A One-Sample Test for Normality with Kernel Methods

Abstract

We propose a new one-sample test for normality in a Reproducing Kernel Hilbert Space (RKHS). Namely, we test the null-hypothesis of belonging to a given family of Gaussian distributions. Hence our procedure may be applied either to test data for normality or to test parameters (mean and covariance) if data are assumed Gaussian. Our test is based on the same principle as the MMD (Maximum Mean Discrepancy) which is usually used for two-sample tests such as homogeneity or independence testing. Our method makes use of a special kind of parametric bootstrap (typical of goodness-of-fit tests) which is computationally more efficient than standard parametric bootstrap. Moreover, an upper bound for the Type-II error highlights the dependence on influential quantities. Experiments illustrate the practical improvement allowed by our test in high-dimensional settings where common normality tests are known to fail. We also consider an application to covariance rank selection through a sequential procedure.

1 Introduction

Non-vectorial data such as DNA sequences or pictures often require a positive semi-definite kernel [1] which plays the role of a similarity function. For instance, two strings can be compared by counting the number of common substrings. Further analysis is then carried out in the associated reproducing kernel Hilbert space (RKHS), that is the Hilbert space spanned by the evaluation functions for every in the input space. Thus embedding data into this RKHS through the feature map allows to apply linear algorithms to initially non-vectorial inputs.

Embedded data are often assumed to have a Gaussian distribution. For instance supervised and unsupervised classification are performed in [6] by modeling each class as a Gaussian process. In [32], outliers are detected by modelling embedded data as a Gaussian random variable and by removing points lying in the tails of that Gaussian distribution. This key assumption is also made in [37] where a mean equality test is used in high-dimensional setting. Moreover, Principal Component Analysis (PCA) and its kernelized version Kernel PCA [34] are known to be optimal for Gaussian data as these methods rely on second-order statistics (covariance). Besides, a Gaussian assumption allows to use Expectation-Minimization (EM) techniques to speed up PCA [33].

Depending on the (finite or infinite dimensional) structure of the RKHS, Cramer-von-Mises-type normality tests can be applied, such as Mardia’s skewness test [29], the Henze-Zirkler test [22] and the Energy-distance test [40]. However these tests become less powerful as dimension increases (see Table 3 in [40]). An alternative approach consists in randomly projecting high-dimensional objects on one-dimensional directions and then applying univariate test on a few randomly chosen marginals [24]. This projection pursuit method has the advantage of being suited to high-dimensional settings. On the other hand, such approaches also suffer a lack of power because of the limited number of considered directions (see Section 4.2 in [24]).

In the RKHS setting, [17] introduced the Maximum Mean Discrepancy (MMD) which quantifies the gap between two distributions through distances between two elements of an RKHS. The MMD approach has been used for two-sample testing [17] and for independence testing (Hilbert Space Independence Criterion, [20]). However to the best of our knowledge, MMD has not been applied in a one-sample goodness-of-fit testing framework.

The main contribution of the present paper is to provide a one-sample statistical test of normality for data in a general Hilbert space (which can be an RKHS), by means of the MMD principle. This test features two possible applications: testing the normality of the data but also testing parameters (mean and covariance) if data are assumed Gaussian. The latter application encompasses many current methods that assume normality to make inferences on parameters, for instance to test the nullity of the mean [37] or to assess the sparse structure of the covariance [39, 2].

Once the test statistic is defined, a critical value is needed to decide whether to accept or reject the Gaussian hypothesis. In goodness-of-fit testing, this critical value is typically estimated by parametric bootstrap. Unfortunately, parametric bootstrap requires parameters to be computed several times, hence heavy computational costs (i.e. diagonalization of covariance matrices). Our test bypasses the recomputation of parameters by implementing a faster version of parametric bootstrap. Following the idea of [26], this fast bootstrap method ”linearizes” the test statistic through a Fréchet derivative approximation and thus can estimate the critical value by a weighted bootstrap (in the sense of [8]) which is computationally more efficient. Furthermore our version of this bootstrap method allows parameters estimators that are not explicitly ”linear” (i.e. that consist of a sum of independent terms) and that take values in possible infinite-dimensional Hilbert spaces.

Finally, we illustrate our test and present a sequential procedure that assesses the rank of a covariance operator. The problem of covariance rank estimation is adressed in several domains: functional regression [9, 7], classification [41] and dimension reduction methods such as PCA, Kernel PCA and Non-Gaussian Component Analysis [3, 12, 13] where the dimension of the kept subspace is a crucial problem.

Here is the outline of the paper. Section 2 sets our framework and Section 3 introduces the MMD and how it is used for our one-sample test. The new normality test is described in Section 4, while both its theoretical and empirical performances are detailed in Section 5 in terms of control of Type-I and Type-II errors. A sequential procedure to select covariance rank is presented in Section 6.

2 Framework

Let be a measurable space, and denote a sample of independent and identically distributed (i.i.d.) random variables drawn from an unknown distribution , where is a set of distributions defined on .

In our framework, is a separable Hilbert space endowed with a dot product and the associated norm (defined by for any ). Our goal is to test whether is a Gaussian random variable (r.v.) of , which is defined as follows.

Definition 2.1.

(Gaussian random variable in a Hilbert space)

Let a measure space, a measurable space where is a Hilbert space, and a measurable map.

is a Gaussian r.v. of if is a univariate Gaussian r.v. for any .

Assuming that , there exists such that:

and a (finite trace) operator satisfying:

and are respectively the mean and the covariance operator of . The distribution of is denoted .

More precisely, the tested hypothesis is that follows a Gaussian distribution , where and is a subset of the parameter space . 111 The parameter space is endowed with the dot product , where is the space of Hilbert-Schmidt (finite trace) operators and for any complete orthonormal basis of . Therefore, for any , the tensor product is defined as the operator . For any and , the tensor product is the operator . Following [28], let us define the null hypothesis , and the alternative hypothesis where the subset of null-hypotheses is

The purpose of a statistical test of against is to distinguish between the null () and the alternative () hypotheses. It requires two elements: a statistic (which we define in Section 4.1) that measures the gap between the empirical distribution of the data and the considered family of normal distributions , and a rejection region (at a level of confidence ). is accepted if and only if . The rejection region is determined by the distribution of under the null-hypothesis such that the probability of wrongly rejecting (Type-I error) is controlled by .

3 The Maximum Mean Discrepancy (MMD)

Following [17] the gap between two distributions and on is measured by

| (3.1) |

where is a class of real valued functions on . Regardless of , (3.1) always defines a pseudo-metric 222 A pseudo-metric satisfies for any , , : (i) , (ii) , and (iii) . on probability distributions [36].

The choice of is subject to two requirements: (i) (3.1) must define a metric between distributions, that is

| (3.2) |

and (ii) (3.1) must be expressed in an easy-to-compute form (without the supremum term).

To solve those two issues, several papers [18, 19, 20] have considered the case when is the unit ball of a reproducing kernel Hilbert space (RKHS) associated with a positive semi-definite kernel .

Definition 3.1.

(Reproducing Kernel Hilbert space, [1]) Let be a positive semi-definite kernel, i.e.

with equality if and only if .

There exists a unique Hilbert space of real-valued functions on which satisfies:

-

•

,

-

•

.

is the reproducing kernel Hilbert space (RKHS) of .

Let be the norm of and denote the unit ball of . When , becomes a metric only for a class of kernels that are called characteristic.

Definition 3.2.

Most common kernels are characteristic: Gaussian kernels where , the exponential kernel and Student kernels where , to name a few. Several criteria for a kernel to be characteristic exist (see [36, 16, 11]).

Moreover taking enables to cast as an easy to compute quantity. This is done by embedding any distribution in the RKHS as follows.

Definition 3.3.

(Hilbert space embedding, Lemma 3 from [18])

Let be a distribution such that .

Then there exists such that for every ,

is called the Hilbert space embedding of in .

Thus can be expressed as the gap between the Hilbert space embeddings of and (Lemma in [18]):

| (3.3) |

(3.3) is called the Maximum Mean Discrepancy (MMD) between and .

Within our framework the goal is to compare the true distribution of the data with a Gaussian distribution for some . Hence the quantity of interest is

| (3.4) |

For the sake of simplicity, we use the notation

to denote the Hilbert space embedding of a Gaussian distribution.

4 Kernel normality test

This section introduces our one-sample test for normality based on the quantity (3.4). As said in Section 2, we test the null-hypothesis where is a subset of the parameter space. Therefore our procedure may be used as test for normality or a test on parameter if data are assumed Gaussian. The test procedure is summed up in Algorithm 1.

-

1.

Compute (Gram matrix).

- 2.

-

3.

-

(a)

Draw (approximate) independent copies of under by fast parametric bootstrap (Section 4.2).

-

(b)

Compute ( quantile of under ) from these replications.

-

(a)

4.1 Test statistic

As in [17], can be estimated by replacing with the sample mean

where is the empirical distribution. The null-distribution embedding is estimated by where and are appropriate and consistent (under ) estimators of and . This yields the estimator

which can be explicited by expanding the square of the norm and using the reproducing property of as follows

| (4.5) |

Proposition 4.1 ensures the consistency of the statistic (4.5).

Proposition 4.1.

Assume that is Gaussian where and are consistent estimators of . Also assume that and is a continuous function of on . Then is a consistent estimator of .

Proof.

First, note that exists since implies . By the Law of Large Numbers in Hilbert Spaces [23], -almost surely since . The continuity of (with respect to ) and the consistency of yield -a.s.. Finally, the continuity of leads to . ∎

The expressions for and in (4.5) depend on the choice of . Those are given by Propositions 4.2 and 4.3 when is Gaussian and exponential. Note that in these cases, the continuity assumption of required by Proposition 4.1 is satisfied.

Before stating Propositions 4.2 and 4.3, the following notation is introduced. For a symmetric operator with eigenexpansion , its determinant is denoted . For any , the operator is defined as .

Proposition 4.2.

(Gaussian kernel case) Let where . Then,

Proposition 4.3.

(Exponential kernel case) Let . Assume that the largest eigenvalue of is smaller than . Then,

For most estimators , the quantities provided in Propositions 4.3 and 4.2 are computable via the Gram matrix . For instance, asumme that are the classical estimators where and . Let and be respectively the identity matrix and the matrix whose all entries equal , and be the centered Gram matrix. Then for any ,

where denotes the determinant of a matrix and

where denotes the entry in the -th row and the -th column of a matrix.

4.2 Estimation of the critical value

Designing a test with confidence level requires to compute the quantile of the distribution under denoted by . Thus serves as a critical value to decide whether the test statistic is significantly close to or not, so that the probability of wrongly rejecting (Type-I error) is at most .

4.2.1 Classical parametric bootstrap

In the case of a goodness-of-fit test, a usual way of estimating is to perform a parametric bootstrap. Parametric bootstrap consists in generating samples of i.i.d. random variables (). Each of these samples is used to compute a bootstrap replication

| (4.6) |

where , and are the estimators of , and based on .

It is known that parametric bootstrap is asymptotically valid [38]. Namely, under ,

where and are i.i.d. random variables. In a nutshell, (4.6) is approximately an independent copy of the test statistic (under ). Therefore replications can be used to estimate the quantile of under the null-hypothesis.

However, this approach suffers heavy computational costs. In particular, each bootstrap replication involves the estimators . In our case, this leads to compute the eigendecomposition of the Gram matrices of size hence a complexity of order .

4.2.2 Fast parametric bootstrap

This computational limitation is alleviated by means of another strategy described in [26]. Let us consider in a first time the case when the estimators of and are the classical empirical mean and covariance and . Introducing the Fréchet derivative [14] at of the function

our bootstrap method relies on the following approximation

| (4.7) |

Since (4.7) consists of a sum of centered independent terms (under ), it is possible to generate approximate independent copies of this sum via weighted bootstrap [8]. Given i.i.d. real random variables of mean zero and unit variance and their empirical mean, a bootstrap replication of (4.7) is given by

| (4.8) |

Taking the square of the norm of (4.8) in and replacing the unknown true parameters and by their estimators and yields the bootstrap replication of

| (4.9) |

where

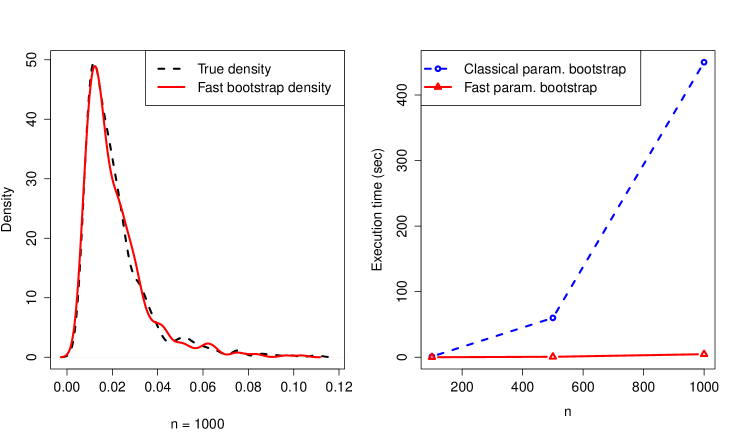

Therefore this approach avoids the recomputation of parameters for each bootstrap replication, hence a computationnal cost of order instead of . This is illustrated empirically in the right half of Figure 1.

4.2.3 Fast parametric bootstrap for general parameter estimators

The bootstrap method proposed by [26] used in Section 4.2.2 requires that the estimators can be written as a sum of independent terms with an additive term which converges to in probability. Formally, where , and . However there are some estimators which cannot be written in this form straightforwardly. This is the case for instance if we test whether data follow a Gaussian with covariance of fixed rank (as in Section 6). In this example, the associated estimators are (empirical mean) and where and are the eigenvalues and eigenvectors of the empirical covariance operator .

We extend (4.9) to the general case when and the estimators are not the classical . We assume that the estimators are functions of the empirical estimators and , namely there exists a continuous mapping such that

Under this definition, are consistent estimators of when . This kind of estimators are met for various choices of the null-hypothesis:

-

•

Unknown mean and covariance: and is the identity map ,

-

•

Known mean and covariance: and is the constant map ,

-

•

Known mean and unknown covariance: and ,

-

•

Unknown mean and covariance of known rank : and where is the rank truncation of .

By introducing , we get a similar approximation as in (4.7) by replacing the mapping with . This leads to the bootstrap replication

| (4.10) |

The validity of this bootstrap method is justified in Section 4.2.4.

Finally we define an estimator of from the generated bootstrap replications (assuming they are sorted)

where stands for the integer part. The rejection region is defined by

4.2.4 Validity of the fast parametric bootstrap

Proposition 4.4 hereafter shows the validity of the fast parametric bootstrap as presented in Section 4.2.3. The proof of Proposition 4.4 is provided in Section B.2.

Proposition 4.4.

Assume and are finite. Also assume that is continuously differentiable on .

If is true, then for each ,

-

(i)

-

(ii)

where and are random variables in .

If otherwise is false, is still true.

Furthermore, and are zero-mean Gaussian r.v. with covariances

By the Continous Mapping Theorem and the continuity of , Proposition 4.4 guarantees that the estimated quantile converges almost surely to the true one as , so that the type-I error equals asymptotically.

Note that in [26] the parameter subspace must be a subset of for some integer . Proposition 4.4 allows to be a subset of a possibly infinite-dimensional Hilbert space ( belongs to and belongs to the space of finite trace operators ).

Figure 1 (left plot) compares empirically the bootstrap distribution of and the distribution of . When , the two corresponding densities are superimposed and a two-sample Kolmogorov-Smirnov test returns a p-value of which confirms the strong similarity between the two distributions. Therefore the fast bootstrap method seems to provide a very good approximation of the distribution of even for a moderate sample size .

5 Test performances

5.1 An upper bound for the Type-II error

Let us assume the null-hypothesis is false, that is or . Theorem 5.1 gives the magnitude of the Type-II error, that is the probability of wrongly accepting . The proof can be found in Appendix B.3.

Before stating Theorem 5.1, let us introduce or recall useful notation :

-

•

,

-

•

,

-

•

,

where and denotes the Fréchet derivative of at . According to Proposition 4.4 and the continuous mapping theorem, corresponds to an order statistic of a random variable which converges weakly to (as defined in Proposition 4.4). Therefore, its mean tends to a finite quantity as . and do not depend on as well.

Theorem 5.1.

(Type II error)

Assume where -almost surely and is independent of .

Then, for any

| (5.11) |

where

and are absolute constants and only depends on the distribution of .

The first implication of Proposition (5.1) is that our test is consistent, that is

Furthermore, the upper bound in (5.11) reflects the expected behaviour of the Type-II error with respect to meaningful quantities. When decreases, the bound increases (alternative more difficult to detect). When (Type-I error) decreases, gets larger and has to be larger to get the bound. The variance term encompasses the difficulty of estimating and of estimating the parameters as well. In the special case when and are known, and the chain rule yields so that reduces to the variance of . As expected, a large makes the bound larger. Note that the estimation of the critical value which is related to the term in (5.11) does not alter the asymptotic rate of convergence of the bound.

Remark that assuming that is independent of is reasonable for a large , since and are asymptotically independent according to Proposition 4.4.

5.2 Empirical study of type-I/II errors

Empirical performances of our test are inferred on the basis of synthetic data. For the sake of brevity, our test is referred to as KNT (Kernel Normality Test) in the following.

One main concern of goodness-of-fit tests is their drastic loss of power as dimensionality increases. Empirical evidences (see Table 3 in [40]) prove ongoing multivariate normality tests suffer such deficiencies. The purpose of the present section is to check if KNT displays a good behavior in high or infinite dimension.

5.2.1 Finite-dimensional case (Synthetic data)

Reference tests. The power of our test is compared with that of two multivariate normality tests: the Henze-Zirkler test (HZ) [22] and the energy distance (ED) test [40]. The main idea of these tests is briefly recalled in Appendix A.1 and A.2.

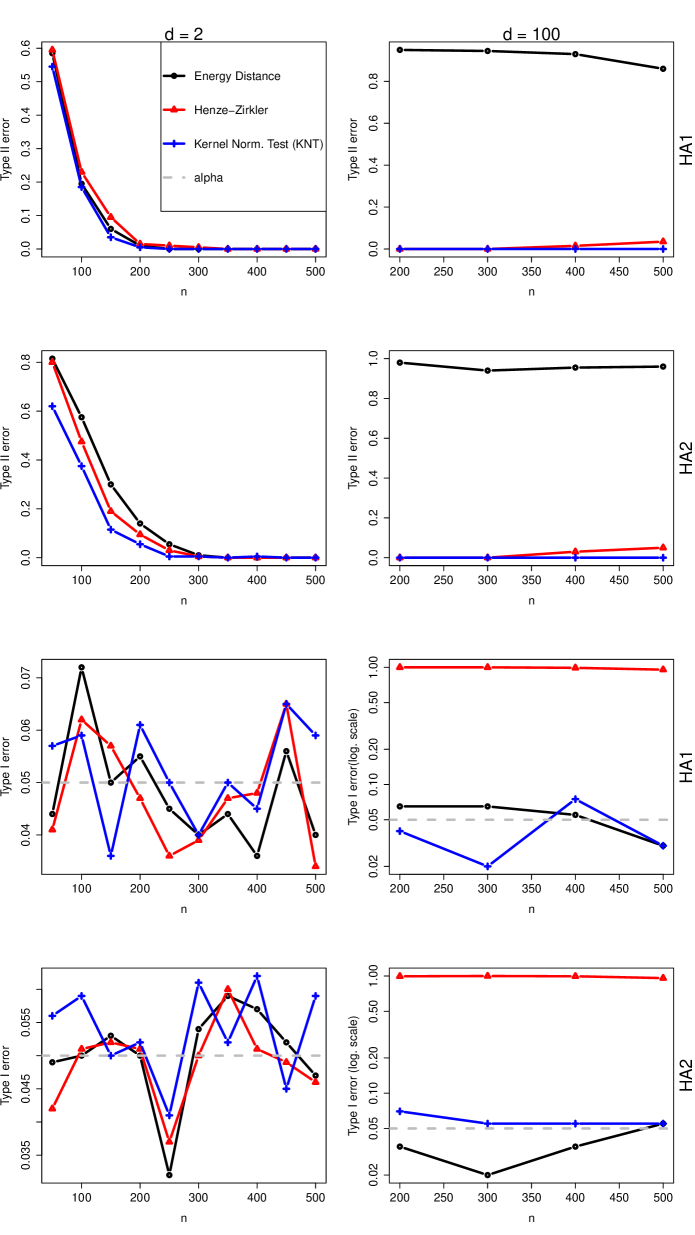

Null and alternative distributions. Two alternatives are considered: a mixture of two Gaussians with different means ( and ) and same covariance , whose mixture proportions equals either (alternative HA1) or (alternative HA2). Furthermore, two different cases for are considered: (small dimension) and (large dimension).

Simulation design. simulations are performed for each test, each alternative and each (ranging from to ). is set at for KNT. The test level is set at for all tests.

Results. In the small dimension case (Figure 2, left column), the actual Type-I error of all tests remain more or less around (). Their Type-II errors are superimposed and quickly decrease down to when . On the other hand, experimental results reveal different behaviors as increases (Figure 2, right column). Whereas ED test lose power, KNT and HZ still exhibits small Type-II error values. Besides, ED and KNT Type-I errors remain around the prescribed level while that of HZ is close to , which shows that its small Type-II error is artificial. This seems to confirm that HZ and ED tests are not suited to high-dimensional settings unlike KNT.

5.2.2 Infinite-dimensional case (real data)

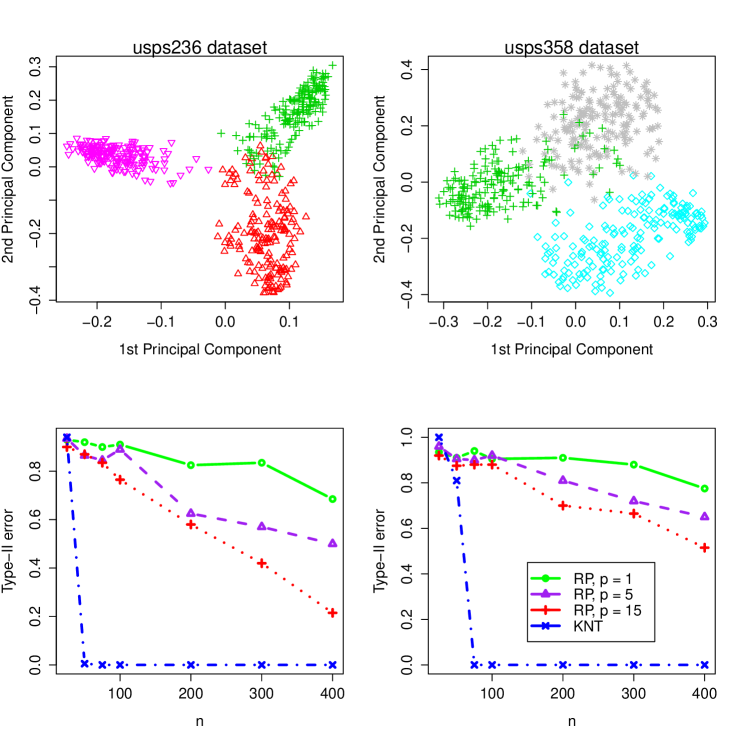

Dataset and chosen kernel. Let us consider the USPS dataset which consists of handwritten digits represented by a vectorized greyscale matrix (). A Gaussian kernel is used with . Comparing sub-datasets ”Usps236” (keeping the three classes ””, ”” and ””, observations) and ”Usps358” (classes ”3”, ”5” and ”8”, observations), the 3D-visualization (Figure 3, top panels) suggests three well-separated Gaussian components for “Usps236” (left panel), and more overlapping classes for “Usps358” (right panel).

References tests. KNT is compared with Random Projection (RP) test, specially designed for infinite-dimensional settings. RP is presented in Appendix A.3. Several numbers of projections are considered for the RP test : and .

Simulation design. We set and repetitions have been done for each sample size.

Results. (Figure 3, bottom plots) RP is by far less powerful KNT in both cases, no matter how many random projections are considered. Indeed, KNT exhibits a Type-II error near when is barely equal to , whereas RP still has a relatively large Type-II error when . On the other hand, RP becomes more powerful as gets larger as expected. A large enough number of random projections may allow RP to catch up KNT in terms of power. But RP has a computational advantage over KNT only when where the RP test statistic is distribution-free. This is no longer the case when and the critical value for the RP test is only available through Monte-Carlo methods.

6 Application to covariance rank selection

6.1 Covariance rank selection through sequential testing

Under the Gaussian assumption, the null hypothesis becomes

and our test reduces to a test on parameters.

We focus on the estimation of the rank of the covariance operator . Namely, we consider a collection of models such that, for each ,

Each of these models correspond respectively to the following null hypotheses

and the corresponding tests can be used to select the most reliable model. These tests are performed in a sequential procedure summarized in Algorithm 2. This sequential procedure yields an estimator defined as

or if all of the hypotheses are rejected.

Sequential testing to estimate the rank of a covariance matrix (or more generally a noisy matrix) is mentionned in [30] and [31]. Both of these papers focus on the probability to select a wrong rank, that is where denotes the true rank. The goal is to choose a level of confidence such that this probability of error converges almost surely to when .

There are two ways of guessing a wrong rank : either by overestimation or by underestimation. Getting greater than implies that the null-hypothesis was tested and wrongly rejected, hence a probability of overestimating at most equal to . Underestimating means that at least one of the false null-hypothesis was wrongly accepted (Type-II error). Let denote the Type-II error of testing with confidence level for each . Thus by a union bound argument,

| (6.12) |

The bound in (6.12) decreases to only if converges to but at a slow rate. Indeed, the Type-II errors grow with decreasing but converge to zero when . For instance in the case of the sequential tests mentionned in [30] and [31], the correct rate of decrease for must satisfy .

-

1.

Set and test

-

2.

If is rejected and , set and return to

-

3.

Otherwise, set the estimator of the rank .

6.2 Empirical performances

In this section, the sequential procedure to select covariance rank (as presented in Section 6.1) is tested empirically on synthetic data.

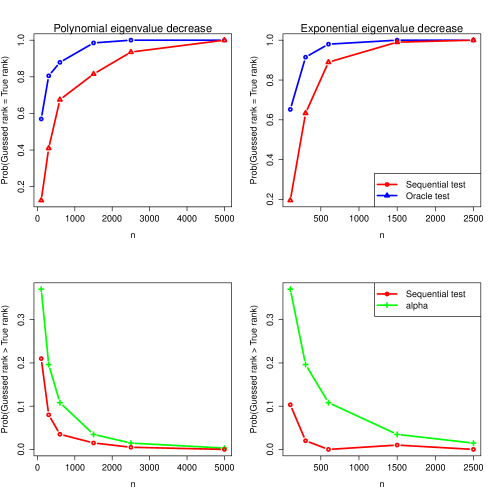

Dataset A sample of zero-mean Gaussian with covariance are generated, where ranges from to . is of rank and its eigenvalues decrease either polynomially ( for all ) or exponentially ( for all ).

Benchmark To illustrate the level of difficulty, we compare our procedure with an oracle procedure which uses the knowledge of the true rank. Namely, the oracle procedure follows our sequential procedure at a level defined as follows

where is the observed statistic for the -th test and follows the distribution of this statistic under . Hence is chosen such that the true rank is selected whenever it is possible.

Simulation design To get a consistent estimation of , the confidence level must decrease with and is set at . Each time, simulations are performed.

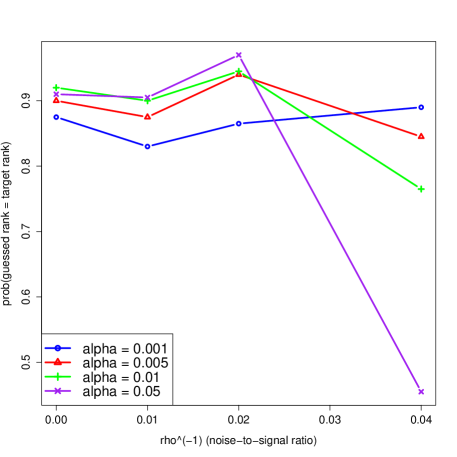

Results The top panels of Figure 4 display the proportion of cases when the target rank is found, either for our sequential procedure or the oracle one. When the eigenvalues decay polynomially, the oracle shows that the target rank cannot be almost surely guessed until . When , our procedure finds the true rank with probability at least and quickly catches up to the oracle as grows. In the exponential decay case, a similar observation is made. This case seems to be easier, as our procedure performs almost as well as the oracle when . In all cases, the consistency of our procedure is confirmed by the simulations.

The bottom panels of Figure 4 compare with the probability of overestimating (denoted by ). As noticed in Section 6.1, the former is an upper bound of the latter. But we must check empirically whether the gap between those two quantities is not too large, otherwise the sequential procedure would be too conservative and lead to excessive underestimation of . In the polynomial decay case, the difference between and is small, even when . The gap is larger in the exponential case but gets broader when .

6.3 Robustness analysis

In practice, none of the models is true. An additive full-rank noise term is often considered in the literature [10, 25]. Namely, we set in our case

| (6.13) |

where with and is the error term independent of . Note that the Gaussian assumption concerns the main signal and not the error term whereas usual models assume the converse [10, 25].

Figure 5 illustrates the performance of our sequential procedure under the noisy model (6.13). We set , , and where for . The noise term is where are i.i.d. Student random variables with degrees of freedom and is the signal-to-noise ratio.

As expected, the probability of guessing the target rank decreases down to as the signal-to-noise ratio diminishes. However, choosing a smaller level of confidence allows to improve the probability of right guesses for a fixed . without sacrificing much for smaller signal-to-noise ratios. This is due to the fact that each null-hypothesis is false, hence the need for a smaller (smaller Type-I error) which yields greater Type-II errors and avoids the rejection of all of the null-hypotheses.

7 Conclusion

We introduced a new normality test suited to high-dimensional Hilbert spaces. It turns out to be more powerful than ongoing high- or infinite-dimensional tests (such as random projection). In particular, empirical studies showed a mild sensibility to high-dimensionality. Therefore our test can be used as a multivariate normality (MVN) test without suffering a loss of power when gets larger unlike other MVN tests (Henze-Zirkler, Energy-distance).

If the Gaussian assumption is validated beforehand, our test becomes a general test on parameters. It is illustrated with an application to covariance rank selection that plugs our test into a sequential procedure. Empirical evidences show the good performances and the robustness of this method.

As for future improvements, investigating the influence of the kernel on the performance of the test would be of interest. In the case of the Gaussian kernel for instance, a method to optimize the Type-II error with respect to the hyperparameter would be welcomed. This aspect has just began to be studied in [21] when performing homogeneity testing with a convex combination of kernels.

Finally, the choice of the level for the sequential procedure (covariance rank selection) is another subject for future research. Indeed, an asymptotic regime for has been exhibited to get consistency, but setting the value of when is fixed remains an open question.

References

- [1] N. Aronszajn. Theory of reproducing kernels. May 1950.

- [2] J. Bien and R. J. Tibshirani. Sparse estimation of a covariance matrix. Biometrika, 98(4):807–820, 2011.

- [3] G. Blanchard, M. Sugiyama, M. Kawanabe, V. Spokoiny, and K.-R. Muller. Non-gaussian component analysis: a semi-parametric framework for linear dimension reduction. NIPS, 2006.

- [4] S. Boucheron, G. Lugosi, and P. Massart. Concentration Inequalities: A Nonasymptotic Theory of Independence. 2013.

- [5] S. Boucheron and M. Thomas. Concentration inequalities for order statistics. Electronic Communications in Probability, 17, 2012.

- [6] C. Bouveyron, M. Fauvel, and S. Girard. Kernel discriminant analysis and clustering with parsimonious gaussian process models. 2012.

- [7] E. Brunel, A. Mas, and A. Roche. Non-asymptotic Adaptive Prediction in Functional Linear Models. arXiv preprint arXiv:1301.3017, 2013.

- [8] M. D. Burke. Multivariate tests-of-fit and uniform confidence bands using a weighted bootstrap. Statistics & Probability Letters, 46(1):13–20, January 2000.

- [9] H. Cardot and J. Johannes. Thresholding projection estimators in functional linear models. Journal of Multivariate Analysis, 101(2):395–408, 2010.

- [10] Y. Choi, J. Taylor, and R. Tibshirani. Selecting the number of principal components: estimation of the true rank of a noisy matrix. arXiv preprint arXiv:1410.8260, 2014.

- [11] A. Christmann and I. Steinwart. Universal kernels on non-standard input spaces. In Advances in neural information processing systems, pages 406–414, 2010.

- [12] E. Diederichs, A. Juditsky, V. Spokoiny, and C. Schutte. Sparse non-Gaussian component analysis. Information Theory, IEEE Transactions on, 56(6):3033–3047, 2010.

- [13] E. Diederichs, A. Juditsky, A.and Nemirovski, and V. Spokoiny. Sparse non Gaussian component analysis by semidefinite programming. Machine learning, 91(2):211–238, 2013.

- [14] B. A. Frigyik, S. Srivastava, and M. R. Gupta. An introduction to functional derivatives. Dept. Electr. Eng., Univ. Washington, Seattle, WA, Tech. Rep, 1, 2008.

- [15] K. Fukumizu, A. Gretton, X. Sun, and B. Schölkopf. Kernel Measures of Conditional Dependence. In NIPS, volume 20, pages 489–496, 2007.

- [16] K. Fukumizu, B. Sriperumbudur, A. Gretton, and B. Schölkopf. Characteristic kernels on groups and semigroups. 2009.

- [17] A. Gretton, K. Borgwardt, M. Rasch, B. Schoelkopf, and A. Smola. A kernel method for the two-sample-problem. In B. Schoelkopf, J. Platt, and T. Hoffman, editors, Advances in Neural Information Processing Systems, volume 19 of MIT Press, Cambridge, pages 513–520, 2007.

- [18] A. Gretton, K.M. Borgwardt, M.J. Rasch, B. Schölkopf, and A. Smola. A kernel two-sample test. Journal of Machine Learning Research, March 2012.

- [19] A. Gretton, K. Fukumizu, Z. Harchaoui, and B. K. Sriperumbudur. A fast, consistent kernel two-sample test. 2009.

- [20] A. Gretton, K. Fukumizu, C. H. Teo, L. Song, B Schölkopf, and A. J. Smola. A kernel statistical test of independence. NIPS, 21, 2007.

- [21] A. Gretton, D. Sejdinovic, H. Strathmann, S. Balakrishnan, M. Pontil, K. Fukumizu, and B. K. Sriperumbudur. Optimal kernel choice for large-scale two-sample tests. In Advances in Neural Information Processing Systems, pages 1205–1213, 2012.

- [22] N. Henze and B. Zirkler. A class of invariant and consistent tests for multivariate normality. Comm. Statist. Theory Methods, 19:3595–3617, 1990.

- [23] J. Hoffmann-Jorgensen and G. Pisier. The law of large numbers and the central limit theorem in banach spaces. The Annals of Probability, 4:587–599, 1976.

- [24] R. Fraiman C. Matran J.A. Cuesta-Albertos, E. del Barrio. The random projection method in goodness of fit for functional data. June 2006.

- [25] J. Josse and F. Husson. Selecting the number of components in principal component analysis using cross-validation approximations. Computational Statistics & Data Analysis, 56(6):1869–1879, 2012.

- [26] I. Kojadinovic and J. Yan. Goodness-of-fit testing based on a weighted bootstrap: A fast large-sample alternative to the parametric bootstrap. Canadian Journal of Statistics, 40:480–500, 2012.

- [27] Michael R. Kosorok. Introduction to empirical processes and semiparametric inference. Springer Science & Business Media, 2007.

- [28] E.L. Lehmann and J. P. Romano. Testing Statistical hypotheses. Springer, 2005.

- [29] K.V. Mardia. Measures of multivariate skewness and kurtosis with applications. Biometrika, 57:519–530, 1970.

- [30] Z. Ratsimalahelo. Strongly consistent determination of the rank of matrix. Econometrics, 2003.

- [31] J.-M. Robin and R. J. Smith. Tests of rank. Econometric Theory, 16:151–175, 2000.

- [32] V. Roth. Kernel Fisher Discriminants for Outlier Detection. Neural Computation, 18(4):942–960, 2006.

- [33] S. Roweis. EM Algorithms for PCA and SPCA. In in Advances in Neural Information Processing Systems, pages 626–632. MIT Press, 1998.

- [34] B. Schölkopf, A. Smola, and K.-R. Müller. Nonlinear Component Analysis as a Kernel Eigenvalue Problem. Neural Computation, 10:1299–1319, 1997.

- [35] R. J. Serfling. Approximation Theorems for Mathematical Statistics. John Wiley & Sons, 1980.

- [36] B. K. Sriperumbudur, A. Gretton, K. Fukumiju, B. Schölkopf, and G. R. G. Lanckriet. Hilbert space embeddings and metrics on probability measures. Journal of Machine Learning Research, pages 1517–1561, 2010.

- [37] M.S. Srivastava, S. Katayama, and Y. Kano. A two-sample test in high dimensional data. Journal of Multivariate Analysis, pages 349–358, 2013.

- [38] W. Stute, W. G. Manteiga, and M. P. Quindimil. Bootstrap based goodness-of-fit-tests. Metrika, 40(1):243–256, 1993.

- [39] T. Svantesson and J. W. Wallace. Tests for assessing multivariate normality and the covariance structure of MIMO data. In Acoustics, Speech, and Signal Processing, 2003. Proceedings.(ICASSP’03). 2003 IEEE International Conference on, volume 4, pages IV–656. IEEE, 2003.

- [40] G.J. Szekely and R.L. Rizzo. A new test for multivariate normality. Journal of Multivariate Analysis, 93:58–80, 2005.

- [41] L. Zwald. Performances d’Algorithmes Statistiques d’Apprentissage: ”Kernel Projection Machine” et Analyse en Composantes Principales à Noyaux. 2005.

Appendix A Goodness-of-fit tests

A.1 Henze-Zirkler test

The Henze-Zirkler test [22] relies on the following statistic

| (A.14) |

where denotes the characteristic function of , is the empirical characteristic function of the sample , and with . The -hypothesis is rejected for large values of . Note that the sample must be whitened (centered and renormalized) beforehand.

A.2 Energy distance test

The energy distance test [40] is based on

| (A.15) |

which is called the energy distance, where and . Note that if and only if . The test statistic is given by

| (A.16) |

where (null-distribution). HZ and ED tests set the -distribution at where and are respectively the standard empirical mean and covariance. As for the Henze-Zirkler test, data must be centered and renormalized.

A.3 Projection-based statistical tests

In the high-dimensional setting, several approaches share a common idea consisting in projecting on one-dimensional spaces. This idea relies on the Cramer-Wold theorem extended to infinite dimensional Hilbert space.

Proposition A.1.

(Prop. 2.1 from [24]) Let be a separable Hilbert space with inner product , and denote two random variables with respective Borel probability measures and . If for every , weakly then .

[24] suggest to randomly choose directions from a Gaussian measure and perform a Kolmogorov-Smirnov test on for each , leading to the test statistic

| (A.17) |

where is the empirical cumulative distribution function (cdf) of and denotes the cdf of .

Since [24] proved too few directions lead to a less powerful test, this can be repeated for several randomly chosen directions , keeping then the largest value for . However the test statistic is no longer distribution-free (unlike the univariate Kolmogorov-Smirnov one) when the number of directions is larger than 2.

Appendix B Proofs

Throughout this section, (resp. ) denotes either or (resp. or ) depending on the context.

B.1 Proof of Propositions 4.2 and 4.3

Consider the eigenexpansion of where is a decreasing sequence of positive reals and where form a complete orthonormal basis of .

Let . The orthogonal projections are and for , and are independent. Let be an independent copy of .

Gaussian kernel case :

Let us first expand the following quantity

| (B.18) | ||||

We can switch the mean and the limit in (B.18) by using the Dominated Convergence theorem since for every

The second quantity is computed likewise

Exponential kernel case :

Let us first expand the following quantity

Expanding ,

| (B.19) |

We can switch the mean and the limit by using the Dominated Convergence theorem since

and

The integrability of is necessary to ensure the existence of the embedding related to the distribution of . As we will see thereafter, it is guaranteed by the condition .

For each ,

| (B.20) |

| (B.21) |

B.2 Proof of Theorem 4.4

The proof of Proposition 4.4 follows the same idea as the original paper [26] and broadens its field of applicability. Namely, the parameter space does not need to be a subset of anymore. The main ingredient for our version of the proof is to use the CLT in Banach spaces [23] instead of the multiplier CLT for empirical processes ([27], Theorem ).

We introduce the following notation :

-

•

denotes the true parameters

-

•

denotes the empirical parameters

-

•

For any and , .

-

•

and

Define the covariance operators , and as

From [23], the CLT is verified in a Hilbert space under the assumption of finite second moment (satisfied in our case since and by assumption). Therefore,

Introducing

we derive likewise

Since

the limit Gaussian processes and are independent.

Since is assumed continuous w.r.t. , we get by the continuous mapping theorem that

converges weakly to

To get the final conclusion of Proposition 4.4, we have to prove two remaining things.

First, under the assumption that ,

because converges weakly to a zero-mean Gaussian and by using the continous mapping theorem with the continuity of , a]nd of .

Secondly, whether is true or not,

we must check that both and converge -almost surely to .

Since by the continuous mapping theorem

and since

as -almost surely and is continuous w.r.t. , it follows

hence the conclusion of Proposition 4.4.

B.3 Proof of Theorem 5.1

The goal is to get an upper bound for the Type-II error

| (B.23) |

In the following, the feature map from to will be denoted as

Besides, we use the shortened notation for the sake of simplicity (see Section 5.1 for definitions).

-

1.

Reduce to a sum of independent terms

The first step consists in getting a tight upper bound for (B.23) which involve a sum of independent terms. This will allow the use of a Bennett concentration inequality in the next step.

Introducing the Fréchet derivative of at , is expanded as follows(B.24) where

and almost surely.

is a degenerate U-statistics so it converges weakly to a sum of weighted chi-squares ([35], page 194). converges weakly to a zero-mean Gaussian by the classic CLT as long as is finite (which is true since is bounded). It follows that becomes negligible with respect to when is large. Therefore, we consider a surrogate for the Type-II error (B.23) by removing with a negligible loss of accuracy.

-

2.

Apply a concentration inequality

-

3.

”Replace” the estimator with the true quantile in the bound

It remains to take the expectation with respect to . In order to make it easy, is pull out of the exponential term of the bound. This is done through a Taylor-Lagrange expansion (Lemma B.5).

The mean (with respect to ) of the right-side multiplicative term of (B.28) is bounded by

because of the Cauchy-Schwarz inequality.

On one hand, (Lemma B.2) implies and thus weakly where (that is almost surely for is a constant). Hencewhere denotes almost sure convergence.

Since the variable is bounded by the constant for every , it follows from the Dominated Convergence Theorem(B.29) On the other hand, Lemma B.2 provides

(B.30) so that an upper bound for the Type-II error is given by

(B.31) which one rewrites as

where

and , and .

Theorem 5.1 is proved.

B.4 Auxilary results

Lemma B.1.

(Bennett’s inequality, Theorem 2.9 in [4])

Let i.i.d. zero-mean variables bounded by and of variance .

Then, for any

| (B.32) |

Lemma B.2.

Lemma B.3.

If -almost surely and , then for any

| (B.34) |

Proof.

∎

Lemma B.4.

| (B.35) |

Proof.

∎

Lemma B.5.

Proof.

A Taylor-Lagrange expansion of order 1 can be derived for since the derivative of

is well defined for every (in particular, the left-side and right-ride derivatives at coincide).

Therefore equals

| (B.37) |

where

and because of the assumption .

For every , and then . It follows

and

Lemma B.5 is proved. ∎