Confidence Intervals for High-Dimensional Linear Regression: Minimax Rates and Adaptivity

Abstract

Confidence sets play a fundamental role in statistical inference. In this paper, we consider confidence intervals for high dimensional linear regression with random design. We first establish the convergence rates of the minimax expected length for confidence intervals in the oracle setting where the sparsity parameter is given. The focus is then on the problem of adaptation to sparsity for the construction of confidence intervals. Ideally, an adaptive confidence interval should have its length automatically adjusted to the sparsity of the unknown regression vector, while maintaining a prespecified coverage probability. It is shown that such a goal is in general not attainable, except when the sparsity parameter is restricted to a small region over which the confidence intervals have the optimal length of the usual parametric rate. It is further demonstrated that the lack of adaptivity is not due to the conservativeness of the minimax framework, but is fundamentally caused by the difficulty of learning the bias accurately.

keywords:

[class=MSC]keywords:

arXiv:0000.0000 \startlocaldefs \endlocaldefs

T1The research was supported in part by NSF Grants DMS-1208982 and DMS-1403708, and NIH Grant R01 CA127334..

, and

1 Introduction

Driven by a wide range of applications, high-dimensional linear regression, where the dimension can be much larger than the sample size , has received significant recent attention. The linear model is

| (1.1) |

where , , and . Several penalized/constrained minimization methods, including the Lasso [22], Dantzig Selector [11], square-root Lasso [1], and scaled Lasso [21] have been proposed and studied. Under regularity conditions on the design matrix , these methods with a suitable choice of the tuning parameter have been shown to achieve the optimal rate of convergence under the squared error loss over the set of -sparse regression coefficient vectors with where is a constant. That is, there exists some constant such that

| (1.2) |

where denotes the number of the nonzero coordinates of a vector . See, for example, [24, 2, 11, 21]. A key feature of the estimation problem is that the optimal rate can be achieved adaptively with respect to the sparsity parameter .

Confidence sets play a fundamental role in statistical inference and confidence intervals for high-dimensional linear regression have been actively studied recently with a focus on inference for individual coordinates. But, compared to point estimation, there is still a paucity of methods and fundamental theoretical results on confidence intervals for high-dimensional regression. Zhang and Zhang [25] was the first to introduce the idea of de-biasing for constructing a valid confidence interval for a single coordinate . The confidence interval is centered at a low-dimensional projection estimator obtained through bias correction via score vector using the scaled Lasso as the initial estimator. [14, 15, 23] also used de-biasing for the construction of confidence intervals and [23] established asymptotic efficiency for the proposed estimator. All the aforementioned papers [25, 14, 15, 23] have focused on the ultra-sparse case where the sparsity is assumed. Under such a sparsity condition, the expected length of the confidence intervals constructed in [25, 15, 23] is at the parametric rate and the procedures do not depend on the specific value of .

Compared to point estimation where the sparsity condition is sufficient for estimation consistency (see equation (1.2)), the condition for valid confidence intervals is much stronger. There are several natural questions: What happens in the region where ? Is it still possible to construct a valid confidence interval for in this case? Can one construct an adaptive honest confidence interval not depending on ?

The goal of the present paper is to address these and other related questions on confidence intervals for high-dimensional linear regression with random design. More specifically, we consider construction of confidence intervals for a linear functional , where the loading vector is given and with being a constant. Based on the sparsity of , we focus on two specific regimes: the sparse loading regime where , with being a constant; the dense loading regime where satisfying (2.7) in Section 2. It will be seen later that for confidence intervals is a prototypical case for the general functional with a sparse loading , and is a representative case for with a dense loading .

To illustrate the main idea, let us first focus on the two specific functionals and . We establish the convergence rate of the minimax expected length for confidence intervals in the oracle setting where the sparsity parameter is given. It is shown that in this case the minimax expected length is of order for confidence intervals for . An honest confidence interval, which depends on the sparsity , is constructed and is shown to be minimax rate optimal. To the best of our knowledge, this is the first construction of confidence intervals in the moderate-sparse region . If the sparsity falls into the ultra-sparse region , the constructed confidence interval is similar to the confidence intervals constructed in [25, 15, 23]. On the other hand, the convergence rate of the minimax expected length of honest confidence intervals for in the oracle setting is shown to be . A rate-optimal confidence interval that also depends on is constructed. It should be noted that this confidence interval is not based on the de-biased estimator.

One drawback of the constructed confidence intervals mentioned above is that they require prior knowledge of the sparsity . Such knowledge of sparsity is usually unavailable in applications. A natural question is: Without knowing the sparsity , is it possible to construct a confidence interval as good as when the sparsity is known? This is a question about adaptive inference, which has been a major goal in nonparametric and high-dimensional statistics. Ideally, an adaptive confidence interval should have its length automatically adjusted to the true sparsity of the unknown regression vector, while maintaining a prespecified coverage probability. We show that, unlike point estimation, such a goal is in general not attainable for confidence intervals. In the case of confidence intervals for , it is impossible to adapt between different sparsity levels, except when the sparsity is restricted to the ultra-sparse region , over which the confidence intervals have the optimal length of the parametric rate , which does not depend on . In the case of confidence intervals for , it is shown that adaptation to the sparsity is not possible at all, even in the ultra-sparse region .

Minimax theory is often criticized as being too conservative as it focuses on the worst case performance. For confidence intervals for high dimensional linear regression, we establish strong non-adaptivity results which demonstrate that the lack of adaptivity is not due to the conservativeness of the minimax framework. It shows that for any confidence interval with guaranteed coverage probability over the set of sparse vectors, its expected length at any given point in a large subset of the parameter space must be at least of the same order as the minimax expected length. So the confidence interval must be long at a large subset of points in the parameter space, not just at a small number of “unlucky” points. This leads directly to the impossibility of adaptation over different sparsity levels. Fundamentally, the lack of adaptivity is caused by the difficulty in accurately learning the bias of any estimator for high-dimensional linear regression.

We now turn to confidence intervals for general linear functionals. For a linear functional in the sparse loading regime, the rate of the minimax expected length is , where is the vector norm of . For a linear functional in the dense loading regime, the rate of the minimax expected length is , where is the vector norm of . Regarding adaptivity, the phenomena observed in confidence intervals for the two special linear functionals and extend to the general linear functionals. The case of confidence intervals for with a sparse loading is similar to that of confidence intervals for in the sense that rate-optimal adaptation is impossible except when the sparsity is restricted to the ultra-sparse region . On the other hand, the case for a dense loading is similar to that of confidence intervals for : adaptation to the sparsity is not possible at all, even in the ultra-sparse region .

In addition to the more typical setting in practice where the covariance matrix of the random design and the noise level of the linear model are unknown, we also consider the case with the prior knowledge of and . It turns out that this case is strikingly different. The minimax rate for the expected length in the sparse loading regime is reduced from to , and in particular it does not depend on the sparsity . Furthermore, in marked contrast to the case of unknown and , adaptation to sparsity is possible over the full range . On the other hand, for linear functionals with a dense loading , the minimax rates and impossibility for adaptive confidence intervals do not change even with the prior knowledge of and . However, the cost of adaptation is reduced with the prior knowledge.

The rest of the paper is organized as follows: After basic notation is introduced, Section 2 presents a precise formulation for the adaptive confidence interval problem. Section 3 establishes the minimaxity and adaptivity results for a general linear functional with a sparse loading . Section 4 focuses on confidence intervals for a general linear functional with a dense loading . Section 5 considers the case when there is prior knowledge of covariance matrix of the random design and the noise level of the linear model. Section 6 discusses connections to other work and further research directions. The proofs of the main results are given in Section 7. More discussion and proofs are presented in the supplement [3].

2 Formulation for adaptive confidence interval problem

We present in this section the framework for studying the adaptivity of confidence intervals. We begin with the notation that will be used throughout the paper.

2.1 Notation

For a matrix , , , and denote respectively the -th row, -th column, and entry of the matrix , denotes the -th row of excluding the -th coordinate, and denotes the submatrix of excluding the -th column. Let . For a subset , denotes the submatrix of consisting of columns with and for a vector , is the subvector of with indices in and is the subvector with indices in . For a set , denotes the cardinality of . For a vector , denotes the support of and the norm of is defined as for with and . We use to denote the -th standard basis vector in . For , . We use as a shorthand for , as a shorthand for and as a shorthand for . For a matrix and , is the matrix operator norm. In particular, is the spectral norm. For a symmetric matrix , and denote respectively the smallest and largest eigenvalue of . We use and to denote generic positive constants that may vary from place to place. For two positive sequences and , means for all and if and if and , and if and if .

2.2 Framework for adaptivity of confidence intervals

We shall focus in this paper on the high-dimensional linear model with the Gaussian design,

| (2.1) |

where the rows of satisfy , , and are independent of . Both and the noise level are unknown. Let denote the precision matrix. The parameter consists of the signal , the precision matrix for the random design, and the noise level . The target of interest is the linear functional of , where is a pre-specified loading vector. The data that we observe is where for .

For and a given parameter space and the linear functional , denote by the set of all level confidence intervals for over the parameter space ,

| (2.2) |

For any confidence interval , the maximum expected length over a parameter space is defined as

where for confidence interval , denotes its length. For two parameter spaces , we define the benchmark as the infimum of the maximum expected length over among all -level confidence intervals over ,

| (2.3) |

We will write for , which is the minimax expected length of confidence intervals over .

We should emphasize that is an important quantity that measures the degree of adaptivity over the nested spaces . A confidence interval that is (rate-optimally) adaptive over and should have the optimal expected length performance simultaneously over both and while maintaining a given coverage probability over , i.e., such that

Note that in this case . So for two parameter spaces , if then rate-optimal adaptation between and is impossible to achieve.

We consider the following collection of parameter spaces,

| (2.4) |

where and are positive constants. Basically, is the set of all -sparse regression vectors. and are two mild regularity conditions on the design and noise level.

The main goal of this paper is to address the following two questions:

-

1.

What is the minimax length in the oracle setting where the sparsity level is known?

-

2.

Is it possible to achieve rate-optimal adaptation over different sparsity levels?

More specifically, for , is it possible to construct a confidence interval that is adaptive over and in the sense that and

| (2.5) | ||||

We will answer these questions by analyzing the two benchmark quantities and . Both lower and upper bounds will be established. If can be achieved, it means that the confidence interval can automatically adjust its length to the sparsity level of the true regression vector . On the other hand, if , then such a goal is not attainable.

For ease of presentation, we calibrate the sparsity level

and restrict the loading to the set

where is a constant. The minimax rate and adaptivity of confidence intervals for the general linear functional also depends on the sparsity of . We are particularly interested in the following two regimes:

-

1.

The sparse loading regime: with

(2.6) -

2.

The dense loading regime: with

(2.7)

The behavior of the problem is significantly different in these two regimes. We will consider separately the sparse loading regime in Section 3 and the dense loading regime in Section 4.

3 Minimax rate and adaptivity of confidence intervals for sparse loading linear functionals

In this section, we establish the rates of convergence for the minimax expected length of confidence intervals for with a sparse loading in the oracle setting where the sparsity parameter of the regression vector is given. Both minimax upper and lower bounds are given. Confidence intervals for are constructed and shown to be minimax rate-optimal in the sparse loading regime. Finally, we establish the possibility of adaptivity for the linear functional with a sparse loading .

3.1 Minimax length of confidence intervals for in the sparse loading regime

In this section, we focus on the sparse loading regime defined in (2.6). The following theorem establishes the minimax rates for the expected length of confidence intervals for in the sparse loading regime.

Theorem 1.

Suppose that and for some constants and . If belongs to the sparse loading regime (2.6), the minimax expected length for level confidence intervals of over satisfies

| (3.1) |

Theorem 1 is established in two separate steps.

-

1.

Minimax upper bound: we construct a confidence interval such that and for some constant

(3.2) -

2.

Minimax lower bound: we show that for some constant

(3.3)

The minimax lower bound is implied by the adaptivity result given in Theorem 2. We now detail the construction of a confidence interval achieving the minimax rate (3.1) in the sparse loading regime. The interval is centered at a de-biased scaled Lasso estimator, which generalizes the ideas used in [25, 15, 23]. The construction of the (random) length is different from the aforementioned papers as the asymptotic normality result is not valid once .

Let be the scaled Lasso estimator with ,

| (3.4) |

Define

| (3.5) |

where and . The confidence interval is centered at the following de-biased estimator

| (3.6) |

where is the scaled Lasso estimator given in (3.4) and is defined in (3.5). Before specifying the length of the confidence interval, we review the following definition of restricted eigenvalue introduced in [2],

| (3.7) |

Define

| (3.8) |

where is the upper quantile of the standard normal distribution and

| (3.9) |

Define the event

| (3.10) |

The confidence interval for is defined as

| (3.11) |

It will be shown in Section 7 that the confidence interval has the desired coverage property and achieves the minimax length in (3.1).

Remark 1.

In the special case of , the confidence interval defined in (3.11) is similar to the ones based on the de-biased estimators introduced in [25, 15, 23]. The second term in (3.6) is incorporated to reduce the bias of the scaled Lasso estimator . The constrained estimator defined in (3.5) is a score vector such that the variance term is minimized and one component of the bias term is constrained by the tuning parameter . The tuning parameter is chosen as such that lies in the constraint set in (3.5) with overwhelming probability. For defined in (3.9), it will be shown that it is upper bounded by a constant with overwhelming probability.

3.2 Adaptivity of confidence intervals for in the sparse loading regime

We have constructed a minimax rate-optimal confidence interval for in the oracle setting where the sparsity is assumed to be known. A major drawback of the construction is that it requires prior knowledge of , which is typically unavailable in practice. An interesting question is whether it is possible to construct adaptive confidence intervals that have the guaranteed coverage and automatically adjust its length to .

We now consider the adaptivity of the confidence intervals for . In light of the minimax expected length given in Theorem 1, the following theorem provides an answer to the adaptivity question (2.5) for the confidence intervals for in the sparse loading regime.

Theorem 2.

Suppose that and for some constants and . Then

| (3.12) |

for some constant .

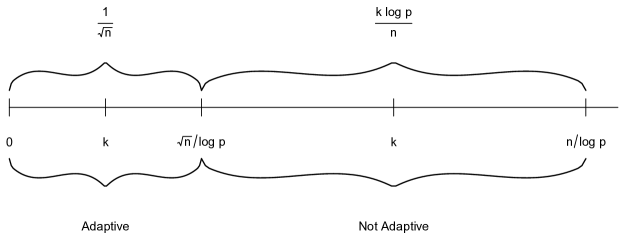

Note that Theorem 2 implies the minimax lower bound in Theorem 1 by taking . Theorem 2 rules out the possibility of rate-optimal adaptive confidence intervals beyond the ultra-sparse region. Consider the setting where and . In this case,

So it is impossible to construct a confidence interval that is adaptive simultaneously over and when and . The only possible region for adaptation is in the ultra-sparse region , over which the optimal expected length of confidence intervals is of order and in particular does not depend on the specific sparsity level. These facts are illustrated in Figure 1.

So far the analysis is carried out within the minimax framework where the focus is on the performance in the worst case over a large parameter space. The minimax theory is often criticized as being too conservative. In the following, we establish a stronger version of the non-adaptivity result which demonstrates that the lack of adaptivity for confidence intervals is not due to the conservativeness of the minimax framework. The result shows that for any confidence interval , under the coverage constraint that , its expected length at any given must be of order So the confidence interval must be long at a large subset of points in the parameter space, not just at a small number of “unlucky” points.

Theorem 3.

Suppose that and for some constants and . Let and for some constant . Then for any and ,

| (3.13) |

for some constant .

3.3 Minimax rate and adaptivity of confidence intervals for

We now turn to the special case , which has been the focus of several previous papers [25, 14, 15, 23]. Without loss of generality, we consider , the first coordinate of , in the following discussion and the results for any other coordinate are the same. The linear functional is the special case of linear functional of sparse loading regime with .

Theorem 1 implies that the minimax expected length for level confidence intervals of over satisfies

| (3.14) |

In the ultra-sparse region with , the minimax expected length is of order . However, when falls in the moderate-sparse region , the minimax expected length is of order and in this case . Hence the confidence intervals constructed in [25, 14, 15, 23], which are of parametric length , asymptotically have coverage probability going to 0. The condition is necessary for the parametric rate . [23] established asymptotic normality and asymptotic efficiency for a de-biased estimator under the sparsity assumption . Similar results have also been given in [19] for a related problem of estimating a single entry of a -dimensional precision matrix based on i.i.d. samples under the same sparsity condition . It was also shown that is necessary for the asymptotic normality and asymptotic efficiency results.

The following corollary, as a special case of Theorem 3, illustrates the strong non-adaptivity for confidence intervals of when .

Corollary 1.

Suppose that and for some constants and . Let for some constant . Then for any ,

| (3.15) |

for some constant

4 Minimax rate and adaptivity of confidence intervals for dense loading linear functionals

We now turn to the setting where the loading is dense in the sense of (2.7). We will also briefly discuss the special case and the computationally feasible confidence intervals.

4.1 Minimax length of confidence intervals for in the dense loading regime

The following theorem establishes the minimax length of confidence intervals of in the dense loading regime (2.7).

Theorem 4.

Suppose that and for some constants and . If belongs to the dense loading regime (2.7), the minimax expected length for level confidence intervals of over satisfies

| (4.1) |

Note that the minimax rate in (4.1) is significantly different from the minimax rate for the sparse loading case given in Theorem 1. In the following, we construct a confidence interval achieving the minimax rate (4.1) in the dense loading regime. Define

| (4.2) |

It will be shown that is upper bounded by a constant with overwhelming probability. The confidence interval is defined to be,

| (4.3) |

where is defined in (3.10) and is the scaled Lasso estimator defined in (3.4) and

| (4.4) |

The confidence interval constructed in (4.3) will be shown to have the desired coverage property and achieve the minimax length in (4.1). A major difference between the construction of and that of is that is not centered at a de-biased estimator. If a de-biased estimator is used for the construction of confidence intervals for with a dense loading, its variance would be too large, much larger than the optimal length .

4.2 Adaptivity of confidence intervals for in the dense loading regime

In this section, we investigate the possibility of adaptive confidence intervals for in the dense loading regime. The following theorem leads directly to an answer to the adaptivity question (2.5) for confidence intervals for in the dense loading regime.

Theorem 5.

Suppose that and for some constants and . Then, for some constant ,

| (4.5) |

Theorem 5 implies the minimax lower bound in Theorem 4 by taking . If (4.5) implies

| (4.6) |

which shows that rate-optimal adaptation over two different sparsity levels and is not possible at all for any . In contrast, in the case of the sparse loading regime, Theorem 2 shows that it is possible to construct an adaptive confidence interval in the ultra-sparse region , although adaptation is not possible in the moderate-sparse region .

Similarly to Theorem 3, the following theorem establishes the strong non-adaptivity results for in the dense loading regime.

Theorem 6.

Suppose that and for some constants and . Let satisfies (2.7) and for some positive constant . Then for any and , there is some constant such that

| (4.7) |

4.3 Minimax length and adaptivity of confidence intervals for

We now turn to to the special case of , the sum of all coefficients. Theorem 4 implies that the minimax expected length for level confidence intervals of over satisfies

| (4.8) |

The following impossibility of adaptivity result for confidence intervals for is a special case of Theorem 6.

Corollary 2.

Suppose that and for some constants and . Let for some constant . Then for any ,

| (4.9) |

for some constant .

Remark 2.

In the Gaussian sequence model, the problem of estimating the sum of sparse means has been considered in [5, 7] and more recently in [12]. In particular, minimax rate is given in [5] and [12]. The problem of constructing minimax confidence intervals for the sum of sparse normal means was studied in [6].

4.4 Computationally feasible confidence intervals

A major drawback of the minimax rate-optimal confidence intervals given in (3.11) and given in (4.3) is that they are not computationally feasible as both depend on restricted eigenvalue , which is difficult to evaluate. In this section, we assume the prior knowledge of the sparsity and discuss how to construct a computationally feasible confidence interval.

The main idea is to replace the term involved with restricted eigenvalue by a computationally feasible lower bound function defined by

| (4.10) |

The lower bound relation is established by Lemma 13 in the supplement [3], which is based on the concentration inequality for Gaussian design in [18]. Except for and , all terms in (4.10) are based on the data and the prior knowledge of . To construct a data-dependent computationally feasible confidence interval, we make the following assumption,

| (4.11) |

where and is a pre-specified parameter space for and denotes the probability distribution with respect to .

Remark 3.

We assume is a subspace of the precision matrix defined in (2.4), . By assuming is the set of precision matrix of special structure, we can find estimators satisfying (4.11). If is assumed to be the set of sparse precision matrix, we can estimate the precision matrix by CLIME estimator proposed in [4]. Under proper sparsity assumption on , the plugin estimator satisfies (4.11). Other special structures can also be assumed, for example, the covariance matrix is sparse. We can use the plugin estimator of the estimator proposed in [10].

5 Confidence intervals for linear functionals with prior knowledge and

We have so far focused on the setting where both the precision matrix and the noise level are unknown, which is the case in most statistical applications. It is still of theoretical interest to study the problem when and are known. It is interesting to contrast the results with the ones when and are unknown. In this case, we consider the setting where it is known a priori that and and specify the parameter space as

| (5.1) |

We will discuss separately the minimax rates and adaptivity of confidence intervals for the linear functionals in the sparse loading regime and dense loading regime over the parameter space .

5.1 Confidence intervals for linear functionals in the sparse loading regime

The following theorem establishes the minimax rate of confidence intervals for linear functionals in the sparse loading regime when there is prior knowledge that and .

Theorem 7.

Suppose that and for some constants and . If belongs to the sparse loading regime (2.6), the minimax expected length for level confidence intervals of over satisfies

| (5.2) |

Compared with the minimax rate for the unknown and case given in Theorem 1, the minimax rate in (5.2) is significantly different. With the prior knowledge of and , the above theorem shows that the minimax expected length of confidence intervals for is always of parametric rate and in particular does not depend on the sparsity parameter . In this case, adaptive confidence intervals for is possible over the full range . A similar result for confidence intervals covering all has been given in a recent paper [16]. The focus of [16] is on individual coordinates, not general linear functionals.

The minimax lower bound of Theorem 7 follows from the parametric lower bound of Theorem 1. As both and are known, the upper bound analysis is easier than the unknown and case and is similar to the one given in [16]. For completeness, we detail the construction of a confidence interval achieving the minimax length in (5.2) using the de-biasing method. We first randomly split the samples into two subsamples and with sample sizes and , respectively. Without loss of generality, we assume that is even and . Let denote the Lasso estimator defined based on the sample with the proper tuning parameter ,

| (5.3) |

We define the following estimator of ,

| (5.4) |

Based on the estimator, we construct the following confidence interval

| (5.5) |

where with . It will be shown in the supplement [3] that the confidence interval proposed in (5.5) has valid coverage and achieves the minimax length in (5.2).

5.2 Confidence intervals for linear functionals in the dense loading regime

In marked contrast to the sparse loading regime, the prior knowledge of and does not improve the minimax rate in the dense loading regime. That is, Theorem 4 remains true by replacing and with and , respectively. However, the cost of adaptation changes when there is prior knowledge of and . The following theorem establishes the adaptivity lower bound in the dense loading regime.

Theorem 8.

Suppose that and for some constants and , then, for some constant ,

| (5.6) |

6 Discussion

In the present paper we studied the minimaxity and adaptivity of confidence intervals for general linear functionals with a sparse or dense loading for the setting where and are unknown as well as the setting with the prior knowledge of and . In the more typical case in practice where and are unknown, the adaptivity results are quite negative: With the exception of the ultra-sparse region for confidence intervals for with a sparse loading , it is necessary to know the true sparsity in order to have guaranteed coverage probability and rate-optimal expected length. In contrast to estimation, knowledge of the sparsity is crucial to constructing honest confidence intervals. In this sense, the problem of constructing confidence intervals is much harder than the estimation problem.

The case of known and is strikingly different. The minimax expected length in the sparse loading regime is of order and in particular does not depend on and adaptivity can be achieved over the full range of sparsity . So in this case, the knowledge of and is very useful. On the other hand, in the dense loading regime the information on and is of limited use. In this case, the minimax rate and lack of adaptivity remain unchanged, compared with the unknown and case, although the cost of adaptation is reduced.

Regarding the construction of confidence intervals, there is a significant difference between the sparse and dense loading regimes. The de-biasing method is useful in the sparse loading regime since such a procedure reduces the bias but does not dramatically increase the variance. However, the de-biasing construction is not applicable to the dense loading regime since the cost of obtaining a near-unbiased estimator is to significantly increase the variance which would lead to an unnecessarily long confidence interval. An interesting open problem is the construction of a confidence interval for achieving the minimax length where the sparsity of the loading is in the middle regime with for some .

In addition to constructing confidence intervals for linear functionals, another interesting problem is constructing confidence balls for the whole vector . Such has been considered in [17], where the authors established the impossibility of adaptive confidence balls for sparse linear regression. These problems are connected, but each has its own special features and the behaviors of the problems are different from each other. The connections and differences in adaptivity among various forms of confidence sets have also been observed in nonparametric function estimation problems. See, for example, [6] for adaptive confidence intervals for linear functionals, [13, 9] for adaptive confidence bands, and [8, 20] for adaptive confidence balls.

In the context of nonparametric function estimation, a general adaptation theory for confidence intervals for an arbitrary linear functional was developed in Cai and Low [6] over a collection of convex parameter spaces. It was shown that the key quantity that determines adaptivity is a geometric quantity called the between-class modulus of continuity. The convexity assumption on the parameter space in Cai and Low [6] is crucial for the adaptation theory. In high-dimensional linear regression, the parameter space is highly non-convex. The adaptation theory developed in [6] does not apply to the present setting of high-dimensional linear regression. It would be of significant interest to develop a general adaptation theory for confidence intervals in such a non-convex setting.

7 Proofs

In this section, we prove two main results, Theorem 3 and minimax upper bound of Theorem 1. For reasons of space, the proofs of the other results are given in the supplement [3].

A key technical tool for the proof of the lower bound results is the following lemma which establishes the adaptivity over two nested parameter spaces. Such a formulation has been considered in [6] in the context of adaptive confidence intervals over convex parameter spaces under the Gaussian sequence model. However, the parameter space considered in the high dimension setting is highly non-convex. The following lemma can be viewed as a generalization of [6] to the non-convex parameter space, where the lower bound argument requires testing for composite hypotheses.

Suppose that we observe a random variable which has a distribution where the parameter belongs to the parameter space . Let be the confidence interval for the linear functional with the guaranteed coverage over the parameter space . Let and be subsets of the parameter space where . Let denote the prior distribution supported on the parameter space for . Let denote the density function of the marginal distribution of with the prior on for . More specifically,

Denote by the marginal distribution of with the prior on for . For any function , we write for the expectation of with respect to the marginal distribution of with the prior on . We define the distance between two density functions and by

| (7.1) |

and the total variation distance by It is well known that

| (7.2) |

Lemma 1.

Assume for and for and For any ,

| (7.3) |

7.1 Proof of Lemma 1

The supremum risk over is lower bounded by the Bayesian risk with the prior on ,

| (7.4) |

By the definition of we have

| (7.5) |

for . By the following inequality

then we have This together with yields which leads to Hence, The lower bound follows from inequality

7.2 Proof of Theorem 3

The lower bound in (3.13) is involved with a parametric term and a non-parametric term. The proof of the parametric lower bound is postponed to the supplement. In the following, we will prove the non-parametric lower bound

| (7.6) |

for some constant . Without loss of generality, we assume . We generate the orthogonal matrix such that its first row is and define the orthogonal matrix as . We transform both the design matrix and the regression vector and view the linear model (2.1) as where and . The transformed coefficient vector is of sparsity at most . The first coefficient of is . The covariance matrix of is and its corresponding precision matrix is To represent the transformed observed data and parameter, we abuse the notation slightly and also use and . We define the parameter space of as

| (7.7) |

For a given , there exists a bijective mapping between and . To show that , it is equivalent to show . Let denote the set of confidence intervals for with guaranteed coverage over . If , then ; If , then . Because of such one to one correspondence, we have

| (7.8) |

By (7.6) and (7.8), we reduce the problem to

| (7.9) |

Under the Gaussian random design model, follows a joint Gaussian distribution with mean . Let denotes the covariance matrix of . Decompose into blocks where , and denote the variance of , the variance of and the covariance of and , respectively. We define the function as . The function is bijective and its inverse mapping is

The null space is taken as and denotes the point mass prior at this point. The proof is divided into three steps:

-

1.

Construct and show that ;

-

2.

Control the distribution distance ;

-

3.

Calculate the distance where and with . We show that is a fixed constant for all and then apply Lemma 1.

Step 1. We construct the alternative hypothesis parameter space . Let denote the covariance matrix of corresponding to . Let and . Let denote the size of and denote the size of and we have and . Without loss of generality, let . We have the following expression for the covariance matrix of under the null,

| (7.10) |

To construct , we define the following set,

| (7.11) |

Define the parameter space for by , where

| (7.12) |

Then we construct the alternative hypothesis space for , which is induced by the mapping and the parameter space ,

| (7.13) |

In the following, we show that . It is necessary to identify for and show . Firstly, we identify the expression under the alternative joint distribution (7.12). Assuming we have

| (7.14) |

and

| (7.15) |

Based on , the sparsity of in the alternative hypothesis space is upper bounded by and hence the sparsity of the corresponding is controlled by

| (7.16) |

Secondly, we show that satisfies the condition The covariance matrix of in the alternative hypothesis parameter space is expressed as

| (7.17) |

Since the second matrix on the above equation is of spectral norm , Weyl’s inequality leads to When is chosen such that then we have Since and have the same eigenvalues, we have . Combined with (7.15) and (7.16), we show that .

Step 2. To control , it is sufficient to control and apply (7.2). Let denote the uniform prior on over . Note that this uniform prior induces a prior distribution over the parameter space . Let denote the expectation with respect to the independent random variables with uniform prior over the parameter space . The following lemma controls the distance between the null and the mixture over the alternative distribution.

Lemma 2.

Let . Then

| (7.18) |

The following lemma is useful in controlling the right hand side of (7.18).

Lemma 3.

Let be a variable with then

| (7.19) |

7.3 Proof of upper bound in Theorem 1

The following propostion establishes the coverage property and the expected length of the constructed confidence interval constructed in (3.11). Such a confidence interval achieves the minimax length in (3.1).

Proposition 1.

Suppose that where is a small positive constant, then

| (7.21) |

and

| (7.22) |

for some constant .

In the following, we are going to prove Proposition 1. By normalizing the columns of and the true sparse vector , the linear regression model can be expressed as

| (7.23) |

where

| (7.24) |

denotes the diagonal matrix with entry to be . Take and , and we have Take , , , and . Rather than use the constants directly in the following discussion, we use and to represent the above fixed constants in the following discussion. We also assume that and Define the cone invertibility factor () as follows,

| (7.25) |

where is an index set. Define

| (7.26) |

To facilitate the proof, we define the following events for the random design and the error ,

Define and The following lemmas control the probability of events , and . The detailed proofs of Lemma 4, 7.31 and 6 are in the supplement.

Lemma 4.

| (7.27) |

and

| (7.28) |

where and are universal positive constants. If , then

| (7.29) |

where and are universal positive constants and .

The following lemma establishes a data-dependent upper bound for the term .

Lemma 5.

On the event ,

| (7.30) |

where

| (7.31) |

The following lemma controls the radius of the confidence interval.

Lemma 6.

On the event , there exists such that if ,

| (7.32) |

and

| (7.33) |

In the following, we establish the coverage property of the proposed confidence interval. By the definition of in (3.6), we have

| (7.34) |

We now construct a confidence interval for the variance term by normal distribution and a high probability upper bound for the bias term . Since is independent of and and is a function of , we have and

By (7.34), we have where

Integrating with respect to , we have

| (7.35) |

Since on the event , Lemma 7.31 and the constraint in (3.5) lead to

| (7.36) |

where is defined in (7.31). On the event , we also have and We define the following confidence interval to facilitate the discussion, where On the event , we have

| (7.37) |

On the event , if , then . Hence, the event holds and . By Lemma 6, on the event , if , we have and hence

| (7.38) |

We have the following bound on the coverage probability,

where the first inequality follows from (7.37) and (7.38) and the first equality follows from (7.35). Combined with Lemma 4, we establish (7.21). We control the expected length as follows,

| (7.39) | ||||

where the first inequality follows from (7.32) and second inequality follows from Lemma 4. If , then and hence

Acknowledgements

The authors thank Zhao Ren for the discussion on the confidence intervals for linear functionals with sparse loadings. {supplement} \stitleSupplement to “Confidence Intervals for High-Dimensional Linear Regression: Minimax Rates and Adaptivity”. \slink[url]http://www-stat.wharton.upenn.edu/tcai/paper/CI-Reg-Supplement.pdf \sdescription Detailed proofs of the adaptivity lower bound and minimax upper bound for confidence intervals of the linear functional with a dense loading are given. The minimax rates and adaptivity of confidence intervals of the linear functional are established when there is prior knowledge that and . Extra propositions and technical lemmas are also proved in the supplement.

References

- [1] Alexandre Belloni, Victor Chernozhukov, and Lie Wang. Square-root lasso: pivotal recovery of sparse signals via conic programming. Biometrika, 98(4):791–806, 2011.

- [2] Peter J Bickel, Ya’acov Ritov, and Alexandre B Tsybakov. Simultaneous analysis of lasso and dantzig selector. The Annals of Statistics, 37(4):1705–1732, 2009.

- [3] T Tony Cai and Zijian Guo. Supplement to “confidence intervals for high-dimensional linear regression: Minimax rates and adaptivity”. 2015.

- [4] T Tony Cai, Weidong Liu, and Xi Luo. A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106(494):594–607, 2011.

- [5] T Tony Cai and Mark G Low. Minimax estimation of linear functionals over nonconvex parameter spaces. The Annals of statistics, 32(2):552–576, 2004.

- [6] T Tony Cai and Mark G Low. An adaptation theory for nonparametric confidence intervals. The Annals of statistics, 32(5):1805–1840, 2005.

- [7] T Tony Cai and Mark G Low. On adaptive estimation of linear functionals. The Annals of Statistics, 33(5):2311–2343, 2005.

- [8] T Tony Cai and Mark G Low. Adaptive confidence balls. The Annals of Statistics, 34(1):202–228, 2006.

- [9] T Tony Cai, Mark G Low, and Zongming Ma. Adaptive confidence bands for nonparametric regression functions. Journal of the American Statistical Association, 109:1054–1070, 2014.

- [10] T Tony Cai and Harrison H Zhou. Optimal rates of convergence for sparse covariance matrix estimation. The Annals of Statistics, 40(5):2389–2420, 2012.

- [11] Emmanuel Candès and Terence Tao. The dantzig selector: statistical estimation when p is much larger than n. The Annals of Statistics, 35(6):2313–2351, 2007.

- [12] Olivier Collier, La titia Comminges, and Alexandre B. Tsybakov. Minimax estimation of linear and quadratic functionals on sparsity classes. arXiv preprint arXiv:1502.00665, 2015.

- [13] Marc Hoffmann and Richard Nickl. On adaptive inference and confidence bands. The Annals of Statistics, 39(5):2383–2409, 2011.

- [14] Adel Javanmard and Alessandro Montanari. Hypothesis testing in high-dimensional regression under the gaussian random design model: Asymptotic theory. Information Theory, IEEE Transactions on, 60(10):6522–6554, 2014.

- [15] Adel Javanmard and Andrea Montanari. Confidence intervals and hypothesis testing for high-dimensional regression. The Journal of Machine Learning Research, 15(1):2869–2909, 2014.

- [16] Adel Javanmard and Andrea Montanari. De-biasing the lasso: Optimal sample size for gaussian designs. arXiv preprint arXiv:1508.02757, 2015.

- [17] Richard Nickl and Sara van de Geer. Confidence sets in sparse regression. The Annals of Statistics, 41(6):2852–2876, 2013.

- [18] Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Restricted eigenvalue properties for correlated gaussian designs. The Journal of Machine Learning Research, 11:2241–2259, 2010.

- [19] Zhao Ren, Tingni Sun, Cun-Hui Zhang, and Harrison H Zhou. Asymptotic normality and optimalities in estimation of large gaussian graphical model. arXiv preprint arXiv:1309.6024, 2013.

- [20] James Robins and Aad Van Der Vaart. Adaptive nonparametric confidence sets. The Annals of Statistics, 34(1):229–253, 2006.

- [21] Tingni Sun and Cun-Hui Zhang. Scaled sparse linear regression. Biometrika, 101(2):269–284, 2012.

- [22] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), 58(1):267–288, 1996.

- [23] Sara van de Geer, Peter Bühlmann, Ya acov Ritov, and Ruben Dezeure. On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202, 2014.

- [24] Nicolas Verzelen. Minimax risks for sparse regressions: Ultra-high dimensional phenomenons. Electronic Journal of Statistics, 6:38–90, 2012.

- [25] Cun-Hui Zhang and Stephanie S Zhang. Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242, 2014.