Bayesian inference for latent factor GARCH models

Abstract

Latent factor GARCH models are difficult to estimate using Bayesian methods because standard Markov chain Monte Carlo samplers produce slowly mixing and inefficient

draws from the posterior distributions of the model parameters. This paper describes how to apply the particle Gibbs algorithm to estimate factor GARCH models efficiently. The method has two advantages over previous approaches. First, it

generalises in a straightfoward way to models with multiple factors and to various members of the GARCH family. Second,

it scales up well as the dimension of the observation vector increases.

Keywords: Particle Gibbs; Reversible jump

JEL codes: C11, C38.

1 Introduction

This paper discusses latent factor generalised autoregressive conditionally heteroscedastic (GARCH) models. Factor GARCH models play two roles. The first is that they are a convenient type of multivariate GARCH model (Bauwens et al., 2006), in which the factor structure provides a direct and parsimonious way to model the effects of time-varying volatility in a multivariate setting. Second, they are a natural extension of the latent factor model approach to time series modelling. For instance, factor models have a good track record in macroeconomic time series analysis (Stock and Watson, 2002), and the addition of GARCH errors could improve a model’s fit when the observations are conditionally heteroscedastic.

The use of factor GARCH models in a Bayesian context has been hampered by their computational difficulty. While it is possible to use single-move MCMC methods for this class of models, the resulting draws only explore the posterior distribution of the parameter vector slowly and inefficiently (Fiorentini et al., 2004). These methods are also difficult to implement in models with more than one latent factor.

The main contribution of our article is to demonstrate that the particle Gibbs sampler (Andrieu et al., 2010) is particularly well suited to nonlinear latent factor models with a GARCH structure because we can use a fully adapted particle filter (Pitt and Shephard, 1999) to produce rapidly mixing draws from the parameter vector. Our article shows that the method can handle multiple factors and can be easily be generalised to apply to other members of the GARCH family. The statistical structure of factor GARCH models means that the method scales well with the dimension of the observation vector because the variability in the estimated likelihood due to generating the latent factors decreases as the dimension of the observation vector increases. Our article also shows that in certain cases we can make the inference invariant to the order of the elements in the vector of the dependent variable, while in the general case we take care to ensure that the empirical results are invariant to the order. Although not shown in this article, it is clear that our method will accommodate regime changes and structural breaks in a straightforward way.

2 Inference

We consider a factor model given by

| (1) |

where is an vector of observations, is a vector of latent factors (where ), and is an vector of idiosyncratic errors. The distributions of and can be chosen in many ways. Our focus is on versions of (1) in which the latent factors have volatilities given by GARCH processes, so that

| (2) | ||||

| (3) |

for . In other words, represents the conditional variance of the factor. We represent the diagonal variance-covariance matrix as , where the entry on the diagonal is .

The methods described here can be applied to models with many different distributions over the idiosyncratic errors . In what follows, we will assume that , with a diagonal matrix. Within this framework, we will consider two broad cases. The first is when is is the same unknown parameter at all time periods; in the second case, the idiosyncratic variances can follow GARCH processes similarly to the variances of the latent factors:

| (4) | ||||

| (5) |

for . Conditional on information up to period , using either assumption regarding the behaviour of , the vector of latent factors is distributed as , and the observation vector . We show below that this conditionally Gaussian structure makes sequential Monte Carlo inference particularly efficient because a fully adapted particle filter can be applied.

The free parameters of the model are the elements of , the factor GARCH parameters for , and either the fixed values of or the GARCH pararameters for the idiosyncratic errors indexed by . We can carry out inference on these parameters, and generate forecasts of future observations, using the Gibbs sampler. The following sections briefly outline how an efficient Gibbs sampler can be applied to the model in (1).

Note that the estimation method described below can be generalised straightforwardly to any variant of the model which is conditionally linear and Gaussian (that is, conditional on the latent state at time ). For instance, we use a GARCH-in-mean (GARCH-M) model for the observation vector in the empirical application described in detail below. In general, the methods described here can be applied to many members of the GARCH family. It is also straightforward to include exogenous observed variables on the right-hand side of (1), though we omit this option throughout the paper for clarity.

2.1 The latent factors

Conditional on the parameters of the model, we can draw of the latent factors using a fully adapted variant of particle Gibbs (Andrieu et al., 2010). To improve the efficiency of the Gibbs draws, we implement ancestor sampling (Lindsten et al., 2012), as described below. In addition to conditioning on the parameters, the particle Gibbs algorithm also uses a draw of from a previous iteration. The sampler is initialised by setting this previous draw to an arbitrary value. We begin the particle Gibbs algorithm with copies of the factor variance in the first period, , initialised to its unconditional value,

Additionally, the first particle takes the value of from the previous draw that we condition on, and the remaining particles get a draw of . Conditional on the first observation , we resample the particles in proportion to their likelihood

We then choose a particle index using an ancestor sampling step, described below.

For the following periods , we carry out the following steps:

-

1.

Calculate the one-step prediction weights for ,

where

and the values of and are conditional on the value of the particle indexed by .

-

2.

Resample the particles with probability , but keep the particle indexed by unchanged.

-

3.

Draw a value of for each particle . This density can be calculated as , where

Keep the particle indexed by unchanged.

- 4.

-

5.

Carry out an ancestor sampling step by calculating the backward weights given by

(6) where we condition on the particular draw and associated for the first period, then on the given path thereafter. Following Lindsten et al. (2012), we truncate the product in (6) after a fixed number periods. (In the examples below, we truncate after five periods, since this provided satisfactory approximations to the exact values.) As a result, the computing time increases linearly with , rather than quadratically.

-

6.

Choose a particle index , and set .

2.2 The factor loadings

Conditional on a draw of , we can take a draw of the factor loadings . Broadly, there are two approaches that can both be used at this point. The first approach, widely used in Bayesian inference, involves imposing restrictions on the structure of to guarantee identification. A well-known aspect of factor models such as (1) is that we cannot directly identify a single set of values for the latent factor series , but only an equivalence class under the action of orthogonal rotations. In other words, if is any orthogonal matrix, then a vector of factors with loadings will have the same likelihood as another vector with loadings . In order to pin down particular values for the latent factors, we therefore need extra identifying assumptions. Two common choices in the Bayesian econometric literature are, first, to let be a triangular matrix and assume that has unit variance (Geweke and Zhou, 1996); or, second, to have an unrestricted variance for and assume that is triangular with ones on the diagonal (Aguilar and West, 2000). Using one of these assumptions, and given a draw of , the posterior distribution of is conditionally normal. Taking a conditional draw of effectively means carrying out a linear regression. Thus it is straightforward to apply one of these identification schemes in the Gibbs sampler, and we use one of them for our GARCH-M example below.

This type of identification scheme is simple, generally applicable, and widely used. Its main drawback is that the resulting inference can depend on the order in which the components of happen to be arranged (Chan et al., 2014). The reason for this is that the triangular identification schemes introduce a discontinuity into the mapping from the reduced-form values to the factor loadings . One can understand this intuitively by considering arrangements in which the observation is in fact uncorrelated with the factor. The triangular identification schemes effectively place a prior weight of zero on those cases. Thus their assessment of the model’s fit to the data can be severely hampered. Instead, it is possible to use a sampling method that is invariant to reorderings of the observation vector (Chan et al., 2014), which we summarise here. The disadvantage of this method is that at present it may not be as widely applicable; its assumptions are invalidated if the latent factors have a GARCH-M structure instead of GARCH, for instance. We must also assume in this case that the idiosyncratic errors have constant variance, . These restrictions may or may not be important, depending on the application in question. We use this method for our simulated examples in Section 3 where we assume constant error variances, as well as using it to provide a robustness check in the more general model of Section 4

Briefly, the invariant method for inference on first stacks the row vectors into a matrix . The matrix , which has rank , can be decomposed as

where and . Here is a Stiefel manifold. A Stiefel manifold is a space consisting of orthogonal -frames in the ambient space (James, 1954; Strachan and Inder, 2004). The prior for is chosen to be matrix-normal, so that each element of is independently normally distributed with mean zero and variance . The matrix functions as the coordinates of the row space of the reduced-rank matrix , seen as an element of , the Grassmannian being the space of all linear -dimensional subspaces embedded in (James, 1954; Strachan and Inder, 2004). The decomposition of into is not convenient enough to work with, because has a fixed orientation within the plane as the plane moves through . However, suppose we act on it with an orthogonal matrix (writing for the space of orthogonal matrices), so that

Then the matrix will have the same prior as , by the rotational invariance of the normal distribution; and if and have uniform priors on and , then their product will have a uniform prior on , given by , where and are the normalising constants for and (James, 1954).

Finally, the Chan et al. (2014) procedure introduces parameter expansion (Liu and Wu, 1999) to turn the prior distribution into a convenient conjugate form. Let , and let be its Cholesky decomposition, so that . Here, is a Wishart distribution with scale matrix and degrees of freedom. Rewrite the reduced-form matrix as

The Jacobian for this transformation is

. Based on the assumptions made so far, the prior is

with representing the normalising constant for the Wishart distribution. From this, it follows that

.

Therefore, conditional on , the prior on is Gaussian. Thus, the parameter expansion introduced by Chan et al. (2014) produces a conjugate prior for the regression of on , meaning that the conditional posterior is Gaussian. Note that, while the original analysis by Chan et al. (2014) uses homoscedastic latent factors, that assumption seems not to be required for this derivation to go through; in particular, it still applies when the rows of have time-varying volatility governed by a GARCH process. Writing for the row of the loading matrix, and for the vector of observations on the data series, we have

| (7) |

Although the Chan et al. (2014) method can be used to generate draws of , which then provide conditional draws of , it does not circumvent the original problem of separately identifying the rotation of . In other words, the draws of and generated by the Gibbs sampler are implicitly providing draws of the reduced-rank matrix . If an econometrician wishes to interpret the latent factors or the loadings separately, they must still impose some kind of identification scheme, such as the diagonal structures of Geweke and Zhou (1996) or Aguilar and West (2000). The advantage of the Chan et al. (2014) approach is that the estimates of , and the resulting judgements about the accuracy of the model, do not depend on the order of the components of . That would not be the case if we imposed the identification scheme during the estimation.

2.3 The idiosyncratic errors

If the idiosyncratic error variances are homoscedastic, then it is convenient to impose independent inverse Gamma prior distributions with mean and degrees of freedom . Consequently, their posterior distributions are inverse Gamma with degrees of freedom and mean .

If the idiosyncratic error variances are assumed to follow GARCH processes, then we can carry out inference on their parameters in the same manner as described in the next subsection.

2.4 The GARCH parameters

Having obtained draws of and , we can use a Metropolis-within-Gibbs step to obtain draws of the GARCH parameters. To increase the efficiency of the Metropolis Hastings moves, we first reparameterise the set of GARCH parameters for factor number by

| (8) |

and then by

| (9) |

Writing , we use these coordinates to propose new parameters via . The proposal covariance is initialised to a matrix with small positive numbers on the diagonal, and then updated using the adaptive Metropolis Hastings scheme of Haario et al. (2001). The new parameters are accepted with probability

The conditional likelihood is given by

where the variance follows

. Here the proposed GARCH parameters are calculated from by inverting (8) and (9).

When using the reordering-invariant specification for the factor loadings, the marginal variance of the latent factors becomes unidentified. In our implementation, we fix the marginal variance at 1, by assuming that . This restriction is straightforward to impose in the Metropolis Hastings steps.

2.5 The number of latent factors

Inference on the number of factors can be carried out using the Reversible Jump method (Green, 1995). The Reversible Jump implementation described by Lopes and West (2004) for the homoscedastic factor case is straightforward to extend to models in which the latent factors and idiosyncratic variances follow GARCH processes. In this section, we summarise and explain this extension of the Reversible Jump method. We note in passing that models with homoscedastic latent factors can use the Savage-Dickey Density Ratio (SDDR) (Verdinelli and Wasserman, 1995), as described by Chan et al. (2014). However, after applying that alternative method to simulated examples, we concluded that it is not feasible for GARCH factor models, since the changing volatilities of the latent factors make the estimation of the SDDR inefficient and slow to converge.

In implementing the Reversible Jump method in the style of Lopes and West (2004), we begin with separate preliminary estimation runs for all values of up to a chosen maximum . The draws of the factor loadings and the GARCH parameters from these preliminary runs are then used to generate proposal draws for the model-choice steps, as follows. Let and denote the posterior mean and covariance of the factor loadings estimated from the preliminary estimation run with latent factors. The proposal density for , conditional on using latent factors, is then , where is a scale factor chosen to ensure that the tails of the proposal density are fat enough. Similarly, let the estimated posterior mean of the GARCH parameters, transformed as in equation (9), be denoted , and the estimated posterior covariance be . The proposal density for the transformed GARCH parameters is then , with a fixed scale parameter. Note that using the transformed values , rather than the original parameters , ensures that the proposed GARCH parameters are always positive and within the stable region. The proposal density for the idiosyncratic error variance parameters, which we will write as , can either be an inverse gamma in the homoscedastic case, or a Gaussian on the GARCH parameters transformed as in equation (9).

Writing for the entire parameter vector used in a model with latent factors, the proposal density is

| (10) |

At the end of each Gibbs sampler iteration, we can then generate a between-model move as follows. We sample a proposed value uniformly from . We then use the fully-adapted particle filter to obtain a simulated value of the proposed likelihood and the current likelihood . This allows us to compute the Reversible Jump acceptance probability

| (11) |

Here is the prior density on the parameter vector , and is the prior mass on the number of latent factors. With probability , the proposed value is accepted, and we carry out the next Gibbs iteration using the proposed parameters . In that case, the current draw of the latent factors can be padded with zeros if , or truncated if .

3 Simulated examples

To evaluate the performance of the estimation method described above, we carried out a series of tests on simulated data. We simulated 200 periods of data using a model with two latent factors. For both factors’ GARCH parameters, we chose , , and (as discussed above) . Unless otherwise specified, we used observation components, particles, and idiosyncratic variances . We carried out five replications of each experiment. That is, we simulated five different data sets using each combination of settings, then estimated the model on each one. For each replication, we obtained 20,000 parameter draws. In our estimation, we constrained the draws of to be equal to as discussed above. The diagonal values of (which are in fact the same) were estimated independently.

We evaluated the efficiency of the estimation method by calculating the integrated autocorrelation times (IACTs) for particular groups of parameters. Given a vector of draws , the IACT is defined as

| (12) |

where is the autocorrelation between and . We calculated the IACTs using the overlapping batch means method of Flegal and Jones (2010). The times can be intuitively interpreted as inflation factors relative to independent draws from a parameter’s marginal posterior distribution. That is, a value of 20 would suggest that we require 20 draws from the algorithm to obtain the equivalent of one independent draw from the posterior.

3.1 Results

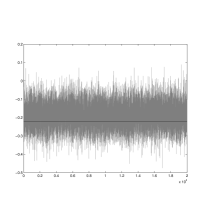

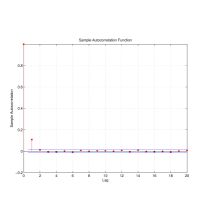

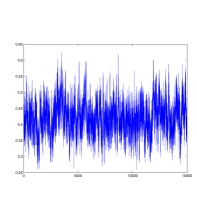

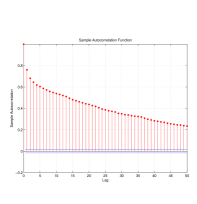

The sampler produced parameter draws with a low degree of autocorrelation. The left panel of Figure 1 shows a typical trace plot of the draws of —in this case, corresponding to the first observational component in the fifth time period. It appears that the sampler is exploring the posterior distribution quite rapidly. This impression is supported by the estimated autocorrelations of those draws, presented in the right-hand panel of the figure.

We carried out the Reversible Jump procedure to estimate the number of latent factors. It selected two latent factors (the correct number) with a high probability.

3.2 The number of particles

We tried varying the number of particles to ascertain its effect on the efficiency of the estimation. Table 1 reports the median integrated autocorrelation times for different groups of the model parameters over the five replications. Table 2 reports the maximum IACTs for each parameter group. The results suggest that the worst-case performance is fairly good, even for small numbers of particles.

| 5 | 1.73 | 6.4 | 37.8 | 55.0 |

|---|---|---|---|---|

| 10 | 1.30 | 3.2 | 26.4 | 19.4 |

| 20 | 1.17 | 2.9 | 29.1 | 17.4 |

| 40 | 1.08 | 2.2 | 23.6 | 15.3 |

| 5 | 97.11 | 74.9 | 69.9 | 94.7 |

|---|---|---|---|---|

| 10 | 79.70 | 52.2 | 63.4 | 95.9 |

| 20 | 76.35 | 36.1 | 68.3 | 93.1 |

| 40 | 4.26 | 8.0 | 42.5 | 30.8 |

The estimated median autocorrelation times are relatively low for all groups of parameters, but particularly for the reduced-form factor values and the idiosyncratic noise variances . The values for in Table 1 are consistent with the asymptotic theory developed by Pitt et al. (2012) for particle Metropolis Hastings: the IACTs decrease in proportion to . However, the levels of the IACTs are considerably lower than might be expected from a Metropolis Hastings estimation run.

| 5 | 8.66 | 32.1 | 189.0 | 274.8 |

|---|---|---|---|---|

| 10 | 13.03 | 32.1 | 263.6 | 193.7 |

| 20 | 23.45 | 58.8 | 582.1 | 348.3 |

| 40 | 43.21 | 86.7 | 944.6 | 613.7 |

Since the time required for running the particle Gibbs algorithm scales roughly in proportion to , we can use the product of and the IACT as a measure of computing time. These values, reported in Table 3, suggest that around 5 to 10 particles is optimal for this model.

3.3 The number of observations

We varied the number of observations from 5 up to 50. Table 4 summarises the results. The inference on the latent factors (our main object of inference) remains broadly similar, though the efficiency of inference about the idiosyncratic errors improves as the number of observations increases. The efficiency of the estimates of the GARCH parameters becomes somewhat poorer for medium-sized , partly reflecting the difficulty of separately identifying the and parameters. However, the efficiency then improves for as the increase in helps to reduce the noise in the estimated likelihood because of the GARCH structure.

| 5 | 1.29 | 4.8 | 44.0 | 13.6 |

|---|---|---|---|---|

| 10 | 1.30 | 3.2 | 26.4 | 19.4 |

| 25 | 1.29 | 2.1 | 65.6 | 69.8 |

| 50 | 1.32 | 2.4 | 60.8 | 61.1 |

| 100 | 1.53 | 5.2 | 25.0 | 18.2 |

3.4 The idiosyncratic noise variance

We also varied , the variance of the idiosyncratic noise vector . That is, the values on the diagonal of the matrix were set to the same value on each repetition, but we made that common value higher and lower, using the values listed in Table 5.

| 0.10 | 6.15 | 44.7 | 27.6 | 39.1 |

|---|---|---|---|---|

| 0.02 | 1.30 | 3.2 | 26.4 | 19.4 |

| 0.01 | 1.28 | 3.3 | 40.9 | 31.5 |

Unsurprisingly, the performance of the sampler degrades somewhat as increases, meaning that the observations become less informative about the latent factors.

4 Empirical application to US stock returns

We applied the estimation method described above to a sample of monthly US stock returns. Our data, kindly provided by Kenneth French, consisted of the monthly returns for 17 value-weighted industry portfolios. We used a sample running from January 1980 to December 2012, a total of 396 observations.

In this case, we used a GARCH-M model for the volatility of the latent factors. This is equivalent to positing a leverage effect—that is, an interaction between the factors’ volatilities and their conditional means. The model is summarised by

| (13) |

where now the latent factors have conditional means depending on their volatility

| (14) |

Inference on this model can be carried out through a straightforward generalisation of (1), since it maintains the conditionally linear and Gaussian structure of the basic factor GARCH model. The conditional variances and are assumed to have GARCH structures, as described in section 2.

This model invalidates the assumptions of the invariant factor loading estimation method, so we chose instead to identify the factor loadings by assuming that the loading matrix has ones on the main diagonal and zeros above the main diagonal. We imposed independent priors on the rest of the elements of . For the leverage parameters, we assumed independent priors given by , and each of the GARCH parameters , , , , and were given independent priors.

Given the difficulties identified by Chan et al. (2014), the ordering of the components of the observation vector should be chosen with some care. Inference becomes unstable if the observation component is not, in fact, correlated with the latent factor. In the case of the dataset used here, we have no prior information about industry groups that would make one ordering seem more reasonable than another. We therefore chose an ordering in two stages, starting by roughly ranking the series in order of the explanatory power, and then confirming that the resulting order was not obviously inconsistent with an invariant specification.

For the first stage, we carried out a linear regression of each of the 17 industry return series on every other series, selecting the series that provided the highest single as our first observation component. We chose the second and subsequent series by recursively adding them to the set of independent variables in the linear regressions, each time choosing the series that provided the highest single , and stopping after choosing the first eight components of the observation vector.

Having established this ordering, we checked it against the results of a factor GARCH model that we estimated with reordering-invariant loadings, as described above. (Note that this model assumes homoscedastic idiosyncratic errors and no GARCH-in-mean effect, so it is only an approximation of our final model specification; this check is indicative rather than conclusive.) Consider a single draw of the factor loadings from the invariant specification of the model. We can relate it to the specification with ones on the main diagonal by using a QR decomposition of to write

| (15) |

where is orthogonal, is lower triangular, is lower triangular with ones on the diagonal, and is diagonal and positive. So, if the corresponding draw of the latent factors is , then the estimate of produced by the specification with ones on the diagonal can be calculated as . This will be numerically unstable if the numbers on the diagonal of are too small. We therefore took 1000 draws using the invariant algorithm and the proposed ordering of variables, with the number of latent factors ranging from 1 to 8. The smallest element of was found to be , which occurred in the eight factor case. While far from ideal, this is well within floating-point precision. This suggests that our variable ordering is adequate.

We estimated this model on the monthly equity return data using the Reversible Jump method described above to choose the number of latent factors. In the preliminary estimation runs, we estimated models with between one and eight latent factors.

4.1 Results

The Reversible Jump method placed a high probability on the version of the model with seven latent factors. In Table 6, we report the estimated signal to noise ratios for each of the 17 observation components. The table reports the sample variance of each component (with the monthly returns measured in percentage points), and its estimated idiosyncratic variance. The latter was calculated as the mean of the unconditional noise variance , given by . The final column reports the signal to noise ratio, calculated as the difference between the sample variance and the idiosyncratic variance, divided by the idiosyncratic variance. Most components are estimated to have fairly high SNRs. This means that the fully adapted filter for the GARCH components will be very efficient in this case.

| Industry sector |

|

|

SNR | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Food | 18.5 | 1.2 | 14.6 | ||||||

| Mining and Minerals | 65.9 | 29.1 | 1.3 | ||||||

| Oil and Petroleum Products | 33.1 | 4.2 | 6.8 | ||||||

| Textiles, Apparel & Footwear | 39.1 | 15.0 | 1.6 | ||||||

| Consumer Durables | 33.0 | 7.7 | 3.3 | ||||||

| Chemicals | 34.9 | 7.2 | 3.8 | ||||||

| Drugs, Soap, Perfumes, Tobacco | 20.4 | 14.4 | 0.4 | ||||||

| Construction & Construction Materials | 37.8 | 11.5 | 2.3 | ||||||

| Steel Works Etc | 66.6 | 49.2 | 0.4 | ||||||

| Fabricated Products | 31.4 | 6.8 | 3.6 | ||||||

| Machinery & Business Equipment | 50.4 | 24.5 | 1.1 | ||||||

| Automobiles | 46.2 | 6.5 | 6.1 | ||||||

| Transportation | 30.6 | 7.3 | 3.2 | ||||||

| Utilities | 15.8 | 3.7 | 3.3 | ||||||

| Retail Stores | 28.0 | 7.9 | 2.5 | ||||||

| Banks & Insurance Companies | 31.3 | 2.6 | 10.8 | ||||||

| Other | 26.1 | 6.9 | 2.8 |

We find no evidence for leverage effects in this dataset, with the posterior credible intervals of each including zero in all model variants. This stands in contrast to the results on UK stock return data analysed in Fiorentini et al. (2004), which used a single latent factor with homoscedastic idiosyncratic errors. It may be that putative leverage effects can appear as artefacts of time-varying idiosyncratic volatility.

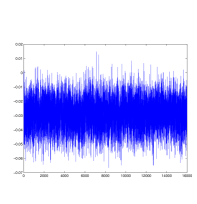

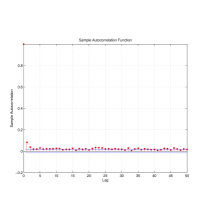

The Gibbs sampler produced these results efficiently. The draws of show a particularly rapid degree of mixing; Figure 2 shows an example trace plot. The low autocorrelation of the draws is echoed in their low IACT, estimated to be 1.7. The median IACT for all components of was 2.8, and the maximum was 26. The draws of are a little slower mixing than in the simulated examples considered above, with a typical example plotted in Figure 3. The draws of the factor loadings still mix relatively rapidly, with a median IACT of 16 and a maximum of 37.

5 Conclusion

Recent developments in sequential Monte Carlo methods have opened up new possibilities for Bayesian computation on latent factor models with time-varying volatility. As our article demonstrates, the particle Gibbs algorithm provides a flexible and efficient framework for carrying out inference on latent factor models with GARCH factors and GARCH errors. It can be applied to models using an invariant specification for the factor loadings (where possible), or to those using a more traditional triangular identification scheme. The conditionally linear-Gaussian structure of GARCH makes it particularly well suited to particle methods. The resulting parameter estimates mix well and explore the posterior distribution rapidly. It is possible to extend the methodology in a straightforward way to GARCH factor models with regime changes and structural breaks.

6 Acknowledgement

Jamie Hall was partially supported by ARC grants DP120104014 and LP0774950. Robert Kohn was partially supported by ARC grant DP120104014.

References

- Aguilar and West (2000) Aguilar, O. and West, M. (2000), “Bayesian Dynamic Factor Models and Portfolio Allocation,” Journal of Business & Economic Statistics, 18, 338–357.

- Andrieu et al. (2010) Andrieu, C., Doucet, A., and Holenstein, R. (2010), “Particle Markov chain Monte Carlo methods,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 72, 269–342.

- Bauwens et al. (2006) Bauwens, L., Laurent, S., and Rombouts, J. V. K. (2006), “Multivariate GARCH models: a survey,” Journal of Applied Econometrics, 21, 79–109.

- Chan et al. (2014) Chan, J., Leon-Gonzalez, R., and Strachan, R. W. (2014), “Efficient computation and invariant inference in the static factor model,” Mimeo, Australian National University, http://people.anu.edu.au/joshua.chan/cls.pdf.

- Fiorentini et al. (2004) Fiorentini, G., Sentana, E., and Shephard, N. (2004), “Likelihood-Based Estimation of Latent Generalized ARCH Structures,” Econometrica, 72, 1481–1517.

- Flegal and Jones (2010) Flegal, J. M. and Jones, G. L. (2010), “Batch means and spectral variance estimators in Markov chain Monte Carlo,” The Annals of Statistics, 38, 1034–1070.

- Geweke and Zhou (1996) Geweke, J. and Zhou, G. (1996), “Measuring the pricing error of the arbitrage pricing theory,” Review of Financial Studies, 9, 557–587.

- Green (1995) Green, P. J. (1995), “Reversible jump Markov chain Monte Carlo computation and Bayesian model determination,” Biometrika, 82, 711–732.

- Haario et al. (2001) Haario, H., Saksman, E., and Tamminen, J. (2001), “An Adaptive Metropolis Algorithm,” Bernoulli, 7, 223–242.

- James (1954) James, A. T. (1954), “Normal Multivariate Analysis and the Orthogonal Group,” The Annals of Mathematical Statistics, 25, 40–75.

- Lindsten et al. (2012) Lindsten, F., Jordan, M. I., and Schön, T. B. (2012), “Ancestor Sampling for Particle Gibbs,” arXiv:1210.6911.

- Liu and Wu (1999) Liu, J. S. and Wu, Y. N. (1999), “Parameter Expansion for Data Augmentation,” Journal of the American Statistical Association, 94, 1264–1274.

- Lopes and West (2004) Lopes, H. F. and West, M. (2004), “Bayesian Model Assessment in Factor Analysis,” Statistica Sinica, 14, 41—67.

- Pitt and Shephard (1999) Pitt, M. K. and Shephard, N. (1999), “Filtering via Simulation: Auxiliary Particle Filters,” Journal of the American Statistical Association, 94, 590–599.

- Pitt et al. (2012) Pitt, M. K., Silva, R. d. S., Giordani, P., and Kohn, R. (2012), “On some properties of Markov chain Monte Carlo simulation methods based on the particle filter,” Journal of Econometrics, 171, 134–151.

- Stock and Watson (2002) Stock, J. H. and Watson, M. W. (2002), “Forecasting Using Principal Components from a Large Number of Predictors,” Journal of the American Statistical Association, 97, 1167–1179.

- Strachan and Inder (2004) Strachan, R. W. and Inder, B. (2004), “Bayesian analysis of the error correction model,” Journal of Econometrics, 123, 307–325.

- Verdinelli and Wasserman (1995) Verdinelli, I. and Wasserman, L. (1995), “Computing Bayes Factors Using a Generalization of the Savage-Dickey Density Ratio,” Journal of the American Statistical Association, 90, 614–618.