Uncertainty Quantification Under Group Sparsity

Abstract

Quantifying the uncertainty in penalized regression under group sparsity is an important open question. We establish, under a high-dimensional scaling, the asymptotic validity of a modified parametric bootstrap method for the group lasso, assuming a Gaussian error model and mild conditions on the design matrix and the true coefficients. Simulation of bootstrap samples provides simultaneous inferences on large groups of coefficients. Through extensive numerical comparisons, we demonstrate that our bootstrap method performs much better than popular competitors, highlighting its practical utility. The theoretical result is generalized to other block norm penalization and sub-Gaussian errors, which further broadens the potential applications.

Keywords: confidence region, group lasso, high-dimensional inference, parametric bootstrap, sampling distribution, significance test.

1 Introduction

1.1 Overview and background

The surge of recent work on statistical inference for high-dimensional models can be roughly grouped into a few categories. The first group of methods quantify the uncertainty in the lasso (Tibshirani 1996) and its modifications via subsampling, data splitting, or the bootstrap, such as Wasserman and Roeder (2009), Meinshausen et al. (2009), Chatterjee and Lahiri (2013), Liu and Yu (2013) and Zhou (2014). The second category makes inference along the lasso solution path or conducts post-selection inference via conditional tests, including Lockhart et al. (2014), Taylor et al. (2014) and Lee et al. (2016). Methods in the third category rely on a de-biased lasso to construct confidence intervals or perform significance tests (Zhang and Zhang 2014; van de Geer et al. 2014; Javanmard and Montanari 2014). In addition, Ning and Liu (2017) and Voorman et al. (2014) have proposed different score tests for penalized M-estimators or penalized regression. Under certain sparsity assumptions on the parameter space, all the methods make use of regularization, particularly penalization.

This paper focuses on statistical inference under group sparsity, which arises naturally in many applications. Furthermore, individual coefficients that are too small to detect may be reliably identified when grouped together. This gives another motivation for the present work. Consider the linear model

| (1.1) |

where is the unknown true parameter, is the response vector, is the design matrix and is an independent and identically distributed error vector with mean zero and variance . Suppose that the predictors are partitioned into nonoverlapping groups, denoted by for . That is, and for every . For , let for each . The group lasso (Yuan and Lin 2006) is then defined as

| (1.2) |

where denotes the Euclidean norm. The weights and are usually in proportion to , where is the size of the th group. In (1.2), we use to indicate that , when not unique, is one of the minimizers. Given the group structure and , the associated -group norm, sometimes referred to as the norm, is defined as

| (1.3) |

where denotes the norm of a vector. Thus, the penalty term in (1.2) is a weighted -group norm of . One may also use other -group norm penalties in the above formulation (Negahban et al. 2012). See Huang et al. (2012) for recent developments on regularization methods respecting group structure. Despite the wide applications of these methods, there are quite limited efforts devoted to uncertainty quantification and inference under group sparsity. Mitra and Zhang (2016) propose to de-bias the group lasso for inference about a group of coefficients, which generalizes the idea of those methods in the third category reviewed above. For each group, a highly nontrivial optimization problem has to be solved, and thus it might be difficult to apply this approach to a large number of groups. Meinshausen (2015) develops a conservative group-bound method to detect whether a group of highly correlated variables have nonzero coefficients.

1.2 Contributions of this work

In this article, we tackle the problem of group inference from a different angle. Our goal is to directly quantify the uncertainty in the group lasso (1.2) and other penalized estimators under group sparsity. Neither of the two aforementioned group inference methods provides an answer to this question. Instead, we consider the parametric bootstrap, a simple simulation-based approach. Given a proper choice of a point estimator , we simulate an error vector and put . After minimizing the penalized loss (1.2) we obtain a group lasso solution for the simulated data . Under quite mild conditions on the design matrix and the true parameter , we provide theoretical justification for using the distribution of , conditional on , to make inference about for all . Our theory is developed under a high-dimensional asymptotic framework as and applies to large groups with size . To the best of our knowledge, such consistency in estimation of sampling distributions has not been established for group norm penalized estimators. Allowing for unbounded group sizes makes the group lasso fundamentally different from the lasso, so this work represents a distinct contribution from existing bootstrap methods for a lasso-type estimator (Chatterjee and Lahiri 2013; Zhou 2014). It is also different from the work by McKeague and Qian (2015) and by Shah and Bühlmann (2015), in which the bootstrap is used for correlation screening or simulation of a scaled residual without considering any group structure.

In addition to the novel theoretical result, an important strength of this work is its great potential in practical applications, as seen from the following aspects.

-

1.

Flexibility: By simulation one can easily estimate the distributions of many functions of , and thus has much more freedom in choosing which statistic to use in an inference problem. The simulation approach allows for interval estimation and significance tests for all groups simultaneously and in fact for all individual coefficients as well. This is in sharp contrast to the de-biased methods which solve an optimization problem for each individual coefficient or each coefficient group.

-

2.

Implementation: There is no need for any additional optimization algorithm. For most cases, simple thresholding of the group lasso is a valid choice for the point estimate . Therefore, a practitioner can simply use the same software package to find the group lasso solution and to quantify its uncertainty. According to our empirical study, a few hundred bootstrap samples are usually sufficient for accurate inference, which as a whole cost much less time than solving optimization problems as used in the de-biased lasso approach.

-

3.

Performance: Through extensive numerical comparisons, we demonstrate that our bootstrap method outperforms competing methods by a large margin for finite samples, which implies that this method is much less dependent on asymptotic approximation. Moreover, our method is not very sensitive to the threshold value used to define , which is the only user-input parameter in our current implementation.

Although out of the scope of this paper, the method of estimator augmentation (Zhou 2014) may greatly improve the simulation efficiency, particularly, in calculating tail probabilities in a significance test, making a simulation-based method more appealing in applications. This has been demonstrated for group inference by Zhou and Min (2016).

1.3 Organization and notation

The paper is organized as follows. Our parametric bootstrap method for inference with the group lasso is proposed and described in Section 2. We develop asymptotic theory under a Gaussian error distribution in Section 3 to show that our inferential method is valid in a high-dimensional framework. Numerical results are provided in Section 4 to demonstrate the advantages of our method in finite-sample inference over competing methods. In Section 5, we generalize our results to the use of the -group norm penalty (1.3), for , and to sub-Gaussian errors, with a discussion on future work. All proofs are deferred to Supplemental Material which also contains auxiliary theoretical and numerical results.

Notation used throughout the paper is defined here. Define for an integer . Let be an index set. For a vector , denote by the restriction of to the components in . For a matrix with columns , , define as a matrix of size consisting of columns in , and similarly define for . Denote by the diagonal matrix with as the diagonal elements and by the block diagonal matrix with and as the diagonal blocks. For a square matrix , extracts the diagonal elements, denotes the trace of , and , for , denotes its eigenvalues. Moreover, and denote the maximum and the minimum eigenvalues, respectively, or the supremum and the infimum when . Denote by the identity matrix. Given the group structure , let for . For a vector , define and, in particular, . We call the set of active groups of . For an matrix , , and when , for . For two sequences and , write if and if and . Their probabilistic counterparts are written as and , respectively. We use to denote the distribution of a random vector . Positive constants , , etc. and positive integers , , etc. are defined locally and may have different values from line to line. Small positive numbers are often denoted by , which should be distinguished from the error vector .

2 Bootstrapping the group lasso

2.1 Bootstrap and inference

We will assume that the noise vector throughout the paper until Section 5, in which sub-Gaussian and other error distributions are considered. Let and be point estimates of and . We first describe our proposed parametric bootstrap for the group lasso, given point estimates and , and discuss how to make inference with a bootstrap sample. In next subsection, we will propose methods to construct and from the data .

Let denote the set of minimizers of the loss in (1.2) so that . Our parametric bootstrap for the group lasso contains two steps:

-

(1)

Given , draw and set ;

-

(2)

Solve (1.2) with in place of to obtain .

After drawing a large sample of values via the above procedure, we can make inference for each group . By default, we choose the function

| (2.1) |

to build a confidence region and carry out a significance test for . From the bootstrap sample of , we estimate the -quantile such that

Then our confidence region for is

| (2.2) |

We may also test the hypothesis , which will be rejected at level if , that is, if . This approach can make inference about simultaneously for . One may choose other matrices in place of to define (2.1), as long as they satisfy some very mild conditions specified in Corollary 3.2.

2.2 Estimation of parameters

Multiple methods may be applied to obtain the point estimates, and . Roughly speaking, must consistently recover the groups of with a large norm and needs to be a consistent estimator of with a certain convergence rate.

One possible way to construct is to threshold the group lasso ,

| (2.3) |

where is a cutoff value. Useful practical guidance is to choose the cutoff so that all small coefficient groups will be thresholded to zero. Let be the active groups of and be the set of active coefficients of . Then we perform a least-squares regression of on to re-calculate the nonzero coefficients of , which reduces their bias, and to estimate the error variance , provided that . This will be implemented in our method for the numerical comparisons with more details provided in Section 4.1. See Section 3.2 for other choices of the point estimates and theoretical justifications.

The parametric bootstrap is commonly used for fixed-dimensional inference problems, such as linear regression with fixed and . However, there is no general theory on its validity for a high-dimensional problem. Thus, rigorous asymptotic theory for our bootstrap method, including the choice of the point estimators, will be developed in Section 3 to justify its use under a setting that allows and . If is drawn by resampling the residual , then our method implements the standard residual bootstrap. To the best of our knowledge, consistency of either bootstrap method for the group lasso under the above high-dimensional setting has not been established in the literature.

When the group size for all , our method reduces to a parametric bootstrap for the lasso. In this special case, it is closely related to the modified residual bootstrap proposed by Chatterjee and Lahiri (2011). However, the consistency of their method is established under the assumption that is fixed, while our theory applies to the more interesting case of .

3 Asymptotic theory

3.1 Convergence of the bootstrap distribution

Let , and so that is the number of active groups and the number of active coefficients of . Denote by and the minimum and the maximum of , respectively. Assume that for all with throughout this section. We adopt a high-dimensional asymptotic framework for model (1.1), where , may be unbounded, and stays as a constant. Accordingly, , , and all depend on . For brevity the index is often suppressed. We say a sequence of events happens with high probability if as .

We first develop theoretical results assuming that the noise variance is known, in which case we let in our bootstrap sampling of . To facilitate our analysis, we introduce an intermediate variable , which follows the same distribution as since . Define centered and rescaled estimators

| (3.1) |

where is a sequence of positive numbers to be specified later. We will show that the deviation between and , conditioning on a proper choice of , converges to zero in probability, which leads to weak convergence of functions of to . The case of unknown will be covered in Section 3.2.

We assume the following conditions on and . Denote by the Gram matrix. Let , and

where is conjugate to satisfying .

Assumption 1.

With high probability, we have for all and

| (3.2) |

where are universal constants.

Assumption 2.

The true coefficient vector is sparse:

| (3.3) |

and such that

| (3.4) |

where .

Our next assumption is on the point estimator . For , define

| (3.5) |

Assumption 3.

The estimator satisfies for some , where the set is defined by

| (3.6) |

The inequality (3.2) in Assumption 1 guarantees the restricted eigenvalue assumption (Bickel et al. 2009; Lounici et al. 2011) under group sparsity, which is shown in Supplemental Material. It is also sufficient for the restricted strong convexity condition for the group lasso as demonstrated in Negahban et al. (2012). Assumption 2 shows that is sparse at both group and individual levels, and its active groups can be separated into strong and weak signals. A beta-min condition (3.4) is satisfied by the strong signal groups. As implied by (3.6), the point estimator must identify only the strong groups and converge to the active groups of at certain rate. A detailed discussion of these assumptions with comparisons to existing methods is provided in Section 3.3.

Theorem 3.1.

For , can be regarded as an average length of its components. Using such averages serves as a normalization across groups of different sizes. Since , the in (3.7) is the convergence rate of the supremum of the normalized errors for the active groups. As shown in the proof of Theorem 3.1 in Supplemental Material,

| (3.10) |

In Remark 1 below, we will see that may achieve the optimal rate of under certain conditions. The key conclusion (3.9) shows that the deviation between and converges to zero. We do not assume that (1.2) has a unique minimizer in Theorem 3.1. However, (3.8) implies that any two minimizers follow the same asymptotic distribution and thus there is no need to distinguish these minimizers when is large.

We briefly comment on some technical aspects in the proof of this result, while leaving the detail to Supplemental Material. The overall idea is to bound the difference in the group lasso loss function (1.2) when is used in place of and then translate this into a bound on the deviation between and , which are centered minimizers of the loss. The challenge in the first step comes from the non-linearity of the regularizer and the high-dimensionality of the space. As a result, we cannot restrict our analysis to any finite-dimensional compact subset. Although and satisfy the so-called cone condition which allows one to make use of restricted eigenvalue assumptions on , the deviation does not necessarily lie in a cone and is usually not sparse. This presents another technical challenge in the second step.

Now consider the implications of Theorem 3.1 for inference about a coefficient group. Theorem 5.1 in Lounici et al. (2011) asserts that

| (3.11) |

under a generalized coherence condition for the group lasso setting. Let

| (3.12) |

, and , where is a matrix for each . Recall that is the distribution of . We have the following result regarding group inference:

Corollary 3.2.

The above result applies directly to simultaneous inference about all groups, each of a possibly unbounded size, based on the bootstrap distributions of . Under mild assumptions such as those in Proposition 3.4 below, the singular values of are uniformly bounded between two positive constants with high probability. Thus, this corollary validates theoretically our bootstrap inference using the function (2.1). In fact, one may use many other matrices to carry out the inference. Moreover, the explicit rate of is irrelevant to the practical implementation of our method.

Remark 1.

The order of in (3.12) shows that the radius of a confidence region constructed according to (3.13) is wider than the optimal rate by no more than a factor of . It should be clarified that this suboptimality is caused by the intrinsic bias of the group lasso, instead of the bootstrap procedure. When the order of the group size is comparable to or larger than , however, the rate may become optimal with . This is not possible for the lasso with and , which demonstrates another advantage of grouping a large number of coefficients for inference with the group lasso. Comparing (3.7) to (3.11) shows that in general. As a result, when becomes optimal we also have .

3.2 Justification for point estimates

To complete our validation of the proposed bootstrap inference in Section 2 assuming is known, it remains to verify that the thresholded group lasso satisfies Assumption 3:

Proposition 3.3.

Under Assumption 2 with , the condition that requires to be model selection consistent and to have a certain rate of convergence to . Of the two, model selection consistency is the key, since conditional on and (3.3), one can always apply the ordinary least-squares method to reestimate the active coefficients of , which will satisfy the convergence rate requirement. Here, we mention a few other methods for constructing , which are model selection consistent. The first method is the adaptive group lasso (Wei and Huang 2010), a natural generalization of the adaptive lasso (Zou 2006), which minimizes (1.2) with weights defined by an initial estimator. If we choose the group lasso as the initial estimator, Corollary 3.1 in Wei and Huang (2010) asserts that the adaptive group lasso is model selection consistent, while allowing , , and to grow with . The second choice is to use a concave penalty, such as the MCP (Zhang 2010). By Theorem 4.2 and Corollary 4.2 in Huang et al. (2012), a penalized estimator under the group MCP enjoys the oracle property, achieving model selection consistency and the optimal rate in estimating active coefficients. Other possible methods may include stability selection (Meinshausen and Bühlmann 2010) and the sample splitting approach of Wasserman and Roeder (2009).

When the noise variance is unknown, we plug in an estimate in bootstrap sampling. To establish similar results as in Theorem 3.1 and Corollary 3.2, it suffices that

| (3.16) |

See Supplemental Material for the precise statement. This essentially requires converge to faster than the rate of . If is -consistent, then for (3.16) to hold it is sufficient to have , which does not impose any additional assumption on the scaling among beyond the one in (3.3). There are a few possible approaches that can achieve this desirable convergence rate. One may employ a two-stage approach, which selects a model in the first stage and then estimates the error variance by ordinary least-squares using only the variables in . For our bootstrap approach, we let , where is the set of active groups of the thresholded group lasso defined in (2.3). For a proper choice of the cutoff value (3.15), with high probability, selecting the strong coefficients consistently. Then the two-step approach leads to a -consistent estimator , because under Assumption 2, does not affect the convergence rate of . One can also consider a model selection procedure with a sure screening property (Fan and Lv 2008), that is, with probability tending to one. Fan et al. (2012) have shown that constructed by the two-stage approach can be -consistent if . The authors also propose a refitted cross-validation estimator of which only requires . The lasso estimator satisfies the sure screening property under a suitable beta-min condition and may be used as the model selection procedure in the above two methods for variance estimation. It is also possible to use with a different convergence rate, such as the estimators in the scaled lasso (Sun and Zhang 2012) and the scaled group lasso (Mitra and Zhang 2016). See these references for the exact convergence rate of , which may impose a different scaling among for (3.16) to hold.

3.3 Comparison to other methods

We discuss the main assumptions and conclusions of our asymptotic results, in comparison with other competing methods.

Assumption 1, imposed on the design matrix , is quite mild and holds for random Gaussian designs:

Proposition 3.4.

Assume each row of is drawn independently from with covariance matrix . Then Assumption 1 holds if and , with , for all .

The random Gaussian design, often referred to as the -Gaussian ensemble, is a very common model used in high-dimensional inference. Particularly, the de-biased lasso methods either assume the same model or use it to verify the regularity conditions on . The scaling among in (3.3) justifies the application of our method in a high-dimensional setting allowing and . If restricted to the special case of the lasso ( for all ), (3.3) requires , which turns out to be the same scaling assumed in the aforementioned de-biased lasso methods. We have assumed in (3.4) that the true coefficients of the active groups can be separated into two subsets. The subset contains strong signals under a beta-min condition on , only allowing its normalized norm to decay at a certain rate, while the subset includes small coefficients. This is a weaker assumption than the usual beta-min condition imposed on all nonzero components of . Suppose that and for . Then the normalized norm of may be of any order outside the interval . When is sufficiently small, we almost remove the beta-min condition in the sense that the normalized norm of an active group can be of any order except . To apply Theorem 3.1 to the lasso, the beta-min condition on large signals becomes . It is stronger than the minimum signal strength for variable selection consistency. This is because we did not assume any irrepresentable condition on or require the point estimator have an optimal convergence rate. By Assumption 3 it is sufficient for to have the same suboptimal rate as the group lasso and to include only the strong signal groups. These are quite reasonable assumptions satisfied by a simple thresholded group lasso. Nevertheless, the signal strength assumption (3.4) is relatively strong, since an ideal inference method should be valid for any parameter value. It will be an important future contribution to develop bootstrap inference methods for high-dimensional data without such assumptions.

The de-biased lasso estimator , constructed with a relaxed inverse of the Gram matrix , is asymptotically unbiased and can be expressed as

| (3.17) |

where is a Gaussian random vector and the bias term . This result may not be directly applicable to group inference about when . To perform group inference, Mitra and Zhang (2016) propose to de-bias the group lasso with a relaxed projection matrix for each group . The authors establish that finding is feasible for certain sub-Gaussian designs with high probability, leaving the possibility of failing to find a suitable when is finite. These methods do not rely on any beta-min condition, which is an advantage over our approach. However, the importance of our theoretical results are seen as follows. First, our results answer the fundamental question about quantifying the uncertainty in the group lasso , instead of a particular modification or function of such as the de-biased estimators. In this sense, the two approaches are not directly comparable. Second, (3.9) is a stronger result that bounds the total deviation over all groups. The uniform convergence in Corollary 3.2, not established for the de-biased group lasso, provides the theoretical foundation for simultaneous inference on a large number of groups.

Chatterjee and Lahiri (2013) establish in their Theorem 5.1 the consistency of a residual bootstrap for the adaptive lasso (Zou 2006), which can be defined via (1.2) with and specified by an initial estimator . Their beta-min condition, for some , is obviously stronger than our Assumption 2. They require to be -consistent and to satisfy some form of deviation bound, which are much more restrictive than our Assumption 3 on the initial point estimator. There are also a number of technical assumptions on the design matrix in Chatterjee and Lahiri (2013). It is not clear whether the random Gaussian design in Proposition 3.4 satisfies these assumptions. On the other hand, due to the use of the adaptive lasso, their confidence intervals will have lengths of the optimal rate , while our method applied to the lasso will construct wider intervals asymptotically, as discussed in Remark 1.

4 Numerical results

4.1 Methods and simulated data

To evaluate its finite-sample performance, we applied our parametric bootstrap method on simulated and real data sets. For each data set, we obtain a solution path of the group lasso using the R package grpreg (Breheny and Huang 2015) and choose the tuning parameter by cross-validation. Let denote the solution for the chosen and be the number of active groups of . In light of (3.15), we set the threshold value to obtain . When has or more nonzero components, we keep only its largest groups in terms of norm. Then the active coefficients of are re-computed via least-squares, and the noise variance is estimated by the residual. Given , we draw bootstrap samples of to make inference following the procedure described in Section 2.1.

We compare our method with competitors, including two methods of the de-biased lasso approach (Javanmard and Montanari 2014; van de Geer et al. 2014) and the group-bound method (Meinshausen 2015), implemented in the R package hdi (Dezeure et al. 2015) and R function SSlasso. To distinguish from the de-biased lasso method of Javanmard and Montanari (2014), we will call the method of van de Geer et al. (2014) the de-sparsified lasso. The hdi package allows the user to input an estimate of the noise variance for the de-sparsified lasso, for which we use the same estimate in our approach to make results more comparable. Other tuning parameters are chosen via the default methods in their respective implementation.

The rows of are independent draws from , with chosen from the following two designs: (i) Toeplitz, ; (ii) Exponential decay, . Recall that denotes the number of active coefficients. We adopt two distinct ways to assign active coefficients: (1) Set the first coefficients, , , to be nonzero; (2) the active coefficients are evenly spaced in . Since neighboring ’s are highly correlated in both designs, the two different ways of assigning active coefficients lead to distinct correlation patterns among the true predictors and between the true and false predictors. Index the two designs by and the two ways of assigning active coefficients by . Given and , the response is simulated from . In the first simulation study described in Sections 4.2 and 4.3, we fixed and drew for . We chose . The combination of above choices created eight different data generation settings. In each setting, we generated data sets, i.e. independent realizations of .

4.2 Group inference

We first examine the performance in group inference. The predictors were partitioned into groups of size by two different methods. In the first method, we group the active coefficients into one group and the other zero coefficients into the remaining groups, in which case there is only one active group. In the second way of grouping, there are two active groups, each containing five nonzero coefficients and five zero coefficients. We will denote these two ways of grouping by and . Clearly, the signal strength of the active groups in is weaker.

Our bootstrap method, the de-sparsified lasso, and the group-bound method were used to test the hypothesis for each group. The de-sparsified lasso method outputs a p-value for each individual test for . If , we adjust the p-value by Bonferroni correction with the group size to obtain . Then the hypothesis will be rejected at level if . For each , the group-bound method constructs a lower bound for to test the hypothesis at level . We chose and recorded the numbers of rejections among the active and the zero groups, denoted by and , respectively. Then for each method, we calculated the power and the type-I error rate, i.e. false positive rate, . Our method can build a confidence region for each group (2.2), and we recorded the coverage rate for the active groups. Note that the coverage rate for the zero groups . The other two competing methods do not construct confidence regions for a group of coefficients. The average result over the data sets in each data generation setting is reported in Table 1.

| Data Setting | bootstrap | de-sparsified | group-bound | ||||||

|---|---|---|---|---|---|---|---|---|---|

| PWR | FPR | PWR | FPR | PWR | FPR | ||||

| (1, i) | 95.0 | 95.0 | 5.5 | 100.0 | 44.2 | 0.0 | 0.0 | ||

| 92.5 | 67.5 | 5.3 | 97.5 | 48.9 | 0.0 | 0.0 | |||

| (1, ii) | 95.0 | 100.0 | 5.0 | 100.0 | 50.3 | 0.0 | 0.0 | ||

| 90.0 | 97.5 | 3.6 | 100.0 | 54.4 | 0.0 | 0.0 | |||

| (2, i) | 100.0 | 100.0 | 5.3 | 100.0 | 53.4 | 0.0 | 0.0 | ||

| 90.0 | 85.0 | 4.7 | 100.0 | 52.5 | 0.0 | 0.0 | |||

| (2, ii) | 100.0 | 100.0 | 4.2 | 100.0 | 61.8 | 0.0 | 0.0 | ||

| 100.0 | 95.0 | 4.7 | 100.0 | 61.7 | 0.0 | 0.0 | |||

| (1, i) | 95.0 | 100.0 | 4.9 | 100.0 | 42.6 | 0.0 | 0.0 | ||

| 85.0 | 75.0 | 3.2 | 100.0 | 45.4 | 0.0 | 0.0 | |||

| (1, ii) | 90.0 | 100.0 | 4.4 | 100.0 | 64.2 | 0.0 | 0.0 | ||

| 85.0 | 87.5 | 6.2 | 97.5 | 61.4 | 0.0 | 0.0 | |||

| (2, i) | 90.0 | 100.0 | 4.0 | 100.0 | 65.8 | 0.0 | 0.0 | ||

| 85.0 | 67.5 | 4.3 | 100.0 | 64.7 | 0.0 | 0.0 | |||

| (2, ii) | 100.0 | 100.0 | 4.0 | 100.0 | 74.6 | 0.0 | 0.0 | ||

| 82.5 | 90.0 | 3.0 | 100.0 | 66.6 | 0.0 | 0.0 | |||

: coverage rate of active groups; PWR: power; FPR: false positive rate.

The big picture of this comparison is very clear. Our bootstrap method shows a very satisfactory control of type-I errors, around the nominal level of for all cases, while its coverage rate for active groups is with power for a strong majority. In contrast, the de-sparsified lasso method is too optimistic with very high type-I error rates, ranging between and , and the group-bound approach is extremely conservative, resulting in no false rejections but having little power at all. Although the bias term (3.17) can be far from negligible when is finite, the de-sparsified lasso method totally ignores this term, and as a result its confidence intervals are often too narrow and its p-values become severely underestimated. On the contrary, our approach takes care of the bias in the group lasso via simulation instead of asymptotic approximation, which turns out to be very important for finite samples as suggested by the comparison. This is one of the reasons for the observed better performance of our method in Table 1. Another reason is our explicit use of the group lasso so that group structures are utilized in both the estimation of and the bootstrap simulation. These points will be further confirmed in our subsequent comparison on inference for individual coefficients.

The group-bound method is by nature a conservative approach, testing the null hypothesis for with a lower-bound of the norm . By design, the type-I error is controlled simultaneously for all groups at the significance level even if one specifies a particular group, like what we did in this comparison. It suffers from low power, especially when the group does not include all the covariates that are highly correlated with the true variables. To verify this observation, we did more test on the data sets of size . For the Toeplitz design with the first coefficients being active, its power stayed close to zero until we included the first 100 variables in the group and increased to 0.86 when including all variables. We then increased the signal strength by simulating active coefficients . In this case, the power of the group-bound method increased to 0.45 for and to 0.52 for , which are still substantially lower than the power of our bootstrap method under weaker signals; see the first row in Table 1. This numerical comparison demonstrates the advantage of our method in presence of between-group correlations, while the group-bound method might be more appropriate when groups are defined by clustering highly correlated variables together. Since its target application is different, we exclude the group-bound method from the following comparisons.

4.3 Individual inference

Since the de-sparsified lasso was designed without considering variable grouping, we conducted another set of comparisons on inference about individual coefficients. We included the de-biased lasso in these comparisons as well. For our bootstrap method, we completely ignore any group structure and set for all throughout all the steps in our implementation. Under this setting, the confidence region in (2.2) reduces to an interval. We applied the three methods on the same data sets used in the previous comparison to construct confidence intervals for individual coefficients and to test for . To save space, the detailed results are relegated to Supplemental Material. Here, we briefly summarize the key findings.

First, our bootstrap method shows an almost perfect control of the type-I error, slightly lower than but very close to , while its power is quite high, between and for almost every setting. The type-I error rate of the de-sparsified lasso is again substantially higher than the desired level. The de-biased lasso, on the other hand, is seen to be conservative with type-I error rate close to or below 1% for all the cases. Second, in terms of interval estimation, our method shows a close to coverage rate, averaging over all coefficients, with a shorter interval length than the other two competitors. Our bootstrap method built shorter intervals with coverage rate close to for zero coefficients, while the other two methods showed higher coverage rates with slightly wider intervals for active coefficients. We observe that the interval lengths between active and zero coefficients are very different for our method but are almost identical for the two de-biased lasso methods. For , the variance of the lasso is in general smaller and can be exactly zero. Our method makes use of such sparsity to improve the efficiency of interval estimation for zero coefficients. The de-biased lasso (3.17) de-sparsifies all components of the lasso, in some sense averaging the uncertainty over all coefficients. Lastly, the effect of grouping variables can be seen by comparing the results for our parametric bootstrap with those in Table 1: At almost the same level of type-I error rate, its power and coverage rate of active coefficients can be boosted substantially through either way of grouping, which numerically confirms our motivation to group coefficients for a more sensitive detection of signals.

Finally, we compared the running time between our method applied to the lasso and the de-sparsified lasso method. The time complexity of our method is in proportion to the bootstrap sample size , which has been fixed to above. We ran both methods without parallelization to make inference about all coefficients. For a wide range of choices for , our method was uniformly, in some settings more than 10 times, faster than the de-sparsified lasso. Bootstrapping the group lasso is even faster, since the group lasso in general runs faster than the lasso.

4.4 Weak and dense signals

In the second simulation study, we added a third active group of 10 coefficients to the setting of with grouping . We set the coefficients in the third group and chose . The signal of this group, in particular when , was much weaker than that of the first two groups. The vector also became denser with and . Both aspects make the data sets more challenging for an inferential method. We note that neither the sparsity condition (3.3) nor the signal strength condition (3.4) in Assumption 2 is satisfied. The results here thus can indicate how the bootstrap method works when key assumptions of our asymptotic theory are violated. To obtain accurate estimation of coverage rates in presence of such small signals, we increased the number of data sets generated in each setting to .

We applied our bootstrap method and the de-sparsified lasso with Bonferroni adjustment to perform group inference on these data sets, as we did in Section 4.2. Moreover, we conducted a Wald test with the de-sparsified lasso as follows. The asymptotic distribution of (3.17) implies that, for a fixed group of size , follows a distribution with degrees of freedom as , where is the covariance of the Gaussian random vector . Thus, one may use the statistic to test whether a group of coefficients is zero such as in . The results of the three methods are reported in Table 2. To highlight the expected difference in performance, we separately report the coverage rate and power for the strong groups, and PWRS, and those for the weak group, and PWRW.

| (1, i) | (1, ii) | (2, i) | (2, ii) | (1, i) | (1, ii) | (2, i) | (2, ii) | ||

| bootstrap | 86.0 | 86.0 | 83.0 | 84.0 | 86.0 | 87.0 | 82.0 | 87.0 | |

| 42.0 | 60.0 | 52.0 | 62.0 | 46.0 | 12.0 | 14.0 | 22.0 | ||

| PWRS | 77.0 | 94.0 | 75.0 | 94.0 | 66.0 | 94.0 | 68.0 | 87.0 | |

| PWRW | 8.0 | 6.0 | 4.0 | 6.0 | 84.0 | 54.0 | 70.0 | 78.0 | |

| FPR | 4.9 | 4.2 | 5.0 | 4.1 | 2.6 | 3.6 | 3.2 | 2.2 | |

| de-sparsified | PWRS | 99.0 | 99.0 | 100.0 | 100.0 | 97.0 | 99.0 | 98.0 | 97.0 |

| (Bonferroni) | PWRW | 18.0 | 32.0 | 8.0 | 20.0 | 84.0 | 48.0 | 70.0 | 78.0 |

| FPR | 20.8 | 23.9 | 16.2 | 18.6 | 18.2 | 27.5 | 16.9 | 19.1 | |

| de-sparsified | PWRS | 71.0 | 88.0 | 83.0 | 91.0 | 58.0 | 85.0 | 70.0 | 81.0 |

| (Wald) | PWRW | 0.0 | 0.0 | 0.0 | 0.0 | 30.0 | 0.0 | 0.0 | 0.2 |

| FPR | 0.0 | 0.2 | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.3 | |

, : coverage rate for strong and weak signal groups, respectively; PWRS, PWRW: power for strong and weak signal groups, respectively; FPR: false positive rate.

Again our bootstrap method achieved a good control of type-I error rate, all around or below 5%. The coverage rate and power for the strong groups are comparable to those in Table 1, indicating that they were not affected by the inclusion of a weak group. The power for detecting the third group is low when , which is fully expected given the low signal strength, and becomes much higher when is increased to . As discussed above, the data simulated here do not satisfy Assumption 2. As a consequence, the bootstrap samples might not provide a good approximation to the sampling distribution, which could be a reason for the low coverage rate of the weak group. We observe that was in general higher when than when . This is because with is closer to the requirement in (3.4) for small coefficients. The de-sparsified lasso with Bonferroni correction failed to control the type-I error rate at the desired level. While it shows a higher detection power for the weak group when , its power is largely comparable to our method when . The gain in power could simply be the result of high false positive rates. Compared to Table 1, we see a decrease in the false positive rates. This is because the error variance was overestimated for these data sets, which alleviated the underestimate of p-values by the de-sparsified lasso. On the contrary, the Wald test seems too conservative, almost never rejecting any zero group. Its power of detecting the weak group is close to zero for most of the cases. These results are the consequence of ignoring the term in (3.17), which introduces systematic bias in the Wald test statistic for finite samples. This numerical comparison demonstrates the advantage of our bootstrap method in the existence of weak coefficient groups under a relatively dense setting.

4.5 Real data designs

We further tested our method on design matrices drawn from a gene expression data set (Ivanova et al. 2006), which contains expression profiles for about mouse genes across samples. The expression profile of each gene was transformed to a standard normal distribution via quantile transformation. The following procedure was used to generate data sets for our comparison. First, randomly pick genes and denote their expression profiles by for . We calculate the correlation coefficients among ’s and the total absolute correlation for each gene . For the gene with the highest , we identify the genes that have the highest absolute correlation with this gene. These genes are put into one group of size . Then we remove them from the gene set and repeat this grouping process until we partition all genes into groups. This grouping mechanism results in high correlation among covariates in the same group. Next, fixing the first groups to be active, we draw their coefficients . The parameters in the above procedure were chosen as , , , and . For each combination of , we obtained independent realizations of . Given each realization, a range of the noise variance was then used to simulate the response . Compared to the data generation settings in Section 4.1, data sets in this subsection have a smaller sample size but a higher dimension , and the correlation among the covariates is much higher. These put great challenges on an inferential method.

| Data Setting | Group inference | Individual inference () | |||||||

|---|---|---|---|---|---|---|---|---|---|

| bootstrap | bootstrap | de-sparsified lasso | |||||||

| PWR | FPR | PWR | FPR | PWR | FPR | PWR∗ | |||

| 0.1 | 50.3 | 1.6 | 14.2 | 3.1 | 41.9 | 19.3 | 12.9 | ||

| 0.5 | 24.7 | 1.8 | 13.1 | 3.1 | 36.1 | 15.0 | 12.0 | ||

| 1 | 24.7 | 2.4 | 12.0 | 3.0 | 31.8 | 12.7 | 13.0 | ||

| 0.1 | 61.3 | 1.0 | 15.7 | 3.3 | 51.0 | 27.1 | 13.2 | ||

| 0.5 | 54.7 | 1.1 | 15.0 | 3.2 | 46.2 | 21.0 | 10.7 | ||

| 1 | 48.7 | 1.2 | 15.1 | 3.4 | 47.3 | 22.4 | 11.2 | ||

| 0.1 | 58.7 | 1.4 | 14.9 | 3.1 | 48.5 | 24.4 | 14.3 | ||

| 0.5 | 57.7 | 1.2 | 14.9 | 3.1 | 43.1 | 20.0 | 10.8 | ||

| 1 | 55.7 | 0.9 | 14.2 | 3.1 | 44.4 | 19.2 | 14.3 | ||

| 0.1 | 41.0 | 1.1 | 12.4 | 2.0 | 36.3 | 14.0 | 12.0 | ||

| 0.5 | 29.3 | 2.0 | 11.5 | 2.0 | 29.8 | 10.6 | 15.3 | ||

| 1 | 30.3 | 1.1 | 10.4 | 1.8 | 29.4 | 10.5 | 13.2 | ||

| 0.1 | 41.0 | 0.8 | 13.9 | 2.1 | 34.8 | 13.9 | 14.2 | ||

| 0.5 | 33.7 | 0.7 | 12.2 | 2.1 | 37.4 | 15.5 | 13.8 | ||

| 1 | 46.7 | 1.3 | 12.8 | 2.1 | 39.5 | 17.7 | 13.4 | ||

| 0.1 | 50.0 | 1.0 | 12.4 | 2.1 | 33.6 | 12.3 | 13.9 | ||

| 0.5 | 47.7 | 0.9 | 12.8 | 2.1 | 34.3 | 14.3 | 10.9 | ||

| 1 | 45.7 | 0.8 | 11.8 | 2.1 | 36.9 | 15.9 | 11.9 | ||

FPR: false positive rate; PWR: power; PWR∗: power of the de-sparsified lasso after matching false positive rate to 5%.

We applied both the bootstrap and the de-sparsified lasso methods to perform group inference as we did in Section 4.2. As reported in Table 3, our bootstrap method gives a good and slightly conservative control over type-I errors, with false positive rates all close to but below , the desired level. Its power in general increases as the signal-to-noise ratio increases and is seen to be around 0.5 when the signal-to-noise ratio is reasonably high. On the contrary, the type-I error rate of the de-sparsified lasso method, not reported in the table, was even for most of the cases, showing that it failed to provide an acceptable p-value approximation for these data sets. This might be caused by the facts that this method is not designed for group inference and that is too small for asymptotic approximation. To conduct a complete comparison, we then used both methods to make inference about individual coefficients as in Section 4.3, in which the group structures were totally ignored in our method by setting all . Our method again controlled the type-I error to a level slightly lower than , but showed a decrease in power, as expected, without utilizing grouping. The false positive rate of the de-sparsified lasso became smaller for individual inference, ranging between and , but still far from the desired level of . This makes it difficult to compare power between the two methods, as the observed higher power of one method could simply come at the cost of more false positives. To resolve this issue, we sorted the p-values for all the zero coefficients output from the de-sparsified lasso method, and chose a cutoff such that of them would be rejected. In this way, the false positive rate by definition is always , slightly higher than that of our bootstrap method, while the corresponding power becomes largely comparable. We also noticed that the overestimate of the significance level by the de-sparsified lasso method was severe for these data sets: To achieve the target type-I error rate of , the cutoff for its p-values turned out to be for all the settings and was even much smaller for many of them.

This comparison shows that our parametric bootstrap method can achieve a desired level of false positive control in presence of high correlation among a large number of predictors. It again confirms that grouping variables can lead to substantial power gain.

4.6 Sensitivity to thresholding

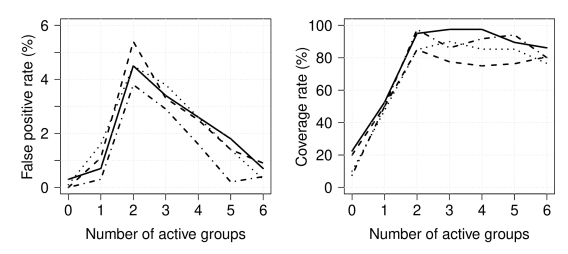

With chosen by cross-validation, the only parameter that requires user input in our method is the threshold value . The following experiment has been conducted to examine how sensitive our method is to this parameter. Given the group lasso solution , we reorder its groups so that . Then we choose a range of threshold values, , such that the thresholded has active groups for , say . We applied this procedure on the simulated data sets generated from the four settings with and in Table 1, which have active groups. These were the most difficult settings for which our bootstrap method had the lowest power and coverage rate . Figure 1 plots the curve of the false positive rate and the curve of the active group coverage rate against , the number of active groups after thresholding, in each of the four settings.

The false positive rates are well-controlled at the desired level of for all the threshold values. They are around 0.05 when is well-chosen so that has active groups, and become smaller when deviates from the optimal value. This suggests that our method is not sensitive to the threshold value in terms of type-I error control. The coverage of the active groups stays at a high level when contains two or more active groups, but can be substantially lower if one or both of the true active groups are missing. Thus, including a few zero groups in the active set of will not hurt the performance of our method that much, since via refitted least-squares, the estimated coefficients of these groups tend to be small. Similar patterns were observed for inference on individual coefficients, when was chosen for to have up to 30 nonzero coefficients while the true active set contained only variables.

5 Generalizations and discussions

5.1 Block lasso and sub-Gaussian error

The bootstrap method outlined in Section 2.1 can be generalized to other sparse regularization methods under different error distributions in an obvious way. However, the difficulty is to validate such generalizations theoretically. In this subsection, we provide theory for two generalizations: First, we assume that the error vector is zero-mean sub-Gaussian. Second, we consider the general -group norm (1.3) for and correspondingly the block lasso estimator

| (5.1) |

Our method is essentially to bootstrap the block lasso under a sub-Gaussian error distribution. We assume the error distribution is given from which we can draw . Define , , and as in (3.1) but with , and denoting the corresponding block lasso estimates instead.

Recall that is conjugate to . To establish asymptotic theory for bootstrapping the block lasso, we need a modified version of Assumption 2:

Assumption 4.

The true coefficient vector is sparse:

| (5.2) |

and such that

| (5.3) |

where .

Together with a proper choice of , we can now generalize Theorem 3.1 to the block lasso.

Theorem 5.1.

The assumptions of this theorem are in parallel to those of Theorem 3.1. The differences appear in Assumption 4 on and the order of (5.4), both reducing to the corresponding assumptions in Theorem 3.1 when . This theorem does not include the case . For this case, we need to impose an additional assumption on the margin of defined as follows. For , let be a permutation of the set such that . Define the margin of by

| (5.7) |

Theorem 5.2.

The additional assumption on the margin of ensures that the norm is differentiable in a neighborhood of . Letting in (5.2) and (5.4), we have

It is seen that assumption (5.8) is quite mild, allowing the margin of to decay to zero.

Let be defined by for the block lasso . We can obtain similar result as that in Corollary 3.2 for , although it is unclear when would become optimal in this more general case for statistical inference. We have assumed that the error distribution is known, , in the above. This may be relaxed to using an estimated error distribution. If we assume that the only unknown parameter of the sub-Gaussian error distribution is a scale parameter, one can show that a point estimator satisfying certain convergence rate will suffice for establishing the above theorems. More general situations are to be studied in the future.

5.2 Future work

We have developed asymptotic theory on the consistency of a parametric bootstrap method for group norm penalized estimators, which allows for the use of simulation to construct interval estimates and quantify estimation uncertainty under group sparsity. Due to the intrinsic bias of a sparse penalized estimator, however, the length of an estimated interval, in general, may not be on the order of the optimal parametric rate of ; see, for example, (3.12). One possible improvement is to simulate from a less biased estimator instead, such as the de-biased estimator in Zhang and Zhang (2014) and van de Geer et al. (2014), as discussed in Section 3.3. In order to reach the optimal rate, the authors rely on solving lasso problems to obtain the relaxed inverse , which becomes a computational bottleneck for this approach. We may use a different relaxed inverse that is computationally cheaper to define the de-biased estimator . The same bootstrap method can be applied to approximate the distribution, , with determined by the convergence rate of . If converges at a faster rate as it is less biased than the group lasso , the confidence intervals will be shorter asymptotically. Using the bootstrap instead of asymptotic approximation, this approach is also expected to have superior finite-sample performance, as was observed in the numerical comparisons in Section 4. In a similar spirit, Ning and Liu (2017) used a bootstrap strategy to approximate the distribution of their decorrelated score function for high-dimensional inference.

We have proposed multiple approaches that can provide a point estimate for our bootstrap method. However, it is arguable that thresholding the group lasso is still the most convenient choice in practice, without solving another optimization problem. From this perspective, an interesting future direction is to develop a method to determine an appropriate threshold value from data. It remains to find out whether Assumption 3 on is a necessary condition by further analysis. At least, the numerical results in Section 4.6 seem to suggest that this may not be the case. Another future direction is to develop estimator augmentation (Zhou 2014) under group sparsity, which, by employing Monte Carlo methods, could offer great flexibility in sampling from the distribution of a sparse regularized estimator.

Supplemental Material

Appendix A Proofs of results in Section 3

A.1 Preliminaries and published results

Throughout Sections A and B, we assume that and for all with the positive constants . Let be the Gram matrix, , and . To motivate the definitions of the centered and rescaled estimators in (3.1), we note that the penalized loss in (1.2), up to an additive constant, is identical to

| (A.1) |

where . Put . It follows from (3.1) that

| (A.2) | ||||

| (A.3) | ||||

| (A.4) |

We wish to approximate the distribution by the conditional distribution .

We first collect relevant existing results on the group lasso. The most relevant are the upper bounds of the and the errors of the group lasso, under the restricted eigenvalue assumption. For , define the cone

| (A.5) |

Assumption S1 (RE()).

For ,

| (A.6) |

This assumption is used by Lounici et al. (2011) to derive error bounds for the group lasso, which generalizes the restricted eigenvalue assumption for regularization (Bickel et al. 2009). The restricted eigenvalue assumption, or the closely related compatibility condition (van de Geer and Bühlmann 2009), is one of the weakest on the design matrix for obtaining useful results for the lasso and its variates. We state the following result on relevant error bounds for the group lasso from Theorem 3.1 and its proof in Lounici et al. (2011). Let and denote, respectively, the minimum and the maximum of .

Theorem A.1.

Another key result is the following inequality from Proposition 1 in Negahban et al. (2012), which has been used to establish the so-called restricted strong convexity condition for least-squares loss under group norm regularization.

Lemma A.2.

Let , , and

| (A.10) |

where is conjugate to satisfying . Assume that each row of is drawn independently from with . Then there are positive constants that depend only on such that, with probability greater than ,

| (A.11) |

We have assumed (A.11) in Assumption 1. The above lemma shows that this assumption holds with high probability for the random Gaussian design. It is likely that (A.11) also holds with high probability for sub-Gaussian designs, as suggested by the analysis of Rudelson and Zhou (2013). Moreover, the restricted eigenvalue assumption is implied by inequality (A.11) when is large:

Lemma A.3.

Assume (A.11) holds. Then Assumption RE holds with if , where and depends only on .

A.2 Proof overview

A key step in the proof of Theorem 3.1 is to establish the nonasymptotic bound for contained in Theorem A.7, from which the main asymptotic results follow. Before going through the details, we briefly overview the basic ideas behind the proof.

Let be a fixed design matrix such that (A.11) holds. Put . Our goal is then to find an upper bound, say , such that is close to one for a large set of ; see (A.24) in Theorem A.7. Rewrite (A.11) for as

which shows that we need to control three terms, , and . Lemma C.2 below provides an upper bound for , which reduces to

| (A.12) |

for . The bounds for the other two terms will be developed conditioning on a few events. Let and be constants. We define

| (A.13) |

and ,

| (A.14) |

and by

| (A.15) |

Consider events

| (A.16) | ||||

| (A.17) | ||||

| (A.18) |

where is defined in (3.5). For a fixed , the first two events are in the probability space for while is in the joint probability space for and . By Theorem A.1, can be bounded using (A.7) on the event . We will find an upper bound for in Lemma A.5 on the event . Putting together, for we have

for every . By Lemma A.6, the last conditional probability reduces to . This leads to the nonasymptotic bound in Theorem A.7. We further show that and under our asymptotic framework to establish the main results.

The upper bound for is established by next two lemmas, of which the first is a special case of Lemma C.4. Define

| (A.19) |

where is the same constant as in (A.17) and (A.18). By definition for .

Lemma A.4.

For any , and , we have

| (A.20) |

Suppose is sufficiently small. The assumptions on and can be expressed in a more explicit way to show that the estimate is close to . The subset contains active groups with a large norm and for . For , by definition is small or zero, and according to (A.15).

Lemma A.6.

Assume that , and . Choose . Suppose that (A.11) holds with universal constants when is large. Then for every , there is such that

| (A.22) |

when .

As an immediate consequence of (A.22), for any and ,

| (A.23) |

when . Now we are ready to establish a nonasymptotic bound for the deviation , regarding as a fixed matrix that satisfies a couple assumptions.

Theorem A.7.

Our proof of Theorem 3.1 is based on Theorem A.7. We will show that the assumptions for (A.24) are satisfied with high probability and then derive the desired conclusions from there. For the detailed proof, see Section A.4.

Remark S1.

In step 2 of the proof of Theorem 3.1, the exact order of the upper bound in (A.24) is derived: Conditioning on a large set of ,

| (A.25) |

which under Assumption 2 implies . Under orthogonal designs, (A.11) holds with and . Then the upper bound can be improved to , and consequently, the last term on the right side of (A.25) drops.

A.3 Proofs of auxiliary results

Proof of Lemma A.3.

We prove an inequality that will be used in the proofs of a few results.

Lemma A.8.

Let be any minimizer of for and . Then for any ,

| (A.26) |

Proof.

Proof of Lemma A.5.

Proof of Lemma A.6.

We prove by contradiction. Condition on , and suppose , that is, happens. For , define function

which is subadditive and continuous. By our hypothesis, . Thus, there is such that , since . Let . By (A.4),

| (A.30) |

Since , (A.4) applies to both and . Using a similar argument as in (A.3), we can show that

where . If , then

| (A.31) |

where the second inequality is due to the convexity of . This leads to a contradiction. Therefore, it remains to show when is greater than some . According to (A.11), a sufficient condition for this is

| (A.32) |

The first term

where the subadditivity of is used for the second inequality. The third term by assumption. By Lemma A.3, (A.11) implies RE when and . Since for , by (A.7) in Theorem A.1, on event we have and with , which implies

| (A.33) |

Since , the second term

| (A.34) |

where we have used the facts that and both and are . Therefore, (A.32) holds, and a contradiction is reached when is large. ∎

A.4 Proofs of main results

Proof of Theorem 3.1.

The proof is broken down into four steps.

Step 1: We verify all the assumptions of Theorems A.1 and A.7 hold with high probability. Since , by Lemma A.3 and Assumption 1, RE is satisfied with high probability for any and . As a consequence of Assumption 1, , and thus a suitable choice of satisfies (A.9). The above arguments show that all the assumptions of Theorem A.1 are satisfied with high probability. Put . We see that and in (A.7) and (A.8) are bounded from below by a positive constant, and therefore and . It follows from (3.7) that

which implies . Consequently, the order of is given by

| (A.35) |

Then, (3.4) implies that, when is large, and , with and defined by (A.13). We will show in Step 2 that and invoke Lemma A.6 to obtain (A.22) when is large. Thus, all the assumptions of Theorem A.7 are satisfied with high probability.

Step 2: We demonstrate that the upper bound for in (A.24) is . It is immediate that

by (A.35), (A.12) and (3.3). To bound (A.4), we first show that . Recall the respective definitions of , and in (3.6), (A.14) and (A.19). For ,

| (A.36) |

On the other hand, by (3.4) and (A.35),

| (A.37) |

and thus . It then follows from (A.4) that

| (A.38) |

by plugging (A.37) and (3.4) in the first and the second term, respectively.

Proof of Corollary 3.2.

Proof of Proposition 3.3.

By Assumption 1, with defined in (A.39), which then implies that RE holds with high probability. Under Assumption 2,

where is as in (A.8) with . Since , it follows from (A.8) that

where is defined in Theorem A.1. Thus, only the strong coefficient groups in will be kept after thresholding. Conditioning on the event ,

where the first line comes from (3.7) and the second from (3.4) with . This shows that and completes the proof. ∎

Proof of Proposition 3.4.

By Lemma A.2, with high probability, (A.11) is satisfied with constants and ; see the proof of Proposition 1 in Negahban et al. (2012). If for all , we can find universal constants such that

This shows that (A.11) holds with universal constants . Put . Since and ,

for any given , according to the proof of Proposition 2 in Zhang and Huang (2008). ∎

Appendix B Estimation of error variance

B.1 Problem setup

Let be an estimator of when it is unknown. Recall that in our bootstrap method we draw . Put and define as in (A.4). We want to show that, with high probability, the conditional distribution is close to . In this case, the distribution of is different from that of . To facilitate our analysis, let

| (B.1) |

Since , we have . Our goal is then to bound for a large set of . By triangle inequality,

where is as in (A.3). The difference in the first term on the right is the result of using an estimated instead of and can be bounded by Theorem A.7 conditioning on any . In what follows, we will derive a bound for the second term, which represents the effect of using a different noise level than the true in the above simulation. Proofs of all the results in this section can be found in Section B.4.

B.2 Main results

For , define

| (B.2) | ||||

| (B.3) |

Lemma B.1.

For notational brevity, put

| (B.5) |

so that the upper bound in (B.4) is . Assuming (A.11), we can bound conditional on , in analogy to Theorem A.7.

Theorem B.2.

Under the asymptotic framework introduced in Section 3.1, we obtain the main results when an estimator of the unknown error variance is used in the simulation procedure. Recall that is defined via (3.7).

Theorem B.3.

By the same argument, we can establish the conclusion in Corollary 3.2 conditioning on , which extends our inferential framework to the use of an estimated noise level.

B.3 Lasso as a special case

Let for all , and . Consider a simpler situation with in Assumption 2, i.e., all active coefficients satisfy the beta-min condition. In this case, (A.12) and (A.4). Under the assumptions of Theorems A.7 and B.2, we may combine (A.24) and (B.6) to obtain

| (B.8) |

in probability for the lasso. Plugging in , and that due to Lemma A.3, the upper bound

where and are positive constants. Under the scaling (3.3), , since represents the convergence rate of . Consequently, .

Under comparable conditions, Theorem 4 in Zhou (2014) contains a similar bound for the lasso,

where , , and

Note that here is the set of nonzero components of . By definition for . It is thus necessary to have for to be of the same order as . However, by Lemma B.4 below, with nearly full measure for column-normalized design matrices, and therefore, it is necessary that . This severely limits the growth of the dimension , as compared to the scaling of for . We see that, in addition to the substantial generalization to groups of unbounded size, this work also greatly improves the result in Zhou (2014) even for the special case of the lasso.

Let be the -dimensional unit sphere. The following lemma contains bounds for , assuming that the columns of are normalized so that for all .

Lemma B.4.

Assume that , is drawn independently and uniformly over for , and follows the -distribution with degrees of freedom. Then for every ,

| (B.9) |

where for all .

Remark S2.

In this lemma, the distribution of is assumed to be the uniform measure over all matrices with normalized columns. The result shows that the bounds for apply to most of such matrices, with nearly full measure as .

B.4 Proofs

Proof of Lemma B.1.

This result can be obtained by a straightforward generalization of Lemma 8 in Zhou (2014). ∎

Proof of Theorem B.2.

For , we have

and thus for all . Consequently, implies that for and therefore, by Theorem A.1, . On the other hand, obviously implies (A.16) and thus . By (A.11) with ,

where (B.4) and triangle inequality are used in the second line. Then (B.6) follows since the above inequality holds on for any . ∎

Proof of Theorem B.3.

Following the same reasoning in the proof of Theorem 3.1, all assumptions on in Theorem B.2 are satisfied with high probability and . A consequence of assumption (3.16) is that for some , which then implies . By Theorem B.2, with probability tending to one,

Since (3.16) implies that in probability, choosing a suitable guarantees that with high probability. Thus, for every ,

| (B.10) |

Since Theorem 3.1 applies for every , it follows from (3.9) that

| (B.11) |

Appendix C Proofs of results in Section 5

C.1 Error bounds for the block lasso

Recall that is conjugate to . We first develop error bounds for the block lasso (5.1) under a sub-Gaussian error. That is, for any fixed ,

| (C.1) |

where is a constant. Define the operator norm for , , by

Assumption S2 (Block normalization).

This assumption will be satisfied if , since

By Proposition 3.4, if the rows of are independent draws from , then with high probability, and thus Assumption S2 holds. This shows that it is indeed a reasonable and mild assumption.

The following theorem generalizes Theorem A.1 to the use of the -group norm for based on the results in Negahban et al. (2012).

Theorem C.1.

To prove this theorem, we establish in the following lemma an upper bound for (A.10), which will be used in the proofs of a few other key results.

Lemma C.2.

Let and . Then for ,

| (C.7) |

Proof.

We first bound . Let be independent random variables with , and put . Then by definition (A.10), we have

due to the concavity of . By (4.3) in Laurent and Massart (2000), for any ,

| (C.8) |

For , and thus

Equivalently,

| (C.9) |

for . Now for every we have

where (C.9) is used in the second inequality. Taking gives

when and thus,

| (C.10) |

Proof of Theorem C.1.

The desired results follow from Corollary 1 in Negahban et al. (2012). Define

We verify that the restricted strong convexity condition (Negahban et al. 2012) holds over . This amounts to verifying that, for ,

| (C.11) |

where is a positive constant. Since

for and , it follows from (A.11) that

Simple algebra with (C.7) shows that when (C.5) holds, which leads to in (C.11). All the other assumptions of Corollary 1 in Negahban et al. (2012) can be verified as in the proof of their Corollary 4. Then (C.3) and (C.4) follow immediately by plugging in and the compatibility constant . Thus we have shown that (C.3) and (C.4) hold on the event . It remains to show the lower bound for with the choice of in (C.6). With some modifications of the proof of Lemma 5 in Negahban et al. (2012), one can show that

| (C.12) |

for all and under Assumption S2. Setting

and applying the union bound over all , we have

which completes the proof. ∎

C.2 Proofs of Theorems 5.1 and 5.2

Generalize the definition of in (A.1) to

| (C.13) |

which is identical to the penalized loss function in (5.1), up to an additive constant, when for all . Suppose . Letting , we have

| (C.14) | ||||

| (C.15) |

We first bound the eigenvalues of the Hessian of the norm, and then generalize a few lemmas in Section A.2 before our proof of Theorems 5.1 and 5.2.

Lemma C.3.

Let and be the Hessian of evaluated at when exists. If and , then

| (C.16) |

Proof.

Let . For , straightforward calculations lead to

| (C.17) |

and second-order partial derivatives

Let . Then for ,

| (C.18) |

Since for some , is positive semi-definite and for all . By definition . Therefore,

On the other hand, is a direct consequence of the convexity of . When , and for . This completes the proof. ∎

Remark S3.

If for some and for all , then

for . Thus, the upper bound in (C.16) can be decreased by no more than a factor of .

Recall that is a constant. For , define

| (C.19) |

and . For define

| (C.20) | ||||

| (C.21) |

and

| (C.22) |

which generalize the definitions of , , and in Section A.2. For , we have . The following two lemmas bound the difference in when is replaced by .

Lemma C.4.

Assume that . Then for any , and as defined in (3.5),

| (C.23) |

Proof.

Put and

It follows from (C.22) that

First consider . The assumption in (C.22) implies

With (C.20) and by (3.5), this leads to

| (C.24) |

since . Two direct consequences of (C.24) are

and . Therefore, the function , , is differentiable in the ball centered at or with radius . By the mean value theorem,

| (C.25) | ||||

| (C.26) |

where and for some . Let and . For any ,

where and the last inequality follows from (C.24). Thus, the mapping is differentiable at for every ; see (C.17) and (C.18). By Theorem 5.19 in Rudin (1976), there exits such that

It then follows from Lemma C.3 that

| (C.27) |

Triangle inequality applied to (C.27) with and gives

Together with and the definitions of and , we obtain the following bound for all ,

| (C.28) |

For , by definition (C.22) we have and thus

| (C.29) |

by triangle inequality. The desired upper bound follows immediately by combining (C.2) and (C.29). ∎

For , an additional assumption on the margin of is needed to bound the difference between and . Following the definition in (5.7), let if . It is easy to show that for any ,

and the function is differentiable at :

| (C.30) |

where is the th unit vector in . If for all , define

| (C.31) | ||||

| (C.32) |

Lemma C.5.

Let , , and assume that

| (C.33) |

Then for any and , we have

| (C.34) |

Proof.

Let . Define , , and for . We will show that for every . Assumption (C.33) implies that

and consequently,

| (C.35) |

It then follows that

Again by (C.35) we have and

Then since lies between and . By (C.30) with ,

Now we arrive at (C.25), (C.26), and , which implies for all . Then (C.34) follows immediately from (C.29) with . ∎

Our next result is the counterpart of Lemma A.6. Define three events, and as in (A.17) and (A.18), and

| (C.36) |

Lemma C.6.

Proof.

With simple modifications, the proof follows closely to that of Lemma A.6. The only difference is to show

| (C.38) |

instead of (A.32), where for some . It then suffices to show that the second term is . Since for , it follows from Theorem C.1 that on we have and , which implies

As ,

| (C.39) |

by (5.4), the upper bound for (C.7), and the assumption (C.37). ∎

We are now in a position to prove the main results.

Proof of Theorem 5.1.

First, we note that Lemma A.5 holds with in place of . That is, implies

Following a similar proof as that of Theorem A.7, together with Lemma C.6, we can show that on the event ,

| (C.40) |

when . Next, we show that and , in place of (A.37) and (A.38) in the proof of Theorem 3.1. By (C.21) and (5.3)

| (C.41) |

where the second step is due to the choice of (5.4). It then follows from (A.35) that . Similar to (A.36), for . Thus, from (C.4) we have

by (C.41) and (5.3). Furthermore, by (C.39). Therefore, the upper bound for in (C.40) is . Then, one may show all the desired results by an essentially identical proof to that of Theorem 3.1. ∎

Appendix D Supplemental numerical results

D.1 Results for individual inference

Let , and denote the coverage rates for active, zero, and all coefficients, respectively, and let , and be the corresponding average interval lengths. Note that reports the type-I error rate of the test, , for , and the power can be calculated by checking whether or not an estimated interval for an active coefficient covers zero. Reported in Table S1 are the average results for each of the eight data generation settings in the first simulation study.

| Data Setting | Method | PWR | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1, i) | bootstrap | 54.0 | 43.5 | 0.456 | 96.7 | 0.136 | 94.0 | 0.152 | |

| de-sparsified | 67.5 | 76.5 | 0.540 | 89.3 | 0.542 | 88.6 | 0.542 | ||

| de-biased | 60.0 | 81.0 | 0.566 | 98.8 | 0.568 | 97.9 | 0.568 | ||

| (1, ii) | bootstrap | 61.0 | 56.5 | 0.414 | 96.4 | 0.110 | 94.4 | 0.127 | |

| de-sparsified | 74.5 | 74.5 | 0.434 | 86.1 | 0.433 | 85.6 | 0.433 | ||

| de-biased | 68.0 | 83.0 | 0.443 | 98.8 | 0.441 | 98.1 | 0.441 | ||

| (2, i) | bootstrap | 60.5 | 54.5 | 0.426 | 96.2 | 0.131 | 94.1 | 0.146 | |

| de-sparsified | 70.0 | 79.0 | 0.498 | 85.1 | 0.503 | 84.8 | 0.503 | ||

| de-biased | 60.0 | 95.0 | 0.519 | 98.9 | 0.525 | 98.7 | 0.525 | ||

| (2, ii) | bootstrap | 72.0 | 60.0 | 0.408 | 96.2 | 0.138 | 94.4 | 0.152 | |

| de-sparsified | 79.5 | 85.0 | 0.422 | 82.8 | 0.420 | 82.9 | 0.420 | ||

| de-biased | 72.0 | 96.0 | 0.443 | 99.1 | 0.441 | 99.0 | 0.442 | ||

| (1, i) | bootstrap | 47.0 | 35.5 | 0.335 | 96.2 | 0.065 | 94.7 | 0.071 | |

| de-sparsified | 65.0 | 74.0 | 0.537 | 85.0 | 0.539 | 84.8 | 0.539 | ||

| de-biased | 53.0 | 73.5 | 0.523 | 99.1 | 0.526 | 98.5 | 0.526 | ||

| (1, ii) | bootstrap | 59.5 | 41.5 | 0.359 | 96.9 | 0.077 | 95.5 | 0.084 | |

| de-sparsified | 70.5 | 69.0 | 0.485 | 88.4 | 0.483 | 88.0 | 0.483 | ||

| de-biased | 64.0 | 68.5 | 0.429 | 99.2 | 0.428 | 98.4 | 0.428 | ||

| (2, i) | bootstrap | 62.0 | 46.5 | 0.416 | 96.5 | 0.095 | 95.3 | 0.103 | |

| de-sparsified | 72.0 | 85.5 | 0.550 | 83.3 | 0.554 | 83.4 | 0.554 | ||

| de-biased | 65.5 | 89.0 | 0.506 | 99.3 | 0.510 | 99.1 | 0.510 | ||

| (2, ii) | bootstrap | 71.0 | 40.5 | 0.374 | 96.8 | 0.099 | 95.4 | 0.106 | |

| de-sparsified | 78.5 | 83.5 | 0.501 | 81.2 | 0.499 | 81.2 | 0.499 | ||

| de-biased | 73.0 | 85.0 | 0.445 | 99.2 | 0.444 | 98.8 | 0.444 | ||

PWR: power; : coverage rate; interval length.

Largely consistent with the results in Table 1, we see that our bootstrap method shows a good control of the type-I error, implied by the observation that , the coverage rate for zero coefficients, is slightly greater than but very close to . The for the de-sparsified lasso method is uniformly lower than , dropping to in some cases, implying that its type-I error rate is again substantially higher than the desired level of . Although this might lead to some moderate degree of increase in power, we argue that a strict control of false discoveries is critical for large-scale screening when is large and . For instance, the type-I error rate of the de-sparsified lasso is around for . This means that it brought about more than expected false positives, which was much larger than the number of true positives . This would be a severe disadvantage of the de-sparsified lasso method in the typical high-dimensional and sparse setting, , under which the method was developed. The de-biased lasso, on the contrary, reached very high coverage of zero coefficients, close to or above 99% for all the cases. Its coverage of nonzero coefficients is also seen to be higher than the other two methods. However, the coverage rates for active coefficients of all three methods can be substantially lower than the desired level in many cases. For our method, this was caused by the inaccuracy in detecting active coefficients by thresholding a lasso estimate, which kept only 30% to 40% of them for the case . Even including the largest 20 components of the lasso would still identify of the true active variables. Furthermore, without grouping the signal strength became small and Assumption 2 was not satisfied, as was uniformly distributed over .

To give a concrete illustration of the effect of grouping variables, for the setting grouping improved the power of our method from to or and increased its from to or , depending on the way of grouping. Grouping may also serve as a remedy for the observed low power of the bootstrap method in individual inference. Given identified active groups, detection of individual nonzero coefficients becomes an easier job due to the substantial dimension reduction.

D.2 Running time