Bootstrapped Thompson Sampling and Deep Exploration

Abstract

This technical note presents a new approach to carrying out the kind of exploration achieved by Thompson sampling, but without explicitly maintaining or sampling from posterior distributions. The approach is based on a bootstrap technique that uses a combination of observed and artificially generated data. The latter serves to induce a prior distribution which, as we will demonstrate, is critical to effective exploration. We explain how the approach can be applied to multi-armed bandit and reinforcement learning problems and how it relates to Thompson sampling. The approach is particularly well-suited for contexts in which exploration is coupled with deep learning, since in these settings, maintaining or generating samples from a posterior distribution becomes computationally infeasible.

1 Introduction

To perform well in a sequential decision task while learning about its environment, an agent must balance between exploitation, making good decisions given available data, and exploration, taking actions that may help to improve the quality of future decisions. Perhaps the most principled approach is to compute a Bayes optimal solution, which optimizes the long-run expected rewards given prior beliefs. Although conceptually simple, this approach is computationally intractable for all but the simplest of problems. As such, engineers typically turn to tractable heuristic exploration strategies.

Upper-confidence bound approaches offer one popular class of exploration heuristics that come with performance guarantees. Such approaches assign to poorly-understood actions high but statistically plausible values, effectively allocating an optimism bonus to incentivize exploration of each such action. For a broad class of problems, if optimism bonuses are well-designed, upper-confidence bound algorithms enjoy optimal learning rates. However, designing, tuning, and applying such algorithms can be challenging or intractable, and as such, upper-confidence bound algorithms applied in practice often suffer poor empirical performance.

Another popular heuristic, which on the surface appears unrelated, is called Thompson sampling or probability matching. In this algorithm the agent maintains a posterior distribution of beliefs and, ain each time period, samples an action randomly according to the probability that it is optimal. Although this algorithm is one of the oldest recorded exploration heuristics, it received relatively little attention until recently when its strong empirical performance was noted, and a host of analytic guarantees followed. It turns out that there is a deep connection between Thompson sampling and optimistic algorithms; in particular, as shown in [1], Thompson sampling can be viewed as a randomized approximation that approaches the performance of a well-designed and well-tuned upper confidence bound algorithm.

Almost all of the literature on Thompson sampling takes the ability to sample from a posterior distribution as given. For many commonly used distributions, this is served through conjugate updates or Markov chain Monte Carlo methods. However, such methods do not adequately accommodate contexts in which models are nonlinearly parameterized in potentially complex ways, as is the case in deep learning. In this paper we introduce an alternative approach to tractably attaining the behavior of Thompson sampling in a manner that accommodates such nonlinearly parameterized models and, in fact, may offer advantages more broadly when it comes to efficiently implementing and applying Thompson sampling.

The approach we propose is based on a bootstrap technique that uses a combination of observed and artificially generated data. The idea of using the bootstrap to approximate a posterior distribution is not new, and has been noted from inception of the bootstrap concept. Further, the application of the bootstrap [2] and other related sub-sampling approaches [3] to approximate Thompson sampling is not new. However, we show that these existing approaches fail to ensure sufficient exploration for effective performance in sequential decision problems. As we will demonstrate, the way in which we generate and use artificial data is critical. The approach is particularly well-suited for contexts in which exploration is coupled with deep learning, since in such settings, maintaining or generating samples from a posterior distribution becomes computationally infeasible. Further, our approach is parallelizable and as such scales well to massive complex problems. We explain how the approach can be applied to multi-armed bandit and reinforcement learning problems and how it relates to Thompson sampling.

2 Priors, posteriors, and the bootstrap

The term bootstrap refers to a class of methods for nonparametric estimation from data-driven simulation [4]. In essence, the bootstrap uses the empirical distribution of a sampled dataset as an estimate of the population statistic. Algorithm 1 provides pseudocode for what is perhaps the most common form of bootstrap [4]. We use to denote the set of probability measures over a set .

Bootstrap

Input: Data , function ,

Output: Probability measure

This procedure allows estimates the distribution of any unknown parameter in a non-parametric manner. As described with a function of probability measures as input, the algorithm is somewhat abstract. However, it easily specializes to familiar concrete versions. For example, suppose is the expectation operator. Then, each sample is the mean of a sample of the data set, and is the relative frequency measure of these sample means.

The output is reminiscent of a Bayesian posterior with an extremely weak prior. In fact, with a small modification, Algorithm 1 becomes Algorithm 2, the so-called Bayesian bootstrap, for which the distribution produced can be interpreted as a posterior based on the data and a degenerate Dirichlet prior [5].

BayesBootstrap

Input: Data , function ,

Output: Probability measure

With the bootstrap approaches we have described, the support of distributions is restricted to the dataset . We will show that in sequential decision problems this poses a significant problem. To address the problem, we propose a simple extension to the bootstrap. In particular, we augment the dataset with artificially generated samples and apply the bootstrap to the combined dataset. The artificially generated data can be viewed as inducing a prior distribution. In fact, if is finite and , then as grows, the distribution produced by the Bayesian bootstrap converges to the posterior distribution conditioned on , given a uniform Dirichlet prior.

When the set is large or infinite, the idea of generating one artificial sample per element does not scale gracefully. If we require one prior observation for every single possible value then the observed data will bear little influence on the distribution relative to the artificial data . To address this, for a selected value of , we sample the artificial data points from a “prior” distribution . The important thing here is that the relative strength of the induced prior can be controlled in an explicit manner. Similarly, depending on the choice of the prior sampling distribution the posterior is no longer restricted to finite support. In many ways this extension corresponds to using a Dirichlet process prior with generator .

This augmented bootstrap procedure is especially promising for nonlinear functions such as deep neural networks, where sampling from a posterior is typically intractable. In fact, given any method of training a neural network on a dataset of size , we can generate an approximate posterior through bootstrapped versions of the neural network. In its most naive implementation this increases the computational cost by a factor of . However, this approach is parallelizable and therefore scalable with compute power. In addition, it may be possible to significantly reduce the computational cost of this bootstrap procedure by sharing some of the lower-level features between bootstrap sampled networks or growing them out in a tree structure. This could even be implemented on a single chip through a specially constructed dropout mask for each bootstrap sample. With a deep neural network this could provide significant savings.

3 Multi-armed bandit

Consider a problem in which an agent sequentially chooses actions from an action set and observes corresponding outcomes . There is a random outcome associated with each and time . For each random outcome the agent receives a reward where is a known function. The “true outcome distribution” is itself drawn from a family of distributions . We assume that, conditioned on , is an iid sequence with each element distributed according to . Let be the marginal distribution corresponding to . The -period regret of the sequence of actions is the random variable

The Bayesian regret to time is defined by , where the expectation is taken with respect to the prior distribution over .

We take all random variables to be defined with respect to a probability space . We will denote by the history of observations realized prior to time . Each action is selected based only on and possibly some external source of randomness. To represent this external source, we introduce a sequence of iid random variables . Each action is measurable with respect to the sigma-algebra generated by .

The objective is to choose actions in a manner that minimizes Bayesian regret. For this purpose, it is useful to think of actions as being selected by a randomized policy , where each is a distribution over actions and is measurable with respect to the sigma-algebra generated by . An action is chosen at time by randomizing according to . Our bootstrapped Thompson sampling algorithm, presented as Algorithm 3, serves as such a policy. The algorithm uses a bootstrap algorithm, like Algorithms 1 or 2 as a subroutine. Note that the sequence of action-observation pairs is not iid, though bootstrap algorithms effectively treat data passed to them as iid. The function passed to the bootstrap algorithm maps a specified history of action-observation pairs to a probability distribution over reward vectors. The resulting probability distribution can be thought of as a model fit to the data provided in the history. Note that the algorithm takes as input a distribution from which artificial samples are drawn. This can be thought of as a subroutine that generates action-observation pairs. As a special case, this subroutine could generate deterministic pairs. There can be advantages, though, to using a stochastic sampling routine, especially when the space of action-observation pairs is large and we do not want to impose too strong a prior.

BootstrapThompson

Input: Bootstrap algorithm , artificial history length and sampling distribution

This algorithm is similar to Thompson sampling, though the posterior sampling step has been replaced by a single bootstrap sample. As we will establish in Section 3.2, for several multi-armed bandit problems BootstrapThompson with appropriate artificial data is equivalent to Thompson sampling.

One drawback of Algorithm 3 is that the computational cost per timestep grows with the amount of data . For applications at large scale this will be prohibitive. Fortunately there is an effective method to approximate these bootstrap samples in an online manner at constant computational cost [2]. Instead of generating a new bootstrap sample every step we can approximate the bootstrap bootstrap distribution by training online bootstrap models in parallel and then sampling between them uniformly. In its most naive implementation this parrallel bootstrap will have a computational cost per timestep times larger than a greedy algorithm. However, for specific function classes such as neural networks it may be possible to share some computation between models and provide significant savings.

3.1 Simulation results

We now examine a simple problem instance designed to demonstrate the need for an artificial history to incentivize efficient exploration in BootstrapThompson. The action space , outcomes and rewards . We fix and describe the true underlying distribution in terms of the Dirac delta function which assigns all probability mass to :

The optimal policy is to pick at every timestep, since this has an expected reward of instead of just . However, with probability at least , BootstrapThompson without artificial history () will never learn the optimal policy.

To see why this is the case note that BootstrapThompson without artificial history must begin by sampling each arm once. In our system this means that with probability the agent will receive a reward of from arm one and from arm two. Given this history, the algorithm will prefer to choose arm one for all subsequent timesteps, since its bootstrap estimates will always put all their mass on and respectively. However, we show that this failing can easily be remedied by the inclusion of some artificial history.

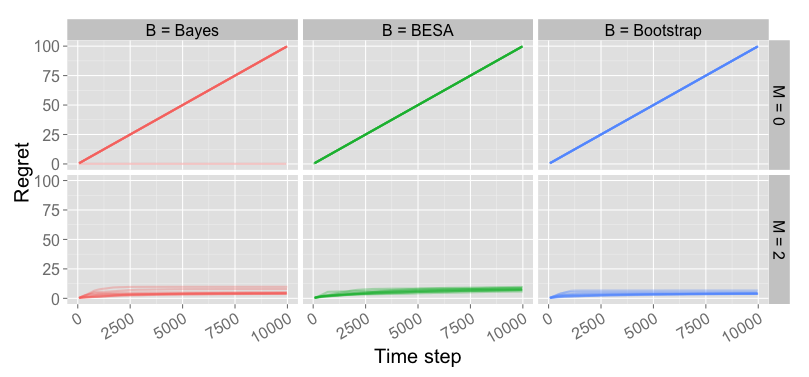

In Figure 1 we plot the cumulative regret of three variants of BootstrapThompson using different bootstrap algorithms with or . For our simulations we set and ran Monte Carlo simulations for each variant of the algorithm. In each simulation and each time period, the pair of artificial data points for cases with was sampled from a distribution that selects each of the two actions once and samples an observation uniformly from for each. We found that, in this example, the choice of bootstrap method makes little difference but that injecting artificial data is crucial to incentivizing efficient exploration.

The six subplots in Figure 1 present results differentiated by choice of bootstrap algorithms and whether or not to include artificial data. The columns indicate which bootstrap algorithm is used with labels “Bootstrap” for Algorithm 1, “Bayes” for Algorithm 2, and “BESA” for a recently proposed bootstrap approach. The rows indicate whether or not artificial prior data was used. We see that BootstrapThompson generally fails to learn with , however the inclusion of artificial data helps to drive efficient exploration. The choice of bootstrap algorithm seems to make relatively little difference, however we do find that Algorithms 1 and 2 seem to outperform BESA on this example111The BESA algorithm is a variant of the bootstrap that applies to two armed bandit problems. In each time period, the algorithm estimates the reward of each arm by drawing a sample average (with replacement) with sample size equal to the number of times the other arm has been played. This apparently performs well in some settings [3], but the approach does not generalize gracefully to settings with dependent arms..

3.2 Analysis

The BootstrapThompson algorithm is similar to Thompson sampling, the only difference being that a draw from the posterior distribution is replaced by a bootstrap sample. In fact, we can show that, for particular choices of bootstrap algorithm and artificial data distribution, the two algorithms are equivalent.

Consider as an example a multi-armed bandit problem with independent arms, for which each th arm generates rewards from a Bernoulli distribution with mean . Suppose that our prior distribution over is . Then, the posterior conditioned on observing outcomes with reward zero and outcomes with reward one is . If and are positive integers, a sample from this distribution can be generated by the following procedure: sample and let . This sampling procedure is identical to BayesBootstrap (Algorithm 2) with artificial data generated by a distribution that assigns all probability to a single outcome that, for each arm , produces data samples, with of them associated with reward one and of them associated with reward .

The example we have presented can easily be generalized to the case where each arm generates rewards from among a finite set of possibilities with probabilities distributed according to a Dirichlet prior. We expect that, with appropriately designed schemes for generating artificial data, such equivalences can also be established for a far broader range of problems.

4 Reinforcement learning

In reinforcement learning, actions taken by the agent can impose delayed consequences. This makes the design of exploration strategies more challenging than for multi-armed bandit problems. To fix a context, consider an agent that interacts with an environment over repeated episodes of length . In each time period of each episode episode , the agent observes a state and selects an action according to a policy which maps states to actions. A reward of and state transition to are then realized. The agent’s goal is to maximize the long term sum of expected rewards, even though she is initially unsure of the system dynamics and reward structure.

A common approach to reinforcement learning involves learning a state-action value function , which for each time , state , and action , provides an estimate of expected rewards over the remainder of the episode: . Given a state-action value function , it is natural for the agent to select an action that maximizes when at state at time .

There is a large literature on reinforcement learning algorithms which balance exploration with exploitation in a variety of ways [7, 8, 9]. However, the vast majority of these algorithms operate in the “tabula rasa” setting, which does not allow for generalization between state-action pairs. For most practical systems where the numbers of states and actions is very large or even infinite the ability to generalize is crucial for good performance. Of those algorithms which do combine generalization with exploration, many require an intractable model-based planning step, or are restricted to unrealistic parametric domains [10, 11, 12].

By contrast, some of the most successful applications of reinforcement learning generalize using nonlinearly parameterized models, like deep neural networks, that approximate the state-action value function [13, 14]. These algorithms have attained superhuman performance and generated excitement for a new wave of artificial intelligence, but still fail at simple tasks that require efficient exploration since they use simple exploration schemes that do not adequately account for the possibility of delayed consequences. Recent research has shown how to combine efficient generalization and exploration via randomized linearly parameterized value functions [15]. The approach presented in [15] can be viewed as a variant of Thompson sampling applied in a reinforcement learning context. But this approach [15] does not serve the needs of nonlinear parameterizations. What we present now, as Algorithm 4, is a version of Thompson sampling that does serve such needs via leveraging the bootstrap and artificial data.

Reinforcement Learning with Bootstrapped Value Function Randomization

In the context of our episodic setting, each element of the data set corresponds to a sequence of observations made over an episode. The algorithm takes as input a function , which should itself be viewed as an algorithm that estimates the state-action value function from this data set. For example, could output a deep neural network trained to fit a state-action value function via least-squares value iteration. A number of conventional reinforcement learning algorithms would fit the state-action value function to the observed history . Two key features that distinguishes Algorithm 4 is that the state-action value function is fit to a random subsample of data and that this subsample is drawn from a combination of historical and artificial data.

Before the beginning of each episode, the algorithm applies to generate a randomized state-action value function. The agent then follows the greedy policy with respect to that sample over the entire episode. As is more broadly the case with Thompson sampling, the algorithm balances exploration with exploitation through the randomness of these samples. The algorithm enjoys the benefits of what we call deep exploration in that it sometimes selects actions which are neither exploitative nor informative in themselves, but that are oriented toward positioning the agent to gain useful information downstream in the episode. In fact, the general approach represented by this algorithm may be the only known computationally efficient means of achieving deep exploration with nonlinearly parameterized representations such as deep neural networks.

As discussed earlier, the inclusion of an artificial history can be crucial to incentivize proper exploration in multi-armed bandit problems. The same is true for reinforcement learning. One simple approach to generating artificial data that accomplishes this in the context of Algorithm 4 is to sample state-action pairs from a diffusely mixed generative model and assign them stochastically optimistic rewards (see [15] for a definition) and random state transitions. When prior data is available from episodes of experience with actions selected by an expert agent, one can also augment this artificial data with that history of experience. This offers a means of incorporating apprenticeship learning as a springboard for the learning process.

Fitting a model like a deep neural network can itself be a computationally expensive task. As such it is desirable to use incremental methods that incorporate new data samples into the fitting process as they appear, without having to refit the model from scratch. It is important to observe that a slight variation of Algorithm 4 accommodates this sort of incremental fitting by leveraging parallel computation. This variation is presented as Algorithms 5 and 6. The algorithm makes use of an incremental model learning method , which takes as input a current model, previous data set, and new data point, with a weight assigned to each data point. Algorithm 6 maintains models (for example, deep neural networks), incrementally updating each in parallel after observing each episode. The model used to guide action in an episode is sampled uniformly from the set of . It is worth noting that this is akin to training each model using experience replay, but with past experiences weighted randomly to induce exploration.

IncrementalBayesBootstrapSample

Input: Data , weights ,

function

Output: Sampled weight , sampled outcome

Incremental Reinforcement Learning with Bootstrapped Value Function Randomization

References

- [1] Daniel Russo and Benjamin Van Roy. Learning to optimize via posterior sampling. Mathematics of Operations Research, 39(4):1221–1243, 2014.

- [2] Dean Eckles and Maurits Kaptein. Thompson sampling with the online bootstrap. CoRR, abs/1410.4009, 2014.

- [3] Akram Baransi, Odalric-Ambrym Maillard, and Shie Mannor. Sub-sampling for multi-armed bandits. In Machine Learning and Knowledge Discovery in Databases, pages 115–131. Springer, 2014.

- [4] Bradley Efron. Bootstrap methods: another look at the jackknife. The annals of Statistics, pages 1–26, 1979.

- [5] Donald B Rubin et al. The bayesian bootstrap. The annals of statistics, 9(1):130–134, 1981.

- [6] S. Agrawal and N. Goyal. Further optimal regret bounds for Thompson sampling. In Proceedings of the Sixteenth International Conference on Artificial Intelligence and Statistics, 2013.

- [7] Ronen Brafman and Moshe Tennenholtz. R-max-a general polynomial time algorithm for near-optimal reinforcement learning. The Journal of Machine Learning Research, 3:213–231, 2003.

- [8] Thomas Jaksch, Ronald Ortner, and Peter Auer. Near-optimal regret bounds for reinforcement learning. The Journal of Machine Learning Research, 99:1563–1600, 2010.

- [9] Ian Osband, Daniel Russo, and Benjamin Van Roy. (More) Efficient Reinforcement Learning via Posterior Sampling. Advances in Neural Information Processing Systems, 2013.

- [10] Ian Osband and Benjamin Van Roy. Near-optimal regret bounds for reinforcement learning in factored MDPs. arXiv preprint arXiv:1403.3741, 2014.

- [11] Ian Osband and Benjamin Van Roy. Model-based reinforcement learning and the eluder dimension. In Advances in Neural Information Processing Systems, pages 1466–1474, 2014.

- [12] Yasin Abbasi-Yadkori and Csaba Szepesvári. Regret bounds for the adaptive control of linear quadratic systems. Journal of Machine Learning Research-Proceedings Track, 19:1–26, 2011.

- [13] Gerald Tesauro. Temporal difference learning and td-gammon. Communications of the ACM, 38(3):58–68, 1995.

- [14] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A Rusu, Joel Veness, Marc G Bellemare, Alex Graves, Martin Riedmiller, Andreas K Fidjeland, Georg Ostrovski, et al. Human-level control through deep reinforcement learning. Nature, 518(7540):529–533, 2015.

- [15] Benjamin Van Roy and Zheng Wen. Generalization and exploration via randomized value functions. arXiv preprint arXiv:1402.0635, 2014.