Junpei Komiyama \Emailjunpei@komiyama.info

\addrThe University of Tokyo

\NameJunya Honda \Emailhonda@stat.t.u-tokyo.ac.jp

\addrThe University of Tokyo

\NameHisashi Kashima \Emailkashima@i.kyoto-u.ac.jp

\addrKyoto University

\NameHiroshi Nakagawa \Emailnakagawa@dl.itc.u-tokyo.ac.jp

\addrThe University of Tokyo

\DeclareMathOperator*\argmaxarg max

\DeclareMathOperator*\argminarg min

Regret Lower Bound and Optimal Algorithm

in Dueling Bandit Problem

Abstract

We study the -armed dueling bandit problem, a variation of the standard stochastic bandit problem where the feedback is limited to relative comparisons of a pair of arms. We introduce a tight asymptotic regret lower bound that is based on the information divergence. An algorithm that is inspired by the Deterministic Minimum Empirical Divergence algorithm (Honda and Takemura, 2010) is proposed, and its regret is analyzed. The proposed algorithm is found to be the first one with a regret upper bound that matches the lower bound. Experimental comparisons of dueling bandit algorithms show that the proposed algorithm significantly outperforms existing ones.

keywords:

multi-armed bandit problem, dueling bandit problem, online learning1 Introduction

A multi-armed bandit problem is a crystallized instance of a sequential decision-making problem in an uncertain environment, and it can model many real-world scenarios. This problem involves conceptual entities called arms, and a forecaster who tries to identify good arms from bad ones. At each round, the forecaster draws one of the arms and receives a corresponding reward. The aim of the forecaster is to maximize the cumulative reward over rounds, which is achieved by running an algorithm that balances the exploration (acquisition of information) and the exploitation (utilization of information).

While it is desirable to obtain direct feedback from an arm, in some cases such direct feedback is not available. In this paper, we consider a version of the standard stochastic bandit problem called the -armed dueling bandit problem (DBLP:conf/colt/YueBKJ09), in which the forecaster receives relative feedback, which specifies which of two arms is preferred. Although the original motivation of the dueling bandit problem arose in the field of information retrieval, learning under relative feedback is universal to many fields, such as recommender systems (Gemmis09preferencelearning), graphical design (DBLP:conf/sca/BrochuBF10), and natural language processing (DBLP:conf/acl/ZaidanC11), which involve explicit or implicit feedback provided by humans.

Related work: Here, we briefly discuss the literature of the -armed dueling bandit problem. The problem involves a preference matrix , whose entry corresponds to the probability that arm is preferred to arm .

Most algorithms assume that the preference matrix has certain properties. Interleaved Filter (IF) (DBLP:journals/jcss/YueBKJ12) and Beat the Mean Bandit (BTM) (DBLP:conf/icml/YueJ11), early algorithms proposed for solving the dueling bandit problem, require the arms to be totally ordered, that is, . Moreover, IF assumes stochastic transitivity: for any triple with , . Unfortunately, stochastic transitivity does not hold in many real-world settings (DBLP:conf/icml/YueJ11). BTM relaxes this assumption by introducing relaxed stochastic transitivity: there exists such that for all pairs with , holds. The drawback of BTM is that it requires the explicit value of on which the performance of the algorithm depends. DBLP:conf/icml/UrvoyCFN13 considered a wide class of sequential learning problems with bandit feedback that includes the dueling bandit problem. They proposed the Sensitivity Analysis of VAriables for Generic Exploration (SAVAGE) algorithm, which empirically outperforms IF and BTM for moderate . Among the several versions of SAVAGE, the one called Condorcet SAVAGE makes the Condorcet assumption and performed the best in their experiment. The Condorcet assumption is that there is a unique arm that is superior to the others. Unlike the two transitivity assumptions, the Condorcet assumption does not require the arms to be totally ordered and is less restrictive. IF, BTM, and SAVAGE either explicitly require the number of rounds , or implicitly require to determine the confidence level .

Recently, an algorithm called Relative Upper Confidence Bound (RUCB) (DBLP:conf/icml/ZoghiWMR14) was proven to have an regret bound under the Condorcet assumption. RUCB is based on the upper confidence bound index (LaiRobbins1985; Agr95; auerfinite) that is widely used in the field of bandit problems. RUCB is horizonless: it does not require beforehand and runs for any duration. zoghiwsdm2015 extended RUCB into the mergeRUCB algorithm under the Condorcet assumption as well as the assumption that a portion of the preference matrix is informative (i.e., different from ). They reported that mergeRUCB outperformed RUCB when was large. DBLP:conf/icml/AilonKJ14 proposed three algorithms named Doubler, MultiSBM, and Sparring. MultiSBM is endowed with an regret bound and Sparring was reported to outperform IF and BTM in their simulation. These algorithms assume that the pairwise feedback is generated from the non-observable utilities of the selected arms. The existence of the utility distributions associated with individual arms restricts the structure of the preference matrix.

In summary, most algorithms either has regret under the Condorcet assumption (SAVAGE) or require additional assumptions to achieve regret (IF, BTM, MultiSBM, and mergeRUCB). To the best of our knowledge, RUCB is the only algorithm with an regret bound111DBLP:journals/corr/ZoghiWMR13 first proposed RUCB with an regret bound and later modified it by adding a randomization procedure to assure ) regret in DBLP:conf/icml/ZoghiWMR14.. The main difficulty of the dueling bandit problem lies in that, there are candidates of actions to test “how good” each arm is. A naive use of the confidence bound requires every pair of arms to be compared times and yields an regret bound.

Contribution: In this paper, we propose an algorithm called Relative Minimum Empirical Divergence (RMED). This paper contributes to our understanding of the dueling bandit problem in the following three respects.

-

•

The regret lower bound: Some studies (e.g., DBLP:journals/jcss/YueBKJ12) have shown that the -armed dueling bandit problem has a regret lower bound. In this paper, we further analyze this lower bound to obtain the optimal constant factor for models satisfying the Condorcet assumption. Furthermore, we show that the lower bound is the same under the total order assumption. This means that optimal algorithms under the Condorcet assumption also achieve a lower bound of regret under the total order assumption even though such algorithms do not know that the arms are totally ordered.

-

•

An optimal algorithm: The regret of RMED is not only , but also optimal in the sense that its constant factor matches the asymptotic lower bound under the Condorcet assumption. RMED is the first optimal algorithm in the study of the dueling bandit problem.

-

•

Empirical performance assessment: The performance of RMED is extensively evaluated by using five datasets: two synthetic datasets, one including preference data, and two including ranker evaluations in the information retrieval domain.

2 Problem Setup

The -armed dueling bandit problem involves arms that are indexed as . Let be a preference matrix whose entry corresponds to the probability that arm is preferred to arm . At each round , the forecaster selects a pair of arms , then receives a relative feedback that indicates which of is preferred. By definition, holds for any and .

Let be the number of comparisons of pair and be the empirical estimate of at round . In building statistics by using the feedback, we treat pairs without taking their order into consideration. Therefore, for , and , where is the indicator function. For , let be the number of times is preferred over . Then, , where we set here. Let .

Throughout this paper, we will assume that the preference matrix has a Condorcet winner (DBLP:conf/icml/UrvoyCFN13). Here we call an arm the Condorcet winner if for any . Without loss of generality, we will assume that arm is the Condorcet winner. The set of preference matrices which have a Condorcet winner is denoted by . We also define the set of preference matrices satisfying the total order by ; that is, the relation induces a total order iff .

Let . We define the regret per round as when the pair is compared. The expectation of the cumulative regret, is used to measure the performance of an algorithm. The regret increases at each round unless the selected pair is .

2.1 Regret lower bound in the -armed dueling bandits

In this section we provide an asymptotic regret lower bound when . Let the \textsuperiors of arm be a set , that is, the set of arms that is preferred to on average. The essence of the -armed dueling bandit problem is how to eliminate each arm by making sure that arm is not the Condorcet winner. To do so, the algorithm uses some of the arms in and compares with them.

A dueling bandit algorithm is strongly consistent for model iff it has regret for any and any . The following lemma is on the number of comparisons of suboptimal arm pairs.

Lemma 2.1.

(The lower bound on the number of suboptimal arm draws) (i) Let an arm and preference matrix be arbitrary. Given any strongly consistent algorithm for model , we have

| (1) |

where is the KL divergence between two Bernoulli distributions with parameters and . (ii) Furthermore, inequality \eqrefineq:drawlower holds for any given any strongly consistent algorithm for .

Lemma 2.1 states that, for arbitrary arm , an algorithm needs to make comparisons between arms and to be convinced that arm is inferior to arm and thus is not the Condorcet winner. Since the regret increase per round of comparing arm with is , eliminating arm by comparing it with incurs a regret of

| (2) |

Therefore, the total regret is bounded from below by comparing each arm with an arm that minimizes \eqrefregret_ij and the regret lower bound is formalized in the following theorem.

Theorem 2.2.

(The regret lower bound) (i) Let the preference matrix be arbitrary. For any strongly consistent algorithm for model ,

| (3) |

holds. (ii) Furthermore, inequality \eqrefineq:regretlower holds for any given any strongly consistent algorithm for .

The proof of Lemma 2.1 and Theorem 2.2 can be found in Appendix LABEL:sec:lowerboundproof. The proof of Lemma 2.1 is similar to that of LaiRobbins1985 for the standard multi-armed bandit problem but differs in the following point that is characteristic to the dueling bandit. To achieve a small regret in the dueling bandit, it is necessary to compare the arm with itself if is the Condorcet winner. However, we trivially know that without sampling and such a comparison yields no information to distinguish possible preference matrices. We can avoid this difficulty by evaluating and in different ways.

3 RMED1 Algorithm

In this section, we first introduce the notion of empirical divergence. Then, on the basis of the empirical divergence, we formulate the RMED1 algorithm.

3.1 Empirical divergence and likelihood function

In inequality \eqrefineq:drawlower of Section 2.1, we have seen that , the sum of the divergence between and multiplied by the number of comparisons between and , is the characteristic value that defines the minimum number of comparisons. The empirical estimate of this value is fundamentally useful for evaluating how unlikely arm is to be the Condorcet winner. Let the \textopponents of arm at round be the set . Note that, unlike the superiors , the opponents for each arm are defined in terms of the empirical averages, and thus the algorithms know who the opponents are. Let the empirical divergence be

The value can be considered as the “likelihood” that arm is the Condorcet winner. Let (ties are broken arbitrarily) and . By definition, . RMED is inspired by the Deterministic Minimum Empirical Divergence (DMED) algorithm (HondaDMED). DMED, which is designed for solving the standard -armed bandit problem, draws arms that may be the best one with probability , whereas RMED in the dueling bandit problem draws arms that are likely to be the Condorcet winner with probability . Namely, any arm that satisfies

| (4) |

is the candidate of the Condorcet winner and will be drawn soon. Here, can be any non-negative function of that is independent of . Algorithm 1 lists the main routine of RMED. There are several versions of RMED. First, we introduce RMED1. RMED1 initially compares all pairs once (initial phase). Let be the last round of the initial phase. From , it selects the arm by using a loop. is the set of arms in the current loop, and is the remaining arms of that have not been drawn yet in the current loop. is the set of arms that are going to be drawn in the next loop. An arm is put into when it satisfies . By definition, at least one arm (i.e. at the end of the current loop) is put into in each loop. For arm in the current loop, RMED1 selects (i.e. the comparison target of ) determined by Algorithm 2.

The following theorem, which is proven in Section 5, describes a regret bound of RMED1.

Theorem 3.1.

For any sufficiently small , the regret of RMED1 is bounded as:

where is a constant as a function of . Therefore, by letting and choosing an for arbitrary , we obtain

3.2 Gap between the constant factor of RMED1 and the lower bound

From the lower bound of Theorem 2.2, the regret bound of RMED1 is optimal up to a constant factor. Moreover, the constant factor matches the regret lower bound of Theorem 2.2 if for all where

| (5) |

Here we define if and otherwise, and . Note that, there can be ties that minimize the RHS of \eqrefineq:mostsuperior. In that case, we may choose any of the ties as to eliminate arm . For ease of explanation, we henceforth will assume that is unique, but our results can be easily extended to the case of ties.

We claim that holds in many cases for the following mathematical and practical reasons. (i) The regret of drawing a pair is , whereas it is simply for the pair . Thus, has to be much larger than in order to satisfy . (ii) The Condorcet winner usually wins over the other arms by a large margin, and therefore, . For example, in the preference matrix of Example (Table 1), as long as . Example (Table 1) is a preference matrix based on six retrieval functions in the full-text search engine of ArXiv.org (DBLP:conf/icml/YueJ11)222In the original preference matrix of DBLP:conf/icml/YueJ11, . To satisfy , we replaced and of the original with and , respectively.. In Example , holds for all , even though . In the case of a -ranker evaluation based on the Microsoft Learning to Rank dataset (details are given in Section 4), occasionally occurs, but the difference between the regrets of drawing arm and is fairly small (smaller than % on average). Nevertheless, there are some cases in which comparing arm with is not such a clever idea. Example (Table 1) is a toy example in which comparing arm with makes a large difference. In Example , it is clearly better to draw pairs (, ), (, ) and (, ) to eliminate arms , , and , respectively. Accordingly, it is still interesting to consider an algorithm that reduces regret by comparing arm with .

[Example ][caption] 1 2 3 1 0.5 0.7 0.7 2 0.3 0.5 3 0.3 1- 0.5 \subtable[Example ][caption] 1 2 3 4 5 6 1 0.50 0.55 0.55 0.54 0.61 0.61 2 0.45 0.50 0.55 0.55 0.58 0.60 3 0.45 0.45 0.50 0.54 0.51 0.56 4 0.46 0.45 0.46 0.50 0.54 0.50 5 0.39 0.42 0.49 0.46 0.50 0.51 6 0.39 0.40 0.44 0.50 0.49 0.50 \subtable[Example ][caption] 1 2 3 4 1 0.5 0.6 0.6 0.6 2 0.4 0.5 0.9 0.1 3 0.4 0.1 0.5 0.9 4 0.4 0.9 0.1 0.5

3.3 RMED2 Algorithm

We here propose RMED2, which gracefully estimates during a bandit game and compares arm with . RMED2 and RMED1 share the main routine (Algorithm 1). The subroutine of RMED2 for selecting is shown in Algorithm 3. Unlike RMED1, RMED2 keeps drawing pairs of arms at least times (Line 10 in Algorithm 1). The regret of this exploration is insignificant since . Once all pairs have been explored more than times, RMED2 goes to the main loop. RMED2 determines by using Algorithm 2 based on the estimate of given by

| (6) |

where ties are broken arbitrarily, and we set . Intuitively, RMED2 tries to select for most rounds, and occasionally explores in order to reduce the regret increase when RMED2 fails to estimate the true correctly.

3.4 RMED2FH algorithm

Although we believe that the regret of RMED2 is optimal, the analysis of RMED2 is a little bit complicated since it sometimes breaks the main loop and explores from time to time. For ease of analysis, we here propose RMED2 Fixed Horizon (RMED2FH, Algorithm 1 and 3), which is a “static” version of RMED2. Essentially, RMED2 and RMED2FH have the same mechanism. The differences are that (i) RMED2FH conducts an exploration in the initial phase. After the initial phase (ii) for each is fixed throughout the game. Note that, unlike RMED1 and RMED2, RMED2FH requires the number of rounds beforehand to conduct the initial draws of each pair. The following Theorem shows the regret of RMED2FH that matches the lower bound of Theorem 2.2.

Theorem 3.2.

For any sufficiently small , the regret of RMED2FH is bounded as:

{multline}

E[R(T)] ≤∑_i ∈[K] ∖{1}

(Δ1,i+ Δ1,b⋆(i)) ((1 + δ) logT)2d(μi,b⋆(i), 1/2)

+ O(αK^2 loglogT) + O(K e^AK - f(K))

+ O( K logTloglogT ) + O(Kδ2)

+ O(Kf(K))

,

where is a constant as a function of .

By setting and choosing an () we obtain

| (7) |

Note that all terms except the first one in \eqrefrmedtworegretsnd are . From Theorems 2.2 and 7 we see that (i) RMED2FH is asymptotically optimal under the Condorcet assumption and (ii) the logarithmic term on the regret bound of RMED2FH cannot be improved even if the arms are totally ordered and the forecaster knows of the existence of the total order. The proof sketch of Theorem 7 is in Section 5.

4 Experimental Evaluation

[Six rankers]

[Cyclic]

[Arithmetic]

[Sushi]

[MSLR ]

[MSLR ]

To evaluate the empirical performance of RMED, we conducted simulations333The source code of the simulations is available at https://github.com/jkomiyama/duelingbanditlib. with five bandit datasets (preference matrices). The datasets are as follows:

Six rankers is the preference matrix based on the six retrieval functions in the full-text search engine of ArXiv.org (Table 1).

Cyclic is the artificial preference matrix shown in Table 1. This matrix is designed so that the comparison of with is not optimal.

Arithmetic dataset involves eight arms with and has a total order.

Sushi dataset is based on the Sushi preference dataset (kamishimakdd2003) that contains the preferences of Japanese users as regards types of sushi. We extracted the most popular types of sushi and converted them into arms with corresponding to the ratio of users who prefer sushi over . The Condorcet winner is the mildly-fatty tuna (chu-toro).

MSLR: We tested submatrices of a preference matrix from zoghiwsdm2015, which is derived from the Microsoft Learning to Rank (MSLR) dataset (mslr2010; DBLP:journals/ir/QinLXL10) that consists of relevance information between queries and documents with more than K queries. zoghiwsdm2015 created a finite set of rankers, each of which corresponds to a ranking feature in the base dataset. The value is the probability that the ranker beats ranker based on the navigational click model (hofmann:tois13). We randomly extracted rankers in our experiments and made sub preference matrices. The probability that the Condorcet winner exists in the subset of the rankers is high (more than 90%, c.f. Figure 1 in DBLP:conf/wsdm/ZoghiWRM14), and we excluded the relatively small case where the Condorcet winner does not exist.

A Condorcet winner exists in all datasets. In the experiments, the regrets of the algorithms were averaged over runs (Six rankers, Cyclic, Arithmetic, and Sushi), or runs (MSLR).

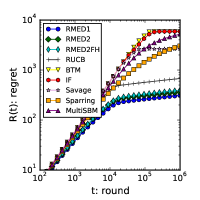

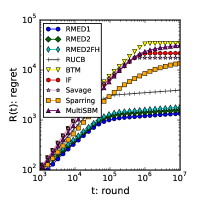

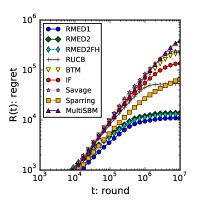

4.1 Comparison among algorithms

[Six rankers]

[Cyclic]

[MSLR ]

We compared the IF, BTM with , RUCB with , Condorcet SAVAGE with , MultiSBM and Sparring with , and RMED algorithms. There are two versions of RUCB: the one that uses a randomizer in choosing (DBLP:conf/icml/ZoghiWMR14), and the one that does not (DBLP:journals/corr/ZoghiWMR13). We implemented both and found that the two perform quite similarly: we show the result of the former one in this paper. We set for all RMED algorithms and set for RMED2 and RMED2FH. The effect of is studied in Appendix LABEL:sec:depfk. Note that IF and BTM assume a total order among arms, which is not the case with the Cyclic, Sushi, and MSLR datasets. MultiSBM and Sparring assume the existence of the utility of each arm, which does not allow a cyclic preference that appears in the Cyclic dataset.

Figure 1 plots the regrets of the algorithms. In all datasets RMED significantly outperforms RUCB, the next best excluding the different versions of RMED. Notice that the plots are on a base log-log scale. In particular, regret of RMED1 is more than twice smaller than RUCB on all datasets other than Cyclic, in which RMED2 performs much better. Among the RMED algorithms, RMED1 outperforms RMED2 and RMED2FH on all datasets except for Cyclic, in which comparing arm with arm is inefficient. RMED2 outperforms RMED2FH in the five of six datasets: this could be due to the fact that RMED2FH does not update for ease of analysis.

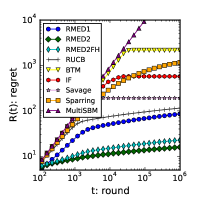

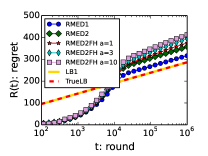

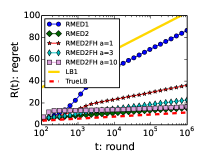

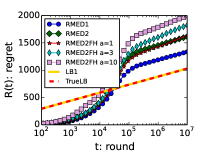

4.2 RMED and asymptotic bound

Figure 2 compares the regret of RMED with two asymptotic bounds. LB1 denotes the regret bound of RMED1. TrueLB is the asymptotic regret lower bound given by Theorem 2.2.

RMED1 and RMED2: When , the slope of RMED1 should converge to LB1, and the ones of RMED2 and RMED2FH should converge to TrueLB. On Six rankers, LB1 is exactly the same as TrueLB, and the slope of RMED1 converges to this TrueLB. In Cyclic, the slope of RMED2 converges to TrueLB, whereas that of RMED1 converges to LB1, from which we see that RMED2 is actually able to estimate correctly. In MSLR , LB1 and TrueLB are very close (the difference is less than %), and RMED1 and RMED2 converge to these lower bounds.

RMED2FH with different values of : We also tested RMED2FH with several values of . On the one hand, with , the initial phase of RMED2FH is too short to identify ; as a result it performs poorly on the Cyclic dataset. On the other hand, with , the initial phase was too long, which incurs a practically non-negligible regret on the MSLR dataset. We also tested several values of parameter in RMED2FH. We omit plots of RMED2 with for the sake of readability, but we note that in our datasets the performance of RMED2 is always better than or comparable with the one of RMED2FH under the same choice of , although the optimality of RMED2 is not proved unlike RMED2FH.

5 Regret Analysis

This section provides two lemmas essential for the regret analysis of RMED algorithms and proves the asymptotic optimality of RMED1 based on these lemmas. A proof sketch on the optimal regret of RMED2FH is also given.

The crucial property of RMED is that, by constantly comparing arms with the opponents, the true Condorcet winner (arm ) actually beats all the other arms with high probability. Let

Under , for all , and thus, . Therefore, implies that is unique with and . Lemma 5.1 below shows that the average number of rounds that occurs is constant in , where the superscript denotes the complement.

Lemma 5.1.

When RMED1 or RMED2FH is run, the following inequality holds:

| (8) |

where is a constant as a function of .

Note that, since RMED2FH draws each pair times in the initial phase, we define for RMED2FH. We give a proof of this lemma in Appendix LABEL:sec:armoptimality. Intuitively, this lemma can be proved from the facts that arm is drawn within roughly rounds and is not very large with high probability.

Next, for and , let

which is a sufficient number of comparisons of with to be convinced that the arm is not the Condorcet winner. The following lemma states that if pair is drawn times then is rarely selected as again.

Lemma 5.2.

When RMED1 or RMED2FH is run, for , ,

We prove this lemma in Appendix LABEL:sec:suboptimalpairdrawmore based on the Chernoff bound.

Now we can derive the regret bound of RMED1 based on these lemmas.