Seasonal Stochastic Volatility and Correlation together with the Samuelson Effect in Commodity Futures Markets ††thanks: We would like to thank Ennio Fedrizzi, François Le Grand and Cassio Neri for helpful and stimulating comments, discussions and suggestions.

Abstract

We introduce a multi-factor stochastic volatility model based on the CIR/Heston volatility process that incorporates seasonality and the Samuelson effect.

First, we give conditions on the seasonal term under which the corresponding volatility factor is well-defined.

These conditions appear to be rather mild.

Second, we calculate the joint characteristic function of two futures prices for different maturities in the proposed model.

This characteristic function is analytic.

Finally, we provide numerical illustrations in terms of implied volatility and correlation produced by the proposed model with five different specifications of the seasonality pattern.

The model is found to be able to produce volatility smiles at the same time as a volatility term-structure that exhibits the Samuelson effect with a seasonal component.

Correlation, instantaneous or implied from calendar spread option prices via a Gaussian copula, is also found to be seasonal.

Keywords: Seasonal Commodities Seasonal Volatility Seasonal Correlation Samuelson Effect Stochastic Volatility Calendar Spread Option Multi-Factor Model Joint Characteristic Function

JEL: C63 C52 G13

1 Introduction

Seasonality is a well-known empirical feature of several commodities markets. In the energy sector, among fossil fuels, natural gas futures curves, and among refined products, gasoline, heating oil and fuel oil futures curves all typically display seasonality. In the agricultural sector, almost all futures curves show seasonality due to harvest times and the seasons of the year.

It is important to distinguish from the outset between two types of seasonality: seasonality of futures prices and seasonality of volatility of futures prices.

Regarding seasonality of prices, consider agricultural commodities such as corn, soybeans and wheat. These tend to be in high supply after the harvest in summer, and in low supply in the months preceding the harvest. This typically leads to relatively low prices of futures contracts with delivery months in the summer or early fall, and high futures prices of contracts with delivery months in late winter or spring. Therefore, when the prices of these contracts are plotted as a function of their maturity, they tend to rise and fall with the maturity in some seasonal way. In other words, the futures curve shows seasonality. However, the price of an individual futures contract with a given maturity should not rise and fall over time in any kind of seasonal way: indeed, such a behaviour would lead to easy arbitrage opportunities.

Regarding seasonality of volatility, the situation is different in the sense that now an individual futures contract, with fixed maturity, tends to go through phases of relatively high or low volatility according to a seasonal pattern. To take again the example of agricultural commodities, the weather in the months leading up to the harvest has a direct impact on its quality and quantity, and futures prices can fluctuate strongly as forecasts for the new crop change. In contrast to this, weather patterns in winter tend to be of minor consequence for the harvest, and futures prices tend to fluctuate less strongly.

It follows from these empirical observations that for commodity models, seasonality is usually only an issue for the volatility, but not for the futures price itself. Mathematically, individual futures prices are modelled as martingales, and martingales do not have a tendency to rise or fall in a pre-determined way. Clark (2014) gives a general discussion and numerous examples of seasonality in various commodities markets.

Traditionally, there are two approaches to modelling the prices of futures contacts: futures-based models and spot-based models. An advantage of futures-based models models is that since the futures price curve is an input of the model, any arbitrage-free shape of the initial futures curve can be accommodated, including any type of seasonality. In contrast, a first step for spot-based models is to make them fit the initial futures curve, which uses up model parameters and doesn’t necessarily lead to satisfactory results.

Sørensen (2002) studies the modelling of seasonality in corn, soybean and wheat futures markets. Analysis of a large data set of CBOT futures prices data from 1972 to 1997 confirms clearly that futures prices exhibit a seasonality. Another feature that is suggested by the data is seasonal behaviour of the futures price volatilities. In this vein, Richter and Sørensen (2002) propose a model for the spot price of soybeans based on seasonal stochastic volatility. Geman and Nguyen (2005) also introduce a spot-based model for soybean prices with seasonality both for the price level and the (possibly stochastic) volatility level. Back et al. (2013) analyze data from corn, soybean, heating oil and natural gas markets and compare various spot-based models with deterministic seasonal volatility. They conclude that a volatility with seasonality is an important feature when valuing options on futures in these markets. Back et al. (2011) also study a futures-based model with seasonal stochastic volatility, which is essentially the Heston (1993) stochastic volatility model with deterministic, seasonal mean-reversion level in the square-root process followed by the variance. Schmitz et al. (2013) study calendar spread options in agricultural grain markets relying on a joint Heston model for the two underlying futures contracts. These two contracts share the same variance process, which has a constant mean-reversion level, and therefore does not display seasonality. In the context of interest rates, the Cox et al. (1985) (CIR) model has been extended to time-dependent parameters by Maghsoodi (1996), and the Heston (1993) model with time-dependent parameters, including the correlation between the spot price and its variance, has been studied by Benhamou et al. (2010). Let us also note that in the context of electricity markets, Lucia and Schwartz (2002) give a detailed justification of the choice of seasonality function, as do Geman and Roncoroni (2006).

In parallel to his remark about seasonality in futures prices, Sørensen (2002) confirms the Samuelson (1965) hypothesis that “the variations of distant maturity futures are lower than nearby futures prices.” We call this pattern the Samuelson effect. Popular futures-based models that incorporate this effect are those of Clewlow and Strickland (1999a, b). The volatility functions used in these models are deterministic. Schneider and Tavin (2015) extend the multi-factor model of Clewlow and Strickland (1999b) to incorporate stochastic volatility. Not only is stochastic volatility an incontestible empirical feature of prices in futures markets, its inclusion also allows to calibrate the model to option volatility smiles and skews typically seen in futures option markets. In agricultural markets, a reflection of stochastic volatility is the recent introduction of several volatility indices on the CBOE/CBOT: the Corn Volatility Index (CIV) and Soybean Volatility Index (SIV) were introduced in 2011, and the Wheat Volatility Index (WIV) was introduced in 2012.

In this paper, we extend the model introduced in Schneider and Tavin (2015) to incorporate seasonal trends in the stochastic volatility processes. To achieve this, we begin by studying the mathematical conditions to impose on the seasonality function to guarantee that the generalized CIR process retains important features, such as existence and uniqueness of a strong solution, and positivity. It turns out that these conditions are very mild. These conditions appear to be not only interesting from a theoretical point of view, but also useful in practice, because different markets may need to be modelled with different seasonality patterns for the volatility.

We then introduce the model with seasonal volatility and show how, by a generalisation of the results in Schneider and Tavin (2015), the joint characteristic function of the log-returns of two futures prices can be obtained. It turns out that the Riccati ODE for the first function is not affected, and only the integral ODE for the second function depends on and is altered. Therefore, the same closed-form solution for as in Schneider and Tavin (2015) can be used.

Next, we propose several specifications of seasonality functions and compare them.

Then, we calculate implied volatility surfaces in our model. We also calculate calendar spread option prices and examine the effect of changes in the seasonality function on these prices.

Regarding correlations, we study the effect seasonality has on the instantaneous correlation between two futures contracts in the case when the variances are deterministic. We find that the influence of the seasonality on the correlation depends on the magnitude of the exponential damping of the volatility factors. And from the calendar spread option prices we calculate implied correlations, where again we can observe how the seasonal pattern of the variance translates into a seasonal pattern of the implied correlation.

The rest of the paper proceeds as follows. In Section 2 we discuss the CIR process with time-dependent drift. In Section 3 we define the proposed model and calculate the associated joint characteristic function. We also give the methods to be used for vanilla and calendar spread option pricing. In Section 4 we review various seasonality functions that can be used to specify the proposed model. Section 5 gives a numerical illustration of the implied volatility patterns produced by the proposed model with different seasonality functions. Section 6 deals with the seasonal behaviour of the instantaneous correlation when volatility is seasonal. In this section we also study the effect of seasonality on calendar spread option prices. Section 7 concludes.

2 The CIR Process with Time-Dependent Drift

To our knowledge, Hull and White (1990) were the first to consider extending the Cox et al. (1985) (CIR) interest rate model to time-dependent coefficients. They conclude that in this general case, it is no longer possible to obtain European bond option prices analytically. Maghsoodi (1996) also studies the “extended” CIR process in which the parameters and are time-dependent and finds, under certain conditions, the unique strong solution to the SDE describing the evolution of the process.

In the context of the Heston (1993) stochastic volatility model, the CIR process represents the variance process of a stock price or foreign-exchange rate. Benhamou et al. (2010) study the “time dependent Heston model” and derive analytical formulas approximating European option prices. In their setup, the mean-reversion parameter is constant, but the parameters and (giving the correlation between the stock price, or foreign-exchange rate, and its variance) are all allowed to vary with time .

In the model introduced here, we only let the mean-reversion level given by depend on time, while the other parameters and (and later also ) remain constant.

Let be a filtered probability space, and let be a Brownian motion on this space. Let be a set of times having only finitely many points in every bounded interval, and let be the partition of defined by . Finally, let the seasonality function be piecewise continuous with respect to , and assume that it is bounded from below and above by positive constants and .

We will compare two processes (seasonal) and (non-seasonal), which are given, respectively, by the SDEs

| (1) | ||||

| (2) |

with identical parameters and initial conditions .

It is well known that (2) has a unique strong solution. The following result describes the solution to (1).

Proposition 2.1

Assume that the seasonality function is piecewise continuous w.r.t. the partition of , and bounded by positive constants and , i.e. for all . Let the processes and be given by (1) and (2), respectively. Then:

-

(i).

The process (1) has a unique strong solution with continuous sample paths.

-

(ii).

.

-

(iii).

If the Feller condition is satisfied for , then the process is strictly positive.

We prove this result in appendix A.

Note that if the Feller condition is violated, then can possibly reach , but it still cannot become negative.

The piecewise continuity condition on means that even discontinuous specifications of the mean-reversion level, such as the sawtooth function given by

| (3) |

with and , pose no problems. Some other examples of the form of are discussed in Section 4.

3 A Model with Seasonal Stochastic Volatility for Agricultural Futures

3.1 The Financial Framework and the Model

We begin by giving a mathematical description of our model under the risk-neutral measure . Let be an integer, and let be Brownian motions under . Let be the maturity of a given futures contract. The futures price at time , is assumed to follow the stochastic differential equation (SDE)

| (4) |

The processes are stochastic variance processes with time-dependent seasonal mean-reversion level assumed to follow the SDE

| (5) |

Various possibilities of the specification of the seasonal mean-reversion level functions are presented and discussed in Section 4. Note that the initial futures curve is exogenous in our model and can therefore accommodate any seasonal pattern shown by the futures prices.

For the correlations, we assume

| (6) |

and that otherwise the Brownian motions are independent of each other. As we will see, this assumption has as a consequence that the characteristic function factors into separate expectations.

For fixed , the futures log-price follows the SDE

| (7) |

Integrating (7) from time up to a time , gives

| (8) |

We define the log-return between times and of a futures contract with maturity as

In the following, the joint characteristic function of two log-returns will play an important role. For , is given by

| (9) |

The joint characteristic function of the futures log-prices is then given by

| (10) |

Note that futures prices in our model are not mean-reverting, and that the log-price at time and the log-return are independent random variables.

In the following proposition, we show how the joint characteristic function , and therefore also the single characteristic function , is given by a system of two ordinary differential equations (ODE).

Proposition 3.1

The joint characteristic function at time for the log-returns of two futures contracts with maturities is given by

where

and the functions and satisfy the two differential equations

with

The single characteristic function at time for the log-return of a futures contract with maturity is given by setting in the joint characteristic function.

Note that the integrals only depend on the specification of the seasonality functions and the maturity . Therefore, their value can be calculated once and then stored, avoiding recalculations during repeated calls to the characteristic function. Of course, if is a constant function, then the joint characteristic function given above is the same as the one given in Schneider and Tavin (2015).

We prove this result in appendix A.

3.2 Pricing Vanilla Options

European options on futures contracts can be priced using the Fourier inversion technique as described in Heston (1993) and Bakshi and Madan (2000). Let denote the strike and the maturity of a European call option on a futures contract with maturity . The function needed for this technique is the single characteristic function of the futures log-price , given by , with obtained from Proposition 3.1. European put options can be priced via put-call parity .

3.3 Pricing Calendar Spread Options

Calendar spread options (CSO) are popular options in commodity markets. To give a recent example, in February 2015 the Minneapolis Grain Exchange (MGX) introduced North American Hard Red Spring Wheat (HRSW) CSOs for trade on CME Globex. Calendar spread options are defined as follows.

Let two futures maturities , an option maturity , and a strike (which is allowed to be negative) be fixed. Then the payoffs of calendar spread call and put options, and , are respectively given by

| (11) |

| (12) |

To evaluate such options with a pricing model, the discounted expectation of the payoff must be calculated in the risk-neutral measure. As for “vanilla” European options, there is a model-independent put-call parity for calendar spread options:

| (13) |

Caldana and Fusai (2013) show how to calculate CSC prices with models for which the joint characteristic function is known. Strictly speaking, their methods give a lower bound for the calendar spread option price, but usually this bound is very close to the true price. Note that in case the strike the formula is exact. When we calculate CSO prices, we do so with this method. An alternative method, based on the -dimensional FFT algorithm, is given by Hurd and Zhou (2010). We refer to Schneider and Tavin (2015) and references therein for more details on calendar spread options.

4 Seasonality Functions

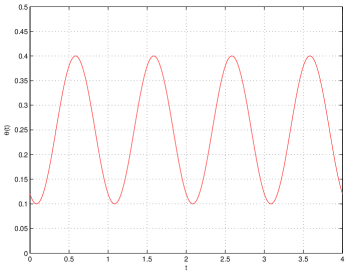

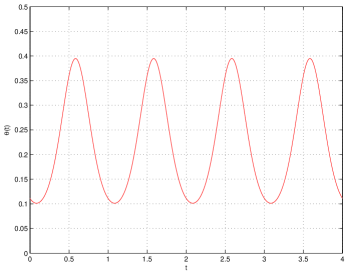

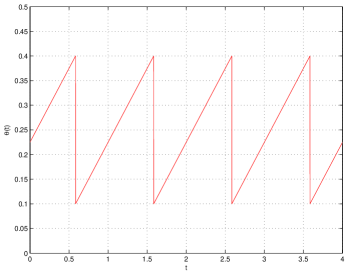

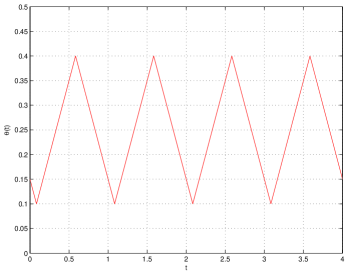

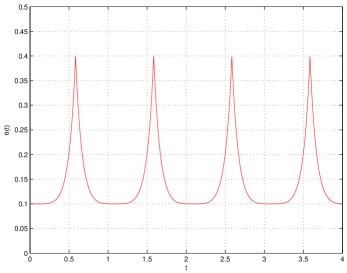

Below we present four types of seasonality functions that can be used as parametric forms to model seasonal variations of the volatility. For a given factor, represents the seasonality term of the volatility dynamics and is an integral involving appearing in different expressions such as the characteristic function. For and , is written

| (14) |

The presented seasonality functions are parametric and work with three parameters: and . Parameter controls for the volatility level. Parameter controls the magnitude of the seasonality pattern and corresponds to the time of the year when the volatility reaches its maximum.

It seems relevant to consider different seasonality patterns as the reasons underpinning the seasonality phenomena in volatility may vary from a market to another. The first two patterns considered below are smooth and are based on the sinus function. The three others have points of non-differentiability and/or discontinuity, and may be used to represent a less regular evolution of the volatility.

The sinusoidal pattern is written, with and ,

| (15) | ||||

| (16) |

For a proof of this expression, we refer to Appendix A.

The exponential-sinusoidal pattern is written, with and ,

| (17) |

This parametric form for is used in Back et al. (2011). There is no closed form expression for .

The sawtooth pattern is written, with and ,

| (18) | ||||

| (19) |

where denotes the floor function, is the indicator function and, by convention, if . The proof leading to this expression is found in Appendix A.

The triangle pattern is written, with and ,

| (20) | |||

| (21) |

with , , , and and with convention, if . The proof leading to this expression is found in Appendix A.

The spiked pattern is written, with and ,

| (22) |

This parametric form for can be found in Geman and Roncoroni (2006) where it is used to model the time varying intensity of a jump process. There is no closed form expression for .

Figure 1 presents the plots of these seasonal patterns with .

5 Implied Volatility Smiles and Term-Structures

In this section we present implied volatility smiles and term-structures produced by a one-factor version of the proposed model with seasonality. We have chosen the one-factor model here because our purpose is to illustrate the effect of seasonality on option prices. The considered options are vanilla options on futures. Following the market convention, their maturity is the same as the maturity of the underlying futures contract. The parameters of the considered model with seasonality are gathered in Table 1. Only the parameters corresponding to the seasonality pattern change from one setting to another. The seasonality functions obtained with these parameters are those shown in Figure 1. This numerical application is presented for an illustrative purpose and we take an initial futures curve that is flat in price at USD.

| seasonality function | |||||

|---|---|---|---|---|---|

| parameters | sinusoid | exp-sinusoid | sawtooth | triangle | spiked |

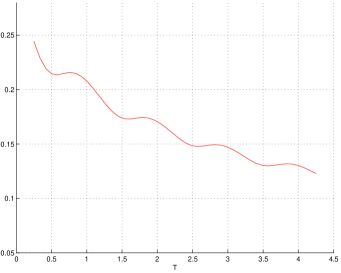

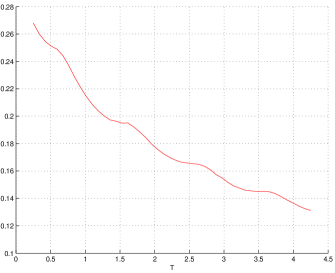

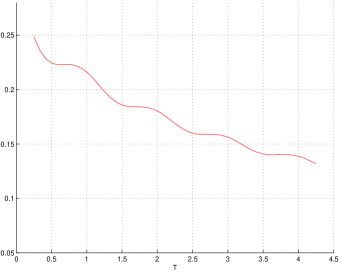

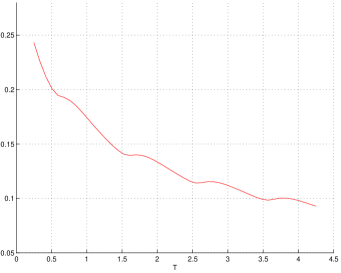

In Figures 2 and 3 we present, for the different seasonality patterns, the implied volatility smiles obtained for different maturities and the term-structure of implied volatility for at-the-money options. The obtained term-structures exhibit both seasonality and the Samuelson effect. The obtained strike-structures exhibit smiled shapes. The implied volatility produced with the sinusoidal and exponential-sinusoidal patterns are similar to each other. For the sawtooth, triangle and spiked patterns, the irregularities of the function seem not to be transferred to the implied volatility. It can also be observed that the choice of the seasonality pattern seems to have very little impact on the shape of the volatility smile. This last remark is particularly striking if one compares the volatility term-structures produced by the sinusoidal and triangle patterns.

6 Seasonal Stochastic Correlation and Calendar Spread Option Prices in the Multi-Factor Model

6.1 Seasonal Stochastic Correlation

We will show in this section that if we specify our model with two or more volatility factors, then the correlation of the returns of two given futures contracts is influenced by the seasonality functions. In other words, the correlation becomes seasonal.

Let us take the -factor model for an illustration. Futures returns follow the SDE

| (23) |

and the two variance processes follow the SDEs

| (24) | ||||

| (25) |

The correlations are given by , , and all other correlations are zero.

Define

| (26) |

Then the instantaneous correlation at time is given by:

| (27) |

Using (26) together with (23) gives for the instantaneous correlation

| (28) |

In contrast to the -factor model, the instantaneous correlation in the -factor model, with , is stochastic.

To illustrate the seasonality of the correlation function , we consider the case when both variances and are deterministic functions of time . The two SDEs (5) then become ordinary differential equations

| (29) |

It is straightforward to see that the solution to (29) is given by

| (30) | ||||

| (31) |

Note that the same transform function already introduced in (14) appears again. For several specifications of , the function is available in closed form, and it is easy to plot the correlation function given by (28).

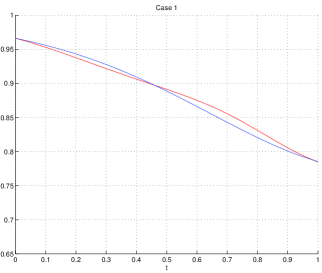

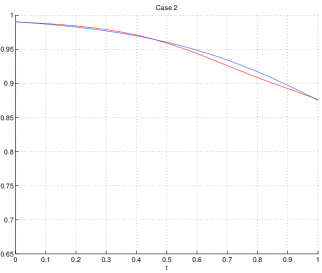

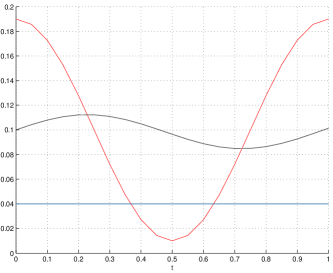

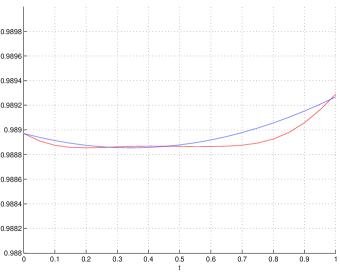

Figure 4 presents the instantaneous correlation obtained with the two-factor model with seasonality in the special case . It also plots the correlation obtained with the version without seasonality and the other terms involved in expression (28). For the seasonal model, only the first factor is seasonal and follows the sinusoidal pattern (15). To produce Figure 4, we consider two cases in order to illustrate different seasonal patterns of the correlation when compared to the non-seasonal case. The non-seasonal case is our benchmark, which is obtained by setting in the seasonality function of each factor. The model parameters for these cases are gathered in Table 2.

| parameters | Case 1 | Case 2 |

|---|---|---|

It is worth remarking that, compared to the non-seasonal case, the instantaneous correlation is modified by the presence of seasonality in the dynamics of the first factor. In the first case (high for the seasonal factor) this correlation is lower at the beginning of the period under scrutiny and higher at the end. In the second case (low for the seasonal factor) it is the opposite. The reasons underpinning the influence of and on the seasonal behaviour of the correlation are still conjectural and need to be further investigated. So far, it seems on the one hand that if we have , then the effect of the first seasonal function on the instantaneous correlation is in the opposite direction, i.e. during periods of high variance the correlation is decreased, and during periods of low variance the correlation is increased. This pattern can be observed in the three l.h.s. panels of Figure 4 illustrating Case 1. On the other hand, if we have , then the effect of the first seasonal function on the instantaneous correlation is in the same direction, i.e. during periods of high variance the correlation is increased, and during periods of low variance the correlation is decreased. This pattern can be observed in the three r.h.s. panels of Figure 4 illustrating Case 2.

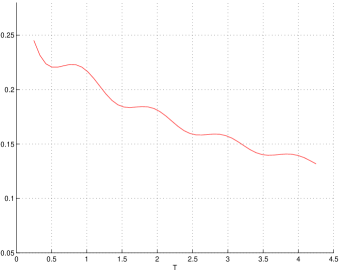

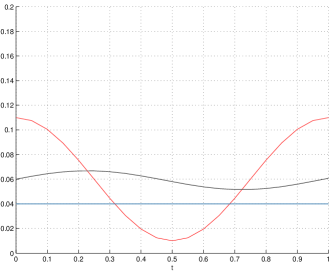

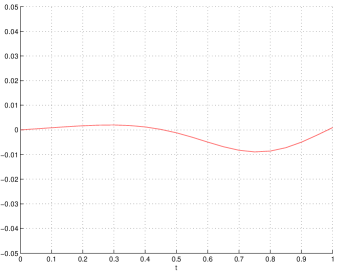

Note also that the instantaneous correlation is not always decreasing with . This remark holds true for the model with seasonality as well as for the case without seasonality. Figure 5 presents a non-decreasing instantaneous correlation obtained with the two-factor model with and without seasonality in the special case . The other parameters are chosen such that the curves are non-decreasing. In the presented illustration the correlation seems to be constant at first sight, but on closer inspection can be seen to be decreasing then increasing.

6.2 The Effect of Seasonality on Calendar Spread Option Prices

In this section, we investigate the effect of seasonality on the prices of calendar spread options. We do so by means of a numerical study in which we consider different cases of model parameters and compute calendar spread option prices with and without seasonality.

This investigation is conducted with the two-factor model with stochastic volatility on both factors but seasonality only on the first one in order to isolate the effect of seasonality. The form of the seasonal pattern is again the sinusoidal one given by equation (15). Calendar spread option prices are obtained with the Caldana and Fusai (2013) method that is well suited for our model. Implied correlations are extracted using a numerical root search.

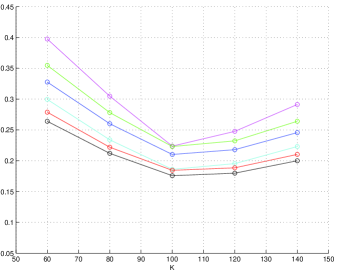

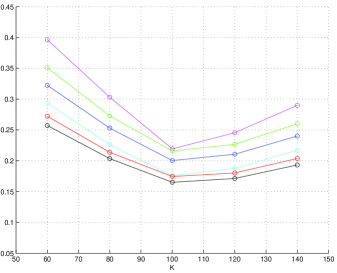

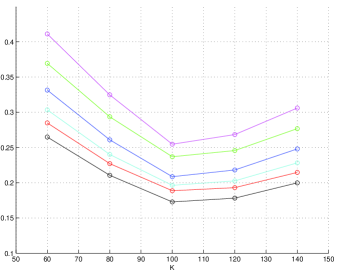

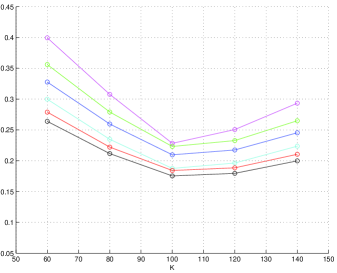

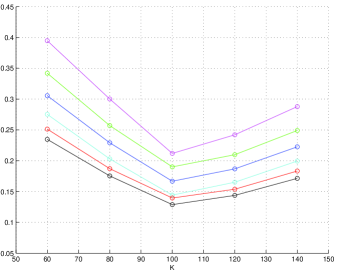

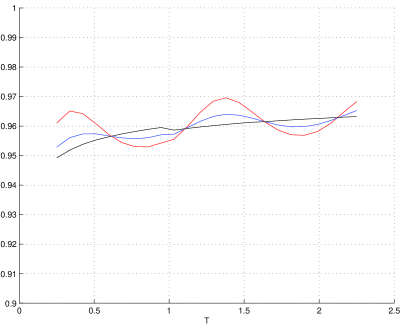

Table 3 presents, for different magnitudes of seasonality, calendar spread option prices obtained with the two-factor model. Case 1 corresponds to the model without seasonality, Case 2 corresponds to a moderate seasonality and Case 3 to a stronger seasonality. The model parameters for these three cases are shown in Table 4. Figure 6 plots the implied correlation term-structures obtained from calendar spread options in the considered cases.

Prices presented in Table 3 show the effect of seasonality on calendar spread options. Irrespective of the strike, prices are increasing with the seasonality magnitude for the two maturities before and at a multiple of and decreasing for the two maturities after a multiple of .

Figure 6 shows that seasonality has a noticeable effect on the implied correlation term-structure for calendar spread options. Compared to the non-seasonal case, implied correlations are higher for maturities before a multiple of and lower for maturities after a multiple of .

| Case 1: no seasonality | Case 2: moderate seasonality | Case 3: strong seasonality | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| parameters | Case 1 | Case 2 | Case 3 |

|---|---|---|---|

7 Conclusion

We introduce a multi-factor seasonal stochastic volatility model for futures contracts that is capable of reproducing the Samuelson effect. We show that the model can accommodate very general specifications of the seasonality functions, including only piece-wise continuous ones. As an illustration, we suggest five different seasonality functions, some of which are familiar from the literature, and provide details of how to incorporate these into the joint characteristic function of the model in a numerically fast and efficient way.

In a series of examples, we show that this model can reproduce seasonal implied volatility surfaces of European options on futures contracts. Furthermore, implied correlations calculated from calendar spread option prices also show seasonal patterns. Finally, we demonstrate that the instantaneous correlation between the returns of two futures contracts with different maturities is both stochastic and seasonal, and make a conjecture about the relationship between the magnitudes of the Samuelson damping factors and the effect of the seasonality functions on this correlation.

Appendix A Proofs

In this appendix we prove Propositions 2.1 and 3.1. We also give the proofs of expressions (16) and (19).

Proof of Proposition 2.1.

- (i).

-

(ii).

The comparison result given in Proposition 2.18 of Karatzas and Shreve (1988) establishes a.s. for all under the hypothesis that the drift function is continuous. Now, if has a discontinuity at time , we know from this argument applied to the interval that (a.s.). It then follows from the continuity of the sample paths that (a.s.), and we can apply the argument again to the interval to obtain (a.s.). Since by assumption the set of times where has discontinuities has no limit points, we can proceed in this manner to cover all of .

-

(iii).

The Feller condition for implies the strict positivity a.s. of . The strict positivity of itself therefore follows immediately from (ii).

Proof of Proposition 3.1. The proof is an extension of the proof of Proposition 2.1 of Schneider and Tavin (2015) to the case where the variance mean-reversion level is time-dependent. Going from to leads to changes in two places. The first is in Lemma A.1 of Schneider and Tavin (2015), which needs to be modified as follows.

Lemma A.1

Let be the seasonal mean-reversion level function, and let

be its transform. Then

| (32) |

Proof. Multiplying equation (5) by and then integrating from to gives

| (33) |

Using Itô-integration by parts (see Øksendal (2003)), we also have

| (34) |

Equating the right hand sides of equations (33) and (34) gives

which proves the lemma.

The second change in the proof is due to the appearance of in the generator of the process . As in Schneider and Tavin (2015), let the function be given by

Now satisfies the PDE

| (35) |

with terminal condition

Again, we know from Duffie et al. (2000) that has affine form

| (36) |

with Putting (36) in (35) gives

and collecting the terms with and without leads to the two ODEs

| (37) | ||||

| (38) |

This completes the proof of the proposition.

Note that only appears in the second ODE (38), and that therefore the closed-form expression previously given for in Schneider and Tavin (2015) can still be used. Only the function changes due to the time-dependence of .

Proof of expression (16). Transform of the sinusoidal pattern.

With

| (39) | ||||

| (40) |

A primitive of is

| (41) |

and

| (42) | ||||

| (43) | ||||

| (44) |

Proof of expression (19). Transform of the sawtooth pattern.

With and

| (45) | ||||

| (46) |

The first integral is computed as

| (47) |

The integral involving the floor function can be split, with , as

| (48) |

Noting that for we have

| (49) |

The other part of the term with the floor function can be written, when , as

| (50) |

with and .

When , as , and for so that we have

| (51) |

Gathering the components, the integral involving the floor function can now be written as

| (52) |

Proof of expression (21). Transform of the triangle pattern.

With and

| (53) | ||||

| (54) |

With , the last integral becomes

| (55) |

Two integrals remain to be computed, one on and the other on . To compute the first, one needs to distinguish two cases. When , it can be computed as

| (56) |

and when , it is

| (57) |

with . To compute the other integral, on , one needs first to distinguish two cases. First, when , we have

| (58) |

with and . For , the integral in the sum can be computed as

| (59) | ||||

| (60) | ||||

| (61) |

where . The sum becomes

| (62) |

The integral on is computed, as

| (63) |

with .

The second case is when . In this case, the integral on becomes

| (64) |

Gathering the components now gives the result.

References

- Back et al. (2011) Janis Back, Marcel Prokopczuk, and Markus Rudolf. Seasonal stochastic volatility: Implications for the pricing of commodity options. ICMA Centre Discussion Papers in Finance, June 2011.

- Back et al. (2013) Janis Back, Marcel Prokopczuk, and Markus Rudolf. Seasonality and the valuation of commodity options. Journal of Banking and Finance, 37:273–290, 2013.

- Bakshi and Madan (2000) Gurdip Bakshi and Dilip Madan. Spanning and derivative-security valuation. Journal of Financial Economics, 55(2):205–238, 2000.

- Benhamou et al. (2010) Eric Benhamou, Emmanuel Gobet, and Mohammed Miri. Time dependent Heston model. SIAM Journal on Financial Mathematics, 1(1):289–325, 2010.

- Caldana and Fusai (2013) Ruggero Caldana and Gianluca Fusai. A general closed-form spread option pricing formula. Journal of Banking and Finance, 37(12):4893–4906, December 2013.

- Clark (2014) Iain J. Clark. Commodity Option Pricing: A Practitioner’s Guide. Wiley Finance. Wiley, 2014.

- Clewlow and Strickland (1999a) Les Clewlow and Chris Strickland. Valuing energy options in a one factor model fitted to forward prices. Working Paper, 30 pages, April 1999a.

- Clewlow and Strickland (1999b) Les Clewlow and Chris Strickland. A multi-factor model for energy derivatives. Working Paper, 20 pages, August 1999b.

- Cox et al. (1985) J. C. Cox, J. E. Ingersoll, and S. A. Ross. A theory of the term structure of interest rates. Econometrica, 53:385–408, 1985.

- Duffie et al. (2000) Darrell Duffie, Jun Pan, and Kenneth Singleton. Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68(6):1343–1376, November 2000.

- Geman and Nguyen (2005) Hélyette Geman and Vu-Nhat Nguyen. Soybean inventory and forward curve dynamics. Management Science, 51(7):1076–1091, July 2005.

- Geman and Roncoroni (2006) Hélyette Geman and Andrea Roncoroni. Understanding the fine structure of electricity prices. Journal of Business, 79(3):1225–1261, 2006.

- Heston (1993) Steven Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6(2):327–343, 1993.

- Hull and White (1990) John Hull and Alan White. Pricing interest-rate-derivative securities. The Review of Financial Studies, 3(4):573–592, 1990.

- Hurd and Zhou (2010) T. R. Hurd and Zhuowei Zhou. A Fourier transform method for spread option pricing. SIAM Journal on Financial Mathematics, 1(1):142–157, 2010.

- Karatzas and Shreve (1988) Ioannis Karatzas and Steven E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer, second edition, 1988.

- Lucia and Schwartz (2002) Julio J. Lucia and Eduardo S. Schwartz. Electricity prices and power derivatives: Evidence from the Nordic power exchange. Review of Derivatives Research, 5(1):5–50, 2002.

- Maghsoodi (1996) Yoosef Maghsoodi. Solution of the extended CIR term structure and bond option valuation. Mathematical Finance, 6(1):89–109, January 1996.

- Øksendal (2003) Bernt Øksendal. Stochastic Differential Equations: An Introduction with Applications. Universitext. Springer, sixth edition, 2003.

- Richter and Sørensen (2002) Martin Richter and Carsten Sørensen. Stochastic volatility and seasonality in commodity futures and options: The case of soybeans. Technical report, Copenhagen Business School, 2002. Working Paper, 45 pages.

- Samuelson (1965) Paul A. Samuelson. Proof that properly anticipated prices fluctuate randomly. Industrial Management Review, 6(2):41–49, Spring 1965.

- Schmitz et al. (2013) Adam Schmitz, Zhiguang Wang, and Jung-Han Kimn. Pricing and hedging calendar spread options on agricultural grain commodities. In Proceedings of the NCCC-134 Conference on Applied Commodity Price Analysis, Forecasting, and Market Risk Management. St. Louis, MO, 2013.

- Schneider and Tavin (2015) Lorenz Schneider and Bertrand Tavin. From the Samuelson volatility effect to a Samuelson correlation effect: Evidence from crude oil calendar spread options. Working Paper, February 2015.

- Sørensen (2002) Carsten Sørensen. Modeling seasonality in agricultural commodity futures. Journal of Futures Markets, 22(5):393–426, May 2002.