Expected Shortfall is jointly elicitable with Value at Risk – Implications for backtesting

Abstract

In this note, we comment on the relevance of elicitability for backtesting risk measure estimates. In particular, we propose the use of Diebold-Mariano tests, and show how they can be implemented for Expected Shortfall (ES), based on the recent result of Fissler and Ziegel (2015) that ES is jointly elicitable with Value at Risk.

There continues to be lively debate about the appropriate choice of a quantitative risk measure for regulatory purposes or internal risk management. In this context, it has been shown by Weber (2006) and Gneiting (2011) that Expected Shortfall (ES) is not elicitable. Specifically, there is no strictly consistent scoring (or loss) function such that, for any random variable with finite mean, we have

Recall that ES of at level is defined as

where Value at Risk (VaR) is given by . In contrast, VaR at level is elicitable for random variables with a unique -quantile. The possible strictly consistent scoring functions for VaR are of the form

| (1) |

where is a strictly increasing function.

However, it turns out that ES is elicitable of higher order in the sense that the pair (VaRα, ESα) is jointly elicitable. Indeed, we have that

where possible choices of are given by

| (2) | ||||

with and being strictly increasing continuously differentiable functions such that the expectation exists, and ; see Fissler and Ziegel (2015, Corollary 5.5). One can nicely see the structure of : The first summand in (2) is exactly a strictly consistent scoring function for VaRα given at (1) and hence only depends on , whereas the second summand cannot be split into a part depending only on and one depending only on , respectively, hence illustrating the fact that ESα itself is not elicitable. A possible choice for and is and . Acerbi and Székely (2014) proposed a scoring function for the pair (VaRα, ESα) under the additional assumption that there exists a real number such that for all assets under consideration. Despite encouraging simulation results, there is currently no formal proof available of the strict consistency of their proposal. In contrast, the scoring functions given at (2) do not require additional assumptions, and it has been formally proven that they provide a class of strictly consistent scoring functions.

The lack of elicitability of ES (of first order) has led to a lively discussion about whether or not and how it is possible to backtest ES forecasts; see, for example, Acerbi and Székely (2014), Carver (2014), and Emmer et al. (2015). It is generally accepted that elicitability is useful for model selection, estimation, generalized regression, forecast comparison, and forecast ranking. Having provided strictly consistent scoring functions for (VaRα, ESα), we take the opportunity to comment on the role of elicitability in backtesting.

The traditional approach to backtesting aims at model verification. To this end, one tests the null hypothesis:

Specifically, suppose we have sequences and , where is the realized value of the asset at time point , and and denote the estimated VaRα and ESα given at time for time point , respectively. A backtest uses some test statistic , which is a function of , such that we know the distribution of (at least approximately) if the null hypothesis of correct risk measure estimates holds. If we reject at some small level, the model or the estimation procedure for the risk measure is deemed inadequate. For this approach of model verification, elicitability of the risk measure is not relevant, as pointed out by Acerbi and Székely (2014) and Davis (2014). However, tests of this type can be problematic in regulatory practice, notably in view of the anticipated revised standardised approach (Bank for International Settlements, 2013, pp. 5–6), which “should provide a credible fall-back in the event that a bank’s internal market risk model is deemed inadequate”. If the internal model fails the backtest, the standardised approach may fail the test, too, and in fact it might be inferior to the internal model. Generally, tests of the hypothesis are not aimed at, and do not allow for, model comparison and model ranking.

Alternatively, one could use the following null hypothesis in backtesting:

Here, the standard procedure could be a method specified by the regulator, or it could be a technique that has proven to yield good results in the past. Specifically, let us write for the sequence of VaRα and ESα estimates by the standard procedure. Making use of the elicitability of (VaRα, ESα), we take one of the scoring functions given at (2) to define the test statistic

| (3) |

where

and is a suitable estimate of the respective standard deviation. Under , the test statistic has expected value less than or equal to zero. Following the lead of Diebold and Mariano (1995), comparative tests that are based on the asymptotic normality of the test statistics have been employed in a wealth of applications.

Under both and , the backtest is passed if the null hypothesis fails to be rejected. However, as Fisher (1949, p. 16) noted, “the null hypothesis is never proved or established, but it is possibly disproved, in the course of experimentation.” In other words, a passed backtest does not imply the validity of the respective null hypothesis. Passing the backtest simply means that the hypothesis of correctness () or superiority (), respectively, could not be falsified.

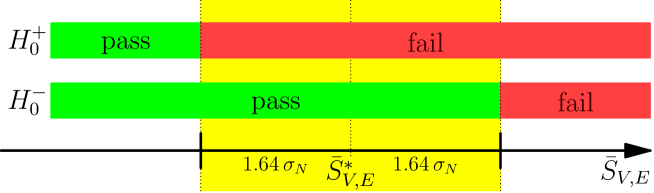

In the case of comparative backtests, a more conservative approach could be based on the following null hypothesis:

This can also be tested using the statistic in (3), which has expected value greater than or equal to zero under . The backtest now is passed when is rejected. The decisions taken in comparative backtesting under and are illustrated in Figure 1, where the colors relate to the three-zone approach of the Bank for International Settlements (2013, pp. 103–108). In regulatory practice, the distinction between Diebold-Mariano tests under the two hypotheses amounts to a reversed onus of proof. In the traditional setting, it is the regulator’s burden to show that the internal model is incorrect. In contrast, if a backtest is passed when is rejected, banks are obliged to demonstrate the superiority of the internal model. Such an approach to backtesting may entice banks to improve their internal models, and is akin to regulatory practice in the health sector, where market authorisation for medicinal products hinges on comparative clinical trials. In the health context, decision-making under corresponds to equivalence or non-inferiority trials, which are “not conservative in nature, so that many flaws in the design or conduct of the trial will tend to bias the results”, whereas “efficacy is most convincingly established by demonstrating superiority” under (European Medicines Agency, 1998, p. 17). Technical detail is available in a specialized strand of the biomedical literature; for a concise review, see Lesaffre (2008).

We now give an illustration in the simulation setting of Gneiting et al. (2007). Specifically, let be a sequence of independent standard normal random variables. Conditional on , the return is normally distributed with mean and variance 1, denoted . Under our Scenario A, the standard method for estimating risk measures uses the unconditional distribution of , whereas the internal procedure takes advantage of the information contained in and uses the conditional distribution . Therefore,

and

where and denote the density and the cumulative distribution function of the standard normal distribution, respectively. Under Scenario B, the roles of the standard method and the internal procedure are interchanged.

We use sample size and repeat the experiment 10,000 times. As tests of traditional type, we consider the coverage test for described by the Bank for International Settlements (2013, pp. 103–108) and the generalized coverage test for proposed by Costanzino and Curran (2015). As shown by Clift et al. (2015), the latter performs similarly to the approaches of Wong (2008) and Acerbi and Székely (2014), but is easier to implement. The outcome of the test is structured into green, yellow, and red zones, as described in the aforementioned references. For the comparative backtest for , we use the functions and in (2) and define the zones as implied by Figure 1. Finally, our comparative backtest for uses the function in (1), which is equivalent to putting and in (2). For in the test statistic in (3) we use the standard estimator.

| Scenario A | Green | Yellow | Red | |

|---|---|---|---|---|

| Traditional | 89.35 | 10.65 | 0.00 | |

| Traditional | 93.62 | 6.36 | 0.02 | |

| Comparative | 88.23 | 11.77 | 0.00 | |

| Comparative | 87.22 | 12.78 | 0.00 | |

| Scenario B | Green | Yellow | Red | |

| Traditional | 89.33 | 10.67 | 0.00 | |

| Traditional | 93.80 | 6.18 | 0.02 | |

| Comparative | 0.00 | 11.77 | 88.23 | |

| Comparative | 0.00 | 12.78 | 87.22 |

Table 1 summarizes the simulation results under Scenario A and B, respectively. The traditional backtests are performed for the internal model in the scenario at hand. Under Scenario A, the four tests give broadly equivalent results. The benefits of the comparative approach become apparent under Scenario B, where the traditional approach yields highly undesirable decisions in accepting a simplistic internal model, while a more informative standard model would be available. This can neither be in banks’ nor in regulators’ interests. We emphasize that this problem will arise with any traditional backtest, as a traditional backtest assesses optimality only with respect to the information used for providing the risk measure estimates.

Comparative tests based on test statistics of the form in (3) can be used to compare forecasts in the form of full predictive distributions, provided a proper scoring rule is used (Gneiting and Raftery, 2007), or to compare risk assessments, provided the risk measure admits a strictly consistent scoring function, so elicitability is crucial. In particular, proper scoring rules and consistent scoring functions are sensitive to increasing information utilized for prediction; see Holzmann and Eulert (2014). However, as consistent scoring functions are not unique, a question of prime practical interest is which functions ought to be used in regulatory settings or internally.

Arguably, now may be the time to revisit and investigate fundamental statistical issues in banking supervision. Chances are that comparative backtests, where a bank’s internal risk model is held accountable relative to an agreed-upon standardised approach, turn out to be beneficial to all stakeholders, including banks, regulators, and society at large.

Acknowledgements

We thank Paul Embrechts, Fernando Fasciati, Fabian Krüger, Alexander McNeil, Alexander Schied, Patrick Schmidt, and the organisor, Imre Kondor, and participants of the “International Workshop on Systemic Risk and Regulatory Market Risk Measures” in Pullach for inspiring discussions and helpful comments. Tobias Fissler acknowledges funding by the Swiss National Science Foundation (SNF) via grant 152609, and Tilmann Gneiting by the European Union Seventh Framework Programme under grant agreement no. 290976.

References

- Acerbi and Székely (2014) C. Acerbi and B. Székely. Back-testing expected shortfall. Risk, December, 2014.

- Bank for International Settlements (2013) Bank for International Settlements. Consultative Document: Fundamental review of the trading book: A revised market risk framework. 2013.

- Carver (2014) L. Carver. Back-testing expected shortfall: mission possible? Risk, November, 2014.

- Clift et al. (2015) S. S. Clift, N. Costanzino, and M. Curran. Empirical performance of backtesting methods for expected shortfall. 2015. URL ssrn.com/abstract=2618345.

- Costanzino and Curran (2015) N. Costanzino and M. Curran. Backtesting general spectral risk measures with application to expected shortfall. Risk, March, 2015.

- Davis (2014) M. Davis. Consistency of internal risk measure estimates. 2014. URL arXiv:1410.4382.

- Diebold and Mariano (1995) F. X. Diebold and R. S. Mariano. Comparing predictive accuracy. Journal of Business and Economic Statistics, 13:253–263, 1995.

- Emmer et al. (2015) S. Emmer, M. Kratz, and D. Tasche. What is the best risk measure in practice? A comparison of standard measures. 2015. URL arXiv:1312.1645v4.

- European Medicines Agency (1998) European Medicines Agency. ICH Topic E 9: Statistical Principles for Clinical Trials. Note for Guidance on Statistical Principles for Clinical Trials, 1998. URL www.ema.europa.eu.

- Fisher (1949) R. A. Fisher. The Design of Experiments. Oliver and Boyd, London, 5th edition, 1949.

- Fissler and Ziegel (2015) T. Fissler and J. F. Ziegel. Higher order elicitability and Osband’s principle. 2015. URL arXiv:1503.08123.

- Gneiting (2011) T. Gneiting. Making and evaluating point forecasts. Journal of the American Statistical Association, 106:746–762, 2011.

- Gneiting and Raftery (2007) T. Gneiting and A. E. Raftery. Strictly proper scoring rules, prediction, and estimation. Journal of the American Statistical Association, 102:359–378, 2007.

- Gneiting et al. (2007) T. Gneiting, F. Balabdaoui, and A. E. Raftery. Probabilistic forecasts, calibration and sharpness. Journal of the Royal Statistical Society Series B, 69:243–268, 2007.

- Holzmann and Eulert (2014) H. Holzmann and M. Eulert. The role of the information set for forecasting – with applications to risk management. Annals of Applied Statistics, 8:79–83, 2014.

- Lesaffre (2008) E. Lesaffre. Superiority, equivalence, and non-inferiority trials. Bulletin of the NYU Hospital for Joint Diseases, 66:150–154, 2008.

- Weber (2006) S. Weber. Distribution-invariant risk measures, information, and dynamic consistency. Mathematical Finance, 16:419–441, 2006.

- Wong (2008) W. K. Wong. Backtesting trading risk of commercial banks using expected shortfall. Journal of Banking & Finance, 32:1404–1415, 2008.