Parameter stability and semiparametric inference in time-varying ARCH models

Abstract

In this paper, we develop a complete methodology for detecting time-varying/non time-varying parameters in ARCH processes. For this purpose, we estimate and test various semiparametric versions of the time-varying ARCH model (tv-ARCH) which include two well known non stationary ARCH type models introduced in the econometric literature. Using kernel estimation, we show that non time-varying parameters can be estimated at the usual parametric rate of convergence and for a Gaussian noise, we construct estimates that are asymptotically efficient in a semiparametric sense. Then we introduce two statistical tests which can be used for detecting non time-varying parameters or for testing the second order dynamic. An information criterion for selecting the number of lags is also provided. We illustrate our methodology with several real data sets.

1 Introduction

The modeling of financial data using nonstationary time series has recently received considerable attention both in econometrics and in statistics. For classical daily series such as stock market indices or currency exchange rates, the stationarity assumption seems often incompatible with a long history of data and the necessity of using non stationary ARCH models has been pointed out by several authors. See for instance Mikosch and Stǎricǎ (2004), Granger and Stǎricǎ (2005), Engle and Rangel (2008), Fryzlewicz et al. (2008) and the references therein. However, it is difficult to find in the literature a consensus for representing non-stationary ARCH models. A natural approach is to allow time-varying parameters in the classical ARCH model of Engle (1982). Such an extension has been proposed by Dahlhaus and Subba Rao (2006) with the so-called time-varying ARCH model (tv-ARCH). The tv-ARCH processes are defined by the recursive equations

| (1.1) |

where for , is a smooth function and a strong white noise with variance . Since they can be locally approximated by stationary ARCH processes, the tv-ARCH processes are called locally stationary (the notion of local stationarity is introduced in Dahlhaus (1997) for linear processes but the meaning of local stationarity for the non linear tv-ARCH can be found in Dahlhaus and Subba Rao (2006)). From this important feature, a nice asymptotic theory can be developed for estimation of parameters, in particular local inference methods such as the local Quasi-maximum likelihood estimation studied in Dahlhaus and Subba Rao (2006), the local weighted least-squares estimation developed in Fryzlewicz et al. (2008) or the recursive online algorithms considered by Dahlhaus and Subba Rao (2007). In Fryzlewicz et al. (2008), it was shown that tv-ARCH processes provide good fits and accurate forecasts for some financial series. However, statistical inference in model (1.1) is complex, even for large samples, because functions have to be estimated using nonparametric methods. Thus, in practice, reducing complexity can be interesting to improve model fit or forecasts accuracy. For example, Granger and Stǎricǎ (2005) have shown that the simple model

| (1.2) |

with a smooth deterministic function can already produce significantly better forecasts for the returns of the SP500 index than the classical GARCH model. A process of type (1.2) can be seen as a tv-ARCH process with zero lag coefficients. Note that model (1.2) does not assume autocorrelation for the absolute values or the squares of the process (a correlation property often called second order dynamic in the literature) but only some changes in the unconditional variance. In Granger and Stǎricǎ (2005), it is argued that most of dynamic of the SP index can be explained with a time-varying unconditional variance.

But nonstationarity and second order correlation can also be combined in a very simple way, assuming constant lag coefficients in (1.1):

| (1.3) |

Model (1.3) combine a time-varying unconditional variance compatible with the analysis of Granger and Stǎricǎ (2005) and a second order dynamic for the series with a single nonparametric component. Note also that a process defined by equations (1.3) can be written using the multiplicative form

| (1.4) |

where

if we neglect the ratio which is of order when the function is positive and Lipschitz continuous over . One can also notice that writing the model with the latter approximation or not lead to two processes that are both approximated by the same stationary ARCH processes with parameters (see Lemma for this kind of approximation). In the stationary case, we remind that multiplying an ARCH process by a positive constant is equivalent to multiply the initial intercept coefficient. Then for a large sample size , the process behaves as a stationary ARCH process and is (up to a constant) the time-varying unconditional variance of the process . Such a multiplicative form for ARCH models has been first considered by Engle and Rangel (2008) with the so-called Spline-GARCH model which writes as model (1.4) but with a GARCH process .

Since the previous models satisfy the inclusions (1.2) (1.3) (1.1), a natural question for any real data set is to test some properties of the lag coefficients. Testing the constancy of the lag coefficients can help to decide between model (1.3) and model (1.1) while testing the second order dynamic in model (1.3) is useful to determine if model (1.2) provides a sufficient fit. Statistical tools to help the practitioners to choose among the three important specifications described above seems not available in the literature except in a recent paper of Patilea and Raïssi (2014) which introduces a test for the second order dynamic in model (1.3).

In this paper, we propose a general approach for estimating an arbitrary subset of non time-varying coefficients in tv-ARCH processes. Our estimators are consistent and we will also study the semi-parametric asymptotic efficiency of our method when the noise is Gaussian. Using these results, we construct two statistical tests. The first test can be used to decide whether a given subset of parameters is time-varying or not. This test is based on a distance between a nonparametric kernel estimator of the coefficients and the semiparametric estimator introduced in this paper. The second test can be used for deciding if the constant parameters are different from zero. Various applications can be considered as a simple particular case of our methodology: testing model (1.3) versus model (1.1), testing model (1.2) versus model (1.3), estimating parameters and selecting lag variables in models (1.3) or (1.1). When some coefficients are assumed to be non time-varying in (1.1), the decomposition leads to semiparametric inference in a time-varying regression model. Detecting and estimating a parametric component in general time-varying regression models has been considered recently by Zhang and Wu (2012). However these authors do not consider the case of tv-ARCH processes with optimal moment condition for the marginal distribution, asymptotic semi-parametric efficiency for the estimation and Lipschitz continuity for the time-varying coefficients. Moreover, our approach for estimating non-time varying coefficients is quite different.

We applied our methodology to three real data sets: the daily exchange rates between the US Dollar and the Euro or between the US Dollar and the Indian Rupee and the FTSE index. For the three series of interest, a non time-varying intercept is clearly rejected over the considered period. The conclusion for the lag coefficients depends on the series. In fitting model (1.3), we also found that incorporating non stationarity reduces the values of lag parameters with respect to the stationary case. Then the time-varying unconditional variance has an important contribution to volatility.

The paper is organized as follows. In Section 2, we introduce our notations and we describe the basis of our method for statistical inference in a tv-ARCH model for which some coefficients are assumed to be non time-varying. In Section 3, we give the asymptotic results for our estimators and we discuss the problem of semiparametric asymptotic efficiency using the LAN theory. Statistical testing and their practical implementation are considered in Section 4 and Section 5 is devoted to real data applications. All the proofs of our results are postponed to the supplementary material which also contains many simulation studies showing the good behavior of our methodology. The Matlab codes and the data sets discussed in Section 5 are available at the URL

https://github.com/time-varying/tests-and-estimation-for-tv-ARCH-

2 Semiparametric volatility and tv-ARCH processes

2.1 Formulation and notations

In this section, we consider semiparametric versions of model (1.1), assuming that some of the ARCH coefficients are not time-varying. For , let and be two random vectors of size and respectively, with and defined as follows. We split the interval into two parts and with and . If , we set , with the convention if . If , we set . The vector is defined similarly, replacing the ’s with the ’s. In particular, the coordinates of the random vectors and form a bipartition of the set . Now, we assume that the coefficients vector is constant. We also set . Then the model writes

| (2.1) |

for . Throughout this paper, we will assume that for all realization in the probability space, is a path of a stationary ARCH process with noise and coefficients . From this convention, one can get a local approximation of a tv-ARCH process by stationary ARCH processes with parameters . See Lemma in the supplementary material for details.

2.2 Estimators of the parametric part

Considering the square of the process (2.1), statistical inference in model (2.1) can be viewed as a linear regression problem. More precisely, we have for ,

| (2.2) |

In the sequel, we consider a sequence of weights such that is a measurable function of and . For stating our results, we will only consider sequences of the form

| (2.3) |

where the ’s are positive and Lipschitz continuous functions defined over . The use of this kind of weights is classical in weighted least squares estimation in order to relax moment conditions on the marginal distribution or to gain in efficiency. The first goal of our procedure is to estimate the parameter . This is the most difficult part of our methodology since a consistent estimate is expected. Once an estimate with the classical parametric rate of convergence is available, a pointwise estimate of parameter can easily be obtained. One can just plug in (2.2) and apply standard nonparametric methods (in this paper we will use the local weighted least-squares method studied in Fryzlewicz et al. (2008)). Our aim here is to first eliminate the nonparametric component . Our approach is classical in the setting of partially linear models, for which the regression function involves a parametric component and a nonparametric component (see for example Härdle et al. (2000), Chapter for some results in the case of time series). However, our method is based on nonparametric estimation of linear projections of and onto the subspace generated by the components of instead of a nonparametric estimation of the conditional expectations. Moreover, our two-step approach involving some weights and leading to semiparametric efficient estimates is not common for nonstationary time series and no existing results from the theory of partially linear models can be used here for our purpose. Here, our approach can be also interpreted as a partial regression. For stationary ARCH processes, estimation of the whole set of parameters using a regression model for the squares and least squares estimation has been studied by Bose and Mukherjee (2003) and Horváth and Liese (2004).

Now we introduce our estimator. We first multiply the two members of equation (2.2) by . If and denote the (componentwise) orthogonal projection of and onto the linear subspace generated by the coordinates of , it is easily seen that

| (2.4) |

The use of these orthogonal projections are natural in order to eliminate the nuisance parameter and to get a partial regression involving parameter only. Let us introduce some notations for expressing these projections. For , we set

where

Then setting

we have

and equation (2.4) writes

The idea is now to use a least squares estimator for . Of course, in order to obtain a feasible estimator, it is necessary to first estimate the two quantities and . To this end, we consider

where for is a kernel and is a bandwidth parameter. Throughout this paper, the kernel is assumed to be absolutely continuous and with support . Then we set

| (2.5) |

Now we introduce the following notations. The quantities

estimate and respectively. Our estimator of parameter will be denoted by and minimizes the function defined by

We get

| (2.6) |

It is now possible to define an estimate of parameter for by minimizing the function

for an integer such that (e.g where denotes the integer part of a real number ). Since the nonparametric estimation of the function requires a less restrictive assumption on the bandwidth parameter than for the estimation of parameter , we introduce a new bandwidth . This leads to the estimate

| (2.7) |

Note.

Expression and involve the inverse of the matrix . One can show that

See Lemma and its proof. However invertibility problems can occur when the noise has a mass at point , for instance. For simplicity, we always assume that all these matrices are invertible. Studying our estimator on an event with probability tending to one only complicates the statements and proofs of our results by adding some indicator sets but does not change the used approach. One can also show that this distinction is unnecessary for a noise having a density.

3 Asymptotic results

3.1 Estimation of the parametric component

Our first result shows that the estimator (2.6) is consistent under some conditions. Here are our main assumptions.

- A1.

-

For , the function is non-negative and Lipschitz continuous. The function is positive and Lipschitz continuous. Moreover,

- A2(h).

-

For the integer , there exists a real number such that .

Assumption A1 is the classical contraction condition used in Fryzlewicz et al. (2008) to define tv-ARCH processes. Assumption A2(h), used for different values of in the sequel, implies a restriction on the noise distribution. Let us mention that this condition does not restrict the moment condition for the marginal (in the stationary case, i.e when the ’s are deterministic, assumption A1 is the necessary and sufficient condition for the condition ).

In the sequel, will denote the stationary ARCH process with coefficients . Then we will use the notation (resp. , ) for the stationary approximation of (resp. , ). For example,

Theorem 1.

Assume that assumptions and hold, and

.

Then we have the following convergence in distribution:

with

and

Notes.

-

1.

The bandwidth conditions used in Theorem 1 are classical for estimating the parametric component in partially linear models. With this restriction, the nonparametric estimation step involved in the expression of becomes negligible (i.e for , can be replaced with without changing the asymptotic behavior of ). Let us explain the rule of these conditions. Some nonparametric estimates are introduced to approximate the two ratio and . But, up to ( denotes a positive constant), this two ratio can be seen as some Lipschitz functions of (see Lemma in the supplementary material). The mean square error for the kernel estimation of a Lipschitz functional in a regression model with deterministic design is bounded by (up to a constant). Then our bandwidth conditions entail that this mean square error converges to zero with a faster rate than .

-

2.

The goal of the proof of Theorem 1 is to show that the asymptotic distribution of is the same as if the two quantities , are replaced by , respectively. Hence, the control of sums involving differences between these quantities are shown to be negligible. To this end, we make Taylor expansions and bound the variance of some multiple weighted sums appearing in this expansion using Lemma given in the supplementary material.

-

3.

The asymptotic variance in Theorem 1 can be estimated consistently using the data. Indeed, the proof of Theorem 1 given in the supplementary material shows that

Moreover, we have

(3.1) Then an estimate of can be obtained if we replace with , with a pointwise estimate (see Theorem 3) and using the same kind of empirical counterpart as for .

The asymptotic variance given in Theorem 1 depends on some weights . One can show that its minimal value (in the sense of non-negative definite matrices) is obtained for the choice . Indeed, setting and , where

we have for all ,

Then if , we have from the Cauchy-Schwarz inequality

where . Now setting and for , we get

Then we have proved the following result.

Proposition 1.

Now, we show that it is possible to construct an estimate of parameter which has the asymptotic variance given in Proposition 1. A natural candidate is obtained by replacing the weights in (2.6) with an estimation of the optimal weights . We set where

is an estimator of . The sequence is a sequence of positive real numbers such that . The use of this sequence is just technical and avoids possible small values for the fitted volatility which is not ensured to be bounded away from for finite samples. However, for a large sample size, our simulations show that the choice does not alter the performance of the plug-in estimate. Let us define the quantities

We also set

Now we introduce the following notations in order to simplify the expression of our estimator.

Our plug-in estimate of parameter is now defined by

With respect to Theorem 1, we impose more restrictive assumptions.

- A3.

-

has moments of any order.

- A4.

-

For , the coefficient is a positive function.

Theorem 2.

Assume that the assumptions , and hold and , for some . Then we have

3.2 Estimation of the nonparametric component

Now let us investigate the asymptotic properties for time-varying coefficients estimate defined by (2.7). The estimator appearing in the expression (2.7) is constructed using the initial bandwidth parameter which satisfies the assumptions of Theorem 1.

Theorem 3.

This result is similar to that obtained in Fryzlewicz et al. (2008), Proposition . The part can be interpreted as a term of deviation with respect to stationarity. As pointed out in Fryzlewicz et al. (2008), this term satisfies . One can easily check that the optimal asymptotic variance in Theorem 3 corresponds to the choice for the weights. Thus, a plug-in approach is natural. We set , where

and is a sequence of positive real numbers which now plays the rule of the sequence previously used for the optimal estimator . Once again, this choice is only technical and we impose here . Then we define the following estimator of parameter .

where for , is obtained as but replacing with .

Theorem 4.

Assume that assumptions , and hold, and for a given integer . Then, if , we have

where

-

-

-

.

Moreover, .

Notes

- 1.

-

2.

When all the coefficients of the volatility are time-varying, replacing by , we recover the expression of the optimal asymptotic variance given in Fryzlewicz et al. (2008) for the (local) weighted least-squares estimation. This asymptotic variance coincides with that obtained with the local QML estimator studied in Dahlhaus and Subba Rao (2006). However, a crucial assumption in Theorem 4 is the positivity of all the coefficients of the volatility. To avoid this restriction, Fryzlewicz et al. (2008) consider the sequence of weights where is a nonparametric estimate of . For the nonparametric estimation of the whole set of coefficients, they show that the corresponding weighted least squares estimator is asymptotically normal, even if the ARCH coefficients are only nonnegative, but at the price of a small loss of efficiency. We claim that the weights can also be used in our context to obtain a result similar to Fryzlewicz et al. (2008), Proposition . Details are omitted.

-

3.

As usual for this kind of nonparametric estimation, a better finite sample approximation of the distribution of the parameter estimators can often be obtained using bootstrap methods. With straightforward modifications, it is possible to use the bootstrap method studied in Fryzlewicz et al. (2008) (see Section of that paper) to obtain pointwise confidence intervals for the components of . Since this paper is mainly devoted to testing and estimating some non-time varying coefficients, we will not consider this bootstrap scheme.

- 4.

3.3 Asymptotic semiparametric efficiency

For Gaussian inputs (i.e, ), it is possible to show that the matrix given in Proposition 1 is a lower bound in semiparametric estimation. We refer the reader to Bickel et al. (1998) for a general introduction to semiparametric models and the problem of efficient estimation of a finite dimensional parameter in such models. In our case case, the problem of semiparametric efficiency for estimating the parameter involves triangular arrays. This is why we will use an abstract result using the classical formalism presented in van der Vaart and Wellner (1996) (see Chapter ). Intuitively, one can see the matrix as the smallest asymptotic variance obtained for estimating in submodels for which the nuisance parameter is projected onto a finite dimensional space of square integrable functions. Formally, the approach consists in writing a LAN expansion of the likelihood ratio and then using a general convolution theorem. In the sequel, we set for , . Then is an Hilbert space for the classical scalar product

However, in the sequel, the space will be endowed with an equivalent scalar product defined by

where

Now, we denote by the set of Lipschitz functions and we set where (resp. ) is the dimension of vector (resp. ). Then is a linear subspace of . The set will be referred to the tangent space. For Gaussian inputs, we first derive a LAN expansion for the (conditional) likelihood ratio. We denote by the conditional distribution .

Proposition 2.

Assume that where the coordinates of and are positive. Then we have

where

Moreover,

From this LAN expansion, we derive a lower bound for the asymptotic variance of regular estimators of .

For , we set . Then, the sequence of parameters is regular: if is the projection operator defined by , then

Corollary 1.

If the assumptions of Proposition 2 hold, then the adjoint operator of is given by

Consequently, the limit distribution of a regular estimator of equals the distribution of a sum of independent random vectors of and such that

4 Statistical testing

4.1 Testing parameter constancy

For a real data set, it is necessary, before applying the methodology given in Section 2, to test if a coefficients vector of the form is time-varying or not in model (1.1). This is equivalent to test model (2.1) versus model (1.1). When and , such a statistical test is interesting for deciding if model (1.3) is a convenient restriction of the tv-ARCH model. This case is of particular interest for real data applications. In Zhang and Wu (2012), a procedure is proposed for testing if some coefficients are constant in a general time-varying regression model. The null hypothesis is : constant. The test statistic used in Zhang and Wu (2012) is based on a distance between an estimate under the alternative and an estimate under the null hypothesis. In this part, we derive asymptotic properties of this test for tv-ARCH processes. For simplicity, we will only consider some estimates without plug-in (i.e we fix a sequence of weights of the form (2.3) and use the corresponding least-squares estimates). Let us first introduce some additional notations.

For a function , we set and for ,

Setting for , and for , , the kernel estimate of the full vector of ARCH coefficients is given by (see Fryzlewicz et al. (2008))

where . Then we set where is the matrix of size defined by . Note also that . We also set and

Let be a family of positive definite matrices of size such that is a Lipschitz function. Finally, we set for ,

We define our test statistic by

| (4.1) |

The proof of the following theorem is given in the supplementary material.

Theorem 5.

Notes

-

1.

As pointed out in Zhang and Wu (2012), if we are interested in prediction, the matrix can be chosen as the asymptotic variance of the kernel estimate (which has to be estimated in practice). In our numerical studies, we will use the simple choice where denotes the identity matrix of size .

-

2.

Quantities and involved in the bias and asymptotic variance in (4.2) can be estimated consistently, taking empirical counterpart. Then we obtain a pivotal statistic

and one can reject the null hypothesis for large values of this statistic. However, in practice, such nonparametric tests suffer from the slow convergence in Theorem 5. As in Zhang and Wu (2012), one can use a Monte-Carlo type procedure which can improve the finite-sample performance (a similar Monte Carlo procedure is also used in Patilea and Raïssi (2014)). Note that the result of Theorem 5 is valid for i.i.d series with a standard Gaussian marginal distribution. In particular, if denotes the pivotal statistics computed with an i.i.d sample of standard Gaussian variables, we have in distribution. Then one can use the quantiles of the distribution of to compute the critical values for the test (instead of the Gaussian quantiles). Let us give the details of the method proposed in Zhang and Wu (2012). We assume that the bandwidth has been already selected.-

•

First simulate samples of size of i.i.d Gaussian random variables. For each sample, compute the values of the estimators and as well as the realization of the pivotal statistics .

-

•

Then, from these realizations of the random variable , compute the empirical quantile of order .

-

•

Reject if is greater than .

-

•

-

3.

In Zhang and Wu (2012), the power of the test under some local alternatives is studied (see Theorem of this paper). A similar result can be derived here under the assumptions of Theorem 5. In particular, for some local alternatives of the form , with and a Lipschitz function defined over , the power of the test still converges to .

4.2 Testing if a constant parameter is equal to zero

In this part, we consider model (2.1) and our goal is to test whether the vector is equal to zero. Two approaches are discussed below.

-

1.

One possibility is to use the asymptotic normality of the estimator given in Theorem 1. Under the null hypothesis : , the asymptotic distribution of is that of a centered Gaussian vector with covariance matrix . We have already discussed how to estimate the covariance matrix . If denotes such an estimate, the statistics is asymptotically distributed as a with degrees of freedom (here denotes the euclidean norm on ). As for the test given in the previous subsection, one can use a Monte Carlo method instead of using the quantiles of the asymptotic distribution (the convergence in distribution of the previous statistics is quite slow because of the incorporation of nonparametric kernel estimates). If a bandwidth is selected, one can simulate samples of Gaussian i.i.d random variables and compute the corresponding values of our statistics. From these values, we can compute the empirical quantile of order and reject the null hypothesis if . This test has an asymptotic level and a power converging to under a fixed alternative. However such approach is not completely natural because the value is on the boundary of the parameter space, our test is similar to the bilateral test for testing the hypothesis in regression models and we ignore the sign of . This will result in a loss of power and it is more natural to consider a statistics based on the random vector . The vector will be called truncated least squares estimator. As discussed in Francq and Zakoïan (2008) for stationary ARCH processes, truncated least squares estimators are natural for testing if some lag coefficients are equal to zero. However, the limiting distribution of this truncated random vector is that of where is a Gaussian vector, with dependent entries in general. Then, except if is diagonal, it is not possible to get a pivotal statistics from truncated least squares estimators. Then the Monte-Carlo method used for testing parameter constancy cannot be applied. Note also that bootstrapping the model is not appropriated here because the bootstrap is generally inconsistent for testing a parameter on the boundary (see for instance Andrews (2000) for this problem). However, when denotes the full vector of lag coefficients, it is possible to use truncated least squares and the Monte Carlo method, provided . This point is discussed below.

-

2.

When is the full vector of lag coefficients, the problem is to test model (1.2) versus model (1.3). For testing if the lag coefficients are equal to zero in model (1.3), our test is based on the following result. The following notation will be used. If , we set . Note that is an estimator of .

Proposition 3.

Assume that A2(4) holds and that with , where are positive constants. Then under ,

satisfies where standard Gaussian vector and

Testing the second order dynamic.

From this result, we reject for large values of the statistics where is a consistent estimator of . Typically one can choose

which gives a consistent estimate under . A first solution is to reject if is larger than the quantile of order of the distribution of the random variable . But the statistics is also asymptotically pivotal and its quantiles can be approximated by a Monte Carlo procedure similar to that used for testing parameter constancy.

Notes

- 1.

-

2.

In the stationary case, two benchmark tests are usually used for testing the second order dynamic: the Lagrange multiplier test of Engle (1982) and the portmanteau test of McLeod and Li (1983). Patilea and Raïssi (2014) have recently extended these two tests for model (1.3), taking in account of nonstationarity. Here we provide an alternative test based on a direct estimation of the lag coefficients. A comparison of the different approaches is beyond the scope of this paper. Let us observe that in the stationary case, the constant in Proposition 3 is equal to whereas in the nonstationary case, this constant is a correction factor which can be written

The correction factor also appears in the asymptotic results of Patilea and Raïssi (2014) (see the ratio appearing in the two statistics used in that paper). Ignoring this factor leads to an oversized test and the null hypothesis will be often rejected when the data are independent but not identically distributed. Moreover, let us notice that our moment condition for the noise distribution is less restrictive for applying the test (a moment greater than is assumed in Patilea and Raïssi (2014)).

-

3.

One can study the power of our test under local alternatives of type where is a vector of nonnegative real numbers. One can show that if and the bandwidth satisfies and , then

where is the quantile of order of the distribution of . Details are omitted.

5 Real data applications

Before real data applications, let us provide some recommendations on the choice of tuning parameters.

5.1 Choice of tuning parameters

The practical implementation of our estimation and testing procedures requires the choice of some weights , some bandwidth parameters as well as the number of lags in the model. In this subsection, we discuss the practical choices of these parameters. In all our studies, the kernel will be the Epanechnikov kernel. For simplicity, only one bandwidth parameter will be selected for the semiparametric models (this means that we set in (2.7)). We use a cross-validation method as specified below. The selected bandwidth will be used for the tests. For the tests, the Monte-Carlo procedure will be always applied with samples of i.i.d standard Gaussian random variables.

-

•

In practice, a sequence of weights has to be chosen for applying our method. One possibility is to use the weights suggested in Horváth and Liese (2004). In our implementation, we use the weights where is an estimate of the average of the variance . There are several advantages in using these weights. First, the lag estimates obtained in model 1.3 do not depend on the scale of the returns, a property always satisfied for the true lag coefficients (if denotes the price at time , or are two different scales used in practice). Moreover, for stationary Arch processes, this choice is equivalent to the weights used in Fryzlewicz et al. (2008). We also noticed better finite sample performances for our tests and inference procedures with this choice. However, the introduction of the random quantity is not taken in account in our theoretical results. But, inspection of our proofs shows that the conclusions of the theorems remain unchanged if . The latter condition is satisfied if for (this can be justified using the moment inequality given in Fryzlewicz et al. (2008), see Lemma A2). A sufficient condition for the finiteness of this moment is which is more restrictive than the initial condition given in A3. Despite this slight restriction, we only consider the aforementioned sequence of weights in the sequel.

- •

-

•

For model (1.3), we choose the bandwidth by minimizing

Here for , is the version of (see (2.5)) defined as , and . This type of cross-validation is a weighted version of the method proposed by Hart (1994) for AR models with a time-varying mean. Note that minimizing the latter function with respect to , being fixed, leads to an estimate close to the estimate defined in (2.6).

-

•

Finally, we discuss the selection of the number of lags in model 1.1. An information criterion has been studied recently by Zhang and Wu (2012) for time-varying regression models. It is possible to adapt the approach used by these authors to our setting. To this end, we define for ,

where , , are the coefficients estimates obtained for the tv-ARCH with lags but computed with the weights and is a vanishing sequence of positive numbers. The goal of the selection procedure is to minimize in the spirit of AIC or BIC criterion used for regression models. The bandwidth is selected by cross validation for the tv-ARCH model with lags. Of course, condition on the decrease of has to be imposed to get consistency (i.e if is the true number of lags). Inspecting the proofs of Lemma A and Theorem in Zhang and Wu (2012), we find that condition guarantees consistency (using the arguments of the proof of Theorem , one can show that the quantity in Lemma A of Zhang and Wu (2012) can be replaced with in our context). For real data applications we choose where is selected using cross-validation. Our intensive simulation study reported in the supplementary material shows that this choice gives reasonable performances. This choice can be also justified using the argument given in Zhang and Wu (2015): can be seen as the effective number of parameters in kernel smoothing. Hence our choice has a similarity with the Hannan-Quinn information, except that we gave up the constant with used in Hannan and Quinn (1979). We found that adding such a factor underestimates the order in our case. A precise justification of our choice using a version of the law of iterated logarithm is not the goal of this paper. However, one can notice that applying cross-validation on an interval of type is compatible with our consistency condition. In the applications, the maximal number of lags is set to .

Using the approach described above, we conducted an extensive simulation study. Some numerical experiments are reported in the supplementary material and show the good behavior of our method for various simulation setups. This simulation study shows that our estimators and tests have reasonable performances for the sample sizes considered in the sequel. Here we only report the results obtained with real data.

For real data applications, the bandwidth will be always chosen using CV over a grid of the form where and are two positive constants (we recall that is the optimal rate of convergence for the bandwidth in the nonparametric estimation of a Lipschitzian regression function). We will also use some acronyms for our models. Model tv denotes the tvARCH model with lags (the case refers to model (1.2)) while model sptv denotes model (1.3) with . In the sequel, we consider two currency exchange rates and one stock market index. The log returns of the initial series will be modelized with ARCH processes.

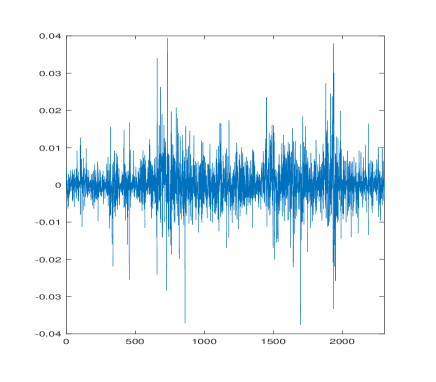

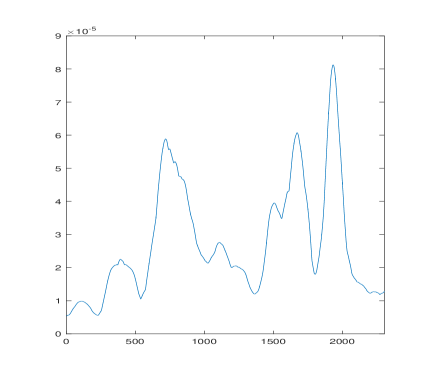

5.2 Exchange rate USD/Euro

In this subsection, we study the exchange rate series between the US Dollar and the Euro. We consider the period from January , to February , . The sample size is . As usual for this type of series, the autocorrelograms suggest correlation for the squares of the transformed series.

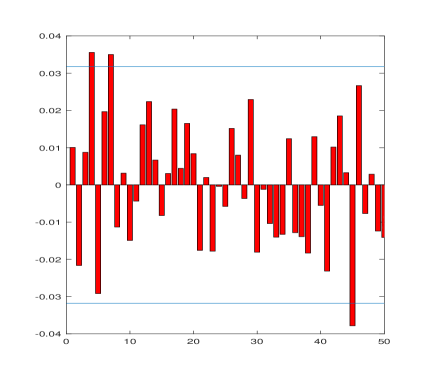

For this data set, the information criterion selects . To confirm this choice, we apply our procedure with . The results for testing the hypothesis of non time-varying coefficients are reported in Table 1. The intercept function seems not constant in contrast to the lag coefficients for which it is not possible to reject the null hypothesis. Fitting a sptv process gives small negative values for the lag coefficients and it is of course not necessary to test if they are equal to zero. This conclusion suggests an absence of second order dynamic for this series. We refer the reader to Granger and Stǎricǎ (2005) and Herzel et al. (2006) for other analysis suggesting a similar behavior for some financial time series.

| Non t-v | Non t-v | Non t-v | Non t-v | |

|---|---|---|---|---|

A plot of the series with the final estimate of the intercept function is given Figure 2.

5.3 A second example: the exchange rates between the US Dollar and the Indian Rupee

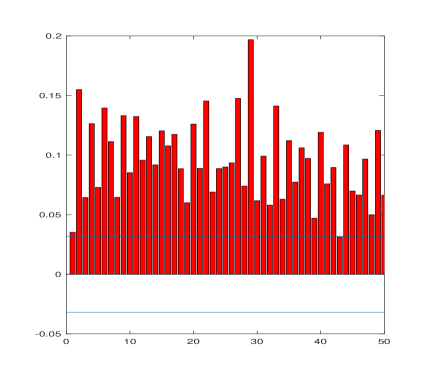

In this subsection, we analyze the exchange rates series between the US Dollar and the Indian Rupee over the period starting from December , to February , . The sample size is . The information criterion selects lag for this series. From the values reported in Table 2, the hypothesis of a constant intercept function is clearly rejected but it is not possible to reject the assumption of a non time-varying first lag coefficient. Fitting a sp process gives a small but significant lag estimates (the value for testing the second order dynamic is less than ). In contrast, fitting a stationary ARCH process with one lag (one can simply use and our procedure) leads to (s.e ) and several significant lag estimates are found for larger values of .

| Non t-v | Non t-v | |||

|---|---|---|---|---|

| (s.e ) |

5.4 A classical stock market index: the FTSE

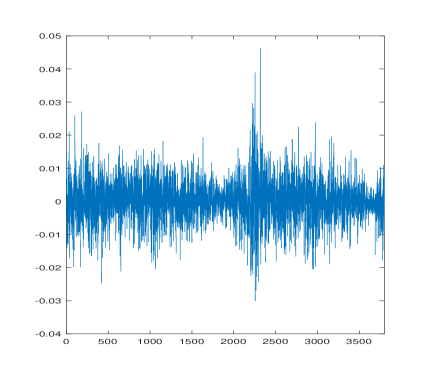

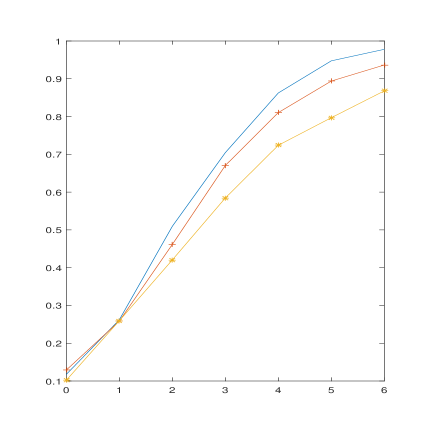

Finally, we consider the closing values of the FTSE index from January , to March , , taking as usual the logged and differenced daily returns. Our information criterion selects lags. Testing constancy of the intercept function gives a value of and the value for testing constant lag coefficients is . Hence, the assumption of constant lag coefficients is rejected at level (testing constancy of the third and fourth coefficients gives the p-values and respectively, the other values exceed ) and considering a tv-ARCH process for this data set could be interesting. We also fit a sptvprocess. The estimated lag parameters and their standard errors are reported in Table 3. The value for testing the absence of second order dynamic is close to zero.

| (s.e ) | (s.e ) | (s.e ) |

| (s.e ) | (s.e ) |

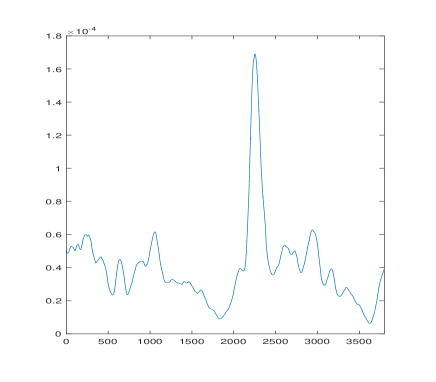

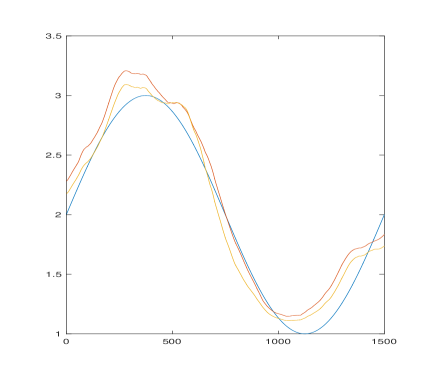

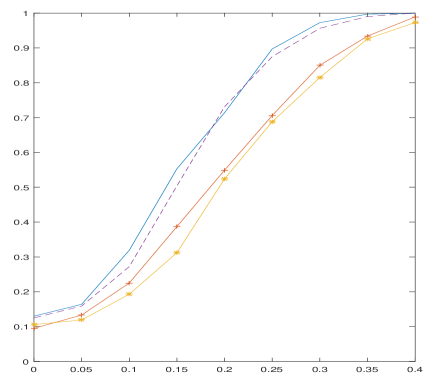

Here selecting the number of lags is important because fitting a sptvprocess for instance does not give significant lag estimates and the selected bandwidth for is very small. In Fryzlewicz et al. (2008), it is suggested that stationnary GARCH models give better forecasts for stock market indices than tvARCH processes and that this result could be explained by a more stationarity behavior of these series with respect to currency exchange rates. This observation is compatible with our analyze of the FTSE index on this period of time which suggests that adding non linearity has a tendency to take away non stationarity, with larger selected bandwidths. However, Figure 4 shows that incorporating a time-varying unconditional variance significantly reduces the values of ARCH parameters. In Figure 4, two extreme cases are observed. When , the sum of lag coefficients becomes arbitrary small whereas the value (which corresponds to the fitting of a stationnary ARCH process) leads to larger lag estimates. Moreover, in fitting a sptv process, the ratio has an average of (s.e ) which means that the contribution of the time-varying intercept has a strong contribution to volatility.

Acknowlegements.

We would like to thank two anonymous referees, the Associate Editor and the Joint Editor for their constructive comments which helped to improve the presentation of the results and some methodological aspects. We also thank Valentin Patilea for numerous suggestions about nonparametric kernel estimation and bandwidth selection.

References

- Andrews (2000) D.K.W Andrews. Inconsistency of the bootstrap when a parameter is on the boundary of the parameter space. Econometrica, 68:399–405, 2000.

- Bickel et al. (1998) P.J. Bickel, C.A.J. Klaassen, Y. Ritov, and J.A. Wellner. Efficient and Adaptive Estimation for Semiparametric Models. Springer-Verlag New York, 1998.

- Bose and Mukherjee (2003) A. Bose and K. Mukherjee. Estimating the arch parameters by solving linear equations. J. Time Ser. Anal., 24:127–136, 2003.

- Dahlhaus (1997) R. Dahlhaus. Fitting time series models to nonstationary processes. Ann. Statist., 25:1–37, 1997.

- Dahlhaus and Subba Rao (2006) R. Dahlhaus and S. Subba Rao. Statistical inference for time-varying arch processes. Ann. Statist., 34:1075–1114, 2006.

- Dahlhaus and Subba Rao (2007) R. Dahlhaus and S. Subba Rao. A recursive online algorithm for the estimation of time-varying arch parameters. Bernoulli, 13:389–422, 2007.

- Dedecker et al. (2007) J. Dedecker, P. Doukhan, J.-R. Leon, S. Louhichi, and C. Prieur. Weak dependence, with examples and some applications. Springer Berlin, 2007.

- Engle (1982) R. Engle. Autoregressive conditional heteroscedastic with estimates of the variance of united kingdom inflation. Econometrica, 50:987–1007, 1982.

- Engle and Rangel (2008) R. Engle and J.G. Rangel. The spline-garch model for low-frequency volatility and its global macroeconomic causes. Rev. Financ. Stud., 21:1187–1222, 2008.

- Francq and Zakoïan (2008) C. Francq and J-M. Zakoïan. Estimating arch models when the coefficients are allowed to be equal to zero. Austrian J. Stat., 37:31–40, 2008.

- Fryzlewicz et al. (2008) P. Fryzlewicz, T. Sapatinas, and S. Subba Rao. Normalized least-squares estimation in time-varying arch models. Ann. Statist., 36:742–786, 2008.

- Granger and Stǎricǎ (2005) C. Granger and C. Stǎricǎ. Nonstationarities in stock returns. Review of Economics and Statistics, 87:503–522, 2005.

- Hannan and Quinn (1979) E.T. Hannan and B. G. Quinn. The determination of the order of an autoregression. J. R. Statist. Soc. B, 41(2):190–195, 1979.

- Härdle et al. (2000) W. Härdle, H. Liang, and J. Gao. Partially Linear Models. Springer Physica-Verlag, 2000.

- Hart (1994) J. D. Hart. Automated kernel smoothing of dependent data by using time series cross-validation. J. R. Statist. Soc. B, 56(3):529–542, 1994.

- Herzel et al. (2006) S. Herzel, C. Stǎricǎ, and R. Tütüncu. A non-stationary paradigm for the dynamics of multivariate financial returns, volume 187 of Lecture Notes in Statistics. Springer, 2006.

- Horváth and Liese (2004) L. Horváth and F. Liese. estimators in arch models. J. Statist. Plann. Inference, 119:277–309, 2004.

- McLeod and Li (1983) A.I. McLeod and W.K. Li. Diagnostic checking arma time series models using squared-residual autocorrelations. J. Time Series Anal., 4:269–273, 1983.

- Mikosch and Stǎricǎ (2004) T. Mikosch and C. Stǎricǎ. Non-stationarities in financial time series, the long-range dependence and the igarch effect. The Review of Economics and Statistics, 86:378–390, 2004.

- Patilea and Raïssi (2014) V. Patilea and H. Raïssi. Testing second-order dynamics for autoregressive processes in presence of time-varying variance. J. Amer. Statist. Assoc., 109:1099–1111, 2014.

- Pollard (1984) D. Pollard. Convergence of stochastic processes. Springer Verlag, 1984.

- Subba Rao (2006) S. Subba Rao. On some nonstationary, nonlinear random processes and their stationary approximations. Adv. in App. Probab., 38:1155–1172, 2006.

- van der Vaart and Wellner (1996) A.W. van der Vaart and J.A. Wellner. Weak convergence and empirical processes. Springer Verlag, New-York, 1996.

- Zhang and Wu (2012) T. Zhang and W.B. Wu. Inference of time-varying regression models. Ann. Statist., 40:1376–1402, 2012.

- Zhang and Wu (2015) T. Zhang and W.B. Wu. Time-varying nonlinear regression models: Nonparametric estimation and model selection. Ann. Statist., 43:741–768, 2015.

Supplementary material

Appendix A Auxiliary results for the proofs

In this subsection, we consider a general time-varying ARCH process defined by

The different coefficients can be time-varying or not and we assume that assumption A1 is satisfied. Let us introduce additional notations.

-

•

We will always denote by the euclidean norm on for an arbitrary positive integer . The corresponding operator norm on , the set of matrices of size and with real coefficients, will be also denoted by .

-

•

If is an integrable random variable taking values in , we set .

-

•

For a sequence of bandwidths, we recall the notation

Note that . This bound will be extensively used in the sequel.

-

•

For , we set

-

•

Finally, we set for . Then is centered.

-

•

Important notations: for simplicity of notations, the quantities appearing in the statements of Theorems and will be simply denoted by for .

We first give a lemma about the regularity of tv-ARCH processes. The following result is crucial for deriving asymptotic properties of our estimators and it is a direct consequence of Theorem in Dahlhaus and Subba Rao (2006) (see also Subba Rao (2006), Theorem and the discussion in Section ).

Lemma 1.

-

1.

There exists a constant such that for all ,

From this lemma, we get .

In the sequel, we will use the following terminology.

Definition 1.

We will say that a sequence of functions , , is in the class if there exists two positive real numbers and , not depending on , such that

Now, we will consider two particular classes of processes.

Definition 2.

-

1.

A process is said to be of type I if

where is in the class .

-

2.

A process is said to be of type II if

where and are both in the class and .

-

3.

A process defined by

with of type I or II will be called a smoothing .

Notes

-

1.

An important example of processes of type II is , for . Here is given by equation () in the paper. This is due to the decomposition and to the particular form of the weights and of .

-

2.

Some smoothings appear in the expression of for . Our method for proving Theorem is to make an asymptotic expansion of the estimator and to show that the effect of the smoothings incorporated in is negligible by computing some moments. The terminology type I or type II is just used for identifying the number of smoothings which impose a moment restriction.

A.1 Covariance inequalities

Here, we assume that the assumptions of Theorem are fulfilled. Sometimes, assumption A2(h) can be used for a general value of the integer , this will be precised in the statements of our Lemma/Propositions.

Lemma 2.

Let and be two natural integers such that .

Now let be a random vector independent from

the sequence and with the same distribution as

.

For , we define recursively

Then

where and is defined in assumption .

Proof of Lemma 2

-

•

Assume first that . Then

Since , the result follows in this case.

-

•

Suppose the inequality true for any , where . Then

Then the result of the lemma follows from a finite induction.

Lemma 3.

Let be three integers such that and . Assume that with . Let be an integrable random variable measurable and a bounded and Lipschitzian function. We set

with and . Assume that . Then, we have

where, setting ,

and

where is given in Lemma 2 and (resp. ) denotes the supremum (resp. the Lipschitz constant) of the function .

Proof of Lemma 3.

-

•

Assume first that . Then, it is easy to get the bounds

- •

Then the result announced in Proposition 3 is a direct consequence of the two previous points.

The following corollary is a direct consequence of Lemma 3.

Corollary 2.

Let be an integer. Assume that with . Let four non-negative integers such that and . Let and two random variables defined by

where and are two elements of and and . Then, we have the bound

where and

A.2 Moment bounds

The two next results are crucial for proving the asymptotic normality of our estimators. In particular, Proposition 4 gives conditions under which some partial sums involving smoothings are convergent to zero with a faster rate than .

Lemma 4.

Assume that for a positive integer . Let be process of type I or II with at most processes of type II. Then for a family of deterministic positive weights, we have

where and .

Proof of Lemma 4

We set . The result is clear for . Assume that . First, we observe that from Corollary 2, we have for and ,

| (A.1) |

where does not depend on and on . Inequality (A.1) follows from the fact that the covariance given in (A.1) can be decomposed as a sum of covariances of the form given in Corollary 2 (replacing and with and respectively). Inequality (A.1) is crucial for the sequel.

We set for ,

We use a classical method for bounding sums of cross moments using bounds on covariances (see Dedecker et al. (2007) p. ). For a uplet such that , we define

Then, using the bound (A.1), we have

Since,

we conclude that

Since , we have . Then using an induction on , it easy to prove that

This proves Lemma .

Proposition 4.

Assume that for a positive integer and that . Let be processes of type I or II with at most processes of type II. We denote by the corresponding smoothings.

-

1.

If denotes a family of real numbers such that

we have, using the notations of point ,

-

2.

We have also .

-

3.

If is a process of type (resp. ), we have for all positive integer (resp. ), .

-

4.

Assume that is a process of type . Then converges to a.s.

Proof of Proposition 4

-

1.

Assume that . Taking the second order moment, we get

Using Lemma (replacing with ) with and , the last bound is . The result follows using the bandwidth assumptions.

-

2.

The second order moment writes

Using the bound and applying Lemma with , it is easy to show that this second order moment is . This leads to the result.

-

3.

This is a consequence of Lemma , using the inequality

-

4.

We have for ,

Using Lemma , the last bound is . Then the result follows from the Borel-Cantelli Lemma.

A.3 Control of deterministic quantities using local stationarity

Lemma 5.

-

1.

For , we set and . Then we have

(A.2) (A.3) (A.4) (A.5) -

2.

We have

-

3.

Setting for , we have

-

4.

We have

(A.6)

Proof of Lemma 5

-

1.

We prove the four assertions successively.

-

2.

Since

we have

The same kind of inequality holds for .

It remains to prove that(A.7) If , with , we have using (A.2),

for a suitable constant . Then, using (A.3), there exists such that . We deduce that if is large enough, the smallest eigenvalue of is bounded from below. This means that there exists an integer such that

But since each of the matrices is easily shown to be positive definite for and , (A.7) easily follows.

-

3.

For a Lipschitzian function defined over , the assumptions made on the kernel implies that

We only prove that , the proof for is similar. We use the decomposition

(A.8) From the proof of the two first points of the present Lemma, it is easily seen that

(A.9) Moreover

Since , the choice of the weights entails also

Now, since the two applications

are Lipschitz continuous, we get

(A.10) Then, the result announced follows easily from (A.8), (A.9) and (A.10).

-

4.

We use the decomposition . From the previous points, we have

Moreover for , we have using point of Proposition ,

Then we conclude that . Then (A.6) easily follows.

Appendix B Proof of Theorem

Setting

we have . Using the two relations we obtain

We also set . Observe that . This yields to the following decomposition.

where

is the main term in the asymptotic expansion of the numerator . We will use the formula

| (B.1) |

Now for , we set . Using (B.1), we have for ,

To prove Theorem , we will prove that

| (B.3) |

| (B.4) |

| (B.5) |

Proof of assertion (B.3)

To prove (B.3), we use the central limit theorem for triangular arrays of martingale differences (see Pollard (1984) Chapter VIII., Theorem ). Using the Cramer-Wold device, it is enough to prove that

| (B.6) |

for each vector . We set

Then, if , the two families and form a martingale difference. Their corresponding partial sums are asymptotically equivalent because the quantity is simply replaced by in the expression of . Indeed, we have

Using the fact that is bounded uniformly in and Lemma 5, , we deduce that , in probability. As a consequence, it is sufficient to prove (B.6) for instead of . Moreover,

The process defined by

is (coordinatewise) a process of type and Proposition 4 (point ) leads to

in probability.

Moreover, using Lemma 1, Lemma 5 (A.3) and some Lipschitz properties, one can show that

Then we get , in probability. Next, we check the Lindberg condition. If , we have

We easily deduce that in probability. This proves (B.6) and (B.3) follows.

Proof of for

.

We only prove the result for . The two other cases can be treated in the same way. We set . The proof of the result follows from the following points.

- 1.

- 2.

-

3.

Using the same arguments as for point , one can easily show that

- 4.

Proof of for

.

We only prove the result for , the proof for the case is similar. Here, we only use the basic decompositions

| (B.9) |

for and with

Then we have

where . It remains to prove that for ,

| (B.10) |

We only prove (B.10) for , the proof for being the same. The proof easily follows from the three following points.

-

1.

From Lemma 5 () and our bandwidth condition, we have

- 2.

-

3.

Finally, we show that

(B.11) We have , where is defined in the previous point. We have (see Lemma 5, point ) and

Without loss of generality, one can assume that is an integer. Using Proposition 4 (point ), we have Moreover, using convexity, the moment assumption on the noise and the fact that is bounded,

Then assertion (B.11) easily follows from the condition .

B.1 Proof of assertion B.5

Appendix C Auxiliary results for the proof of Theorem

Corollary 3.

Let be a process of type . We denote by the corresponding smoothing. Then, under the assumptions of Theorem , we have

Consequently, if for , is a smoothing then

Proof of Corollary 3

We set . Then using the point of Proposition , we have

where denotes a generic constant and is arbitrary. Since, , the result follows from the assumptions made on .

Finally, we state a Lemma which will be useful for the proof of Theorem . For a matrix-valued process , measurable with the sigma field , we will use the equality when . We also introduce additional notations. For , we define as , replacing with .

Lemma 6.

Assume that the assumptions of Theorem hold.

-

1.

For , we have

and

-

2.

We have

with

In particular, we have with .

-

3.

We have

-

4.

For , there exists two matrices and such that

(C.1) where

Moreover, .

-

5.

For , we have , where

Moreover, .

Proof of Lemma 6

-

1.

Under the assumptions of Theorem , we recall that for all univariate smoothing (see Corollary 3). Then, applying this property coordinatewise, we have for . The announced decomposition is then a consequence of decomposition given in the paper and of Lemma 5, point . Next, the second assertion follows from the condition and Lemma 5 (point ).

-

2.

We use the decomposition

(C.2) Now, using the fact that , we get

From this decomposition, we deduce that . Then we get

which also yields to the approximation with .

-

3.

We have

Indeed, is bounded uniformly in and from point , . Then the result follows from the fact that .

-

4.

We only consider the case , the cases or being similar. Using the point , we have the decomposition

Now we set and . Moreover, we have from Lemma 3

which leads to

Then it remains to show that

(C.3) Considering the decomposition given in point , assertion (C.3) will follow if we show the two following assertions. For all real-valued sequences such that and all real-valued processes , of type or ,

(C.4) and

(C.5) where

The assertion (C.5) can be proved as follows. For and an even integer , we have

where . Using Lemma , we deduce that the right hand side of the previous inequality is But when . Using the bandwidth conditions, we get (C.5). Next, using Corollary 3 and the bandwidth conditions, we get

This proves (C.4). Finally, since and , the decomposition (F.1) holds true. Using some arguments discussed before, we easily get .

-

5.

Using the equality

the result of point is an easy consequence of the previous points.

Appendix D Proof of Theorem

We recall that for a triangular array of matrices, we will denote when

Notations.

Let us also recall the following notations.

The proof of Theorem uses the same decomposition as for Theorem . More precisely, we have

where

Using Lemma 6, it is easy to get

Then the proof of Theorem will follow from the three following points.

-

1.

We first show that for . We only consider the case , the proofs for the cases , or being similar. Using the notations introduced in Lemma 6 (points and ), we have

The proof will be a consequence of the following points.

-

•

Since is centered, we get The proof is similar to the proof given in Theorem (see the proof of for ).

-

•

Next, we prove that . First we will show that

Using Lemma 6, we have the expression

Since is centered, we have

Then, it remains to show that

(D.1) The assertion (D.1) will follow if we work with each entry of different matrices and if we prove the following property. If is a real-valued centered process of type I or II, is a real-valued smoothing of type or and , are deterministic sequences satisfying and , then

(D.2) The first assertion in (D.1) has been already proved using the bound for the covariance function of the process (see the proof of in the proof of Theorem ). Then it remains to prove the second assertion in (D.2). Writing , we have

with satisfies . Moreover, using Lemma , we have for a generic constant ,

Using the assumption , we deduce the second assertion in (D.2). This proves (D.1).

- •

-

•

-

2.

Next, we prove the following convergence in distribution: . We have

The convergence of is obtained as in the proof of Theorem . Moreover, using the expression of given in Lemma 6 and arguments which are now familiar, the convergence can be obtained.

-

3.

Finally we show that a.s. It just remains to prove that

Using the fact that and is uniformly bounded in , the first assertion follows. The second assertion has been already shown in the proof of Theorem with general weights .

Appendix E Proof of Theorem

The proof uses the arguments given in Fryzlewicz et al. (2008) (see Proposition of that paper). We have the decomposition

| (E.1) |

Note that

and using the central limit theorem for martingale differences, we obtain as in Fryzlewicz et al. (2008),

From Theorem , we have . Moreover, using Lemma 5 (point ), and the fact that is uniformly bounded in , we get

This leads to

| (E.2) |

Moreover we have

| (E.3) |

To justify (E.3), it is sufficient to show that for every real-valued process of the form with bounded and Lipschitz, we have . Using Lemma , the Lipschitz property of and the properties of the kernel , it is easy to get

For the stochastic part, we have, using Proposition , . This justifies the convergence (E.3).

Appendix F Proof of Theorem

In this proof, we will set

Then, setting , we have the expressions

As in the proof of Theorem , we have the decomposition

-

•

We first show that in probability. We set and . Define the following event

Note that we have,

and is a random variable bounded by a constant . Then we have the inclusion

But

for a suitable constant and from Theorem and Theorem , . This yields to . Then we conclude that . On the event , we have

But since , we conclude that

with . Using the properties of the kernel , this yields to

Using the arguments used in the proof of Theorem , we have in probability and the last expectation is also the limit of .

-

•

Next we show the convergence in distribution

As shown in the proof of Theorem , this convergence holds if is replaced with in the last expression and it remains to show that

(F.1) in probability. We will use the following equality

First, it is easy to show that for ,

(F.2) Indeed, using the equality

developing and using the decomposition it is clear that

is composed of terms which write as a product of factors involving some coordinates of the vector , and of one factor of type where is bounded and measurable w.r.t . Such a term is because and since is a sequence of martingale differences, we have

This proves (F.2).

-

•

Finally, we show that . We consider the event . We have of course . We will just show that

the control of the difference being the same for the two other quantities and . Since , we have . Now, on the event , we have

where

On we have for a suitable constant ,

Moreover, is bounded uniformly in . Then, we obtain for a suitably chosen constant ,

Using the fact that , the support condition on the kernel and Lemma , we conclude that

Similarly, we also get

This proves that and then . The proof is now complete.

Appendix G Auxiliary results for the proof of Theorem

In this section, we assume that the assumptions of Theorem hold true. The quantities studied in the following lemma are defined in (H.1).

Lemma 7.

We set .

-

1.

We have and for all positive integer , .

-

2.

.

-

3.

We have for all positive integer ,

-

4.

We set . We have , and .

Proof of Lemma 7

-

1.

The first assertion is obvious. For the second assertion, we use Lemma . It is sufficient to show that for some subscripts ,

where satisfies

Then the result follows from Lemma if we write the moment of order as a multiple sum.

-

2.

The result follows from Proposition .

-

3.

Using Proposition , we have . Moreover for the bias part

The first term is bounded by where does not depend on and

is or when or respectively.

-

4.

Since , note that if , then where does not depend on and (we recall that is bounded). Then it is sufficient to show that . This can be proved as in Lemma 5, point . Details are omitted. The other assertions are a consequence of the previous point and of the bound .

Lemma 8.

Let be a family of positive definite matrices such that is Lipschitz. Set . Then

where

Moreover

Proof of Lemma 8

We set for , . Moreover, let . Then

We use the decomposition with

and

Note that and .

-

•

We first show that

(G.1) To show this, we decompose

with

Since is bounded and is a sum of uncorrelated random variables, the second moment of is . Then . Moreover, one can decompose as a finite sum of terms of order . This can be easily seen taking the second moment of these terms and then using Lemma . This leads to (G.1).

-

•

Next, we prove the assertion on . We have

Next, note that for a Lipschitz function ,

This yields to

But using the fact that , the last quantity is .

-

•

Finally, we study the convergence in distribution of . The argument is to apply the central limit theorem for martingales differences. First, we show the Lindberg condition. We set . Then . It is enough to show that

(G.2) Using the independence between and , the fact that is bounded and the Burhh lder inequality, we have for a generic constant ,

This leads to (G.2), using the condition . Now, to obtain the convergence mentioned in Lemma 8, it remains to prove that

(G.3) We will use the following decomposition

where

with

and

We also set .

-

–

We first show that . We have

where . Then the last quantity is

Indeed, can be bounded by (up to a constant) and we can apply Lemma with . Since , we get the result.

-

–

Next, we show that . Using the fact that is bounded and the Burkh lder inequality, we get

Since , we find that

This proves .

-

–

Finally, we study the convergence of . First, observing that and using Lemma , we get

Then it remains to show that

(G.4) We first note that

Next, one can verify (we skip the details) that one can replace with and with without changing the limit in (G.4). Then it remains to study the limit of

where

and

Note first that

Moreover, if , we have

where . Since

and

we get (G.4).

-

–

Appendix H Proof of Theorem

The proof of Theorem uses two lemma, Lemma 7 and Lemma 8, which are stated in the next section. We set and . Under the null assumption ( is non time-varying), we use the following decomposition of the difference .

| (H.1) |

where

Note that . The first part of Theorem will follow from Lemma 8, if we show that

| (H.2) |

We set . To show (H.2), we use the previous decomposition and proceed as follows.

- 1.

- 2.

- 3.

-

4.

Under our bandwidth conditions, we have .

-

5.

Next we show that

(H.6) If is a subinterval of , we have for a positive constant ,

When , the last bound is , using Lemma 7. Then,

When , Lemma 7 leads to

Using our bandwidth conditions, this yields to

Moreover, if or , we have

Using Lemma 7 and our bandwidth conditions, we also obtain and then (H.6).

- 6.

- 7.

- 8.

The first part of the theorem is now complete. Now we prove that the asymptotic of our statistic remains the same if we replace with the estimate of Theorem . Since , we have

where and it remains to prove that

| (H.10) |

Using decomposition (H.1), we have already shown that

Using Cauchy-Schwarz inequality, it is easily seen that

Then to show (H.10), it remains to show . We have

The last equality follows after noticing that and applying Lemma componentwise. Then we get (H.10). The proof of Theorem is now complete.

Appendix I Proof of Proposition

Setting and for , we have

where . We use the decomposition

To prove the result, we will show that

| (I.1) |

and

| (I.2) |

Using (I.1) and (I.2) and some arguments given in the proof of Theorem , one can show that has the same asymptotic distribution than the same estimator but with replaced by . Then one can deduce that converges to a dimensional Gaussian vector with distribution and the result of Proposition easily follows. Let us prove (I.1) and (I.2).

-

1.

For (I.1), we decompose the sum into two terms,

The expectation of the (positive) first term is smaller to where is a positive constant. Under the assumptions of Proposition , we have . Then the latter expectation is . The variance of the second term is

It is easy to show that this variance is of order . This shows (I.1).

- 2.

The proof of Proposition is now complete.

Appendix J Asymptotic semiparametric efficiency

J.1 Proof of Proposition

We set and . Then using the inequalities

we have

with . Since is bounded, we have . Next, observe that is Lipschitz in . Setting , we have and since is a processes of type , we get from Lemma 4,

This entails . Finally, noticing that is a bounded and Lipschitz function in , we deduce from Lemma 1,

where . From Lemma 1, is continuous. This leads to

where the limit is in probability. This achieves the proof of Proposition .

J.2 Proof of Corollary

To prove the first assertion, it is enough to check the equality

| (J.1) |

for all . Using the notations , with

we have and it is easy to verify the equality

Then, it is easy to get (J.1) using the expression of the scalar product on . For the second assertion, we apply Theorem of van der Vaart and Wellner (1996), using the equality .

Appendix K Numerical experiments for inference/testing

K.1 Example of semiparametric estimation.

We first illustrate the methods of parameters inference in the semiparametric model with constant lag coefficients. We consider the noise distributions , (Student distribution with degrees of freedom) and . These three distributions satisfy the moment assumption used in Theorem , Theorem and Theorem . The number of lags is fixed to and the intercept function is defined by . We compare the estimates obtained using the procedure described in the paper and the plug-in estimates which are asymptotic optimal. Two sample sizes are considered: and . Only one bandwidth is used and selected by the CV procedure (the same bandwidth is used for estimating the intercept function and plug-in estimates are also computed using this initial bandwidth). Note that the distributions do not satisfy the moment assumption for the asymptotic normality of the plug-in estimator of lag coefficients (in Theorem , we assumed that has moments of any order but our assumption is probably not optimal). The plug-in estimator seems to have a smaller RMSE (see Table 4), even when . Observe also that our estimates are less accurate when the noise has fatter tails. The RMSE for is defined by .

K.2 Testing the constancy of coefficients in a tv(1) process.

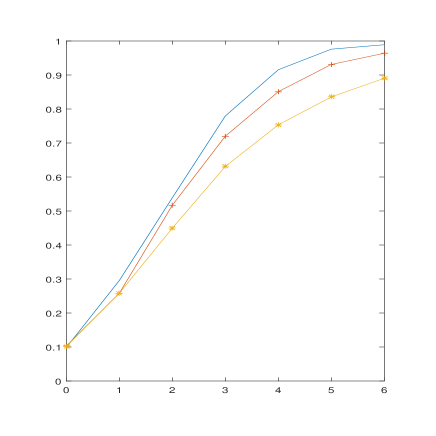

We consider here a tv-ARCH model with and or . We consider two setups. In Setup , we have and . In Setup , we have and . Considering two levels and , we approximate the probability of rejecting : constant or : constant. Results are reported in Table 5. Under , this probability has to be close to the level of the test. One can observe that using a distribution for the noise does not create size distortion. However, under the alternative , the distribution entails a smaller power than for the standard Gaussian. This suggests that the power of our tests is impacted by a fat tail noise, which is not surprising. Reasonable powers are obtained when , the order of the sample size used in our real data applications.

| Setup | Setup | ||||||||

A comparison with the Gaussian quantiles.

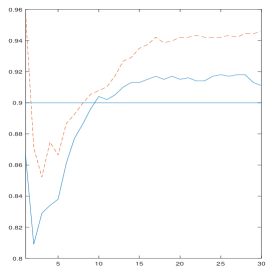

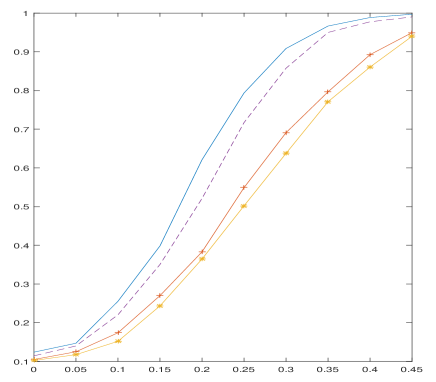

For and , we consider the setup . When and , , we compare the coverage probabilities obtained using the Monte Carlo method with the coverage probabilities using the Gaussian quantiles when and for testing the constancy of the first lag coefficient. In Figure 6, one can see that the Monte Carlo method is interesting because the coverage probabilities seem more precise and less sensitive to the bandwidth parameter if we exclude very small bandwidths.

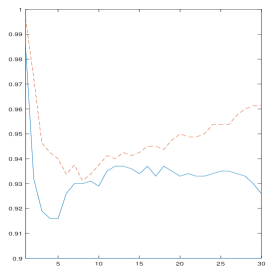

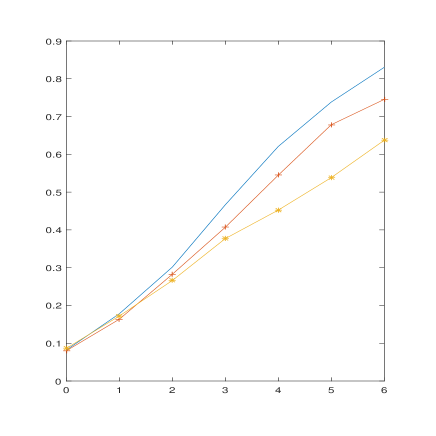

K.3 Power curves for testing non time-varying coefficients in a tv(2) process

In this subsection, we simulate approximation of the power for testing (resp. constant, constant, constant) when , , with . The noise distribution will be either Gaussian or a student distribution with degrees of freedom (we remind that Theorem is only valid when ). Figure 7 represents an approximation of the power curves when and . One can observe that a more fat tail for the noise leads to a slightly smaller power for our tests.

K.4 Testing the second order dynamic in the semiparametric model

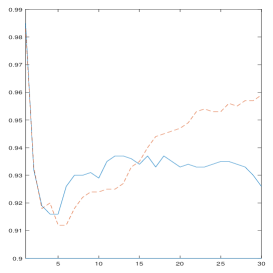

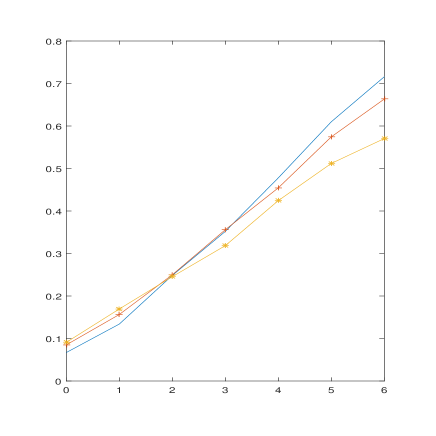

Here we assume that . The null hypothesis is . We use the procedure described in the paper after choosing the bandwidth parameter by cross-validation. We restrict our study to the case . For the simulation setup, we consider two scenarios. In setup , we consider a constant intercept . In setup , is a piecewise affine function such that and . The noise distribution will be Gaussian, , or . We also consider two sample sizes: and . Table 6 and Table 7 provide approximations of the coverage probabilities. In Figure 8, approximations of some power curves are given under the alternative , with . The results seem satisfying for the three noise distributions.

| Setup | ||

|---|---|---|

| Setup | ||

|---|---|---|

| Setup | ||

|---|---|---|

| Setup | ||

|---|---|---|

K.5 Information criterion for the number of lags in tv-ARCH processes

In this subsection, we study numerically the performance of the information criterion used for selecting the number of lags in time-varying ARCH processes. We first consider the case , with and . Two distributions are considered for the noise: the standard Gaussian and the distribution. In Table 8, we simulate models for both noise distributions and three sample sizes: , and . The results are correct for large sample sizes. As for the estimation, one observe that the performance of the criterion is sensitive to the tail of the noise distribution.

| CF | UF | OF | ||

|---|---|---|---|---|

In a second simulation setup, we consider the case , using the same intercept and setting , . In this case, the lag coefficients can be arbitrary close to zero and the true model more difficult to select. Numerical experiments are reported in Table 9. When , large sample sizes are necessary to obtain good results. Once again, one can explain this behavior by the difficulty of getting accurate estimates with such noise distribution tail when the sample size is not large enough.

| CF | UF | OF | CF | UF | OF | CF | UF | OF | ||

|---|---|---|---|---|---|---|---|---|---|---|