Selective Inference and Learning Mixed Graphical Models

SELECTIVE INFERENCE AND LEARNING MIXED GRAPHICAL MODELS

A DISSERTATION

SUBMITTED TO THE DEPARTMENT OF COMPUTATIONAL MATH AND ENGINEERING

AND THE COMMITTEE ON GRADUATE STUDIES

OF STANFORD UNIVERSITY

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS

FOR THE DEGREE OF

DOCTOR OF PHILOSOPHY

Jason Dean Lee

March 2024

Abstract

This thesis studies two problems in modern statistics. First, we study selective inference, or inference for hypothesis that are chosen after looking at the data. The motiving application is inference for regression coefficients selected by the lasso. We present the Condition-on-Selection method that allows for valid selective inference, and study its application to the lasso, and several other selection algorithms.

In the second part, we consider the problem of learning the structure of a pairwise graphical model over continuous and discrete variables. We present a new pairwise model for graphical models with both continuous and discrete variables that is amenable to structure learning. In previous work, authors have considered structure learning of Gaussian graphical models and structure learning of discrete models. Our approach is a natural generalization of these two lines of work to the mixed case. The penalization scheme involves a novel symmetric use of the group-lasso norm and follows naturally from a particular parametrization of the model. We provide conditions under which our estimator is model selection consistent in the high-dimensional regime.

Acknowledgements

-

•

I would like to thank my advisors Trevor Hastie and Jonathan Taylor. Trevor has given me the perfect amount of guidance and encouragement through my PhD. I greatly benefited from his numerous statistical and algorithmic insights and intuitions and input on all my projects. Jonathan has been a great mentor throughout my PhD. He has been generous with sharing his ideas and time. With Yuekai Sun, we have spent countless afternoons trying to understand Jonathan’s newest ideas.

-

•

I would like to thank Lester Mackey for serving on my oral exam committee and reading committee. The Stats-ML reading group discussions also introduced me to several new areas of research. I would also like to thank Andrea Montanari and Percy Liang for their spectacular courses and serving on my oral exam committee.

-

•

Emmanuel Candes, John Duchi, and Rob Tibshirani have always been available to provide advice, guiadance, and fantastic courses.

-

•

Yuekai Sun and I have collaborated on many projects. I’ve benefited from his numerous insights, and countless discussions. I am lucky to have a collaborator like Yuekai. I would also like to thank my classmates in ICME for their friendship.

-

•

ICME has been a great place to spend the past 5 years. Margot, Indira, Emily, and Antoinette have kept ICME running smoothly, for which I am very grateful.

-

•

Microsoft Research and Technicolor for hosting me in the summers. In particular, I want to thank my mentors Ran Gilad-Bachrach, Emre Kiciman, Nadia Fawaz, and Brano Kveton for making my summers enjoyable. I would also like to thank the numerous friends I met at Microsoft Research and Technicolor.

-

•

I would like to thank my parents for their unconditional love and support. They are the best parents one could hope for.

Dedicated to my parents Jerry Lee and Tien-Tien Chou.

Chapter 1 Introduction

This thesis is split into two parts: selective inference and learning mixed graphical models. The contributions are summarized below:

-

•

Selective Inference:

-

–

Chapter 2: This chapter studies selective inference for the lasso-selected model. We show how to construct confidence intervals for regression coefficients corresponding to variables selected by the lasso, and how to test the significance of a lasso-selected model by conditioning on the selection event of the lasso. The results of this chapter appear in Lee et al., 2013a and is joint work with Dennis Sun, Yuekai Sun, and Jonathan Taylor.

-

–

Chapter 3: This chapter shows how the Condition-on-Selection method developed in Chapter 2 is not specific to the lasso. In Chapter 3.1, we show that controlling the conditional type 1 error implies control of the selective type 1 error, which motivates the use of the Condition-on-Selection method to control conditional type 1 error. Chapter 3.2 studies several other variable selection methods including marginal screening, orthogonal matching pursuit, and non-negative least squares with affine selection events, so we can apply the results of Chapter 2. Motivated by more complicated selection algorithms that do not simple selection events,such as the knockoff filter, SCAD/MCP regularizers, and -logistic regression, we develop a general algorithm that only requires a blackbox evaluation of the selection algorithm in Chapter 3.3. Finally in Chapter 3.4 we study inference for the full model regression coefficients. We show a method for FDR control, and the asymptotic coverage of selective confidence intervals in the high-dimensional regime. This chapter is joint work with Jonathan Taylor and will appear in a future publication.

-

–

-

•

Learning Mixed Graphical Models:

-

–

We propose a new pairwise Markov random field that generalizes the Gaussian graphical model to include categorical variables.

-

–

We design a new regularizer that promotes edge sparsity in the mixed graphical model.

-

–

Three methods for parameter estimation are proposed: pseudoliklihood, node-wise regression, and maximum likelihood.

-

–

The resulting optimization problem is solved using the proximal Newton method Lee et al., (2012).

-

–

We use the framework of Lee et al., 2013b to establish edge selection consistency results for the MLE and pseudolikelihood estimation methods.

-

–

The results of this chapter originally appeared in Lee and Hastie, (2014) and is joint work with Trevor Hastie.

-

–

Part I Selective Inference

Chapter 2 Selective Inference for the Lasso

2.1 Introduction

As a statistical technique, linear regression is both simple and powerful. Not only does it provide estimates of the “effect” of each variable, but it also quantifies the uncertainty in those estimates, paving the way for intervals and tests of the effect size. However, in many applications, a practitioner starts with a large pool of candidate variables, such as genes or demographic features, and does not know a priori which are relevant. The problem is especially acute if there are more variables than observations, when it is impossible to even fit linear regression.

A practitioner might wish to use the data to select the relevant variables and then make inference on the selected variables. As an example, one might fit a linear model, observe which coefficients are significant at level , and report -confidence intervals for only the significant coefficients. However, these intervals fail to take into account the randomness in the selection procedure. In particular, the intervals do not have the stated coverage once one marginalizes over the selected model.

To see this formally, assume the usual linear model

| (2.1.1) |

where is the design matrix and . Let denote a (random) set of selected variables. Suppose the goal is inference about . Then, we do not even form intervals for when , so the first issue is to define an interval when in order to evaluate the coverage of this procedure. There is no obvious way to do this so that the marginal coverage is . Furthermore, as varies, the target of the ordinary least-squares (OLS) estimator is not , but rather

where denotes the Moore-Penrose pseudoinverse of . We see that , the projection of onto the columns of , so represents the coefficients in the best linear model using only the variables in . In general, unless contains the support set of , i.e., . Since may not be estimating at all, there is no reason to expect a confidence interval based on it to cover . Berk et al., (2013) provide an explicit example of the non-normality of in the post-selection context. In short, inference in the linear model has traditionally been incompatible with model selection.

2.1.1 The Lasso

In this paper, we focus on a particular model selection procedure, the lasso (Tibshirani,, 1996), which achieves model selection by setting coefficients to zero exactly. This is accomplished by adding an penalty term to the usual least-squares objective:

| (2.1.2) |

where is a penalty parameter that controls the tradeoff between fit to the data and sparsity of the coefficients. However, the distribution of the lasso estimator is known only in the less interesting case (Knight and Fu,, 2000), and even then, only asymptotically. Inference based on the lasso estimator is still an open question.

We apply our framework for post-selection inference about to form confidence intervals for and to test whether the the fitted model captures all relevant signal variables.

2.1.2 Related Work

Most of the theoretical work on fitting high-dimensional linear models focuses on consistency. The flavor of these results is that under certain assumptions on , the lasso fit is close to the unknown (Negahban et al.,, 2012) and selects the correct model (Zhao and Yu,, 2006; Wainwright,, 2009). A comprehensive survey of the literature can be found in Bühlmann and van de Geer, (2011).

There is also some recent work on obtaining confidence intervals and significance testing for penalized M-estimators such as the lasso. One class of methods uses sample splitting or subsampling to obtain confidence intervals and p-values. Recently, Meinshausen and Bühlmann, (2010) proposed stability selection as a general technique designed to improve the performance of a variable selection algorithm. The basic idea is, instead of performing variable selection on the whole data set, to perform variable selection on random subsamples of the data of size and include the variables that are selected most often on the subsamples.

A separate line of work establishes the asymptotic normality of a corrected estimator obtained by “inverting” the KKT conditions (van de Geer et al.,, 2013; Zhang and Zhang,, 2014; Javanmard and Montanari,, 2013). The corrected estimator usually has the form

where is a subgradient of the penalty at and is an approximate inverse to the Gram matrix . This approach is very general and easily handles M-estimators that minimize the sum of a smooth convex loss and a convex penalty. The two main drawbacks to this approach are:

-

1.

the confidence intervals are valid only when the M-estimator is consistent

-

2.

obtaining is usually much more expensive than obtaining .

Most closely related to our work is the pathwise signficance testing framework laid out in Lockhart et al., (2014). They establish a test for whether a newly added coefficient is a relevant variable. This method only allows for testing at that are LARS knot values. This is a considerable restriction, since the lasso is often not solved with the LARS algorithm. Furthermore, the test is asymptotic, makes strong assumptions on , and the weak convergence assumes that all relevant variables are already included in the model. They do not discuss forming confidence intervals for the selected variables. Section 2.5.2 establishes a nonasymptotic test for the same null hypothesis, while only assuming is in general position.

In contrast, we provide a test that is exact, allows for arbitrary , and arbitrary design matrix . By extension, we do not make any assumptions on and , and do not require the lasso to be a consistent estimator of . Furthermore, the computational expense to conduct our test is negligible compared to the cost of obtaining the lasso solution.

Like all of the preceding works, our test assumes that the noise variance is known or can be estimated. In the low-dimensional setting , can be estimated from the residual sum-of-squares of the saturated model. Strategies in high dimensions are discussed in Fan et al., (2012) and Reid et al., (2013). In Section 2.8, we also provide a strategy for estimating based on the framework we develop.

2.1.3 Outline of Chapter

We begin by defining several important quantities related to the lasso in Section 2.2; most notably, we define the selected model in terms of the active set of the lasso solution. Section 2.3 provides an alternative characterization of the selection procedure for the lasso in terms of affine constraints on , i.e., . Therefore, the distribution of conditional on the selected model is the distribution of a Gaussian vector conditional on its being in a polytope. In Section 2.4, we generalize and show that for , the distribution of is roughly a truncated Gaussian random variable, and derive a pivot for . In Section 2.5, we specialize again to the lasso, deriving confidence intervals for and hypothesis tests of the selected model as special cases of . Section 2.6 presents an example of these methods applied to a dataset.

In Section 2.7, we consider a refinement that produces narrower confidence intervals. Finally, Section 2.8 collects a number extensions of the framework. In particular, we demonstrate:

-

•

modifications needed for the elastic net (Zou and Hastie,, 2005).

-

•

different norms as test statistics for the “goodness of fit” test discussed in Section 2.5.

-

•

estimation of based on fitting the lasso with a sufficiently small .

-

•

composite null hypotheses.

-

•

fitting the lasso for a sequence of values and its effect on our basic tests and intervals.

2.2 Preliminaries

Necessary and sufficient conditions for to be solutions to the lasso problem (2.1.2) are the Karush-Kuhn-Tucker (KKT) conditions:

| (2.2.1) | |||

| (2.2.2) |

where denotes the subgradient of the norm at . We consider the active set (Tibshirani,, 2013)

| (2.2.3) |

so-named because by examining only the rows corresponding to in (2.2.1), we obtain the relation

where is the submatrix of consisting of the columns in . Hence

i.e. the variables in this set have equal (absolute) correlation with the residual . Since for any , all variables with non-zero coefficients are contained in the active set.

Recall that we are interested in inference for in the model (2.1.1) for some direction , which is allowed to depend on the selected variables . In most applications, we will assume , although our results hold even if the linear model is not correctly specified.

A natural estimate for is . As mentioned previously, we allow to depend on the random selection procedure, so our goal is post-selection inference based on

For reasons that will become clear, a more tractable quantity is the distribution conditional on both the selected variables and their signs

Note that confidence intervals and hypothesis tests that are valid conditional on the finer partition will also be valid for , by summing over the possible signs :

From this, it is clear that controlling to be, say, less than (as in the case of hypothesis testing) will ensure .

It may not be obvious yet why we condition on instead of . In the next section, we show that the former can be restated in terms of affine constraints on , i.e., . We revisit the problem of conditioning only on in Section 2.7.

2.3 Characterizing Selection for the Lasso

Recall from the previous section that our goal is inference conditional on . In this section, we show that this selection event can be rewritten in terms of affine constraints on , i.e.,

for a suitable matrix and vector . Therefore, the conditional distribution is simply . This key theorem follows from two intermediate results.

Lemma 2.3.1.

Without loss of generality, assume the columns of are in general position. Let and be a candidate set of variables and signs, respectively. Define

| (2.3.1) | ||||

| (2.3.2) |

Then the selection procedure can be rewritten in terms of and as:

| (2.3.3) |

Proof.

First, we rewrite the KKT conditions (2.2.1) and (2.2.2) by partitioning them according to the active set :

Since the KKT conditions are necessary and sufficient for a solution, we obtain that if and only if there exist and satisfying:

| (2.3.4) | |||

| (2.3.5) | |||

| (2.3.6) |

Solving (2.3.4) and (2.3.5) for and yields the formulas (2.3.1) and (2.3.2). Finally, the requirement that and satisfy (2.3.6) yields (2.3.3). ∎

Lemma 2.3.1 is remarkable because it says that the selection event is equivalent to affine constraints on . To see this, note that both and are affine functions of , so can be written as affine constraints . The following proposition provides explicit formulas for and .

Proposition 2.3.2.

Proof.

Theorem 2.3.3.

The selection procedure can be rewritten in terms of affine constraints on :

To summarize, we have shown that in order to understand the distribution of conditional on the selection procedure , it suffices to study the distribution of conditional on being in the polytope . The next section derives a pivot for for such distributions, which will be useful for constructing confidence intervals and hypothesis tests in Section 2.5.

2.4 A Pivot for Gaussian Vectors Subject to Affine Constraints

The distribution of a Gaussian vector conditional on affine constraints , while explicit, still involves the intractable normalizing constant . In this section, we show that one dimensional projections of (i.e., ) are univariate truncated normal, which will allow us to form tests and intervals for .

The key to deriving this pivot is the following lemma:

Lemma 2.4.1.

The conditioning set can be rewritten in terms of as follows:

where

| (2.4.1) | ||||

| (2.4.2) | ||||

| (2.4.3) | ||||

| (2.4.4) |

Furthermore, is independent of . Then, conditioned on and , has a truncated normal distribution, i.e.

However, before stating the proof of this lemma, we show how it is used to obtain our main result.

Theorem 2.4.2.

Proof.

By Lemma 2.4.1, . We apply the CDF transform to deduce

is uniformly distributed. By integrating over , we conclude . Let .

∎

We now prove Lemma 2.4.1.

Proof.

The linear constraints are equivalent to

| (2.4.7) |

Since conditional expectation has the form

(2.4.7) simplifies to . Rearranging, we obtain

We take the max of the lower bounds and min of the upper bounds to deduce

Since is normal, are independent of . Hence are also independent of .

To complete the proof, we must show given , is truncated normal.

where the second to last equality follows from the independence of and . This is the CDF of a truncated normal. ∎

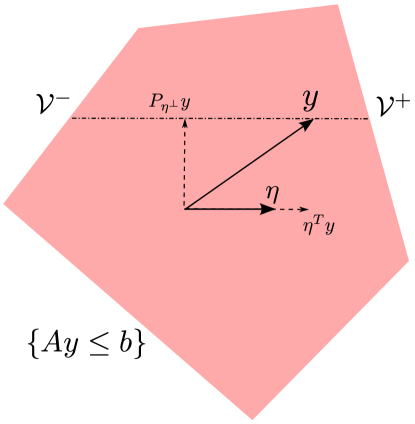

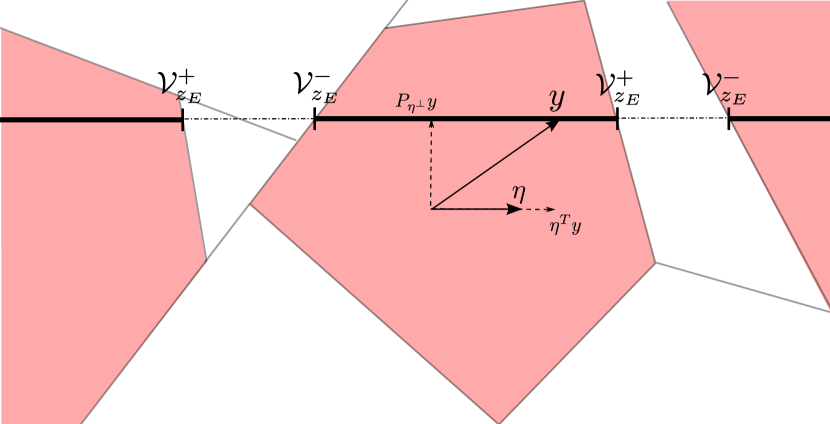

Although the proof of Lemma 2.4.1 is elementary, the geometric picture gives more intuition as to why and are independent of . Without loss of generality, we assume and (since otherwise we could replace by ). Now we can decompose into two independent components, a 1-dimensional component and an -dimensional component orthogonal to :

The case of is illustrated in Figure 2.1. and are independent of , since they are functions of only, which is independent of .

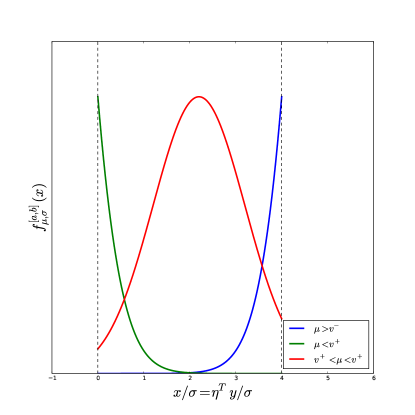

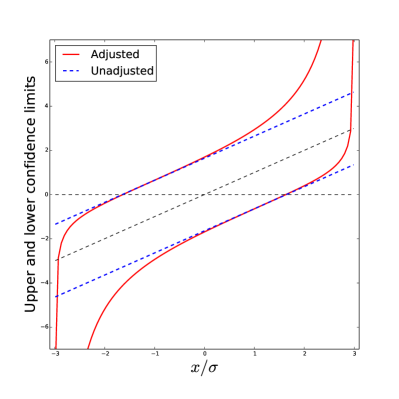

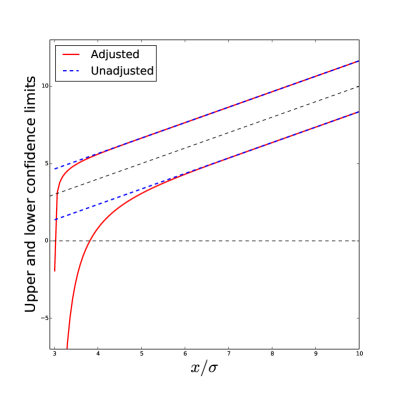

In Figure 2.2, we plot the density of the truncated Gaussian, noting that its shape depends on the location of relative to as well as the width relative to .

2.4.1 Adaptive choice of

For the applications to forming confidence intervals and significance testing, we will need choices of that are adaptive, or dependent on . We will restrict ourselves to functions that are functions of the partition, . This choice of functions includes which is used for forming confidence intervals in Section 2.5.

Theorem 2.4.3.

Let be a function of the form , then

Proof.

2.5 Application to Inference for the Lasso

In this section, we apply the theory developed in in Sections 2.3 and 2.4 to the lasso. In particular, we will construct confidence intervals for the active variables and test the chosen model based on the pivot developed in Section 2.4.

To summarize the developments so far, recall that our model says that . The distribution of interest is . By Theorem 2.3.1, this is equivalent to defined in Proposition 2.3.2. Now we can apply Theorem 2.4.2 to obtain the (conditional) pivot

| (2.5.1) |

for any , where and are defined in (2.4.2) and (2.4.3). Note that and appear in this pivot through and . This pivot will play a central role in all of the applications that follow.

2.5.1 Confidence Intervals for the Active Variables

In this section, we describe how to form confidence intervals for the components of . If we choose

| (2.5.2) |

then , so the above framework provides a method for inference about the variable in the model . Note that this reduces to inference about the true if , as discussed in Section 2.1. Conditions under which this holds are well known in the literature, cf. Bühlmann and van de Geer, (2011), and provided in Section 2.11.

By applying Theorem 2.4.2, we obtain the following (conditional) pivot for :

Note that and are both random—but only through , a quantity which is fixed after conditioning—so Theorem 2.4.2 holds even for this “random” choice of . The obvious way to obtain an interval is to “invert” the pivot. In other words, since

one can define a (conditional) confidence interval for as

In fact, is monotone decreasing in , so to find its endpoints, one need only solve for the root of a smooth one-dimensional function. The monotonicity is a consequence of the fact that the truncated Gaussian distribution is a natural exponential family and hence has monotone likelihood ratio in . The details can be found in Appendix 2.10.1.

We now formalize the above observations in the following result, an immediate consequence of Theorem 2.4.2.

Corollary 2.5.1.

Let be defined as in (2.5.2), and let and be the (unique) values satisfying

Then is a confidence interval for , conditional on :

| (2.5.3) |

The above discussion has focused on constructing intervals for a single . If we repeat the procedure for each , our intervals in fact control the false coverage rate (FCR) of Benjamini and Yekutieli, (2005).

Corollary 2.5.2.

For each ,

| (2.5.4) |

Furthermore, the FCR of the intervals is .

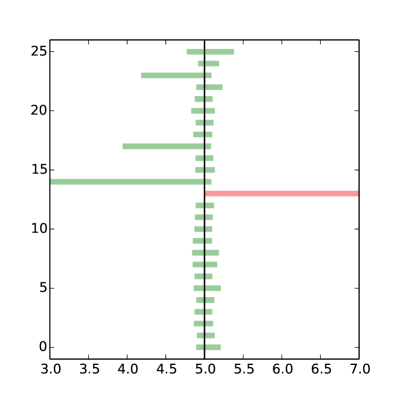

If are not near the boundaries , then the intervals will be relatively short. This is shown in Figure 2.4. Figure 2.5 shows two simulations that demonstrate our intervals cover at the nominal rate. We leave an exhaustive study of such intervals for the lasso to future work, noting that the truncation framework described can be used to form intervals with exact coverage properties.

2.5.2 Testing the Lasso-Selected Model

Having observed that the lasso selected the variables , another relevant question is whether it has captured all of the signal in the model, i.e.,

| (2.5.5) |

We consider a slightly more general question, which does not assume the correctness of the linear model and also takes into account whether the non-selected variables can improve the fit:

| (2.5.6) |

This quantity is the partial correlation of the non-selected variables with , adjusting for the variables in . This is more general because if we assume for some and is full rank, then rejecting (2.5.6) implies that there exists not in , so we would also reject (2.5.5).

The natural approach is to compare the observed partial correlations to . However, the framework of Section 2.4 only allows tests of in a single direction . To make use of that framework, we can choose such that it selects the maximum magnitude of . In particular, this direction provides the most evidence against the null hypothesis of zero partial correlation, so if the null hypothesis cannot be rejected in this direction, it would not be rejected in any direction.

Letting and , we set

| (2.5.7) |

and test . However, the results in Section 2.4 cannot be directly applied to this setting because and are random variables that are not measurable with respect to .

To resolve this issue, we propose a test conditional not only on , but also on the index and sign of the maximizer:

| (2.5.8) |

A test that is level conditional on (2.5.8) for all and is also level conditional on .

In order to use the results of Section 2.4, we must show that (2.5.8) can be written in the form . This is indeed possible, and the following proposition provides an explicit construction.

Proposition 2.5.3.

Let be defined as in Proposition 2.3.2. Then:

where is defined as

and and are operators that compute the difference and sum, respectively, of the element with the other elements, e.g.,

Proof.

The constraints and come from Proposition (2.3.2) and encode the constraints . We show that the last two sets of constraints encode .

Let denote the vector of partial correlations. If , then for all if and only if and for all . We can write this as and . If , then the signs are flipped: and . This establishes

∎

Because of Proposition 2.5.3, we can now obtain the following result as a simple consequence of Theorem 2.4.2, which says that , conditional on the set (2.5.8) and . We reject when is large because is monotone increasing in the argument and is likely to be positive under the alternative.

Corollary 2.5.4.

Let and be defined as in (2.5.7). Then, the test which rejects when

is level , conditional on . That is,

| In particular, since this holds for every , this test also controls Type I error conditional only on , and unconditionally: | |||

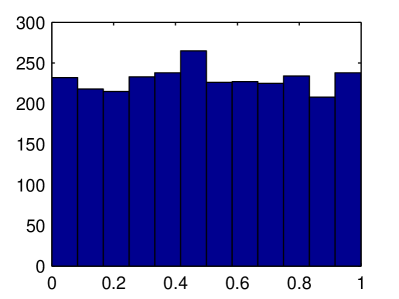

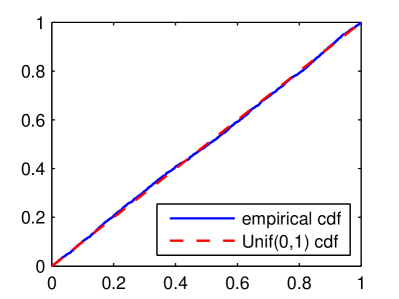

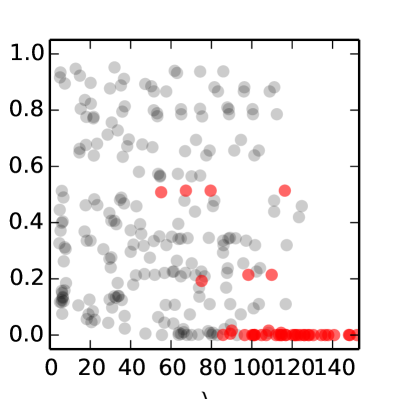

Figures 2.6 and 2.7 show the results of four simulation studies that demonstrate that the p-values are uniformly distributed when is true and stochastically smaller than when it is false.

2.6 Data Example

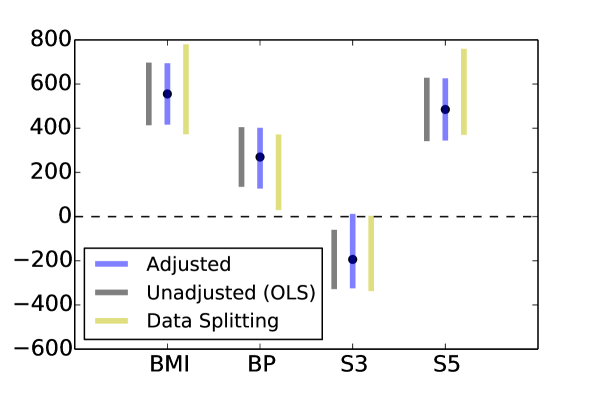

We illustrate the application of inference for the lasso to the diabetes data set from Efron et al., (2004). First, all variables were standardized. Then, we chose according to the strategy in Negahban et al., (2012), , using an estimate of from the full model, resulting in . The lasso selected four variables: BMI, BP, S3, and S5.

The intervals are shown in Figure 2.8, alongside the unadjusted confidence intervals produced by fitting OLS to the four selected variables, ignoring the selection. The latter is not a valid confidence interval conditional on the model. Also depicted are the confidence intervals obtained by data splitting; that is, if one splits the observations into two halves, then uses one half for model selection and the other for inference. This is a competitor method that also produces valid confidence intervals conditional on the model. In this case, data splitting selected the same four variables, and the confidence intervals were formed based on OLS on the half of the data set not used for model selection.

We can make two main observations from Figure 2.8.

-

1.

The adjusted intervals provided by our method essentially reproduces the OLS intervals for the strong effects, whereas data splitting results in a loss of power by roughly a factor of (since only observations are used in the inference).

-

2.

One variable,

S3, which would have been deemed significant using the OLS intervals, is no longer significant after adjustment. This demonstrates that taking model selection into account can have substantive impacts on the conclusions that are made.

2.7 Minimal Post-Selection Inference

We have described how to perform post-selection inference for the lasso conditional on both the active set and signs . However, recall from Section 2.1 that the goal was inference conditional solely on the model, i.e., . In this section, we extend our framework to this setting, which we call minimal post-selection inference because we condition on the minimal set necessary for the random to be measurable. This results in more precise confidence intervals at the expense of greater computational cost.

To this end, we note that is simply

where the union is taken over all choices of signs. Therefore, the distribution of conditioned on only the active set is a Gaussian vector constrained to a union of polytopes

where and are given by (2.3.2).

To obtain inference about , we follow the arguments in Section 2.4 to obtain that this conditional distribution is equivalent to

| (2.7.1) |

where are defined according to (2.4.2), (2.4.3), (2.11.4) with and . Moreover, all of these quantities are still independent of , so instead of having a Gaussian truncated to a single interval as in Section 2.4, we now have a Gaussian truncated to the union of intervals . The geometric intuition is illustrated in Figure 2.9.

Finally, the probability integral transform once again yields a pivot:

It is now more useful to think of the notation of as indicating the truncation set :

| (2.7.2) |

where is the law of a random variable. We summarize these results in the following theorem.

Theorem 2.7.1.

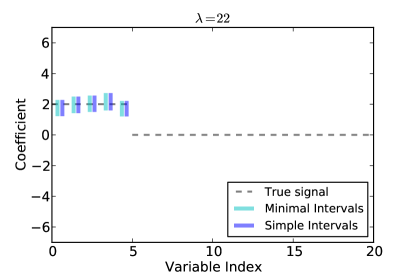

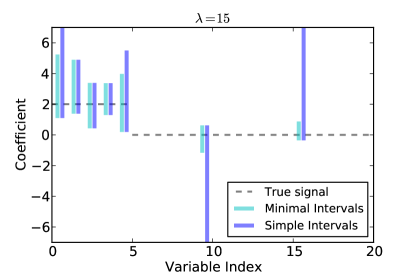

The derivations of the confidence intervals and hypothesis tests in Section 2.5 remain valid using (2.7.3) as the pivot instead of (2.5.1). Figure 2.10 illustrates the effect of minimal post-selection inference in a simulation study, as compared with the “simple” inference described previously. The intervals are similar in most cases, but one can obtain great gains in precision using the minimal intervals when the simple intervals are very wide.

However, the tradeoff for this increased precision is greater computational cost. We computed and for all , which is only feasible when is fairly small. In what follows, we revert to the simple intervals described in Section 2.5, but extensions to the minimal inference setting are straightforward.

2.8 Extensions

2.8.1 Elastic net

One problem with the lasso is that it tends to select only one variable out of a set of correlated variables, resulting in estimates which are unstable. The elastic net (Zou and Hastie,, 2005) adds an penalty to the lasso objective in order to stabilize the estimates:

| (2.8.1) |

Using a nearly identical argument to the one in Section 2.3, we see that necessary and sufficient conditions for are the existence of and satisfying

Solving for and , we see that the selection event can be written

| (2.8.2) |

where , , , and are the same as in Proposition 2.3.2, except replacing , which appears in the expressions through and , by the “damped” version .

2.8.2 Alternative norms as test statistics

In Section 2.5.2 we used the test statistic

and its conditional distribution on to test whether we had missed any large partial correlations in using as the estimated active set. If we have indeed missed some variables in there is no reason to suppose that the mean of is sparse; hence the norm may not be the best norm to use as a test statistic.

In principle, we could have used virtually any norm, as long as we can say something about the distribution of this norm conditional on . Problems of this form are considered in Taylor et al., (2013). For example, if we consider the quadratic

the general approach in Taylor et al., (2013) derives the conditional distribution of conditioned on

In general, this distribution will be a subject to random truncation as in Section 2.4 (see the group lasso examples in Taylor et al., (2013)). Adding the constraints encoded by affects only the random truncation .

2.8.3 Estimation of

As noted above, all of our results rely on a reliable estimate of . While there are several approaches to estimating in the literature, the truncated Gaussian theory described in this work itself provides a natural estimate.

Suppose the linear model is correct (). Then, on the event , which we assume, the residual

is a (multivariate) truncated Gaussian with mean , with law

As , one obtains a one-parameter exponential family with density

and natural parameter . On the event , we set

and then choose (or equivalently, ) to satisfy the score equation

| (2.8.3) |

This amounts to a maximum likelihood estimate of . The expectation on the left is generally impossible to do analytically, but there exist fast algorithms for sampling from , c.f. Geweke, (1991); Rodriguez-Yam et al., (2004). A rough outline of a naive version of such algorithms is to pick a direction such as one of the coordinate axes. Based on the current state of , draw a new entry for the from the appropriate univariate truncated normal determined from the cutoffs described in Section 2.4. We repeat this procedure to evaluate the expectation on the left, and use gradient descent to find .

2.8.4 Composite Null Hypotheses

In Section 2.5, we considered hypotheses of the form , which said that the partial correlation of the variables in with , adjusting for the variables in , was exactly 0. This may be unrealistic, and in practice, we may want to allow some tolerance for the partial correlation.

We consider testing instead the composite hypothesis

| (2.8.4) |

The following result characterizes a test for .

Proposition 2.8.1.

The test which rejects when is exact level .

Proof.

Let . Define . Then:

| Type I error | |||

Next, we have that , i.e., the infimum is achieved at , so calculating is a simple matter of evaluating . This follows from the fact that is monotone decreasing in (c.f. Appendix 2.10.1).

Finally, the Type I error is exactly because the reverse inequality also holds:

∎

Although the test is exact level , the significance level of a test for a composite null is a “worst-case” Type I error; for most values of such that , the Type I error will be less than , so the test will be conservative. Of course, what we lose in power, we gain in robustness to the assumption that exactly.

2.8.5 How long a lasso should you use?

Procedures for fitting the lasso, such as glmnet (Friedman et al., 2010b, ), solve (2.1.2) for a decreasing sequence of values starting from . The framework developed so far provides a means to decide when to stop along the regularization path, i.e., when the lasso has done enough “fitting.” In this section, we describe a path-wise testing procedure for the lasso,

The path-wise procedure is simple. At each value of :

-

1.

Solve the lasso and obtain an active set and signs .

-

2.

Test at level . Rather than being conditional on only , this test is conditional on the entire sequence of active sets and signs , as we describe below.

As decreases, we expect to reject the null hypotheses as the fit improves and stop once the first null hypothesis has been accepted.

To understand the properties of this procedure, we formalize it as a multiple testing problem. For each value , we test . We test these hypotheses sequentially and stop after the first hypothesis has been accepted. Implicitly, this means that we accept all the remaining hypotheses.

Our next result shows that this procedure controls the family-wise error rate (FWER) at level . Let denote that number of false rejections. Then FWER is defined as . The practical implication of this result is the model selected by this procedure will be larger than the true model with probability .

Proposition 2.8.2.

The path-wise testing procedure controls FWER at level .

Proof.

Let and denote the complete sequence of active sets and signs at , i.e.,

We seek to control the family-wise error rate (FWER) when testing the hypotheses , i.e., . We partition the space over all possible sequences and :

Since , we can ensure by ensuring

Let denote the first for which is true. Then the event is equivalent to the event that we reject because the preceding hypotheses are all false so we cannot make a false discovery before the hypothesis. Thus

Therefore, we can control FWER at level by ensuring

for each . ∎

To perform a test of conditioned on , we apply the framework of Section 2.4. Let

be the affine constraints that characterize the event from Proposition 2.3.2. The event is equivalent to the intersection of all of these constraints:

Now Theorem 2.4.2 applies, and we can obtain the usual pivot as a test statistic.

2.9 Conclusion

We have described a method for making inference about in the linear model based on the lasso estimator, where is chosen adaptively after model selection. The confidence intervals and tests that we propose are conditional on . In contrast to existing procedures on inference for the lasso, we provide a pivot whose conditional distribution can be characterized exactly (non-asymptotically). This pivot can be used to derive confidence intervals and hypothesis tests based on lasso estimates anywhere along the solution path, not necessarily just at the knots of the LARS path as in Lockhart et al., (2014). Finally, our test is computationally simple: the quantities required to form the test statistic are readily available from the solution of the lasso.

2.10 Appendix

2.10.1 Monotonicity of

Lemma 2.10.1.

Let denote the cumulative distribution function of a truncated Gaussian random variable, as defined as in (2.4.5). Then is monotone decreasing in .

Proof.

First, the truncated Gaussian distribution with CDF is a natural exponential family in , since it is just a Gaussian with a different base measure. Therefore, it has monotone likelihood ratio in . That is, for all and :

where denotes the density. (Instead of appealing to properties of exponential families, this property can also be directly verified.)

This implies

Therefore, the inequality is preserved if we integrate both sides with respect to on for . This yields:

Now we integrate both sides with respect to on to obtain:

which establishes for all . ∎

2.11 Lasso Screening Property

In this section, we state some sufficient conditions that guarantee . Let and . The results of this section are well known in the literature and can be found in (Bühlmann and van de Geer,, 2011, Chapter 2.5).

Definition 2.11.1 (Restricted Eigenvalue Condition).

Restricted eigenvalue condition requires that satisfy

for all .

Definition 2.11.2 (Beta-min Condition).

The beta-min condition requires that for all ,

Theorem 2.11.3.

Let , where is subgaussian with parameter , and be the solution to 2.1.2 with . Assume that satisfies the restricted eigenvalue condition, satisfies the beta-min condition with , and is column normalized, . Then .

Proof.

From (Negahban et al.,, 2012, Corollary 2),

Assume that their is a such that , but . We must have

This is a contradiction, so for all we have . ∎

Next we provide a geometric proof of Lemma 2.4.1 which will be useful in the next chapter.

Lemma 2.11.4.

The conditioning set can be rewritten in terms of as follows:

where

| (2.11.1) | ||||

| (2.11.2) | ||||

| (2.11.3) | ||||

| (2.11.4) |

Moreover, are independent of .

Proof.

Although the proof of Lemma 2.11.4 is elementary, the geometric picture gives more intuition as to why and are independent of . Since is assumed known, let so that . We can decompose into two independent components: a one-dimensional component along and a -dimensional component orthogonal to :

From Figure 2.1, it is clear that the extent of the set (i.e., and ) along the direction depends only on and is hence independent of . We present a geometric derivation below. The values and are the maximum and minimum possible values of , holding fixed, while remaining inside the polytope . Writing where is allowed to vary, and are the optimal values of the optimization problems:

| max. / min. | |||

| subject to |

Rewriting this problem in terms of the original variables and , we obtain:

| max. / min. | |||

| subject to |

Since is the only free variable, we see from the constraints that the optimal values and are precisely those given in (2.4.2) and . ∎

Chapter 3 Condition-on-Selection Method

In the previous chapter, we focused on selective inference for the sub-model coefficients selected by the lasso by conditioning on the event that lasso selects a certain subset of variables. However the procedure we developed is not restricted to the sub-model coefficients, nor is it restricted to the lasso. In Lee and Taylor, (2014), we used the same Condition-on-Selection (COS) method for marginal screening, orthogonal matching pursuit, and screening+lasso variable selection methods.

In this chapter, we first discuss some definitions and formalism, which will help us understand how to generalize the results of Chapter 2 to other selection procedures. In Section 3.1, we see that the COS method results in tests that control the selective type 1 error. Then in Section 3.2, we show how the selection events for several variable selection methods such as marginal screening, and orthogonal matching pursuit are affine in the response . For non-affine selection events, we propose a general algorithm in Section 3.3. We then describe inference for the full model regression coefficients, provide a method for FDR control and establish the asymptotic coverage property in the high-dimensional setting in Section 3.4. Finally in Section 3.5, we show how to construct selectively valid confidence intervals for regression coefficients selected by the knockoff filter (Foygel Barber and Candes,, 2014).

3.1 Formalism

This section closely follows the development in Fithian et al., (2014), which in turn uses the COS method developed in earlier works Lee and Taylor, (2014); Lee et al., 2013a ; Taylor et al., (2014). Our main result of this section is to show that tests constructed using the COS method control selective type 1 error. This is the original motivation of Lee and Taylor, (2014); Lee et al., 2013a for designing tests with the COS method.

We start off by defining a valid test in the classical setting.

Definition 3.1.1 (Valid test).

Let be a hypothesis, and is a test of meaning we reject if . is a valid test of if

for all null with respect to , meaning , where is the set of distributions null with respect to .

For selective inference, there is an analog of type 1 error.

Definition 3.1.2 (Selective Type 1 Error ).

is a valid test of the hypothesis if it controls the selective type 1 error,

The framework laid out in Chapter 2 proposes controlling the selective type 1 error via the COS method. As we showed in the case of confidence intervals for regression coefficients and goodness-of-fit tests, by conditioning on the lasso selection event, we are guaranteed to control the conditional type 1 error by design, and this implies the control of the unconditional type 1 error. We now show that this is not specific to the lasso; in fact controlling the conditional type 1 error always controls the unconditional type 1 error in Definition 3.1.2.

Definition 3.1.3.

Let be the hypothesis space. The selection algorithm maps data to hypothesis. This induces the selection event .

The following definition motivates the construction in Equation (2.5.3).

Definition 3.1.4 (Condition-on-Selection method).

A test is constructed via the Condition-on-Selection (COS) method if for all

| (3.1.1) |

This means that controls the conditional type 1 error rate.

By a simple generalization of the argument in Theorem 2.4.3, we show that using the COS method to design a conditional test 3.1.1 implies control of the selective type 1 error 3.1.2.

Theorem 3.1.5 (Selective Type 1 Error control).

A test constructed using the COS method, i.e. satisfies (3.1.1), controls the selective type 1 error meaning

Proof.

where all of the previous probabilities are with respect to the distribution . The first equality is the law of total probability, and the second equality is breaking the sum over disjoint sets. Since , implies , so , which establishes the third equality. The fourth equality is the definition of conditional probability, and the fifth follows from noticing that . The sixth equality uses the COS property of : for any . Finally, the result follows since probabilities sum to less than or equal to 1. ∎

This result allows us to interpret the tests constructed via the COS method as unconditionally valid.

3.2 Marginal Screening, Orthogonal Matching Pursuit, and other Variable Selection methods

In lieu of the developments of the previous section, it is clear that the COS method developed for affine selection events in Chapter 2 is not specific to the lasso. By changing the variable selection method, we are simply changing the selection algorithm and the selection event. The main work is in characterizing the selection event , the event that the variable selection methods chooses the subset . In this section, we characterize the selection event for several variable selection methods: marginal screening, orthogonal matching pursuit (forward stepwise), non-negative least squares, and marginal screening+lasso.

3.2.1 Marginal Screening

In the case of marginal screening, the selection event corresponds to the set of selected variables and signs :

| (3.2.1) |

for some matrix .

3.2.2 Marginal screening + Lasso

The marginal screening+Lasso procedure was introduced in Fan and Lv, (2008) as a variable selection method for the ultra-high dimensional setting of . Fan et al. Fan and Lv, (2008) recommend applying the marginal screening algorithm with , followed by the Lasso on the selected variables. This is a two-stage procedure, so to properly account for the selection we must encode the selection event of marginal screening followed by Lasso. This can be done by representing the two stage selection as a single event. Let be the variables and signs selected by marginal screening, and the be the variables and signs selected by Lasso. In Proposition 2.2 of Lee et al., 2013a , it is shown how to encode the Lasso selection event as a set of constraints 111The Lasso selection event is with respect to the Lasso optimization problem after marginal screening., and in Section 3.2.1 we showed how to encode the marginal screening selection event as a set of constraints . Thus the selection event of marginal screening+Lasso can be encoded as .

3.2.3 Orthogonal Matching Pursuit

Orthogonal matching pursuit (OMP) is a commonly used variable selection method 222OMP is sometimes known as forward stepwise regression.. At each iteration, OMP selects the variable most correlated with the residual , and then recomputes the residual using the residual of least squares using the selected variables. The description of the OMP algorithm is given in Algorithm 1.

The OMP selection event as a set of linear constraints on .

The selection event encodes that OMP selected a certain variable and the sign of the correlation of that variable with the residual, at steps to . The primary difference between the OMP selection event and the marginal screening selection event is that the OMP event also describes the order at which the variables were chosen. The marginal screening event only describes that the variable was among the top most correlated, and not whether a variable was the most correlated or most correlated.

3.2.4 Nonnegative Least Squares

Non-negative least squares (NNLS) is a simple modification of the linear regression estimator with non-negative constraints on :

| (3.2.2) |

Under a positive eigenvalue conditions on , several authors Slawski et al., (2013); Meinshausen et al., (2013) have shown that NNLS is comprable to the Lasso in terms of prediction and estimation errors. The NNLS estimator also does not have any tuning parameters, since the sign constraint provides a natural form of regularization. NNLS has found applications when modeling non-negative data such as prices, incomes, count data. Non-negativity constraints arise naturally in non-negative matrix factorization, signal deconvolution, spectral analysis, and network tomography; we refer to Chen and Plemmons, (2009) for a comprehensive survey of the applications of NNLS.

We show how our framework can be used to form exact hypothesis tests and confidence intervals for NNLS estimated coefficients. The primal dual solution pair is a solution iff the KKT conditions are satisfied,

Let . By complementary slackness , where is the complement to the “active” variables chosen by NNLS. Given the active set we can solve the KKT equation for the value of ,

which is a linear contrast of . The NNLS selection event is

The selection event encodes that for a given the NNLS optimization program will select a subset of variables .

3.2.5 Logistic regression with Screening

The focus up to now has been on the linear regression estimator with additive Gaussian noise. In this section, we discuss extensions to conditional MLE (maximum likelihood estimator) such as logistic regression. This section is meant to be speculative and non-rigorous; our goal is only to illustrate that these tools are not restricted to the linear regression. A future publication will rigorously develop the inferential framework for conditional MLE.

Consider the logistic regression model with loss function and gradient below,

where is the sigmoid function applied entrywise. By taylor expansion, the empirical estimator is given by

By the Lindeberg CLT (central limit theorem), , and thus converges to a Gaussian. The marginal screening selection procedure can be expressed as a set of inequalities . Thus conditional on the selection, is approximately a constrained Gaussian. The framework in Chapter 2.4 and 3.1 can be applied to , instead of , to derive hypothesis tests and confidence intervals for the coefficients of logistic regression. The resulting test and confidence intervals should be correct asymptotically. However, this is the best we can expect for logistic regression and other conditional MLE because even in the classical case the Wald test is only asymptotically correct. For other conditional maximum likelihood estimator similar reasoning applies, since the gradient converges in distribution to a Gaussian.

For logistic regression with regularizer, the selection event cannot be analytically described. However, the COS method can still be applied using the general method presented in Chapter 3.3.

3.3 General method for Selective inference

In this section, we describe a computationally-intensive algorithm for finding selection events, when they are not easily described analytically.

We first review the construction used in Chapter 2 for affine selection events. Let . Recall that can be decomposed into two independent components . This is derived by defining and . can be orthogonally decomposed as , so

Lemma 2.4.1 shows that

We can generalize this result to arbitrary selection events, where the selection event is not explicitly describable. Recall that is a selection algorithm that maps . The selection event is , so . In the upcoming section, it will be convenient to work with the definition using , since the set cannot be described, but the function can be efficiently computed. Thus we can only verify if a point .

The following Theorem is a straightforward generalization of Theorem 2.4.2 from polyhedral sets to arbitrary sets .

Theorem 3.3.1 (Arbitrary selection events).

Let be a multivariate truncated normal, so . Then

and .

Proof.

We know that , so is a univariate normal truncated to some region . The goal is to check that . We can describe the conditioning set as

Thus we have that

where the second equality follows from independence of and . ∎

3.3.1 Computational Algorithm for arbitrary selection algorithms

In this section, we study the case of where the set cannot be explicitly described, but the function is easily computable. Our goal will be to approximately compute the p-value , where is the cdf of .

Algorithm 2 is the primary contribution of this section. This allows us to compute the pivotal quantity for algorithms with difficult to describe selection events. This includes linear regression with the SCAD/MCP regularizers, and logistic regression with -regularizer, where the selection events do not have analytical forms.

Let be the pdf of a univariate truncated normal with mean and variance .

Algorithm 2 gives an approximate p-value for the null hypothesis . The advantage of this algorithm is it does not need an explicit description of the set , nor the set . It runs the selection algorithm at the grid points , and determines if the point is in the selection event. Then it approximates the CDF of the univariate truncated normal by a discrete truncated normal.

Conjecture 3.3.2.

Let be a set of grid points grid points that is equispaced on . Let be an open interval, and be the p-value from Algorithm 2 using . We have

3.4 Inference in the full model

In Chapter 2, we focused on inference for the submodel coefficients . In selective inference, the choice of the model is selected via an algorithm e.g. the lasso, and the COS method constructed confidence intervals

One possible criticism of the selective confidence intervals for submodel coefficients is the interpretability of the quantity , since this is the population regression coefficient of variable within the model . The significance of variable depends on the choice of model meaning variable can be significant in model , but not significant in , which makes interpretation difficult.

However, this is not an inherent limitation of the COS method. As we saw in the previous two sections, the COS method is not specific to the submodel coefficients. We simply need to change the space of hypothesis and the selection function to perform inference for other regression coefficients.

In many scientific applications, the quantity of interest is the regression coefficient within the full model . We first discuss the case of . Let us assume that . In ordinary least squares , the parameter of interest is , and a classical confidence interval guarantees

In the case of least squares after variable selection, we only want to make a confidence interval for the , or variables selected by the lasso. This corresponds to inference for a subset , where selects the coordinates in . The interpretation of for is clear; this is the regression coefficient of the least squares coefficient restricted to the set selected by the lasso.

For each coefficient , Equation (2.5.1) provides a valid p-value of the hypothesis ,

| (3.4.1) |

where . By inverting, we obtain a selective confidence interval

| (3.4.2) |

3.4.1 False Discovery Rate

In this section, we show how to combine selective confidence intervals with the Benjamini-Yeuketieli procedure for FDR control. False discovery rate (FDR) is defined as,

where is the number of incorrectly rejected hypotheses and is the total number of rejected hypotheses. We will restrict ourselves to the case of the well-specified linear model, , and with having full rank. In the context of linear regression, there is a sequence of hypotheses and a hypothesis is considered to be incorrectly rejected if is true, yet the variable is selected.

Given p-values, we can now apply the Benjamini-Yekutieli procedure (Benjamini et al.,, 2001) for FDR control. Let be the order statistics, and . Let be

| (3.4.3) |

then reject .

Theorem 3.4.1.

Proof.

Conditioned on the event that variable is in the lasso active set, , then is uniformly distributed among the null variables. Applying the Benjamini-Yekutieli procedure to the p-values guarantees FDR. The Benjamini-Yekutieli procedure allows for arbitrary dependence among the p-values, and only requires that the null p-values are uniformly distributed ∎

3.4.2 Intervals for coefficients in full model when

In this section, we present a method for selective inference for coordinates of the full-model parameter . We will assume the sparse linear model, namely,

where and is -sparse. Since , we cannot use the method in the previous section since . Instead, we will construct a quantity that is extremely close to and show that . We do this by constructing a population version of the debiased estimator.

The debiased estimator presented in Javanmard and Montanari, (2013); van de Geer et al., (2013); Zhang and Zhang, (2014) is

where and is an approximate inverse covariance that is the solution to

| subject to |

Define the population quantity by replacing all occurrences of with :

| (3.4.4) | |||

where is the matrix such that it takes an vector and pads with to make a vector.

By choosing as a row of , COS framework provides a selective test and confidence interval,

The next step is to show that is close to , so by appropriately widening , we cover .

Theorem 3.4.2.

Assume that lasso is consistent in the sense , satisfies , and has the sparse eigenvalue condition , and the empirical sparsity , then

Proof.

Starting from Equation (3.4.4), we have

where we used the lasso consistency assumption,n, and the second to last inequality uses the fact that , so

We now show .

, where ,and .

Plugging this into the expression for ,

| (3.4.5) | ||||

| (3.4.6) |

∎

Lemma 3.4.3 (Assumptions hold under random Gaussian design with additive Gaussian noise).

Assume that the rows of and . Then the estimation consistency property, existence of a good approximation , empirical sparsity , and with probability tending to 1.

Proof.

The estimation consistency property follows from Negahban et al., (2012). The bound is established in Javanmard and Montanari, (2013). The empirical sparsity result is from Belloni et al., (2011, 2013).

The condition on concentration of sparse eigenvalues can be derived using Loh and Wainwright, (2012, Lemma 15, Supplementary Materials). Lemma 15 states if is a zero-mean sub-Gaussian matrix with covariance and subgaussian parameter , then there is a universal constant such that

| (3.4.7) |

With high probability and for all ,

We now use this to show . Let , then by the previous argument and Equation (3.4.7),

with probability at least

For , we have with probability at least,

∎

Corollary 3.4.4.

Corollary 3.4.5.

Let be a selective confidence interval for meaning , then

Proof.

With probability at least , and with probability tending to , . Thus with probability at least , . ∎

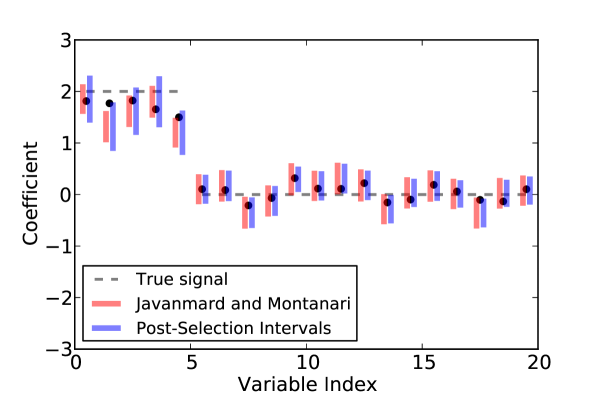

Figure 3.1 shows the results of a simulation study. It makes clear that the intervals of Javanmard and Montanari, (2013) and our selective confidence intervals cover , which is close to . The Javanmard-Montanari intervals are the high-dimensional analog of a z-interval, so they are not selectively valid, unlike the selective intervals in blue.

3.5 Selective Inference for the Knockoff Filter

In this section, we show how to make selectively valid confidence intervals for the knockoff method Foygel Barber and Candes, (2014). Let be the knockoff design matrix, so the knockoff regression is done on . The introduction of the knockoff variables, , allows us to estimate the FDP as the number of knockoff variables selected divided by the number of true variables selected:

| (3.5.1) |

Given a sequence of models be a sequence of nested models . For the lasso, where the correspond to the lasso active set at , the models are not necessarily nested. We define , where is the active set of lasso at . We have an estimate FDP estimate for each model, , where and represent the indices of the real and knockoff variables respectively. This suggests selecting the largest model such that the FDP estimate is less than ,

| (3.5.2) |

To show this controls modified FDR, we need to construct -statistics such that our stopping rule, corresponds to the stopping rule of Foygel Barber and Candes, (2014).

Theorem 3.5.1.

The model selected by the stopping rule in Equation (3.5.2) controls the modified FDR, that is

where .

Theorem 3.5.2.

We construct some W statistics. Define and . Define

By using the estimate in place of equation (3.5.2),

| (3.5.3) | |||

| (3.5.4) |

we can control FDR, instead of modified FDR.

Theorem 3.5.3.

Proof.

Same as the previous theorem. ∎

Let be the final model returned by the knockoff procedure applied to the regression pair using the lasso models at the sequence . Our goal is to do inference for for some . The selection event, the set of ’s that lead us to testing , is . This precise set is difficult to analytically describe, so we resort to Algorithm 2.

We can analytically describe the finer event

where is the active set of lasso at . For any , the knockoff procedure defined by the stopping rule (3.5.2) returns the same set of variables, so . The set is described by the intersection of the union of linear inequalities given in Section 2.7. This allows us to do inference using the results of Theorem 2.4.3.

We next describe a method using the general method of Chapter 3.3. Using the COS method, we first describe the knockoff selection event. The selection event for variable is . The general method instead uses the one-dimensional finer selection event . This set is approximated using Algorithm 2 that computes an approximation to and an approximate p-value.

Since the knockoff method assumes a well-specified linear model, we can use the reference distribution instead of . This is the well-specified linear regression model of Fithian et al., (2014). The selection event is now . A multi-dimensional analog of Algorithm 2 can now be applied, but the search set is now over a dimensional subset.

Part II Learning Mixed Graphical Models

Chapter 4 Learning Mixed Graphical Models

4.1 Introduction

Many authors have considered the problem of learning the edge structure and parameters of sparse undirected graphical models. We will focus on using the regularizer to promote sparsity. This line of work has taken two separate paths: one for learning continuous valued data and one for learning discrete valued data. However, typical data sources contain both continuous and discrete variables: population survey data, genomics data, url-click pairs etc. For genomics data, in addition to the gene expression values, we have attributes attached to each sample such as gender, age, ethniticy etc. In this work, we consider learning mixed models with both continuous Gaussian variables and discrete categorical variables.

For only continuous variables, previous work assumes a multivariate Gaussian (Gaussian graphical) model with mean and inverse covariance . is then estimated via the graphical lasso by minimizing the regularized negative log-likelihood . Several efficient methods for solving this can be found in Friedman et al., 2008a ; Banerjee et al., (2008). Because the graphical lasso problem is computationally challenging, several authors considered methods related to the pseudolikelihood (PL) and nodewise regression (Meinshausen and Bühlmann,, 2006; Friedman et al., 2010a, ; Peng et al.,, 2009). For discrete models, previous work focuses on estimating a pairwise Markov random field of the form , where are pairwise potentials. The maximum likelihood problem is intractable for models with a moderate to large number of variables (high-dimensional) because it requires evaluating the partition function and its derivatives. Again previous work has focused on the pseudolikelihood approach (Guo et al.,, 2010; Schmidt,, 2010; Schmidt et al.,, 2008; Höfling and Tibshirani,, 2009; Jalali et al.,, 2011; Lee et al.,, 2006; Ravikumar et al.,, 2010).

Our main contribution here is to propose a model that connects the discrete and continuous models previously discussed. The conditional distributions of this model are two widely adopted and well understood models: multiclass logistic regression and Gaussian linear regression. In addition, in the case of only discrete variables, our model is a pairwise Markov random field; in the case of only continuous variables, it is a Gaussian graphical model. Our proposed model leads to a natural scheme for structure learning that generalizes the graphical Lasso. Here the parameters occur as singletons, vectors or blocks, which we penalize using group-lasso norms, in a way that respects the symmetry in the model. Since each parameter block is of different size, we also derive a calibrated weighting scheme to penalize each edge fairly. We also discuss a conditional model (conditional random field) that allows the output variables to be mixed, which can be viewed as a multivariate response regression with mixed output variables. Similar ideas have been used to learn the covariance structure in multivariate response regression with continuous output variables Witten and Tibshirani, (2009); Kim et al., (2009); Rothman et al., (2010).

In Section 4.2, we introduce our new mixed graphical model and discuss previous approaches to modeling mixed data. Section 4.3 discusses the pseudolikelihood approach to parameter estimation and connections to generalized linear models. Section 4.4 discusses a natural method to perform structure learning in the mixed model. Section 4.5 presents the calibrated regularization scheme, Section 4.6 discusses the consistency of the estimation procedures, and Section 4.7 discusses two methods for solving the optimization problem. Finally, Section 4.8 discusses a conditional random field extension and Section 4.9 presents empirical results on a census population survey dataset and synthetic experiments.

4.2 Mixed Graphical Model

We propose a pairwise graphical model on continuous and discrete variables. The model is a pairwise Markov random field with density proportional to

| (4.2.1) |

Here denotes the th of continuous variables, and the th of discrete variables. The joint model is parametrized by . The discrete takes on states. The model parameters are continuous-continuous edge potential, continuous node potential, continuous-discrete edge potential, and discrete-discrete edge potential. is a function taking values . Similarly, is a bivariate function taking on values. Later, we will think of as a vector of length and as a matrix of size .

The two most important features of this model are:

-

1.

the conditional distributions are given by Gaussian linear regression and multiclass logistic regressions;

-

2.

the model simplifies to a multivariate Gaussian in the case of only continuous variables and simplifies to the usual discrete pairwise Markov random field in the case of only discrete variables.

The conditional distributions of a graphical model are of critical importance. The absence of an edge corresponds to two variables being conditionally independent. The conditional independence can be read off from the conditional distribution of a variable on all others. For example in the multivariate Gaussian model, is conditionally independent of iff the partial correlation coefficient is . The partial correlation coefficient is also the regression coefficient of in the linear regression of on all other variables. Thus the conditional independence structure is captured by the conditional distributions via the regression coefficient of a variable on all others. Our mixed model has the desirable property that the two type of conditional distributions are simple Gaussian linear regressions and multiclass logistic regressions. This follows from the pairwise property in the joint distribution. In more detail:

-

1.

The conditional distribution of given the rest is multinomial, with probabilities defined by a multiclass logistic regression where the covariates are the other variables and (denoted collectively by in the right-hand side):

(4.2.2) Here we use a simplified notation, which we make explicit in Section 4.3.1. The discrete variables are represented as dummy variables for each state, e.g. , and for continuous variables .

-

2.

The conditional distribution of given the rest is Gaussian, with a mean function defined by a linear regression with predictors and .

(4.2.3) As before, the discrete variables are represented as dummy variables for each state and for continuous variables .

The exact form of the conditional distributions (4.2.2) and (4.2.3) are given in (4.3.5) and (4.3.4) in Section 4.3.1, where the regression parameters are defined in terms of the parameters .

The second important aspect of the mixed model is the two special cases of only continuous and only discrete variables.

-

1.

Continuous variables only. The pairwise mixed model reduces to the familiar multivariate Gaussian parametrized by the symmetric positive-definite inverse covariance matrix and mean ,

-

2.

Discrete variables only. The pairwise mixed model reduces to a pairwise discrete (second-order interaction) Markov random field,

Although these are the most important aspects, we can characterize the joint distribution further. The conditional distribution of the continuous variables given the discrete follow a multivariate Gaussian distribution, . Each of these Gaussian distributions share the same inverse covariance matrix but differ in the mean parameter, since all the parameters are pairwise. By standard multivariate Gaussian calculations,

| (4.2.4) | ||||

| (4.2.5) | ||||

| (4.2.6) |

Thus we see that the continuous variables conditioned on the discrete are multivariate Gaussian with common covariance, but with means that depend on the value of the discrete variables. The means depend additively on the values of the discrete variables since . The marginal has a known form, so for models with few number of discrete variables we can sample efficiently.

4.2.1 Related work on mixed graphical models

Lauritzen, (1996) proposed a type of mixed graphical model, with the property that conditioned on discrete variables, . The homogeneous mixed graphical model enforces common covariance, . Thus our proposed model is a special case of Lauritzen’s mixed model with the following assumptions: common covariance, additive mean assumptions and the marginal factorizes as a pairwise discrete Markov random field. With these three assumptions, the full model simplifies to the mixed pairwise model presented. Although the full model is more general, the number of parameters scales exponentially with the number of discrete variables, and the conditional distributions are not as convenient. For each state of the discrete variables there is a mean and covariance. Consider an example with binary variables and continuous variables; the full model requires estimates of mean vectors and covariance matrices in dimensions. Even if the homogeneous constraint is imposed on Lauritzen’s model, there are still mean vectors for the case of binary discrete variables. The full mixed model is very complex and cannot be easily estimated from data without some additional assumptions. In comparison, the mixed pairwise model has number of parameters and allows for a natural regularization scheme which makes it appropriate for high dimensional data.

An alternative to the regularization approach that we take in this paper, is the limited-order correlation hypothesis testing method Tur and Castelo, (2012). The authors develop a hypothesis test via likelihood ratios for conditional independence. However, they restrict to the case where the discrete variables are marginally independent so the maximum likelihood estimates are well-defined for .

There is a line of work regarding parameter estimation in undirected mixed models that are decomposable: any path between two discrete variables cannot contain only continuous variables. These models allow for fast exact maximum likelihood estimation through node-wise regressions, but are only applicable when the structure is known and (Edwards,, 2000). There is also related work on parameter learning in directed mixed graphical models. Since our primary goal is to learn the graph structure, we forgo exact parameter estimation and use the pseudolikelihood. Similar to the exact maximum likelihood in decomposable models, the pseudolikelihood can be interpreted as node-wise regressions that enforce symmetry.

To our knowledge, this work is the first to consider convex optimization procedures for learning the edge structure in mixed graphical models.

4.3 Parameter Estimation: Maximum Likelihood and Pseudolikelihood

Given samples , we want to find the maximum likelihood estimate of . This can be done by minimizing the negative log-likelihood of the samples:

| (4.3.1) | ||||

| (4.3.2) |

The negative log-likelihood is convex, so standard gradient-descent algorithms can be used for computing the maximum likelihood estimates. The major obstacle here is , which involves a high-dimensional integral. Since the pairwise mixed model includes both the discrete and continuous models as special cases, maximum likelihood estimation is at least as difficult as the two special cases, the first of which is a well-known computationally intractable problem. We defer the discussion of maximum likelihood estimation to the supplementary material.

4.3.1 Pseudolikelihood

The pseudolikelihood method Besag, (1975) is a computationally efficient and consistent estimator formed by products of all the conditional distributions:

| (4.3.3) |

The conditional distributions and take on the familiar form of linear Gaussian and (multiclass) logistic regression, as we pointed out in (4.2.2) and (4.2.3). Here are the details:

-

•

The conditional distribution of a continuous variable is Gaussian with a linear regression model for the mean, and unknown variance.

(4.3.4) -

•

The conditional distribution of a discrete variable with states is a multinomial distribution, as used in (multiclass) logistic regression. Whenever a discrete variable is a predictor, each of its levels contribute an additive effect; continuous variables contribute linear effects.

(4.3.5)

Taking the negative log of both gives us

| (4.3.6) | ||||

| (4.3.7) |

A generic parameter block, , corresponding to an edge appears twice in the pseudolikelihood, once for each of the conditional distributions and .

Proposition 4.3.1.

The negative log pseudolikelihood in (4.3.3) is jointly convex in all the parameters over the region .

We prove Proposition 4.3.1 in the Supplementary Materials.

4.3.2 Separate node-wise regression

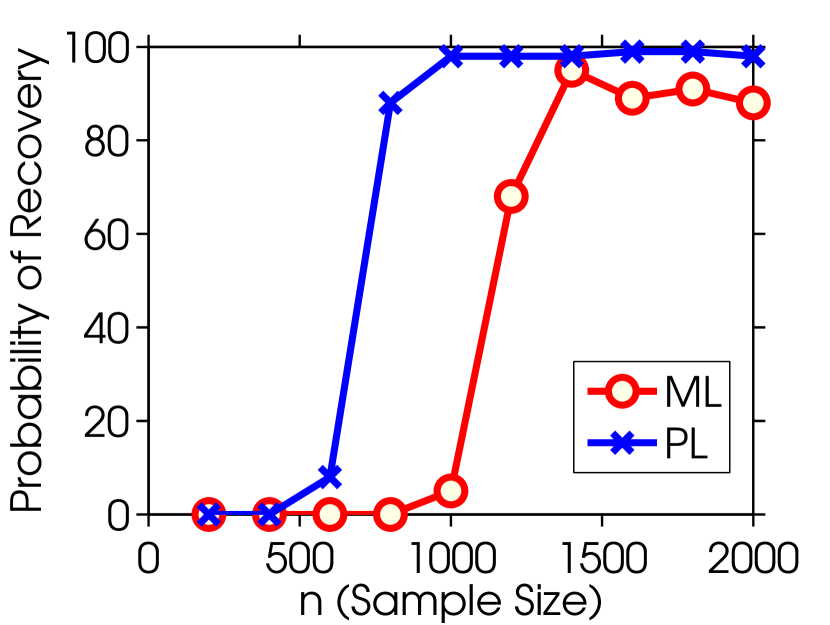

A simple approach to parameter estimation is via separate node-wise regressions; a generalized linear model is used to estimate for each . Separate regressions were used in Meinshausen and Bühlmann, (2006) for the Gaussian graphical model and Ravikumar et al., (2010) for the Ising model. The method can be thought of as an asymmetric form of the pseudolikelihood since the pseudolikelihood enforces that the parameters are shared across the conditionals. Thus the number of parameters estimated in the separate regression is approximately double that of the pseudolikelihood, so we expect that the pseudolikelihood outperforms at low sample sizes and low regularization regimes. The node-wise regression was used as our baseline method since it is straightforward to extend it to the mixed model. As we predicted, the pseudolikelihood or joint procedure outperforms separate regressions; see top left box of Figures 4.6 and 4.7. Liu and Ihler, (2012, 2011) confirm that the separate regressions are outperformed by pseudolikelihood in numerous synthetic settings.

Concurrent work of Yang et al., (2012, 2013) extend the separate node-wise regression model from the special cases of Gaussian and categorical regressions to generalized linear models, where the univariate conditional distribution of each node is specified by a generalized linear model (e.g. Poisson, categorical, Gaussian). By specifying the conditional distributions, Besag, (1974) show that the joint distribution is also specified. Thus another way to justify our mixed model is to define the conditionals of a continuous variable as Gaussian linear regression and the conditionals of a categorical variable as multiple logistic regression and use the results in Besag, (1974) to arrive at the joint distribution in (4.2.1). However, the neighborhood selection algorithm in Yang et al., (2012, 2013) is restricted to models of the form In particular, this procedure cannot be applied to edge selection in our pairwise mixed model in (4.2.1) or the categorical model in (2) with greater than 2 states. Our baseline method of separate regressions is closely related to the neighborhood selection algorithm they proposed; the baseline can be considered as a generalization of Yang et al., (2012, 2013) to allow for more general pairwise interactions with the appropriate regularization to select edges. Unfortunately, the theoretical results in Yang et al., (2012, 2013) do not apply to the baseline nodewise regression method, nor the joint pseudolikelihood.

4.4 Conditional Independence and Penalty Terms

In this section, we show how to incorporate edge selection into the maximum likelihood or pseudolikelihood procedures. In the graphical representation of probability distributions, the absence of an edge corresponds to a conditional independency statement that variables and are conditionally independent given all other variables (Koller and Friedman,, 2009). We would like to maximize the likelihood subject to a penalization on the number of edges since this results in a sparse graphical model. In the pairwise mixed model, there are 3 type of edges

-

1.

is a scalar that corresponds to an edge from to . implies and are conditionally independent given all other variables. This parameter is in two conditional distributions, corresponding to either or is the response variable, and .

-

2.