The Spectral Norm of Random Inner-Product Kernel Matrices

Abstract.

We study an “inner-product kernel” random matrix model, whose empirical spectral distribution was shown by Xiuyuan Cheng and Amit Singer to converge to a deterministic measure in the large and limit. We provide an interpretation of this limit measure as the additive free convolution of a semicircle law and a Marcenko-Pastur law. By comparing the tracial moments of this random matrix to those of a deformed GUE matrix with the same limiting spectrum, we establish that for odd kernel functions, the spectral norm of this matrix convergences almost surely to the edge of the limiting spectrum. Our study is motivated by the analysis of a covariance thresholding procedure for the statistical detection and estimation of sparse principal components, and our results characterize the limit of the largest eigenvalue of the thresholded sample covariance matrix in the null setting.

1. Introduction

Let be a random matrix with independent entries of mean 0 and variance 1, and let be the sample covariance. Define a matrix entrywise as

| (1) |

where is a (nonlinear) “kernel” function. In this paper, we study the spectral norm in the asymptotic regime such that , when is a fixed function independent of and .

Our study of this model is motivated by the analysis of a covariance thresholding procedure proposed in [36] and subsequently analyzed in [22] for the sparse PCA problem in statistics. In the simplest setting, this problem may be formulated as follows:

1.1. Sparse PCA

Consider a data matrix with independent columns distributed as , where is a covariance matrix of the “spiked model” form

| (2) |

with a constant and a vector of unit Euclidean norm. Assume further that where denotes the number of nonzero entries of , and (for simplicity of discussion) that each such nonzero entry equals . Based on observing , we would like to detect the spike (i.e. distinguish this from the null model ) and to recover the support of [1, 5].

As with , in the “supercritical” regime where , the largest eigenvalue separates from the bulk, and the corresponding eigenvector partially aligns with . Consequently, consistent spike detection and support recovery may be performed using and [36]. However, in the “subcritical” regime , almost surely, cannot distinguish the null and spiked models, and furthermore no test using only the eigenvalues of can distinguish the models with probability approaching one [32, 3, 4, 44, 42, 43]. In this regime, [36] proposed to exploit the sparsity of by applying a thresholding operation entrywise to to yield a matrix , and then performing a spectral decomposition of . Here, is a constant and is a threshold function satisfying as and for , so that entries of of magnitude less than are set to 0 while large entries are essentially preserved. (The matrix in (1) when is precisely with diagonal set to 0.)

The choice of threshold level is motivated by the following consideration: For , it is in fact conjectured that no polynomial-time algorithm can consistently detect the spike or recover the support of if , for any [6, 36]. Hence it is believed that the most difficult setting which permits a computationally tractable solution to these problems is when . In this setting, both the non-zero off-diagonal entries of (the “signal”) and the fluctuations of the entries of (the “noise”) are of order , so the threshold must also be of order to preserve the signal while reducing the noise.

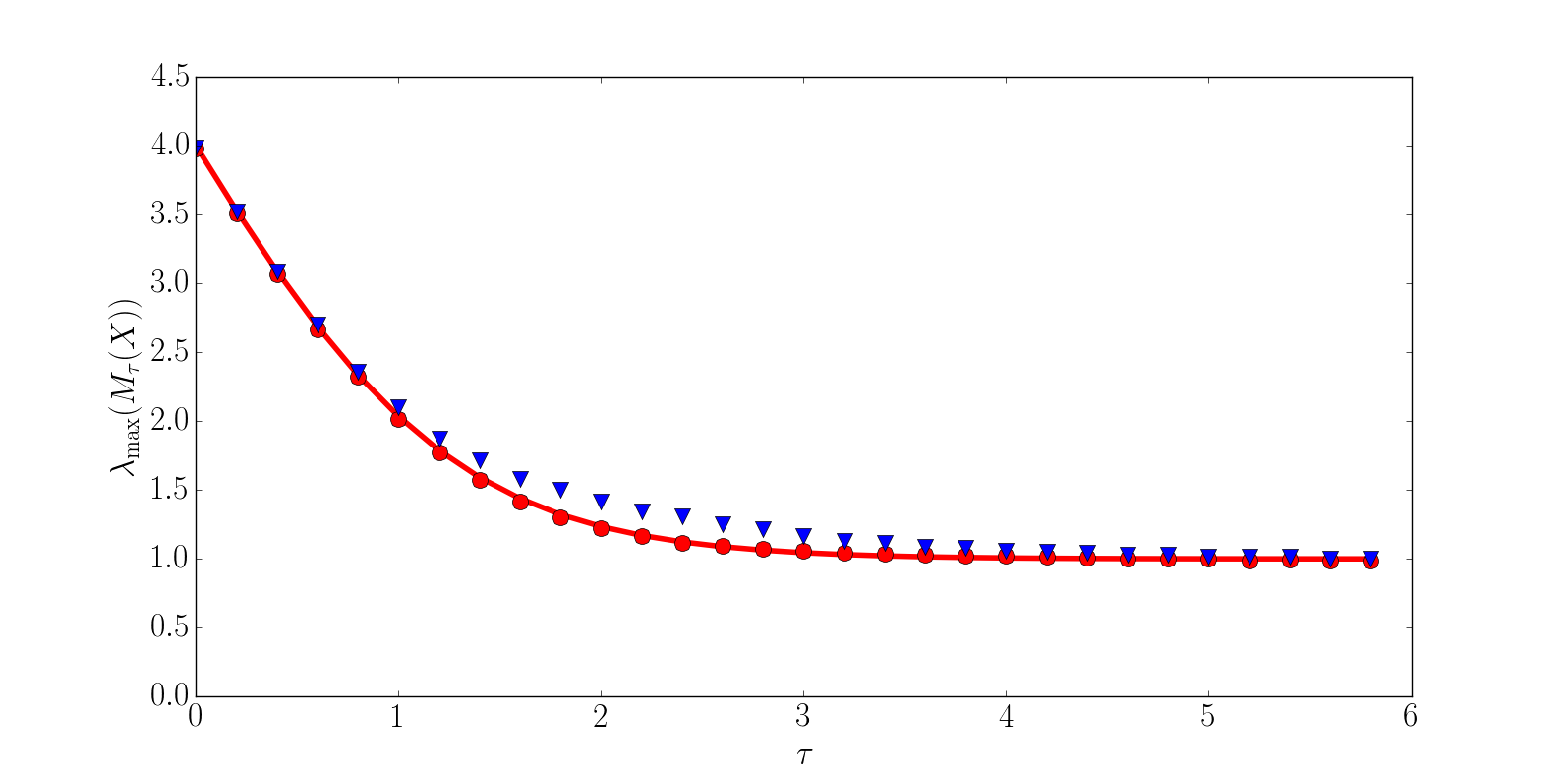

In [22], it was shown that for any , spike detection and support recovery based on and the corresponding eigenvector can succeed with probability approaching 1 when , for some constants and . This phenomenon is illustrated in Figure 1, which shows that for a range of thresholds , there is a difference between the values of under the null model and under a spiked alternative with and sparsity . The main result of this paper strengthens the non-asymptotic analysis in [22] under the null model to establish an exact asymptotic value for in terms of . Procedurally, this indicates the point above which this method should reject the null model in favor of a spiked alternative. We are not aware of a similar analytic characterization of the value of under the alternative model; such a characterization may yield insight on the exact critical sparsity level and optimal choices of and for spike detection using this method to succeed.

In the null model of this example, since all diagonal entries of concentrate around 1 and thresholding essentially preserves the diagonal, the thresholded sample covariance satisfies , where is as in (1) for . Hence the largest eigenvalue limit of is simply that of translated by 1. For odd and increasing threshold functions, the condition of Corollary 1.5 below is satisfied, so the largest eigenvalue of equals its spectral norm.

1.2. Properties of the limit measure

For the model (1), the weak limit of the empirical spectral measure of was characterized by Cheng and Singer [20, Theorem 3.4 and Remark 3.2]. We restate this result in the following form:

Theorem 1.1 (Cheng, Singer).

Let have entries . For , suppose , , and as where and are the density functions of the laws of and . Then, denoting and , as with ,

weakly almost surely, where is a deterministic measure whose Stieltjes transform is the unique solution (in , for any ) to the equation

| (3) |

This result was generalized by Do and Vu to the setting of non-Gaussian entries in [23].

Before stating our main results, let us discuss some basic properties of this limit measure: For a linear kernel function , is a translation and rescaling of the Marcenko-Pastur law. Interestingly, it was observed in [20] that for kernel functions for which , is a Wigner semicircle law. In fact, the measure in general is the additive free convolution (in the sense of Voiculescu [57]) of these two laws.

Proposition 1.2.

Let be the semicircle law supported on and let denote the law of for . Let be the standard Marcenko-Pastur law that is the limiting spectral measure of when and , and let denote the law of for . Then

Proof.

Recalling that the additive free convolution of semicircle laws is itself a semicircle law, Proposition 1.2 implies the following further decomposition of : Let denote any orthonormal basis of functions with respect to the inner product when , where and . Consider the corresponding orthogonal decomposition of the kernel function

(where because ), and the decomposition

where is the matrix (1) with kernel function . Letting denote the limiting spectral measure of , which is for and for , the limiting spectral measure of is given by

| (5) |

In the proof of our main result, we will apply such a decomposition of the kernel matrix when each is the degree- Hermite polynomial.

Proposition 1.2 implies, via the general analysis of [7], that is compactly supported, has one interval of support when and at most two intervals of support when , and (except for the singularity at 0 in the Marcenko-Pastur case and ) admits a density on all of that is analytic in the interior of the support. The following may also be deduced from the -transform:

Proposition 1.3.

Let denote the support of . If , then

and if , then

Proof.

Replacing by , it suffices to consider . The -transform (4) admits the series expansion

around , implying that the free cumulants of are given by , , and for [51]. The moments of are then

where denotes the set of all non-crossing partitions of [51]. In particular, when , all moments of are non-negative, whereas if , then the moment must be negative for a sufficiently large odd integer . ∎

1.3. Main results

Denoting , the following is the main result of this paper:

Theorem 1.4.

Suppose is odd (i.e. ) and continuously differentiable, with for some constants and all . Let have entries . Then with as defined in Theorem 1.1, almost surely as with ,

Proposition 1.3 yields the following corollary:

Corollary 1.5.

Under the conditions of Theorem 1.4, if , then almost surely

(It may be verified, cf. our proof of the above corollary in Section 2, that any kernel function satisfying the conditions of Theorem 1.4 also satisfies the conditions of Theorem 1.1.)

We will prove Theorem 1.4 via the following two auxiliary results, the first giving a non-asymptotic concentration bound on that is of constant order when , and the second providing an asymptotically tight bound in the case where is a polynomial function:

Theorem 1.6.

Suppose is odd, continuous, and differentiable almost everywhere with for some and all . Let have entries . Then, for any , there exist constants depending only on , , and such that

Theorem 1.7.

Let be a polynomial function such that when , and let . Let have IID entries that are symmetric in law () and satisfy and

| (6) |

for all and some . Then

where and are such that, as with ,

-

(1)

almost surely, and

-

(2)

if , and otherwise is of rank at most two, with non-zero eigenvalues converging to .

The precise form of the rank-two matrix is given by (9) in Section 2. We make the trivial observation that and if the polynomial is an odd function.

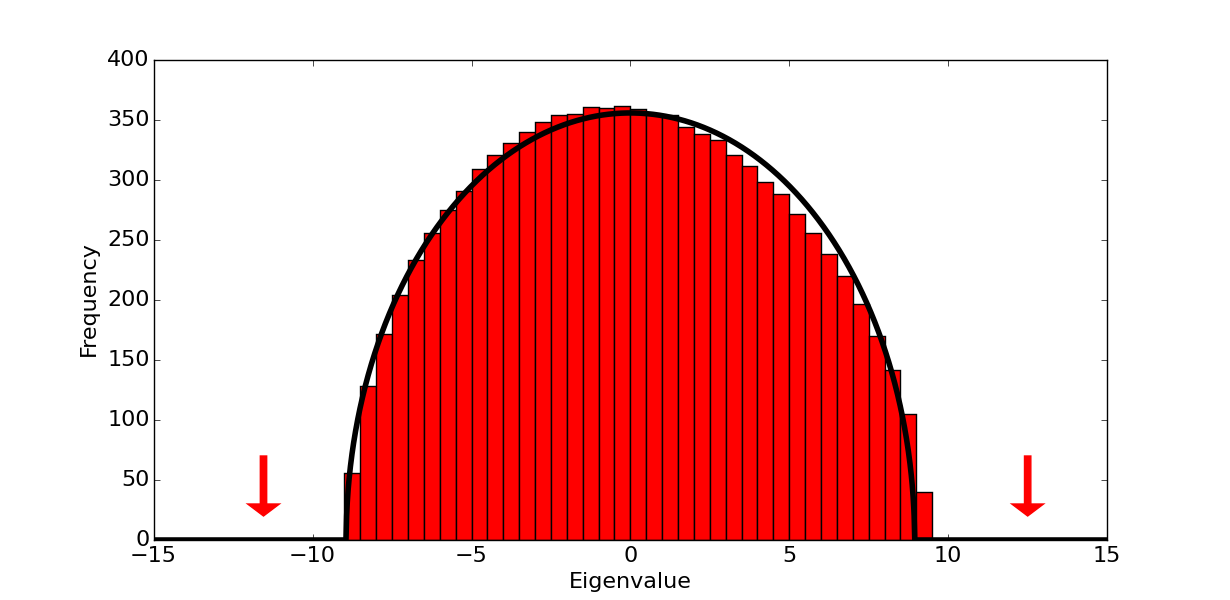

Theorem 1.4 follows from Theorems 1.6 and 1.7 via a polynomial approximation argument, which we present in Section 2. The assumption that is odd, or more specifically that , is important: Figure 2 displays the simulated spectrum of for a kernel function where , in which we see that contributes two spike eigenvalues to that fall outside of . In the covariance thresholding application of Section 1.1, commonly-used threshold functions are indeed odd. We recommend caution if using a non-odd threshold function, as the possible presence of these spurious spike eigenvalues may lead to the incorrect inference that has non-trivial spike eigenvectors, even in this null setting where .

1.4. Further related literature

The off-diagonal entries of are the evaluations of a symmetric kernel on pairs of rows of . Such matrices for general kernels are used in “kernel methods” in statistics and machine learning, such as SVM classifiers [10] and kernel PCA [47]. Koltchinskii and Giné [35] studied the spectra of kernel matrices in a regime where each row of is sampled from a probability distribution over a fixed space (for example for fixed ), showing that under suitable conditions, as , the spectrum converges to that of a limiting infinite-dimensional operator. El Karoui [25] studied kernel matrices in the regime with under the alternative scaling , showing that under mild conditions, the matrix is asymptotically equivalent to a linear combination of , the all-1’s matrix, and the identity, and hence the limiting spectrum is Marcenko-Pastur. The scaling in (1) is different from the regime considered in [25]: Each off-diagonal entry of has typical size , and hence (1) applies the nonlinearity to values of size rather than . This and more general scalings were studied probabilistically in [20], and the results were further generalized in [23]. Let us remark that [35, 25] considered distributions for the rows of where the entries are not necessarily IID, but that the extension of our result to more general covariances for the application of Section 1.1 will require the study of a model in which the columns (rather than the rows) of are independent with this covariance.

Sparse PCA has been widely studied in statistics for both the “single spike” model (2) as well as multi-spike models. Computationally-efficient procedures for estimating sparse principal components include diagonal thresholding [31, 32, 9], - and model-selection-penalization approaches [33, 62, 21, 49, 60, 12], iterative thresholding via the QR method [40], approximate message passing [22], and covariance thresholding as discussed in Section 1.1 [36, 22]. From the theoretical perspective, both exact [1, 36] and approximate [32, 9, 40, 59, 12, 13] sparsity models have been considered, and a major focus has been on rate-optimal recovery of the sparse eigenvectors, their spanned subspace, and/or the sparse covariance [9, 40, 12, 59, 13]. Support recovery and spike detection in the specific model (2) were considered in [1, 5, 6, 36, 22]. In this setting, non-polynomial-time algorithms can detect the spike and recover the support even when has sparsity near-linear in [1, 5, 13], but it is conjectured that polynomial-time methods require the higher sparsity levels . This problem is closely related to the planted clique problem in computer science [5, 6] upon which this conjecture is based, with a vector of sparsity corresponding to a planted clique of size in a graph of vertices.

Consistency of elementwise hard-thresholding for estimating sparse covariance matrices was studied in [8, 24]. Optimal rates of convergence under various matrix norms and sparsity models were established in [15, 14], and generalizations to other thresholding functions and to “adaptive” entry-specific thresholds were studied respectively in [46] and [11]. Many analyses assume that each row of contains non-zero elements and perform thresholding at the level or higher, which does not apply to the regime of interest discussed in Section 1.1 where has sparsity and non-zero elements of size . Thresholding at more general levels, including , was studied in [22], which established a special case of Theorem 1.6 for the soft-thresholding kernel function . The proof of [22] may be extended to globally Lipschitz functions , but we require the application of such a bound when is the difference of the (possibly Lipschitz) kernel function of interest and a polynomial approximation to this function. This difference may increase at any polynomial rate as , hence requiring new ideas in the proof of Theorem 1.6 to extend beyond Lipschitz kernels. Other spectral norm bounds for polynomial kernels were derived in [20] and [34], but they do not yield the desired bound of constant order when restricted to our setting.

In the context of random matrix theory, convergence of the extremal eigenvalues of was posed as an open question in [20]. For linear kernels , is equivalent to a translation and rescaling of the sample covariance , and almost-sure convergence of the extremal eigenvalues follows from [29, 61, 2]. Proposition 1.2 implies that in the general case, has the same limiting spectrum as a deformed Wigner matrix where is Wigner and is deterministic with spectral measure converging to [58]. When is GUE and has no spike eigenvalues, the results of [16, 41] imply that the eigenvalues of stick to the limiting support, and the fluctuations of the eigenvalues at the edges of the support are also understood in various settings [48, 17, 39]. The proof of our main result leverages the connection between these models.

Our proof uses the moment method and is different from the resolvent analysis of [20], although the decomposition of in the Hermite polynomial basis plays an important role in both analyses. While the resolvent method has been successful in establishing many properties of Wigner and covariance matrices (see e.g. [50, 30, 55, 26, 45] as well as the recent work of [52, 19] in a non-independent setting), the model (1) for nonlinear kernels does not have the same independence structure as these models, and it is also not a sum of rank-one updates. These difficulties were overcome in [20] via Gaussian conditioning arguments, but strengthening the bounds of [20] to yield finer control of the Stieltjes transform near the real axis does not seem (in our viewpoint) more straightforward than our moment-based approach. We believe that our combinatorial estimates and moment-comparison argument, in the simpler setting of a fixed moment not varying with , are sufficient to yield an alternative proof of Theorem 1.1 and also to establish asymptotic freeness of the matrices leading to the decomposition (5). For brevity, we will not discuss this in the current paper.

1.5. Notation

denotes the Euclidean norm for vectors. denotes the spectral norm (i.e. -operator norm) for matrices. denotes the row of . If is symmetric, denote the ordered eigenvalues of . denotes the support of a measure , and denotes .

In an asymptotic setting, for positive (-dependent) quantities and , means for constants , means , means , and means for a constant .

We will use for indices in , and for indices in .

2. Overview of proof

In this section, we summarize the high-level proof ideas for Theorems 1.6 and 1.7, and we establish Theorem 1.4 and Corollary 1.5 using these results.

The proof of Theorem 1.6 uses a covering net argument:

for a constant and a finite covering net of the unit ball . We use a particular construction of a covering net due to Latala [37]:

Definition 2.1.

For , let

For each , let be defined by , and let be defined by .

Corresponding to the identity for any , may be decomposed as

| (7) |

Each of the terms

may be bounded via a standard union bound, with quantities of the form controlled by bounding the gradient and applying Gaussian concentration of measure for Lipschitz functions. The key idea of the construction of and the decomposition (7) is that for each , the union bound may be applied over , which has smaller cardinality for smaller . For larger , the entries of are smaller, which we will show implies stronger control of the gradient over a high-probability set . The moment generating function of may be controlled using the integration argument of Maurey and Pisier, by extending this high-probability set to pairs of matrices in such a way that we remain in this set along the entire integration path. The cardinality of balances the moment generating function bound thus obtained for each , yielding Theorem 1.6. Details of this argument are given in Section 3.

The proof of Theorem 1.7 uses the moment method and a moment comparison with a deformed GUE matrix. We first define the orthonormal Hermite polynomials, which play a central role in our proof (as well as in the proof in [20] for Theorem 1.1):

Definition 2.2.

Let denote the orthonormal Hermite polynomials with respect to the inner product when , i.e. is of degree and .

The first few such polynomials are given by , , , and .

Our proof of Theorem 1.7 follows three high-level steps:

-

(1)

For IID random variables with and , we show that

(8) (The summation on the right side is over all tuples of distinct indices .) Each has leading coefficient , so . Replacing with on the left side would yield the right side of (8) without the restriction that the indices of summation are distinct; (8) states that the terms of this summation in which the indices are not distinct are essentially cancelled out by the lower degree terms of . We prove this approximation in Section 4 by induction on , using the three-term recurrence for Hermite polynomials. The right side of (8) is of typical size , and we also quantify the error of the approximation by computing a second-order term, which is of typical size , and showing that the third and higher-order terms in this approximation are of typical size .

-

(2)

Since is a polynomial such that , we may write

where is the degree of . Applying the approximation in step (1) above to each , we obtain a decomposition

where , , and correspond to the first-order, second-order, and third-and-higher-order terms of these approximations (each summed over all ). We establish for the first-order matrix that

almost surely, via a moment comparison argument: For an even integer , we apply the standard moment method bound [28, 29]. By (8), the non-diagonal entries of are given by

We expand the trace and interpret the terms of the resulting sum as labelings of a certain graph. We then consider a deformed GUE matrix having the same limiting spectrum as , and employ a combinatorial argument to upper-bound using . We conclude the proof by using the known convergence result from [16] and a concentration of measure argument to bound . We present the main ideas of this step in Section 5, with details deferred to Appendices A and B.

-

(3)

Finally, we analyze the remainder matrices and from the decomposition in step (2) above. It is easily shown that . For , we may write

where is the contribution from the Hermite polynomial . (The linear polynomial does not have such a remainder term in the decomposition.) We show for each , and where

(9) , and has entries . Noting that is a rank-two matrix, this yields Theorem 1.7 upon setting . This argument and the conclusion of the proof of Theorem 1.7 are presented in Section 6.

Let us now prove Theorem 1.4 and Corollary 1.5 using Theorems 1.6 and 1.7. We approximate the derivative of the kernel function by a polynomial using the following result:

Theorem 2.3 (Carleson [18]).

Suppose is an even, lower semi-continuous function on with , such that is a convex function of . Let be the class of continuous functions on such that for all , and suppose contains all polynomial functions. If , then for any and , there exists a polynomial such that for all .

Proof of Theorem 1.4.

By the given conditions, there exists such that . Applying Theorem 2.3 with , for any , there exists a polynomial such that for all . As is an odd function, is even, so we may take to be an even polynomial function. (Otherwise, take the polynomial to be .) Let for all , and let . Then is an odd polynomial function, is hence also an odd function, and by construction. Let be the kernel matrix (1) with kernel function , and let be the kernel matrix (1) with kernel function , so that . (These matrices and are not related to the matrices , , and in the above proof outline.)

Applying Theorem 1.6 with to , almost surely for some constant . On the other hand, if where are the orthonormal Hermite polynomials of Definition 2.2, then for all even (since is an odd function), and Theorem 1.7 implies where and . Hence, almost surely,

for any . Note that for all , so by dominated convergence for . Then and as , where and . As is continuous in , , and , , and hence taking yields almost surely. ∎

Proof of Corollary 1.5.

We verify the conditions of Theorem 1.1: The kernel function is odd and bounded as for a constant , so and . Writing , for any

Note that for all , so is bounded by a constant for all large . By Lemma C.4 of [20], as uniformly in . Then Lemma C.5 of [20] implies that the remaining technical condition of Theorem 1.1 holds. Theorems 1.1 and 1.4 then together imply

and the result follows as the left and right sides coincide by Proposition 1.3. ∎

3. Proof of concentration inequality

In this section, we prove Theorem 1.6 following the outline sketched in Section 2. By rescaling , we may assume without loss of generality . We denote by the row of .

Lemma 3.1.

For any , there exist constants depending only on and such that the following holds: Define as the set of pairs of matrices such that , , and for each

If are random and independent with , then

Proof.

By Corollary 5.35 of [56], , and similarly for .

For and any , and . Let and denote large and small constants that may change from instance to instance. Defining , . Then for , applying Corollary 4 of [27] with ,

For any , where is independent of . Hence

and

for some constants and . Lemma 1 of [38] implies the chi-squared tail bound . The same argument holds for the analogous sums with , , and in place of , and the result follows by a union bound over . ∎

Lemma 3.2.

Proof.

Consider as a function from to . The gradient with respect to column of is

for with and . This yields the gradient bound

where the last inequality applies . Applying Cauchy-Schwarz and the bound ,

| (10) |

We apply the integration argument of Maurey and Pisier: For each , let and . Then

where represents the vector inner-product in . Noting that and are independent and both equal in law to , we may first condition on and use the Cauchy-Schwarz inequality and the bound to obtain

The definition of implies that is controlled over the entire integration path : We have

and also

by Hölder’s inequality. Then for any and , (10) implies

and the result follows. ∎

Let us now recall , , and from Definition 2.1.

Lemma 3.3.

For any symmetric matrix , .

Proof.

For any with , we may construct such that

Then and, letting ,

The result then follows from Lemma 5.4 of [56]. ∎

Lemma 3.4.

Let . For some and all ,

Proof.

Let denote a constant that may change from instance to instance. For any ,

as there are at most non-zero entries of , and for each non-zero entry there are two choices of sign. Using , and noting that is monotonically increasing over and that for , this implies

For , we use the bound , as each coordinate of takes one of three values. Then

Combining these bounds,

∎

Lemma 3.5.

Proof.

For notational convenience, define the event . Applying Lemma 3.4 and a union bound over , for any ,

Let be the set of all diagonal matrices in with all diagonal entries in . Note that if and only if for all . Then, conditional on and the event , equals in law for uniformly distributed over . Hence

where the last equality follows from as the kernel function is odd. Then Jensen’s inequality yields, for any and ,

and so

where the last line applies Lemma 3.2 and the bound . Optimizing over yields the desired result. ∎

We now conclude the proof of Theorem 1.6.

Proof of Theorem 1.6.

4. Decomposition of Hermite polynomials of sums of IID random variables

In this section, we prove the approximation (8) formalized as the following proposition:

Proposition 4.1.

Let , where are IID random variables such that , , and for each . Let denote the orthonormal Hermite polynomial of degree . Define

| (11) | ||||

| (12) | ||||

| (13) |

Then, for each and any , for all sufficiently large (i.e. for where may depend on , , , and the distribution of ).

The following lemma shows that and for any and all sufficiently large . Hence Proposition 4.1 may be interpreted as decomposing into the sum of an term , an term , and an term .

Lemma 4.2.

Suppose are IID random variables, with for all . Let be any polynomial functions such that for each . Then for any ,

for all sufficiently large .

Proof.

Fix . Let

and let be an even integer such that . Then

and it suffices to show for a constant independent of . Note that

For each term of the above sum, if there is some such that for exactly one pair of indices and , then the expectation of that term is 0 as and is independent of . Hence, for terms in the sum with non-zero expectation, there are at most distinct values of . Then the number of such terms is at most , and the magnitude of each such term is at most , for some constants independent of , establishing . ∎

Proof of Proposition 4.1.

Let . It will be notationally convenient to work with the monic Hermite polynomials . Let us accordingly define , , and . Then

and we wish to show for any , for all sufficiently large .

We proceed by induction on . Note that , , and . Then for , , and for ,

Hence the proposition holds with .

Let us assume by induction that the proposition holds for and . Recall that the monic Hermite polynomials satisfy the three-term recurrence (c.f. eq. (5.5.8) of [53]). We may compute

Substituting these expressions into the three-term recurrence,

for

Fix . Note that , , and , so by Lemma 4.2,

for all large . By the induction hypothesis, for all large , and also for all large by Lemma 4.2 (applied to the simple case where and ). Then for all large . Similarly, the induction hypothesis implies for all large . Putting this together,

for all large , completing the induction. ∎

5. Bounding the dominant matrix

Consider the polynomial kernel matrix in Theorem 1.7. Throughout this section, we let denote the (fixed) degree of the polynomial , and we write

Corresponding to the decomposition of given in Proposition 4.1, we consider the following decomposition of :

Definition 5.1.

With the above definitions, . In this section, we establish the following result:

Proposition 5.2.

Our proof uses the moment method and the moment comparison argument described in Section 2. The following definitions of an -graph and a multi-labeling of such a graph will correspond to the primary combinatorial object of interest in the subsequent analysis.

Definition 5.3.

For any integer , an -graph is a graph consisting of a single cycle with vertices and edges, with the vertices alternatingly denoted as -vertices and -vertices.

We will consider the vertices of the -graph to be ordered by picking an arbitrary -vertex as the first vertex and ordering the remaining vertices according to a traversal along the cycle. A vertex “follows” or “precedes” another vertex if comes before or after , respectively, in this ordering, and the last vertex of the cycle (which is an -vertex) is followed by the first -vertex.

Definition 5.4.

A multi-labeling of an -graph is an assignment of a -label in to each -vertex and an ordered tuple of -labels in to each -vertex, such that the following conditions are satisfied:

-

(1)

The -label of each -vertex is distinct from those of the two -vertices immediately preceding and following it in the cycle.

-

(2)

The number of -labels in the tuple for each -vertex satisfies , and these -labels are distinct.

-

(3)

For each distinct -label and distinct -label , there are an even number of edges in the cycle (possibly 0) such that its -vertex endpoint is labeled and its -vertex endpoint has label in its tuple.

A -multi-labeling is a multi-labeling with all -labels in and all -labels in .

A key bound on the number of possible distinct -labels and -labels that appear in a multi-labeling of an -graph is provided by the following lemma. We will always consider -labels to be distinct from -labels, even though (for notational convenience) we use the same label set for both.

Lemma 5.5.

Suppose a multi-labeling of an -graph has -labels on the first through -vertices, respectively, and suppose that it has total distinct -labels and -labels. Then .

We defer the proof of Lemma 5.5 to Appendix A. Figure 3 shows an example of a multi-labeling of an -graph for and . In this multi-labeling, and the number of total distinct labels is , so Lemma 5.5 holds with equality.

The non-negative quantity appears in many of our combinatorial lemmas, and we give it a name:

Definition 5.6.

Suppose a multi-labeling of an -graph has -labels on the first through -vertices, respectively, and suppose that it has total distinct -labels and -labels. The excess of the multi-labeling is .

A high-level intuition, which we make precise in various ways in Appendix A, is that multi-labelings with zero or small excess satisfy many regularity properties. For example, we prove the following in Appendix A:

Lemma 5.7.

Suppose a multi-labeling of an -graph has excess . For each and , let be the number of edges in the -graph such that the -vertex endpoint is labeled and the -vertex endpoint has label in its tuple. Then .

In particular, a multi-labeling with excess has either or for every label-pair , by the above lemma and condition (3) of Definition 5.4. This indeed holds for the example of Figure 3.

Definition 5.8.

Two multi-labelings of an -graph are equivalent if there is a permutation of and a permutation of such that one labeling is the image of the other upon applying to all of its -labels and to all of its -labels. For any fixed , the equivalence classes under this relation will be called multi-labeling equivalence classes.

The number of distinct -labels, number of distinct -labels, number of -labels on each of the -vertices, and excess are equivalence class properties, i.e. they are the same for all labelings in the same multi-labeling equivalence class. The connection between Definition 5.4 of a multi-labeling and our matrix of interest is provided by the following lemma:

Lemma 5.9.

Let be as in Proposition 5.2, and let be an even integer. Let denote the set of all multi-labeling equivalence classes for an -graph. For each multi-labeling equivalence class , let be the excess, the number of distinct -labels, and the number of -labels on the first to -vertices, respectively. Then, for as in (6) and with the convention ,

| (14) |

Proof.

By Definition 5.1, letting for notational convenience,

Note that as by assumption, for any positive odd integer . Hence, if any appears an odd number of times in the expression , then as the entries of are independent, . We identify the combination of sums above, over the remaining non-zero terms, as the sum over all possible -multi-labelings of an -graph. Here, the first sum over is over all choices of -labels, with condition (1) in Definition 5.4 corresponding to the constraints in the sum. The sum over is over all choices of the number of -labels in the tuple for each -vertex, and the sum over is over all choices of -labels for the -vertex, with condition (2) in Definition 5.4 corresponding to the constraint that are distinct. The product expression then corresponds to a product, over all -vertices, all -labels for that -vertex, and both -vertices immediately preceding and immediately following that -vertex, of , where is the -label and is the -label of the -vertex. The condition that each appears an even number of times so that this term has non-zero expectation is precisely condition (3) in Definition 5.4. Thus, to summarize,

where are the numbers of -labels for the first through -vertices, respectively.

Consider a fixed -multi-labeling and write , where is the number of times appears as a term in this product. Note that each is even (possibly 0). As , , and the entries of are independent,

where the last inequality applies Lemma 5.7 and we use the convention . (14) then follows upon noting that each -multi-labeling with distinct -labels and distinct -labels has -multi-labelings in its equivalence class, and . ∎

We wish to compare the upper bound in (14) to an analogous quantity for a deformed GUE matrix:

Definition 5.10.

For , let be distributed according to the GUE, i.e. are IID , and for . Let be standard real Wishart-distributed with degrees of freedom and zero diagonal, i.e. where , , and denotes with its diagonal set to 0. Take and to be independent, and define

As with , the limiting spectral distribution of is also . It follows from the results of [16] that, in fact, a norm convergence result holds for , i.e. , using which we may establish the following Proposition:

Proposition 5.11.

Let be as in Definition 5.10. Suppose is an even integer and with and for some constant . Then, for any and all sufficiently large ,

The proof of Proposition 5.11 is deferred to Appendix B. As , our strategy for proving Proposition 5.2 will be to show that the upper bound in (14) can in turn be bounded above using the quantity , for some choices of and . To analyze , we consider the following notion of a simple-labeling of an -graph:

Definition 5.12.

A simple-labeling of an -graph is an assignment of a -label in to each -vertex and either one -label in or the empty label to each -vertex, such that the following conditions are satisfied:

-

(1)

The -label of each -vertex is distinct from those of the two -vertices immediately preceding and following it in the cycle.

-

(2)

For each distinct -label and distinct non-empty -label , there are an even number of edges in the cycle (possibly 0) such that its -vertex endpoint is labeled and its -vertex endpoint is labeled .

-

(3)

For any two distinct -labels and , the number of occurrences (possibly 0) of the three consecutive labels on a -vertex, its following -vertex, and its following -vertex is equal to the number of occurrences of the three consecutive labels .

A -simple-labeling is a simple-labeling with all -labels in and all non-empty -labels in .

Analogous to Lemma 5.5, the following lemma provides a key bound on the number of possible distinct -labels and -labels that appear in a simple-labeling of an -graph.

Lemma 5.13.

Suppose a simple-labeling of an -graph has -vertices with non-empty label and total distinct -labels and distinct non-empty -labels. Then .

The proof of Lemma 5.13 is deferred to Appendix A. We may then define the excess of a simple-labeling, analogous to Definition 5.6, and note that the excess is always nonnegative.

Definition 5.14.

Suppose a simple-labeling of an -graph has -vertices with non-empty label and total distinct -labels and distinct non-empty -labels. The excess of the simple-labeling is .

Figure 4 shows a simple-labeling of an -graph for , with -vertices having non-empty label and distinct -labels and non-empty -labels. Hence in this example, Lemma 5.13 holds with equality, and the excess is .

Definition 5.15.

Two simple-labelings of an -graph are equivalent if there is a permutation of and a permutation of such that one labeling is the image of the other upon applying to all of its -labels and to all of its -labels. (The empty -label remains empty under any such permutation .) For any fixed , the equivalence classes under this relation will be called simple-labeling equivalence classes.

Motivation for Definition 5.12 of a simple labeling is provided by the following lemma, which gives a lower bound for the quantity :

Lemma 5.16.

Let be as in Definition 5.10, and let be an even integer. Let denote the set of all simple-labeling equivalence classes for an -graph. For each simple-labeling equivalence class , let be its excess, be the number of -vertices with non-empty label, and be the number of distinct -labels. Then, with the convention ,

| (15) |

Proof.

By Definition 5.10, letting for notational convenience,

In the fourth line above, we restricted the summation to , as for each by Definition 5.10.

Let us write where is the number of times appears in this product, and let us write , where and are the numbers of times and appear in this product, respectively. only if each is even (possibly zero), in which case this quantity is at least 1. Similarly, note that if is such that , then and are independent with and . Then for all nonnegative integers , and this is 0 if and at least 1 if . Hence unless for each and is even (possibly zero) for each , in which case this quantity is also at least 1.

The above arguments imply, in particular, that unless is even. As is even by assumption, then must also be even, in which case . Hence each term of the sum in the above expression for is nonnegative, so a lower bound is obtained if we further restrict the summation to (rather than just ), i.e.

We identify the combination of these sums as a sum over all -simple-labelings of an -graph. Here, the first sum over is over all choices of the subset of -vertices having non-empty label. The second sum over is over all choices of -labels, with condition (1) in Definition 5.12 corresponding to the constraints . The last sum over is over all choices of -labels for the -vertices that have nonempty label. The product expression then corresponds to a product over all -vertices with non-empty label and both -vertices immediately preceding and following that -vertex, and the condition that each appears an even number of times corresponds to condition (2) in Definition 5.12. Similarly, the product expression corresponds to a product over all -vertices with empty label, and the condition that each appears the same number of times as is precisely condition (3) in Definition 5.12. (By restricting the sum to for all , no diagonal terms appear in this product.) Applying the bound whenever this quantity is nonzero,

where is the number of -vertices in the simple-labeling with non-empty label. Any simple labeling with distinct -labels and at most distinct non-empty -labels has at most labelings in its equivalence class (where we have used and ). The desired result then follows upon identifying . ∎

The remainder of the proof of Proposition 5.2 involves a comparison of the upper bound in (14) and the lower bound in (15). The intuition for the comparison is the following: The dominant contributions to the sums in (14) and (15) come from labelings with small excess. Focusing on labelings with excess 0, if we take any multi-labeling equivalence class with and replace the labels of -vertices having more than one -label with , then it may be shown that we obtain a valid simple-labeling equivalence class with . For example, the multi-labeling of Figure 3 is mapped to the simple labeling of Figure 4 under this procedure. Furthermore, for any with , we may show

(The arguments that establish these claims are a specialization of our combinatorial lemmas in Appendix A to the cases of and .) Hence, this mapping yields an exact correspondence between terms in (14) with excess and terms in (15) with excess .

As we must consider to establish a tight bound in spectral norm, we need to also handle terms in (14) where . We do so by extending the above mapping to all multi-labeling equivalence classes , in the case . The properties of this mapping that we will need are summarized in the following proposition.

Proposition 5.17.

Suppose and . Let and denote the set of all multi-labeling and simple labeling equivalence classes of an -graph, respectively. For , let be its excess and be the number of distinct -labels, and for , let be its excess, be the number of distinct -labels, and be the number of -vertices with non-empty label. Then there exists a map such that, for some constants depending only on ,

-

(1)

For all , ,

-

(2)

For all , , and

-

(3)

For any and ,

(16)

The proof of this proposition and the explicit construction of the map require some detailed combinatorial arguments, which we defer to Appendix A. Using this result, we may complete the proof of Proposition 5.2 in the case .

Proof of Proposition 5.2 (Case ).

For any and even integer ,

By Lemma 5.9, Definition 5.6, and Proposition 5.17,

where the last line holds for all sufficiently large if . Let

and let . Then for all sufficiently large and , , and also (as , , and ). Then

On the other hand, by Lemma 5.16,

for all sufficiently large . Since and if , Proposition 5.11 implies for all large . Thus

Taking with sufficiently large such that (which is possible for any sufficiently small ), this implies for all large . Then almost surely, and taking concludes the proof. ∎

As is continuous in , , and , Proposition 5.2 in the case may be established via a continuity argument:

Proof of Proposition 5.2 (Case ).

For any , let , and let be the matrix as defined in Definition 5.1 for the kernel function . Then , where has zero diagonal and equals off of the diagonal. By Proposition 5.2 for the case, established above, . By standard results for covariance matrices (see e.g. [29]), almost surely under the assumption (6), for a constant . This implies for any , and the desired result follows by taking . ∎

6. Analyzing the remainder matrices

To conclude the proof of Theorem 1.7, we analyze in this section the remainder matrices and of Definition 5.1.

Lemma 6.1.

As with , almost surely.

Proof.

Definition 6.2.

For , define with entries

Note that in Definition 5.1 is given by .

Lemma 6.3.

As with , almost surely for any .

Proof.

Letting for notational convenience, note that

where we set

| (17) |

and

| (18) |

If there is some such that for exactly one pair of indices , then as , independence of the entries of implies . Hence, we may restrict the sum in (17) to terms where each index equals some other index . Then the number of distinct indices is at most . Furthermore, it is clear that always, for a constant independent of and .

We now consider several cases for a nonzero term , depending on the number of distinct indices among :

Case 1: . Letting denote the sum over terms of (17) belonging to this case, the above implies for a constant independent of and .

Case 2: . Then either or for some (where and are taken modulo 6), with the remaining indices all distinct. Suppose without loss of generality that and are distinct from each other and from . Let and (which exists when ). By the distinctness conditions in (17), for all . If furthermore for all , then appears exactly once in (18), so . If , then appears twice, once as the term and once in the term . The product of these terms is , and as and , this also implies . Hence we must have for some . The same argument applied to and shows that we must have for some . Then , so there cannot be exactly distinct indices . Then there are at most such distinct indices, and letting denote the sum over terms of (17) belonging to this case, we obtain for a constant .

Case 3: . Then all indices are distinct. Applying the argument of Case 2, there exists such that . There exists further such that , such that , etc., and for each we obtain some such that . Then the number of distinct indices is at most . Letting denote the sum over terms of (17) belonging to this case, we obtain .

Putting the cases together,

for a constant and all large and . Then for any ,

so almost surely, and the result follows by taking . ∎

Proof.

We now conclude the proof of Theorem 1.7.

Proof of Theorem 1.7.

Recall Definitions 5.1 and 6.2 and the decompositions and . Proposition 5.2 and Lemmas 6.1, 6.3, and 6.4 imply . The conditions of Theorem 1.1 are verified for the kernel function as in the proof of Corollary 1.5 in Section 2. Furthermore, and have the same limiting empirical spectral distribution, since has finite rank. Then Theorem 1.1 implies almost surely, and this establishes property (1) of Theorem 1.7.

To verify the claim regarding the non-zero eigenvalues of in property (2) of Theorem 1.7, we compute from (9) and . If and are the two non-zero eigenvalues of , then and , so and are the roots of the equation

By the law of large numbers, and almost surely. Since the roots of a polynomial are continuous in its coefficients, the result follows. ∎

Appendix A Combinatorial results

This appendix contains the proofs of Lemmas 5.5, 5.7, and 5.13 used in Section 5, as well as the proof of Proposition 5.17 and the explicit construction of the map in that proposition.

A.1. Proof of Lemmas 5.5, 5.7, and 5.13

We restate the lemmas using their original numbering. See 5.13

Proof.

Let and , and consider an undirected graph on the vertex set (the disjoint union of and with elements, treating elements of and the elements of as distinct). Let have an edge between if there are three consecutive vertices (, , ) of the -graph with the labels , , or , , . Let have an edge between and if there are two consecutive vertices of the -graph such that the -vertex has label and the -vertex has label . The number of vertices of incident to at least one edge is , and must be connected, so it has at least edges. An edge in between corresponds to at least two consecutive pairs of -vertices in the -graph having an -vertex with empty label in between, by condition (3) of Definition 5.12, so the number of such edges is at most . Similarly, an edge in between and corresponds to at least two pairs of consecutive and -vertices of the -graph such that the -vertex has non-empty label, by condition (2) of 5.12, so the number of such edges is at most . Then . ∎

Turning now to multi-labelings, for each and a given multi-labeling, let us denote throughout

Then the following two lemmas hold:

Lemma A.1.

In any multi-labeling of an -graph, each that appears as an -label has .

Proof.

Suppose that an -label appears only once. The two -vertices preceding and following that -vertex must have distinct labels, say and , by condition (1) of Definition 5.4. Then exactly one edge in the -graph has -vertex endpoint labeled and -vertex endpoint having label (and similarly for and ), contradicting condition (3) of Definition 5.4. ∎

Lemma A.2.

Suppose a multi-labeling of an -graph has at most distinct -labels. If this multi-labeling has excess , then

Consequently, the number of -vertices having any label for which is also at most .

Proof.

Observe that if total distinct -labels and -labels appear in the labeling, and at most of these are -labels, then the labeling has at least distinct -labels. Let . Then Lemma A.1 implies (where are the numbers of -labels on the -vertices), so . Then the -labels in account for at least of the total -labels, implying that at most total -labels remain. This establishes the first claim, and the second follows directly from the first. ∎

We will prove many subsequent claims regarding multi-labelings by induction on . The following two lemmas describe the base case of the induction and the basic inductive step.

Lemma A.3.

Suppose or . Then for any multi-labeling of the -graph, all -labels are distinct, and all -vertices have the same tuple of -labels, up to reordering.

Proof.

Lemma A.4.

In a multi-labeling of an -graph with , suppose a -vertex is such that its -label appears on no other -vertices. Let the -vertex preceding be , the -vertex preceding be , the -vertex following be , and the -vertex following be .

-

(1)

If and have different -labels, then the graph obtained by deleting and and connecting to is an -graph with valid multi-labeling.

-

(2)

If and have the same -label, then the graph obtained by deleting , , , and and connecting to the -vertex after is an -graph with valid multi-labeling.

Proof.

First consider case (1). As and have distinct -labels, it remains true that no two consecutive -vertices in the -graph have the same -label, so condition (1) of Definition 5.4 holds. Condition (2) of Definition 5.4 clearly still holds as well. If has -label and has -labels , then has -labels as well, up to reordering, by conditions (2) and (3) of Definition 5.4 and the fact that is the only -vertex with label . Then in the -graph obtained by deleting and , the number of edges with -vertex endpoint labeled and -vertex endpoint having label for any is zero, and the number of edges with -vertex endpoint labeled and -vertex endpoint having label is the same as in the original -graph for all other pairs . Thus condition (3) of Definition 5.4 still holds as well, so the -graph has a valid multi-labeling.

Now consider case (2). and the -vertex after must have different -labels in the original -graph, by condition (1) of Definition 5.4. As and have the same -label, this implies and the -vertex after must have different -labels, so condition (1) of Definition 5.4 still holds in the -graph. Condition (2) of Definition 5.4 clearly still holds in the -graph as well. Suppose has -label , and have -label , and has -labels . As in case (1), must also have -labels up to reordering. Then in the -graph obtained by deleting , , , and , the number of edges with -vertex endpoint labeled and -vertex endpoint having label for any is zero, the number of edges with -vertex endpoint labeled and -vertex endpoint having label for any is two less than in the original -graph, and the number of edges with -vertex endpoint labeled and -vertex endpoint having label is the same as in the original -graph for all other pairs . Hence condition (3) of Definition 5.4 still holds as well, so the -graph has a valid multi-labeling. ∎

See 5.5

Proof.

We induct on . For , a multi-labeling must have and , and for , a multi-labeling must have and , by Lemma A.3. The result is then easily verified in these two cases.

Suppose by induction that the result holds for and , and consider a multi-labeling of an -graph with . If each distinct -label appears at least twice, then there are at most distinct -labels. Lemma A.1 implies there are at most distinct -labels, so , establishing the result.

Thus, suppose that some -vertex has a label that appears exactly once, and let be as in Lemma A.4. If and have different -labels, follow procedure (1) in Lemma A.4 to obtain a multi-labeling of an -graph. This multi-labeling now has total distinct -labels and -labels, and so the induction hypothesis implies where is the number of -labels of the deleted -vertex . Hence .

If and have the same -label, follow procedure (2) of Lemma A.4 to obtain a multi-labeling of an -graph. This multi-labeling has between and (inclusive) total distinct -labels and -labels, where is the number of -labels of the deleted -vertex . The induction hypothesis implies , so . This completes the induction in both cases, establishing the desired result. ∎

See 5.7

Proof.

We induct on . For or 3, we must have or 2 for all by Lemma A.3, and by Lemma 5.5, so the result holds.

Suppose the result holds for and , and consider a multi-labeling of an -graph with . If each distinct -label appears at least twice, then there are at most distinct -labels, so Lemma A.2 applies. For any with , we have or for all , by conditions (1) and (3) of Definition 5.4. For any with , we apply the bound . Then by Lemma A.2.

Now suppose that some -vertex has a -label appearing exactly once. Consider the -graph or -graph obtained by Lemma A.4. In the case of the -graph, it is easily verified that is the same as in the original -graph, so the induction hypothesis implies , where is the number of -labels on the deleted -vertex .

In the case of the -graph, suppose the deleted -vertex (and ) has -labels, of which also appear on an -vertex different from and . If does not appear on or , then clearly is the same in the -graph and the original -graph for all . If is one of the -label values appearing only on and , then or 2 in both the -graph and the original -graph for all . If is one of the other -label values appearing on and , then in deleting , , , and , we may have reduced by 2 for at most two distinct values of (corresponding to the -labels of and ). This implies that reduces by at most 8 for this , with the maximal reduction occurring if for both of these values of in the original -graph. Then by the induction hypothesis, , as the -graph has total distinct and -labels. Then , so the result holds in this case as well, completing the induction. ∎

A.2. Construction of the map

Definition A.5.

In an -graph with a multi-labeling, an -vertex is single if it has only one -label. It is a good single if it is single and if its -label appears only on single -vertices. Otherwise, it is a bad single.

Definition A.6.

In an -graph with a multi-labeling, a pair of distinct (not necessarily consecutive) -vertices is a good pair if the following conditions hold:

-

(1)

and have the same tuple of -labels, up to reordering,

-

(2)

and are not single, and

-

(3)

for each appearing as an -label on and (i.e. this label appears on no other -vertices).

If an -vertex is not single and not part of any good pair, then is a bad non-single.

Thus, every -vertex is either a good single, a bad single, a bad non-single, or part of a good pair. Conditions (1) and (3) of Definition 5.4 require that, if is a good pair, then the two (distinct) -labels of the -vertices preceding and following are the same as those of the -vertices preceding and following (but not necessarily in the same order).

Definition A.7.

Suppose is a good pair of -vertices. Let the -vertices preceding and following be and , respectively, and let the -vertices preceding and following be and , respectively. Then the good pair is proper if has the same label as and has the same label as , and it is improper if has the same label as and has the same label as .

Definition A.8.

The label-simplifying map is the map from -multi-labelings of an -graph to -simple-labelings of an -graph, defined by the following procedure:

-

(1)

While there exists an improper good pair of -vertices , iterate the following: Let be the -vertex following and be the -vertex following , and reverse the sequence of vertices starting at and ending at (together with their labels).

-

(2)

For each -vertex in a good pair, relabel it with the empty label.

-

(3)

For each -vertex that is a bad single or a bad non-single, relabel it with the single label .

Remark A.9.

In the case where there are multiple improper good pairs in step (1) of this procedure, it will not be important for our later arguments in which order the pairs are selected and which vertex we choose as and which as . For concreteness, we may always select to be the improper good pair whose sorted -label-tuple is smallest lexicographically, and we may take to come before in the -graph cycle.

Lemma A.10.

The following are true for the label-simplifying map in Definition A.8:

-

(1)

Step (1) of the procedure in Definition A.8 always terminates in a valid -multi-labeling with no improper good pairs.

-

(2)

The image of any -multi-labeling under the map is a valid -simple-labeling.

-

(3)

If two multi-labelings are equivalent, then their image simple-labelings are also equivalent.

Proof.

Clearly each reversal in step (1) of the procedure preserves condition (2) of Definition 5.4 as well as the number of good pairs and -labels of each good pair. As and have the same -label because is improper, it also preserves conditions (1) and (3) of Definition 5.4, so the resulting labeling is still a valid -multi-labeling. Each time this reversal is performed, and become consecutive -vertices in the -graph, and the pair becomes a proper good pair. As and are consecutive, they must remain consecutive under each subsequent reversal, so their properness is preserved. Hence the procedure must terminate after a number of iterations at most the total number of good pairs in the multi-labeling, and the final multi-labeling is such that all good pairs are proper. This establishes (1).

To prove (2), note that the image labeling has either one -label or the empty label for each -vertex. Condition (1) of Definition 5.12 holds for the image labeling by condition (1) of Definition 5.4, as the -labels are preserved. As all good pairs in the multi-labeling obtained after applying step (1) of the procedure are proper, and step (2) of the procedure maps their labels to the empty label, condition (3) of Definition 5.12 holds for the image labeling. Finally, note that if is an -label appearing on good single vertices in the multi-labeling, then condition (2) of Definition 5.12 holds in the image labeling for this and all -labels by condition (3) in Definition 5.4. For the new -label created in step (3) of the map, note that for each there must be an even number of edges in the -graph with -endpoint labeled . Of these, there must be an even number with -endpoint for any good single label , by the above argument, and there must also be an even number with -endpoint belonging to a good pair since these edges must come in pairs. Hence the number of remaining edges adjacent to any -vertex with label must also be even. These are precisely the edges with -endpoint labeled and -endpoint labeled in the image labeling, so condition (2) of Definition 5.12 holds for the new -label and all -labels as well. Hence the image labeling is a valid -simple-labeling, establishing (2).

(3) is evident, as equivalent multi-labelings have the same proper and improper good pairs of -vertices and the same good single -vertices. ∎

Definition A.11.

Let and be the set of all multi-labeling equivalence classes and simple-labeling equivalence classes, respectively, of an -graph. For and any multi-labeling in , let contain its image simple-labeling under the label-simplifying map of Definition A.8, and define by .

A.3. Verification of Proposition 5.17, properties (1) and (2)

For the map of Definition A.11, property (1) of Proposition 5.17 is evident as the -labels are preserved. We verify property (2) by bounding the number of bad non-single -vertices.

For each pair with , and for a given multi-labeling, let us denote

Lemma A.12.

Suppose a multi-labeling of an -graph has excess . Then

Proof.

We induct on . For and 3, or 1 for all pairs , and by Lemma 5.5, so the result holds.

Suppose by induction that the result holds for and , and consider a multi-labeling of an -graph with . First suppose each distinct -label appears at least twice, so there are at most distinct -labels. If an -label is such that , then the pairs of -vertices before and after the two -vertices with label must have the same pairs of -labels, by conditions (1) and (3) of Definition 5.4. Thus the number of pairs with is at most the number of -vertices for which for all of its -labels . This is at most by Lemma A.2. On the other hand, the number of distinct -labels is at most one more than the number of distinct pairs of consecutive -labels. (This is easily seen by considering the undirected graph with vertices having an edge between if and only if some consecutive pair of -vertices have labels and , and noting that this graph is connected.) Lemma A.1 implies there are at most distinct -labels, and hence at least distinct pairs of consecutive -labels. At least of these have . If of these have , then , so . These account for at least pairs of consecutive -vertices, implying that at most pairs of consecutive -vertices remain. This establishes the result in this case.

Now suppose that there is some -vertex whose -label appears only once. Consider the -graph or -graph obtained by Lemma A.4. It is easily verified that is the same in this graph as in the original -graph, because if in the original -graph, then neither nor can be the -label of . On the other hand, our proof of Lemma 5.5 verified that this -graph or -graph has excess at most that of the original -graph, so the desired result follows from the induction hypothesis. ∎

The next lemma bounds the number of bad non-single -vertices, i.e. it shows that in any multi-labeling with small excess , most of the non-single -vertices must belong to a good pair.

Lemma A.13.

Suppose a multi-labeling of an -graph has excess and single -vertices. Then there are at least good pairs of -vertices.

Proof.

Let be the number of distinct and -labels and let be the numbers of -labels on the -vertices. We induct on . If , then Lemma A.3 implies , , and . If , then and there are no good pairs, and if , then and there is one good pair. Hence the result holds. If , then Lemma A.3 implies , , and . If , then , , and there are no good pairs. If , then , , and there are still no good pairs. In either case, the result also holds.

Consider , and assume by induction that the result holds for and . First suppose each distinct -label appears at least twice, so there are at most distinct -labels. By Lemma A.2 there are at most -vertices with some -label such that , so there are at least non-single -vertices for which each of its -labels has . Let be one such -vertex. We consider three cases:

Case 1: has two -labels and that appear on two different other -vertices and . Then Definition 5.4 implies that the three pairs of consecutive -vertices around , , and must have the same pair of -labels. By Lemma A.12, there are at most such -vertices .

Case 2: All -labels of appear on a single other -vertex , but has some additional -label not appearing on . Then either all such additional -labels have , or there is some such with . In the former case, the number of such vertices is at most by Lemma A.2. As is the unique -vertex sharing an -label with for which , this implies the number of such vertices is also at most . In the latter case, appears on a vertex distinct from and . Then the three pairs of -vertices around , , and must have the same pair of -labels, and by Lemma A.12 the number of such vertices is at most . Hence the number of -vertices belonging to this case is at most

Case 3: forms a good pair with some other vertex . By the bounds in cases 1 and 2, there are at least such vertices , hence at least good pairs, and the result holds.

Now suppose there is some -vertex whose -label appears only once. Let be as in Lemma A.4, and recall that and have the same -labels up to reordering. Consider four cases:

Case 1: and have different -labels, and and are single. Lemma A.4 yields an -graph with single -vertices, total -labels, and total distinct - and -labels. By the induction hypothesis, this -graph has at least

good pairs, which are also good pairs in the -graph.

Case 2: and have different -labels, and and each have -labels. Lemma A.4 yields an -graph with single -vertices, total -labels, and distinct - and -labels. By the induction hypothesis, this -graph has at least

good pairs. It can have at most one more good pair than the original -graph (which occurs if has a tuple of -labels appearing on exactly three different -vertices in the -graph).

Case 3: and have the same -label, and and are single. Lemma A.4 yields an -graph with single -vertices, total -labels, and either distinct - and -labels if and have an -label appearing only those two times, or distinct - and -labels otherwise. Supposing the former, this -graph has at least

good pairs, and it has the same number of good pairs as the original -graph. Supposing the latter, this -graph has at least

good pairs, and it can have at most one more good pair than the original -graph (which occurs if the -graph has a good pair containing the -label of the removed vertices and ).

Case 4: and have the same -label, and and each have -labels. Lemma A.4 yields an -graph with single -vertices, total -labels, and between and (inclusive) distinct - and -labels. If it has exactly distinct - and -labels, then we must have removed a good pair, and the -graph has at least

good pairs. If, instead, the -graph has distinct - and -labels for , then and cannot be a good pair in the original -graph as they have -labels for which , and the -graph can have at most more good pairs than the -graph, one for each such . The -graph has at least

good pairs. In all cases, we establish that the -graph has at least good pairs, completing the induction. ∎

Proof of Proposition 5.17, property (2).

Let be any multi-labeling equivalence class. Let have -vertices with non-empty label. This means has -vertices that do not belong to a good pair. These vertices have at least total -labels in , implying that there are at most total -labels on the good pair vertices. These good pair vertices account for at most distinct -labels in , and these are mapped to the empty label under the label-simplifying map. Furthermore, by Lemma A.13, there are at most bad non-single -vertices, and these have at most additional distinct -labels that are mapped to the new -label . Any bad single -vertex has an -label that is the same as one of these distinct -labels (otherwise it is a good single by definition), and the -label of any good single -vertex is preserved under the label-simplifying map. Hence, if is the number of total distinct - and -labels in and is the number of total distinct -labels and non-empty -labels in , then , so . Hence property (2) holds. ∎

A.4. Verification of Proposition 5.17, property (3)

Recall that we order the vertices of an -graph according to a cyclic traversal starting from a (arbitrary) -vertex.

Definition A.14.

The canonical simple labeling in a simple labeling equivalence class is the one in which each new -vertex label that appears in the cyclic traversal is , and each new non-empty -vertex label is .

The canonical multi-labeling in a multi-labeling equivalence class is the one in which each new -vertex label is and each new -vertex label is , with the new -vertex labels in the label-tuple for each -vertex appearing in sorted order.

Each has a unique canonical simple-labeling, which is an -simple labeling, and each has a unique canonical multi-labeling, which is an -multi-labeling.

For each and , property (3) of Proposition 5.17 is a bound on a certain weighted cardinality of the set

We describe a series of non-determined steps by which the mapping may be “inverted” to obtain the canonical multi-labeling of any , given :

-

(1)

Choose a non-empty -label value appearing in to be “n+1”, or assume there is no such label. (The -vertices with empty label will be the good pairs, and the remaining -vertices with label different from “n+1” will be the good singles.)

-

(2)

Choose a subset of -vertices with label “n+1” to be the bad non-singles in . (The remaining -vertices with label “n+1” will be the bad singles.)

-

(3)

For each -vertex in , choose the size of its -label tuple in to be between 2 and (inclusive), and pick -labels from for that tuple.

-

(4)

For each -vertex with label “n+1” not in , pick a single value in for its -label in .

-

(5)

For all -vertices with empty label in , pair them up into good pairs for .

-

(6)

For each good pair, choose the size of its -label tuple in to be between 2 and (inclusive), and choose a permutation of the second -label tuple of the pair that matches the first.

-

(7)

Let be the set of good pairs that are consecutive -vertices in the -graph and such that the -label (in ) of the -vertex between them appears at least twice. Choose an ordered subset of . For each in this subset, if is the -vertex between and , choose some other -vertex having the same -label as , and reverse the sequence of vertices from to or from to .

-

(8)

Choose -labels for such that the resulting labeling is canonical and two -vertices have the same label if and only if they do in . Choose the remaining -labels for (corresponding to the good pairs and good singles) such that the resulting labeling is canonical, the properties of Definitions A.5 and A.6 are satisfied, and two good single vertices have the same -label if and only if they do in .

These steps are non-determined in the sense that each step may be performed in multiple ways, yielding many possible output multi-labelings . They “invert” in the following sense:

Lemma A.15.

For any , the canonical multi-labeling of is a possible output of the above procedure.

Proof.

Let denote the -multi-labeling obtained by applying step (1) of the label-simplifying map in Definition A.8 to . (It is an -multi-labeling by Lemma A.10.)

may be obtained by the above procedures as follows: Perform steps (1) and (2) to correctly partition the -vertices into the good pair, good single, bad single, and bad non-single -vertices of . Perform steps (3) and (4) to recover the -labels in of the bad single and bad non-single -vertices. Perform steps (5) and (6) to correctly identify the good pairs of and the permutation that maps the label-tuple of the second vertex to that of the first vertex in each pair. Perform step (7) to invert the reversals that mapped to (in the reverse order of how they were applied in the label-simplifying map): This is possible because each reversal in step (1) of the label-simplifying map causes an additional good pair of -vertices to become consecutive in the -graph, with the -vertex between them having -label appearing at least twice, and these three vertices remain consecutive after each subsequent reversal. Finally, perform step (8) to recover the -labels and the good single and good pair -labels of , which is possible because (by assumption) is a valid canonical multi-labeling. ∎

To obtain the desired weighted cardinality bound for , we bound the number of ways each of the above 8 steps may be performed such that the final output is the canonical multi-labeling for some . The bounds for all but steps (4) and (7) follow from our preceding combinatorial estimates. The following simple lemma will yield a bound for step (7):

Lemma A.16.

Suppose a multi-labeling of an -graph has excess . Then there are at most good pairs of -vertices such that the two vertices in the pair are consecutive in the -graph cycle and the -label of the -vertex between them appears at least twice in the labeling.

Proof.

Call a -vertex “sandwiched” if it is between two consecutive -vertices that form a good pair. Let be a -label appearing on a total of -vertices, of which are sandwiched. If , then change the appearances of on the sandwiched -vertices to new -labels not yet appearing in the labeling. Otherwise if (so ), then change appearances of on the sandwiched -vertices to new -labels not yet appearing in the labeling. Do this for every such . Note that changing the -label of any sandwiched -vertex does not violate any of the conditions of Definition 5.4, so the resulting labeling is still a valid multi-labeling. If is the number of good pairs originally satisfying the condition of the lemma, then we have added at least new -labels to the labeling. Hence Lemma 5.5 implies , so . ∎

The remaining challenge is to bound the number of ways of performing step (4). This bound is not straightforward because the number of bad singles is not necessarily small when is small. We instead show that the number of bad singles that we may “freely label” is small:

Definition A.17.

In a multi-labeling of an -graph, is a connector if it appears as a -label and, among all -vertices that are adjacent to any -vertex with label , exactly two are bad singles and none are bad non-singles; these two bad singles are connected. A sequence of bad singles is a connected cycle if is connected to , is connected to , etc., and is connected to .

Note that “connector” refers to a label , not to any specific -vertex having as its label, and two “connected” bad singles are adjacent to -vertices having the connector label , but these -vertices may be distinct in the -graph. Each bad single -vertex may be connected to at most two other bad single -vertices (where the connectors are the -labels of its two adjacent -vertices), and hence this notion of connectedness partitions the set of bad single -vertices into connected components that are either individual vertices, linear chains, or cycles.

Motivation for this definition comes from the observation that if two bad single -vertices are connected, then they must have the same -label, as follows from condition (3) of Definition 5.4 and the fact that -labels appearing on good singles and good pairs must be distinct from those appearing on the remaining -vertices.

Lemma A.18.

Suppose a multi-labeling of an -graph has excess and single -vertices, of which are good single and are bad single. Then at least distinct -labels are connectors, and there are at most connected cycles of bad single -vertices.

Proof.

Suppose the multi-labeling is a -multi-labeling. Construct an undirected multi-graph with vertex set , where each edge of has one label in , as follows: For each -vertex in the -graph and each -label of , if is preceded and followed by -vertices with labels and , then add an edge in with label . (Thus has total edges.) Condition (3) of Definition 5.4 implies for any , each vertex of has even degree in the sub-graph consisting of only edges with label .

We will sequentially remove edges of corresponding to good pairs and good singles, until only edges corresponding to bad singles and bad non-singles remain. At any stage of this removal process, let us call a vertex of “active” if there is at least one edge still adjacent to that vertex. Let us define a “component” as the set of active vertices that may be reached by traversing the remaining edges of from a particular active vertex. (Hence a component of is a connected component, in the standard sense, that contains at least two vertices.) We will track the quantity

Initially, has active vertices plus distinct edge labels (where is the number of distinct - and -vertices of the -graph), and one component, so . Let us remove the edges of corresponding to good pairs. If an -vertex of a good pair has -labels, then the good pair corresponds to edges between a single pair of vertices in whose edge labels do not appear elsewhere in . Removing these edges removes distinct edge labels, and if this also changes the connectivity structure of , then either increases by 1, decreases by 1, or decreases by 1 and decreases by 2. In all cases, decreases by at most . Then after removing all edges of corresponding to good pairs, , as there are at most distinct -labels for the good pairs and at most good pairs.

Let us now remove the edges of corresponding to good singles. Let be an -label of a good single, and consider removing the edges of with label one at a time. As each vertex of has even degree in the subgraph of edges with label , when the first such edge is removed, the number of components and active vertices cannot change. Subsequently, the removal of each additional edge might increase by 1 upon considering the same three cases as above. When the last such edge is removed, there are no longer any edges with label by the definition of a good single, so decreases by 1. Hence removing all edges with label decreases by at most the number of such edges, and after removing the edges corresponding to all good singles.

Call the resulting graph . Every vertex of still has even degree in the subgraph of edges with label , for any . In particular, every active vertex of has degree at least two. By Definition A.17, is a connector if and only if has degree exactly two in , in which case the edges incident to in must have the same label , and the -vertices with label in the -graph are the bad singles connected by . A connected cycle of bad singles corresponds to the edges of a cycle of (necessarily distinct) vertices in with degree exactly two.