Acharya et al. [1], law invariant convex risk measures for portfolio vectors of Rüschendorf [45], the systemic risk measure of Acharya et al. [2] and Brownlees and Engle [13], the delta conditional value-at-risk of Adrian and Brunnermeier [3] or the contagion index of Cont et al. [20]. In parallel, theoretical economical and mathematical considerations have led to multivalued and set-valued risk measures, in static or even dynamic setup; see for instance Cascos and Molchanov [15], Hamel et al. [36] and Jouini et al. [37].

Recently, the risk management of financial institutions raised concerns about the allocation of the overall risk among the different components of a financial system. A bank, for instance, for real time monitoring purposes, wants to channel to each trading desk a cost reflecting its responsibility in the overall capital requirement of the bank. A central clearing counterparty — CCP for short, also known as a clearing house — is interested in quantifying the size of the so-called default fund and allocating it in a meaningful way among the different clearing members, see [19, 5, 34]. On a macroeconomic level, regulators are considering to require from financial institutions an amount of capital reflecting their systemic relevance. The aforementioned approaches can only address the allocation problem indirectly, through the sensitivity of the risk measure with respect to the different risk components. For instance, the so-called Euler rule allocates the total amount of risk according to the marginal impact of each risk factor. However, a practical limitation of the Euler rule is that it is based on Gâteaux derivatives which in general is difficult to compute beyond simple cases. Also this Euler rule consider the marginal risk of one element with respect to the full system rather than the marginal risk with respect to each individual components. In addition, the Euler risk allocation does not add up to the total risk, unless the univariate risk measure that is used in the first place is sub-additive, see [46]. In other words, the Euler rule does not automatically fulfill the so-called full allocation property. The work by Brunnemeier and Cheridito [14] addresses systematically the question of allocation of systemic risk with regard to certain economic properties:

-

•

Full allocation: the sum of the components of the risk allocation is equal to the overall risk measure;

-

•

Riskless allocation: if a risk factor is riskless, the corresponding component of the risk allocation is equal to it;

-

•

Causal responsibility: any system component bears the entire additional costs of any additional risk that it takes.

More specifically, Brunnemeier and Cheridito [14] propose a framework where an overall capital requirement is first determined by utility indifference principles and then allocated according to a rule such that the above three properties are fulfilled, at least at a first order level of approximation. In fact, as far as dependence is concerned, whether the last two properties should hold is debatable. One may argue that each component in the system is not only responsible for its own risk taking but also for its relative exposure to other components. This is also what comes out from the present study, see Section 4.3. In a general framework, Kromer et al. [39] characterized systemic risk out of axioms allowing for a decomposition between and aggregation function and a univariate risk measure. In the spirit of this aggregation function, in two recent papers, Feinstein et al. [28] and Biagini et al. [10] proposed a general approach similar in spirit to ours. We precise thereafter and later in the paper the relationship to these references and in which sense our take on differs.

Contribution and Outline of the Paper:

Our approach addresses simultaneously the design of an overall risk measure regarding a financial system of interconnected components and the allocation of this risk measure among the different risk components; the emphasis lies on the allocation and its sensitivities. In contrast to [14, 16], we first allocate the monetary risk among the different risk components and then aggregate and minimizes the risk allocations in order to obtain the overall capital requirement. As previously mentioned, [39], [28] and [10] develop approaches in a similar spirit, covering allocation first followed by aggregation, in general frameworks with different aggregation procedures. They focus on the resulting risk measure, conducting systematic studies of their properties in terms of set valued functions, diversification and monotonicity, among others. The multivariate shortfall risk measure of this paper can be viewed as a special case of their definition, in a way precised in Remark 2.11. Sharing with these references the “allocate first, then aggregate” perspective, our approach is restricted to a systemic extension of shortfall risk measures, see [31], based on multivariate loss functions. However, in contrast to the aforementioned references, we focus on the resulting risk allocation in terms of existence, uniqueness, sensitivities and numerical applications. In our framework, the systemic risk is the risk that stems specifically from the intrinsic dependence structure of an interconnected system of risk components. In this perspective, the risk allocation and its properties provide a “cartography” of the systemic risk, see Section 5 on the numerical aspects of risk allocation and the empirical study in Section 6 on real data for an illustration thereof. It turns out that special care has to be given to the specifications of the loss function in order to stress the systemic risk. In [10], by allowing random allocations, the impact of the interdependence structure can be observed in the future. Such random allocations may be interesting in view of a posterior management of defaults. By contrast, our deterministic allocation is sensitive to the dependence of the system already at the moment of the quantification, see Section 4 and see a contrario Proposition 3.11. We study the sensitivity of the risk allocation with respect to external shocks as well as internal dependence structure. We show in particular that a causal responsibility can be derived in marginal terms, see Proposition 4.4. In addition, we discuss computational aspects of risk allocation and finally, we provide an empirical study on the risk allocation of a default fund of a CCP based on real data provided by LCH S.A.

The univariate shortfall risk measure as a law invariant risk measure holds additional properties as an operator on probability distributions. Indeed, as studied by Weber [47] and Krätschmer et al. [38], it has some continuity properties with respect to the -weak topology on distributions. It has been furthermore characterised in [47] as the only convex law invariant convex risk measure on the level of distributions and therefore the unique one having elicitability properties, a wishful statistical property, see [41, 8]. Extensions of these results, such as elicitability characterization in multidimensional case as proposed by Ziegel [48] and Fissler and Ziegel [30], as well as the axiomatic characterization along the lines of [47], are highly non trivial and therefore let for further study. A set-valued multivariate shortfall risk measure has been introduced by Ararat et al. [4]. However, allocation is the not focus of their work and the loss function that they then consider is decoupled in the sense of (C2), which from our viewpoint is too restrictive in view of Proposition 3.11.

The paper is organized as follows: Section 2 introduces the class of systemic loss functions, acceptance sets and risk measures that we use in the paper. Section 3 establishes the existence and uniqueness of a risk allocation. Section 4 focuses on sensitivities with respect to external shocks, dependence structure, nature of the loss function as well as the properties of full allocation, causal responsibility and riskless allocation mentioned beforehand. Section 5 discusses the computational aspects and challenges of risk allocation. Section 6, applies our approach to the concrete allocation of the default fund of a CCP. Appendices A and B gather classical facts from convex optimization and results on multivariate Orlicz spaces. Appendix C provides additional insight on the data of the empirical study.

1.1 Basic Notation

Let denote the generic coordinate of a vector , and the -th unit vector. By we denote the lattice order on , that is, if and only if for every . We denote by the Euclidean norm and by the lattice operations on . For we write for componentwise, , and . We denote by the convex conjugate of a function , and for , we denote by the indicator function of being equal to on and otherwise.

Let be a probability space, and denote by the space of -measurable -variate random variables on this space identified in the -almost sure sense. The space inherits the lattice structure of , hence we can use the above notation in a -almost sure sense. For instance, for and in we say that or if or , respectively. Since we mainly deal with multivariate functions or random variables, to simplify notation we drop the reference to in , writing simply unless necessary.

2 Multivariate Shortfall Risk

Let be a random vector of financial losses, that is, negative values of represent actual profits. We want to determine an overall monetary measure of the risk of as well as a sound risk allocation of among the risk components. We consider a flexible class of risk measures defined by means of loss functions and sets of acceptable monetary allocations. This class allows us to discuss in detail the properties of the resulting risk allocation as an indicator of systemic risk. Inspired by the shortfall risk measure introduced in [31] in the univariate case, we start with a loss function defined on used to measure the expected loss of the financial loss vector .

Definition 2.1.

A function is called a loss function if

-

(A1)

is increasing, that is, if ;

-

(A2)

is convex, lower semi-continuous with ;

-

(A3)

for some constant .

A loss function is permutation invariant if for every permutation of the components.

A risk neutral assessment of the losses corresponds to . Thus, (A3) expresses a form of risk aversion, whereby the loss function puts more weight on high losses than a risk neutral evaluation. As for (A1) and (A2), they express the respective normative facts about risk that “the more losses, the riskier” and “diversification should not increase risk”; see [22] for related discussions.

Remark 2.2.

The choice of the terminology “loss function” stems from [31] for which this paper is a multivariate extension. Our notion of a loss function coincide with the one of “aggregation function” in [28, 10], in the sense that it aggregate several loss profiles into a univariate random variable for which it can be decided whether or not it is acceptable, see Remark 2.11. Due to the obvious extension from the shortfall risk measure, throughout this paper we stick to the terminology “loss function”.

As for the permutation invariance, the considered risk components are often of the same type — banks, members of a clearing house or trading desks within a trading floor. In that case, the loss function should not discriminate a particular component against another.

Example 2.3.

Let be a one-dimensional loss function such as for instance

Using these as building blocks, we obtain the following classes of multivariate loss functions, which will be used for illustrative purposes in the discussion of systemic risk, see Section 3 and 4.

-

(C1)

;

-

(C2)

;

-

(C3)

, where non both zero.

Note that each of these loss functions are permutation invariant.

For integrability reasons we consider loss vectors in the following multivariate Orlicz heart:111Orlicz spaces are natural spaces in this context. The theory of Orlicz spaces has been used for long in the theory of risk measures, see [21, 11, 18, 12].

where , ; see Appendix B.

Remark 2.4.

Definition 2.5.

A monetary allocation is acceptable for if

We denote by

| (1) |

the corresponding set of acceptable monetary allocations.

Example 2.6.

In a centrally cleared trading setup, each clearing member is required to post a default fund contribution in order to make the risk of the clearing house acceptable with respect to a risk measure accounting for extreme and systemic risk. The default fund is a pooled resource of the clearing house, in the sense that the default fund contribution of a given member can be used by the clearing house not only in case the liquidation of this member requires it, but also in case the liquidation of another member requires it. For the determination of the default fund contributions, the methodology of this paper can be applied to the vector defined as the vector of stressed losses-and-profits of the clearing members. According to the findings of Section 3 and 4, a “systemic” loss function such as (C3) with would be consistent with the purpose of a default fund. Note however that our setup applied to clearing houses takes the view of a closed system, so an internal assessment. In principle we ignore additional systemic risk such as a competition between clearing houses with common membership, or the external risk to which these members may be subject to, as addressed for instance in [35]. However, our method could also assess such a systemic risk by taking as the overall vector of positions of each member in each clearing house.

The next proposition gathers the main properties of the sets of acceptable monetary allocations. The convexity property in (i) means that a diversification between two acceptable monetary allocations remains acceptable. If a monetary allocation is acceptable, then any greater amount of money should also be acceptable, which is the monotonicity property in (i). As for (ii), it says that, if the losses are less than almost surely, then any monetary allocation that is acceptable for is also for . Next, (iii) means that a convex combination of allocations acceptable in two markets is still acceptable in the diversified market. In particular, the acceptability concept pushes towards a greater diversification among the different risk components. From the viewpoint of a clearing house for instance, a diversified position of its members is preferable to a concentrated one and therefore may enforce default fund allocations that incite its members towards this goal. Also, from a trading floor supervision, an overall diversified position of the traders is preferable, an incentive which is a current practice, see example 5.2. Finally, (iv) means that acceptable positions translate with cash in the sense of scalar monetary risk measures à la [6, 31, 32]. As an immediate consequence of these properties, defines a monetary set-valued risk measure in the sense of [36], that is, a set-valued map from into the set of monotone, closed and convex subsets of .

Proposition 2.7.

For in , it holds:

-

(i)

is convex, monotone and closed;

-

(ii)

whenever ;

-

(iii)

for any ;

-

(iv)

for any ;

-

(v)

.

If furthermore

-

(vi)

is positive homogeneous, then for every ;

-

(vii)

is permutation invariant, then for every permutation ;

Proof 2.8.

Since is convex, increasing and lower semi-continuous, it follows that is convex and lower semi-continuous, decreasing in and increasing in . This implies the properties (i) through (iii) by Definition 2.5 of . Regarding (iv), a change of variables yields

As for (v), on the one hand, as component-wise. Since it follows that , thus monotone convergence yields and in turns the existence of such that , showing that . On the other hand, being increasing and such that , it implies that as , component-wise. Hence, monotone convergence yields , therefore there exists such that , that is, . As for (vi), if is positive homogeneous, for any it holds . Hence is in if and only if is in if and only if is in . Finally, if is permutation invariant, for any permutation it holds . Hence is in if and only if is in , if and only if is in showing (vii).

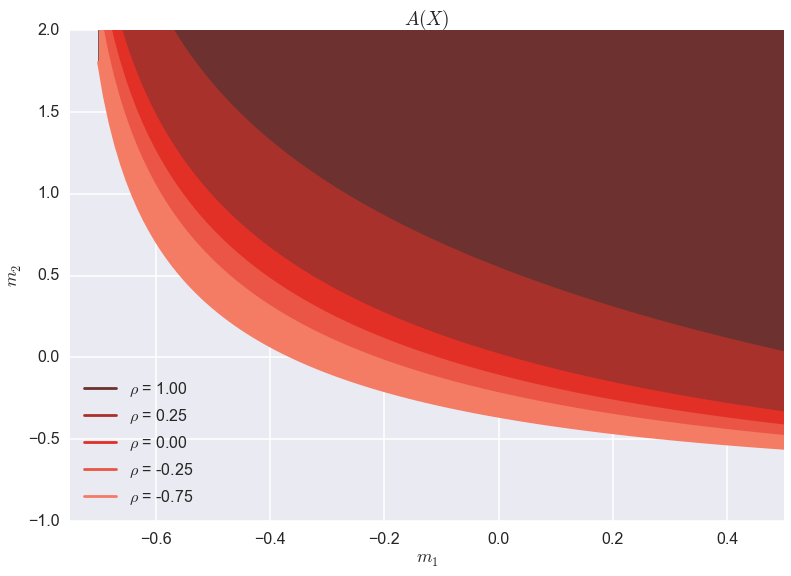

Figure 1 shows sets of acceptable monetary allocations for a bivariate normal distribution with varying correlation coefficient. The location and shape of these sets change with the correlation: the higher the correlation, the more costly the acceptable monetary allocations, as expected in terms of systemic risk. As discussed in Sections 3 and 4, this feature is not always immediate and depends on the specification of the loss function.

Given an acceptable monetary allocation , its aggregated liquidity cost is . The smaller the cost, the better, which motivates the following definition.

Definition 2.9.

The multivariate shortfall risk of is

| (2) |

Example 2.10.

Following up on the central clearing house Example 2.6, any acceptable allocation yields a corresponding value for the default fund. Clearing houses are in competition with each other, hence they are looking for the cheapest acceptable allocation to require from their members.

Remark 2.11.

When , the above definition corresponds exactly to the shortfall risk measure in [31], of which this paper is a multivariate extension.

The set valued risk measure introduced in (1) can be seen as an example of the set valued systemic risk measures presented in [28], which in their notation translates as follows

where the aggregation is given by for and the acceptance set is . Their setting considers more general random fields associated with capital allocations denoted by accommodating for instance the modelling of financial networks, among others. The case we consider can be embedded into [28, Case (ii), Page 5]. Even if set valued risk measure is not the primary focus of [10], it is included in the definition of the acceptance family which, in their notation, is given as follows

where and . The resulting systemic risk measure can also be translated in their notation and denomination in terms of an aggregating function , acceptance set and a measure of risk , resulting into

Therefore the case we consider can be embedded into the class presented in [10, Section 1.3].

Our next result, which uses the concepts and notation of Appendix B, shows that all the classical properties of the shortfall risk measure, including its dual representation, can be extended to the multivariate case. We denote by

the set of -dimensional measure densities in normalized to . For the sake of simplicity, we use the notation for and .

Theorem 2.12.

The function

is real valued, convex, monotone and translation invariant.222In the sense that . In particular, it is continuous and sub-differentiable. If is positive homogeneous, then so is . Moreover, it admits the dual representation

| (3) |

where the penalty function is given by

| (4) |

Remark 2.13.

This robust representation can also be inferred from the general results of [27]. However, for the sake of completeness and since the multivariate shortfall risk measure is closely related to a multidimensional version of the optimized certainty equivalent, we give a self contained proof tailored to our context.

The argumentation follows the original one by [31], which however cannot be directly applied on the product space since the optimization is done here according to multidimensional allocations rather than one dimensional allocations . Moreover, in the course of our derivation of the dual representation we extend to the multidimensional setting the following relationship between the optimized certainty equivalent and the shortfall risk provided in [9, Chapter 5.2]

where

is the optimized certainty equivalent of .333Here is a one dimensional loss function and a one dimensional random variable.

Proof 2.14.

By Proposition 2.7 (v), we have and in turn . If for some , then there exists a sequence such that , in contradiction with . Hence, . Monotonicity, convexity and translation invariance readily follow from Proposition 2.7 (ii), (iii) and (iv), respectively. In particular, is a convex, real-valued and increasing functional on the Banach lattice . Hence, by [18, Theorem 4.1], is continuous and sub-differentiable. Therefore, the results recalled in Appendix B and the Fenchel-Moreau theorem imply

| (5) |

where , . By the bipolar theorem, for , there exists , with for some . By monotonicity of , it follows that for every . Hence

Furthermore, by translation invariance, setting for , it follows that

where the right hand side can be made arbitrarily large whenever . It shows that the supremum and maximum in (5) can be restricted to the set of those such that and , that is, can be identified to . In order to obtain a more explicit expression of the penalty function , we set

The functional is a multivariate version of the so called optimized certainty equivalent, see [9]. Clearly,

Since is nonempty and monotone, there exists and so the Slater condition is fulfilled. As a consequence of [42, Theorem 28.2], there is no duality gap. Namely, . Via the first part of the proof, an easy multivariate adaptation of [9, Chapter 4] and [23, Chapter 2] yields

where , hence . Combining this with the dual representation (4) follows.

Example 2.15.

We consider the two positive homogeneous loss functions of the empirical study:

| (6) | ||||

| (7) |

for . A simple computation yields that where

Note that where and are identified with their vector of equal components. Furthermore, is an extreme point of . It follows in particular that . By positive homogeneity, only takes values or . It follows that if and only if there exits such that almost surely. Since has to be in for this to happen, we can constrain in the case of and in the case of . Thus

3 Risk Allocation

We have established in Theorem 2.12 that the infimum over all allocations used for defining is real valued and has the desired properties of a risk measure. Beyond the question of the overall liquidity reserve, the allocation of this amount between the different risk components is key for systemic risk purposes. We therefore address in this section the following questions:

-

•

The existence of a risk allocation;

-

•

The uniqueness of a risk allocation;

-

•

The impact of the interdependence structure,

The first question is important in some applications such as the default fund contribution of each member of a clearing house or the allocation of the capital among the different business lines of a bank. As for the second question, non-uniqueness can become an issue when this allocation is a regulatory cost for the different members or desks. If no additional clear rule is provided, the members would then face arbitrariness as for their contributions for the same overall risk. As for the last question, systemic risk should reflect the level of dependence of the system. For instance, highly correlated losses, while having the same marginal risk, should result into a higher systemic risk and different optimal allocations.

Definition 3.1.

A risk allocation is an acceptable monetary allocation such that . When a risk allocation is uniquely determined, we denote it by .

Remark 3.2.

By definition, if a risk allocation exists, then the full allocation property automatically holds; see also Section 4.3.

In contrast to the univariate case, where the unique risk allocation is given by , existence and uniqueness are no longer straightforward in the multivariate case. The following example shows that existence may fail.

Example 3.3.

Consider the loss function if and otherwise. It follows that . Computations yield . However, the infimum is not attained.

Our next result introduces conditions towards the existence and uniqueness of a risk allocation.

Definition 3.4.

We call a loss function permutation invariant if, holds for every permutation of the components of the vector .

Note that the loss function used in Example 3.3 is not permutation invariant. We denote by the set of zero-sum allocations.

Theorem 3.5.

If is a permutation invariant loss function, then, for every , risk allocations exist. They are characterized by the first order conditions

| (8) |

where is a Lagrange multiplier. In particular, when has no zero-sum direction of recession444We refer the reader to Appendix A regarding the notions and properties of recession cones and functions. In particular, if has no zero-sum direction of recession except , then is an unbiased loss function. except , the set of the solutions to the first order conditions (8) is bounded.

If is strictly convex along zero-sums allocations for every with , then the risk allocation is unique.

Proof 3.6.

Let in , according to Theorem A.1, it holds

Further, we define . It follows that is increasing, convex, lower semi-continuous, proper and such that . Since and , for it holds

showing that . By [42, Theorem 27.1 (b)], the existence of a risk allocation follows from being constant along its directions of recession , which according to Theorem A.1, is equivalent to implies . However, since is permutation invariant it follows that and therefore implies that . Thus the existence of a risk allocation.555Note that this computation shows that the condition is sufficient to get the existence of a risk allocation. In particular, if , then by [42, Theorem 27.1, (d)], the set of risk allocations is non-empty and bounded. Furthermore, since for some large enough, the Slater condition for the convex optimization problem is fulfilled. Hence, according to [42, Theorems 28.1, 28.2 and 28.3], optimal solutions are characterized by (8).

Finally, let be two risk allocations. It follows that is a risk allocation as well for every . Furthermore, is a zero sum allocation. By convexity, it follows that for every , which shows that -almost surely for every . Since is strictly convex on for every such that , it follows that for every , showing in particular that , a contradiction.

Corollary 3.7.

Let be a permutation invariant loss function, such that is strictly convex along zero-sum allocations for every with . It holds

If is additionally positive homogeneous, it holds

Proof 3.8.

From Theorem 3.5, the assumptions on ensure the existence and uniqueness of a risk allocation uniquely characterized, together with the Lagrange multiplier, by the first order conditions. Let , for which there exists a unique such that and . Hence, and satisfy the first order conditions and , which by uniqueness shows that . As for the second assertion, it follows from for every according to Proposition 2.7.

Remark 3.9.

In general, the positivity of the risk allocation is not required. However, if positivity or any other convex constraint is imposed, for instance by regulators, it can easily be embedded in our setup. In case of positivity, this would modify the definition of into

with accordingly modified first order conditions.

As already mentioned, the following example illustrates the importance of the uniqueness.

Example 3.10.

Any loss function of class (C1), that is, , is permutation invariant. Thus, a risk allocation exists by means of Theorem 3.5. However, for any zero-sum allocation , we have and , so that is another risk allocation.

In terms of regulatory costs, this is a problematic situation. Indeed, consider two banks and require from them M € and M €, respectively, as capital allocation. In such a case, one could equally well require M € from the first bank and nothing from the second. Such arbitrariness is unlikely to be accepted in that case.

Example 3.10 shows that loss functions of the class (C1) lack the uniqueness of a risk allocation. By contrast, for loss functions of class (C2), that is, , the following proposition shows that, while there exists a unique risk allocation under very mild conditions, the risk allocation only depends on the marginal distributions of the loss vector . In other words, the risk measure and the risk allocation do not reflect the dependence structure of the system.

Proposition 3.11.

Let for univariate loss functions strictly convex on , . For every , there exists a unique optimal risk allocation and we have , for every such that has the same distribution as .

Proof 3.12.

Let be such that for every . It follows that . The loss function is furthermore unbiased. Indeed, for every zero-sum allocation , assuming without loss of generality , it follows that

since is strictly convex and . Hence, has no zero-sum direction of recession other than . The strict convexity of yields, according to Theorem 3.5, the existence of a unique risk allocation for every . The first order conditions (8) are written as

which only depend on the marginal distributions of .

Following Rüschendorf [44] we can characterise in terms of supermodular, directionally convex and upper orthant stochastic ordering the risk of positive dependence in terms of . For a function we define

We say that a continuous function is

-

•

super-modular, if for every ;

-

•

directionally convex, if for every ;

-

•

-monotone, if for every ;

for every and in with . We denote by , and the integral orders given by the respective class of functions. We refer to [44] for a discussion of these orders in terms of dependence risk. Note that if and only if for every .

Proposition 3.13.

The shortfall risk measure is monotone with respect with , or whenever is super-modular, directionally convex, or -monotone, respectively.

Proof 3.14.

The assertion follows immediately from the fact that if is one of super-modular, directionally convex, or -monotone, so is for every . Therefore if , it follows that showing that .

Remark 3.15.

Any loss function of the form (C1), (C2) and (C3) are directionally convex and therefore super-modular. They are -monotone if . As for the specific loss functions used in this paper in several places for illustration

are both directionally convex and -monotone. However, if they are degenerated in terms of these monotonicity since for every . As soon as , these loss functions are strictly monotone on .

Remark 3.16.

A loss function can be chosen in view of an a-priori list of wished properties in terms of risk measurement and allocation as the Proposition above mentioned. However, loss function may also arise in systemic risk problems as an intrinsic property of the system as presented by Eisenberg and Noe [25] or recently by Awiszus and Weber [7].

Example 3.17.

The following simple example shows the impact of the dependence in a simple case for a loss function

| (9) |

that is -monotone and bivariate normal vector with . Solving the first order conditions yield

showing that the risk allocations are disentangled into the respective individual contributions , , and a systemic risk contribution

| (10) |

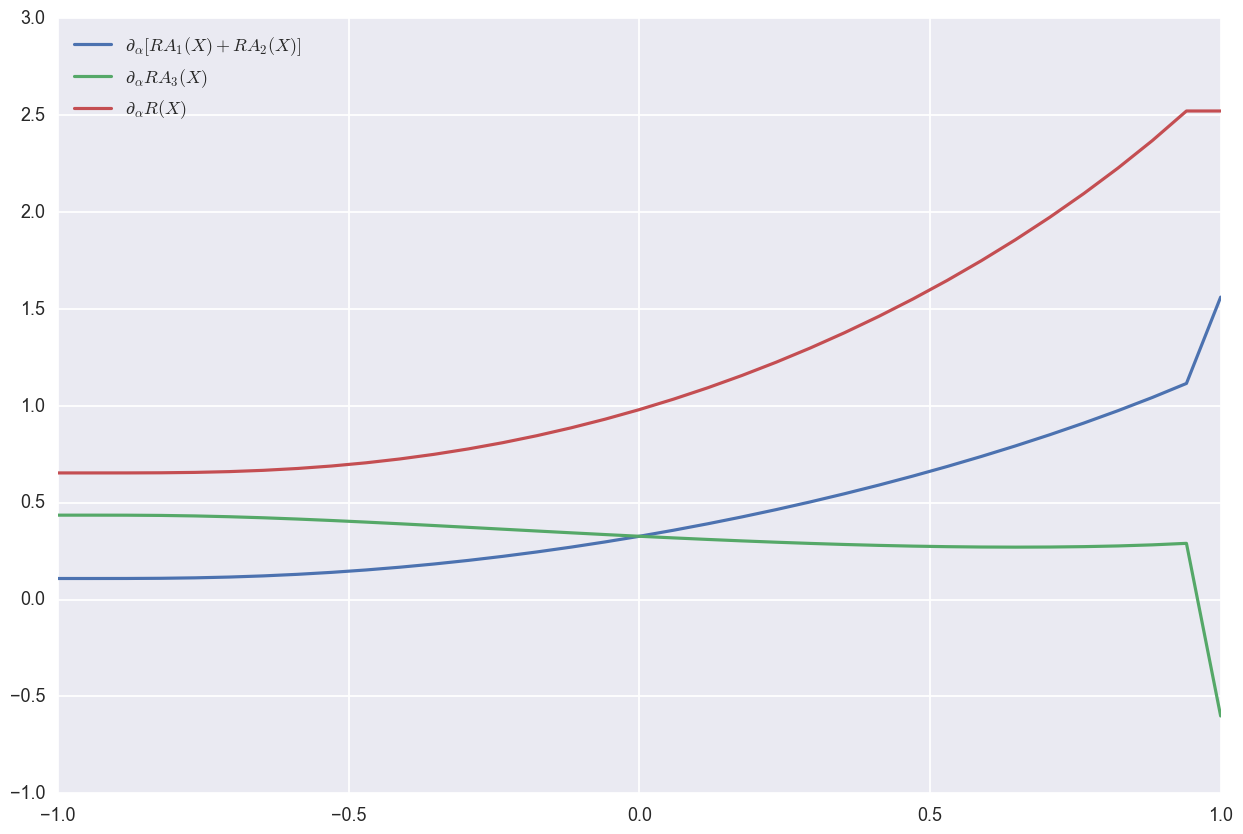

which depends on the correlation parameter and on the systemic weight of the loss function. Figure 2 shows the value of this systemic risk contribution as a function of and .

Computing the partial derivatives with respect to and yields

showing that the systemic risk contribution is

-

•

increasing with respect to the correlation ;

-

•

decreasing with respect to if the correlation is negative;

-

•

increasing up to and then decreasing with respect to if the correlation is positive as the individual risk of dominates the risk of the system.

4 Systemic Sensitivity of Shortfall Risk and its Allocation

The previous results emphasize the importance of using a loss function that adequately captures the systemic risk inherent to the system. This motivates the study of the sensitivity of shortfall risk and its allocation so as to identify the systemic features of a loss function.

Definition 4.1.

The marginal risk contribution of to is defined as the sensitivity of the risk of with respect to the impact of , that is

In the case where admits a unique risk allocation for every , the risk allocation marginals of the risk of with respect to the impact of are given by

Theorem 2.12 and its proof show that the determination of the risk measure reduces to the saddle point problem

Using [42], the “argminmax” set of saddle points is a product set that we denote by .

Theorem 4.2.

Assuming that is permutation invariant, then

Supposing further that is twice differentiable and that is such that

is non-singular, then

-

•

there exists such that is a singleton, for every ;

-

•

the corresponding unique saddle point is differentiable as a function of and we have

where and

Proof 4.3.

Let . Theorem 2.12 yields

for every selection . Regarding the first assertion of the theorem, since has no zero-sum direction of recession other than , it follows from Theorem 3.5 that is non empty and bounded. Hence, the assumptions of Golshtein’s Theorem on the perturbation of saddle values, see Rockafellar and Wets [43, Theorem 11.52], are satisfied and the first assertion follows. As for the second assertion, the assumptions of Fiacco and McCormick [29, Theorem 6, pp. 34–45] are fulfilled. The Jacobian of the vector

that is used to specify the first order conditions is given by the matrix . Hence, the second assertion follows from [29, Theorem 6, pp. 34–35].

Theorem 4.2 allows to explicitly derive the impact of an independent exogenous shock as stated in the following proposition.

Proposition 4.4.

Under the assumptions of Theorem 4.2 ensuring the uniqueness of a saddle point, suppose that is independent of . Then

Proof 4.5.

Since is independent of , denoting by , it follows from the first order conditions that

Furthermore, we have

where , and . Using the classical formula of block matrix inversion, we obtain

According to the discussion about causal responsibility in Section 4.3, it follows that each member is marginally paying for the additional risk is takes provided this one is independent of the system. In particular, if the risk factor is affected by a shock independent of the system, it follows that , showing that the member pays for the full risks it takes.

4.1 Impact of an Exogenous Shock

The following Section illustrates the case when the exogenous shock may depend on . We consider a bivariate situation where , and exogenous factor impacting only the first component. We consider the loss function

which gives rise to a unique risk allocation by virtue of Theorem 3.5. Note that is -monotone, and strictly on if . For ease of notations, we assume that , which, since is permutation invariant, implies that . Let and . According to Theorem 4.2, and the first order condition (8), we have

As for the allocation of this marginal risk contribution, in the notation of Theorem 4.2, we have:

which by inverting yields

Beyond the fact that according to Proposition 4.4, if is independent of then and , observe in general that:

-

•

The two risk components marginally share first equally the additional cost of the exogenous impact in terms of each.

-

•

The asymmetry of the shock that concerns only is reflected in the correction with respect to the second term which is added to the first one and subtracted to the second. Furthermore, for every . It implies that the additional risk taken by the first risk factor is always positively proportional to while the second one is negatively proportional to .

-

•

If , then the marginal change impact the risk factors according to .

-

•

If and and are strongly anti-correlated, then is likely very small and therefore the effect is similar to the case where . On the other hand, if and are strongly correlated, then and in that case showing that the full dependence with yields an equal share of the marginal risk changes.

4.2 Sensitivity to Dependence

Following the previous section where the loss function depends on that impacts the risk allocation with respect to the degree of dependence between risk factors, we apply the techniques of Theorem 4.2 to study the sensitivity with respect to . To this end we consider a loss function of the following form

where is a one dimensional loss function and a multidimensional function such that is a loss function for all close enough to . For instance a loss function of the class (C3). We also suppose that is twice differentiable. Using the same strategy as in the proof of the Theorem 4.2, we can provide the marginal risk contribution and allocation as a function of around , stressing the dependence part of the loss function. Computations yield

where is given by and and and as in the proof of Proposition 4.4. In the case where

and with , and independent of , it follows that for every . Defining , computations yields

Hence, with increasing correlation between and the marginal risk increases. As for the impact on the risk allocation, since it simplifies to

Due to the asymmetric dependence of the system:

-

•

One the one hand, if and are highly anti-correlated, then

The systemic risk factor is advantaging those who are anti-correlated, with respect to the others.

-

•

On the other hand, if and are highly correlated, then for ,

Since , the systemic risk factor penalizes those who are highly correlated and reduces the costs for the one who is independent with respect to the previous case.

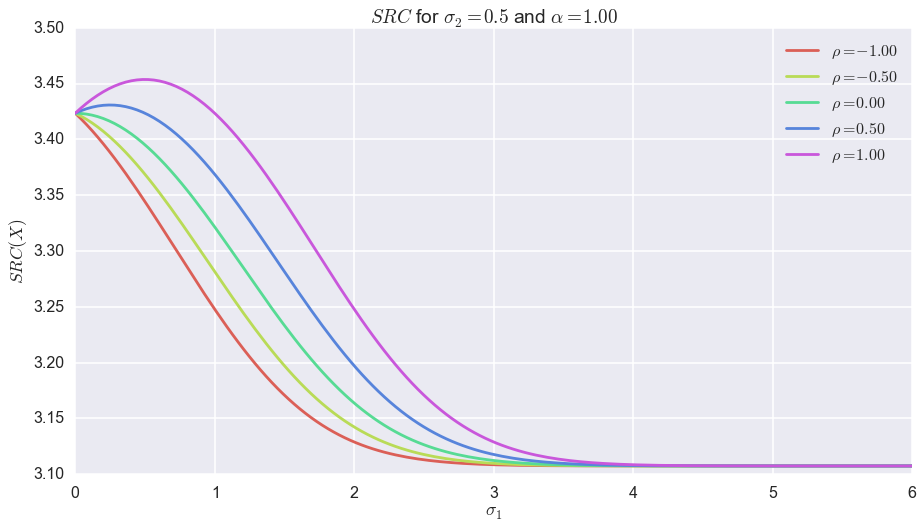

Figure 3 illustrate this fact for different correlation values in the case of a 3-variate normal distribution

4.3 Riskless Allocation, Causal Responsibility and Additivity

We conclude this section regarding risk allocation and its sensitivity by a discussion of their properties in light of the following economic features of risk allocations introduced in [14].

-

(FA)

Full Allocation: ;

-

(RA)

Riskless Allocation: if is deterministic;

-

(CR)

Causal Responsibility: , where is a loss increment of the -th risk component;

As mentioned before, per design, shortfall risk allocations always satisfy the full allocation property (FA). As visible from the above case studies, riskless allocation (RA) and causal responsibility (CR) are not satisfied in general. In fact, from a systemic risk point of view, we think that (RA) and (CR) are not desirable properties. Indeed, both imply that risk taking, or non-taking, should only impact the concerned risk component. However, the risk components are interdependent and any move in one of them bears consequences to the rest of the system. The search for an optimal allocation is a non-cooperative game between the different system components, each of them respectively looking for its own minimal risk allocation while impacting the others by doing so. In other words, everyone is responsible for its own risk but also for its relative exposure with respect to the others. The sensitivity analysis of this section however shows that external shocks are primarily born by the risk component that is hit at least in a first order. In the case where this shock is independent of the system, by Proposition 4.4 it is then a full causal responsibility. Otherwise, a correction appears and a fraction of the shock is offloaded to the other risk components according to their relative exposure to the concerned component and dependence with the shock.

5 Computational Aspects of Risk Allocation

In this section we present computational results based on the loss function of Example 2.3, that is,

| (11) |

for or . In that case, the constrained problem (2) becomes:

| (12) | ||||

According to Theorem 3.5, the risk allocation is determined by the first order conditions (8), which read in this case:

| (13) |

We use Gaussian distributions with mean vector and variance-covariance matrix for the loss vector . In the bi- and tri-variate cases the variance-covariance matrix is parameterized by a single correlation factor and the variances of for all . In other words, for . We write CT for computational time. The implementation was done on standard desktop computers in the Python programming language. To solve the constrained problem (2), we use the Sequential Least SQuares Programming (SLSQP) algorithm, in combination with Monte Carlo, Fourier or Chebychev interpolation schemes, briefly described below, for the computation of the expectations in (13).

Fourier methods

Assuming that the moment generating functions of the considered distributions are available, Fourier methods allow us to compute the different expectations in (13), based on methods presented among other in Eberlein et al. [24] and Drapeau et al. [23] for details. The main advantage of this method is that it is theoretically possible to compute the value of the integrals at any level of precision, while the basic computational time is roughly doubled for every additional digit of accuracy. However, as seen in the subsequent computations this method suffers from the large number of double integrals to be computed, for which the computational time can become prohibitively long.

Monte-Carlo Methods

We can also use Monte Carlo simulations for the estimation of the many integrals in (13). An important observation here is that we can generate and store all realizations in advance, and then use them for the estimation of the functions for different in every step of the root-finding procedure. The main advantage of Monte Carlo relative to Fourier methods is that a wider variety of models can be considered; think, for example, of models with copulas or of random variables with Pareto type distributions as considered in the empirical study in Section 6. The main disadvantage is the slow statistical convergence of the scheme, in our context though is fast enough. In addition, the time to generate, once and for all, the samples, as well as to compute the Monte Carlo averages, is very fast and independent of the value of .

Chebychev interpolation

A numerical scheme well-suited to approximate the large numbers of functions in the context of optimization routines is the Chebyshev interpolation method. This method, recently applied to option pricing by Gaß et al. [33], can be summarized as follows: Suppose you want to evaluate quickly a function , of one or several variables, for a large number of ’s. The first step of the Chebyshev method is to evaluate the function on a given set of nodes , . These evaluations can be computed by Fourier or Monte Carlo schemes, are independent of each other and can thus be realized in parallel. The next step, in order to compute for an outside the nodes , is to perform a polynomial interpolation of the ’s using the Chebyshev coefficients. In other words, the Chebyshev method provides a polynomial approximation of .

Discussion:

Whether it is advantageous to use the Chebyshev interpolation or not, is a matter of two competing factors that affect the computational time: On the one hand, the number of iterations needed to find the root of the system and, on the other hand, the size of the grid used in the Chebyshev interpolation. Our findings reveals that the Monte Carlo schemes are better than the Fourier schemes in the range of our accuracy requirements, since they require the least amount of work during each step of the root-finding procedure or for the pre-processing computations in the Chebyshev method. Only when the dimension is low, less than three or can the Fourier methods be faster. Next, the choice between Chebyshev or not is a matter of comparison between and . In high dimensions, when dominates , with being in principle of order and usually between and , then the Chebyshev method is less costly. Furthermore, the Chebyshev method can intensively benefit from parallel computing as the pre-processing step is not sequential.

5.1 Bivariate case

We suppose that and consider a bivariate Gaussian distribution with zero mean, and correlation in . When setting , that is without systemic risk weight, the result does not depend on the correlation value. Since the allocation is symmetric and we find . Explicit formulas for the involved expectations are available in this case and this yields of course the fastest computation. Fourier methods are quite fast (CT explicit formula) as we only need to compute 1-dimensional integrals. In order to get a high approximation in the Chebychev approximation, one must use 20 nodes for each integral. Since the number of iterations in the optimizations is about, the Chebychev method coupled with Fourier transforms is slower than Fourier without it. Finally, Monte-Carlo is slower than Fourier, becoming the slowest method in that case. When setting , the values of the risk allocation are increasing with respect to , as expected, see Table 1. The Monte-Carlo method becomes the fastest one. Indeed, we now need to compute bi-variate integrals in (13). Even if Fourier methods are fast (from 30 seconds to almost 3 minutes), they are still slower than Monte-Carlo. Moreover, using even as little as 10 nodes in the Chebychev interpolation, which is not very accurate, increases the total computational time because of the number of 2-dimensional integrals to compute in the preprocessing step.

| Fourier | Fourier + Chebychev 10 nodes | Monte Carlo 2 Mio | |||||||

|---|---|---|---|---|---|---|---|---|---|

| CT | CT | CT | |||||||

| -0.167 | 61520 ms | -0.150 | 45 m 18 s | -0.167 | 3257 ms | ||||

| -0.143 | 37100 ms | -0.132 | 30 m 27 s | -0.143 | 3357 ms | ||||

| -0.120 | 45200 ms | -0.113 | 25 m 21 s | -0.120 | 3414 ms | ||||

| -0.103 | 51800 ms | -0.098 | 24 m 52 s | -0.103 | 3302 ms | ||||

| -0.085 | 75700 ms | -0.082 | 27 m 55 s | -0.085 | 3417 ms | ||||

| -0.057 | 158000 ms | -0.055 | 32 m 10 s | -0.056 | 3250 ms | ||||

| -0.013 | 88900 ms | -0.012 | 55 m 04 s | -0.012 | 3387 ms | ||||

5.2 Trivariate Case

In this section, we illustrate the systemic contribution of the loss function with three risk components and study the impact of the interdependence of two components with respect to the third one. We start with a Gaussian vector with the variance-covariance matrix

for different correlations . Here the third risk component has a higher marginal risk than the first two so that, in the absence of systemic component, it should contribute most to the overall risk. When , this is indeed the case. The result is independent of the correlation and is typically overall lower, charging the risk component with the highest variance more – – than the other two – . However, with systemic risk weight, the contribution of the first two overcomes the third one for high correlation, as emphasised in red in Table 2. These results illustrate that the systemic risk weights correct the risk allocation as the correlation between the first two risk components increases. The Monte Carlo scheme in this trivariate case is radically faster than Fourier, (and Chebychev interpolation was not found useful in this case either), from 30 times up to 60 times more efficient.

| Fourier Method | Monte Carlo 2 Mio | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCP | TCP | |||||||||||

| -0.189 | 0.096 | -0.258 | 2 m 55 s | -0.190 | 0.095 | -0.283 | 3159 ms | |||||

| -0.135 | 0.016 | -0.253 | 1 m 39 s | -0.134 | 0.017 | -0.252 | 2799 ms | |||||

| -0.099 | -0.030 | -0.229 | 1 m 32 s | -0.098 | -0.030 | -0.228 | 2760 ms | |||||

| -0.076 | -0.059 | -0.212 | 2 m 22 s | -0.077 | -0.058 | -0.212 | 3188 ms | |||||

| -0.053 | -0.086 | -0.194 | 1 m 37 s | -0.055 | -0.086 | -0.195 | 2741 ms | |||||

| -0.020 | -0.125 | -0.165 | 1 m 47 s | -0.020 | -0.124 | -0.164 | 3358 ms | |||||

| 0.025 | -0.173 | -0.121 | 2 m 07 s | 0.026 | -0.171 | -0.119 | 2722 ms | |||||

5.3 Higher Dimensions

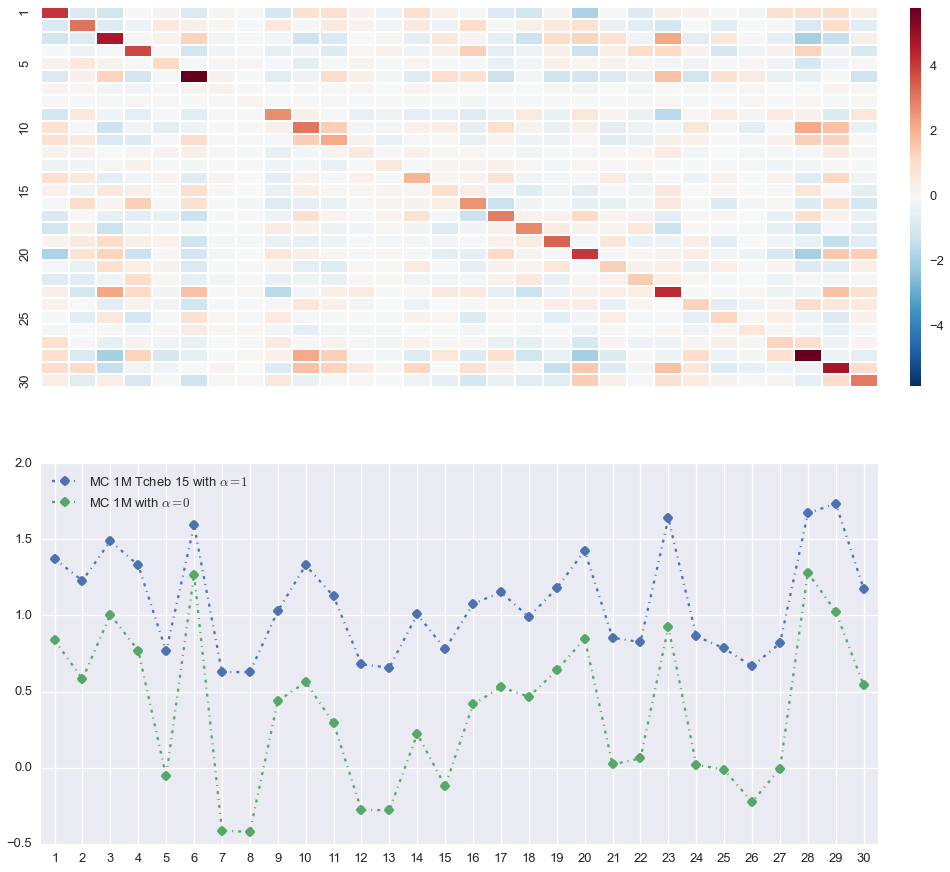

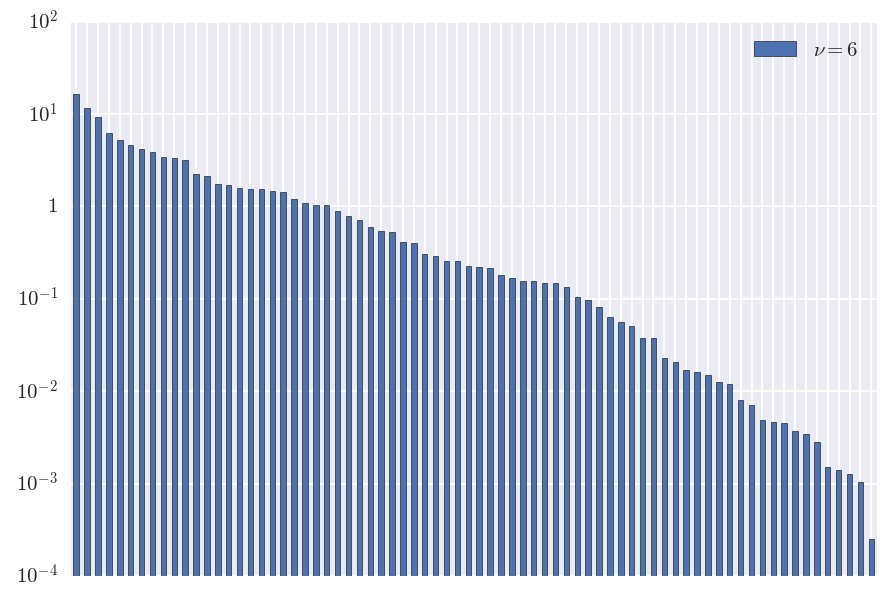

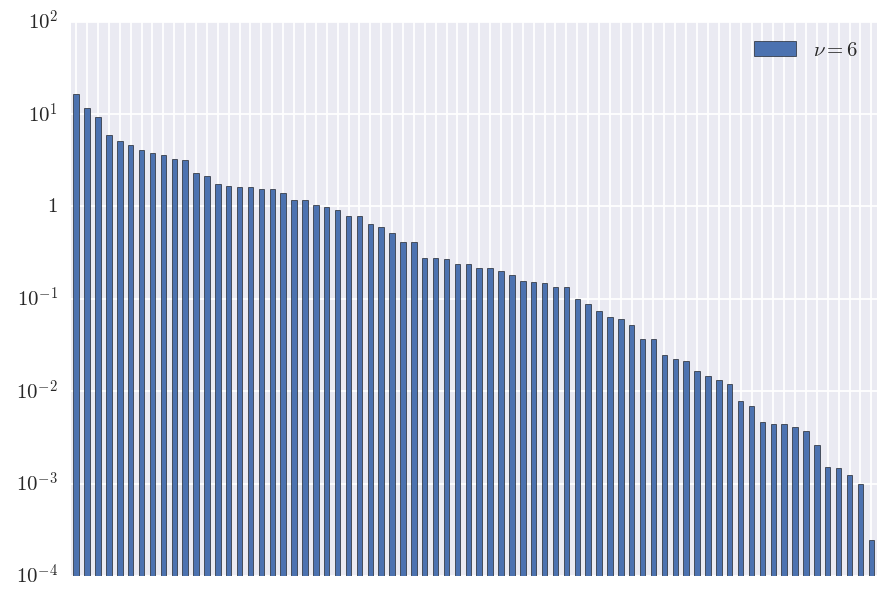

Figure 4 show the variance-covariance matrix and the resulting risk allocation in a 30-variate case using Monte Carlo, coupled with 15 node Chebychev interpolation when . Indeed, the dimension being large, the preprocessing time with Monte-Carlo to compute the Chebychev coefficients together with the computational time resulting from the root-finding with the polynom is lower than the raw Monte-Carlo root finding. The plot shows that the risk allocation depends not only on the variance of the different risk components, but also, in the case where , on the corresponding dependence structure. For instance, compare components 28 and 29 in the 10-variate case in Figure 4. In the first case we observe that when , component 28 contributes more than 29, and conversely when . The reason is that even if component 28 has a slightly higher variance, it is relatively less correlated than 29 to the components 2, 3, 6, 20 and 23 that have the highest variance, and thus are the most ‘dangerous’ from the systemic point of view. Hence, component 29 is more exposed than 28 in case of a systemic event.

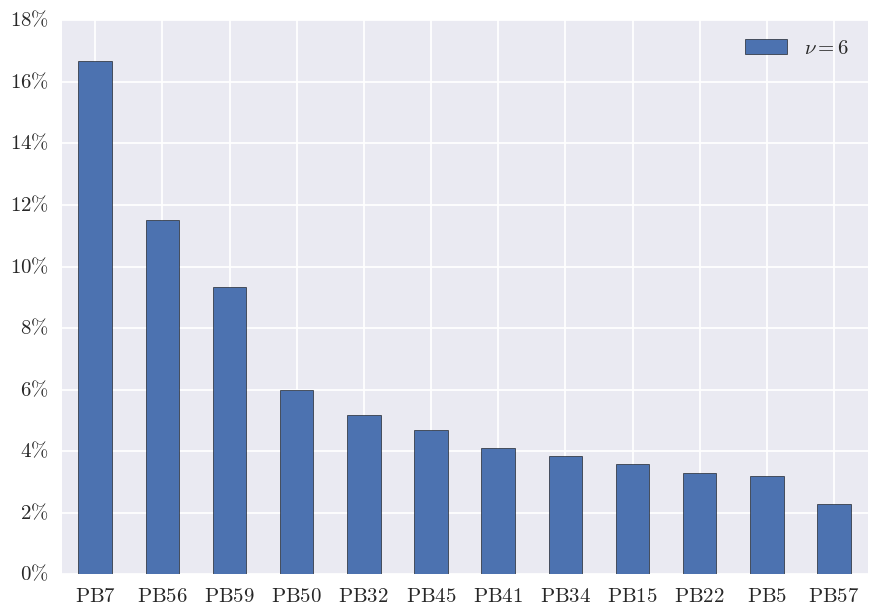

6 Empirical Study: Default Fund Allocation

In the sequel we consider loss functions of the type

| (14) | ||||

| (15) |

The first loss function means that a position is acceptable if on average, the losses are compensated by gains twice as large.666The coefficient is naturally subject to consensus and can be taken as any real number between and . In this case, the risk assessment of the losses is marginal or component-wise. The second one is similar, however, it also aggregates pairwise losses and gains among the different components. Here the risk assessment considers additionally the pairwise dependence between the losses. Note that each of these loss function is positive homogeneous (hence so is ) and permutation invariant.

The default fund of a CCP is a protection against extreme and systemic risk. As of today, it is sized according to the Cover 2 rule, see [26, article 42, §3, p. 37]. In a rough way, this corresponds to the maximal joint loss of two members over their posted collateral (initial margin) in a stressed situation over the last 60 days. The relative contribution of each member to the default fund is proportional to their respective initial margin – that is, the value at risk at a given level of confidence of their loss and profit over a three-day time horizon. Hence, denoting by the total size of the default fund and by the initial margin of member , the contribution of member is given by

| (16) |

As an alternative, we propose to define the contribution of member to the default fund as follows. According to theorem 3.5 there exists a unique optimal capital allocation for a given loss vector . We define therefore the relative risk contribution of each financial component as

| (17) |

The value at risk for the initial margins , the overall risk measure as well as the optimal capital allocation are all positive homogeneous. It follows that for every , that is, the relative risk contribution is scaling invariant as for instance the Sharpe ratio, Minmax ratio or Gini ratio among others, see Cheridito and Kromer [17]. The scaling invariance property allows one to consider the allocation independently of the total size of the default fund. The contribution of member is then given as

| (18) |

The current practice based on the ratio of initial margins (16) provides an allocation that only depends on the marginal risk of each member profit and loss , and does not take their joint dependence into account, that is, the systemic risk component. By contrast, the approach (18) allows one to take this systemic risk component into account in the allocation of the default fund in the sense of the following proposition already discussed in Section 4.

6.1 Data

In this section we compare a standard IM based allocation of the default fund of a CCP with the multivariate shortfall risk allocation resulting from the use of the loss functions and . This empirical study is based on an LCH real dataset corresponding to the clearing of 74 portfolios of equity derivatives bearing on 90 underlyings. The clearing members have been anonymized and are referenced in the sequel by labels starting by PB plus number (e.g. PB7), whereas the underlying assets are identified by their real tickers, such as FCE for CAC40 index future and AEX for Amsterdam exchange index, which can all be retrieved online. The Jupyter notebook corresponding to this empirical study, including all the data and numerical codes, is publically available at https://github.com/yarmenti/MSRA. In order to avoid the repricing of the options, all the derivative positions have been linearized and reformulated in equivalent Delta positions in their underlyings. We denote by the matrix of the positions of the 74 clearing members in the underlyings. As the CCP clears, each column of sums up to zero. The vector of the clearing member losses at a three day (3d) horizon is given by

| (19) |

where is the vector of the underlying price processes. The vector is observed and the vector is simulated in a Student’s t model estimated by maximum-likelihood on the underlying return time series, i.e.

| (20) |

where is a Student’s t random variable with degrees of freedom and where a calibration fudge coefficient. The dependence between the underlyings is modeled by a Student’s t copula with correlation matrix and degrees of freedom, that is

Here is the cumulative distribution function of the multivariate Student’s t distribution with correlation matrix and degrees of freedom, and is the Student’s t cdf with degrees of freedom.

6.2 Simulations

The correlation matrix is estimated empirically on the return time series and the dependence copula parameter is set to . Each of realizations of , hence of the loss vector , is simulated as follows:

-

1.

Simulate a Gaussian random vector of size 90 with zero-mean and correlation

-

2.

Generate a random variable with parameter

-

3.

Obtain the Student’s t vector

-

4.

Transform into uniform coordinates by and compute

- 5.

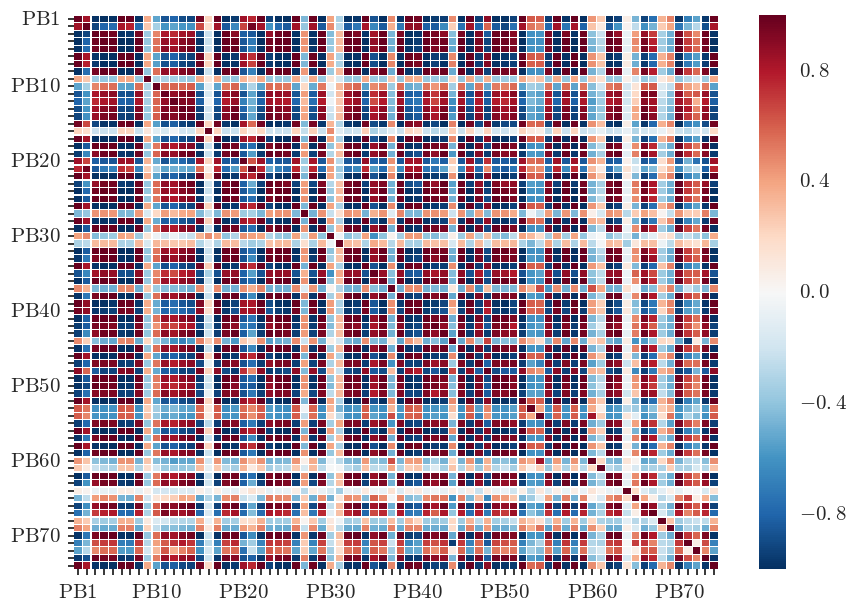

The resulting inputs to the allocation optimization problem are analysed in Appendix C. Figure 5 shows the correlation matrices of the underlying assets and of the loss vector of the clearing members, in a heatmap representation. In the left panel, which is directly estimated from the data, we see that the underlying assets are all positively correlated, as commonly found in the case of equity derivatives. However, due to positions in opposite directions taken by the clearing members, some of their losses exhibit significant negative correlations, as shown by the blue cells in the right panel.

6.3 Allocation Results

The total size of the default fund as of a standard Cover 2 methodology are shown in Table 3, for three values of the dependence copula parameter and for 99% vs. 99.7% initial margins (IM). Since a Cover 2 default fund is a cushion over IM, its size is directly responsive to the level of the quantile which is used for setting the IM (compare the two lines in Table 3). In relative terms the size of the default fund is quite stable with respect to . However we emphasize that these are monetary amounts, so that the difference between for instance 6.16 and 6.72 corresponds to 0.56 , i.e. more than half a billion of the corresponding currency.

| 99 % IM | 6.16 | 6.72 | 6.27 | |

|---|---|---|---|---|

| 99.7 % IM | 4.96 | 5.48 | 5.00 |

In the sequel we set which corresponds to an intermediate level of tail dependence, and we use 99% IM, which corresponds to the EMIR regulatory floor on initial margins.

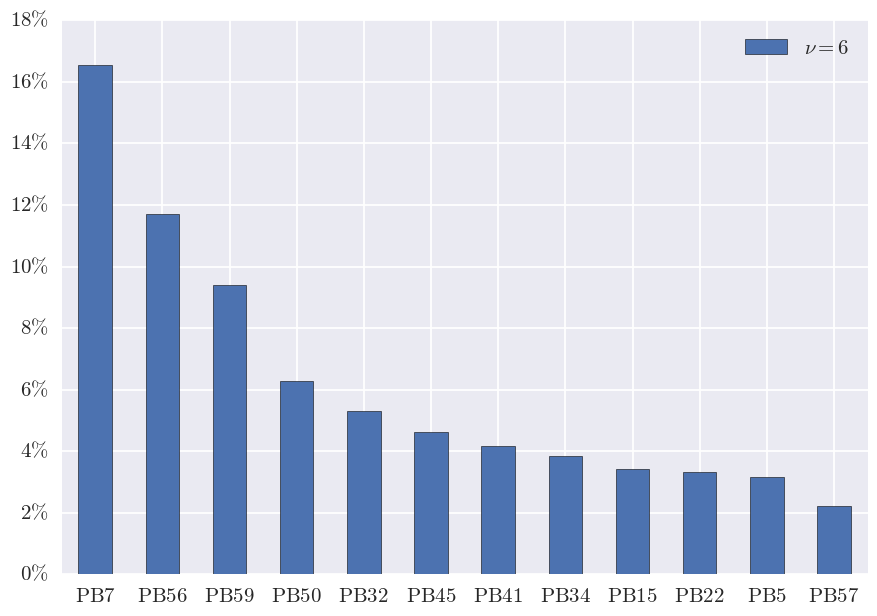

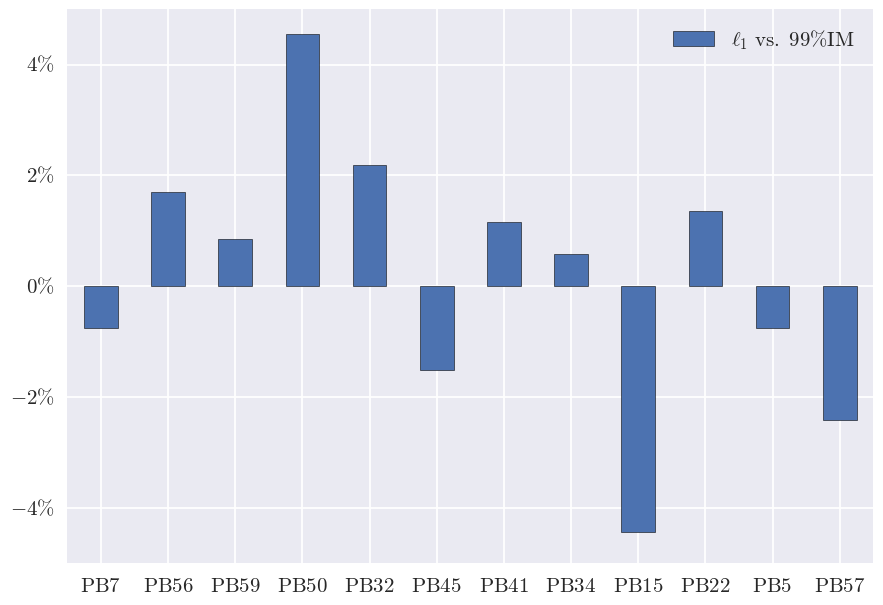

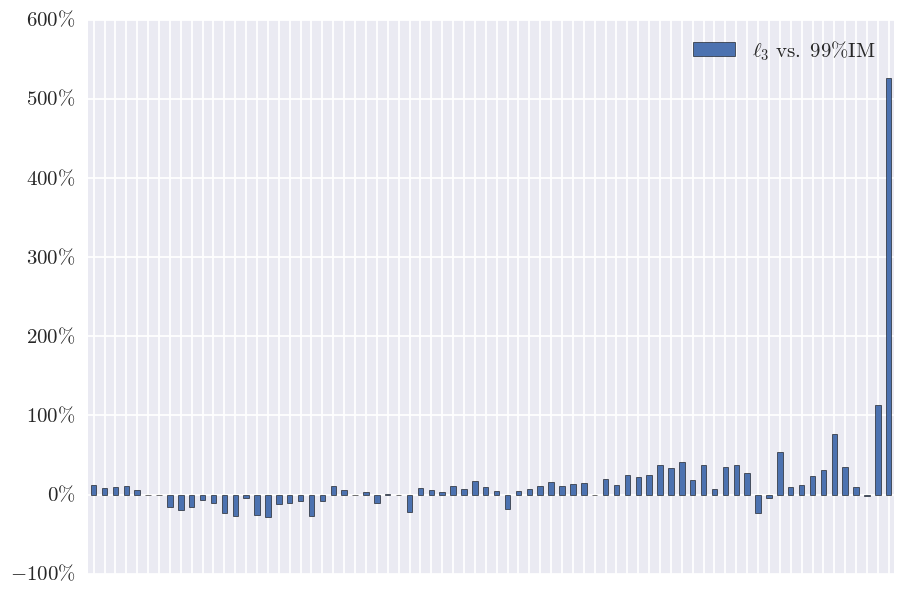

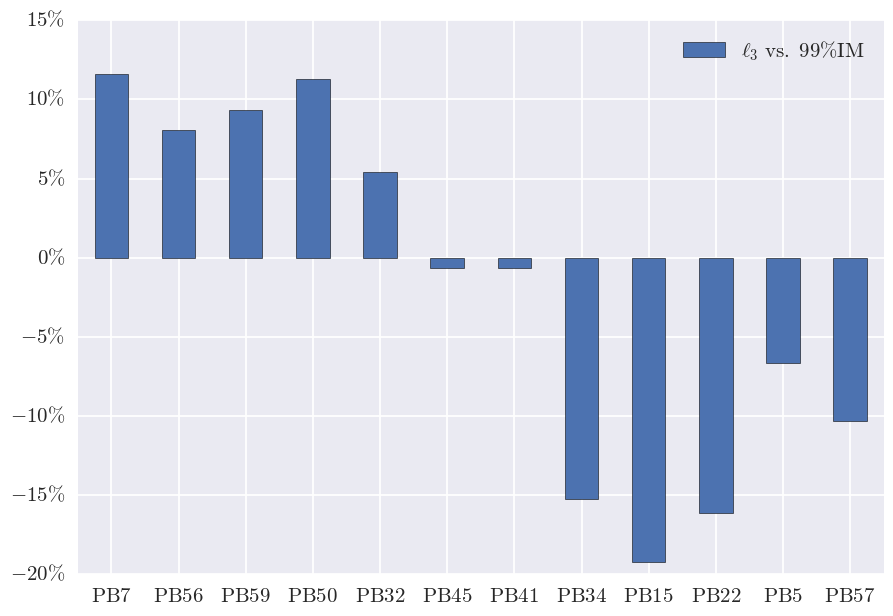

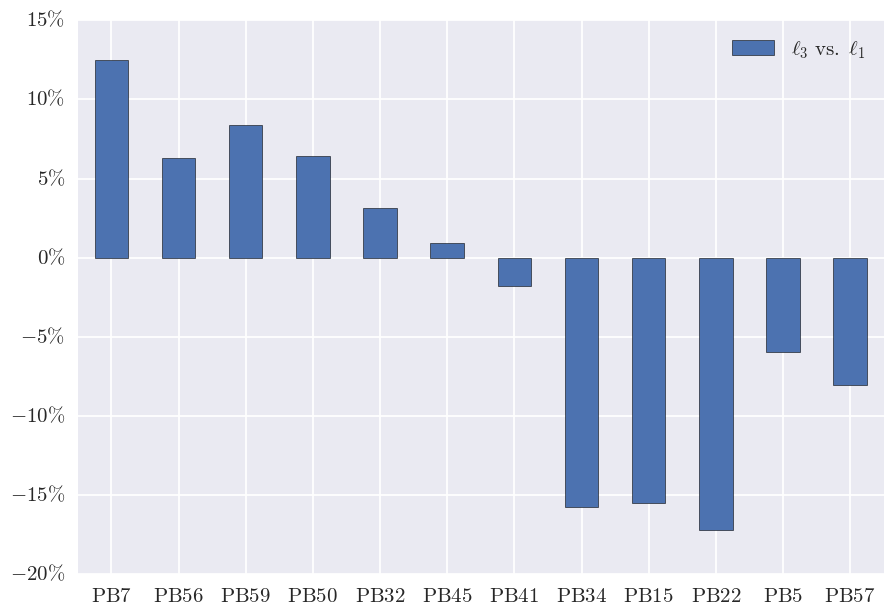

Figure 6 compares the allocation weights implied by the loss function with the ones implied by 99% IM. The allocations are very similar, as confirmed by the examination of the percentage relative differences displayed in the upper panels of Figure 6. By contrast, the lower panels of Figure 7 show that the allocation weights implied by the loss function and the dependence sensitive loss function differ significantly in relative terms, including for the names with the greatest contributions to the default fund. These results illustrate the impact of the use of a “systemic” loss function on the allocation of the default fund.

Acknowledgements

This paper greatly benefited from regular exchanges with the quantitative research team of LCH in Paris: Quentin Archer, Julien Dosseur, Pierre Mouy and Mohamed Selmi. In particular we are grateful to Pierre Mouy for the preparation of the real dataset used for the empirical study of Section 6.

Appendix A Some Classical Facts in Convex Optimization

For an extended real valued function on a locally convex topological vector space , its convex conjugate is defined as

where is the topological dual of . The Fenchel–Moreau theorem states that if is lower semi-continuous, convex and proper, then so is , and it holds

Following Rockafellar [42], for any non-empty set we define its recession cone

By [42, Theorem 8.3], if is non-empty, closed and convex, then

| (21) |

By [42, Theorem 8.4], a non-empty, closed and convex set is compact if and only if .

Given a proper, convex and lower semi-continuous function on , we call a direction of recession of if there exists such that the map is decreasing on . We denote by the recession function of , that is, the function with epigraph given as the recession cone of the epigraph of , and we call

the recession cone of . The following theorem gathers results from [42, Theorems 8.5, 8.6, 8.7 and Corollaries pp. 66–70].

Theorem A.1.

Let be a proper, closed and convex function on .

-

1.

Given in , if then is decreasing.

-

2.

All the non-empty level sets of have the same recession cone, namely the recession cone of . That is:

-

3.

is a positively homogeneous, proper, closed and convex function, such that

for every .

-

4.

There exists such that the map is decreasing on , that is, is a direction of recession of , if and only if this map is decreasing for every which in turn is equivalent to .

-

5.

The map is constant on for every if and only if and .

Appendix B Multivariate Orlicz Spaces

In this appendix we briefly sketch how the classical theory of univariate Orlicz spaces carries over to the -variate case without any significant change. We follow the lecture notes by Léonard [40], only providing the proofs that differ structurally from the univariate case.

A function is called a Young function if it is

-

•

convex and lower semi-continuous;

-

•

such that and ;

-

•

non trivial, that is, contains a neighborhood of and for some .

In particular, achieves its minimum at and is increasing on . It is said to be finite if and strict if .

Lemma B.1.

The function is Young if and only if is Young. Furthermore, is strict if and only if is strict if and only if and are both finite.

Proof B.2.

This follows by application of the Fenchel-Moreau theorem and from the relation .

For , the Luxembourg norm of is given as

where . The Orlicz space and heart are respectively defined as

Lemma B.3.

-

1.

We have if and only if .

-

2.

If , then . In particular, .

-

3.

The gauge is a norm both on the Orlicz space and on the Orlicz heart .

-

4.

The following Hölder Inequality holds:

-

5.

is continuously embedded into , the space of integrable random variables on for the product measure 777The case where corresponds to

-

6.

The normed spaces and are Banach spaces.

Proof B.4.

These results can be established along the same lines as in the univariate case [See 40, Lemmas 1.8 and 1.10 and Propositions 1.11, 1.14, 1.15 and 1.18], using the Fenchel-Moreau Theorem in .

Theorem B.5.

If is finite, then the topological dual of is .

Proof B.6.

Again, the proof follows the univariate case [see 40, Proposition 1.20, Theorem 2.2 and Lemmas 2.4 and 2.5].

Appendix C Data Analysis

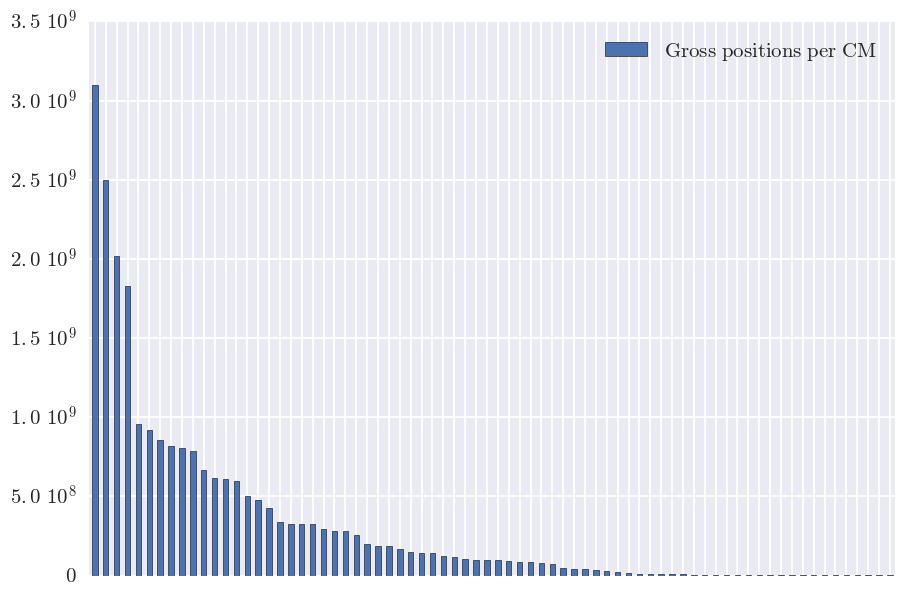

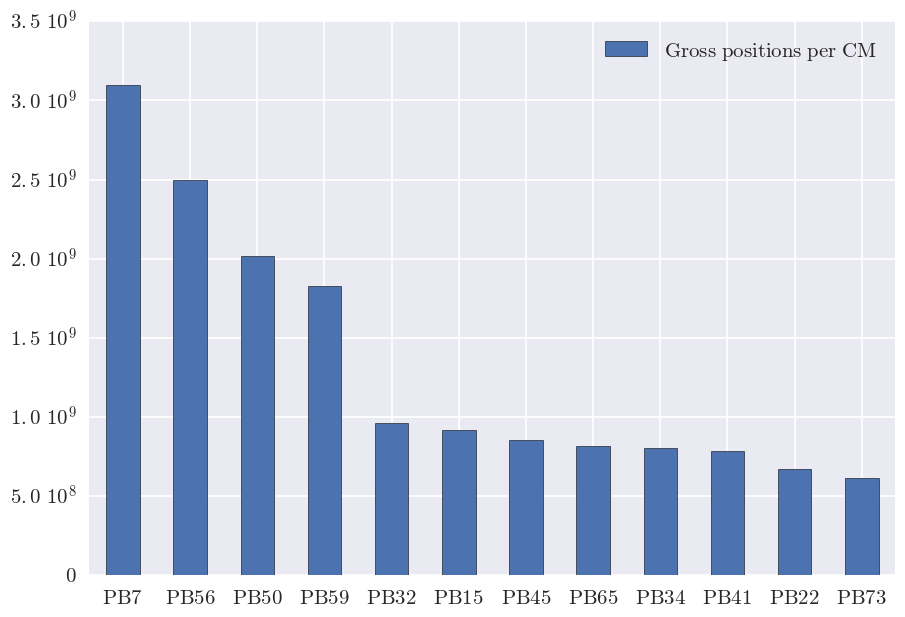

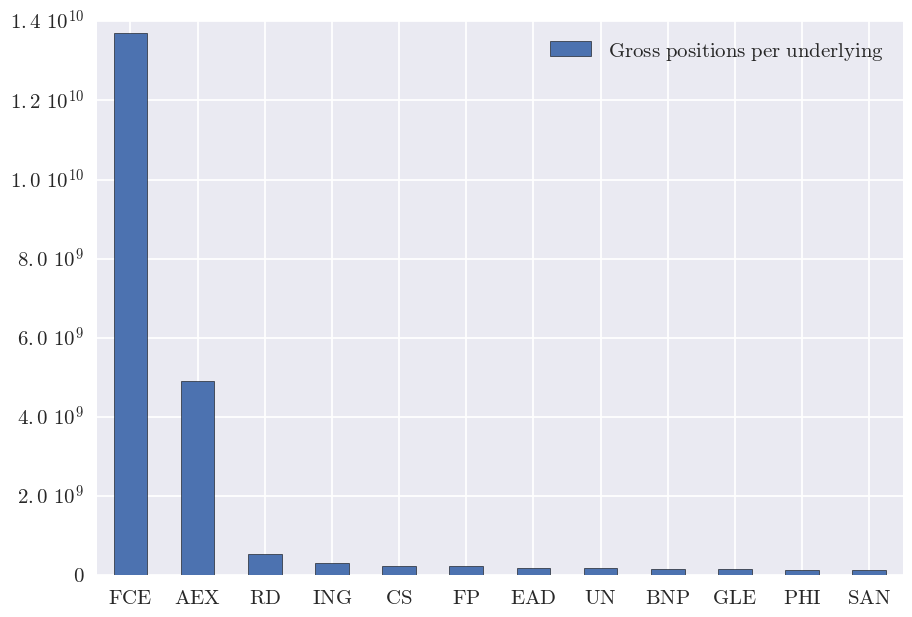

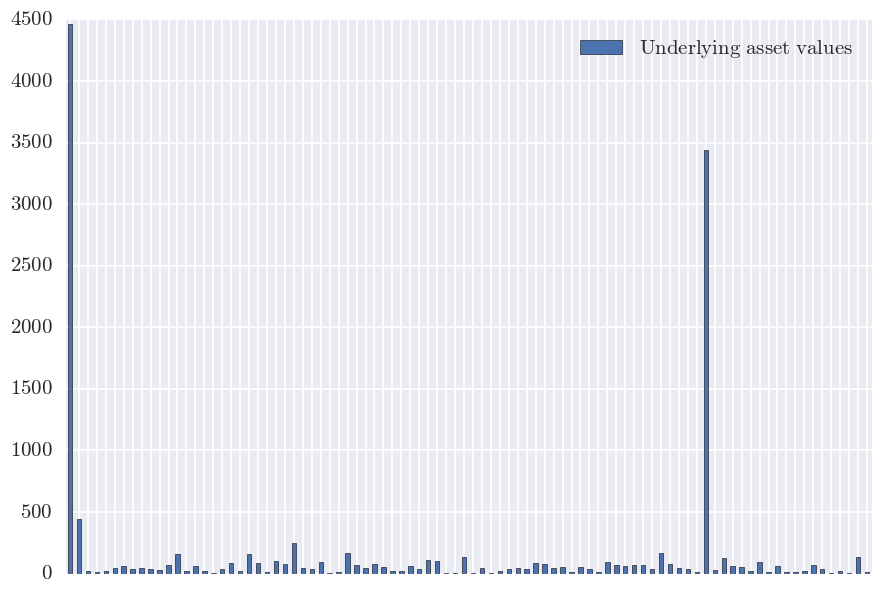

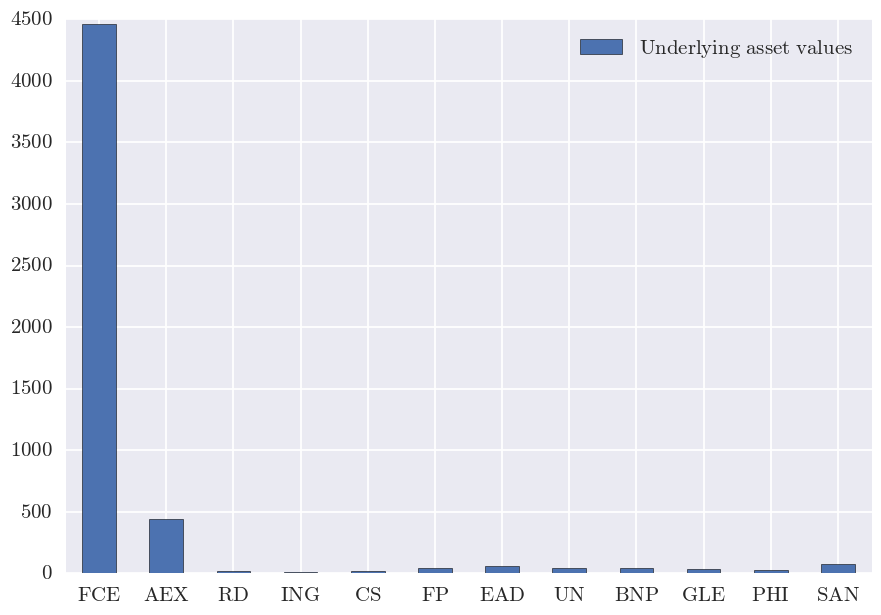

Figure 8 shows the gross positions (sum of the absolute values of the positions in the underlying asset) per clearing member. Four members concentrate particularly high positions in the CCP. Figure 9 shows the gross positions of the CCP per underlying asset (top) and the corresponding underlying asset values (bottom). The largest investment by far of the clearing members is in the asset with ticker FCE (CAC40 index future, with spot value 4463), by a factor about three to the second one AEX (Amsterdam exchange index, with spot value 443.83). The investments of the clearing members in the other assets are comparatively much smaller.

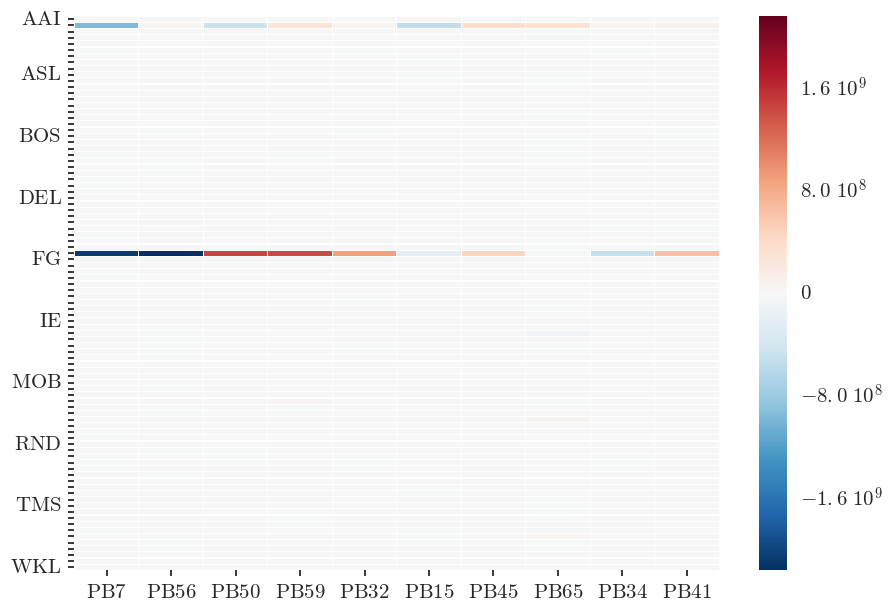

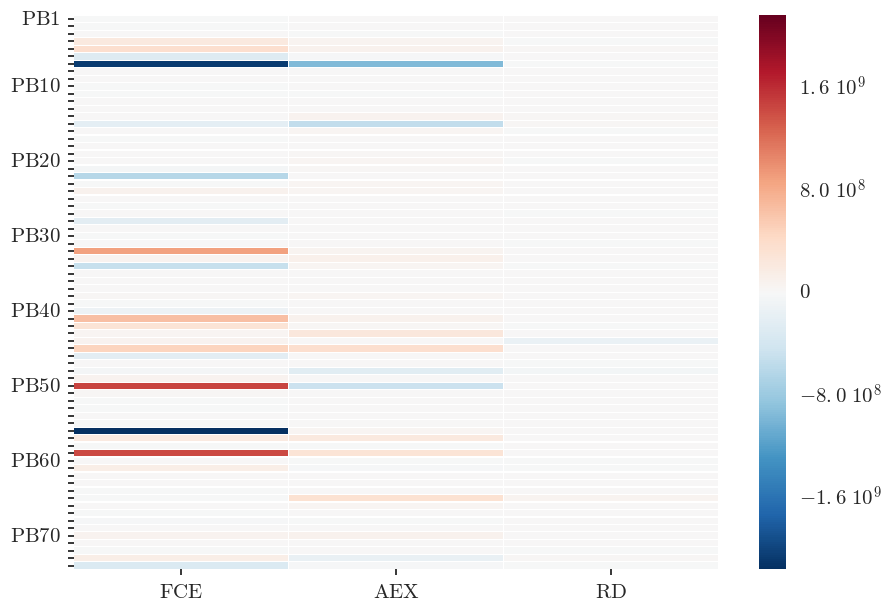

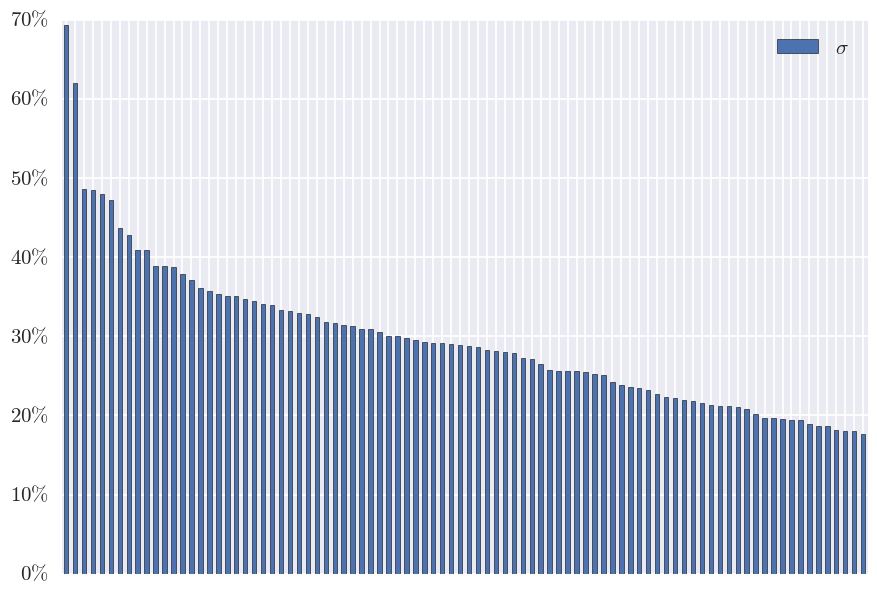

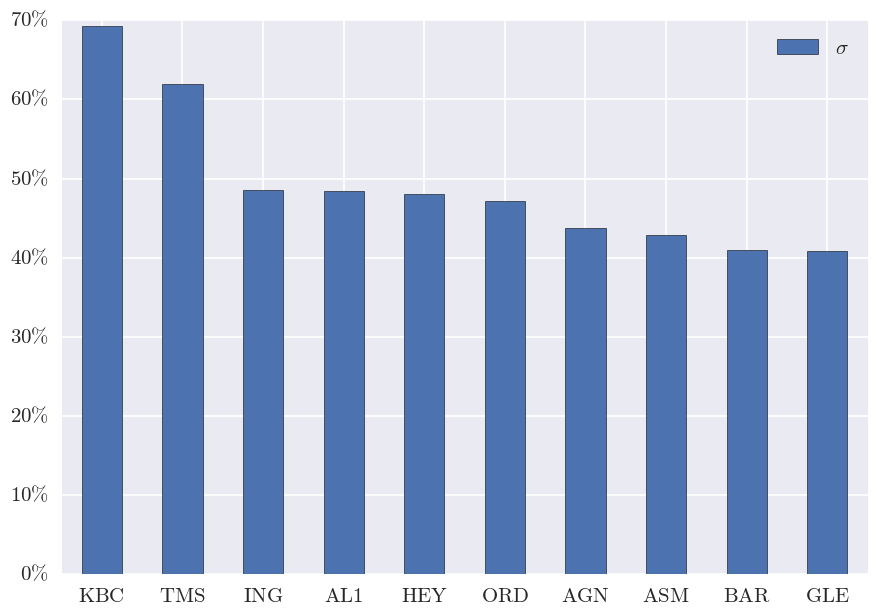

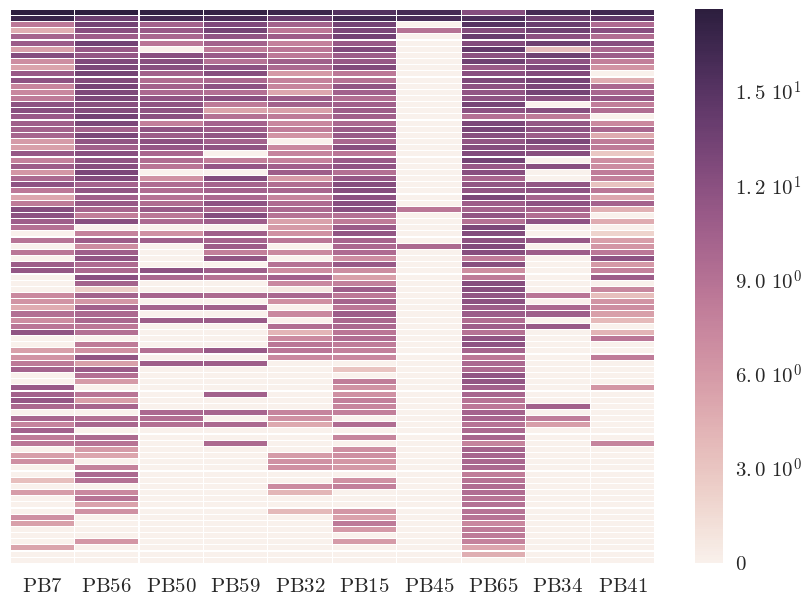

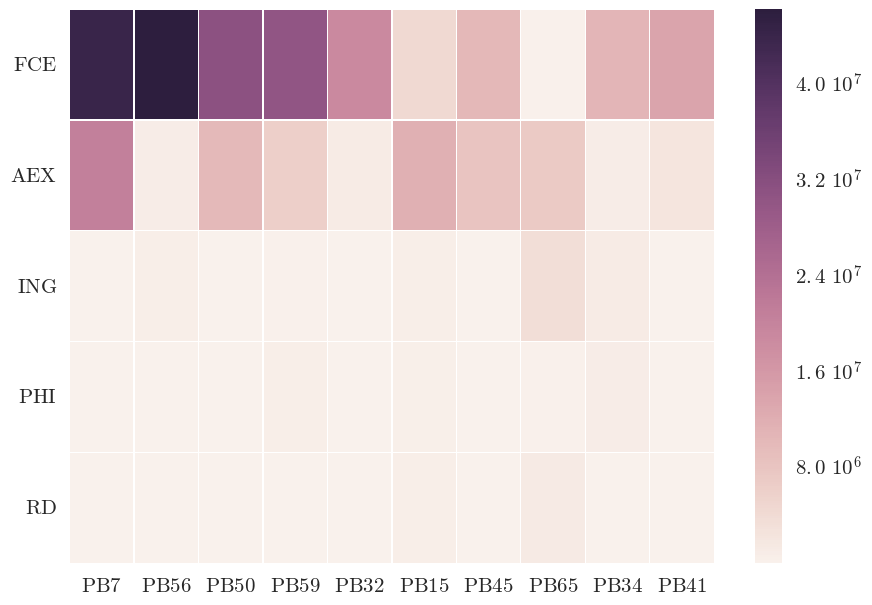

Figure 10 shows the signed positions in the underlying assets of the twelve clearing members with the largest gross positions (left) and the signed positions of the clearing members in the nine most traded underlying assets (right), in a heatmap representation. In particular, we observe from the left panel that the biggest players in the CCP, namely the members labeled PB7, PB56, PB59 and PB50, have opposite sign positions in the main asset (the one with ticker FCE). The right panel shows that the dominant asset position in the CCP, i.e. the one in FCE, is shared (with opposite signs) between a significant number of clearing members. Figure 11 shows the annualized volatilities of the underlying assets (cf. (20)). Most of these volatilities are comprised between 15% and 40%, with two assets, KBC and TMS, spiking over 60% volatility. However, the clearing members are only very marginally invested in these two assets (their tickers do not even appear in the right panel of Figure 9). Figure 12 shows the monetary risks (3d volatilities absolute monetary positions) in the underlying assets of the ten clearing members with the largest gross positions. From the right panel we see that the FCE and AEX assets (CAC40 index future FCE and Amsterdam exchange index AEX, two major indices) concentrate most of the risk of the clearing members. The comparison with Figure 11 shows that this is not an effect of the volatility of these assets, but of very large monetary positions of the clearing members.

References

- Acharya et al. [2010] V. Acharya, T. P. L. Pedersen, and M. Richardson. Measuring systemic risk. SSRN: 1573171, 2010.

- Acharya et al. [2012] V. Acharya, R. Engle, and M. Richardson. Capital shortfall: A new approach to ranking and regulating systemic risks. American Economic Review: Papers & Proceedings, 102(3):59–64, 2012.

- Adrian and Brunnermeier [2011] T. Adrian and M. Brunnermeier. CoVaR. National Bureau of Economic Research Working Paper, 1745, 2011.

- Ararat et al. [2014] Ç. Ararat, A. H. Hamel, and B. Rudloff. Set-valued shortfall and divergence risk measures. ArXiV:1405.4905, 2014.

- Armenti and Crépey [2017] Y. Armenti and S. Crépey. Central clearing valuation adjustment. SIAM Journal on Financial Mathematics, 2017. Forthcoming.

- Artzner et al. [1999] P. Artzner, F. Delbaen, J. M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9:203–228, 1999.

- Awiszus and Weber [2016] K. Awiszus and S. Weber. The joint impact of bankruptcy costs, fire sales and cross-holdings on systemic risk in financial networks. Preprint, 2016.

- Bellini and Bignozzi [2015] F. Bellini and V. Bignozzi. Elicitable risk measures. Quantitative Finance, 15(5):725–733, 2015.

- Ben-Tal and Teboulle [2007] A. Ben-Tal and M. Teboulle. An old-new concept of convex risk measures: the optimized certainty equivalent. Mathematical Finance, 17(3):449–476, 2007.

- Biagini et al. [2015] F. Biagini, J.-P. Fouque, M. Frittelli, and T. Meyer-Brandis. A unified approach to systemic risk measures via acceptance sets. ArXiV:1503.06354, 2015.

- Biagini and Frittelli [2008] S. Biagini and M. Frittelli. A unified framework for utility maximization problems: An orlicz space approach. The Annals of Applied Probability, 18(3):929–966, 06 2008.

- Biagini and Frittelli [2010] S. Biagini and M. Frittelli. On the Extension of the Namioka-Klee Theorem and on the Fatou Property for Risk Measures, pages 1–28. Springer Berlin Heidelberg, Berlin, Heidelberg, 2010.

- Brownlees and Engle [2012] C. Brownlees and R. Engle. Volatility, correlation and tails for systemic risk measurement. SSRN: 1611229, 2012.

- Brunnemeier and Cheridito [2014] M. K. Brunnemeier and P. Cheridito. Measuring and allocating systemic risk. SSRN: 2372472, 2014.

- Cascos and Molchanov [2014] I. Cascos and I. Molchanov. Multivariate risk measures: a constructive approach based on selections. Mathematical Finance, 2014. Forthcoming.

- Chen et al. [2013] C. Chen, I. Garud, and M. Ciamac C. An axiomatic approach to systemic risk. Management Science, 59(6):1373–1388, 2013.

- Cheridito and Kromer [2013] P. Cheridito and E. Kromer. Reward-risk ratios. Journal of Investment Strategies, 3(1):1–16, 2013.

- Cheridito and Li [2009] P. Cheridito and T. Li. Risk measures on Orlicz hearts. Mathematical Finance, 19(2):189–214, 2009.

- Cont [2015] R. Cont. The end of the waterfall: Default resources of central counterparties. Journal of Risk Management in Financial Institutions, 8(4), 2015.

- Cont et al. [2013] R. Cont, E. Santos, and A. Moussa. Network structure and systemic risk in banking systems. In J.-P. Fouque and J. Langsam, editors, Handbook of Systemic Risk. Cambridge University Press, 2013.

- Delbaen [2002] F. Delbaen. Coherent Risk Measures on General Probability Spaces, pages 1–37. Springer Berlin Heidelberg, Berlin, Heidelberg, 2002.

- Drapeau and Kupper [2013] S. Drapeau and M. Kupper. Risk preferences and their robust representation. Mathematics of Operations Research, 28(1):28–62, 2013.

- Drapeau et al. [2014] S. Drapeau, M. Kupper, and A. Papapantoleon. A Fourier approach to the computation of CV@R and optimized certainty equivalents. Journal of Risk, 16(6):3–29, 2014.

- Eberlein et al. [2010] E. Eberlein, K. Glau, and A. Papapantoleon. Analysis of Fourier transform valuation formulas and applications. Applied Mathematical Finance, 17:211–240, 2010.

- Eisenberg and Noe [2001] L. Eisenberg and T. H. Noe. Systemic risk in financial systems. Management Science, 47(2):236–249, 2001.

- European Parliament [2012] European Parliament. Regulation (EU) no 648/2012 of the European parliament and of the council of 4 july 2012 on OTC derivatives, central counterparties and trade repositories. Official Journal of the European Union, 2012.

- Farkas and Koch-Medina [2015] W. Farkas and P. Koch-Medina. Measuring risk with multiple eligible assets. Mathematics and Financial Economics, 9(1):3–27, 2015.

- Feinstein et al. [2015] Z. Feinstein, B. Rudlof, and S. Weber. Measures of systemic risk. ArXiV:1502.07961, 2015.

- Fiacco and McCormick [1990] A. Fiacco and G. McCormick. Nonlinear Programming: Sequential Unconstrained Minimization Techniques. Classics in Applied Mathematics. Society for Industrial and Applied Mathematics, 1990. ISBN 9780898712544.

- Fissler and Ziegel [2015] T. Fissler and J. F. Ziegel. Higher order elicitability and osband’s principle. ArXiV:1503.08123, Mar. 2015.

- Föllmer and Schied [2002] H. Föllmer and A. Schied. Convex measures of risk and trading constraint. Finance and Stochastics, 6(4):429–447, 2002.

- Frittelli and Rosazza Gianin [2002] M. Frittelli and E. Rosazza Gianin. Putting order in risk measures. Journal of Banking & Finance, 26(7):1473–1486, July 2002.

- Gaß et al. [2015] M. Gaß, K. Glau, M. Mahlstedt, and M. Mair. Chebyshev interpolation for parametric option pricing. ArXiV:1505.04648, 2015.

- Ghamami and Glasserman [2016] S. Ghamami and P. Glasserman. Does OTC derivatives reform incentivize central clearing? Technical report, Office of Financial Research, 2016.

- Glasserman et al. [2016] P. Glasserman, C. C. Moallemi, and K. Yuan. Hidden illiquidity with multiple central counterparties. Operations Research, 64(5):1143–1158, 2016.

- Hamel et al. [2011] A. Hamel, F. Heyde, and B. Rudloff. Set-valued risk measures for conical market models. Mathematics and Financial Economics, 5(1):1–28, 2011.

- Jouini et al. [2004] E. Jouini, M. Meddeb, and N. Touzi. Vector-valued coherent risk measures. Finance and Stochastics, 8:531–552, 2004.

- Krätschmer et al. [2014] V. Krätschmer, A. Schied, and H. Zähle. Comparative and qualitative robustness for law-invariant risk measures. Finance and Stochastics, 18:271–295, 2014.

- Kromer et al. [2016] E. Kromer, L. Overbeck, and K. Zilch. Systemic risk measures on general measurable spaces. Mathematical Methods of Operations Research, 84(2):323–357, 2016.

- Léonard [2007] C. Léonard. Some notes on Orlicz spaces. 2007. URL http://www.cmap.polytechnique.fr/~leonard/papers/orlicz.pdf.

- Osband [1985] K. H. Osband. Providing incentives for better cost forecasting. PhD thesis, University California, Berkeley, 1985.

- Rockafellar [1970] R. T. Rockafellar. Convex Analysis. Princeton Mathematical Series, No. 28. Princeton University Press, Princeton, N.J., 1970.

- Rockafellar and Wets [2009] R. T. Rockafellar and R. J.-B. Wets. Variational Analysis. Springer, Berlin, New York, 3rd edition, 2009.

- Rüschendorf [2004] L. Rüschendorf. Comparison of multivariate risks and positive dependence. Journal of Applied Probability, 41(2):391–406, 2004.

- Rüschendorf [2006] L. Rüschendorf. Law invariant convex risk measures for portfolio vectors. Statistics & Decisions, 24:97–108, 2006.

- Tasche [2008] D. Tasche. Pillar II in the New Basel Accord: The Challenge of Economic Capital, chapter Capital allocation to business units and sub-portfolios: the Euler principle, pages 423–453. Risk Books, 2008.

- Weber [2006] S. Weber. Distribution-invariant risk measures, information and dynamic consistency. Mathematical Finance, 16(2):419–441, 2006.

- Ziegel [2014] J. F. Ziegel. Coherence and elicitability. Mathematical Finance, pages n/a–n/a, 2014. ISSN 1467–9965.