Factorisable Multitask Quantile Regression

Abstract

A multivariate quantile regression model with a factor structure is proposed to study data with many responses of interest. The factor structure is allowed to vary with the quantile levels, which makes our framework more flexible than the classical factor models. The model is estimated with the nuclear norm regularization in order to accommodate the high dimensionality of data, but the incurred optimization problem can only be efficiently solved in an approximate manner by off-the-shelf optimization methods. Such a scenario is often seen when the empirical risk is non-smooth or the numerical procedure involves expensive subroutines such as singular value decomposition. To ensure that the approximate estimator accurately estimates the model, non-asymptotic bounds on error of the the approximate estimator is established. For implementation, a numerical procedure that provably marginalizes the approximate error is proposed. The merits of our model and the proposed numerical procedures are demonstrated through Monte Carlo experiments and an application to finance involving a large pool of asset returns.

KEY WORDS: Factor model; quantile regression; non-asymptotic analysis; multivariate regression; nuclear norm regularization.

JEL: C13, C38, C61, G17.

1. Introduction

In a variety of applications in economics, the interest is in the conditional quantiles of response variable (Koenker and Hallock, 2001). Quantile regression (Koenker and Bassett, 1978) is arguably one of the most popular methods for estimating the quantile of a response variable. However, in the situation of multivariate responses with common predictors, equation-by-equation quantile regression fails to capture the latent common structure. In econometrics literature, factor models are used for quantile regression with multiple responses (Ando and Tsay, 2011; Chen et al., 2015), but the factors are usually invariant to the quantile level, or do not include the information of exogenous predictors. This seems to contradict with the reality that the upper and lower quantiles are usually interpreted differently.

To fill this gap, we consider quantile level dependent factors formed by covariates , where is the quantile level. We assume that the conditional quantile of , the th component in the response vector , satisfies

| (1.1) |

where is the factor loading, and is assumed small and quantile level dependent. At first glance, Model (1.1) appears to be a factor-augmented regression model (FAR) of Stock and Watson (2002), but in fact they are drastically different. The predictors and the response variables are both generated by factors in the FAR model, but (1.1) assumes that the factors are functions of predictors, where the functions are unknown but non-random. Besides the factor models, Fan et al. (2015) consider transnormal models to allow for ultrahigh dimensional covariates.

From a practical perspective, the factors in (1.1) are unobservable, so computing the parameters can be challenging. To tackle this challenge, instead of pre-estimating the factors, we adopt a one-shot approach that simultaneously estimates the factors and the loadings. In particular, assume additionally that is linear in , that is, , where . The model (1.1) can be written as

| (1.2) |

where is the th column of , which is a coefficient matrix. Note that this implies , where linearly transforms to factors , and are the loadings defined in (1.1), with th column corresponding to output . Here, we normalize so that the model is identifiable. If the matrix in (1.2) is available, a factorization of gives factors and loadings simultaneously; see Section 2.2.

We observe that the rank of is the number of factors , so the rank of is small when is small. Therefore, estimation of should exploit this low rankness property, so that the estimation can be stable even when both and are large relative to . Recall that the rank corresponds to the number of nonzero singular values. Therefore, with a tuning parameter , an estimation with singular values regularization is considered

| (1.3) |

where denotes the nuclear norm, which is the sum of singular values, and

| (1.4) |

in which is the ”check function” (Koenker and Bassett, 1978). Note that is similar to the loss function used in Koenker and Portnoy (1990) for the low dimensional case, i.e. and do not diverge with . For mean regression, the nuclear norm penalty has been considered by many authors (Yuan et al., 2007; Bunea et al., 2011; Negahban and Wainwright, 2011; Koltchinskii et al., 2011; Maurer and Pontil, 2013; Maurer et al., 2016).

In (1.3), is the minimizer of a convex empirical risk. Its theoretical guarantee has been well studied (Koltchinskii, 2011) and its convergence rate is the best of all admissible estimators. Unfortunately, in reality, many off-the-shelf optimization methods only solves the optimization problem (1.3) approximately with an error . The optimization error may be nonzero for various reasons. For example, may be computed with a surrogate loss function of that is easier to optimize, or is the outcome of an iterative procedure, in which each iteration involves costly subroutines such as singular value decomposition. A question arises naturally: can estimates , as accurately as in some statistical sense?

The main goal of this paper is to provide an affirmative answer to the above question. In particular, we prove a non-asymptotic bound for , that has similar convergence rate as that of , under the condition that is smaller than an explicit upper bound depending on , and . This result is then be applied to prove that the estimator from a simple algorithm has the same convergence rate as , because its optimization error can be marginalized if parameters of the algorithm are well-chosen. Theoretical tools developed in this paper may be potentially useful for other convex problems where finding an exact optimizer is expensive and unrealistic.

In addition to the theoretical guarantees, we experiment the numerical procedure using Monte Carlo simulations with i.i.d. and dependent design. The outputs variables are generated from a two-piece normal distribution (Wallis, 2014), which has been used for the inference of inflation rate by central banks (Wallis, 1999). The results show that our numerical procedure can correctly identify the number of factors. For an empirical illustration of our method, we estimate the market systemic risk from a large pool of assets, and compute the exposure of each asset to the systemic risk. As our method is scalable to high dimensional data, we are able to overcome the computational barriers inherent in the existing studies (Adrian and Brunnermeier, 2016; White et al., 2015).

Lastly, we remark that multitask linear models have been considered in applications where the tails of distribution are the focus of interest. A recent paper Chao et al. (2018) explores the functional magnetic resonance imaging (fMRI) data with multitask expectile regression. They propose an iterative shrinkage algorithm, and show finite-sample convergence rate of the estimator while taking the optimization risk into account. The task undertaken in the current paper is much more challenging than Chao et al. (2018) from both computational and theoretical aspects, because of the non-smoothness of the quantile regression loss function. The model in this paper is more appropriate when response variables are heavy-tailed as moment conditions are not required here.

The rest of this paper is organized as follows. Section 2 discusses the numerical procedure for estimating the coefficient matrix and the factors and loadings. The selection of is also presented. Section 3 provides non-asymptotic analysis for and characterizes the sufficient condition on . The estimator for factors and loadings are also investigated. Results on Monte Carlo experiments are presented in Section 4, and an application on financial systemic risk is shown in Section 5. Section 6 concludes this paper. Appendix contains the detailed development of the algorithm in Section 2 and the proof of key theoretical results. Other proofs and technical details are shifted to the supplementary materials.

Notations. Notations associated with matrices will be used extensively in this paper. For a matrix , denote the singular values of : . and for the largest and smallest singular values of . Let be the spectral norm, be the nuclear norm and be the Frobenius norm. Denote and as the th column vector and the th row vector of . denotes the identity matrix. For vectors in , denote a matrix with being its th column. is the indicator function, which is one when the statement is true.

2. Approximate Estimator and Estimation

In this paper, the approximate estimator is assumed to satisfy

| (2.1) |

for some , where is the empirical risk in (1.3).

Section 2.1 presents an algorithm that computes an , and its optimization error will be characterized. Given , Section 2.2 describe the ways to estimate factors and loadings from . Section 2.3 discusses the choice of tuning parameter .

2.1. Coefficient Matrix

The proposed estimation procedure combines the Fast Iterative Shrinkage-Thresholding Algorithm (FISTA) of Beck and Teboulle (2009) and the smoothing technique of Nesterov (2005). Similar approach is previously applied to estimate regression models with penalties that induce complex structural sparsity (Chen et al., 2012). Comparing with other existing methods, this approach is more scalable to higher dimension than the semidefinite programming (SDP, Fazel et al. (2001); Srebro et al. (2005)), and is more stable than the non-convex reformulations (Rennie and Srebro, 2005; Weimer, Karatzoglou, Le and Smola, 2008; Weimer, Karatzoglou and Smola, 2008). See Ciliberto et al. (2017) for a recent account on the latter issue.

Specifically, the first step is to smooth in (1.4) with a surrogate function parameterized by a smoothing parameter (Nesterov, 2005). The surrogate loss function converges to the original loss function as . has a good property that is globally Lipschitz with constant , where is the design matrix. Next, FISTA (Beck and Teboulle, 2009) is applied on the modified loss function with step size . The procedure is summarized below, and the details are shifted to Section A.1.

-

Step 1:

Given , ;

-

Step 2:

Given and an initial estimator , for each , apply FISTA step on the minimization problem with step size . Return the last iterate .

The quantity is the key that controls both the smoothing quality and the step size of FISTA. Small leads to smaller smoothing error, but slows down the convergence. Therefore, there exists a tradeoff between smoothing error and the speed of convergence. In our simulation and data application, we typically set between and , and 3000 to 4000 iterations are usually sufficient for convergence.

The next theorem shows that is an approximate estimator in the sense of (2.1).

Theorem 2.1.

See Section S.1.2 in the supplementary material for a proof for Theorem 2.1. This theorem shows that the proposed numerical procedure provides an approximate optimizer in the sense of (2.1). The first term on the right-hand side of (2.2) is related to the smoothing error (Step 1), while the second term is related to the FISTA algorithm (Step 2). The quantile level enters (2.2) by the term , which increases when approaches the boundaries of the interval .

2.2. Factors number, factors and Loadings

Factorizing the true coefficient matrix allows to compute the factors and loadings for and at one shot. However, a potential problem here is that the decomposition is not unique. In particular, for any invertible matrix , we have . Therefore, to fix such a matrix , we apply the constraint in equation (2.14) on page 28 of Reinsel and Velu (1998): let the singular value decomposition , where the singular vectors associated with the zero singular values are not included in the expression, and . We set

| (2.3) |

In practice, using singular value decomposition , the factors and loadings can be estimated similarly as (2.3):

| (2.4) | ||||

where is the th largest singular value of .

The nuclear norm penalty in our loss function (1.3) shrinks most singular values to 0, so typically is small relatively to , and . Note that when is not small, the proposed method can still provably work, if the importance (measured by the singular values) of latter factors is small; see Remark 3.5 for details. In practice, the number of factors is estimated by for, e.g. , as adopted in this paper.

2.3. Tuning

It is crucial to appropriately select for the problem (1.3). We propose two ways to select . The first method is based on simulation. In particular, define the random variable

| (2.5) |

where , and are i.i.d. uniform (0,1) random variables for and , independent from . The random variable is pivotal conditioning on design , as it does not depend on the unknown . The formula in (2.5) arises from the subgradient . Set

| (2.6) |

where -quantile of conditional on , for close to 0, for instance . The constant 2 in (2.6) is mainly for the convenience of theoretical development, and it can be replaced by any constant greater than 1. In practice, when is large enough, the constant has little effect on the estimated number of factors, which is shown in our empirical study; see the left panel of Figure 5.1.

For estimating the number of factors, simulation study in Section 4 suggests that the tuning parameter given by (2.6) sometimes leads to too small . Alternatively, we propose to choose by minimizing the penalized testing error:

| (2.7) |

where we include the superscript to to emphasize its dependence on the tuning parameter , and is defined in (1.4). The expectation in (2.7) can be approximated by an empirical average with a testing data set, in which the estimator is computed with a training data set that has no overlap with the testing data, and the minimizer can be found by grid search. To select the grid points, the value in (2.6) can be used as the upper bound of the grid points. The performance of (2.7) will be evaluated by simulation in Section 4.2.

3. Theory

Section 3.1 develops high probability error bound for the approximate optimizer . The bound can be applied with Theorem 2.1 to derive a bound for the estimator proposed in Section 2.1. Section 3.2 characterizes the risk of the factors and loadings estimator.

3.1. Stochastic Risk of the Approximate Estimator

The following assumptions are introduced.

-

(A1)

(Sampling setting) Samples are i.i.d. copies of random vectors in with . , where is the th variable in . Moreover, for each , are i.i.d.

-

(A2)

(Covariates) is centered with covariance matrix . Assume the density function of exists. Suppose , and there exist constants , such that and the sample covariance matrix satisfies

(3.1) for a sequence .

-

(A3)

(Conditional densities) There exist constants , and such that

where is the conditional density function of on .

The i.i.d. condition in Assumption (A1) allows to bound some tail probability with sharp random matrix theory (see Remark S.2.6). This may be replaced by -dependent or weak dependent conditions, but the theory will be more complicated, which is left for future research. In Assumption (A2), is centered. can be assumed bounded by a constant (for example, p.2 of Maurer and Pontil (2013) and Theorem 1 of Yousefi et al. (2018)), but generally if each component of is bounded almost surely. Eigenvalue bounds in (3.1) hold when the components in have light tail; see, for example, Vershynin (2012b). (A3) is standard in quantile regression literature (Belloni and Chernozhukov, 2011). Note that decreases when approaches 0 or 1.

The next lemma gives the bound for , where is an matrix. The detailed proof can be found in the supplementary material.

Lemma 3.1.

See Section S.2.1 for a proof of Lemma 3.1. The constant is the sub-Gaussian norm of the binary random variable (Buldygin and Moskvichova, 2013, Theorem 3.1). Particularly, is a concave function of and is symmetric about . The maximum of is 1/4 at . In addition, [Eqn. (9) on p.36 of Buldygin and Moskvichova (2013)]. See Lemma 2.1 of Buldygin and Moskvichova (2013) for more on .

The next result presents a non-asymptotic risk bound of the approximate optimizer , when the optimization is well controlled. The key ingredient in its proof is the convexity arguments and a new tail probability bound for the empirical process , which builds on a sharp bound for the spectral norm of a partial sum of random matrices (Maurer and Pontil, 2013; Tropp, 2011). Define

| (3.8) |

where is a ”star-shaped” set of matrices defined in (S.2.5) [see more details there]. Note that for all .

Theorem 3.2.

Assume that (A1)-(A3) hold, and satisfies

| (3.9) |

where is defined in (3.7). Let for some constant , where is the upper bound of the optimization error in (2.1). For some , assume that satisfies

| (3.10) |

where is a large constant defined in (3.2). Then,

| (3.11) |

with probability at least , where is the prediction error; in addition,

| (3.12) |

See Section S.2.2 for a proof of Theorem 3.2. A sufficient condition for the bounds (3.11) and (3.12) of Theorem 3.2 is . We note that the conclusion of Theorem 3.2 holds regardless of the algorithm that computes , as long as the optimization error satisfies the bound. Corollary 3.4 provides an application of Theorem 3.2 on the estimator proposed in Section 2.1.

The error bound defined in (3.10) can be regarded as the stochastic error, which is not related to the optimization error . If and are fixed with respect to (low dimensional setting), . The quantity can be viewed as the actual number of unknown parameters, which has to be much smaller than . The covariates can influence through the condition number of the covariance matrix and . The estimation at close to 0 or 1 is challenging as in the denominator decreases when approaches 0 or 1.

The rate in (3.12) achieves the same (up to a constant) convergence rate in and to the multivariate regression for mean (Negahban and Wainwright, 2011; Koltchinskii et al., 2011)111Their regression problem (in mean) is analogous to our multivariate quantile regression setting by adjusting their to . See Example 1 on page 1075 of Negahban and Wainwright (2011). Note also that for a well-behaved in our setting., which is shown to be unimprovable up to a logarithmic factor in the minimax sense (Koltchinskii et al., 2011). Hence, we conjecture that is unimprovable up to a logarithmic factor under the multivariate quantile regression setting, as the convergence rate of quantile regression is typically the same (except for some constants) as the mean regression. If it were true, then is as good as , because the rate of both are unimprovable.

Remark 3.3 (Comment on the growth condition (3.10)).

In Theorem 3.2, the growth condition (3.10) guarantees the difference of population quantile loss is minorized by a quadratic function for inside a well-behaved set. Moreover, it can be easily seen that for all from the definition of in (3.8). Section S.3.1 discusses the details of the growth condition (3.10).

The selection of smoothing parameter has a significant impact on the algorithm in Section 2.1. Indeed, Corollary 3.4 below proves that estimator in Section 2.1 achieves the bound in Theorem 3.2, provided that the smoothing parameter and the number of iterations satisfy certain conditions.

Corollary 3.4.

Assume the conditions of Theorem 3.2 and in (3.10). Suppose in addition that the true coefficient matrix satisfies for some constant , . Let the initial estimator be in the algorithm in Section 2.1, and that

| (3.13) | ||||

| (3.14) |

then for , (3.11) and (3.12) hold with with probability at least , where the last bound in (3.14) uses (3.13).

See Section A.2 for a proof of Corollary 3.4. The key component of the proof is to verify that the optimization error of is less than . The constants in both (3.13) and (3.14) can be improved, and we adopt the current form for transparent exposition. In practice, the based on (3.13) may be too small, and larger usually performs better, as observed in the simulation analysis in Section 4.2.

3.2. Realistic Bounds for Factors and Loadings

The estimation error for the estimators for factors and loadings, defined in (2.4), will be stated in terms of the Frobenius error . Theorem 3.2 can be applied to find the explicit rate for the factors and loadings.

First we observe that by Mirsky’s theorem (see, for example, Theorem 4.11 on page 204 of Stewart and Sun (1990)), the singular values can be consistently estimated.

Lemma 3.6.

Let satisfy (2.1), then

| (3.15) |

Next, the error bounds for the factors and loadings are presented.

Theorem 3.7.

If the nonzero singular values of matrix are distinct, then with the choice of and in (2.4),

| (3.16) |

If, in addition, let the SVDs and , suppose , then

| (3.17) |

See Section S.2.4 for a proof for Theorem 3.7. The proof is based on a new Davis-Kahan type inequality of Yu et al. (2015). The inequalities in Theorem 3.2 can be applied to find the exact rate for the loadings and factors.

Remark 3.8 (Repeated singular values).

Theorem 3.7 is under the condition that the singular values for are distinct. If there are repeated singular values, then the corresponding singular vectors are not uniquely defined, and we can only obtain a bound for the ”canonical angle” (see, for example, Yu et al. (2015)) of the subspaces generated by the singular vectors associated with the repeated singular values.

4. Simulation

The performance of the numerical procedure in Section 2 on the factor quantile models will be checked via Monte Carlo experiments in this section. Section 4.1 presents the results on the Frobenius error. Section 4.2 presents the performance on estimating with i.i.d. data, while Section 4.3 focuses on time series data.

4.1. Estimation Error

Given two distinct matrices with nonnegative entries, and , the ouputs are simulated from the two-piece normal model (Wallis, 2014):

| (4.1) | ||||

where are i.i.d. independent of ; is the cdf of . follows a multivariate distribution with covariance matrix in which for . Simulation of follows by the method of Falk (1999). The number of simulation repetitions is 500.

Because the elements in are non-negative, the conditional quantile function of on for the distribution of is

| (4.2) |

It follows that for and for . In particular, and the -quantile of all responses are equal to 0, because for all . Hence, is the least interesting case, so it is not investigated.

To select and , we first fix and for :

-

I.

Symmetric model: with ;

-

II.

Asymmetrical model: with .

The entries of , and are selected randomly and fixed for all simulations, and their singular values are distinct. We shift the details on selecting these matrices to Section S.3.3.

The algorithm in Section 2.1 (specifics in Algorithm 1) is applied with =5%, 10%, 20%, 80%, 90% and 95% to compute the estimator for , where . We set and stop the algorithm when the change in the loss function is less than . The tuning parameter is selected by the simulation procedure (2.6). We compare with an oracle estimator, which is computed under the knowledge of the true . The performance of and the oracle estimator is measured by the Frobenius error to the true coefficient .

The results are reported in Table 4.1. The oracle estimator errors are generally smaller for all , and their standard deviation is also lower. When the model variance is larger (), the estimation of has greater error. The error of varies with : the error for or 0.95 is almost twice as large as those for and 0.8. For the two models, the errors of are similar when is less than 0.5. However, when is greater than 0.5, the errors of the asymmetric model is around times of that of the symmetric model. The oracle estimator also shows a similar pattern. The outcomes here are consistent with our theoretical analysis in Theorem 3.2, which predicts that the models with a larger rank and with closer to 0 or 1 have greater estimation errors. The prediction errors have similar pattern as the Frobenius error and are omitted for brevity.

| Symmetric | 60.995 | 48.746 | 34.302 | 33.973 | 48.375 | 60.604 |

|---|---|---|---|---|---|---|

| (0.253) | (0.227) | (0.209) | (0.202) | (0.217) | (0.247) | |

| Symmetric Or. | 57.261 | 44.926 | 30.006 | 29.853 | 44.735 | 57.007 |

| (0.191) | (0.152) | (0.116) | (0.118) | (0.152) | (0.184) | |

| Asymmetric | 60.978 | 48.724 | 34.289 | 60.487 | 85.997 | 108.310 |

| (0.263) | (0.220) | (0.207) | (0.539) | (0.567) | (0.820) | |

| Asymmetric Or. | 57.239 | 44.911 | 30.002 | 54.922 | 80.583 | 102.663 |

| (0.202) | (0.164) | (0.120) | (0.744) | (0.464) | (0.572) | |

| Symmetric | 118.245 | 93.419 | 64.289 | 63.634 | 92.519 | 117.365 |

| (0.570) | (0.420) | (0.387) | (0.382) | (0.372) | (0.438) | |

| Symmetric Or. | 113.636 | 88.781 | 58.913 | 58.593 | 88.365 | 113.099 |

| (0.427) | (0.338) | (0.238) | (0.221) | (0.301) | (0.378) | |

| Asymmetric | 118.259 | 93.434 | 64.291 | 120.338 | 170.904 | 217.185 |

| (0.530) | (0.412) | (0.380) | (1.151) | (1.273) | (1.547) | |

| Asymmetric Or. | 113.647 | 88.788 | 58.911 | 108.754 | 161.303 | 205.371 |

| (0.387) | (0.308) | (0.224) | (0.711) | (0.929) | (1.188) | |

4.2. Estimating the Number of Factors for i.i.d. Data

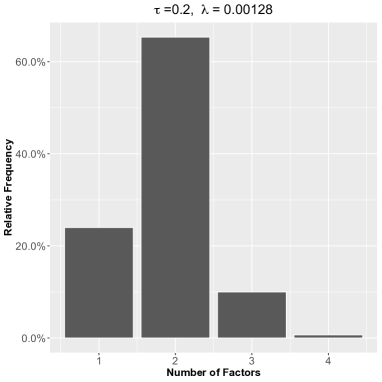

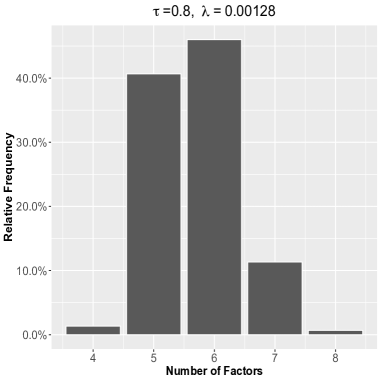

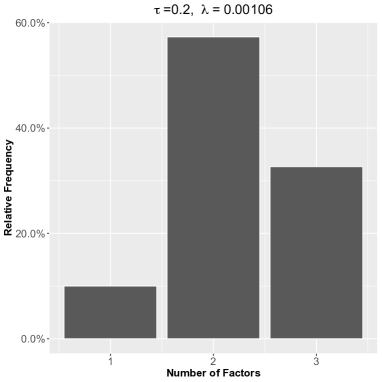

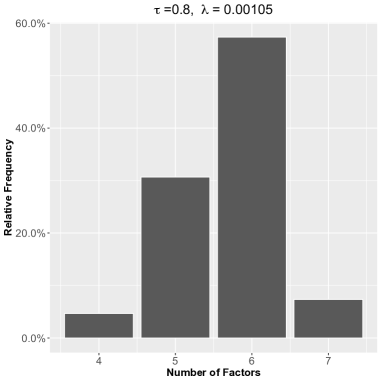

Using the same data generating process (4.1), this section shows the performance of estimating the number of factors. We will focus on the asymmetric case, as it is more challenging. Estimation performance for two representative quantile levels and are shown. Note the the number of factors are and .

The tuning parameter is selected by minimizing the penalized testing error in (2.7) through grid search. The value in (2.6) is used as the upper bound of the grid points. To compute the penalized testing error (2.7) at a given , we independently generate data 150 times and compute 150 . For each , a testing error is computed with a testing data set of size independent of the training data. Finally, we take an average of the 150 testing errors. The algorithm in Section 2.1 (Algorithm 1) is applied with iterations. The estimated number of factor is the number of singular values greater than .

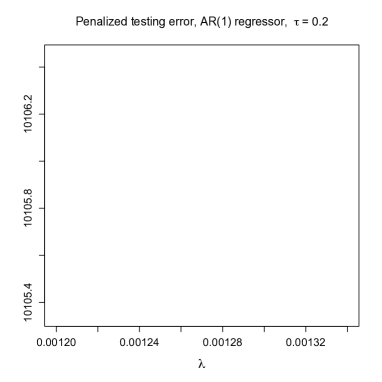

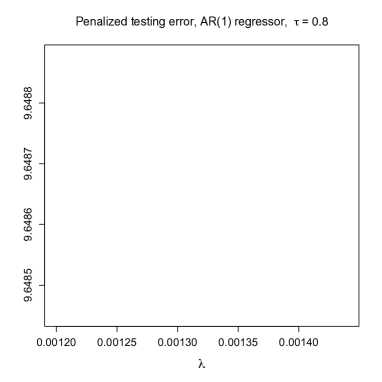

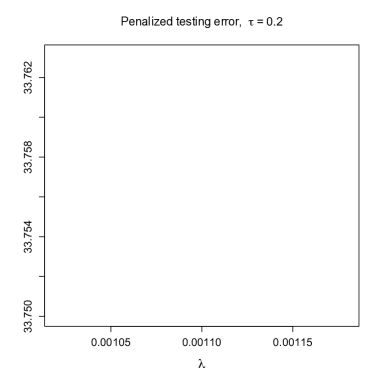

Figure 4.1 shows the relative frequency of the estimated number of factors and the estimated penalized testing error. The penalized testing error shows a quadratic shape, and there exists a minimum of the penalized testing error as a function of for both and 0.8. The that reaches the minimum for the two quantiles are essentially the same because they are symmetric about 0.5. For with the number of factor , the number of factors is correctly estimated over 50% of the time, and in the worst case scenario, the number of factors is misestimated by one. For with , which is greater than of . In this case, to ensure accurate estimation, the optimization error has to be small. For this purpose, (2.2) in Theorem 2.1 implies that one should select smaller and greater . Therefore, a slightly smaller is selected for , but appears to still be sufficient here. The bottom left panel of Figure 4.1 shows that the correct number of factors is identified almost 60% of the time, and at worst it is misestimated by two. We note that the tuned by (2.6) is 0.0189 which leads to a models with only one factor as observed by unpublished simulations.

4.3. Estimating the Number of Factors for Dependent Data

In this section, we consider a time dependent design

| (4.3) |

where is a multivariate Gaussian vector with mean zero and covariance . The matrices and are both , which are selected to imitate the temporal and cross-sectional dependent structure of the vector in (5.1) in the empirical analysis Section 5, where as in (5.1). is set to be a sparse coefficient matrix, which is estimated by a vector autoregressive model with norm penalty (Davis et al., 2016; Nicholson et al., 2017). Note that (4.3) is unstable, as four singular values of are greater than one. The details for selecting and are in Section S.5.

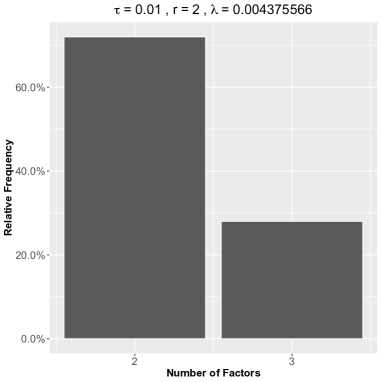

The output is generated as (4.1) with in (4.3). Here, we fix , while or 3. Under this design, the number of quantile factors for all because the distribution of in (4.3) is symmetric about the origin. Similar to the situation in Section 5, we set and . To selection , we adopt the simulation method in (2.6), which yields . Selecting by minimizing penalized testing error in (2.7) is feasible, but it is more computationally demanding. As will be shown, selected by (2.6) can yield accurate estimation in our setting. For all the numerical experiments in this section, and the number of iterations for the algorithm.

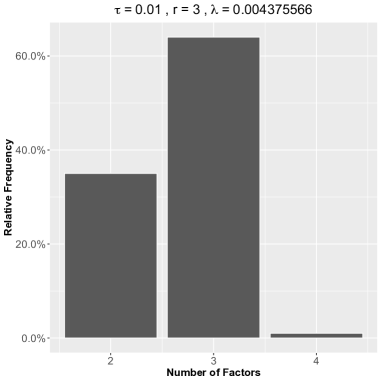

Figure 4.2 shows the performance of factor number estimation at . In 150 Monte Carlo simulations, our method can identify the correct number of factors in over 60% of the simulations. In the worst case scenario, the number of factors is misestimated by one. Note that the quantile level is more extreme than the that in Section 4.2 and is more relevant for the empirical analysis in Section 5. The results in Figure 4.2 show that our method still has a good performance even for extreme quantile level and time series data. We remark that additional numerical experiments with a simpler AR(1) structure is in Section S.6.

As a remark, although numerical results suggest our method is useful even for complex time series data, our theory does not apply to this case. Extension of the theory in this direction is nontrivial, so it is left for future research.

5. Empirical Analysis: Estimating the Systemic Risk

In the aftermath of the financial crisis that started in 2007, governments and supervisory authorities have come to realize the need to quantify the impact of systemic risk on financial institutions. Numerous studies have been made in this direction; see Bisias et al. (2012) or Brunnermeier and Oehmke (2013) for a survey. Quantifying the impact of systemic risk is inherently a high dimensional problem, as hundreds or sometimes thousands of financial institutions have to be included in the model in order to make it realistic. Unfortunately, due to excessive computational cost, the models in the existing studies are low dimensional in nature. For example, Adrian and Brunnermeier (2016) estimate pairwise spillover effect between two institutions by conditioning on a set of variables; White et al. (2015) estimate the impact of market shock by performing bivariate vector autoregression (VAR) between an institution and a pre-calculated proxy of the market shock. The proposed multitask quantile regression can fill this gap, as our method can easily scale up to hundreds of response variables and covariates. In addition, no proxy of the market shock needs to be pre-calculated, because the quantile factors obtained by our method summarize the market information that is most relevant to the downside risk.

We analyze the same set of daily stock closing prices as White et al. (2015), with the same time frame from January 1, 2000 to August 6, 2010. The dataset is downloaded from Dr. Manganelli’s personal website. See Table 1 of White et al. (2015) for a detailed breakdown of the stocks by sector and country, as well as their averaged market value and leverage (the ratio of short and long term debt over common equity) over the data period. There are financial institutions. The daily log-returns of the stock closing prices are used, and this results in .

Let be the asset return for institution at time , where and . For , consider the quantile for , where

| (5.1) |

and . The covariate captures the fact that the positive or negative lag stock returns have different influence to the return today, which is motivated by Engle and Manganelli (2004).

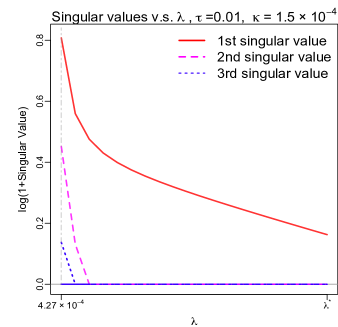

We estimate using the algorithm in Section 2.1 (equivalently, Algorithm 1) with two quantile levels and . The algorithm is performed with and we stop the algorithm when the change in the loss function is less than . The factors and loadings are estimated as (2.4) in Section 2.2. The tuning procedure in (2.6) yields for . Left panel in Figure 5.1 shows the estimated singular values for . Even when is smaller than by ten folds, which corresponds to the case of increasing or by ten folds, the estimated number of factor for is still one, which shows the robustness of the estimated . This result is similar for . This suggests that the number of factor is one for both and 0.99. For later discussion, we set for both and by symmetry.

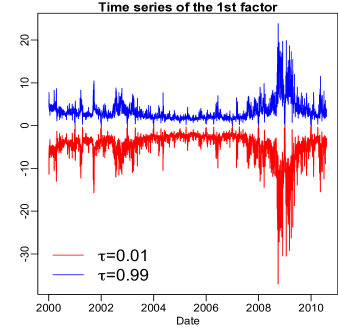

Figure 5.1 presents the estimated first factors at and 0.99. Both first factors and are volatile and moving away from 0 at the end of 2008 and in the first quarter of 2009, which corresponds to the periods of financial crisis.

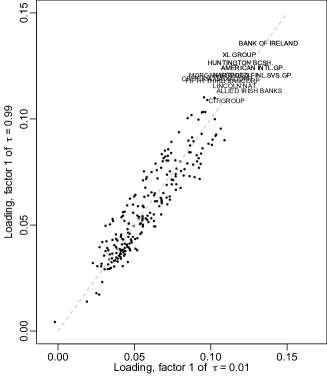

The left panel of Figure 5.2 is the ”tail to tail” plot with and 0.99, on which each point is a pair of loadings defined in (2.4) for th financial institution, . The values are all positive. The fact that they distribute around the 45 degree line suggests that the log-returns of these stocks are roughly equally associated to the two tail quantile factors, but the magnitude of their association to the factors varies dramatically. The points become more disperse and deviate from the 45 degree line in the northeast corner.

The right panel of Figure 5.2 plots the institutions based on their averaged market value (x-axis) and leverage (y-axis), and the color represents the magnitude of the factor loading of the corresponding financial institution. It shows that financial institutions with large market value and high leverage tend to have high loadings of the first left tail factor , as most red and yellow color points are concentrating in the northeastern part of the figure. This shows that they are more vulnerable to the market shock, and this is in line with the conclusion of White et al. (2015). Interestingly, the institutions that are more vulnerable to market shock seem to form clusters. It is an interesting future research to study the geographical and financial properties of the financial institutions in the same cluster.

Remark 5.1 (Extreme quantiles).

As is close to zero or one, the non-asymptotic bounds (3.11) and (3.12) in Theorem 3.2 become loose as increases, so the estimation may not be accurate. In the literature, extreme quantile is often characterized through the low extremal order or extremal rank (Chernozhukov, 1999, 2005; Chernozhukov et al., 2017). In particular, letting as and for some (respectively, for the right extreme quantile, by symmetry we only discuss left quantile in the following), classical asymptotic analysis breaks down if is small or equal to 0, and such scenario is regarded as ”extreme” quantile. Simulation study of asymptotic distribution in Chernozhukov (1999) suggests that might be large enough to regard the quantile as ”non-extreme”. In our application, extreme quantile issue may be mild as with . However, complete analysis for the extreme quantiles under multitask regression scenario is left for future research.

6. Conclusions and Future Works

In this paper, we consider a factor based multitask quantile regression model which allows the factors to vary with quantile levels, and the estimation of such model can be done with the nuclear penalization. Because the typical empirical risk minimizer cannot be efficiently computed due to non-smoothness of the loss function and the expensive subroutines such as singular value decomposition in the algorithm, a numerical procedure that approximately solves the empirical optimization problem is proposed and its theoretical guarantee is proved. Recommendations on how to tune the algorithm for provably accurate estimation are provided. Monte Carlo experiments show the performance of the numerical procedure and the ability to recover the number of factors, even for time series data and extreme quantiles. Potential application of our method is illustrated with a joint analysis on the financial risk of a large pool of stock returns of institutions with large market capitalization.

For future research, the readers may be aware that the model (1.2) could be misspecified for some applications. To remedy this, nonparametric models may be applied to function by regarding it as an element of a sieve space, and use the basis functions of the sieve space to represent as a series. Methods for estimating this nonparametric model can be derived from adapting our algorithm in Section 2. Illustrations of this idea using temperature data are presented in an earlier version of this paper (Chao et al., 2015, Section 7). Its theoretical analysis is left for future research. Other interesting research directions include showing that our bounds in Theorem 3.2 are unimprovable, and extending our framework to extreme quantiles.

APPENDIX

Details on the algorithm in Section 2.1 are provided in Section A.1. Section A.2 provides a proof of Corollary 3.4.

A.1. Details for the Numerical Procedure in Section 2.1

The Fast Iterative Shrinkage-Thresholding Algorithm (FISTA) of Beck and Teboulle (2009) is a popular method for optimizing the loss function consisted of two convex functions. However, one of the major challenge here is that the subgradient of is not Lipschitz, so the FISTA algorithm may not be stable. To resolve this problem, we apply the method of Nesterov (2005) to find a ”nice” surrogate for , as will be shown below.

Recall from (1.3) that the objective function to be minimized is

| (A.1) |

We introduce the dual variables :

| (A.2) |

See Section S.1.1 in the supplementary material for a proof of (A.2). To smooth this function, denote the matrix for , , we consider a smooth approximation to as in equation (2.5) of Nesterov (2005):

| (A.3) |

where , and is a smoothing regularization constant depending on and the desired accuracy. When , converges to . defined in (A.3) has Lipschitz gradient

| (A.4) |

where , performs component-wise truncation on a real matrix to the interval ; in particular,

Observe that (A.4) is similar to the subgradient of , where the operator applies component-wise to the matrix . The major difference lies in the fact that (A.4) replaces the discrete non-Lipschitz with a Lipschitz function .

Now, we replace the optimization problem involving in (A.1) by the one involving

| (A.5) |

where we recall the definition of in (A.3). Since the gradient of is Lipschitz, we may apply FISTA of Beck and Teboulle (2009) for minimizing (A.5). Define to be the proximity operator on :

| (A.6) |

where is the rectangular identity matrix with the main diagonal elements equal to 1, and the SVD . See Theorem S.4.2 in the supplementary material for more detail for the proximity operator.

Specific steps are summarized in Algorithm 1.

A.2. Proof of Corollary 3.4

To apply Theorem 3.2, it is enough to find a bound for the optimization error of that holds with high probability. Suppose the initial estimator is . The bound in (2.2) suggests that

| (A.7) |

where we apply the bound . It is sufficient to show that (I)+(II), and the desired conclusion will follow from Theorem 3.2. Using the bound on in (3.13), elementary calculation verifies that (I) in (A.7) is less than . Under the event that , it follows by elementary calculation that (II), and the corollary is proved.

It is left to show that with high probability. Recall that . The optimization error of can be estimated by

| (A.8) |

Therefore, is an approximate optimizer. The growth condition (3.10) with in the hypothesis of this corollary ensures (3.10) holds with . Hence, (3.12) in Theorem 3.2 yields

| (A.9) |

with probability at least .

References

- (1)

- Adrian and Brunnermeier (2016) Adrian, T. and Brunnermeier, M. K. (2016). CoVaR, American Economic Review 106(7): 1705–1741.

- Ando and Tsay (2011) Ando, T. and Tsay, R. S. (2011). Quantile regression models with factor-augmented predictors and information criterion, Econometrics Journal 14: 1–24.

- Beck and Teboulle (2009) Beck, A. and Teboulle, M. (2009). A fast iterative shrinkage-thresholding algorithm for linear inverse problems, SIAM Journal on Imaging Sciences 2(1): 183–202.

- Belloni and Chernozhukov (2011) Belloni, A. and Chernozhukov, V. (2011). -penalized quantile regression in high-dimensional sparse models, The Annals of Statistics 39(1): 82–130.

- Bhatia and Kittaneh (1990) Bhatia, R. and Kittaneh, F. (1990). Norm inequalities for partitioned operators and an application, Mathematische Annalen 287: 719–726.

- Bisias et al. (2012) Bisias, D., Flood, M., Lo, A. and Valavanis, S. (2012). A survey of systemic risk analytics, Office of Financial Research Working Paper .

-

Brunnermeier and Oehmke (2013)

Brunnermeier, M. K. and Oehmke, M. (2013).

Chapter 18 - bubbles, financial crises, and systemic risk, Vol. 2 of

Handbook of the Economics of Finance, Elsevier, pp. 1221 – 1288.

http://www.sciencedirect.com/science/article/pii/B9780444594068000184 - Buldygin and Moskvichova (2013) Buldygin, V. V. and Moskvichova, K. K. (2013). The sub-Gaussian norm of a binrary random variable, Theory of Probability and Mathematical Statistics 86: 33–49.

- Bunea et al. (2011) Bunea, F., She, Y. and Wegkamp, M. H. (2011). Optimal selection of reduced rank estimators of high-dimensional matrices, The Annals of Statistics 39(2): 1282–1309.

- Cai et al. (2010) Cai, J.-F., Candès, E. J. and Shen, Z. (2010). A singular value thresholding algorithm for matrix completion, SIAM Journal on Optimization 20(4): 1956–1982.

-

Chao et al. (2018)

Chao, S.-K., Härdle, W. K. and Huang, C. (2018).

Multivariate factorizable expectile regression with application to

fMRI data, Computational Statistics & Data Analysis 121: 1 –

19.

http://www.sciencedirect.com/science/article/pii/S0167947317302542 - Chao et al. (2015) Chao, S.-K., Härdle, W. K. and Yuan, M. (2015). Factorisable sparse tail event curves, arXiv preprint arXiv:1507.03833 .

- Chen et al. (2015) Chen, L., Dolado, J. J. and Gonzalo, J. (2015). Quantile factor models.

- Chen et al. (2012) Chen, X., Lin, Q., Kim, S., Carbonell, J. G. and Xing, E. P. (2012). Smoothing proximal gradient method for general structured sparse regression, The Annals of Applied Statistics 6(2): 719–752.

- Chernozhukov (1999) Chernozhukov, V. (1999). Conditional extremes and near-extremes: Estimation, inference, and economic applications, PhD thesis, Department of Economics, Stanford University.

-

Chernozhukov (2005)

Chernozhukov, V. (2005).

Extremal quantile regression, Ann. Statist. 33(2): 806–839.

https://doi.org/10.1214/009053604000001165 - Chernozhukov et al. (2017) Chernozhukov, V., Fernández-Val, I. and Kaji, T. (2017). Extremal quantile regression: An overview, ArXiv Preprint Arxiv 1612.06850 .

- Ciliberto et al. (2017) Ciliberto, C., Stamos, D. and Pontil, M. (2017). Reexamining low rank matrix factorization for trace norm regularization, ArXiv Preprint Arxiv 1706.08934 .

-

Davis et al. (2016)

Davis, R. A., Zang, P. and Zheng, T. (2016).

Sparse vector autoregressive modeling, Journal of Computational

and Graphical Statistics 25(4): 1077–1096.

https://doi.org/10.1080/10618600.2015.1092978 - Engle and Manganelli (2004) Engle, R. and Manganelli, S. (2004). CAViaR: Conditional autoregressive value at risk by regression quantiles, Journal of Business & Economic Statistics 22: 367–381.

- Falk (1999) Falk, M. (1999). A simple approach to the generation of uniformly distributed random variables with prescribed correlation, Communications in Statistics - Simulation and Computation 28(3): 785–791.

- Fan et al. (2015) Fan, J., Xue, L. and Zou, H. (2015). Multi-task quantile regression under the transnormal model, Journal of the American Statistical Association .

- Fazel et al. (2001) Fazel, M., Hindi, H. and Boyd, S. P. (2001). A rank minimization heuristic with application to minimum order system approximation, Proceedings of the American Control Conference, pp. 4734–4739.

- Ji and Ye (2009) Ji, S. and Ye, J. (2009). An accelerated gradient method for trace norm minimization, Proceedings of the 26th International Conference on Machine Learning.

- Knight (1998) Knight, K. (1998). Limiting distributions for regression estimators under general conditions, The Annals of Statistics 26(2): 755–770.

- Koenker and Bassett (1978) Koenker, R. and Bassett, G. S. (1978). Regression quantiles, Econometrica 46(1): 33–50.

- Koenker and Hallock (2001) Koenker, R. and Hallock, K. F. (2001). Quantile regression, Journal of Economic Perspectives 15(4): 143–156.

- Koenker and Portnoy (1990) Koenker, R. and Portnoy, S. (1990). estimation of multivariate regressions, Journal of American Statistical Association 85(412): 1060–1068.

- Koltchinskii (2011) Koltchinskii, V. (2011). Oracle inequalities in empirical risk minimization and sparse recovery problems, Springer.

- Koltchinskii et al. (2011) Koltchinskii, V., Lounici, K. and Tsybakov, A. B. (2011). Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion, The Annals of Statistics 39(5): 2243–2794.

- Ledoux and Talagrand (1991) Ledoux, M. and Talagrand, M. (1991). Probability in Banach Spaces (Isometry and processes), Ergebnis der Mathematik und ihrer Grenzgebiete, Springer-Verlag.

-

Lovász and Vempala (2007)

Lovász, L. and Vempala, S. (2007).

The geometry of logconcave functions and sampling algorithms, Random Structures & Algorithms 30(3): 307–358.

https://onlinelibrary.wiley.com/doi/abs/10.1002/rsa.20135 - Lütkepohl (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis, 1st edn, Springer-Verlag Berlin Heidelberg.

- Maurer and Pontil (2013) Maurer, A. and Pontil, M. (2013). Excess risk bounds for multitask learning with trace norm regularization, JMLR: Workshop and Conference Proceedings 30: 1–22.

- Maurer et al. (2016) Maurer, A., Pontil, M. and Romera-Paredes, B. (2016). The benefit of multitask representation learning, Journal of Machine Learning Research 17: 1–32.

- Negahban et al. (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J. and Yu, B. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers, Statistical Science 27(4): 538–557.

- Negahban and Wainwright (2011) Negahban, S. N. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with nose and high-dimensional scaling, The Annals of Statistics 39(2): 1069–1097.

- Nesterov (2005) Nesterov, Y. (2005). Smooth minimization of non-smooth functions, Mathematical Programming 103(1): 127–152.

-

Nicholson et al. (2017)

Nicholson, W. B., Matteson, D. S. and Bien, J. (2017).

VARX-L: Structured regularization for large vector autoregressions

with exogenous variables, International Journal of Forecasting 33(3): 627 – 651.

http://www.sciencedirect.com/science/article/pii/S0169207017300080 - Reinsel and Velu (1998) Reinsel, G. C. and Velu, R. P. (1998). Multivariate Reduced-Rank Regression, Springer, New York.

-

Rennie and Srebro (2005)

Rennie, J. D. M. and Srebro, N. (2005).

Fast maximum margin matrix factorization for collaborative

prediction, Proceedings of the 22Nd International Conference on Machine

Learning, ICML ’05, ACM, New York, NY, USA, pp. 713–719.

http://doi.acm.org/10.1145/1102351.1102441 - Srebro et al. (2005) Srebro, N., Rennie, J. D. M. and Jaakkola, T. S. (2005). Maximum-margin matrix factorization, Proceedings of the Conference on Neural Information Processing Systems, pp. 1329–1336.

- Stewart and Sun (1990) Stewart, G. W. and Sun, J.-G. (1990). Matrix Perturbation Theory, Academic Press.

-

Stock and Watson (2002)

Stock, J. H. and Watson, M. W. (2002).

Macroeconomic forecasting using diffusion indexes, Journal of

Business & Economic Statistics 20(2): 147–162.

https://doi.org/10.1198/073500102317351921 -

Tibshirani (1996)

Tibshirani, R. (1996).

Regression shrinkage and selection via the lasso, Journal of the

Royal Statistical Society: Series B (Methodological) 58(1): 267–288.

https://rss.onlinelibrary.wiley.com/doi/abs/10.1111/j.2517-6161.1996.tb02080.x - Tropp (2011) Tropp, J. A. (2011). User-friendly tail bounds for sums of random matrices, Foundations of computational mathematics 12(4): 389–434.

- van der Vaart and Wellner (1996) van der Vaart, A. W. and Wellner, J. A. (1996). Weak convergence and empirical processes: with applications to statistics, Springer.

- Vershynin (2012a) Vershynin, R. (2012a). Compressed Sensing, Theory and Applications, Cambridge University Press, chapter 5, pp. 210–268.

- Vershynin (2012b) Vershynin, R. (2012b). How close is the sample covariance matrix to the actual covariance matrix?, Journal of Theoretical Probability 25(3): 655–686.

- Wallis (1999) Wallis, K. F. (1999). Asymmetric density forecasts of inflation and the Bank of England’s fan chart, National Institute Economic Review 167: 106–112.

- Wallis (2014) Wallis, K. F. (2014). The two-piece normal, binormal, or double Gaussian distribution: Its origin and rediscoveries, Statistical Science 29(1): 106–112.

-

Weimer, Karatzoglou, Le and Smola (2008)

Weimer, M., Karatzoglou, A., Le, Q. V. and Smola, A. J.

(2008).

COFI RANK - maximum margin matrix factorization for collaborative

ranking, in J. C. Platt, D. Koller, Y. Singer and S. T. Roweis

(eds), Advances in Neural Information Processing Systems 20, Curran

Associates, Inc., pp. 1593–1600.

http://papers.nips.cc/paper/3359-cofi-rank-maximum-margin-matrix-factorization-for-collaborative-ranking.pdf -

Weimer, Karatzoglou and Smola (2008)

Weimer, M., Karatzoglou, A. and Smola, A. (2008).

Improving maximum margin matrix factorization, Machine Learning

72(3): 263–276.

https://doi.org/10.1007/s10994-008-5073-7 - White et al. (2015) White, H., Kim, T.-H. and Manganelli, S. (2015). VAR for VaR: measuring systemic risk using multivariate regression quantiles, Journal of Econometrics 187: 169–188.

- Yousefi et al. (2018) Yousefi, N., Lei, Y., Kloft, M., Mollaghasemi, M. and Anagnastapolous, G. (2018). Local Rademacher complexity-based learning guarantees for multi-task learning, Journal of Machine Learning Research 19(1): 1385–1431.

- Yu et al. (2015) Yu, Y., Wang, T. and Samworth, R. J. (2015). A useful variant of the Davis–Kahan theorem for statisticians, Biometrika 102(2): 315–323.

- Yuan et al. (2007) Yuan, M., Ekici, A., Lu, Z. and Monteiro, R. (2007). Dimension reduction and coefficient estimation in multivariate linear regression, Journal of the Royal Statistical Society: Series B 69(3): 329–346.

SUPPLEMENTARY MATERIAL: FACTORISABLE

MUITITASK QUANTILE REGRESSION

Section S.1 presents the convergence analysis for the algorithm. Section S.2 provides details on the non-asymptotic risk analysis of . Section S.3 discusses technical detail and remarks. Section S.4 lists some auxiliary results.

Additional notations. For any two matrices , denotes the trace inner product given by . Define the empirical measure of by . For a function , and , define the empirical process . The subgradient for is the matrix

| (A.10) |

where

For the true coefficient matrix , and .

S.1: Proofs for Algorithmic Convergence Analysis

S.1.1. Proof of (A.2)

To see that this equation holds, note that for each pair of , when , , since is the largest ”positive” value in the interval . When , since is the smallest ”negative” value in the interval . This verifies the equation. ∎

S.1.2. Proof of Theorem 2.1

Recall the definition of and in (A.1), and in (A.5) and (A.3). We note a comparison property in (2.7) of Nesterov (2005), for an arbitrary ,

| (S.1.1) |

where

Recall that is a minimizer of defined in (A.1). It follows by (S.1.1) that for an arbitrary ,

| (S.1.2) |

where the first inequality is from the first inequality of (S.1.1), the second is the definition of the minimizer , and the third inequality is from the second inequality of (S.1.1). Recall that is a minimizer of , then (S.1.2) gives

| (S.1.3) |

where the first inequality is from the definition of as a minimizer of and the second inequality is from (S.1.2), which holds for an arbitrary matrix .

S.1.3. Technical Details for Theorem 2.1

Lemma S.1.2.

For any , can be expressed as .

Proof of Lemma S.1.2. One can show by elementary matrix algebra that

The proof is therefore completed. ∎

Lemma S.1.3.

For any , is a well-defined, convex and continuously differentiable function in with the gradient , where is the optimal solution to (A.3), namely

| (S.1.7) |

The gradient is Lipschitz continuous with the Lipschitz constant .

Proof of Lemma S.1.3. In view of Lemma S.1.2, we have from (A.3) that

| (S.1.8) |

matches the form in (2.5) on page 131 of Nesterov (2005), with their which is a continuous convex function, and their which maps from the vector space to the space (the model setting described below (2.2) on page 129 of Nesterov (2005)), and their . Therefore, applying Theorem 1 of Nesterov (2005), with , , the gradient , where is the optimal solution to (A.3):

and the Lipschitz constant of is , where is the spectral norm of (see line 8 on page 129 of Nesterov (2005)). Hence, the proof is completed. ∎

S.2: Proofs for Non-Asymptotic Bounds

Remark S.2.1.

S.2.1. Proof for Lemma 3.1

To prove the first statement, applying the same -net argument on the unit Euclidean sphere as in the first part of the proof of Lemma 3 in Negahban and Wainwright (2011) (page 6 to the beginning of page 7 in their supplemental materials), we obtain

| (S.2.3) |

To bound , first we show the sub-Gaussianity of . Theorem 3.1 of Buldygin and Moskvichova (2013) suggests that the sub-Gaussian norm of the th component of is

where denotes the sub-Gaussian norm. It follows by Lemma S.4.3 (Hoeffding’s inequality) that

We apply Lemma S.4.3 again to bound . Conditioning on , we have

where the second inequality follows from the fact that and on the event that (A2) holds.

To summarize, on the event that (A2) holds,

Therefore, for arbitrary , the event

| (S.2.4) |

has probability smaller than , as .

To prove the second statement, we note that the event in (S.2.4) has probability less than by setting .

∎

S.2.2. Proof for Theorem 3.2

Before we prove Theorem 3.2, we first define the ”support” of matrices by projections.

Definition S.2.2.

For with rank , the singular value decomposition of is . The support of is defined by in which and . Define the projection matrix on : in which ; , where . Denote and . For any matrix , define

Define for any ,

| (S.2.5) |

We note that nuclear norm is decomposable under the projection: for any , . This is analogous to the norm for vectors: for any vector and support , ; see Definition 1 on page 541 of Negahban et al. (2012). Moreover, the rank of is at most .

The shape of is not a cone when , but is still a star-shaped set. This set has a similar shape as the set defined in equation (17) on page 544 in Negahban et al. (2012). See also their Figure 1 on page 544.

To simplify the notations in this proof, let

| (S.2.6) | ||||

| (S.2.7) | ||||

| (S.2.8) | ||||

| (S.2.9) | ||||

| (S.2.10) |

Let the events

| (S.2.11) | |||

where ,

We will prove by contradiction. Suppose to the contrary that . Since minimizes (defined in (1.3)) and , we have

| (S.2.13) |

where we recall (2.1).

Observe that with probability by applying (3.9) and Lemma S.2.3. Hence, from (2.1),

| (S.2.14) |

Note the facts that

-

1.

is convex (unique optimum);

-

2.

is star-shaped (see Figure 1 of Negahban et al. (2012)).

Hence, can be replaced by and the strict inequality in (S.2.14) is maintained

It can be deducted from the last display that

By triangle inequality, on the set by Lemma S.2.4(ii). Applying the bound in obtains

Since , by Remark 3.3,

(where the second inequality is from (3.10); the last inequality will be shown in (S.2.18) below), invoking Lemma S.2.4 (i) to get the minorization

| (S.2.15) |

Rearranging terms to get

| (S.2.16) |

However, the right-hand side of (S.2.16) is strictly greater than 0 whenever

| (S.2.17) |

The right hand side of the last display is upper bounded by (by for all )

which leads to the in (S.2.12). We get a contradiction, so does not hold. Namely, .

To show (3.11), we will prove

| (S.2.18) |

where is defined in (3.10). To see this, first note that,

| (S.2.19) |

since and .

Elementary calculation shows that for ,

| (S.2.20) |

Under the condition that , ,

| (S.2.21) |

since , (as ).

Lastly, again from and (S.2.19),

| (S.2.22) |

where in the third inequality the fact (noted below Lemma 3.1, or in (K4) of Lemma 2.1 on p.35 of Buldygin and Moskvichova (2013)) is applied, where is defined in (3.6); in the last inequality, the fact is applied. Hence,

| (S.2.23) |

where the inequality follows by the facts:

| and from Lemma 3.1) | |||

Note that if , then the matrix and this case is excluded.

∎

S.2.3. Technical Details for Theorem 3.2

The following lemma asserts that the empirical error lies in the cone .

Lemma S.2.3.

Suppose and , where is the subgradient of defined in (A.10). Then for all . That is, for all .

Proof for Lemma S.2.3.

| (S.2.24) |

where the second inequality follows from the definition of subgradient:

and Hölder’s inequality; the third inequality is from the fact that and for any , (the discussion after Definition S.2.2) ; the fourth inequality is from the triangle inequality.

Lemma S.2.4.

Lemma S.2.5.

Proof for Lemma S.2.5. To simplify notations, let

| (S.2.27) |

Let be independent Rademacher random variables independent from and for all . Denote and as the conditional probability and the conditional expectation with respect to , given and . Denote

| (S.2.28) |

is a contraction in the sense that , and for all ,

| (S.2.29) |

First, we note that for any satisfying and ,

| (S.2.30) |

where the first equality and the second inequality follows from elementary computations and i.i.d. assumption (A1), the third inequality is a result of (S.2.29), and the last inequality applies (S.2.1) in Remark S.2.1.

To apply Lemma 2.3.7 of van der Vaart and Wellner (1996), we observe from Chebyshev’s inequality that for any ,

Taking , we have

Thus, applying Lemma 2.3.7 of van der Vaart and Wellner (1996), we have

| (S.2.31) |

Now we restrict the on the event on which (3.1) in (A2) holds, with . Applying Markov’s inequality, for an arbitrary constant , the right-hand side of (S.2.31) can be bounded by

| (S.2.32) |

Now recall (S.2.29), the comparison theorem for Rademacher processes (Lemma 4.12 in Ledoux and Talagrand (1991)) implies the right-hand side of (S.2.32) is bounded by

| (S.2.33) |

To obtain a bound for the right-hand side of (S.2.33), we note that

| (S.2.34) |

where the first inequality is from Hölder’s inequality, and the second inequality is elementary.

Now we apply random matrix theory to bound the right-hand side of (S.2.33). Using matrix dilations (see, for example Section 2.6 of Tropp (2011)), we have

| (S.2.35) |

Notice that the random matrix is self adjoint and symmetrically distributed conditional on . We now obtain

| (S.2.36) |

where the first inequality is from Lemma S.2.4(ii) and (S.2.34) and recall in (S.2.27), the second inequality follows from (S.2.35), Lemma S.2.4 (ii) (), and the fact that

The third inequality is by Theorem 3(ii) of Maurer and Pontil (2013) by the symmetric distribution of , where for a self adjoint matrix ,

From equation (2.4) on page 399 of Tropp (2011), for any and ,

where ”” means the is positive semidefinite for two matrices . From equation (2.8) on page 399 of Tropp (2011), the logarithm defined above preserves the order . Hence, (S.2.36) is bounded by

| (S.2.37) |

where the last inequality follows from a bound for the spectral norm for block matrices in equation (2) of Theorem 1 in Bhatia and Kittaneh (1990) (with Shatten- norm), and Assumption (A2).

Putting (S.2.37) into (S.2.32), we obtain

| (S.2.38) |

Minimizing the expression (S.2.38) with respect to gives

| (S.2.39) |

Taking

| (S.2.40) |

Notice that for large enough , so the symmetrization (S.2.31) is valid. Recall that . The proof is then completed. ∎

Remark S.2.6.

The Lemma 2.3.7 of van der Vaart and Wellner (1996) and Lemma 4.12 of Ledoux and Talagrand (1991) applied in the proof of Lemma S.2.5 require only independence in the random variables , without needing identical distribution. The random matrix theory applied in the proof may also be generalized to matrix martingales; see Section 7 of Tropp (2011) for more details.

Remark S.2.7.

It can be observed that Lemma S.2.5 is valid uniformly for any .

S.2.4. Proof of Theorem 3.7

In this proof, we abbreviate , , and , and by , , and , and .

To prove (3.16), since and , by Theorem 3 of Yu et al. (2015),

| (S.2.41) |

where by the fact that ,

Similar bound like (3.16) also holds for , by the discussion below Theorem 3 of Yu et al. (2015).

For a proof for inequality (3.17), by direct calculation,

| (S.2.42) |

where we apply the fact that . By assumption , . Apply Lemma 3.6 and the bound (S.2.41) with being replaced by to (S.2.42), then (3.17) is proved. Thus, the proof for this theorem is completed. ∎

S.3: Miscellaneous Technical Details

S.3.1. Detail on Remark 3.3

For (3.10) to hold, it is enough to have for all , where is a constant independent of , because

| (S.3.1) |

by the inequality for an arbitrary with . If is i.i.d. sampled from a log-concave density, then Theorem 5.22 of Lovász and Vempala (2007) implies for any . See also Design 1 on p.2 of the supplemental materials of Belloni and Chernozhukov (2011). This implies (3.10) as is small as .

S.3.2. Detail on Remark 3.5

We need some extra notations. Let and be two subspaces with dimension , let ; (defined similarly as in Example 3 on page 542 of Negahban et al. (2012)). For any matrix ,

where , , , and is a set of orthonormal basis for ; analogously, , , , and is a set of orthonormal basis for . Moreover, for any , .

It can be shown that when , the difference lies in the set

| (S.3.2) |

where . Under this situation, the recovery property of can be shown via similar argument as for Theorem 3.2 (possibly under more restrictive conditions), and we leave out the details.

S.3.3. Details for Generating matrices and in Section 4

Given , and are selected with the following procedure:

-

1.

Generate vectors and , where , and i.i.d. for , , ;

-

2.

Set the columns of and by and for , where , are independent random variables in for and .

In our simulation, the first two nonzero singular values for are and the rest singular value is 0. For , the first two nonzero singular values are and the rest is 0. For , the first six nonzero singular values are and the rest is 0.

S.4: Auxiliary Lemmas

Definition S.4.1.

Let with inner product and be the induced norm. a lower semicontinuous convex function. The proximity operator of , :

Theorem S.4.2 (Theorem 2.1 of Cai et al. (2010)).

Suppose the singular decomposition of , where is a rectangular diagonal matrix and and are unitary matrices. The proximity operator associated with is

| (S.4.1) |

where is the rectangular identity matrix with diagonal elements equal to 1.

Lemma S.4.3 (Hoeffding’s Inequality, Proposition 5.10 of Vershynin (2012a)).

Let be independent centered sub-gaussian random variables, and let . Then for every and every , we have

where is a universal constant.

Lemma S.4.4 (Hoeffding’s Inequality: classical form).

Let be independent random variables such that almost surely, then

S.5: Selecting the Matrix in Section 4.3

The in (4.3) is the coefficient estimator obtained by fitting a VAR(1) model (Lütkepohl; 2005) to the in (5.1), and is the sample covariance matrix from the residuals. Due to the high dimensionality (), the VAR model may be over-parameterized especially when the order is high, and straightforwardly estimating the VAR may yield unreliable estimates. Therefore, as suggested by multiple authors (e.g. Davis et al. (2016); Nicholson et al. (2017) and the references therein), we estimate the VAR model with the norm penalty, or Lasso (Tibshirani; 1996), to alleviate the problem of over-parameterization. Henceforth, the VAR model estimated with the Lasso penalty will be called Lasso-VAR. The computation can be carried out with the R package BigVAR (Nicholson et al.; 2017). The Lasso tuning parameter is selected optimally by the cross-validation procedure provided in the package.

To evaluate the adequacy of the VAR(1) model for the real data in (5.1), Table S.5.1 provides the 1-step-ahead mean square forecasting error (MSFE) of Lasso-VAR (see Eq. (12) of Nicholson et al. (2017)) with different lags. As it requires excessive computational time and resource for model estimation and cross-validation, the maximal order under consideration here is three. Lasso-VAR(3) has the smallest MSFE, but the difference between the models seems small, so we take Lasso-VAR(1). The MSFE of VAR with order selected by AIC or BIC (Lütkepohl; 2005; Nicholson et al.; 2017) is 2805 with optimal order of the both being 0, which is higher than that of Lasso-VAR as shown in Table S.5.1.

For a simple diagnosis of Lasso-VAR(1), we check the autocorrelation and partial autocorrelation function of each individual residual series. Autocorrelation and partial autocorrelation functions of some series are significant. However, increasing the order of the VAR model does not improve the situation. To our best knowledge, we are not aware of any literature on vector ARIMA models for high dimensional time series, which might provide a better fit of our data. Fitting a very high dimensional VAR like ours is very subtle. As the Lasso-VAR(1) has demonstrated competent forecasting performance as shown in Table S.5.1, we adopt Lasso-VAR(1). A full exploration of the time series structure of the data is left for future research.

| Order | 1 | 2 | 3 |

|---|---|---|---|

| Lasso-VAR MSFE | 2364.82 | 2353.075 | 2341.046 |

| % of active coef. | 3.9 | 2.836 | 2.381 |

| MSFE of VAR-AIC/BIC (optimal order = 0): 2805 | |||

S.6: Additional Numerical Results: AR(1) Model

In this section, we consider the same data generating model as (4.1) in Section 4.1, but now the regressor follows an AR(1) model

| (S.6.1) |

where follows the multivariate distribution with covariance matrix in which . Because is generated as (4.1), the true number of factors is 2 for and 6 for as in the i.i.d. case. The computational setting is the same as the i.i.d. case.

Figure S.6.1 shows the relative frequency of the estimated number of factors and the estimated penalized testing error when the regressors follow (S.6.1). It appears that the presense of time dependency slightly decreases the recovery accuracy, but the pattern of the penalized testing error and the estimation performance of the number of factors remain similar to the i.i.d. case in Section 4.2. However, for , smaller and greater than than those for are selected to ensure estimation accuracy, which is due to the fact that the true number of factors for is greater than that of .