Rapidly bounding the exceedance probabilities of high aggregate losses

Abstract

We consider the task of assessing the righthand tail of an insurer’s loss distribution for some specified period, such as a year. We present and analyse six different approaches: four upper bounds, and two approximations. We examine these approaches under a variety of conditions, using a large event loss table for US hurricanes. For its combination of tightness and computational speed, we favour the Moment bound. We also consider the appropriate size of Monte Carlo simulations, and the imposition of a cap on single event losses. We strongly favour the Gamma distribution as a flexible model for single event losses, for its tractable form in all of the methods we analyse, its generalisability, and because of the ease with which a cap on losses can be incorporated.

KEYWORDS: Event loss table, Compound Poisson process, Moment bound, Monte Carlo simulation

1 INTRODUCTION

One of the objectives in catastrophe modelling is to assess the probability distribution of losses for a specified period, such as a year. From the point of view of an insurance company, the whole of the loss distribution is interesting, and valuable in determining insurance premiums. But the shape of the righthand tail is critical, because it impinges on the solvency of the company. A simple measure of the risk of insolvency is the probability that the annual loss will exceed the company’s current operating capital. Imposing an upper limit on this probability is one of the objectives of the EU Solvency II directive.

If a probabilistic model is supplied for the loss process, then this tail probability can be computed, either directly, or by simulation. Shevchenko (2010) provides a survey of the various approaches. This can be a lengthy calculation for complex losses. Given the inevitably subjective nature of quantifying loss distributions, computational resources might be better used in a sensitivity analysis. This requires either a quick approximation to the tail probability or an upper bound on the probability, ideally a tight one. In this paper we present and analyse several different bounds, all of which can be computed quickly from a very general event loss table. By making no assumptions about the shape of the righthand tail beyond the existence of the second moment, our approach extends to fat-tailed distributions. We provide a numerical illustration, and discuss the conditions under which the bound is tight.

2 INTERPRETING THE EVENT LOSS TABLE

We use a rather general form for the Event Loss Table (ELT), given in Table I. In this form, the losses from an identified event are themselves uncertain, and described by a probability density function . That is to say, if is the loss from a single occurrence of event , then

for any well-behaved . The special case where the loss for an occurrence of event is treated as a constant is represented with the Dirac delta function .

The choice of for each event represents represents uncertainty about the loss that follows from the event, often termed ‘secondary uncertainty’ in catastrophe modelling. We will discuss an efficient and flexible approach to representing more-or-less arbitrary specifications of in Section 5.

| Event ID | Arrival rate, | Loss distribution |

|---|---|---|

| 1 | ||

| 2 | ||

There are two equivalent representations of the ELT, for stochastic simulation of the loss process through time (see, e.g., Ross, 1996, sec. 1.5). The first is that the events with different IDs follow concurrent but independent homogeneous Poisson processes. The second is that the collective of events follows a single homogeneous Poisson process with arrival rate

and then, when an event occurs, its ID is selected independently at random with probability .

The second approach is more tractable for our purposes. Therefore we define as the loss incurred by a randomly selected event, with probability density function

The total loss incurred over an interval of length is then modelled as the random sum of independent losses, or

The total loss would generally be termed a compound Poisson process with rate and component distribution . An unusual feature of loss modelling is that the component distribution is itself a mixture, sometimes with thousands of components.

3 A SELECTION OF UPPER BOUNDS

Our interest is in a bound for the probability for some specified ELT and time period ; we assume, as is natural, that . We pose the question: is small enough to be tolerable for specified and ? We are aware of four useful upper bounds on , explored here in terms of increasing complexity. The following material is covered in standard textbook such as Grimmett and Stirzaker (2001), and in more specialised books such as Ross (1996) and Whittle (2000). To avoid clutter, we will drop the ‘’ subscript on and .

The Markov inequality.

The Markov inequality states that if then

| (Mar) |

where . As is a compound process,

| (1) |

the second equality following because is Poisson. The second expectation is simply

We do not expect this inequality to be very tight, because it imposes no conditions on the integrability of , but it is so fast to compute that it is always worth a try for a large .

The Cantelli inequality.

If is square-integrable, i.e. is finite, then

| (Cant) |

This is the Cantelli inequality, and it is derived from the Markov inequality. As is a compound process,

| (2) |

the second equality following because is Poisson. The second expectation is simply

We expect the Cantelli bound will perform much better than the Markov bound both because it exploits the fact that is square integrable, and because its derivation involves an optimisation step. It is almost as cheap to compute, and so it is really a free upgrade.

The moment inequality.

This inequality and the Chernoff inequality below use the generalised Markov inequality: if is increasing, then , and so

for any that is increasing and non-negative.

An application of the generalised Markov inequality gives

because is non-negative and increasing for all . Fractional moments can be tricky to compute, but integer moments are possible for compound Poisson processes. Hence we consider

| (Mom) |

This cannot do worse that the Markov bound, which is the special case of .

The integer moments of a compound Poisson process can be computed recursively, as shown in Ross (1996, sec. 2.5.1):

| (3) |

The only new term here is

At this point it would be helpful to know the Moment Generating Function (MGF, see below) of each .

Although not as cheap as the Cantelli bound, this does not appear to be an expensive calculation, if the ’s have standard forms with simple known MGFs. It is legitimate to stop at any value of , and it might be wise to limit in order to avoid numerical issues with sums of very large values.

The Chernoff inequality.

Let be the MGF of , that is

Chernoff’s inequality states

| (Ch) |

It follows from the generalised Markov inequality with , which is non-negative and increasing for all .

If is the MGF of , then

In our model is Poisson, and hence

(see, e.g. Ross, 1996, sec. 1.4). Thus the MGF of simplifies to

The MGF of can be expressed in terms of the MGFs of the ’s:

Now it is crucial that the have standard forms with simple known MGFs.

In an unlimited optimisation, the Chernoff bound will never outperform the Moment bound (Philips and Nelson, 1995). In practice, however, constraints on the optimisation of the Moment bound may result in the best available Chernoff bound being lower than the best available Moment bound. But there is another reason to include the Chernoff bound, from large deviation theory; see, e.g., Whittle (2000, sec. 15.6 and ch. 18). Let be an integer number of years, and define as the loss from one year, so that . Then large deviation theory states that

and so as becomes large the Chernoff upper bound becomes exact. Very informally, then, the convergence of the Chernoff bound and the Moment bound suggest, according to a squeezing argument, that both bounds are converging from above on the actual probability.

4 TWO ‘EXACT’ APPROACHES

There are several approaches to computing to arbitrary accuracy, although in practice this accuracy is limited by computing power (see Shevchenko, 2010, for a review). We mention two here.

Monte Carlo simulation.

One realisation of for a fixed time-interval can be generated by discrete event simulation, also known as the Gillepsie algorithm (see, e.g., Wilkinson, 2012, sec. 6.4). Many such simulations can be used to approximate the distribution function of , and can be used to estimate probabilities, including tail probabilities.

Being finite-sample estimates, these probabilities should have a measure of uncertainty attached. This is obviously an issue for regulation, where the requirement is often to demonstrate that

for some which reflects the insurer’s available capital, and some specified by the regulator. For Solvency II, for one-year total losses. A Monte Carlo point estimate of which was less than would be much more reassuring if the whole of the 95% confidence interval for were less than , than if the 95% confidence interval contained .

A similar problem is faced in ecotoxicology, where one recommendation would be equivalent in this context to requiring that the upper bound of a 95% confidence interval for is no greater than ; see Hickey and Hart (2013). If we adopt this approach, though, it is incorrect simply to monitor the upper bound and stop sampling when it drops below , because the confidence interval in this case ought to account for the stochastic stopping rule, rather than being based on a fixed sample size. But it is possible to do a design calculation to suggest an appropriate value for , the sample size, that will ensure that the upper bound will be larger than with specified probability, a priori, as we now discuss.

Let be the upper limit of a level confidence interval for , where is the number of sample members that are at least , and is the sample size. Suppose that the a priori probability of this upper limit being no larger than is to be at least , where would be specified. In that case, valid ’s satisfy

where .

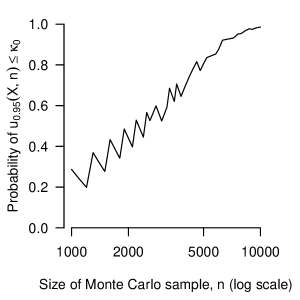

There are several ways of constructing an approximate confidence interval for , reviewed in Brown et al. (2001).222It is not possible to construct an exact confidence interval without using an auxiliary randomisation. We suggest what they term the (unmodified) Jeffreys confidence interval, which is simply the equi-tailed credible interval for with the Jeffreys prior, with a minor modification. Using this confidence interval, Figure 1 shows the probability for various choices of with and . In this case, seems to be a good choice, and this number is widely used in practice.

Panjer recursion.

The second approach is Panjer recursion; see Ross (1996, Cor. 2.5.4) or Shevchenko (2010, sec. 5). This provides a recursive calculation for whenever each is integer-valued, so that itself is integer-valued. This calculation would often grind to a halt if applied literally, but can be used to provide an approximation if the ELT is compressed, as discussed in section 6.1.

Perhaps the main difficulty with Panjer recursion, once it has been efficiently encoded, is that it does not provide any assessment of the error which follows from the compression of the ELT. In this situation, a precise and computationally cheap upper bound may be of more practical use than an approximation. Section 6.1 also discusses indirect ways to assess the compression error, using the upper bounds.

Monte Carlo simulation is an attractive alternative to Panjer recursion, because it comes with a simple assessment of accuracy, is easily parallelisable, and the sample drawn can be used to calculated other quantities of interest for insurers like the net aggregate loss and reinsurance recovery costs.

5 TRACTABLE SPECIAL CASES

In this section we consider three tractable special cases.

First, suppose that

i.e. the loss from event is fixed at . Then

All of the bounds are trivial to compute.

Second, suppose that each is a Gamma distribution with parameters :

for , where is the indicator function and is the Gamma function,

Then

| (4) |

The moments are

| (5) |

and hence

Third, suppose that each is a finite mixture of Gamma distributions:

where for each . Then

In other words, this is exactly the same as creating an extended ELT with plain Gamma ’s (i.e. as in the second case), but where each is shared out among the mixture components according to the mixture weights .

This third case is very helpful, because the Gamma calculation is so simple, and yet it is possible to approximate any strictly positive absolutely continuous probability density function that has limit zero as , with a mixture of Gamma distributions (Wiper et al., 2001). It is also possible to approximate point distributions by very concentrated Gamma distributions, discussed below in Section 6.3. Thus the secondary uncertainty for an event might be represented as a set of discrete losses, each with its own probability, but encoded as a set of highly concentrated Gamma distributions, leading to very efficient calculations.

Capped single-event losses.

For insurers, a rescaled Beta distribution is often preferred to a Gamma distribution, because it has a finite upper limit representing the maximum insured loss. The moment generating function of a Beta distribution is an untabulated function with an infinite series representation, and so will be more expensive to compute accurately; this will affect the Chernoff bound. There are no difficulties with the moments.

However, we would question the suitability of using a Beta distribution here. The insurer’s loss from an event is capped at the maximum insured loss. This implies an atom of probability at the maximum insured loss: if is the original loss distribution for event and is the maximum insured loss, then

where and is the Dirac delta function, as before. A Beta distribution scaled to would be quite different, having no atom at .

The Gamma distribution for is tractable with a cap on losses. If is a Gamma distribution then the MGF is

where is the incomplete Gamma function,

and

The moments of are

Introducing a non-zero lower bound is straightforward.

6 NUMERICAL ILLUSTRATION

We have implemented the methods of this paper in a package for the R open source statistical computing environment (R Core Team, 2013), named tailloss. In addition, this package includes a large ELT for US hurricanes (32,060 rows).

6.1 The effect of merging

We provide a utility function, compressELT, which reduces the number of rows of an ELT by rounding and merging. This speeds up all of the calculations, and is crucial for the successful completion of the Panjer approximation.

The rounding operation rounds each of the losses to a specified number of decimal places, with being to an integer, and being a value with zeros before the decimal point. Then the rounded value is multiplied by to convert it to an integer. Finally, the merge operation combines all the rows of the ELT with the same transformed loss, and adds their rates.

| Event ID | Arrival rate, | Expected Loss, $ |

|---|---|---|

| 1 | 0.09265 | 1 |

| 2 | 0.03143 | 2 |

| 3 | 0.02159 | 3 |

| 4 | 0.01231 | 4 |

| 5 | 0.01472 | 5 |

| 32056 | 0.00001 | 17593790 |

| 32057 | 0.00001 | 18218506 |

| 32058 | 0.00001 | 18297003 |

| 32059 | 0.00001 | 19970669 |

| 32060 | 0.00001 | 24391615 |

Table 6.1 shows some of the original ELT, and Table 6.1 the same table after rounding to the nearest $10k (i.e. ). It is an empirical question, how much rounding can be performed on a given ELT without materially changing the distribution of -year total losses. Ideally, this would be assessed using an exact calculation, like Panjer recursion. Unfortunately it is precisely because Panjer recursion is so numerically intensive that rounding and merging of large ELTs is necessary in the first place. So instead we assess the effect of rounding and merging using the Moment bound, which, as already established, converges to the actual value when the number of events in the time-interval is large.

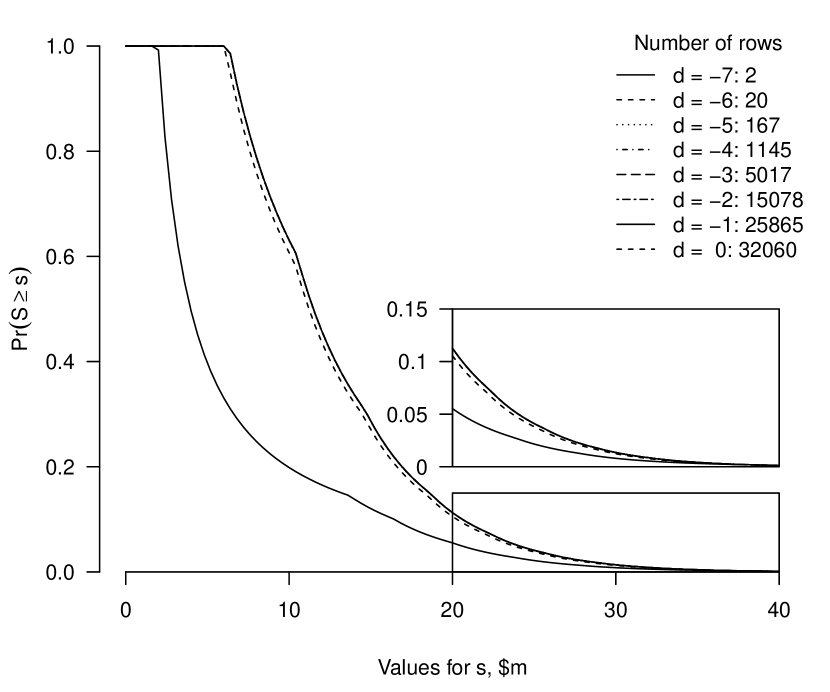

Figure 2 shows the result of eight different values for , from to . The outcome with is materially different, which is not surprising because this ELT only has two rows. More intriguing is that the outcome with is almost the same as that with no compression at all, despite the ELT having only rows.

6.2 Computational expense of the different methods

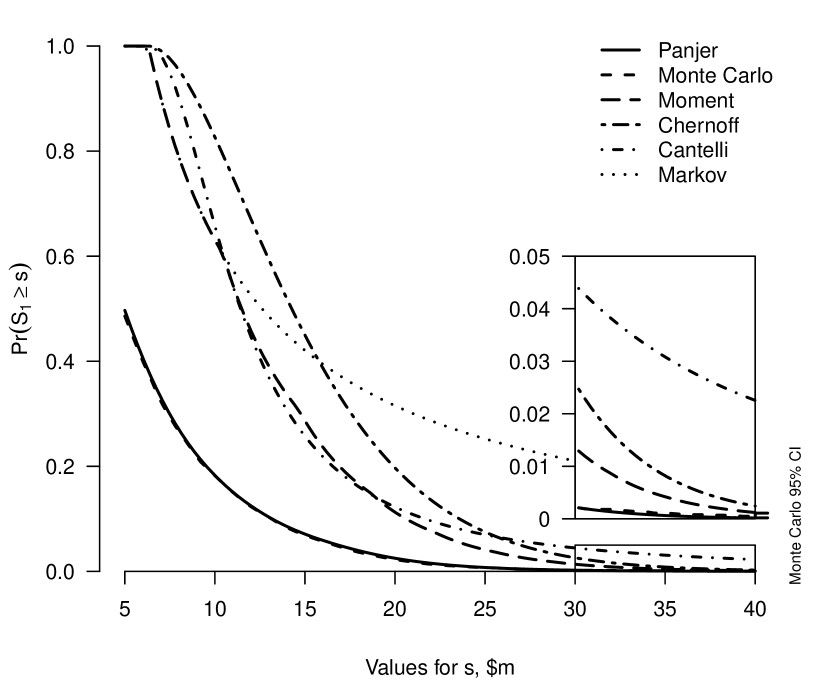

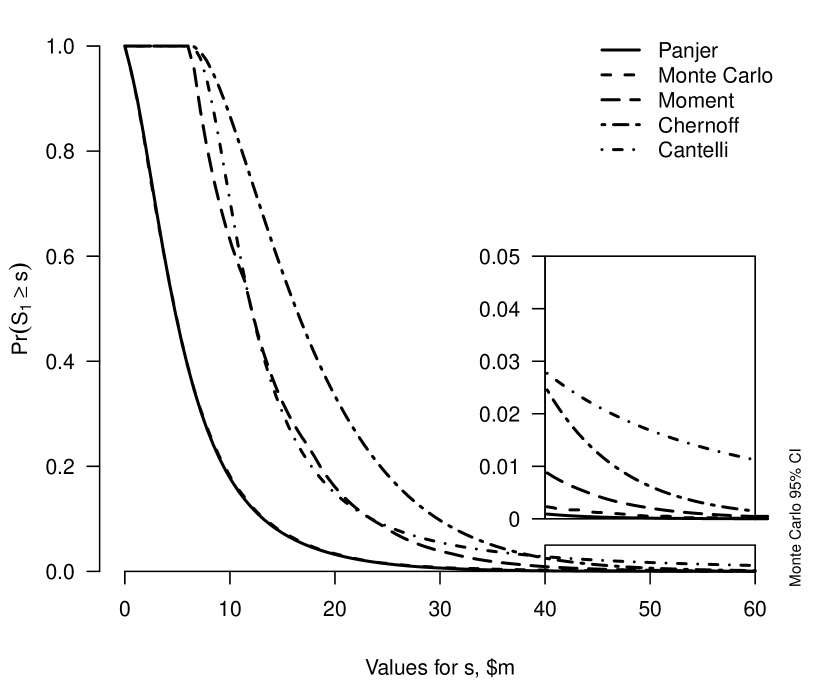

Here we consider one-year losses, and treat the losses for each event as certain; i.e. the first case in section 5. The methods we consider are Panjer, Monte Carlo, Moment, Chernoff, Cantelli, and Markov. The first two provide approximately exact values for . Panjer is an approximation because of the need to compress the ELT. For the Monte Carlo method, we used simulations, as discussed in section 4, and we report the confidence interval in the tail. The remaining methods provide strict upper bounds on . Our optimisation approach for the Moment and Chernoff bounds is given in the Appendix. All the timings are CPU times in seconds on a MacBook Pro processor 2.53 GHz Intel Core 2 Duo.

Figure 3 shows the exceedance probabilities for the methods, computed on equally-spaced ordinates between and , with compression . The Markov bound is the least effective, and the Cantelli bound is surprisingly good. As expected, the Chernoff and Moment bounds converge, and also, in this case, converge on the Panjer and Monte Carlo estimates.

The timings for the methods are given in Table 6.2. These values require very little elaboration. The Moment, Cantelli, and Markov bounds are effectively instantaneous to compute, with timings of a few thousandths of a second. The Chernoff bound is more expensive but still takes only a fraction of a second. The Monte Carlo and Panjer approximations are hundreds, thousands, or even millions of times more expensive. The Panjer bound is impractical to compute at compression below (and from now on we will just consider ).

A similar table to Table 6.2 could be constructed for any specified value , rather than a whole set of values. The timings for the Moment, Chernoff, Cantelli, and Markov bounds would all be roughly one hundredth as large, because these are evaluated pointwise. The timing for Monte Carlo would be unchanged. The timing for Panjer would be roughly the proportion of the total timing, because it is evaluated sequentially, from small to large values of .

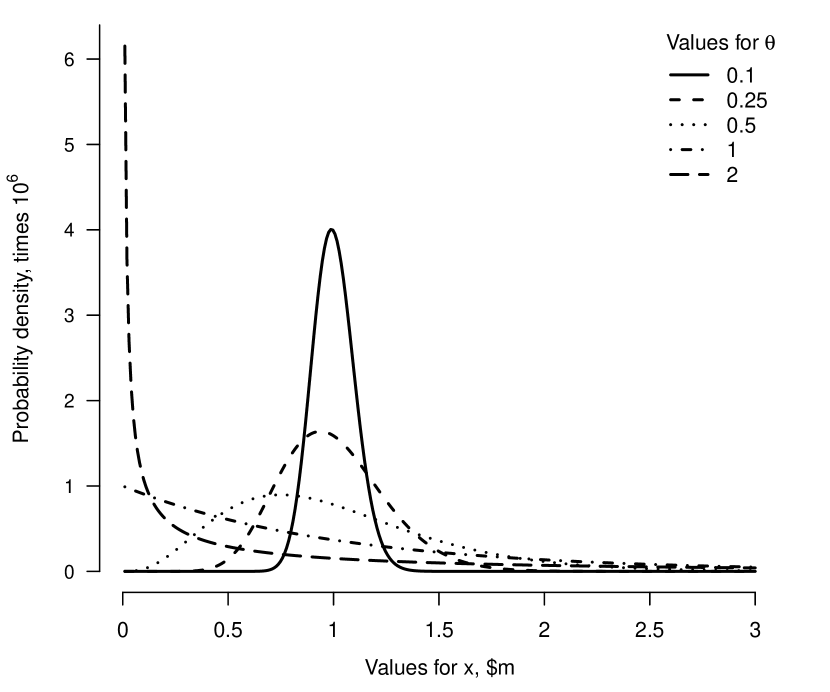

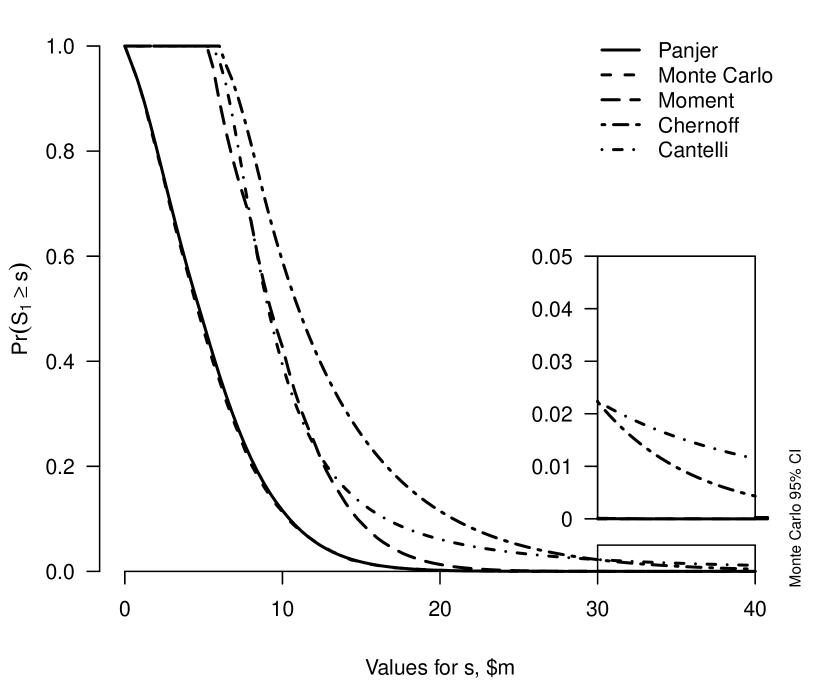

6.3 Gamma thickening of the event losses

We continue to consider one-year losses, but now treat the losses from each event as random, not fixed. For the simplest possible generalisation we use a Gamma distribution with a specified expectation and a common specified coefficient of variation, . The previous case of a fixed loss is represented by , which we write, informally, as . Solving

gives the two Gamma distribution parameters as

Figure 4 shows the effect of varying on a Gamma distribution with expectation .

The only practical difficulty with allowing random losses for each event occurs for the Panjer method; we describe our approach in the Appendix.

Figure 5 shows the exceedance probability curve with : note that the horizontal scale now covers a much wider range of loss values than Figure 3. The timings are given in Table 6.3: these are very similar to the non-random case with (Table 6.2), with the exception of the Panjer method, which takes longer because it scales linearly with the upper limit on the horizontal axis.

6.4 Capping the loss from a single event

Now consider the case where the single-event loss is capped at . The implementation of this cap is straightforward, and we describe it in the Appendix. The results are given in Figure 6 and Table 6.4. For the timings, the main effect of the cap is on the Panjer method, because the cap reduces the probability in the righthand tail of the loss distribution, and allows us to use a smaller upper limit on the horizontal axis. But the Panjer approximation, where it can be computed, still takes a thousand times longer to compute than the Moment bound.

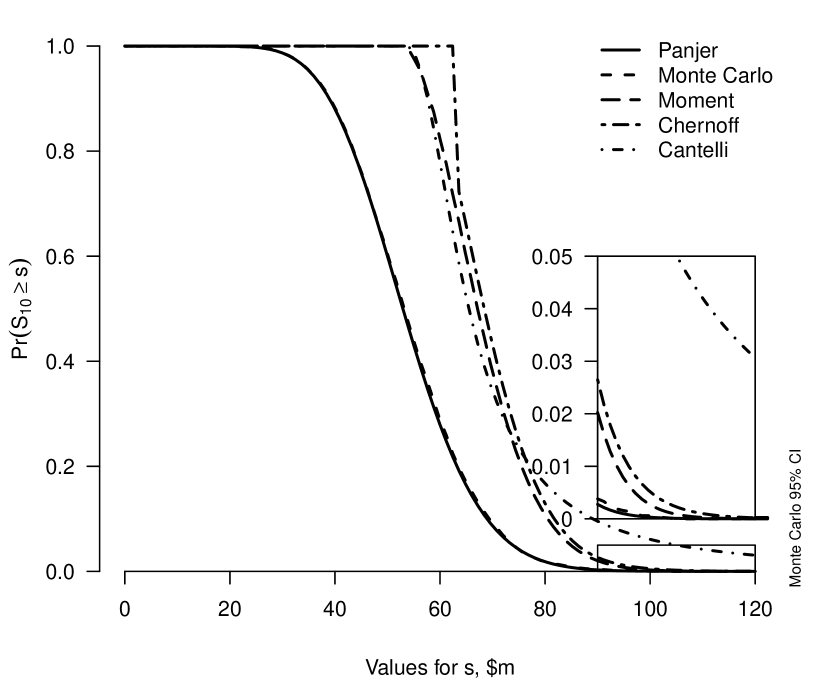

6.5 Ten-year losses

Finally, consider expanding the time period from to years; the results are given in Figure 7 and Table 6.5. The timings of the Markov, Cantelli, Moment, and Chernoff bounds are unaffected by the value of . The timing for the Panjer method grows with , because the righthand tail of grows with . The timing for the Monte Carlo method grows roughly linearly with , but the ‘in simulation’ time for Monte Carlo is dominated by other factors, so the additional computing time for the increase in from to , is small.

7 SUMMARY

We have presented four upper bounds and two approximations for the upper tail of the loss distribution that follows from an Event Loss Table (ELT). We argue that in many situations an upper bound on this probability is sufficient. For example, to satisfy the regulator, in a sensitivity analysis, or when there is supporting evidence that the bound is quite tight. Of the bounds we have considered, we find that the Moment bound offers the best blend of tightness and computational efficiency. In fact, the Moment bound is effectively costless to compute, based on the timings from our R package.

We have stressed that there are no exact methods for computing tail probabilities when taking into account limited computing resources. Of the approximately exact methods we consider, we prefer Monte Carlo simulation over Panjer recursion, because of the availability of an error estimate in the former and the amount of information provided by the latter. A back-of-the-envelope calculation suggests that 10,000 Monte Carlo simulations should suffice to satisfy the Solvency II regulator.

The merging operation is a very useful way to condense an ELT that has become bloated, for example after using mixtures of Gamma distributions to represent more complicated secondary uncertainty distributions. We have shown that the Moment bound provides a quick way to assess how much merging can be done without having a major impact on the resulting aggregate loss distribution.

We have also demonstrated the versatility of the Gamma distribution for single event losses. The Gamma distribution has a simple moment generating function and explicit expressions for the moments. Therefore it fits very smoothly into the compound Poisson process that is represented in an ELT, for the purposes of computing approximations and bounds. We also show how the Gamma distribution can easily be adapted to account for a cap on single event losses. We favour the capped Gamma distribution over the Beta distribution, which is often used in the industry, because the former has an atom (as is appropriate) while the latter does not.

ACKNOWLEDGEMENTS

We would like to thank Dickie Whittaker, David Stephenson and Peter Taylor for valuable comments which helped in improving the exposition of this paper, and for supplying the US Hurricanes event loss table. This work was funded in part by NERC grant NE/J017450/1, as part of the CREDIBLE consortium.

REFERENCES

- Brown et al. (2001) L.D. Brown, T.T. Cai, and A. DasGupta, 2001. Interval estimation for a binomial proportion. Statistical Science, 16(2), 101–117. With discussion, pp 117–133.

- Grimmett and Stirzaker (2001) G.R. Grimmett and D.R. Stirzaker, 2001. Probability and Random Processes. Oxford, UK: Oxford University Press, 3rd edition.

- Hickey and Hart (2013) G.L. Hickey and A. Hart, 2013. Statistical aspects of risk characterisation in ecotoxicology. In J.C. Rougier, R.S.J. Sparks, and L.J. Hill, editors, Risk and Uncertainty Assessment for Natural Hazards, chapter 14. Cambridge University Press, Cambridge, UK.

- Philips and Nelson (1995) T.K. Philips and R. Nelson, 1995. The moment bound is tighter than Chernoff’s bound for positive tail probabilities. The American Statistician, 49(2), 175–178.

- R Core Team (2013) R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2013.

- Ross (1996) S.M. Ross, 1996. Stochastic Processes. John Wiley & Sons, Inc., New York, USA, second edition.

- Shevchenko (2010) P.V. Shevchenko, 2010. Calculation of aggregate loss distributions. The Journal of Operational Risk, 5(2), 3–40.

- Whittle (2000) P. Whittle, 2000. Probability via Expectation. New York: Springer, 4th edition.

- Wilkinson (2012) D.J. Wilkinson, 2012. Stochastic Modelling for Systems Biology. CRC Press, Boca Raton FL, USA, second edition.

- Wiper et al. (2001) Michael Wiper, David Rios Insua, and Fabrizio Ruggeri, 2001. Mixtures of Gamma distributions with applications. Journal of Computational and Graphical Statistics, 10(3), 440–454.

APPENDIX

Minimisation for the Moment bound.

The Moment bound is minimised over the control variable . It is convenient to have an upper bound for , because it is efficient to compute for a set of values, rather than one at a time, as shown in (3). We find an approximate upper bound for as follows. First, we compute the first two moments of exactly using (1) and (2). Then we approximate the distribution of using a Gamma distribution matched to these two moments, for which

The moments for the Gamma distribution were given in (5). Starting from this expression and , we step out in until the Gamma approximation to shows an increase on its previous value. The ceiling of the resulting is taken as the maximum value. If the Moment bound is required for a sequence of values, we use the largest value in the sequence.

Minimisation for the Chernoff bound.

The MGF for a Gamma distribution is given in (4). Hence the range for the control variable is . As explained in section 6.3, we specify the two parameters of the Gamma distribution for event in terms of the fixed loss , now treated as the expected loss, and a coefficient of variation (which could vary with ). This gives , and hence

In the simpler case of a fixed loss for event , we substitute the small coefficient of variation, , to give . We perform the minimisation over a set of equally-spaced values for .

Panjer recursion for random event losses.

The Panjer algorithm needs each event loss to be a fixed (non-negative) integer. Therefore we follow the mixture approach of section 5 to replace an event with a random loss with a collection of events with fixed losses. Consider event , with loss distribution . We replace row in the original ELT with rows each with rate , and with losses , where is the

quantile of . Having done this for all rows, we then compress the expanded ELT back to integer values again (i.e. using ). We used .

Capping single event losses.

In the case where event losses are non-random, a cap at simply replaces each loss for which with the value . Where the event losses are Gamma-distributed with expectation and specified coefficient of variation , the modified Gamma moment generating functions are used for the Markov, Cantelli, Moment, and Chernoff method, see section 5. The Panjer method is implemented on an augmented ELT, as described immediately above, and then each loss is capped at . The Monte Carlo method has each sampled loss capped at .