Stochastic Model of Financial Markets Reproducing Scaling and Memory in Volatility Return Intervals

Abstract

We investigate the volatility return intervals in the NYSE and FOREX markets. We explain previous empirical findings using a model based on the interacting agent hypothesis instead of the widely-used efficient market hypothesis. We derive macroscopic equations based on the microscopic herding interactions of agents and find that they are able to reproduce various stylized facts of different markets and different assets with the same set of model parameters. We show that the power-law properties and the scaling of return intervals and other financial variables have a similar origin and could be a result of a general class of non-linear stochastic differential equations derived from a master equation of an agent system that is coupled by herding interactions. Specifically, we find that this approach enables us to recover the volatility return interval statistics as well as volatility probability and spectral densities for the NYSE and FOREX markets, for different assets, and for different time-scales. We find also that the historical S&P500 monthly series exhibits the same volatility return interval properties recovered by our proposed model. Our statistical results suggest that human herding is so strong that it persists even when other evolving fluctuations perturbate the financial system.

keywords:

Volatility , Return intervals , Agent-based modeling , Financial markets , Scaling behavior1 Introduction

To estimate risk in a financial market it is essential that we understand the complex market dynamics involved [1, 2]. Statistical physics has been found useful dealing with the general concepts of complexity and its applications in finance [3, 4, 5]. Financial markets are among the most interesting examples of such complex social systems where methods of statistical physics face extreme challenges [6]. Although our current understanding of financial fluctuations and the nature of microscopic market interactions remains limited and ambiguous [7, 8], as vast amounts of financial data have become more available we are now able to apply advanced methods of empirical analysis to gain greater insight into the market’s complexity [9, 10, 1, 2].

Here we use a general agent-based stochastic model [11], reproducing first and second order statistics of absolute return in the financial markets and find that with very minor modifications it is able to reproduce various statistical properties of the high volatility return intervals [12, 13, 14, 15, 16].

We focus on the heuristic model of volatility, which is defined as fluctuations in the absolute returns, across a wide range of time-scales from one minute to one month. There are many other attempts of econometric approach to the problem of behavioral opinion dynamics of agents in the financial markets [17, 18, 19, 20, 21, 22, 23] able to explain fat tails and volatility clustering. Usually these econometric analyses based on generalized or simulated method of moments (GMM or SMM) are limited to the oversimplified agent models with small number of parameters. To our knowledge, the values of parameters in these models are dependent on selected time window of return definition and are not universal for other time scales. Earlier proposed model of the financial markets [11], which we use here, accumulates some general features of agent dynamics and price formation from Ref. [24, 25]. This model further generalizes herding dynamics for the three groups of agents [26] by the continuous stochastic differential equations derived for the infinite number of agents with pairwise global interactions. At the same time the proposed model is able to account for the feedback of market volatility on the market trading activity observed in the financial markets [27, 28, 29, 30, 31, 32, 33]. The main task of this work is to demonstrate that proposed stochastic model with the same set of parameters allows to understand statistics of absolute return intervals for wide range of time and threshold scales even when the values are extreme.

We find that the statistical properties of return intervals are universal for a broad range of financial markets, from NYSE and FOREX. The model can reproduce these statistical properties by using the same set of parameters for varying time-scales, from high frequency data to monthly S&P500 index values across a 145-year period [34]. These results imply that the various power-law statistics of financial markets might be due to a non-linear stochasticity, which we incorporate into the herding-based model of financial markets [35, 36]. Though the proposed model is designed to analyze statistical properties of volatility and the price of assets is not considered, the revealed bursting behavior extends our understanding of bubbles in financial markets [34, 33] in general.

2 Method

We use a modified version of the three-state agent-based model [11, 26] to reproduce and explain the origin of the statistical properties of volatility return intervals [12, 13, 14]. The interplay between the endogenous dynamics of agents and exogenous noise is the primary mechanism responsible for the observed statistical properties. By exogenous noise we mean order flow fluctuations.

Though our approach to the financial markets [11, 26] inherits some essential features from herding based modeling proposed in [24, 25] and other numerous papers, there are few significant extensions and different model interpretations we use in our approach. Let us shortly summarize our main assumptions:

-

1.

Pairwise global herding interactions of agents (traders) are assumed as the result of the pairwise interactions of traders during their trade actions. This conditions macroscopic description of agents by SDEs independent from the total number of agents, and macroscopic state feedback on the microscopic trading activity of agents.

-

2.

The clustering of volatility and trading activity, long-range dependence and multifractality are related with the nonlinear nature of SDEs derived for corresponding financial variables.

-

3.

The model has to incorporate endogenous (agent based) and exogenous (order flow) fluctuations as they coexist and interplay in the real markets.

-

4.

There are at least three different time scales of return fluctuations in the financial markets a) the long term fluctuations of fundamentalists and chartists; b) the short term fluctuations of optimists and pessimists; c) the most frequent fluctuations of return related with order flow.

These assumptions lead to the consentaneous microscopic and macroscopic model combining endogenous agent based dynamics with stochastic dynamics driven by exogenous noise. We use visual empirical test here based on a double logarithmic axes histograms to select 9 independent model parameters seeking to reproduce many different power-law statistical properties at the same time. The heuristic consideration of noises generated by derived SDEs makes this parameter selection procedure preferable against formal fitting methods and helps to reproduce many stylized facts based on first and second order statistics with the same set of parameters for different markets and for different time windows of return definition.

2.1 Endogenous versus exogenous

The standard price model [37] and autoregressive conditional heteroskedasticity (ARCH) family of models [38, 39] serve as phenomenological frameworks consistent with endogenous volatility and exogenous noise. For example, by analogy with ARCH family models we can assume that the log return of the market price , defined at any moment for a time interval can be modeled as a product of endogenous volatility and exogenous noise

| (1) |

Here for the sake of simplicity we use a Gaussian noise , and volatility is assumed to be a linear function of the absolute endogenous log price

| (2) |

where can be derived from the agent-based model (ABM) defining the ratio of market price to fundamental price [11]. Here serves as a normalization parameter, while determines the impact of endogenous dynamics on the observed time series. Our model, defined by Eqs. (1) and (2), comprises both the dynamic part described by and the purely stochastic part described by .

The motion of the financial Brownian particle colliding with the flow of limit orders in the real financial market [40] probably serves as a possible physical interpretation of the Gaussian noise in Eq. (1). The selected time window here is limited by the requirement that the change of has to be inconsiderable. This means that exogenous fluctuations in this model are much more frequent than endogenous. Note that Eq. (1) in econometric consideration does not include any limits for as there is not related to the similar physical interpretations and is just formally defined through the auto-regressive model.

2.2 ABM

We use a version of the three-state agent-based herding model [11, 26] to describe the endogenous dynamics of agents in the financial markets and to reproduce the statistical properties of volatility return intervals [12, 13, 14].

Agents interact globally as the pairwise interactions of traders during their trade actions are assumed. This assumption helps to overcome the problem of spacial structure of interactions usually considered in agent modeling approaches [41] and allows to account for the observed relation of return with trading activity. The dynamics of agent population under constraints are described by stochastic differential equations (SDEs) derived from the master equation with one-step transition rates proposed by Kirman [42]:

| (3) |

where describes the individualistic switching tendency, and quantifies influence of peers (). Note that a symmetric relation is usually assumed and in the case of pairwise global coupling of agents number of peers is proportional to the total number of agents . A basic understanding of financial market dynamics allows us to make assumptions that simplify the model.

We first assume that the three states correspond to three trading strategies: fundamental (), optimistic (), and pessimistic (), thus may take values , and . Fundamental traders assume that the price will approach a fundamental price that is determined purely by market fundamentals. Optimistic and pessimistic trading are two opposite approaches in the same chartist () trading strategy, i.e., optimists always buy and pessimists always sell. Mathematical forms of the excess demands, , for both fundamental and chartist strategies are given by [24]

| (4) | |||

| (5) |

where is the current market price of an asset, the relative impact of chartists, and the average mood. These three trading strategies are also considered in numerous other similar approaches [43, 24, 44, 45, 46]. Furthermore fundamentalist trading strategy, as described here, may be related to the concept of “rational” agents as used in [47, 48, 49, 50], while chartists, both optimists and pessimists, are mostly equivalent to “maladapted” agents in [47, 48, 49, 50].

We next simplify the model by assuming that optimists and pessimists are high-frequency trend followers, i.e., chartists. Chartists trade among themselves times more frequently than with fundamentalists. There is no genuine qualitative difference between optimists and pessimists in terms of herding interactions, and certain symmetric relationships are thus implied ( and ). Chartists share their attitude towards fundamental trading () and fundamentalists are indifferent to arbitrary moods ( and ). The assumption that fundamentalists are long-term traders and chartists short-term traders can be written as (, and ). Under these assumptions the dynamics is well approximated by two nearly independent SDEs [26, 11] that resemble the original SDE from the two-state herding model [42, 24],

| (7) | |||

| (8) |

where is the inter-trade time, and and are independent Wiener processes. Equations (7–8) can be derived starting from the 6 one step transition probabilities and corresponding master equation, see [26] for details, or just using adiabatic approximation in the description of optimist-pessimist dynamics as in [11]. Note that in the above equations we scale model parameters, , , and , as well as time (omitting the subscript in the equations).

We consider the inter-trade time a macroscopic feedback function, which can take the form

| (9) |

This form is inspired by empirical analyses [27, 28, 29, 51], where the trading activity is proportional to the square of the absolute returns (thus ). This form depends on the long-term component of returns in the proposed model (see [52]) and converges to unity when approaches 1. The trading activity never reaches zero, and in non-volatile periods it fluctuates around some equilibrium value. Note that in this approach implements the macroscopic feedback based on the pairwise global herding interaction of agents through their exchange in the pairwise trade action, see previous papers [52, 26, 11] for more details.

Note that present form of Eq. (9) is slightly different from the previously published in [11] as here we take off the dependence on high frequency fluctuations and parameter value will be slightly different from . This simplification is very important as it makes Eq. (7) independent from Eq. (8) and provides much more transparent interpretation of the model and results. This minor change of the model conditions some change of the other parameter values.

Equations (7–9) constitute the complete set for the macroscopic description of endogenous agent dynamics and together with Eq. (6) constitute a model of financial markets. Model simulation is based on numerical solution of Eqs. (7) and (8).

Distinctive feature of this particular approach is its analytical tractability in the form of SDEs ((7)-(8)). As was shown in [52], Eq. ((7)) written for the new variable in the region of high values of variable belongs to the class of nonlinear SDE’s, reproducing power-law statistics: PDF and PSD [53, 35]. Furthermore, these equations exhibit a fascinating scaling property [35]: the scaling of variable is equivalent to the scaling of time , where is the exponent of multiplicative noise term. This lies in the background of relation between power-law stationary PDF, , and PSD of , , where the general class of SDE, just with two parameters and together with related exponent of PSD for , , can be written as

| (10) |

The necessary condition for Eq. (10) is , see Eqs. (8, 9) in [54] for the corresponding Fokker-Planck equation and its steady-state solution. Models in finance usually consider the case and only rarely the case [37]. Our herding based consideration belongs to the second one with the best fit to the empirical data in the region . Note that introducing variable trading activity of agents into Eq. (7) [52], we strengthen the non-linearity of the basic stochastic differential equation (10), increasing the exponent of multiplicativity . The SDE (10) exhibits nearly the same statistical properties as proposed endogenous model considered without high frequency fluctuations of the chartists . The main parameters of this power-law behavior can be written as follows [52]:

| (11) |

As in this simplified representation of the model has a meaning of the long-term absolute return (volatility), its power law behavior is very informative about statistical properties of the proposed model. For example, the contribution of introduced feedback on trading activity may be recovered from the dependence of power-law exponents on , see Eqs. (11).

Understanding of the self-similarity and the long range dependence observed in the financial markets is usually based on the fractional Brownian motion [55, 56, 57]. Here we argue that the class of nonlinear stochastic differential equations (10) can serve as an alternative mechanism explaining the property of the long range dependence in the financial markets.

From our point of view, there are too many models based only on the endogenous dynamics of agents. First of all they are not realistic enough and in our approach it is impossible to adjust the both exponents of absolute return power-law behavior and to the empirical data with the same set of parameters. For the more realistic model it is necessary to combine exogenous and endogenous fluctuations of the markets. As exogenous one we consider the noise of order flow fluctuations.

We substitute the endogenous price , Eq. (6), calculated using Eqs. (7–9) for and , into Eqs. (1–2) to complete the model, which now includes the endogenous and exogenous fluctuations. It has been demonstrated [36] that the model now resembles versions of non-linear GARCH(1,1) models [58, 59]. The advantage of agent-based models over pure stochastic models is that their parameters are more closely related to real-world scenarios and real human behavior.

In the following we analyze the one minute, daily and monthly recorded time series. In numerical simulations we set 1/390th of a trading day as the smallest tick size , and individual returns are calculated between these ticks. We calculate the returns for long time periods , e.g., one day, by summing up the consecutive short-time returns .

To account for the daily pattern observed in real data in NYSE and FOREX, we introduce a time dependence [11] into parameter , i.e.,

| (12) |

where quantifies the width of intra-day fluctuations. Although the model is designed to reproduce the power-law behavior of absolute returns PDF and PSD, it also reproduces the statistical features observed in volatility return intervals.

3 Results

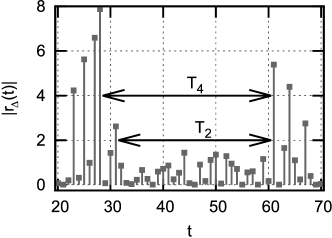

In this study we analyze the empirically established statistical properties of volatility return intervals in financial markets [12, 13, 14] and use the same definition of this financial variable shown in Fig. 1.

For two absolute return threshold values and the return intervals are and , respectively. They measure the time intervals between consecutive spikes of absolute returns that exceed threshold value , measured in units of standard deviation of the returns in the time series of the specific asset.

3.1 PDF and PSD of absolute return

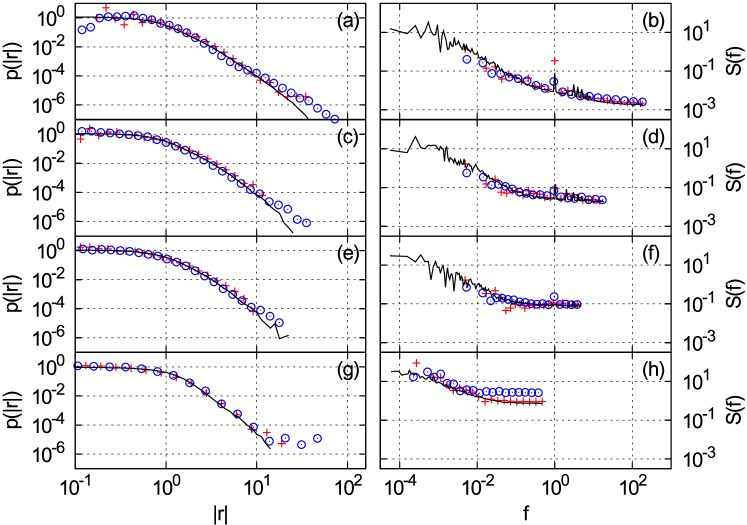

We test how well the model reproduces the empirical PDF and PSD of returns for NYSE stocks and FOREX exchange rates across a wide range of time intervals that range from 1/390th to 1 trading day. We set the model parameters to be day min., which is equivalent to 1 NYSE trading minute, and , which define the anti-symmetric distribution of , , which ensures the symmetric distribution of , which adjusts the PSDs of the empirical and model time series, and , which are empirical parameters defining the sensitivity of market returns and trading activity to the populations of agent states, , which is selected based on the empirical analyses [27, 28, 29, 51] and our numerical simulations confirm this choice as well, and , which is the main time-scale parameter that adjusts the model to fit the real time-scale. All the parameter values are kept constant throughout the analysis that follows.

Figs. 2(a)–2(f) compare high frequency NYSE and FOREX empirical data with the results of the model: numerical solution of Eqs. (1,2,6,7,8,9,12), see [11] for details. The data comprise a set of 26 stocks traded for 27 months from January 2005 and the USD/EUR exchange rate during a 10-year period beginning in 2000, and the empirical return series are normalized using return standard deviation . Figs. 2(a)–2(f) show that the model results are in a good agreement with the high frequency empirical PDFs and PSDs.

3.2 Contribution of various noises into the statistics of return intervals

The heuristic model of volatility was designed to reproduced first and second order statistics of absolute return in the financial markets [11]. The idea was to find the most simple version of consentaneous agent based and stochastic model capable to reproduce PDF and PSD of absolute return observed for various financial markets and assets. It means that we normalize all empirical return data by standard deviation to the same PDF of absolute return first and then define the set of model parameters to reproduce empirical (stylized) PDF and PSD with all peculiarities. This procedure more relies on the understanding of statistical properties arising from the class of stochastic differential equations (10) than on formal econometric procedures such as GMM or SMM. Such stylized peculiarities as PSD with two different values of exponent and spikes related to seasonality make the model much less appropriate for the formal consideration. The major achievement of such approach is ability to reproduce the same scaling of model and stylized statistical properties in very wide range of time windows .

Having such as simple as possible, but sophisticated enough model of absolute return, we demonstrate the capability of this model with the same set of parameters to reproduce a new class of empirical statistical properties: unconditional and conditional PDFs of high volatility return intervals. First of all, we demonstrate that all noises included into this model contribute to the PDF of absolute return intervals. As a first step, we analyze the long-term chartist fundamentalist dynamics, which can be described by ratio defined by Eq. (7) and having statistical properties arising from Eq. (10), which can be derived from Eq. (7) in the region of high values. Note that this is the main constituent of the long-term return fluctuations. Second, we switch on exogenous noise, but keep and constant. This allows us to investigate the interaction of the long-term endogenous dynamics with exogenous noise by analyzing and . Third, we switch on optimist-pessimists dynamics and analyze the absolute return series, keeping constant. And finally, we switch on intraday fluctuations and analyze full model with defined by Eq. (12).

Fig. 3 compares the scaled PDFs of absolute return intervals calculated with four different compositions of the model and for empirical data of NYSE stocks. In both sub-figures full model PDF of is in a good agreement with empirical data and one can observe considerable deviations from empirical data when part of noises is excluded from the model. In sub-figure (a), where , the contribution of optimist-pessimists dynamics , looks less noticeable as frequency of exogenous fluctuations is much higher than of and of fluctuations, nevertheless, the contribution of other noises is noticeable very well. In sub-figure (b), where trading day, PDFs of are different for all four compositions of the model. These and other numerical results confirm that all fluctuations accounted in the proposed model are required to reproduce statistics of empirical return intervals.

3.3 Return intervals of high frequency return series

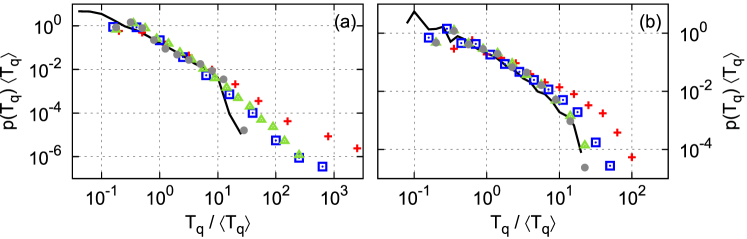

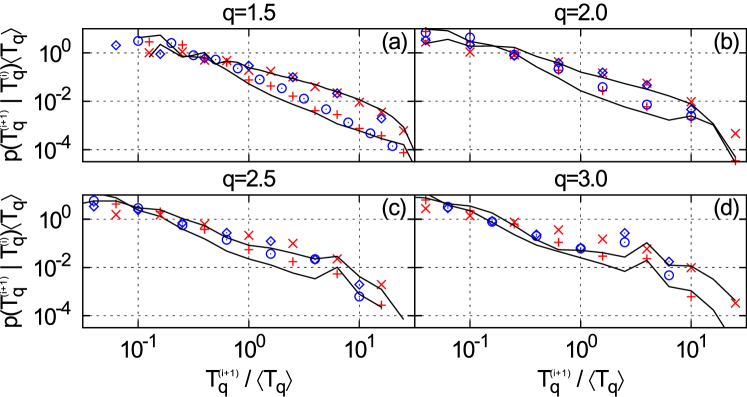

Our goal now is to explain, using model, the statistical properties of the return intervals of both stocks and currencies [12, 13]. Fig. 4 compares the unconditional PDFs of the model with the PDF obtained for 1/390th trading day returns of NYSE stocks and USD/EUR exchange on FOREX, and Fig. 5 compares the conditional distribution functions. These results support the model showing that it successfully reproduces both unconditional and conditional distribution functions. When values are comparable with the returns from their power-law part of PDF, , the power-law behavior of return intervals prevails . Notice that scaled unconditional PDFs of empirical as well as model given in Fig. 4 are nearly the same for each value of . We do observe this power-law behavior with exponent in the model even when we simplify it by replacing the whole model by stochastic dynamics of defined in Eq. (7) and the other noises are switched off. The cutoff of this power-law behavior for high values of appears when other noises are switched on again. Our numerical simulations of the model show that for values of , comparable with returns in very tail of their power-law PDF, the exogenous noise in Eq. (1) is responsible for the deviations from law, when as well as intra-day trading activity dynamics force the scaled PDF back to a power-law behavior. Such impact of the exogenous noise increases with higher values of time window .

For the threshold value , when and the conditional distribution functions are clearly different, indicating that there is a memory effect. Here is the index in the consecutive sequence, the 1/8th quantile and the 7/8th quantile of series. When threshold values are higher the conditional PDFs become closer and might overlap. Our numerical modelings confirm that the necessary condition for this memory effect is the presence of long term dynamics, Eq. (7), and exogenous noise, Eq. (1). The speculative dynamics and intra-day seasonality contribute to the dynamic behavior of the system, the persistence of a 3/2 power-law, and the memory effects. Note that all noises defined by the model are reflected in the PDFs of the volatility return intervals. The intraday fluctuations accounted in the model by Eq. (12) contribute to the high frequency conditional PDFs of return intervals, see Fig. 5, and help to achieve qualitative agreement with empirical data. Nevertheless, we have to acknowledge that the method we use to account the intraday fluctuations is oversimplified and some quantitative deviations from empirical data are present for the higher threshold values.

Our results support the empirical finding [12, 13, 14] that the PDF of the return intervals can be scaled to the same form common for different thresholds . Note that the difference in scaling exponent between what we obtained () and that obtained (2) in previous research is related to the use of different procedures for the return normalization, which in turn leads to different threshold choices. The thresholds used in previous papers are considerably lower than the ones we use in our model simulations and are outside the power-law portion of the return PDF. Because the contribution of the main SDE in Eq. (7) prevails over other noises only in the power-law portion of the return PDF, we choose higher values for threshold and also show the deviation from the law for . This lowest value, , demonstrates the transition to the regime in which the return intervals are extremely short and the dynamic complexity of the signal extremely high. We cannot consider the high frequency fluctuations in this regime as caused by a one-dimensional stochastic process because other noises are also contributing. Thus the exponent of the return intervals tends to values higher than . The empirical studies of return interval statistics described in Refs. [60, 15, 16] demonstrate the transition from a power-law to the exponential distribution of the unconditional PDF. Note that the authors of these studies also select lower values for the thresholds.

3.4 Return intervals of daily return series

We next analyze the daily returns data of 10 NYSE stocks obtained from Yahoo Finance, and also the USD historical exchange rates with currencies AU, NZ, POUND, CD, KRONER, YEN, KRONOR, and FRANCS traded on FOREX and obtained from the Federal Reserve. We first determine the appropriate scaling of the daily series of returns in the FOREX and NYSE exchanges. Because it is unlikely that those return series that exceed 50 years will be stationary, we normalize them by using a moving standard deviation procedure with a 5000-day time window. Each time series of all assets in both markets is normalized using this procedure. Fig. 2(g) compares the normalized empirical PDFs with the model PDF, and Fig. 2(h) shows the PSDs. Notice that PSD of stock absolute returns in high frequency area has a slightly higher value than model and currency exchange PSDs. There is good agreement of PSDs in low frequency area.

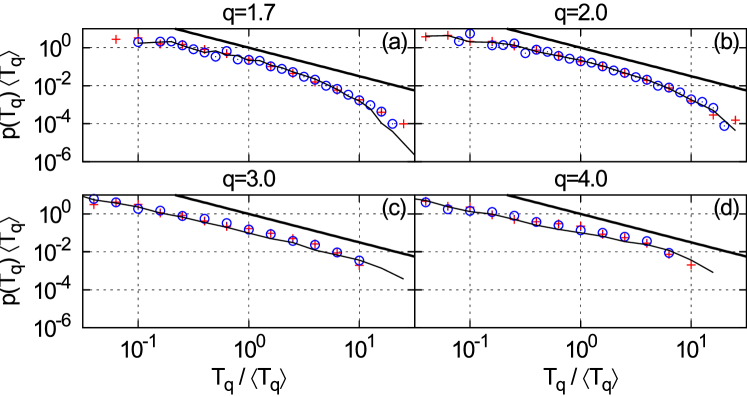

Fig. 6 shows that the unconditional PDFs of the daily scaled return intervals for NYSE stocks and FOREX exchange rates coincide for each threshold value. Note that in both NYSE and FOREX markets the unconditional PDFs agree with the model PDFs. This indicates a high degree of scaling in the return intervals. The theoretical framework provided by our model is able to explain this scaling. Note that for the highest threshold value the power-law exponent of the unconditional PDF in Fig. 6 deviates from and approaches .

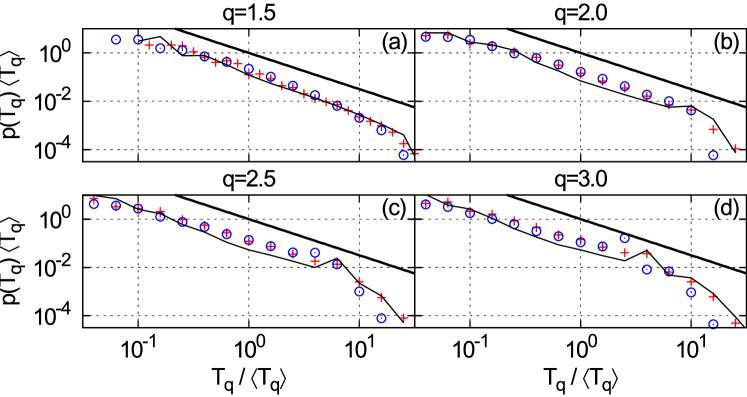

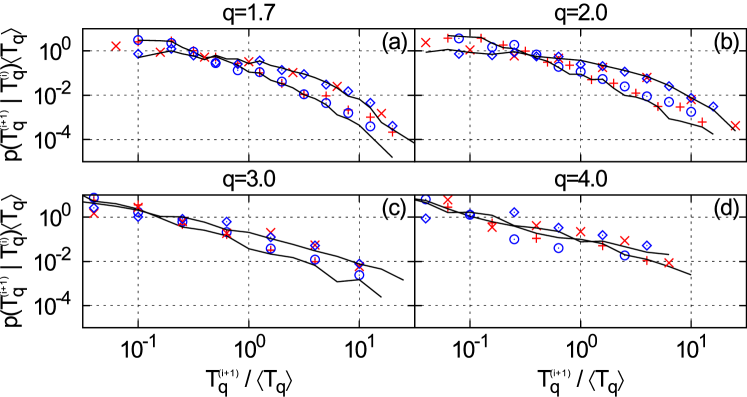

Fig. 7 shows that the conditional PDFs of the model agree with the conditional PDFs of the daily volatility return intervals records of both the NYSE and FOREX markets. When we increase the threshold, the conditional PDFs become closer and seem to overlap in both the empirical data and the model results, but we can not rule out that the seemingly overlap is due to the increased level of noise for high q.

3.5 Return intervals of monthly series for S&P500 index

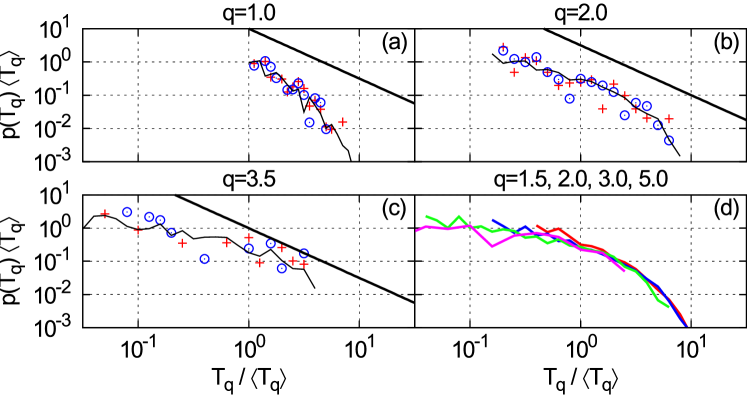

We use data from an S&P500 monthly series spanning a 145-year period provided by Shiller [34] to demonstrate the behavior of return intervals for extremely long time-scales. Fig. 8 shows that the above model, which reproduced the statistics of high frequency data, successfully mimics the PDFs of the volatility return intervals for even the longest time scales. We plot the empirical PDFs of return intervals for a nominal S&P500 and inflation adjusted series and compare them with the model series. The chosen threshold values range from 1.0 to 3.5 and represent several exponents of PDF. In the longest time-scales, the return interval distribution deviates from the power law for both the lowest and highest threshold values. Although the number of data points is limited, the model is able to capture these deviations and reproduce the behavior of index data.

3.6 Deviations from the 3/2 law

Because our model reproduces the statistical properties of empirical data for a wide range of assets and time-scales, we can use it to explain why increasing threshold causes deviations from the theoretical 3/2 power law and the seemingly absence of memory in the conditional PDFs of return intervals. In particular, the model allows us to gradually switch off various noises and analyze how this changes the statistical properties of the return intervals.

The model conditional PDFs and the empirical data conditional PDFs overlap at approximately the same threshold values at which the unconditional PDFs deviate from the power law, for example, see Fig. 6(d) and Fig. 7(d). This phenomenon is stronger for larger time scales, and we see no memory effects in the empirical S&P500 monthly series. Fig. 8(d) shows the unconditional PDFs calculated numerically for several values of , which resemble the exponential function discussed in Ref. [12] and obtained by reshuffling the absolute return time series. This indirectly confirms that the volatility return intervals for the S&P500 historical time series display no memory effect.

Our numerical simulations of the model suggest that the primary cause of the power-law behavior of the return intervals is the long-term SDE (see Eq. (7)). Other dynamic processes such as the speculative mood (see Eq. (8)) and the intra-day seasonality contribute to the stability of this phenomenon. Although the exogenous noise in Eq. (1) causes the unconditional PDFs to deviate from the 3/2 power law, this noise is a necessary condition for the memory effect to emerge in conditional PDFs. From our numerical simulations we conclude that the deviations from the power-law and disappearance of the memory effect occur when the stochastic component is stronger than the dynamic component. This process of domination occurs when the threshold value is so high that the dynamic processes cannot reach it when the noise is switched off. Note that threshold is measured in standard deviations of return, which grow approximately as . Dynamic processes quantified in of Eqs. (6) and (2) with this set of model parameters can only approach the threshold when its value is approximately equal to the standard deviation of the daily return time series. Thus when the thresholds are much higher the dynamic component is weaker than the stochastic component and the return intervals begin to deviate from the power law. The prevailing stochastic nature of the return time series destroys the memory effect, which requires that both dynamic and stochastic components be in the system.

4 Discussion

We have observed scaling and memory properties in the volatility return intervals in empirical data from the NYSE and the FOREX [12, 13, 14]. Our model is in agreement with the empirical return intervals that scale with the mean return interval as . The scaling function is consistent with the power-law form , which arises from the general theory of first-passage times in one-dimensional stochastic processes [61, 37]. We recover the same scaling form for all assets analyzed from the NYSE and FOREX markets for return definition times ranging from one minute to one month and for a wide range of thresholds , which represent the power-law component of the empirical return series. Our model also captures the deviations of the volatility return interval PDF exponent from the main value and explains the origin of these deviations.

We also have observed that at low values at the beginning of the power-law component of the empirical return series, for both one-minute and one-day periods, the conditional PDFs for and are different, and this indicates the presence of a memory effect. Our model suggests that this effect is caused by a complex interplay of all the noises included in the system. The necessary condition for the memory effect is the presence of long-term agent dynamics and exogenous noise. High threshold values seem to cause the memory effect to disappear as the stochastic component of the volatility begins to prevail.

When we compare the results of our model with the monthly data from the S&P500 we are able to extend our research on the scaling properties of the volatility return interval up to the natural limits of the phenomenon. We thus suggest that the deviations of the PDF exponent from are caused by an interplay between agent dynamics and exogenous noise. The standard deviations of return in the S&P500 monthly series are so high that the dynamic component of the system becomes negligible and the stochastic component dominates. This causes the exponential scaling functions of the return intervals and the disappearance of the memory effects.

We have found that the statistical and scaling properties such as the observable power-law behavior in the returns can be explained using non-linear stochastic modeling [11]. The extreme power-law scaling properties observed in all assets, markets, and time-scales can be explained by the scaling properties of a class of nonlinear stochastic differential equations described in detail in Refs. [53, 35]. Our model here is based on the herding interactions of agents, and its macroscopic version is derived as a system of stochastic equations. These equations might be the origin for the power-law properties of the power spectral density and signal autocorrelation represented by long-range memory.

We have also demonstrated that the model can be scaled for markets with trading hours of different durations and that the duration can be extended to a 24-hour day. This allows a general approach to empirical data scaling and the retrieval of the same power law properties in different markets and different assets.

Acknowledgments

This work was partially supported by Baltic-American Freedom Foundation and CIEE. The Boston University work was supported by NSF Grants PHY 1444389, PHY 1505000, CMMI 1125290, and CHE-1213217, and by DTRA Grant HDTRA1-14-1-0017 and DOE Contract DE-AC07-05Id14517.

References

- [1] J. P. Bouchaud, M. Potters, Theory of financial risks and derivative pricing, Cambridge University Press, New York, 2004.

- [2] D. Sornette, Why Stock Markets Crash: Critical Events in Complex Financial Systems, Princeton University Press, Princeton, USA, 2004.

- [3] M. Karsai, K. Kaski, A. L. Barabasi, J. Kertesz, Universal features of correlated bursty behaviour, NIH Scientific Reports 2 (2012) 397.

- [4] A. Chakraborti, I. M. Toke, M. Patriarca, F. Abergel, Econophysics review: I. empirical facts, Quantitative Finance 7 (2011) 991–1012.

- [5] X. Gabaix, Power laws in economics and finance, Annual Review of Economics 1 (2009) 255–293.

- [6] J. D. Farmer, M. Gallegati, C. Hommes, A. Kirman, P. Ormerod, S. Cincotti, A. Sanchez, D. Helbing, A complex systems approach to constructing better models for managing financial markets and the economy, European Physics Journal Special Topics 214 (2012) 295–324.

-

[7]

R. J. Shiller,

Speculative

asset prices, American Economic Review 104 (6) (2014) 1486–1517.

doi:10.1257/aer.104.6.1486.

URL http://www.aeaweb.org/articles.php?doi=10.1257/aer.104.6.1486 - [8] A. Kirman, Ants and nonoptimal self-organization: Lessons for macroeconomics, Macroeconomic Dynamics FirstView (2015) 1–21. doi:10.1017/S1365100514000339.

- [9] J. Campbell, A. Wen-Chuan, A. MacKinlay, The Econometrics of Financial Markets, Princeton University Press, Princeton, USA, 1996.

- [10] R. N. Mantegna, H. E. Stanley, Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press, 2000.

- [11] V. Gontis, A. Kononovicius, Consentaneous agent-based and stochastic model of the financial markets, PLoS ONE 9 (7) (2014) e102201.

- [12] K. Yamasaki, L. Muchnik, S. Havlin, A. Bunde, H. Stanley, Scaling and memory in volatility return intervals in financial markets, PNAS 102 (2) (2005) 9424–9428.

- [13] F. Wang, K. Yamasaki, S. Havlin, H. Stanley, Scaling and memory of intraday volatility return intervals in stock market, Physical Review E 77 (2006) 026117.

- [14] F. Wang, K. Yamasaki, S. Havlin, H. Stanley, Indication of multiscaling in the volatility return intervals of stock markets, Physical Review E 77 (2008) 016109.

- [15] J. Ludescher, C. Tsallis, A. Bunde, Universal behavior of the interoccurrence times between losses in financial markets: An analytical description, EPL 95 (2011) 68002.

- [16] J. Ludescher, A. Bunde, Universal behavior of the interoccurrence times between losses in financial markets: Independence of the time resolution, Physical Review E. 90 (2014) 062809.

- [17] W. A. Brock, S. N. Durlauf, Discrete choice with social interactions, Review of Economic Studies 68 (2001) 235–260.

- [18] C. Diks, R. van der Weide, Herding, a-synchronous updating and heterogeneity in memory in a cbs, Journal of Economic Dynamics & Control 29 (2005) 741–763.

- [19] F. Franke, R. Westerhoff, Structural stochastic volatiliy in asset pricing dynamics: Estimation and model contest, Journal of Economic Dynamics & Control 36 (2012) 1193–1211.

- [20] T. Lux, Estimation of an agent-based model of investor sentiment formmation in financial markets, Journal of Economic Dynamics & Control 36 (2012) 1284–1302.

- [21] D. Godlbaum, R. C. J. Zwinkels, An empirical examination of heterogeneity and switching in foreign exchange markets, Journal of Economic Behavior & Organization 107 (2014) 667–684.

- [22] Y. He, X.-Zh. Li, Testing of a market fraction model and power-law behaviour in the dax 30, Journal of Empirical Finance 31 (2015) 1–17.

- [23] T.-S. Jang, Identification of social interactions effects in financial data, Comput Econ 45 (2015) 207–238.

- [24] S. Alfarano, T. Lux, F. Wagner, Estimation of agent-based models: The case of an asymmetric herding model, Computational Economics 26 (1) (2005) 19–49.

- [25] S. Alfarano, T. Lux, F. Wagner, Time variation of higher moments in a financial market with heterogeneous agents: An analytical approach, Journal of Economic Dynamics and Control 32 (2008) 101–136.

- [26] A. Kononovicius, V. Gontis, Three state herding model of the financial markets, EPL 101 (2013) 28001.

- [27] X. Gabaix, P. Gopikrishnan, V. Plerou, H. E. Stanley, A theory of power law distributions in financial market fluctuations, Nature 423 (2003) 267–270.

- [28] J. D. Farmer, L. Gillemot, F. Lillo, S. Mike, A. Sen, What really causes large price changes, Quantitative Finance 4 (2004) 383–397.

- [29] X. Gabaix, P. Gopikrishnan, V. Plerou, H. E. Stanley, Institutional investors and stock market volatility, The Quarterly Journal of Economics (2006) 461–504.

- [30] V. Gontis, B. Kaulakys, Long-range memory model of trading activity and volatility, Journal of Statistical Mechanics P10016 (2006) 1–11.

- [31] V. Gontis, B. Kaulakys, Modeling long-range memory trading activity by stochastic differential equations, Physica A 382 (2007) 114–120.

- [32] B. Podobnik, D. Horvatic, A. Petersen, H. Stanley, Cross-correlations between volume change and price change, PNAS 106 (2009) 22079–22084.

- [33] J. A. Scheinkman, Speculation, Trading, and Bubbles, Columbia University Press, New York Chichester, West Sussex, 2014.

- [34] R. Shiller, Irrational Exuberance, Princeton University Press, Princeton, USA, 2015.

- [35] J. Ruseckas, B. Kaulakys, Scaling properties of signals as origin of 1/f noise, Journal of Statistical Mechanics (2014) P06004.

- [36] A. Kononovicius, J. Ruseckas, Nonlinear garch model and 1/f noise, Physica A 427 (2015) 74–81.

- [37] M. Jeanblanc, M. Yor, M. Chesney, Mathematical Methods for Financial Markets, Springer, Berlin, 2009.

- [38] R. Engle, Autoregresive conditional heteroscedasticity with estimates of the variance of united kingdom inflation, Econometrica 50 (4) (1982) 987–1008.

- [39] T. Bollerslev, Generalized autoregressive conditional heteroskedasticity, Journal of Econometrics 31 (1986) 307–327.

- [40] Y. Yura, H. Takayasu, D. Sornette, M. Takayasu, Financial knudsen number: Breakdown of continuous price dynamics and asymmetric buy-and-sell structures confirmed by high-precision order-book informationa, Physical Review E 92 (2015) 042811.

- [41] M. Ausloos, H. Dawid, U. Merlone, Spatial interactions in agent-based modelling, in: P. Commendatore, S. S. Kayam, I. Kubin (Eds.), Complexity and Geographical Economics: Topics and Tools, Springer, 2015, pp. 353–377.

- [42] A. P. Kirman, Ants, rationality and recruitment, Quarterly Journal of Economics 108 (1993) 137–156.

- [43] T. Lux, M. Marchesi, Scaling and criticality in a stochastic multi-agent model of a financial market, Nature 397 (1999) 498–500.

- [44] E. Samanidou, E. Zschischang, D. Stauffer, T. Lux, Agent-based models of financial markets, Reports on Progress in Physics 70 (2007) 409.

- [45] S. Cincotti, L. Gardini, T. Lux, New advances in financial economics: Heterogeneity and simulation, Computational Economics 32 (1) (2008) 1–2.

- [46] L. Feng, B. Li, B. Podobnik, T. Preis, H. E. Stanley, Linking agent-based models and stochastic models of financial markets, Proceedings of the National Academy of Sciences of the United States of America 22 (109) (2012) 8388–8393.

- [47] A. Lo, The adaptive markets hypothesis: market efficiency from an evolutionary perspective, The Journal of Portfolio Management 30 (2004) 15–29.

- [48] A. Lo, Reconciling efficient markets with behavioral finance: the adaptive markets hypothesis, Journal of Investment Consulting 7 (2) (2005) 21–44.

- [49] S. Galam, The invisible hand and the rational agent are behind bubbles and crashes, Chaos, Solitons & Fractals 88 (2016) 209 – 217, complexity in Quantitative Finance and Economics.

- [50] G. Dhesi, M. Ausloos, Modelling and measuring the irrational behaviour of agents in financial markets: Discovering the psychological soliton, Chaos, Solitons & Fractals 88 (2016) 119 – 125, complexity in Quantitative Finance and Economics.

- [51] R. Rak, S. Drozdz, J. Kwapien, P. Oswiecimka, Stock returns versus trading volume: is the correspondence more general?, Acta Physica Polonica B 44 (2013) 2035–2050.

- [52] A. Kononovicius, V. Gontis, Agent based reasoning for the non-linear stochastic models of long-range memory, Physica A 391 (4) (2012) 1309–1314.

- [53] B. Kaulakys, V. Gontis, M. Alaburda, Point process model of 1/f noise vs a sum of lorentzians, Physical Review E 71 (5) (2005) 051105.

- [54] J. Ruseckas, B. Kaulakys, 1/f noise from nonlinear stochastic differential equations, Physical Review E 81 (2010) 031105.

- [55] R. T. Baillie, Long memory processes and fractional integration in econoetrics, Journal of Econometrics 73 (1996) 5–59.

- [56] L. Giraitis, R. Leipus, D. Surgailis, Recent advances in arch modelling, in: G. Teyssiere, A. Kirman (Eds.), Long Memory in Economics, Springer, 2007, pp. 3–38.

- [57] L. Giraitis, R. Leipus, D. Surgailis, ARCH() models and long memory, in: T. G. Anderson, R. A. Davis, J. Kreis, T. Mikosh (Eds.), Handbook of Financial Time Series, Springer Verlag, Berlin, 2009, pp. 71–84.

- [58] R. Engle, T. Bollerslev, Modeling the persistence of conditional variances, Economic Reviews 5 (1986) 1–50.

- [59] M. L. Higgins, A. K. Bera, A class of nonlinear arch models, International Economic Review 33 (1992) 137–158.

- [60] M. Bogachev, J. Eichner, A. Bunde, Effect of nonlinear correlations on the statistics of return intervals in multifractal data sets, Physical Review Letters 99 (2007) 240601.

- [61] S. Redner, A guide to first-passage processes, Cambridge University Press, 2001.