Second-Order Cone Programming for P-Spline Simulation Metamodeling

Abstract

This paper approximates simulation models by B-splines with a penalty on high-order finite differences of the coefficients of adjacent B-splines. The penalty prevents overfitting. The simulation output is assumed to be nonnegative. The nonnegative spline simulation metamodel is casted as a second-order cone programming model, which can be solved efficiently by modern optimization techniques. The method is implemented in MATLAB/GNU Octave.

1 Introduction

People use computer simulation to study complex systems that prohibit analytical evaluations, in order to have a basic understanding of the system, or to find robust decisions or policies, or to compare different decisions or policies [20]. Simulation is applied in various areas [4, 23, 27], and it is considered as one of the three most important operations research techniques [22]. Let represent the response and represent the input of a system. A simulation model can then be written as

In situations where the systems are so complex that even their valid simulation models can’t be evaluated in reasonable time, metamodels, or models of models [19], are constructed to approximate the simulation models. Advantages of the simulation metamodel include “model simplification, enhanced exploration and interpretation of the model, generalization to other models of the same type, sensitivity analysis, optimization, answering inverse questions, and providing the researcher with a better understanding of the behaviour of the system under study and the interrelationships among the variables” [15].

Parametric polynomial response surface approximation is the most popular technique for building metamodels [5]. To determine and quantify the unknown or too complex relationship between the response variables and the experimental factors assumed to influence the response, in response surface methodolgy – introduced by Box and Wilson [6], a mathematical model is constructed to fit the data collected from a series of experiments, and the optimal settings of the experimental factors is determined [7, 17, 25]. Usually the mathematical model is a first or second order polynomial, called a response surface.

By Weierstrass approximation theorem, every continuous function can be uniformly approximated as closely as desired by a polynomial. Polynomials are easy to compute and have continuous derivatives of all orders. On the other hand, polynomials are inflexible: their values on a complex plane are determined by an arbitrarily small set [35, Theorem 3.23]; they oscillate increasingly with the increase in the order of the polynomials, while high-order is required for suitable accuracy in polynomial approximation; the Runge phenomenon [31] is the classic example of divergent polynomial interpolation. A polynomial fits data nicely near one data point may display repulsive features at parts of the curve not close to that particular data point.

Approximation by splines (smooth piecewise polynomials) overcomes the inflexibility of polynomial approximation. In practice, B-Splines, which are first thoroughly studied by [33], are widely used in approximation, as there are good properties associated with B-splines [10]. Especiallarly, compared with representations by splines in truncated power basis—defined as for node , B-spline representations are relatively well-conditioned and involve fewer basis functions computationally. Let be a nondecreasing sequence. The th (normalized) B-spline basis function of order for the knot sequence is defined as follows:

When it can be inferred from the context, the knots and variable are omitted in the notations for B-spline representations. Denote

For , the th B-Spline basis function of order for knot sequence can be obtained recursively by:

| (1) |

The spline basis function depends only on the knots . It is positive on the interval and is zero elsewhere. The Curry-Schoenberg Theorem [8] describes how to construct B-spline basis for the linear space of piecewise polynomial functions satisfying predefined continuity conditions based on the muliplicity of the knots. This property simplifies the approximation of functions with required degree of smoothness, compared with truncated power spline approximation, where additional constraints on smoothness need to be included in the model. The de Boor algorithm [9] is a well-conditioned yet efficient way of evaluating B-splines.

P-Spline approximation.

To fit the metamodel with data collected from experiments, i.e., to find the parameters for the B-spline approximation, we conside P-spline regression [14]. The objective function of a P-spline regression combines B-splines with a penalty on high-order finite differences of the coefficients of adjacent B-splines. Similar to the smoothing term in the loss function for smoothing spline regression [30, 34], the penalty in P-spline regression loss function prevents overfitting, i.e., the penalty reduces the variation of the fitted curve caused by data error. Compared with smoothing splines, P-splines are relatively inexpensive to compute and without the complexity of choosing the optimal number and positions of knots — too few data points causes under fitting while too many data points results in overfitting. An algorithm of determining the number of knots for P-spline regression is given in [32].

Let represent the B-spline coefficients. The second-order differences of the adjacent B-spline coefficients for the knot sequence are

Denote the parameter controlling the smoothness of the fit by . The least squares objective function (loss function) of the regression of data points using B-spline basis functions of order four with a penalty on second-order differences of the B-spline coefficients, i.e. the P-spline regression loss function for fitting the metamodel studied in this paper, is

| (2) |

Nonnegative model fitting.

In many applications, the response of the system is known or required to be nonnegative or above some threshold; for instance, when the output of the system describes duration, productions, prices, demand, sales, wages, amount of precipitation, probability mass, etc; see [3, 28]). Because of the noisy or tendency in the data, quite often, the fitted curve doesn’t exhibit nonnegativitiy, even though it should be. For instance, let be the monthly precipitation amount at some region, where is the variable for months and is the rain fall amount. The rain fall amount may be decreasing during some period till at some months there is little or no rain, then it may increase again. Because of the increase and decrease trend before and after these certain months, the fitted curve may have negative values at these points for [29]. Even if the data points are nonnegative, without imposing the nonnegativity constraints, the resulting models may take negative values at some areas [38]. In [3] a numerical example of cubic spline approximation of arrival-rate for an e-mail data set shows that the maximum likelihood spline takes negative values in a significant time period with all positive data points, and the estimation problem may even be unbounded and thus ill-posed.

To obtain a satisfiable and sometimes meaningful model, the nonnegativity constraint on the output needs to be imposed on the regression. The nonnegative cubic spline approximation in truncated power basis is considered in [3]. Constrained smoothing spline approximation is studied in [37], but they acknowledge the computational difficulty in their approach. Since the B-spline basis functions are nonnegative, imposing positivity on B-spline coefficients [16] or integrating B-splines with positive coefficients (I-spline [28]) preserves positivity in regression. But this approach excludes some classes of positive splines and thus reduces the accuracy of the regression. It is proved in [11] that errors in approximation of nonnegative functions by B-splines of order (degree ) with nonnegative coefficients are bigger in magnitude compared with errors in approximation by nonnegative splines of the same order, and the difference between the magnitudes of the errors increases with the order of the splines. The two approximation schemes give errors of the same magnitude only if , i.e. approximation by piece wise constant or piece wise linear functions. Because of the approximation and computational advantage of P-splines, this paper focuses on nonnegative P-spline approximation.

To simplify notation, in this paper, we concatenate vectors row wise by ‘,’ and concatenate vectors column wise by ’;’; for instance, the adjoining of vectors , , and can be represented as

2 Nonnegative Cubic Polynomials

In the context below, matrices are represented by capital letters: , where the element of matrix at both of its th row and th column is denoted as . Let represent the symmetric matrix being positive semidefinite. For two matrices and of the same size, let denote their Hadamard product:

By Markov-Lukacs theorem [26], a cubic polynomial is nonnegative on the interval if and only if there exist such that can be represented as

Denote

Then by [26, Theorem 1], the above representation is equivalent to: existing , such that

Because is equivalent to: , is nonnegative on if and only if there exist such that

| (3) |

3 Nonnegative Representations By B-Splines Of Order Four

Based on the definition of B-spline basis functions (1), the th B-spline basis function of order three for knot sequence is

And the th B-spline basis function of order four for knot sequence is

Hence, on the interval , the B-spline is

Given a finite knot sequence , define

For and , let denote the coefficient of associated with of the polynomial on the interval .

where for , define and . In other words,

Let for . Then can be represented in terms of as below:

Denote

For equally spaced knot sequence, i.e., , the above expression for can be simplified:

By (3), the B-spline is nonnegative on the interval iff there exist , such that

| (4) |

The model.

Adding constraints (4) to the P-spline regression loss function (2), we obtain the formula for fitting the metamodel:

| (5) |

Variable reduction.

Let denote the column vector containing all : . Denote

Let and denote the column vectors containing all ’s and ’s:

Constraints (4) contain homongenous equations and variables: , , and . By Curry-Schoenberg theorem [8, 10], the sequence , …, is a basis for the linear space of piecewise polynomials of order with break sequence that satisfies continuity condition specified by the multiplicities of the elements of . Since the sub-matrix corresponding to in the coefficient matrix of the constraints (4) is the linear transformation from the B-spline basis to the truncated power function basis, the matrix corresponding to has full column rank.

Lemma 3.1.

The coefficient matrix of the equalities in constraints (4) has rank at least , where is the number of total multiple knots – counted with multiplicities, and is the number of different multiple knots – counted without multiplicities.

Proof.

The submatrix of the coefficent matrix for the equalities in constraints (4) with columns corresponding to and is block diagonal, where the th block is:

The block has rank if , and it has rank if . Since the coefficient matrix of the equalities in constraints (4) has rows, the statement of the lemma follows. ∎

Corollary 3.2.

If all the knots are distinct, then the coefficient matrix of the constraints (4) has full row rank.

Therefore, given a distinct knot sequence , we can use Gauss elimination to represent by , and in the constraints (4). Since each relates to only , , , in constraints (4), we can represent each by at most variables , , , , , .

For equally spaced knot sequences, below are representations of :

For , omitting the subscript of for simplicity, we have

| (6) |

For :

For :

For :

Then we can replace in the objective of (5) by the following relation:

| (7) |

4 Second-Order Cone Programming

Index vectors in from . A second-order cone (quadratic cone, Lorentz cone, or ice-cream cone) in is the set

The rotated quadratic cone is obtained by rotating the second-order cone by 45 degrees in the - plane:

The nonnegative orthant is a one-dimensional second-order cone. Because a second-order cone induces a partial ordering, an -dimensional vector can be represented as . The subscript is sometimes omitted when it is clear from the context.

Second-order cone programming is an extension of linear programming. In second-order cone programming, one minimizes a linear objective function under linear equality constraints and second-order cone constraints where variables are required to be in the second-order cones. Let be vectors not necessarily of the same dimensions. Let and be vectors and be matrices. The standard form second-order cone programming problem is

Second-order cone programming has many applications. A solution to a second-order cone programming problem can be obtained approximately by interior point methods in polynomial time of the problem data size. See [2] for a survey of applications and algorithms of second-order cone programming. In addition, the complexity of an interior point method for second-order cone programming doesn’t depend on the dimension of the second-order cone.

The metamodel fitting problem (5) can be casted as a second-order cone programming problem. Below are two constructions.

Model I

Model II.

The square of the norm of a vector no more than the value of can be represented as a second-order cone constraint:

Therefore, problem (5) can also be formulated as the following second-order cone programming model:

5 Numerical Examples

We have implemented the nonnegative P-spline regression by second-order cone programming in MATLAB / GNU Octave [13].

5.1 Parameter Selection

We use equally spaced knots. For each fixed knot sequence, the smoothness parameter is chosen to minimize the GCV (Generalized Cross-Validation) statistic [32]: Let be the optimal coefficients under parameter . The average squared residuals using for the regression is

Denote as

Then the penalty term in the regression loss function can be represented as . Let denote the design matrix whose th row is

The smoother matrix is defined as

Then the generalized cross validation statistic is

The value measures the effective degrees of freedom of the fit.

The number of knots is determined by the Akaike information theoretical criterion (AIC) [1], i.e, we run the algorithm with different number of knots and choose the number for the model that has the minimum :

5.2 Numerical Examples

The second-order cone programming model is solved via SDPT3-4.0 [36]through the YALMIP interface [24]. YALMIP is a modeling language that models the problems into standard second-order cone programs. SDPT3 and SeDuMi are state of the art software for second-order cone programming. The reformatted SDPT3 and SeDuMi for GNU Octave by Michael Grant are available at the repositories on GitHub.

Below are some numerical examples with MATLAB. Data points are depicted by blue “*”; the B-spline fitted function is the green curve. We tested the method with number of internal knots from to . For each knot sequence, the is chosen to minimize . The values of tested are . The number of knots is determined by minimizing .

Density estimation.

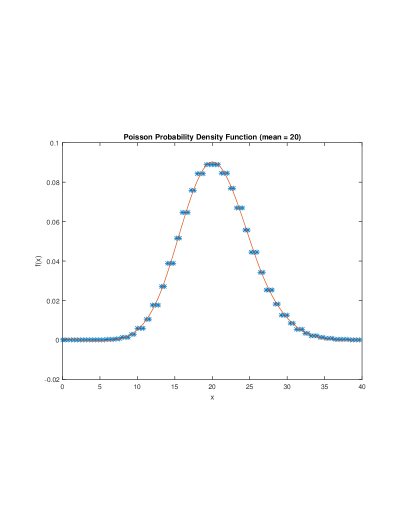

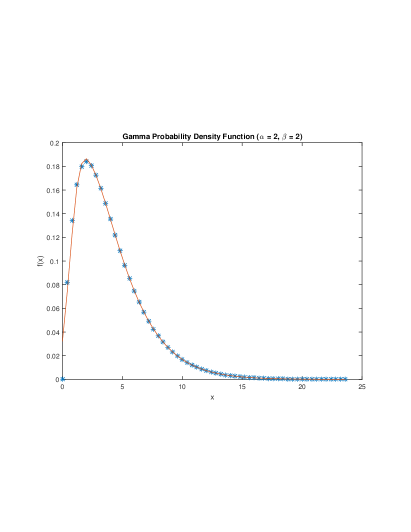

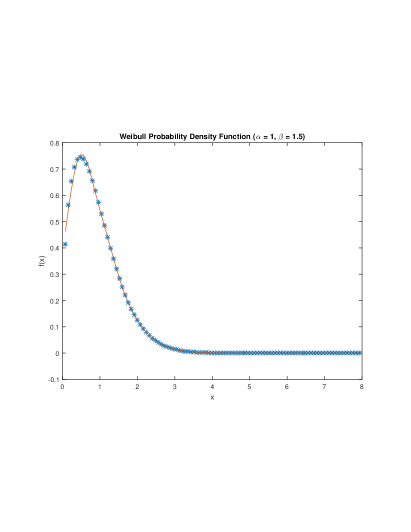

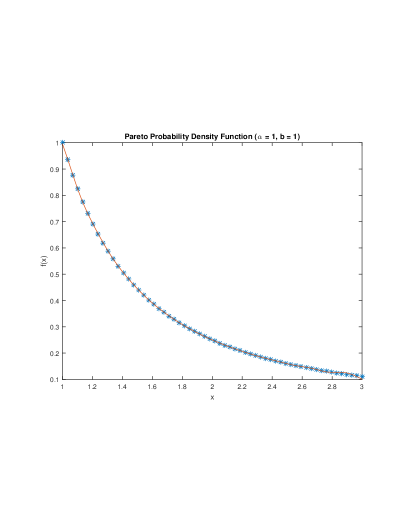

Figure 1 shows the output of our method for density estimation.

For the Poisson probability density function with mean :

based on and , the best model has interior knots and .

For the Gamma probability density function with :

the best model has interior knots and .

For the Weibull probability density function with , :

the best model has interior knots and .

For the Pareto probability density function with , :

the best model has interior knots and .

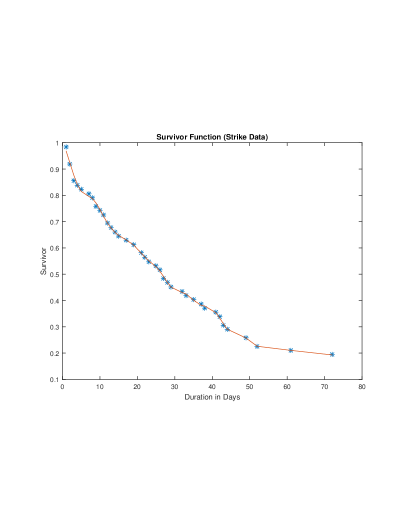

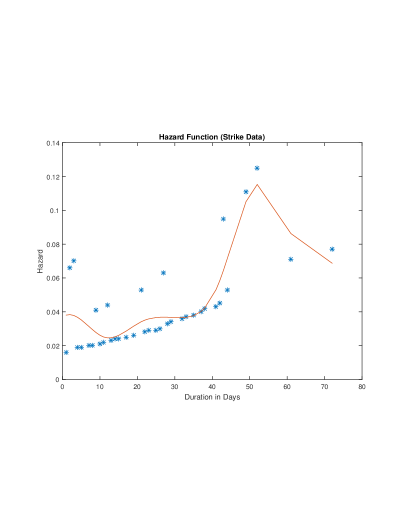

Duration analysis.

Duration analysis [21] studies the spell of an event. Let be the density function of the probability distribution of duration. The survivor function is the probability that the random variable will equal or exceed . The hazard function is the rate at which spells will be completed at .

The data in Figure 2 are strike spells and survivor and hazard estimates from [18]. The duration time are strike lengths in days between 1968 and 1976 involving at least 1,000 works in the U.S. manufacturing industries with major issue.

For the survivor function estimation, the best model has interior knots and ; For the hazard function estimation, the best model has interior knots and ;

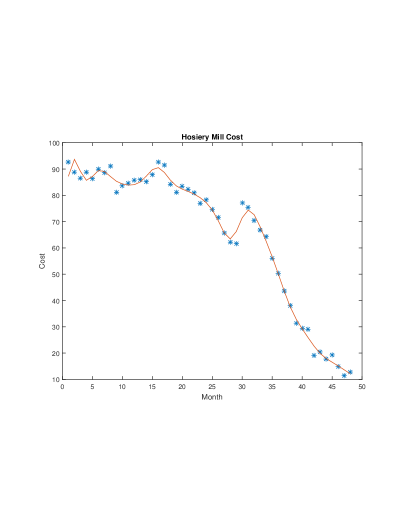

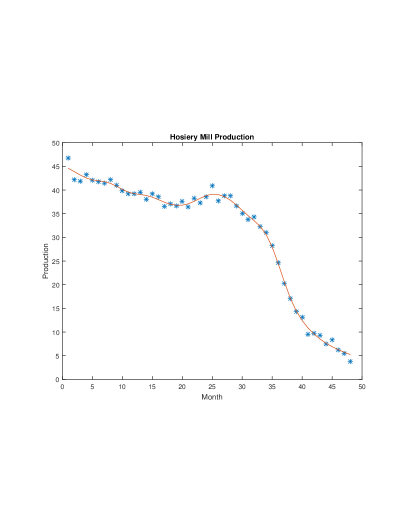

Cost and production.

The data in Figure 3 are the monthly production costs and output for a hosiery mill over a 4-year period from [12]. The production is in thousands of dozens of pairs, and the costs is in thousands of dollars. We downloaded the data from Larry Winner’s web site: \urlhttp://www.stat.ufl.edu/ winner/data/millcost.dat.

For the production data, the best model has interior knots, and . For the cost data, the best model also has interior knots, and .

References

- [1] Hirotogu Akaike. Information theory and an extension of the maximum likelihood principle. In Emanuel Parzen, Kunio Tanabe, and Genshiro Kitagawa, editors, Selected Papers of Hirotugu Akaike, Springer Series in Statistics, pages 199–213. Springer New York, 1998.

- [2] F. Alizadeh and D. Goldfarb. Second-order cone programming. Math. Program., 95(1, Ser. B):3–51, 2003. ISMP 2000, Part 3 (Atlanta, GA).

- [3] Farid Alizadeh, Jonathan Eckstein, Nilay Noyan, and Gábor Rudolf. Arrival rate approximation by nonnegative cubic splines. Oper. Res., 56(1):140–156, 2008.

- [4] Jerry Banks, John S. II Carson, Barry L. Nelson, and David M. Nicol. Discrete-Event System Simulation. Prentice Hall, U.S.A., 2010.

- [5] Russell R. Barton. Simulation metamodels. In Proceedings of the 30th Conference on Winter Simulation, WSC ’98, pages 167–176, Los Alamitos, CA, USA, 1998. IEEE Computer Society Press.

- [6] G. E. P. Box and K. B. Wilson. On the experimental attainment of optimum conditions. Journal of the Royal Statistical Society. Series B (Methodological), 13(1):pp. 1–45, 1951.

- [7] George E. P. Box and Norman R. Draper. Empirical model-building and response surfaces. Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. John Wiley & Sons, Inc., New York, 1987.

- [8] H. B. Curry and I. J. Schoenberg. On Pólya frequency functions. IV. The fundamental spline functions and their limits. J. Analyse Math., 17:71–107, 1966.

- [9] Carl de Boor. On calculating with -splines. J. Approximation Theory, 6:50–62, 1972. Collection of articles dedicated to J. L. Walsh on his 75th birthday, V (Proc. Internat. Conf. Approximation Theory, Related Topics and their Applications, Univ. Maryland, College Park, Md., 1970).

- [10] Carl de Boor. A practical guide to splines, volume 27 of Applied Mathematical Sciences. Springer-Verlag, New York, revised edition, 2001.

- [11] Carl de Boor and James W. Daniel. Splines with nonnegative -spline coefficients. Math. Comp., 28:565–568, 1974.

- [12] Joel Dean. Statistical Cost Functions of a Hosiery Mill, volume XI, no. 4 of Studies in Business Administration. The School of Business, The University of Chicago, Chicago, IL, U.S.A., 1941.

- [13] John W. Eaton, David Bateman, Søren Hauberg, and Rik Wehbring. GNU Octave version 3.8.1 manual: a high-level interactive language for numerical computations. CreateSpace Independent Publishing Platform, 2014. ISBN 1441413006.

- [14] Paul H. C. Eilers and Brian D. Marx. Flexible smoothing with -splines and penalties. Statist. Sci., 11(2):89–121, 1996. With comments and a rejoinder by the authors.

- [15] Linda Weiser Friedman and Israel Pressman. The metamodel in simulation analysis: Can it be trusted? The Journal of the Operational Research Society, 39(10):pp. 939–948, 1988.

- [16] Xuming He and Peide Shi. Monotone -spline smoothing. J. Amer. Statist. Assoc., 93(442):643–650, 1998.

- [17] André I. Khuri and John A. Cornell. Response surfaces, volume 152 of Statistics: Textbooks and Monographs. Marcel Dekker, Inc., New York, second edition, 1996. Designs and analyses.

- [18] Nicholas Kiefer. Economic duration data and hazard functions. Journal of Economic Literature, 26(2):646–79, 1988.

- [19] Jack P. C. Kleijnen. A comment on blanning’s “metamodel for sensitivity analysis: The regression metamodel in simulation”. Interfaces, 5(3):21–23, 1975.

- [20] Jack P.C. Kleijnen, Susan M. Sanchez, Thomas W. Lucas, and Thomas M. Cioppa. State-of-the-art review: A user’s guide to the brave new world of designing simulation experiments. INFORMS Journal on Computing, 17(3):263–289, 2005.

- [21] Tony Lancaster. The econometric analysis of transition data, volume 17 of Econometric Society Monographs. Cambridge University Press, Cambridge, 1990.

- [22] Michael S. Lane, Ali H. Mansour, and John L. Harpell. Operations research techniques: A longitudinal update 1973–1988. Interfaces, 23(2):63–68, 1993.

- [23] Averill M Law, David M Kelton, and David M Kelton. Simulation modeling and analysis. McGraw-Hill, New York, 2015.

- [24] Johan Löfberg. Yalmip : A toolbox for modeling and optimization in MATLAB. In Proceedings of the CACSD Conference, Taipei, Taiwan, 2004.

- [25] Raymond H. Myers, Douglas C. Montgomery, and Christine M. Anderson-Cook. Response surface methodology. Wiley Series in Probability and Statistics. John Wiley & Sons, Inc., Hoboken, NJ, third edition, 2009. Process and product optimization using designed experiments.

- [26] Yurii Nesterov. Squared functional systems and optimization problems. In High performance optimization, volume 33 of Appl. Optim., pages 405–440. Kluwer Acad. Publ., Dordrecht, 2000.

- [27] J Tinsley Oden, Ted Belytschko, Jacob Fish, TJ Hughes, Chris Johnson, David Keyes, Alan Laub, Linda Petzold, David Srolovitz, and S Yip. Revolutionizing engineering science through simulation. National Science Foundation Blue Ribbon Panel Report, 65, 2006.

- [28] J. O. Ramsay. Monotone regression splines in action. Statistical Science, 3(4):pp. 425–441, 1988.

- [29] J. O. Ramsay and B. W. Silverman. Functional data analysis. Springer Series in Statistics. Springer, New York, second edition, 2005.

- [30] Christian H. Reinsch. Smoothing by spline functions. I, II. Numer. Math., 10:177–183; ibid. 16 (1970/71), 451–454, 1967.

- [31] Carl Runge. Über empirische funktionen und die interpolation zwischen äquidistanten ordinaten. Zeitschrift für Mathematik und Physik, 46(224-243):20, 1901.

- [32] David Ruppert. Selecting the number of knots for penalized splines. J. Comput. Graph. Statist., 11(4):735–757, 2002.

- [33] I. J. Schoenberg. Contributions to the problem of approximation of equidistant data by analytic functions. Part B. On the problem of osculatory interpolation. A second class of analytic approximation formulae. Quart. Appl. Math., 4:112–141, 1946.

- [34] I. J. Schoenberg. Spline functions and the problem of graduation. Proc. Nat. Acad. Sci. U.S.A., 52:947–950, 1964.

- [35] Larry L. Schumaker. Spline functions: basic theory. Cambridge Mathematical Library. Cambridge University Press, Cambridge, third edition, 2007.

- [36] Kim-Chuan Toh, Michael J. Todd, and Reha H. Tütüncü. On the implementation and usage of SDPT3—a Matlab software package for semidefinite-quadratic-linear programming, version 4.0. In Handbook on semidefinite, conic and polynomial optimization, volume 166 of Internat. Ser. Oper. Res. Management Sci., pages 715–754. Springer, New York, 2012.

- [37] Miguel Villalobos and Grace Wahba. Inequality-constrained multivariate smoothing splines with application to the estimation of posterior probabilities. J. Amer. Statist. Assoc., 82(397):239–248, 1987.

- [38] Yu Xia and Paul D. McNicholas. A gradient method for the monotone fused least absolute shrinkage and selection operator. Optimization Methods and Software, 29(3):463–483, 2014.