Parameter shifts for nonautonomous systems in low dimension: Bifurcation- and Rate-induced tipping

Abstract

We discuss the nonlinear phenomena of irreversible tipping for non-autonomous systems where time-varying inputs correspond to a smooth “parameter shift” from one asymptotic value to another. We express tipping in terms of properties of local pullback attractors and present some results on how nontrivial dynamics for non-autonomous systems can be deduced from analysis of the bifurcation diagram for an associated autonomous system where parameters are fixed. In particular, we show that there is a unique local pullback point attractor associated with each linearly stable equilibrium for the past limit. If there is a smooth stable branch of equilibria over the range of values of the parameter shift, the pullback attractor will remain close to (track) this branch for small enough rates, though larger rates may lead to rate-induced tipping. More generally, we show that one can track certain stable paths that go along several stable branches by pseudo-orbits of the system, for small enough rates. For these local pullback point attractors, we define notions of bifurcation-induced and irreversible rate-induced tipping of the non-autonomous system. In one-dimension, we introduce the notion of forward basin stability and use this to give a number of sufficient conditions for the presence or absence of rate-induced tipping. We apply our results to give criteria for irreversible rate-induced tipping in a conceptual climate model example.

1 Introduction

In common language, a tipping point or critical transition is a sudden, large and irreversible change in output of a complex system in response to a small change of input. There have been a range of papers in the applied sciences that use the notion of a tipping point in applications such as climate systems [9, 18, 34] or ecosystems [30, 11]. Further work has attempted to find predictors or early warning signals in terms of changes in noise properties near a tipping point [9, 10, 33, 31, 28], other recent work on tipping includes [22, 23]. Indeed there is a large literature on catastrophe theory (for example [2] and references therein) that addresses related questions in the setting of gradient systems.

There seems to be no universally agreed rigorous mathematical definition of what a tipping point is, other than it is a type of bifurcation point, though this excludes both “noise-induced” [32, 10] and “rate-induced” [30, 34, 25] transitions that have been implicated in this sort of phenomenon. Other work on critical transitions includes for example [17] that examines the interaction of noise and bifurcation-related tipping in the framework of stochastically perturbed fast-slow systems. In an attempt to understand some of these issues, a recent paper [3] classified tipping points into three distinct mechanisms: bifurcation-induced (B-tipping), noise-induced (N-tipping) and rate-induced (R-tipping). As noted in [3], a tipping point in a real non-autonomous system will typically be a mixture of these effects but even in idealized cases it is a challenge to come up with a mathematically rigorous and testable definition of “tipping point”.

The aims of this paper are:

-

(a)

to suggest some definitions for B-tipping and R-tipping appropriate for asymptotically constant “parameter shifts” in terms of pullback attractors for non-autonomous systems.

-

(b)

to show how these definitions allow us to exploit the bifurcation diagram of the associated autonomous (i.e. quasi-static) system to obtain a lot of information about B- and R-tipping of the non-autonomous system associated with a parameter shift.

-

(c)

to give some illustrative examples of properties that allow us to predict or rule out B- and R-tipping in various cases.

Restricting to simple attractors and asymptotically constant “parameter shifts” allows us to obtain a number of rigorous results for a natural class of non-stationary parameter changes that may be encountered in natural sciences and engineering.

The paper is organized as follows: In Section 2 we consider arbitrary dimensional non-autonomous systems and introduce a class of parameter shifts that represent smooth (but not necessarily monotonic) changes between asymptotic values and . For such parameter shifts, we relate stability properties of branches of solutions in the autonomous system with fixed parameters to properties of local pullback point attractors of the non-autonomous system with time-varying parameters. This means that the systems we consider are asymptotically autonomous [20, 27] both in forward and backward time.

After some discussion of (local) pullback attractors, we show in Theorem 2.2 that one can associate a unique pullback point attractor with each linearly stable equilibrium for the past limit system (i.e. the autonomous system with ). Then, we define two types of tracking: -close tracking and end-point tracking. We show in Lemma 2.3 that if there is a stable branch of equilibria with no bifurcation points from this to some stable equilibrium for the future limit system (i.e. the autonomous system with ), then this unique pullback point attractor will -closely track a path of stable equilibria for sufficiently slow rates.

On the other hand, there may be a number of stable paths connecting to - each of these with an image that is a union of stable branches, but possibly passing through bifurcation points. In this case, the pullback point attractor can clearly only track at most one of these paths. Allowing arbitrarily small perturbations along the path, there will be pseudo-orbits that can track any stable path. In Theorem 2.4 we give such result by stating necessary conditions for -close tracking by pseudo-orbits.

Section 3 gives some definitions for B- and R-tipping that correspond to lack of end-point tracking for parameter shifts. In that section we prove several results for one-dimensional systems, including the following:

-

•

Certain bifurcation diagrams or parameter ranges will not permit irreversible R-tipping (Theorem 3.2, case 1.).

-

•

Other bifurcation diagrams will give irreversible R-tipping for certain parameter shifts (Theorem 3.2, cases 2. and 3.).

-

•

There are restrictions on the regions in parameter space where irreversible R-tipping can occur (Section 3.3).

These results use some properties of the paths of attractors. We introduce the notion of forward basin stability where at each point in time the basin of attraction of an attractor for the associated autonomous system contains all earlier attractors on the path. We prove that:

-

•

Forward basin stability guarantees tracking (Theorem 3.2 case 1.).

-

•

Lack of forward basin stability, plus some additional assumptions, gives testable criteria for irreversible R-tipping (Theorem 3.2 cases 2. and 3.).

We also give an example application to a class of global energy-balance climate models in Section 4.

In Section 5 we discuss some of the challenges to extend the rigorous results to higher-dimensional state or parameter spaces, to cases where noise is present and to parameter paths that are more general than parameter shifts.

1.1 The setting: non-autonomous nonlinear systems

Suppose we have a non-autonomous system of the form

| (1) |

where , , , and the “rate” is fixed. For , and starting at we write

to denote the solution cocycle [16], where is the corresponding solution of (1). We also assume is defined for all and , and note that it satisfies a cocycle equation

for any and . Note that, in addition to , and , depends on the shape of the parameter shift , its rate of change , as well as on the function that defines the system. The key difference from the evolution operator of an autonomous system is that a cocycle depends on both the time elapsed and the initial time .

The model (1) can be extended to include stochastic effects, e.g. by considering a stochastic differential equation of the form

| (2) |

where represents an -dimensional Wiener process and represents a noise amplitude. A random dynamical systems approach [1] gives a solution cocycle that depends also on the choice of noise path.

One can understand a lot about the asymptotic behaviour of (1) [or (2)] from the bifurcation/attractor diagram of the associated autonomous system

| (3) |

where is fixed rather than time-dependent. General properties of dynamical systems suggest that if is “small enough” then we can expect, for an appropriate definition of attractor, that trajectories of (1) will closely track a branch of attractors of (3) if the branch continues to be linearly stable over the range of the varying . In this paper we consider only the case of linearly stable equilbrium attractors for (3) where such statements can be made rigorous through use of geometric singular perturbation theory [13] or uniform hyperbolicity [5]. The control theory literature discusses related questions; see for example [14] that allows to depend on state as well. However, close tracking of a continuous path that traverses several stable branches of (1) cannot always be guaranteed, even if is small enough.

If the variation of along a branch of attractors brings the system to a bifurcation point where no stable branches are nearby, we have the ingredients of a bifurcation-induced or B-tipping point; no matter how slowly we change the parameter, there will be a sudden and irreversible change in the state of the system on, or near where the parameter passed through a dynamic bifurcation [4, 8, 23].

However, B-tipping is not the only way to get a sudden irreversible change. Even if there is a branch of attractors available for the system to track, a rate-induced tipping or R-tipping [3, 34] can occur; if there is a critical value of the rate beyond which the system cannot track the branch of attractors then it may suddenly move to a different state. This happens even though there is no loss of stability in the autonomous system. Nonetheless, the bifurcation diagram of the associated autonomous system may give us a lot of information and indeed constraints on when R-tipping may or may not happen. Nontrivial behaviour that can appear as a result has been recently studied in [34, 21, 25] in terms of canard trajectories.

2 Tracking of attractors for non-autonomous systems

We consider the behaviour of (1) for one dimensional () “parameter shifts”, i.e. choices of that are -smooth (but not necessarily monotonic), bounded and satisfying

that limit to the ends of the interval, as , where the limiting behaviour is asymptotically constant (i.e. as ). More precisely,

Assumption 2.1

We assume

where we consider the subset of :

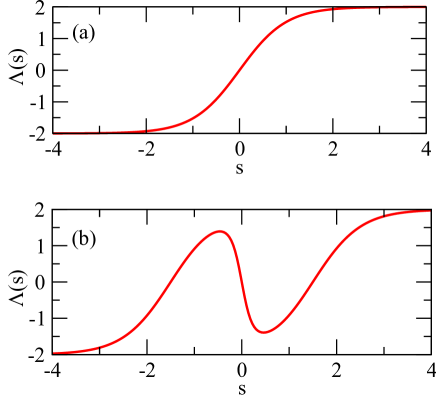

Figure 1 gives two examples of parameter shifts that we consider, though clearly a parameter shift may have an arbitrary number of maxima and minima.

The set of equilibria for the bifurcation diagram of (3) is

Writing to denote the linearization of with respect to , we identify the subsets of that are linearly stable, unstable and bifurcation equilibria:

where denotes the spectrum of the matrix . Note that, in addition to generic bifurcations, may include degenerate bifurcation points and even “bifurcations” that do not involve any topological change in the phase portrait, e.g. at .

We say is regular if (i) the set of bifurcation points are isolated ( has no accumulation point) and (ii) the only asymptotically stable recurrent sets (attractors) are equilibria. The first property of a regular is implied by the Kupka-Smale theorem for flows [15, Thm 7.2.13] under generic assumptions, though our assumption is less restrictive and allows the possibility of high codimension bifurcations in . The second property of a regular holds for one-dimensional systems, but does not hold in general for higher dimensional systems.

Assumption 2.2

We assume is regular. Furthermore, for ease of exposition, we assume w.l.o.g. that throughout and that there are no bifurcations at .

Henceforth, we will denote the closure of by and define:

Definition 2.1

We say a -smooth curve in is a branch if it does not intersect with except possibly at end points. We say it is a stable branch if it is contained in .

Definition 2.2

Given a parameter shift , we say a continuous curve that limits to some as and whose image lies within is a path. We say it is a stable path if its image lies within

Note that branches and paths are defined in terms of solutions to the autonomous system (3) and, to some extent, the shape of the parameter shift , but are independent of the rate . A path can traverse several branches that meet at isolated points in , where the path may be nonsmooth. It may also traverse the same branch several times. As illustrated in Figure 1, some can be monotonic functions of and visit each point on a branch at just one value of , others may have internal minima or maxima and visit the same point on a branch at more than one value of . We mention a minor result that we use in a later theorem.

Lemma 2.1

If is regular then a stable path traverses a finite number of smooth stable branches.

Proof: Regularity of in particular means that there are no

accumulations of bifurcation points . Suppose that a

stable path traverses an infinite number of smooth

stable branches and hence passes through an infinite number of bifurcation

points. As the path is continuous and bifurcation points are isolated

on the path, there must be an accumulation as or

. However, as has well-defined end-points in these

limits , one of

is an accumulation point, which gives a contradiction. QED

2.1 Local pullback attractors for the non-autonomous system

We are interested in the influence of parameter shifts and rates on pullback attractors of the non-autonomous system (1). Note that the limit is singular in the sense that does not exhibit any change in parameter values with time. In terms of the cocycle , the following definition is a local version of the pullback point attractor discussed in [16, Defn 3.48(ii)] that we have adapted to the context of parameter shifts:

Definition 2.3

We say a solution of (1) is a (local) pullback attractor if there is a bounded open set and a time such that (i) for all , and (ii) for any and we have

| (4) |

In contrast to [16, Defn 3.48(ii)] we do not require that the pullback attractor attracts a non-autonomous open set . For the asymptotically autonomous case we consider here, we can relate each attractor for the past limit autonomous system to a pullback attactor for the non-autonomous system via the following theorem, whose proof is given in Appendix A.111We are indebted to an anonymous referee for suggesting this method of proof.

Theorem 2.2

Theorem 2.2 shows that any trajectory that limits to a linearly stable equilibrium in the past is a pullback point attractor, and these pullback attractors are in one-to-one correspondence with choices of such that . Note that this result is similar to [16, Thm 3.54(i)], except that their assumption that is invariant means that . Any small enough open neighbourhood of can be used to define the corresponding pullback attractor of (1), in particular by choosing small enough , the unique pullback attractor with past limit can be expressed as

| (5) |

for a given parameter shift , rate and initial state , where denotes a dimensional ball of radius . We do not use (5) in the following, but note that it may be useful as a basis for numerical approximation of the pullback attractor that limits to a given for .

2.2 Tracking of stable branches by pullback attractors

We define two notions of tracking of branches of stable equilibria of (3) by attractors of (1). The strongest notion of tracking we consider is -close tracking:

Definition 2.4

For a given , we say a (piecewise) solution of (1) for some and -close tracks the stable path if

| (6) |

for all .

The following is another, somewhat weaker notion of tracking, which we call end-point tracking:

Definition 2.5

Consider a stable path from to . We say a solution of (1) end-point tracks this path if it satisfies

Note that end-point tracking implies that for all there is a such that (6) holds for all . The following result gives a sufficient condition for close- and end-point tracking of a stable branch.

Lemma 2.3

Suppose that and is a stable path that traverses a stable branch from to bounded away from . Then for any there is a such that for all the pullback attractor satisfies -close tracking of . The pullback attractor also end-point tracks the stable path for all sufficiently small .

Proof: Let be the stable path whose image is contained within the stable branch bounded away from and we write . Now consider the augmented system on given by

| (7) |

For this has a compact invariant critical manifold

that is foliated with (neutrally stable) equilibria. Note that the section of with constant limits to for . As the branch is bounded away from any bifurcation points, there is a such that the normal Jacobian satisfies for all . In consequence, the one-dimensional invariant manifold is uniformly normally hyperbolic. One can check that is a smooth Riemannian manifold of bounded geometry. Applying222We use and in the notation of [12] and note that because we restrict to there is an empty unstable bundle. [12, Theorem 3.1], there is an such that for any the system (7) has a unique normally hyperbolic invariant manifold , where the distance from to does not exceed .

Moreover, this manifold contains a single trajectory parametrized by . In summary, for any and for all there is a trajectory of (7) with for all .

By Theorem 2.2 there is a neighbourhood containing such that only one trajectory satisfies as . Fixing and such that for all we can see that the trajectory obtained is the pullback attractor

In particular as .

Now consider the behaviour of in the limit . If we set then

where . Noting that

| (8) |

where the error term is uniform in . For any define

and continuity of implies that as . For any ,

for all

and . The fact that means there is a such that

for . Hence

for all . Finally, note

that from the linear stability of , there

is an such that if then

as . It follows that

as and so the

solution end-point tracks the branch. QED

2.3 Tracking of stable paths by pseudo-orbits

One might wish to characterize a wider class of stable paths that can potentially be tracked by including stable paths that pass through bifurcation points where stable branches meet. To do this we have to widen our notion of tracking to consider tracking by pseudo-orbits.

Let us consider the possible stable paths that may be accessible for a given .

Definition 2.6

Given a parameter shift , we say points and on are -connected if they lie on the same stable path

Note that and are -connected if and only if they are -connected for any , so the definition does not depend on . For given and that are -connected, it is not necessarily the case that there will be tracking by orbits of the non-autonomous system for some . In particular, there is no guarantee that the pullback attractor from Theorem 2.2 remains close to , that

or even that is an attractor for the future limit system. Indeed the example in Section 2.4 shows that such a trajectory may not exist: achieving the appropriate branch switching may not be possible even on varying and .

As discussed later in Section 2.4 there may be several stable paths from that end at different . We show that there will be tracking of any stable path by a pseudo-orbit, namely an orbit with occasional arbitrarily small adjustments. Recall the following definition of a pseudo-orbit (N.B. there are several possible definitions of pseudo-orbit for flows; e.g. see [24]). We say is an -pseudo-orbit [29] of (1) on if there is a finite series for , with and , such that for all ,

-

•

-

•

is a trajectory of (1) on the time-interval

-

•

.

We say defined for in some (possibly infinite) interval is an -pseudo-orbit if it is an -pseudo-orbit on all finite sub-intervals. For convenience we refer to an -pseudo-orbit as an -pseudo-orbit.

Theorem 2.4

Suppose that and are -connected by a stable path for some . Then for any there is a such that for all there is an -pseudo-orbit of (1) with

| (9) |

for all .

This Theorem (proved below) suggests that if we consider the system perturbed by noise of arbitrarily low amplitude, for any noise amplitude there will be an initial condition, a rate and a realization of additive noise such that the perturbed system has a trajectory that end-point tracks the given stable path. Under additional assumptions, we believe that stable paths will be -close tracked with positive probability. Before proving Theorem 2.4, we give a special case whose proof uses similar argument to that of Lemma 2.3.

Lemma 2.5

Suppose that and traverses a single stable branch that is bounded away from in the interval (we include the possibility or ). Then for any there is a such that for all there is a trajectory that satisfies -close tracking of this branch in the sense of (9) for .

Proof: This is similar to that of Lemma 2.3 except that instead of

we consider and is not necessarily a pullback attractor

for the system, or even unique. Consider the case of and finite and note

that if the closed set

does not intersect the closed set then they must be isolated by

a neighbourhood. Hence there is

a such that for all . By considering an

augmented system as in the proof of Lemma 2.3 we can apply Fenichel’s theorem [13]

to conclude that for small enough

there is a trajectory that -tracks the branch for .

QED

Proof: (of Theorem 2.4) Let be the stable path that starts at and ends at . Because is regular, we can assume that there are at most finitely many bifurcation points on the path . However, it is possible that may remain at bifurcation points for a set of that may include intervals: there is a finite set of points with

such that is constant and when for some . Note that the generic (transversal) case is but we allow a more general case where the parameter can “linger” at bifurcation points for a time.

We proceed to show that for any there is an such that it is possible to construct an -pseudo-orbit that shadows the stable path for all . All discontinuities of the constructed pseudo-orbit will be near . We show this in detail for the finite interval : similar proofs hold for the semi-infinite intervals and by using uniformity of linear stability near the endpoints . Let us define and .

Pick any . Continuity of means we can find a such that

| (10) |

for all .

Pick any with ; Lemma 2.5 implies that there is a rate (depending on and ) and a trajectory such that for all there is a trajectory of (1) satisfying

| (11) |

on the interval .

The fact that is a bifurcation point () and means that, by Taylor expansion, for any there are such that

whenever and . Similarly, means there is a such that

for all , where . Choosing we have

| (12) |

for all points in

| (13) |

Considering a forward trajectory of (1) we have

| (14) |

for , if between and . Hence by choosing such that

(which is possible as long as ) we can ensure that:

-

•

There is containment .

- •

Because of (15), when we can find a finite number of trajectory segments, each of time length , starting at , such that for all .

Hence there is a choice of and such that, if then there is a pseudo-orbit with the desired property on the interval . More precisely, for any we can find an increasing sequence of and a piecewise solution with , such that . Combining the estimates (10,11) and (15) we have for this solution

| (16) | |||||

for all except where for some .

2.4 An example: dependence on -connectedness

Let us consider the system

| (17) |

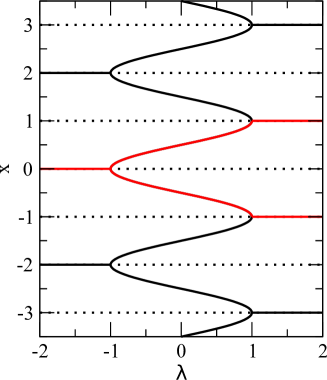

for , and this is a simple example where we can explore which stable paths can be adiabatically tracked for a given . If we note that and then the bifurcation diagram is as in Figure 3. Although there are branches that continue through for , there is an exchange of stability by a combination of pitchfork bifurcations. For this system we see that the set of stable branches is connected into one component and so for any there is a stable path from to . However, if is large then the path will require with a large number of internal maxima and minima.

Now consider any trajectory of (17). As the lines of equilibria at integer values of remain flow-invariant subspaces for any choice of and , it follows that

where is the smallest integer . This means that the pullback attractor from cannot track a stable path from to where , and in Figure 3. Indeed, it is easy to see that the pullback attractor in this case is simply the constant and in all cases this is in fact a repellor for the future limit system.

However, Theorem 2.4 implies that a pseudo-orbit can track such a path - it allows the possibility of arbitrarily small adjustments along the way. Starting at and allowing arbitrarily small adjustments, there are two possible finishing points for a such as Figure 1(a) and four possible finishing points for a such as Figure 1(b).

2.5 Bifurcation-equivalent systems

Since the discussion so far only depends on branches of equilibria, their stabilities and bifurcations, many of the properties carry across to systems that have the same bifurcation diagram. Suppose that

| (18) |

where and is a strictly positive scalar function that is bounded below. The associated autonomous system

| (19) |

will have the same trajectories in the phase portrait, different magnitude but the same sign eigenvalues, and hence the same bifurcation diagram as (3). For the same reason systems (1) and (18) will have the same -connected points and . They also have orbits that are equivalent in the following (rather weak) sense:

Proof: To show , define a (state-dependent) time rescalling through a coupled system

with and . Using the assumption on one can verify that together with a suitable monotonically increasing function solve the coupled system above:

Hence, also solves (18) with replacing .

To show , for a given define a state-dependent time rescaling through the integral

that satisfies and is a monotonically increasing (hence invertible) function of whose first derivative is bounded from below. We can now verify that solves (1) with replacing . On the one hand

On the other hand, the assumption on gives

Since , we have that

QED

In particular, this means that a tracking trajectory in an equivalent system implies that there is a tracking trajectory in the first system for a different . Note that as the transformation from to does depend on the trajectory chosen, one needs to be cautious about applying Theorem 2.6. We also note that varying can lead to different parameter shifts . Nonetheless, it does allow extension of some results to more general bifurcation equivalent systems.

3 Bifurcation- and rate-induced tipping

We now propose some definitions and results on bifurcation (B-) and rate (R-) induced tipping in the sense of [3]. Recall from [3] that B-tipping is associated with a bifurcation point of the corresponding autonomous system, while R-tipping appears only for fast enough variation of parameters and is associated with loss of tracking of a stable branch.

Definition 3.1

Suppose that and fix . Suppose for all small enough we have

If and are not -connected then we say there is B-tipping from for this .

Definition 3.1 requires that the system reaches a point on a stable branch that is not accessible by following a stable path permitted by the chosen . The following result shows that a bifurcation must indeed be responsible for B-tipping.

Corollary 3.1

Suppose there is B-tipping for some starting at . Then there is at least one bifurcation point with on the stable branch starting at .

Proof: If there is no such bifurcation point, then there must be a

stable branch spanning from to .

For any parameter shift ,

Lemma 2.3 implies that we track this branch for all

small enough - a contradiction to the assumption that there is

B-tipping. QED

We define irreversible R-tipping as follows:

Definition 3.2

Suppose that and fix . We say there is irreversible R-tipping from on if there is a and an that is -connected to such that the system end-point tracks a stable path from to for but not for , i.e.

Although Theorem 2.4 guarantees -close tracking by pseudo-orbits for small enough , an increase in may lead to irreversible R-tipping as above, but then further increase of may lead back to tracking again! Indeed the values of that give tracking may be interspersed by several windows of rates that give tipping; see the example in Section 3.1 and Figure 4.

In addition to irreversible R-tipping defined above, there can be transient R-tipping. Recall that our definition of end-point tracking makes no assumption that is small, except in the limits . This means that the system may end-point track the stable path for all , but depart from the path temporarily when to visit a different state/path at intermediate times [34]. Such transient R-tipping is not discussed here.

3.1 An example with rate-induced tipping for intermediate rates

Consider governed by

| (20) |

where and

| (21) |

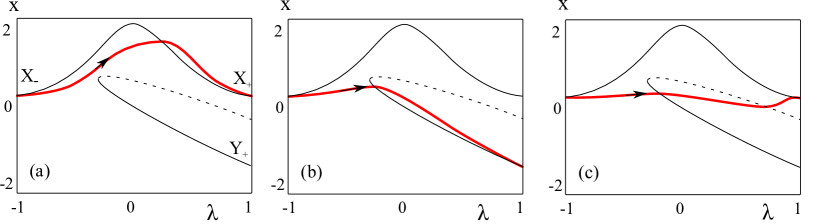

for and constants. This example has a particular bifurcation structure as illustrated in Figure 4 if we choose

Observe that this is a structurally stable bifurcation diagram and so qualitatively robust to small changes in any parameter, and indeed to any small changes in . For and we take solutions of

| (22) |

Figure 4 illustrates the appearance of critical rates such that R-tipping only occurs for a finite range .

3.2 Identifying regions of R-tipping in one-dimensional systems

In this section we assume one state space dimension () throughout and show that geometric properties of the bifurcation diagram can be used to infer where R-tipping is or is not possible.

Consider a stable path for some . For a fixed , let be the basin of attraction of the stable equilibrium for the autonomous system (3) with parameter , i.e.

where is the trajectory of the autonomous system (3) with initial condition . We define a notion of forward basin stability in terms of -dependent basin of attraction for the attractors of the associated autonomous system on a given stable path.

Definition 3.3

We say a stable path for some is forward basin-stable if for every the basin of attraction of the stable equilibrium on the path contains the closure of the set of all earlier positions of this equilibrium along the path:

Note that forward basin stability: (i) is defined in terms of solutions to the autonomous system (3) and the shape of the parameter shift , but is independent of the rate , and (ii) is a property of a stable path rather than a stable branch traversed by the path. We remark that this is a somewhat different notion to basin stability as defined in [19]: this is a quantity that characterises the relative volume of a basin of attraction and is not a property of a branch of attractors.

In the following, we use the notion of forward basin stability to give sufficient conditions for irreversible R-tipping in one dimension to be absent (case 1) or present (cases 2, 3).

Theorem 3.2

Suppose that and in are -connected by the stable path for some :

-

1.

If is forward basin-stable then end-point tracks for all . Hence in such a case there can be no irreversible R-tipping from on .

-

2.

If the stable path traverses a single stable branch , there is another stable branch333NB this may be defined only on where . with and there are such that

then is not forward basin-stable and there is a parameter shift such that there is irreversible R-tipping from on this .

-

3.

If the stable path traverses a single stable branch, and there is a with and not -connected such that

then is not forward basin-stable and there is irreversible R-tipping from for this .

Proof: We define

and note that from these definitions, and for all .

For case 1, let us fix any and suppose that is forward basin-stable. This implies that and also that for all . For any and we define and claim that

satisfies as . To see this, note that if for any then either

In either case and so is monotonic decreasing with . If it converges to some then we can infer there is another equilibrium (not equal to ) within for the future limit system: this is a contradiction. Hence for any trajectory such that as we have

Since this holds for all and we have as . By Theorem 2.2 this trajectory is the pullback attractor and hence the result.

For case 2 the existence of such implies that and hence is not forward basin stable. We construct a reparametrization

using a smooth monotonic increasing that increases rapidly from to but increases slowly otherwise. More precisely, for any and we choose a smooth monotonic function such that

Using the assumption that the stable path traverses a single stable branch, we apply Lemma 2.3 to show that for all small enough rates we have

Note that by construction,

for any . Indeed, by picking large and small, we can ensure that

is as small as desired. In particular this means that is in the basin of . Hence will track for if is small enough (recall that ). Applying Lemma 2.5 again for the interval means that reducing , if necessary, will give a pullback attractor with as .

For case 3 a similar argument to case 2 implies that the path is not forward basin stable. Given any there will be a such that if

then

By continuity, there is an such that for all and . Now pick any

so that for the pullback attractor we have and

Therefore

and so as : there is R-tipping on this path for some .

QED

3.3 Isolation of B-tipping and R-tipping in one-dimensional systems

An interesting consequence of Theorem 3.2 is that rate-induced tipping will appear neither for too small a range of parameters, nor on a segment of a branch that lies too close to a saddle-node bifurcation.

Lemma 3.3

If then there is a such that for there is a stable branch on , and no irreversible R-tipping is possible from for any .

Proof: As is a linearly stable equilibrium, for all small enough there will be a such that if then

Fixing such a , continuity of means that choosing a (possibly smaller) we can ensure

Hence any path on this branch from to will be forward basin stable: by Theorem 3.2 case 1, R-tipping is not possible on such a path.

QED

In fact, a stronger statement may be made near a saddle-node bifurcation. Suppose there is a saddle-node bifurcation at where the branches exist for . The unstable and stable branches from the saddle-node bifurcation will be quadratically tangent to the line in the bifurcation diagram, meaning they will move monotonically in opposite senses near to the bifurcation. More precisely, suppose that there is a branch of stable equilibria and a branch of unstable equilibria . Suppose that a is the nearest branch of unstable equilibria above . Then there is a such that

for all . The branch is therefore forward basin-stable and by Theorem 3.2 case 1 there will be no R-tipping for any parameter shifts within this range of parameters: this is a stronger conclusion than Lemma 3.3.

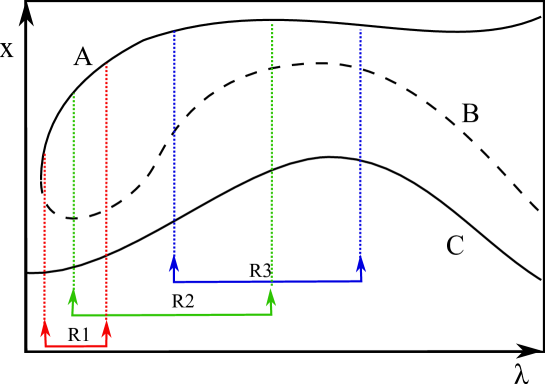

As an example see Figure 5; this shows a bifurcation diagram along with three examples of choices of . Two of these ranges (R1,R3) will not show R-tipping, while R2 can show R-tipping by Theorem 3.2 case 3.

4 Example: R-tipping in an energy balance climate model

We briefly indicate how we can characterise paths where there will be R-tipping for the Fraedrich energy-balance model of global mean temperature: see [3] for more details and an example of a path that gives tipping. We show how this can be deduced from application of Theorem 3.2. This model for the evolution of global mean surface temperature is

| (23) |

where the parameters can be expressed in terms of physical quantities such as the solar output, the planetary albedo etc; note that and from physical arguments. We set and note that (23) transforms to

| (24) |

which (if we are bounded away from ) is bifurcation-equivalent to

| (25) |

in the sense of Theorem 2.6: though we do not need to apply this theorem for the results below. Suppose now that and vary smoothly according to some parameter that undergoes a shift (without loss of generality) from to . If then there are two branches of equilibria for (25) – and hence also for (23); a stable branch

and an unstable branch

These meet at saddle nodes whenever and there are no equilibria for . The next statement summarizes a number of results that can be proved about this system for parameter shifts of from to .

Theorem 4.1

Consider the system (23) with and depending smoothly on a single real parameter . Suppose that varies with time by a parameter shift .

-

(a)

If for all then there is a stable branch from to and there is no B-tipping from for any .

-

(b)

Suppose that (a) is satisfied and for all . Then there is no irreversible R-tipping from on any .

-

(c)

Suppose that (a) is satisfied and there are such that . Then there is a for which there is irreversible R-tipping from .

-

(d)

Suppose that (a) is satisfied and let , be the end-points of the unstable branch. If then there is a for which we have irreversible R-tipping from .

-

(e)

If and there is such that then there is B-tipping for any starting at .

Proof: Conclusion (a) follows using Lemma 2.5.

Conclusion (b,c,d) follow as applications of Theorem 3.2 cases 1, 2 and 3 respectively. Conclusion (e) follows on verifying Definition 3.1 of B-tipping. QED

Some consequences of this are that (i) if we fix and vary just , we cannot find an R-tipping in this system: this is because in that case

for all so that we can apply Theorem 4.1(b), (ii) similarly we cannot get R-tipping if we fix and vary just . For (i) and (ii), note that it is still possible to get B-tipping in either case. (iii) Theorem 4.1(d) can be used to show that the parameter shift considered in [3] leads to R-tipping.

5 Discussion

In this paper we introduce a formalism that uses pullback attractors to describe the phenomena of B-tipping and irreversible R-tipping [3] in a class of non-autonomous systems. We restrict to a specific type of system, namely those undergoing what we call “parameter shifts” between asymptotically autonomous systems and focus on equilibrium attractors. In this setting we show in Theorem 2.2 that there is a unique pullback point attractor associated with each stable equilibrium for the past time asymptotic system, and we can give definitions of what it means to “-close track”, to “end-point track” and to undergo some type of “tipping” depending on the details of the system. For one-dimensional systems, we obtain a number of results (in particular Theorem 3.2) that give necessary conditions for irreversible R-tipping to be present or absent in a system.

We consider smooth parameter shifts that remain within the end-points of their range and that go (possibly non-monotonically) from to for some . It should be possible to relax several of these assumptions and give similar results, as long as the parameters have well-defined limits for , though this may lead to less intuitive statements.

We do not consider noise-induced tipping: for this, one needs to go beyond the purely topological/geometric setup here, and to discuss probabilities of tipping. We note that Theorem 2.4 gives criteria for tracking of stable branches by pseudo-orbits as well as useful conditions for the tracking of branches in the presence of low amplitude noise. Indeed, similar results can be made about the tracking of unstable branches by pseudo-orbits though presumably if these pseudo-orbits are the result of an occasional random process, there will not be tracking of unstable branches for long periods of time with any high probability. We also do not consider interaction of noise and rate-induced tipping - but see for example [28].

Our results rely on an assumption of simple dynamics in state space - in particular that the limiting behaviour of the asymptotically autonomous systems are just equilibria, and (for the later results) that the state space is one-dimensional and so well-ordered. Although many of the phenomena discussed will be present in higher dimensional systems (for example [30]), such systems will clearly display additional types of nonlinear behaviour. This includes more complex branches of attractors, periodic orbits, homoclinic and heteroclinic connections, chaotic dynamics and complex topological structures of attractor branches. Nonetheless, notions such as forward basin-stability should generalize to give similar results for tipping from equilibria in higher dimensions using parameter shifts of the type considered here.

As considered in [3], one particular type of tipping not present in one-dimensional systems may already appear in two dimensional state space where the system has a single globally attracting invariant set for all values of the parameters. Such a case of transient R-tipping, associated with a novel type of excitability threshold in [34, 21, 25], cannot be explained simply in terms of the branches of the bifurcation diagram even if we include all recurrent invariant sets. Instead it is due to the richer geometry of attraction that can appear in two or more dimensional systems.

We end with a brief discussion of an alternative setting that can be used in cases where the parameter shift behaviour is determined by an autonomous ODE, for example for where and for all . In this case we can consider an extended system of the form

As discussed in [26], the presence of irreversible R-tipping can be understood in terms of (heteroclinic) connections between saddle equilibria in this extended system and indeed this can be used as a tool to numerically locate rates corresponding to R-tipping. By contrast, in this paper we make no such assumption and consider the behaviour of the non-autonomous system (1).

Acknowledgements

We thank Ulrike Feudel, Martin Rasmussen and Jan Sieber for interesting conversations and comments in relation to this work and Kate Meyer and Hassan Alkhayuon for comments that helped with the revision. We greatly thank an anonymous referee for several comments and suggesting the detailed proof for Theorem 2.2 that we have included in Appendix A. We also thank Achim Ilchmann for very helpful discussions in relation to this proof. The work of PA was partially supported by EPSRC via grant EP/M008495/1 “Research on Changes of Variability and Environmental Risk” and partially by the European Union’s Horizon 2020 research and innovation programme “CRITICS” under Grant Agreement number No. 643073.

References

- [1] L. Arnold. Random Dynamical Systems. Springer Monographs in Mathematics, Springer Verlag, Berlin, 1998.

- [2] V. I. Arnold, V. S. Afrajmovich, Yu. S. Ilyashenko, and L. P. Shilnikov. Bifurcation theory and catastrophe theory. Springer-Verlag, Berlin, 1999.

- [3] P. Ashwin, S. Wieczorek, R. Vitolo, and P. Cox, Tipping points in open systems: bifurcation, noise-induced and rate-dependent examples in the climate system, Phil Trans Roy Soc A 370:1166–1184 (2012). Correction co-authored with C. Perryman (Née Hobbs) 371:20130098 (2013).

- [4] S. M. Baer, T. Erneux, and J. Rinzel. The slow passage through a Hopf bifurcation: Delay, memory effects and resonance. SIAM J. Appl. Math., 49:55–71, 1989.

- [5] Z. Bishnani and R.M. MacKay. Safety criteria for aperiodically forced systems. Dynamical Systems 18:107–129, 2003.

- [6] W.A. Coppel. Stability and asymptotic behaviour of differential equations, Boston Heath. 1965.

- [7] W.A. Coppel. Dichotomies in stability theory, volume 629 of Lecture Notes in Mathematics. Springer, 1978.

- [8] E. Benoit. Dynamic bifurcations, volume 1498 of Lecture Notes in Mathematics. Springer, 1991.

- [9] V. Dakos, M. Scheffer, E. H. van Nes, V. Brovkin, V. Petoukhov, and H. Held. Slowing down as an early warning signal for abrupt climate change. Proc. Natl Acad. Sci., 105:14308֭-14312, 2008.

- [10] P. D. Ditlevsen and S. Johnsen. Tipping points: early warning and wishful thinking. Geophys. Res. Letters, 37:L19703, 2010.

- [11] J. M. Drake and B. D. Griffen. Early warning signals of extinction in deteriorating environments. Nature, 467:456–459, 2010.

- [12] J. Eldering. Normally hyperbolic invariant manifolds - the noncompact case Springer Atlantis Series in Dynamical Systems vol 2, 2013.

- [13] N. Fenichel. Geometric singular perturbation theory for ordinary differential equations. J. Differential Equations, 31:53–98, 1979.

- [14] S. Hinrichsen and A.J. Pritchard. Mathematical systems theory I: modelling, state space analysis, stability and robustness, vol. 48 (corrected 3rd edn.). Berlin, Germany: Springer (2011).

- [15] A. Katok, and B. Hasselblatt. Introduction to the Modern Theory of Dynamical Systems Cambridge University Press, Cambridge (1995)

- [16] P. Kloeden and M. Rasmussen. Nonautonomous Dynamical Systems. AMS Mathematical Surveys and Monographs, 176, 2011.

- [17] C. Kuehn. A mathematical framework for critical transitions: bifurcations, fast-slow systems and stochastic dynamics. Physica D, 240:1020–1035, 2011.

- [18] T.M. Lenton, H. Held, E. Kriegler, J.W. Hall, W. Lucht, S. Rahmstorf, and H.J. Schellenhuber. Tipping elements in the earth’s climate system. Proc. Natl Acad. Sci., 105:1786֭-1793, 2008.

- [19] P.J. Menck, J. Heitzig, N. Marwan and J. Kurths. How basin stability complements the linear-stability paradigm. Nature Physics, 9:89–92, 2013.

- [20] K. Mischaikow, H. Smith and H.R. Thieme. Asymptotically autonomous semiflows: chain recurrence and lyapunov functions. Trans. AMS, 347:1669-1685, 1995.

- [21] J. Mitry, M. McCarthy, N. Kopell, and M. Wechselberger. Excitable neurons, firing threshold manifolds and canards. J. Math. Neurosci. 3:12 (doi:10.1186/2190-8567-3-12), 2013.

- [22] N.R. Nene and A. Zaikin. Interplay between Path and Speed in Decision Making by High-Dimensional Stochastic Gene Regulatory Networks. PLoS one 7:e40085, 2012.

- [23] T. Nishikawa and E. Ott. Controlling systems that drift through a tipping point. Chaos 24:033107, 2014.

- [24] K.J. Palmer. Shadowing in dynamical systems. Theory and applications. Kluwer, Dordrecht (2000)

- [25] C. Perryman and S. Wieczorek. Adapting to a changing environment: non-obvious thresholds in multi-scale systems. Proceedings of the Royal Society A 470:20140226, 2014.

- [26] C. Perryman. How Fast is Too Fast? Rate-induced Bifurcations in Multiple Time-scale Systems. PhD thesis, University of Exeter (2015).

- [27] M. Rasmussen. Bifurcations of asymptotically autonomous differential equations. Set-Valued Anal. 16:821–849, 2008.

- [28] P. Ritchie and J. Sieber. Early-warning indicators for rate-induced tipping. Preprint arXiv:1509.01696v3 (2015).

- [29] M. Shub. Global stability of dynamical systems. Springer-Verlag, New York, Berlin, Heidelberg (1987)

- [30] M. Scheffer, E.H. van Nes, M. Holmgren and T. Hughes. Pulse-driven loss of top-down control: the critical-rate hypothesis. Ecosystems, 11: 226-–237, 2008.

- [31] J. Shi and T. Li. Towards a critical transition theory under different temporal scales and noise strengths. Physical Review E, 93: 032137, 2016.

- [32] A. Sutera. On stochastic perturbation and long-term climate behaviour. Quarterly Journal of the Royal Meteorological Society, 107:137–151, 1981.

- [33] J.M.T. Thompson and J. Sieber. Predicting climate tipping as a noisy bifurcation: a review. International Journal of Bifurcation and Chaos, 76:27–46, 2011.

- [34] S. Wieczorek, P. Ashwin, C. M. Luke, and P. M. Cox. Excitability in ramped systems: the compost-bomb instability. Proceedings of the Royal Society A, 467:1243–1269, 2010.

Appendix A: Proof of Theorem 2.2

We thank an anonymous referee for suggesting the detailed proof that we reproduce below.

Proof: (of Theorem 2.2) Firstly, we fix and claim there is a unique solution of (1) with as . To see this, let us define

and note, because and , that as and as . Linear stability means that the eigenvalues of

have negative real parts and so there are and such that for (in fact, one can choose any such that : see for example [14, Lemma 3.3.19]).

Now set and note that

| (26) |

where

so that

Hence, for all we have

and we seek a solution of (26) such that for for any . We choose and such that

For any continuous defined for and we define by

and note that the required solution of (26) satisfies . Note that

| (27) | |||||

and hence .

If there are two such functions one can verify that

and so the integral operator is a contraction on the set of continuous with for for the norm . Hence there is a unique fixed point such that for and this is a solution of (26). Note from (27) with that for

Hence when we have for . Hence as . If we consider , the -ball around , and for any define

| (28) |

Then is the unique trajectory for all and we have on and as . Note that (28) is well defined for all and is invariant under (1) - hence it defines a unique trajectory for all .

Moreover, there is a such that for any trajectory with for we have

for .

To see this, note that for , and hence

It follows from [7, Prop 1] that if is the fundamental matrix solution of

then

for . If we choose large enough that

and put then (1) can be written

| (29) |

where

and so if then

where

Uniform continuity of in this region implies that as . If we fix small enough that

then it follows from the argument in [6, Thm 9] that if is a solution of (29) with for some then

for all with where . Hence as .

Moreover, note that if is a solution of (29) where for all we have

for all with . Fixing any and taking the limit implies that . Hence the only solution that satisfies for all is the pullback attractor .

QED