High-order compact schemes for parabolic problems with mixed derivatives in multiple space dimensions

Abstract

We present a high-order compact finite difference approach for a class of parabolic partial differential equations with time and space dependent coefficients as well as with mixed second-order derivative terms in spatial dimensions. Problems of this type arise frequently in computational fluid dynamics and computational finance. We derive general conditions on the coefficients which allow us to obtain a high-order compact scheme which is fourth-order accurate in space and second-order accurate in time. Moreover, we perform a thorough von Neumann stability analysis of the Cauchy problem in two and three spatial dimensions for vanishing mixed derivative terms, and also give partial results for the general case. The results suggest unconditional stability of the scheme. As an application example we consider the pricing of European Power Put Options in the multidimensional Black-Scholes model for two and three underlying assets. Due to the low regularity of typical initial conditions we employ the smoothing operators of Kreiss et al. to ensure high-order convergence of the approximations of the smoothed problem to the true solution.

1 Introduction

In the last decades, starting from early efforts of Gupta et al. [9, 10], high-order compact finite difference schemes were proposed for the numerical approximation of solutions to elliptic [19, 1] and parabolic [20, 12] partial differential equations. These schemes are able to exploit the smoothness of solutions to such problems and allow to achieve high-order numerical convergence rates (typically strictly larger than two in the spatial discretisation parameter) while generally having good stability properties. Compared to finite element approaches the high-order compact schemes are parsimonious and memory-efficient to implement and hence prove to be a viable alternative if the complexity of the computational domain is not an issue. It would be possible to achieve higher-order approximations also by increasing the computational stencil but this leads to increased bandwidth of the discretisation matrices and complicates formulations of boundary conditions. Moreover, such approaches sometimes suffer from restrictive stability conditions and spurious numerical oscillations. These problems do not arise when using a compact stencil.

Although applied successfully to many important applications, e.g. in computational fluid dynamics [18, 16, 15, 8] and computational finance [5, 6, 22, 2, 4], an even wider breakthrough of the high-order compact methodology has been hampered by the algebraic complexity that is inherent to this approach. The derivation of high-order compact schemes is algebraically demanding, hence these schemes are often taylor-made for a specific application or a rather smaller class of problems (with some notable exceptions as, for example Lele’s paper [14]). The algebraic complexity is even higher in the numerical stability analysis of these schemes. Unlike for standard second-order schemes, the established stability notions imply formidable algebraic problems for high-order compact schemes. As a result, there are relatively few stability results for high-order compact schemes in the literature. This is even more pronounced in higher spatial dimension, as most of the existing studies with analytical stability results for high-order compact schemes are limited to a one-dimensional setting.

Most works focus on the isotropic case where the main part of the differential operator is given by the Laplacian. Another layer of complexity is added when the anisotropic case is considered and mixed second-order derivative terms are present in the operator. Few works on high-order compact schemes address this problem, and either study constant coefficient problems [7] or specific equations [2].

Consequently, our aim in the present paper is to establish a high-order compact methodology for a class of parabolic partial differential equations with time and space dependent coefficients and mixed second-order derivative terms in arbitrary spatial dimension. We derive general conditions on the coefficients which allow to obtain a high-order compact scheme which is fourth-order accurate in space and second-order accurate in time. Moreover, we perform a von Neumann stability analysis of the Cauchy problem in two and three spatial dimensions for vanishing mixed derivative terms, and also give partial results for the general case. As an application example we consider the pricing of European Power Put Basket options with two and three underlying assets in the multidimensional Black-Scholes model. The partial differential equation features second-order mixed derivative terms and, as an additional difficulty, is supplemented by an initial condition with low regularity. We use the smoothing operators of Kreiss et al. [13] to restore high-order convergence.

The rest of this paper is organised as follows. In the next section, we state the general parabolic partial differential equation in spatial dimensions and give the central difference approximation for the associated elliptic problem. We then derive auxiliary relations for the higher-order derivatives appearing in the truncation error of the central difference approximation in Section 3. In Section 4 we give conditions on the coefficients of the partial differential equation under which a high-order compact scheme is obtainable. Semi-discrete high-order compact schemes in and space dimensions are derived in Section 5. Section 6 discusses the time discretisation. A thorough von Neumann stability analysis of the Cauchy problem in and space dimensions is performed in Section 7. In Section 8 we apply the schemes to option pricing problems for European Basket Power Put options and report results of our numerical experiments in Section 9. Section 10 concludes.

2 Parabolic problem and its central difference approximation

We consider the following parabolic partial differential equation with mixed derivative terms in spatial dimensions for ,

| (1) |

with initial condition and suitable boundary conditions, with space- and time-dependent coefficients , , and . The spatial domain is of -dimensional rectangular shape with and with for . The temporal domain is given by with . The functions , , and are assumed to be in for any , and is assumed to be differentiable with respect to . Introducing we can rewrite (1) as

| (2) |

We start by defining a grid on ,

| (3) |

where are the step sizes in the -th direction with for . We use for the interior of . On this grid we denote by the discrete approximation of the continuous solution at the point and time . Using the central difference operator and the standard second-order central difference operator in -direction we get

| (4) | ||||

for and , evaluated at the grid points . Using the approximations (4) in (2) gives

| (5) | ||||

where if for for a step size . If the consistency error is in , we call the scheme high-order. In order to achieve a high-order scheme we need to find second-order approximations of the derivatives , and for with . We call the scheme high-order compact, if we can achieve this using only points from a compact computational stencil for . We have

| (6) |

for as the compact computational stencil and define .

3 Auxiliary relations for higher derivatives

In this section we calculate auxiliary relations for the higher derivatives appearing in (5). These relations for the higher derivatives can be calculated by differentiating (2). In doing so no additional error is introduced. Differentiating equation (2) with respect to and then solving for leads to

| (7) |

for . The relation for can be approximated with consistency order two on the compact stencil (6) using the central difference operator, as all derivatives of in the above equation are only differentiated up to twice in each direction.

Differentiating (2) twice with respect to , and solving the resulting equation for , we obtain

| (8) | ||||

We can approximate with second order consistency on the compact stencil (6), when using the central difference operator and the auxiliary relations for in (7) for . Differentiating equation (2) once with respect to and once with respect to leads to

where can be approximated on the compact stencil (6) using and , as defined in equation (7), and the central difference operator for with . This can be written as

| (9) |

4 Conditions for obtaining a high-order compact scheme

In this section we derive conditions on the coefficients of the partial differential equation (1) under which it is possible to obtain a high-order compact scheme, i.e. only using points of the -dimensional compact stencil (6) for discretisation and receiving a fourth-order scheme with for for a given step size . Using equations (7) and (8) and then (9) in (5) leads to

| (10) |

where , if for . The leading error terms are given by for with . If the conditions

| (11) |

are fulfilled for all with these second order terms vanish and the resulting error term is of fourth order. Hence, for any partial differential equation (1) which satisfies (11) we obtain a high-order compact scheme. In the case for all , it is possible to choose freely for each spatial direction, whereas in other possible cases there are interdependencies for at least some of the step sizes. For each pair with the condition has to hold for all . This means has to be constant as is constant, see (3).

5 Semi-discrete high-order compact schemes

In this section we present the semi-discrete high-order compact schemes in spatial dimensions . We consider the case where the cross derivatives do not vanish, hence we assume, for simplicity, in combination with for to satisfy condition (11). Our aim in this section is to derive a semi-discrete scheme of the form

| (12) |

at each point with for and time , where the function depends on the function given in (1).

5.1 Semi-discrete two-dimensional scheme

In this section we derive the high-order compact discretisation of (1) in spatial dimension . Considering the grid point with and time we are able to obtain the coefficients of for and on the compact stencil by employing the central difference operator in (10). To streamline notation we denote by the first derivative with respect to and by the second derivative, once in - and once in -direction with . Note that in the following the functions , , , and are evaluated at and . We omit these arguments for the sake of readability. The coefficients are given by:

Analogously, we obtain the coefficients of for and at each point and time ,

where . Additionally, for , ,

holds, where was used. We have and in (12) with and for and . and are zero otherwise and the approximation only uses points of the compact stencil.

5.2 Semi-discrete three-dimensional scheme

In this section we derive the high-order compact discretisation of (1) in spatial dimension . Considering the conditions in (11) we observe that in the three-dimensional case we have three different possibilities to satisfy the conditions and thus obtain a high-order compact scheme. We focus on the case and set Considering an interior grid point and time we are able to produce the coefficients of for , and by employing the central difference operator in (10). Again, to streamline the notation we denote by and the first and second derivative of the coefficients with respect to , and with respect to and , respectively. Note again that in the following and are evaluated at and , where for . We omit these arguments for the sake of readability. Due to the length of the coefficient expressions , they are given in the appendix.

6 Fully discrete scheme

The semi-discrete scheme presented in the previous sections can be extended to a fully discrete scheme for the parabolic problem (1) by additionally discretising in time. Any time integrator can be implemented to solve the problem as in [20]. Here we consider a Crank-Nicolson type time-discretisation with constant time step to obtain a fully discrete scheme. Let

where . and are defined through a semi-discrete finite difference scheme with fourth-order consistency using only points of the compact stencil (6). Then, a fully discrete high-order compact finite difference scheme for (1) with on the time grid for and for all is given at each point by

| (13) |

where and . This scheme is second-order consistent in time and fourth-order consistent in space. We have fourth-order consistency in terms of for while only using the compact stencil. Note that up to this point only the spatial interior is discussed. The applied boundary conditions may still have an effect the above numerical scheme.

7 Stability analysis for the Cauchy problem in dimensions

In this section we consider the stability analysis of the high-order compact scheme for the Cauchy problem associated with (1) in the case . The coefficients of the semi-discrete scheme are given in Section 5.1 for two spatial dimensions and in Section 5.2, when three spatial dimensions occur. Those coefficients are non-constant, as the coefficients of the parabolic partial differential equation (1) are non-constant.

We consider a von Neumann stability analysis. Other approaches which take into account boundary conditions like normal mode analysis [11] are beyond the scope of the present paper. For both and , we give a proof of stability in the case of vanishing cross derivative terms and frozen coefficients in time and space, which means that all possible values for the coefficients are considered, but as constants, hence the derivatives of the coefficients of the partial differential equation appearing in the discrete schemes are set to zero. This approach has been used as well in [11, 21] and gives a necessary stability condition, whereas slightly stronger conditions are sufficient to ensure overall stability [17]. This approach is extensively used in the literature and yields good criteria on the robustness of the scheme. In (13) we use

for , where is the imaginary unit, is the amplitude at time level and for the wavelength for . Then the fully discrete scheme satisfies the necessary von Neumann stability condition for all , when the amplification factor satisfies

| (14) |

7.1 Stability analysis for the two-dimensional case

In this section we perform the von Neumann stability analysis for the two-dimensional high-order compact scheme of Section 5.1. The analysis of the case with vanishing cross-derivative and frozen coefficients are carried out in detail. In the case of non-vanishing mixed derivatives partial results are given for frozen coefficients.

Theorem 1.

Proof.

Let , , and The stability condition (14) for the fully discrete scheme (13) using the coefficients defined in Section 5.1 yields (explicit expressions for , are given below). We discuss the numerator and the denominator separately in the following.

The numerator can be written as where the polynomials

are non-negative, since

for . Hence, we observe that holds, as .

Now we consider the denominator , which can be written as

where

because and where

with . We observe that changes sign, as, for example and . Hence, we cannot determine the sign of directly.

If , we have and hence . Since is symmetric, we can say without loss of generality that in the following. Furthermore, as both and are frozen coefficients, we set , which leads to

The function can be rewritten as

with In the case we have and thus and . In the case we have , hence the function has a global minimum. This minimum is located at

where

Since we have and thus we have for all cases as

.

We still need to show that for all . It holds

for all

as and . This leads to in these cases. For the case it holds , which leads to and .

Therefore, we have for all and

condition (14) is satisfied. ∎

For the situation becomes much more involved. Many additional terms appear in the expression for the amplification factor and we face an additional degree of freedom through . Since we have proven condition (14) holds for it seems reasonable to assume it also holds at least for values of close to zero. In von Neumann stability analysis it is often most difficult to guarantee that stability condition (14) holds for extreme values of , , and . We have the following partial result which holds in the case of frozen coefficients and non-vanishing coefficient of the mixed derivative, i.e. .

Lemma 2.

Proof.

Using for and for , straight-forward computation shows that on each corner point . Hence, condition (14) holds. ∎

It is worth mentioning that in a comparable situation in [3] (where a specific partial differential equation of type (1) is considered) an additional numerical evaluation of condition (14) revealed it to hold also for non-vanishing mixed derivatives with . However, the left hand side of (14) was very close to zero, and although the inequality was always satisfied, this left little room for analytical estimates. This leads to the conjecture that the stability condition in that case was satisfied also for general parameters, although it would be hard to prove analytically. Lemma 2 above suggests the present case is similar. We remark that in our numerical experiments we observe a stable behaviour throughout, also for general choice of parameters.

7.2 Stability analysis for the three-dimensional case

In this section we analyse the stability of the high-order compact scheme with coefficients given in Section 5.2 in three space dimensions. We first perform a thorough von Neumann stability analysis in the case of vanishing cross derivative terms for frozen coefficients. We observe no additional stability condition in this case. Then we give partial results in the case of non-vanishing cross-derivative terms for frozen coefficients.

Theorem 3.

Proof.

Let and for . The stability condition (14) yields (explicit expressions for , are given below).

For the numerator we have since and the polynomials

are non-negative since

for .

The denominator can be written as

where

since and

for . We still need to show . Since we cannot determine the sign of directly, we consider three different cases.

Having leads to

as and .

Secondly, we consider . This leads directly to .

From now on we have . Since is symmetric with respect to , we assume without loss of generality . Additionally, we have . Setting and gives

To calculate the extremum of ,

is necessary, which leads to

with

It holds for . Since this is the unique root of , as , we have a minimum at . We obtain where

with for . Hence, in all three cases we conclude , and holds.

We still need to show that for all . It holds for all as and . This leads to in these cases. For the case we have , which leads to and . Therefore, holds for all and condition (14) is satisfied. ∎

For the more general case with non-vanishing cross-derivatives we have the following result. The comments made in the previous section also apply here.

Lemma 4.

Proof.

Using for , for and for , straight-forward computation yields just as in the two-dimensional spatial setting to for all corner points. Hence, condition (14) is satisfied. ∎

8 Application to Black-Scholes Basket options

To illustrate the practicality of the proposed scheme we now consider the -dimensional Black-Scholes option pricing PDE (see, e.g. [23]). In the option pricing problem mixed derivatives appear naturally from correlation of the underlying assets. After transformations, the conditions (11) are satisfied, and we give the coefficients of the resulting scheme. Then we discuss the boundary conditions as well as the time discretisation.

8.1 Transformation of the -dimensional Black-Scholes equation

In the multidimensional Black Scholes model the asset prices follow a geometric Brownian motion,

| (15) |

where is the -th underlying asset which has an expected return of , a continuous dividend of , and the volatility for and . The Wiener processes are correlated with for with . Application of It’s lemma and standard arbitrage arguments show that any option price solves the -dimensional Black-Scholes partial differential equation,

| (16) |

where The transformations

| (17) |

for , where is a constant scaling parameter to assure that the resulting computational domain does not get too large, leads to

| (18) |

where Comparing this equation with (1), we identify

| (19) |

for and . We find that the transformed partial differential equation (18) with these coefficients satisfies the conditions given by (11), if for a step size is used. Hence, we are able to obtain a high-order compact scheme in any spatial dimension .

8.2 Semi-discrete two-dimensional Black-Scholes equation

In this section we apply our general two-dimensional semi-discrete scheme, see Section 5.1, to the two-dimensional Black-Scholes model. To obtain the semi-discrete scheme (12) we have to apply (19) with to the coefficients in Section 5.1, which gives

where is the coefficient of for and . The coefficients of are given by

Additionally, it holds . This gives a semi-discrete scheme of the form (12), where and are time-independent. As in 6 we apply Crank-Nicolson type time discretisation and obtain the fully discrete scheme for the spatial interior.

8.3 Semi-discrete three-dimensional Black-Scholes equation

In this section we give the semi-discrete scheme (12) for the three-dimensional Black-Scholes Basket option. Using (19) with in Section 5.1 and the appendix we obtain the coefficients of for , and , which are

Similarly, we get the coefficients of , given by

Additionally, we have . We obtain a semi-discrete scheme of the form (12), where and are time-independent. As in 6 we apply Crank-Nicolson type time discretisation and obtain the fully discrete scheme for the spatial interior.

8.4 Treatment of the boundary conditions

After deriving a high-order compact scheme for the spatial interior we now discuss the boundary conditions.

8.4.1 Lower boundaries

The first boundary we discuss is for some at time . Once the value of the asset is zero, it stays constant over time, see (15). Hence, using for in (16) and applying the transformation (17) leads to

with Hence, at these boundaries we are able to obtain high-order compact schemes in the same manner as shown for the spatial interior with then spatial dimensions, as the coefficients of the partial differential equations of these boundaries satisfy condition (11). The case , i.e. , leads to the Dirichlet boundary condition at time , since in that case .

8.4.2 Upper boundaries

Upper boundaries are boundaries with for some at time . For a sufficiently large for , we set

with for for a European Power Put Basket option. Employing this in (16) and using the transformations (17), yields

| (21) |

with . Hence the upper boundaries show the same behaviour as the lower boundaries for a European Power Put Basket. Analogously, we have the Dirichlet boundary condition for if .

8.5 Combination of upper and lower boundaries

A combination of upper and lower boundaries thus behaves in the same manner and the resulting partial differential equations with spatial dimensions satisfy condition (11) as well. For the corner points of we have and thus again .

9 Numerical experiments for Black-Scholes Basket options

In this section we discuss the numerical experiments for the Black-Scholes Basket Power Puts in spatial dimensions . The equation systems which have to be solved over time have been derived in Section 8. According to [13], we cannot expect fourth-order convergence if the initial condition is not sufficiently smooth. Hence, we have to smooth the initial condition for Power Puts with . In [13] suitable smoothing operators are identified in Fourier space. Since the order of convergence of our high-order compact scheme is four, we use the smoothing operator , given by its Fourier transform

This leads to the smoothed initial condition

in the case for any step size , where is the original initial condition and denotes the Fourier inverse of , see [13]. If is smooth enough in the integrated region around , we have . That means that it is possible to identify the points where smoothing is necessary.

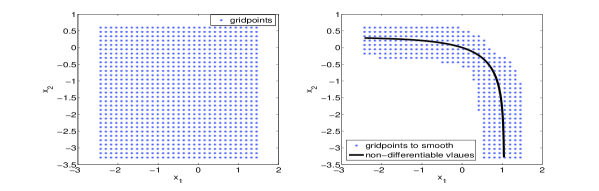

Figure 1 shows an example of a two-dimensional grid on the left side and on the right side a graph of the non-differentiable points of the initial condition given in (20) together with the identified grid points, where smoothing is necessary. The points are chosen in such a way that we ensure that the non-differentiable points have no influence on for those points, which are not shown in Figure 1 on the right hand side. This approach reduces the necessary calculations significantly. As , the smooth initial condition converges towards the original initial condition given in (20). The results in [13] guarantee high-order convergence of the approximation of the smoothed problem to the true solution of (18).

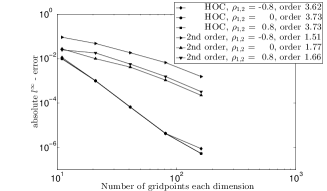

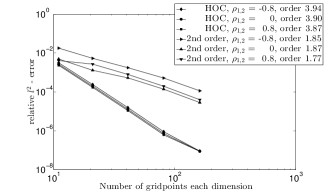

We use the relative -error as well as the -error to examine the numerical convergence rate, where denotes a reference solution on a fine grid and is the approximation. When identifying the convergence order of the schemes, we determine it as the slope of the linear least square fit of the individual error points in the loglog-plots of error versus number of grid points per spatial direction.

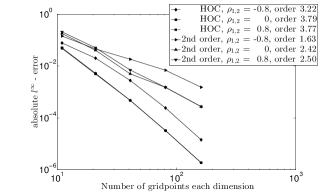

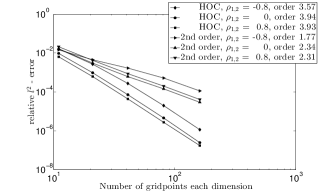

9.1 Numerical example with two underlying assets

In this section we report the numerical results for a two-dimensional Black-Scholes Basket Power Put. We compare the high-order compact scheme (‘HOC’) with the standard scheme (‘2nd order’), which is obtained by using the central difference operator directly in (18) for with no further action and thus leads to a classical second-order scheme. We consider plain European Puts () and use the smoothing procedure outlined above for the initial condition (20). The parameter values

and are used, unless stated otherwise. The parabolic mesh ratio is fixed to , although we point out that neither the von Neumann stability analysis nor our numerical experiments revealed any practical restrictions on its choice.

Figure 2 shows convergence plots for the -error (left) and for the relative -error (right) for a European Put, respectively. The initial condition is smoothed using the procedure outlined above. For both types of errors we observe that the numerical convergence rates agree very well with the theoretical orders of the schemes. The high-order compact scheme yields numerical convergence orders close to four and strongly outperforms the standard second-order scheme. The choice of the correlation parameter , and has very little influence.

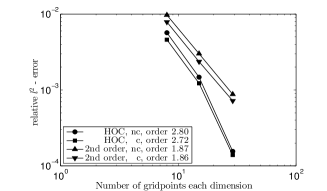

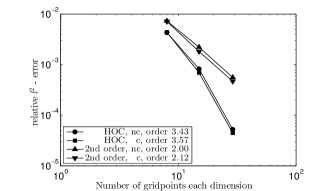

9.2 Numerical example with three assets

In this section we report on numerical experiments with three underlying assets. We choose the parameters

Due to the computational intensity of the three-dimensional problem the number of grid points per spatial dimension is smaller compared to the results in two dimensions reported above. To ensure that at the same time there is a sufficiently large number of grid points in time, we fix the parabolic mesh ratio to (not for stability reasons). We perform two types of experiments: without any correlation between the assets (labeled by ‘nc’ in the plots), and with correlation (labeled by ‘c’ in the plots) using the parameter values , ,

We compare the standard approximation to our high-order compact scheme for European Power Put options with . For the European Power Puts with one would smooth the initial condition, similar as above, to ensure high-order convergence.

Figure 3 shows the convergence of the relative -error for a European Power Put with and . We use the original initial conditions, no smoothing is applied here. The numerical convergence rates of the high-order compact scheme are slightly reduced to about three and three and a half, respectively. Additional smoothing, which we omitted here due to limit the computational load, would result in even better results. Still, in the high-order compact scheme outperforms the standard second-order scheme significantly in all cases.

9.3 Numerical example with space-dependent coefficients

In this section we will apply numerical examples for (16), where the continuous dividends are dependent on the underlying asset price. For both asset prices with we consider the following example, where the continuous dividends are zero for small asset prices and then smoothly increase around an asset price towards a given parameter ,

Financially, the interpretation could be as follows: if the asset is a dividend-paying stock, low stock prices may mean that the company may not be in the financial position to pay dividends. A low value of leads to slow transition from to . We can apply the transformations given in (17) and hence use the coefficients

| (22) |

for to obtain the coefficients of the numerical scheme, see Section 5.1. The boundary conditions of Section 8.4 are employed and the parameter values of Section 9.1 as well as

for are used in the numerical experiments.

Figure 4 shows numerical convergence plots for a European Put with space-dependent continuous dividend. Again, smoothing of the initial condition is employed. For the -error as well as the -error the high-order compact scheme has convergence rates close to four for and . The convergence rate for the case is in the -error, which is mainly due to the two approximations with eleven and 21 grid-points per spatial direction, and in the -error. The convergence orders of the standard scheme are for are slightly above two for both types of errors. For the convergence orders are noticeable lower as well. In all cases of correlation the high-order compact scheme outperforms the standard second-order scheme significantly.

10 Conclusion

We presented a new high-order compact scheme for a class of parabolic partial differential equations with time and space dependent coefficients, including mixed second-order derivative terms in spatial dimensions. The resulting schemes are fourth-order accurate in space and second-order accurate in time. In a thorough von Neumann stability analysis, where we focussed on the case of vanishing mixed derivative terms, we showed that a necessary stability condition holds for frozen coefficients without further conditions in two and three space dimensions. For non-vanishing mixed derivative terms we were able to give partial results. The results suggest unconditional stability of the scheme. As an application example we considered the pricing of European Power Put options in the multidimensional Black-Scholes model. The typical initial conditions of this problem lack sufficient regularity, therefore a suitable smoothing procedure was employed to ensure high-order convergence. In all numerical experiments performed a comparative standard second-order scheme is significantly outperformed.

Although we derived the scheme in arbitrary space dimension, it was not our aim in this paper to attack the so-called curse of dimensionality. The issue of exponentially increasing number of unknowns with growing spatial dimension on full grids is of course alleviated to some degree by a high-order scheme. To obtain a similar accuracy as a second-order scheme which uses unknowns on a full grid, our high-order compact approach will ‘only’ require unknowns. To really attack very high-dimensional problems one would need to combine our approach with hierarchical approaches, e.g. using sparse grids (typically requiring unknowns), which is beyond the scope of the present paper.

Acknowledgment

The authors are grateful to the anonymous reviewers for their constructive comments. The second author acknowledges support by the European Union in the FP7-PEOPLE-2012-ITN Program under Grant Agreement Number 304617 (FP7 Marie Curie Action, Project Multi-ITN STRIKE – Novel Methods in Computational Finance).

References

- [1] G. Berikelashvili, M.M. Gupta, and M. Mirianashvili, Convergence of fourth order compact difference schemes for three-dimensional convection-diffusion equations, SIAM J. Numer. Anal., 45 (2007), pp. 443–455.

- [2] B. Düring and M. Fournié, High-order compact finite difference scheme for option pricing in stochastic volatility models, J. Comput. Appl. Math., 236 (2012), pp. 4462–4473.

- [3] , On the stability of a compact finite difference scheme for option pricing, in Progress in Industrial Mathematics at ECMI 2010, M. Günther and et al., eds., Berlin, Heidelberg, 2012, Springer, pp. 215–221.

- [4] B. Düring, M. Fournié, and C. Heuer, High-order compact finite difference schemes for option pricing in stochastic volatility models on non-uniform grids, J. Comput. Appl. Math., 271 (2014), pp. 247–266.

- [5] B. Düring, M. Fournié, and A. Jüngel, High-order compact finite difference schemes for a nonlinear Black-Scholes equation, Intern. J. Theor. Appl. Finance, 6 (2003), pp. 767–789.

- [6] , Convergence of a high-order compact finite difference scheme for a nonlinear Black-Scholes equation, Math. Mod. Num. Anal., 38 (2004), pp. 359–369.

- [7] M. Fournié and S. Karaa, Iterative methods and high-order difference schemes for 2D elliptic problems with mixed derivative., J. Appl. Math. Comput., 22 (2006), pp. 349–363.

- [8] M. Fournié and A. Rigal, High order compact schemes in projection methods for incompressible viscous flows, Commun. Comput. Phys., 9 (2011), pp. 994–1019.

- [9] M.M. Gupta, R.P. Manohar, and J.W. Stephenson, A single cell high order scheme for the convection-diffusion equation with variable coefficients., Int. J. Numer. Methods Fluids, 4 (1984), pp. 641–651.

- [10] , High-order difference schemes for two-dimensional elliptic equations., Numer. Methods Partial Differ. Equations, 1 (1985), pp. 71–80.

- [11] B. Gustafsson, H.-O. Kreiss, and J. Oliger, Time Dependent Problems and Difference Methods, John Wiley & Sons, New York, 2013.

- [12] S. Karaa and J. Zhang, Convergence and performance of iterative methods for solving variable coefficient convection-diffusion equation with a fourth-order compact difference scheme., Comput. Math. Appl., 44 (2002), pp. 457–479.

- [13] H.O. Kreiss, V. Thomee, and O. Widlund, Smoothing of initial data and rates of convergence for parabolic difference equations., Commun. Pure Appl. Math., 23 (1970), pp. 241–259.

- [14] S.K. Lele, Compact finite difference schemes with spectral-like resolution., J. Comput. Phys., 103 (1992), pp. 16–42.

- [15] M. Li and T. Tang, A compact fourth-order finite difference scheme for unsteady viscous incompressible flows., J. Sci. Comput., 16 (2001), pp. 29–45.

- [16] M. Li, T. Tang, and B. Fornberg, A compact fourth-order finite difference scheme for the steady incompressible Navier-Stokes equations., Int. J. Numer. Methods Fluids, 20 (1995), pp. 1137–1151.

- [17] R.D. Richtmayer and K.W. Morton, Difference Methods for Initial Value Problems, Interscience, New York, 1967.

- [18] W.F. Spotz and G.F. Carey, High-order compact scheme for the steady stream-function vorticity equations., Int. J. Numer. Methods Eng., 38 (1995), pp. 3497–3512.

- [19] , A high-order compact formulation for the 3D Poisson equation., Numer. Methods Partial Differ. Equations, 12 (1996), pp. 235–243.

- [20] , Extension of high-order compact schemes to time-dependent problems., Numer. Methods Partial Differ. Equations, 17 (2001), pp. 657–672.

- [21] J.C. Strickwerda, Finite Difference Schemes and Partial Differential Equations, SIAM, Philadelphia, 2004.

- [22] D.Y. Tangman, A. Gopaul, and M. Bhuruth, Numerical pricing of options using high-order compact finite difference schemes, J. Comp. Appl. Math., 218 (2008), pp. 270–280.

- [23] P. Wilmott, Derivatives. The theory and practice of financial engineering, John Wiley & Sons Ltd., Chichester, UK, 1998.

Appendix A Coefficients for semi-discrete scheme in three dimensions

Considering an interior grid point and time , the coefficients of for , and of the three-dimensional semi-discrete scheme in Section 5.2 are given by:

Note that in the above and are evaluated at and . To streamline the notation we used and to denote the first and second derivative of the coefficients with respect to , and with respect to and , respectively.