General multilevel adaptations for stochastic approximation algorithms

Abstract.

In this article we present and analyse new multilevel adaptations of stochastic approximation algorithms for the computation of a zero of a function defined on a convex domain , which is given as a parameterised family of expectations. Our approach is universal in the sense that having multilevel implementations for a particular application at hand it is straightforward to implement the corresponding stochastic approximation algorithm. Moreover, previous research on multilevel Monte Carlo can be incorporated in a natural way. This is due to the fact that the analysis of the error and the computational cost of our method is based on similar assumptions as used in Giles [7] for the computation of a single expectation. Additionally, we essentially only require that satisfies a classical contraction property from stochastic approximation theory. Under these assumptions we establish error bounds in -th mean for our multilevel Robbins-Monro and Polyak-Ruppert schemes that decay in the computational time as fast as the classical error bounds for multilevel Monte Carlo approximations of single expectations known from Giles [7].

Key words and phrases:

Stochastic approximation; Monte Carlo; multilevel1991 Mathematics Subject Classification:

Primary 62L20; Secondary 60J10, 65C051. Introduction

Let be closed and convex and let be a random variable on a probability space with values in a set equipped with some -field. We study the problem of computing zeros of functions of the form

where is a product measurable function such that all expectations are well-defined. In this article we focus on the case where the random variables cannot be simulated directly so that one has to work with appropriate approximations in numerical simulations. For example, one may think of being a Brownian motion and of being the payoff of an option, where is a parameter affecting the payoff and/or the dynamics of the price process. Alternatively, might be the value of a PDE at certain positions with representing random coefficients and a parameter of the equation.

In previous years the multilevel paradigm introduced by Heinrich [8] and Giles [7] has proved to be a very efficient tool in the numerical computation of expectations. By Frikha [5] it has recently been shown that the efficiency of the multilevel paradigm prevails when combined with stochastic approximation algorithms. In the present paper we take a different approach than the one introduced by the latter author. Instead of employing a sequence of coupled Robbins-Monro algorithms to construct a multilevel estimate of a zero of we basically propose a single Robbins-Monro algorithm that uses in the -th step a multilevel estimate of with a complexity that is adapted to the actual state of the system and increases in the number of steps.

Our approach is universal in the sense that having multilevel implementations for a particular application at hand it is straightforward to implement the corresponding stochastic approximation algorithm. Moreover, previous research on multilevel Monte Carlo can be incorporated in a natural way. This is due to the fact that the analysis of the error and the computational cost of our method is based on similar assumptions on the biases, the -th central moments and the simulation cost of the underlying approximations of as used in Giles [7], see Assumptions C.1 and C.2 in Section 3. Additionally, we require that satisfies a classical contraction property from stochastic approximation theory: there exist and a zero of such that for all ,

where denotes an inner product on . Moreover, has to satisfy a linear growth condition relative to the zero , see Assumption A.1 and Remark 2.1 in Section 2. Note that the contraction property implies that the zero is unique. Theorem 3.1 asserts that under these assumptions the maximum -th mean error of our properly tuned multilevel Robbins-Monro scheme satisfies the same upper bounds in terms of the computational time needed to compute as the bounds obtained in Giles [7] for the multilevel computation of a single expectation.

In general, the design of this algorithm requires knowledge on the constant in the contraction property of . To bypass this problem without loss of efficiency one may work with a Polyak-Ruppert average of our algorithm. Theorem 3.2 states that under Assumptions C.1 and C.2 on the approximations of and Assumption B.1 on , which is slightly stronger than condition A.1 a properly tuned multilevel Polyak-Ruppert average achieves, for , the same upper bounds in the relation of the -th mean error and the corresponding computational time as the previously introduced multilevel Robbins-Monro method.

We briefly outline the content of the paper. The multilevel algorithms and the respective complexity theorems are presented in Section 3 for the case where . General closed convex domains are covered in Section 4. We add that Sections 3 and 4 are self-contained and a reader interested in the multilevel schemes only, can immediately start reading in Section 3.

The error analysis of the multilevel stochastic approximation algorithms is based on new estimates of the -th mean error of Robbins-Monro and Polyak-Ruppert algorithms. These results are presented in Section 2. As a technical tool we employ a modified Burkholder-Davis-Gundy inequality, which is established in the appendix and might be of interest in itself, see Theorem 5.1.

We add that formally all results of the following sections remain true when replacing by an arbitrary separable Hilbert space. However in that case the definition (61) of the computational cost of a multilevel algorithm might not be appropriate in general.

2. New error estimates for stochastic approximation algorithms

Since the pioneering work of Robbins and Monro [21] in 1951 a large body of research has been devoted to the analysis of stochastic approximation algorithms with a strong focus on pathwise and weak convergence properties. In particular, laws of iterated logarithm and central limit theorems have been established that allow to optimise the parameters of the schemes with respect to the almost sure and weak convergence rates and the size of the limiting covariance. See e.g. [2, 3, 6, 9, 10, 13, 14, 15, 17, 18, 19, 20, 22, 23] for results and further references as well as the survey articles and monographs [1, 4, 11, 12, 16, 23]. Less attention has been paid to an error control in -norm for arbitrary orders . We provide such estimates for the Robbins-Monro approximation and the Polyak-Rupert averaging introduced by Ruppert [23] and Polyak [20] under mild conditions on the ingredients of these schemes. These estimates build the basis for the error analysis of the multilevel schemes introduced in Section 3.

Throughout this section we fix , a probability space equipped with a filtration , a scalar product on with induced norm . Furthermore, we fix a measurable function that has a unique zero .

We consider an adapted -valued dynamical system iteratively defined by

| (1) |

for , where is a fixed deterministic starting value,

-

(I)

is a previsible process, the remainder/bias,

-

(II)

is a sequence of martingale differences,

-

(III)

is a sequence of positive reals tending to zero, and and are sequences of non-negative real numbers.

Estimates for the Robbins-Monro algorithm

Our goal is to quantify the speed of convergence of the sequence to in the -th mean sense in terms of the step-sizes , the bias-levels and the noise-levels .

To this end we employ the following set of assumptions in addition to (I)–(III).

-

A.1

(Assumptions on and )

There exist such that for all-

(i)

and

-

(ii)

.

-

(i)

-

A.2

(Assumptions on and )

It holds-

(i)

and

-

(ii)

.

-

(i)

Remark 2.1 (Discussion of Assumption A.1).

We briefly discuss A.1(i) and A.1(ii).

Let and , and consider the conditions

| (i) | ||||

| (ii) | ||||

| (ii’) | ||||

| () |

By the Cauchy-Schwartz inequality we have

| (2) |

and the choice shows that the reverse implication is not valid in general. However, it is easy to check that

Thus, in the presence of condition A.1(i), condition A.1(ii) is equivalent to a linear growth condition on the function relative to the zero .

Finally, conditions (i) and (ii) jointly imply the contraction property (*), which is crucial for the analysis of the Robbins-Monro scheme. We have

| (3) |

In fact, let and use (ii) and then (i) to conclude that

In the following we put for and with ,

| (4) |

First we provide -th mean error estimates in terms of the quantities introduced in (4).

Proposition 2.2.

Assume that (I)-(III) and A.1 and A.2 are satisfied. Then for every there exist and such that for all we have and

| (5) |

Proof.

Without loss of generality we may assume that .

By Assumption A.2 there exists such that for all ,

| (6) |

and

| (7) |

Note further that (2) in Remark 2.1 implies that the dynamical system (1) satisfies for every . With Assumption A.2 we conclude that for every .

Let . Since we may choose such that and for all . Using (3) in Remark 2.1 we obtain that for all and for all ,

| (8) |

In the following we write , and in place of , and , respectively. Let and put

| (9) |

for . Then is adapted, is previsible, is a martingale and for all we have

| (10) |

Below we show that there exists a constant , which only depends on , and such that a.s. for all ,

| (11) |

and

| (12) |

Observing (10) and (11) we may apply the BDG inequality, see Theorem 5.1, to the processes , and to obtain for that

| (13) |

where the constant only depends on . Using (12) we conclude that

which completes the proof of the theorem up to the justification of (11) and (12).

Remark 2.3.

The proof of the -th mean error estimate (5) in Proposition 2.2 for the times makes use of the recursion (1) for strictly larger than only. Hence, if and is the dynamical system given by the recursion (1) with an arbitrary random starting value then estimate (5) is valid for in place of with the same constant for all .

The following theorem provides an estimate for the -th mean error of in terms of the product

It requires the following additional assumptions on the step-sizes , the bias-levels and the noise-levels .

-

A.3

(Assumptions on , and )

We have for all . Furthermore, with according to A.1(i),-

(i)

, and

-

(ii)

.

-

(i)

Theorem 2.4 (Robbins-Monro approximation).

Assume that conditions (I)-(III), A.1, A.2 and A.3 are satisfied. Then there exists such that for all ,

Proof.

Below we show that there exist , and such that for all we have and

| (15) |

Then, by choosing and according to Proposition 2.2 and taking we have for that , and , and therefore for all

which finishes the proof of the theorem, up to the justification of (15).

By Assumption A.3 there exist , and such that for all ,

| (16) |

as well as

| (17) |

Take and assume without loss of generality that for all . In the following we write , and in place of , and , respectively. It follows from (16) and that the sequence is increasing and therefore, for all ,

| (18) |

Furthermore, observing (17) we also have for all ,

| (19) |

Put

for . Observing (16) we obtain that for ,

This entails that

so that . Hence, by induction, for all ,

so that

| (20) |

As a particular consequence of Theorem 2.4 we obtain error estimates in the case of polynomial step-sizes and noise-levels .

Corollary 2.5 (Polynomial step-sizes and noise-levels).

Assume that conditions (I)-(III), A.1 and A.2 are satisfied and choose according to A.1(i). Take , and with

and let for all ,

Assume further that

Then there exists a constant such that for all ,

| (21) |

Proof.

We first verify that Assumption A.3 is satisfied. By definition of and we have

Thus, A.3(i) is satisfied due to the assumption on the sequence . Moreover, it is easy to see that

and therefore A.3(ii) is satisfied as well. Since conditions (I)-(III), A.1 and A.2 are part of the corollary, we may apply Theorem 2.4 to obtain the claimed error estimate. ∎

Remark 2.6 (Exponential decay of noise-levels).

Assumption A.3(ii) may also be satisfied in the case that the noise-levels have a superpolynomial decay. For instance, if

for all , where , , and , then

On the other hand side, if the noise-levels are decreasing with exponential decay and the step-sizes are monotonically decreasing then Assumption A.3(ii) is typically not satisfied. In fact, if for , and then .

The case of an exponential decay of the noise-levels can be treated by applying Proposition 2.2. Assume that conditions (I)-(III), A.1 and A.2 are satisfied.

Assume further that there exist and such that for all ,

-

(a)

and

-

(b)

.

Then there exists such that for all ,

| (22) |

Proof of (22).

Since and for all we have for sufficiently large. Hence there exists such that for all ,

| (23) |

Using (23) as well as Assumption (b) we get for all ,

| (24) |

Choosing large enough we may also assume that for all . Employing (23) and Assumption (a) we then conclude that for all ,

| (25) | ||||

Combining (23) to (25) with Proposition 2.2 completes the proof of (22). ∎

So far we proved error estimates for the single random variables . In the following theorem we establish error estimates, which allow to control the quality of approximation for the whole sequence starting from some time .

To this end we employ the following assumption A.4, which is stronger than condition A.3.

-

A.4

(Assumptions on , and )

We have for all . Furthermore, with according to A.1(i), there exist as well as such that and-

(i)

,

-

(ii)

for all but finitely many ,

-

(iii)

for all but finitely many .

-

(i)

Theorem 2.7 (Robbins-Monro approximation).

Assume that conditions (I)-(III), A.1, A.2 and A.4 are satisfied and let

Then for all there exists a constant and such that for all

| (26) |

Proof.

Clearly, we may assume that . Fix .

We again use the quantities introduced in (4). Since Assumption A.4 is stronger than Assumption A.3 we see from the proof of Theorem 2.4 that there exist , and such that for all we have and

| (27) |

cf. (15). By A.4(ii) and A.4(iii) we may further assume that for all ,

| (28) |

Fix and define a strictly increasing sequence in by

Observing the upper bound for in (28) it is then easy to see that for all ,

| (29) |

In the following we write , and in place of , and , respectively. We estimate the decay of the sequence . Let . Using (28), the fact that for all , the estimate (29) and the fact that for all we get

| (30) |

as well as

| (31) |

Next, we establish a lower bound for the growth of the sequence , namely

| (32) |

for all , where

In fact, by A.4(iii) we get

which yields (32).

We are ready to establish the claimed estimate in -th mean (26). Similar to the proof of Proposition 2.2 we consider the process and the martingale given by (9), where is replaced by . As in the proof of Proposition 2.2 we obtain the maximum estimate in -th mean (13) for the process and the estimate in -th mean (14) for the quadratic variation . Combining these two estimates we see that for sufficiently large there exists a constant , such that for every we have

Using the latter inequality as well as (30), Theorem (2.4) and (27) we may thus conclude that there exists a constant , which may depend on but not on such that for every we have

In analogy to Corollary 2.5 we next treat the particular case of polynomial step-sizes and noise-levels .

Corollary 2.8 (Polynomial step-sizes and noise-levels).

Assume that conditions (I)-(III), A.1 and A.2 are satisfied and choose according to A.1(i). Take , and with

-

(a)

,

-

(b)

and let for all ,

Assume further that

Then for all there exists a constant such that for all ,

| (35) |

Proof.

We first verify Assumption A.4. By definition of and we have

Thus, A.4(i) is satisfied due to the assumption on the sequence and the first part of A.4(ii) is satisfied due to Assumption (a), see the proof of Corollary 2.5. Observing Assumption (b) it is obvious that the second part of A.4(ii) and Assumption A.4(iii) are satisfied for

Since conditions (I)-(III), A.1 and A.2 are part of the corollary, we may apply Theorem 2.7 to obtain the claimed error estimate. ∎

Estimates for the Polyak-Ruppert algorithm

Now we turn to the analysis of Polyak-Ruppert averaging. For we let

| (36) |

where is a fixed sequence of strictly positive reals and

We estimate the speed of convergence of to in -th mean in terms of the sequence given by

To this end we will replace the set of assumptions A.1, A.2 and A.3 by the following set of assumptions B.1, B.2 and B.3. Note that B.2 coincides with A.2 while B.1 is stronger than A.1 and B.3 is stronger than A.3, see Remark 2.9 below.

-

B.1

(Assumptions on and )

There exist and a matrix such that for all-

(i)

,

-

(ii)

and

-

(iii)

.

-

(i)

-

B.2

(Assumptions on and )

It holds-

(i)

and

-

(ii)

.

-

(i)

-

B.3

(Assumptions on , , and )

We have for all . The sequence is decreasing and the sequences and are increasing. Moreover, with and according to B.1 there exist with such that-

(i)

,

-

(ii)

and for all but finitely many ,

-

(iii)

for all but finitely many ,

-

(iv)

for all ,

i.e., the sequence has at most polynomial growth.

-

(i)

Remark 2.9 (Discussion of assumptions B.1 and B.3).

We first show that Assumption B.3 implies Assumption A.3. Since is increasing we have for every , which proves that B.3 implies A.3(i). Furthermore,

for every , which proves that B.3 implies A.3(ii).

We add that, due to the presence of Assumption B.1(ii), it is sufficient to require that satisfies the inequality in B.1(iii) on some open ball around . In fact, let and be such that . Let and and consider the conditions

| (ii) | ||||

| (iii) | ||||

| (iii’) |

Then

| (37) |

where denotes the induced matrix norm of .

For a proof of we first note that (iii’) implies that for every . Using we conclude that . For we have . Observing the latter fact and using again we conclude

As an immediate consequence of (37) with the choice we obtain that if satisfies B.1(ii),(iii) then satisfies B.1(iii) for every with replaced by .

Theorem 2.10 (Polyak-Ruppert approximation).

Assume that conditions (I)-(III) and B.1-B.3 are satisfied. Put with according to B.1. Then there exists such that the Polyak-Ruppert algorithm (36) satisfies for all

For the proof of Theorem 2.10 we follow the approach of the classical paper [20] by first comparing the dynamical system with a linearised version given by and

for .

Lemma 2.11.

Assume that conditions (I)-(III) and B.1-B.3 are satisfied. Put with according to B.1. Then there exists such that for all

Proof.

Without loss of generality we may assume that .

Using B.3(i),(ii) we see that there exist , and such that for all we have

| (38) |

and

| (39) |

Since we may assume that for all .

By Remark 2.9 conditions A.1-A.3 are satisfied and we may apply Theorem 2.4 to obtain the existence of such that for all ,

| (40) |

Furthermore, estimate (8) in the proof of Proposition 2.2 is valid, i.e., there exists such that for all and all ,

| (41) |

By Assumption B.1(iii) we have

| (42) |

for every . Using (41) we may therefore conclude that for all and all ,

| (43) |

Let . For we put

Let . Using (43), Assumptions B.1(iii), B.2(i) and (38) we see that there exists such that

and employing (39), (40), B.3(ii) and the fact that we conclude that

| (44) | ||||

Put and . By (44) we have for that or, equivalently,

which yields,

Since , due to Assumption B.3(iii), we conclude that

which finishes the proof. ∎

Proof of Theorem 2.10.

Without loss of generality we may assume that .

By Assumption B.3(iv) it follows that

| (46) |

where .

Employing Lemma 2.11 as well as (46) and the fact that is increasing we see that there exists such that for all ,

| (47) |

where we used in the latter step.

Next, put and let

where is the identity matrix, as well as

for . Then, for all ,

and

Using the Burkholder-Davis-Gundy inequality we obtain that there exists a constant such that for all ,

| (48) |

By Assumption B.2(ii) there exists a constant such that for all ,

| (49) | ||||

We proceed with estimating the norms . Since we can fix and proceed as in the proof of Lemma 2.11 to conclude that there exists such that for all

see (43). The latter fact and the assumption that the sequence is increasing jointly imply that for

where we used that for all . Employing the latter estimate as well as Assumption B.3(iv) we get that for

| (50) | ||||

Put and note that by the choice of and by B.3(iii) one has for large enough that

Choosing large enough we therefore conclude that there exists such that for ,

In combination with (50) we see that there exists such that for all ,

| (51) |

Using (51) as well as (52) and the fact that the sequence is increasing we conclude that there exists such that for all ,

| (53) |

We consider the particular case of polynomial step-sizes , noise-levels and weights .

Corollary 2.12 (Polynomial step-sizes, noise-levels and weights).

Assume that conditions (I)-(III), B.1 and B.2 are satisfied and let with according to B.1(iii).

Take , , and with

and let for all ,

Assume further that

Then there exists a constant such that for all ,

Proof.

Conditions (I)-(III), B.1 and B.2 are part of the corollary. Further note that by Remark 2.9 condition B.1(iii) remains true when replacing by . We verify that condition B.3 holds as well with in place of . Then the corollary is a consequence of Theorem 2.10 and the fact that .

Since it is clear that is decreasing and is increasing. Furthermore,

is increasing since . B.3(i) is satisfied due to the assumption on . Since the limes superior in B.3(ii) is zero. Moreover, the second estimate of B.3(ii) holds for an appropriate positive constant since and by assumption. Condition B.3(iii) is satisfied for any since , and thus condition B.3(iv) is satisfied with . ∎

3. Multilevel stochastic approximation

Throughout this section we fix , a probability space , a scalar product on with induced norm , a non-empty set equipped with some -field, a random variable and a product-measurable function

such that is integrable for every . We consider the function given by

| (55) |

and we assume that has a unique zero .

Our goal is to compute by means of stochastic approximation algorithms based on the multilevel Monte Carlo approach. To this end we suppose that we are given a hierarchical scheme

of suitable product-measurable approximations to , such that is integrable and can be simulated for all and , where .

To each random vector we assign a positive number , which depends only on the level and may represent a deterministic worst case upper bound of the average computational cost or average runtime needed to compute a single simulation of . As announced in the introduction we impose assumptions on the approximations and the cost bounds that are similar in spirit to the classical multilevel Monte Carlo setting, see [7].

-

C.1

(Assumptions on and )

There exist measurable functions and constants and with such that for all and all-

(i)

,

-

(ii)

, and

-

(iii)

.

-

(i)

We combine the Robbins-Monro algorithm with the classical multilevel approach taken in [7]. The proposed method uses in each Robbins-Monro step a multilevel estimate with a complexity that is adapted to the actual state of the system and increases in time.

The algorithm is specified by the parameters from Assumption C.1, an initial vector ,

-

(i)

a sequence of step-sizes tending to zero,

-

(ii)

a sequence of bias-levels , and

-

(iii)

a sequence of noise-levels .

The maximal level and the number of iterations on level that are used by the multilevel estimator in the -th Robbins-Monro step depend on and are determined in the following way. We take

| (56) |

i.e. is the smallest such that holds true for the bias bound in Assumption C.1(ii). Furthermore,

| (57) |

where

| (58) |

Take a sequence of independent copies of . We use

| (59) |

as a multilevel approximation of in the -th Robbins-Monro step, and we study the sequence of Robbins-Monro approximations given by

| (60) |

We measure the computational cost of by the quantity

| (61) |

That means we take the mean computational cost for simulating the random vectors for the first iterations into account and we ignore the cost of the involved arithmetical operations. Note, however, that the number of arithmetical operations needed to compute is essentially proportional to , and the average of the latter quantity is captured by under the weak assumption that .

Note further that the quantity depends on the parameters , and , which determine the algorithm up to time . For ease of notation we do not explicitly indicate this dependence in the notation .

To obtain upper bounds of we need the following additional assumption C.2 on the functions , which implies that both the variance estimate in C.1(i) and the bias estimate in C.1(ii) are at most of polynomial growth in with exponents related to the parameters , and .

-

C.2

(Assumption on )

With according to Assumption C.1 there exists andsuch that for all

(62)

We are now in the position to state the central complexity theorem on the multilevel Robbins-Monro algorithm.

Theorem 3.1 (Multilevel Robbins-Monro approximation).

Suppose that Assumption A.1 is satisfied for the function given by (55) and that Assumptions C.1 and C.2 are satisfied. Take according to A.1, take according to C.1 and C.2 and let .

Take , , , and let and for all ,

Then for all there exists such that for all ,

In particular, for all we have almost surely.

If additionally and then there exists such that for all ,

The implementation of the multilevel Robbins-Monro approximation from Theorem 3.1 requires the knowledge of a positive lower bound for the parameter from Assumption A.1. This difficulty is overcome by applying the Polyak-Ruppert averaging methodology. That means we consider the approximations

| (63) |

were is the multilevel Robbins-Monro scheme specified by (60), is a sequence of positive reals and

for , see Section 2.

Note that the cost to compute differs from the cost to compute at most by a deterministic factor, which does not depend on . Therefore we again measure the computational cost for the computation of by the quantity given by (61).

We state the second complexity theorem, which concerns Polyak-Ruppert averaging.

Theorem 3.2 (Multilevel Polyak-Ruppert approximation).

Suppose that Assumption B.1 is satisfied for the function given by (55) and that Assumptions C.1 and C.2 are satisfied. Take according to B.1, take according to C.1 and C.2 and let .

Let . Take , , and with

and let and for all ,

Then there exists such that for all

If additionally and then there exists such that for all

Remark 3.3.

Remark 3.4.

The multilevel stochastic approximation algorithms analysed in Theorems 3.1 and 3.2 are based on evaluations of the increments . Consider, more generally, a sequence of measurable mappings , , such that for all ,

and is a worst case cost bound for simulating . Then Theorems 3.1 and 3.2 are still valid for the algorithm obtained by using as a substitute for the increment in (59) if Assumption C.1(i) is satisfied with in place of .

The proofs of Theorems 3.1 and 3.2 are based on the following proposition, which shows that under Assumptions C.1(i),(ii) the scheme (60) can be represented as a Robbins-Monro scheme of the general form (1) studied in Section 2. It further provides an estimate of the computational cost (61) based on Assumptions C.1(iii) and C.2 only.

Proposition 3.5.

-

(i)

Suppose that Assumptions C.1(i),(ii) are satisfied. Let denote the -field generated by the variables with and , and let denote the trivial -field. The scheme given by (60) satisfies

for every , where is a previsible process with respect to the filtration and is a sequence of martingale differences with respect to and and satisfy Assumption A.2.

- (ii)

Proof.

We first prove statement (i) of the proposition. Put and let

for and . By Assumptions C.1(i),(ii) we have

| (66) |

for all and .

By (66) and the definition (56) of we get for all and that

| (67) |

Furthermore, by the Burkholder-Davis-Gundy inequality, the triangle inequality on the -space, and the definition of there exists , which only depends on , such that

Recalling the definition of , see (58), we conclude that there exists such that for all and

| (68) |

With

we obtain that . We verify Assumption A.2.

The process is predictable and using the independence of and we conclude with (67) that . By the latter independence it further follows that is a sequence of martingale differences, which satisfies as a consequence of (68). This completes the proof of statement (i).

We turn to the proof of statement (ii). Let and . Using Assumption C.1(iii), we conclude that there exists , which only depends on , and such that

| (69) | ||||

Furthermore, (56) yields that

| (70) |

Combining (69) with (70) and employing Assumption C.2 we see that there exists , which only depends on , , , and , such that

| (71) | ||||

Suppose that . Then (71) implies

which finishes the proof for the case . In the case we have and therefore the existence of a constant , which does not depend on , such that

One completes the proof of statement (ii) by combining the latter estimate with (71). ∎

We turn to the proof of Theorem 3.1.

Proof of Theorem 3.1.

The error estimate follows by Corollary 2.8 since Assumption A.1 is part of the theorem and Assumptions (I)-(III) and A.2 are satisfied by Proposition 3.5(i).

It remains to prove the cost estimate. The error estimate implies that . Employing Proposition 3.5(ii) we thus see that there exists such that for every

| (72) |

Hence there exists such that for every

| (73) |

If then and , which implies that and therefore

If then and , which implies that and therefore

This completes the proof. ∎

We proceed with the proof of Theorem 3.2.

Proof of Theorem 3.2.

The error estimate follows with Corollary 2.12 since Assumption B.1 is part of the theorem and Assumptions (I)-(III) and B.2 hold by Proposition 3.5(i). The cost estimate in the theorem is proved in the same way as the cost estimate in Theorem 3.1. One only observes that is valid since the assumptions in Corollary 2.12 are stronger than the assumptions in Corollary 2.5. ∎

4. General convex closed domains

In this section we extend the results of Sections 2 and 3 to convex domains. In the following denotes a convex and closed subset of and is a function with a unique zero . We start with the Robbins-Monro scheme.

Let

denote the orthogonal projection on with respect to the given inner product on and define the dynamical system by the recursion

| (74) |

in place of (1), where is a deterministic starting value in . Then the following fact follows by a straightforward modification in the proofs of Proposition 2.2 and Theorem 2.7 using the contraction property of .

Extension 4.1.

Analogously, we extend Theorem 3.1 in Section 3 on the multilevel Robbins-Monro approximation to the case where the mappings are defined on with being a closed and convex subset of and

has a unique zero . In this case we proceed analogously to Extension 4.1 and employ the projected multilevel Robbins-Monro scheme

| (75) |

with and given by (59), in place of the multilevel scheme (60).

Note that if can be evaluated on with constant cost then, up to a constant depending on only, the computational cost of the projected approximation is still bounded by the quantity given by (72) since the computation of requires evaluations of and .

Extension 4.2.

Next we consider the Polyak-Ruppert scheme. In this case we additionally suppose that contains an open ball around the unique zero and we extend the function on : for define

| (76) |

The following lemma shows that property B.1 is preserved for appropriately chosen .

Lemma 4.3.

Let and suppose that and that satisfies B.1(i) to B.1(iii) on . Take according to B.1, let and put

Then satisfies B.1(i) to B.1(iii) on with

| (77) |

in place of , and , respectively.

Proof.

Using (3) with , and it follows that . By (3) and the contractivity of the projection we have for any that

which shows that satisfies B.1(i) on with in place of .

Using the latter estimate, (2) with and the Lipschitz continuity of we get for any that

which shows that satisfies B.1(ii) on with in place of .

Finally, let , which implies that . Using the latter fact and the projection property and the contractivity of we get

Observing that , see (37), completes the proof of the lemma. ∎

Replacing by in (1) we obtain the dynamical system

| (78) |

for , where is a deterministic starting value in .

Employing Lemma 4.3 we immediately arrive at the following fact.

Extension 4.4.

Similar to Extension 4.4 we can extend Theorem 3.2 on the multilevel Polyak-Ruppert averaging. To this end we define for extensions of the mappings by taking

for . Note that and with given by (76).

Clearly, if the mappings satisfy C.1(i),(ii) on then the mappings satisfy C.1(i),(ii) on with in place of . Furthermore, if satisfy Assumption C.2 on then satisfy Assumption C.2 on , since we have for every .

We thus take

with , and given by (56),(57) and (59), respectively, as a multilevel approximation of in the -th Robbins-Monro step, and we use the multilevel scheme

| (80) |

for Polyak-Ruppert averaging.

Employing Lemma 4.3 we get the following result.

5. Numerical Experiments

We illustrate the application of our multilevel methods in the simple case of computing the volatility in a Black Scholes model based on the price of a European call.

Fix and let denote a one-dimensional Brownian motion on . For every we use to denote the geometric Brownian motion on with initial value , trend and volatility , i.e.

| (82) | ||||

In a Black Scholes model with fixed interest rate the fair price of a European call with maturity , strike and underlying geometric Brownian motion with volatility is given by

where

and according to the Black-Scholes formula satisfies

where denotes the standard normal distribution function.

Fix as well as . Our computational goal is to approximate based on the knowledge of and the value of the price .

Within the framework of sections 3 and 4 we take , , and

Moreover, we approximate by employing equidistant Milstein schemes: for with and we define

where denotes the Milstein approximation of based on equidistant steps, i.e.

with .

We briefly check the validity of Assumptions B.1, C.1 and C.2. Clearly, the mapping satisfies

Note that is two times differentiable with respect to on with

| (83) | ||||

where denotes the density of the standard normal distribution. Let and put as well as

Using (83) it is then straightforward to verify that satisfies Assumption B.1 on with parameters

| (84) |

and

| (85) |

As is well known there exists a constant , which depends only on , such that

Since we conclude that Assumption C.1 is satisfied on with parameters

for some constant , which depends only on . Consequently, Assumption C.2 is satisfied on as well.

First, we consider the projected multilevel Robbins-Monro scheme (75) with step-size , noise-level and bias-level given by

Note that the constant does not need to be known in order to implement the scheme. We have

where and for all

| (86) |

with independent copies of . Then by Extension 4.2 of Theorem 3.1 there exists such that for every ,

| (87) |

In the following we use the model parameters

| (88) |

and we choose

| (89) |

in the definition of the Robbins-Monro scheme.

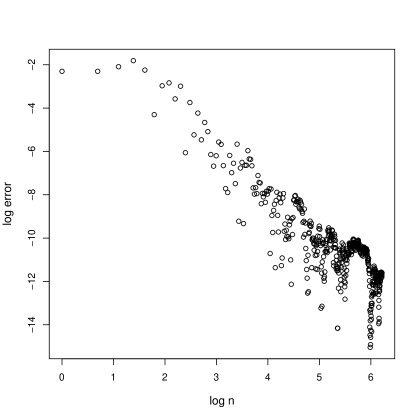

Figure 1 shows a log-log plot of a simulation of the first steps of the error process .

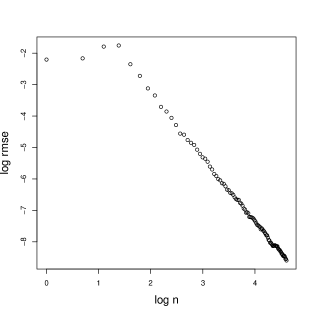

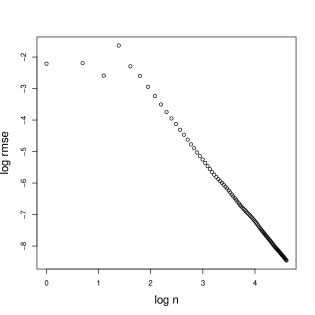

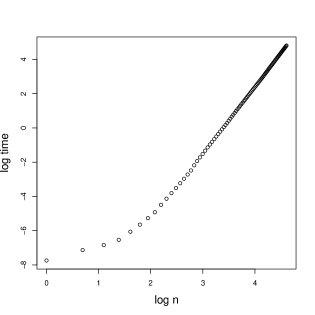

Figure 2 shows the log-log plot of Monte Carlo estimates of the root mean squared error of and the corresponding average computational times for based on replications. Both plots are in accordance with the theoretical bounds in (87).

Next, we consider the multilevel Polyak-Rupert averaging (81) with step-size , noise-level , bias-level , weight and extension parameter given by

Thus

where

with given by (86) and a deterministic . Then by Extension 4.5 of Theorem 3.2 there exists for every a constant such that for every ,

| (90) |

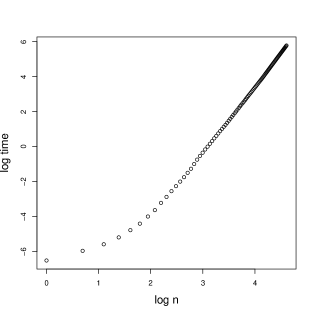

We choose the parameters as in (88) and (89). Figure 3 shows the log-log plot of a trajectory of the error process until .

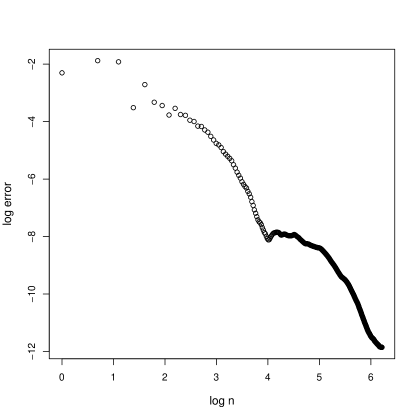

Figure 4 shows the log-log plot of Monte Carlo estimates of the root mean squared error of and the corresponding average computational times for based on replications. As for the multilevel Robbins-Monro scheme, both plots are in accordance with the theoretical bounds in (90).

Appendix

Let be a probability space endowed with a filtration and let denote a Hilbert space norm on .

In this section we provide -th mean estimates for an adapted -dimensional dynamical system with the property that for each , is a zero-mean perturbation of a previsible proposal being comparable in size to . More formally, we assume that there exist a previsible -dimensional process , a -dimensional martingale with and a constant such that for all

| (91) | ||||

where . Note that necessarily .

Theorem 5.1.

Assume that is an adapted -dimensional process, which satisfies (91), and let . Then there exists a constant , which only depends on , such that for every ,

where

Proof.

Fix .

We first consider the case where . Recall that by the BDG inequality there exists a constant depending only on such that for every -dimensional martingale ,

We fix a time horizon and prove the statement of the theorem with by induction: we say that the statement holds up to time , if for every -dimensional adapted process , for every -dimensional previsible process and for every -dimensional martingale with

| () |

one has

Clearly, the statement is satisfied up to time as a consequence of the BDG inequality. Next, suppose that the statement is satisfied up to time . Let be a -dimensional adapted process, be a -dimensional previsible process and be a -dimensional martingale satisfying property (). Consider any -measurable random orthonormal transformation on and put

as well as

Then it is easy to check that is a martingale with for all . Furthermore, is adapted and the triple satisfies property (). Hence, by the induction hypothesis,

| (92) |

Note that for any such random orthonormal transformation , the norm of the random variable is the same as the norm of the variable given by

whence

| (93) |

Clearly, we can choose an -measurable random orthonormal transformation on such that

holds on . Let

Then is -measurable and takes values in since . Moreover, we have so that by property () of the triple ,

for . Note that for . By convexity of we thus obtain

Hence

where is the -measurable random orthonormal transformation given by

Next, we consider the case of . Suppose that and are as stated in the theorem. For we put

and

Furthermore, let . We will show that the triple satisfies (91) with . Clearly, is adapted and is previsible. Moreover, one has for on that

and on that . We may thus apply Theorem 5.1 with to obtain that for every ,

Since for every ,

we conclude that

which completes the proof. ∎

References

- [1] A. Benveniste, M. Métivier, and P. Priouret. Adaptive algorithms and stochastic approximations, volume 22 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1990.

- [2] J. Dippon and J. Renz. Weighted means in stochastic approximation of minima. SIAM J. Control Optim., 35(5):1811–1827, 1997.

- [3] K. Djeddour, A. Mokkadem, and M. Pelletier. On the recursive estimation of the location and of the size of the mode of a probability density. Serdica Math. J., 34(3):651–688, 2008.

- [4] M. Duflo. Algorithmes stochastiques, volume 23 of Mathématiques & Applications (Berlin) [Mathematics & Applications]. Springer-Verlag, Berlin, 1996.

- [5] N. Frikha. Multi-level stochastic approximation algorithms. Ann. Appl. Probab., 26:933–985, 2016.

- [6] V. F. Gaposhkin and T. P. Krasulina. On the law of the iterated logarithm in stochastic approximation processes. Theory Prob. Appl., 19(4):844–850, 1974.

- [7] M. B. Giles. Multilevel Monte Carlo path simulation. Oper. Res., 56(3):607–617, 2008.

- [8] S. Heinrich. Multilevel Monte Carlo methods. In Large-scale scientific computing, pages 58–67. Springer Berlin Heidelberg, 2001.

- [9] V. R. Konda and J. N. Tsitsiklis. Convergence rate of linear two-time-scale stochastic approximation. Ann. Appl. Probab., 14(2):796–819, 2004.

- [10] H. J. Kushner and J. Yang. Stochastic approximation with averaging of the iterates: optimal asymptotic rate of convergence for general processes. SIAM J. Control Optim., 31(4):1045–1062, 1993.

- [11] H. J. Kushner and G. G. Yin. Stochastic approximation and recursive algorithms and applications, volume 35 of Applications of Mathematics (New York). Springer-Verlag, New York, second edition, 2003. Stochastic Modelling and Applied Probability.

- [12] T. L. Lai. Stochastic approximation. Ann. Statist., 31(2):391–406, 2003. Dedicated to the memory of Herbert E. Robbins.

- [13] T. L. Lai and H. Robbins. Limit theorems for weighted sums and stochastic approximation processes. Proc. Nat. Acad. Sci. U.S.A., 75, 1978.

- [14] A. Le Breton and A. Novikov. Averaging for estimating covariances in stochastic approximation. Math. Methods Statist., 3(3):244–266, 1994.

- [15] A. Le Breton and A. Novikov. Some results about averaging in stochastic approximation. Metrika, 42(3-4):153–171, 1995. Second International Conference on Mathematical Statistics (Smolenice Castle, 1994).

- [16] L. Ljung, G. Pflug, and H. Walk. Stochastic approximation and optimization of random systems, volume 17 of DMV Seminar. Birkhäuser Verlag, Basel, 1992.

- [17] A. Mokkadem and M. Pelletier. A generalization of the averaging procedure: the use of two-time-scale algorithms. SIAM J. Control Optim., 49(4):1523–1543, 2011.

- [18] M. Pelletier. On the almost sure asymptotic behaviour of stochastic algorithms. Stochastic Process. Appl., 78(2):217–244, 1998.

- [19] M. Pelletier. Weak convergence rates for stochastic approximation with application to multiple targets and simulated annealing. Ann. Appl. Probab., 8(1):10–44, 1998.

- [20] B. T. Polyak. A new method of stochastic approximation type. Avtomat. i Telemekh., 51(7):937–1008, 1998.

- [21] H. Robbins and S. Monro. A stochastic approximation method. Ann. Math. Statistics, 22:400–407, 1951.

- [22] D. Ruppert. Almost sure approximations to the Robbins-Monro and Kiefer-Wolfowitz processes with dependent noise. Ann. Probab., 10, 1982.

- [23] D. Ruppert. Stochastic approximation. In Handbook of sequential analysis, volume 118 of Statist. Textbooks Monogr., pages 503–529. Dekker, New York, 1991.