Semi-Global Solutions to DSGE Models: Perturbation around a Deterministic Path

Abstract

This study proposes an approach based on a perturbation technique to construct global solutions to dynamic stochastic general equilibrium models (DSGE). The main idea is to expand a solution in a series of powers of a small parameter scaling the uncertainty in the economy around a solution to the deterministic model, i.e. the model where the volatility of the shocks vanishes. If a deterministic path is global in state variables, then so are the constructed solutions to the stochastic model, whereas these solutions are local in the scaling parameter. Under the assumption that a deterministic path is already known the higher order terms in the expansion are obtained recursively by solving linear rational expectations models with time-varying parameters. The present work also proposes a method rested on backward recursion for solving general systems of linear rational expectations models with time-varying parameters and determines the conditions under which the solutions of the method exist.

1 Introduction

Perturbation methods applied in macroeconomics are used to expand the exact solution around a deterministic steady state in powers of state variables and a small parameter scaling the uncertainty in the economy. The solutions based on the Taylor series expansion are intrinsically local, i.e. they are accurate in some neighborhood (presumably small) of the deterministic steady state. Out of the neighborhood the solutions may behave odd, for example, can imply explosive dynamics (Kim et al., 2008). The other problem with the perturbation method is that we do not know a priori for non-trivial models how small the neighborhood must be to achieve a given level of accuracy.

The recent crisis has renewed an interest in methods that provide global solutions to DSGE models, i.e. the solutions some points of which are far away from the steady state. This may occur after a big shock hitting the economy, or if the initial conditions are far away from the steady state, the examples of this situation are the economies in transition and developing economies.

This study presents an approach based on a perturbation technique to construct global solutions to DSGE models. The proposed solutions are represented as a series in powers of a small parameter scaling the covariance matrix of the shocks. The zero order approximation corresponds to the solution to the deterministic model, because all shocks vanish as . Global solutions to deterministic models can be obtained reasonably fast by effective numerical methods333The algorithms incorporated in the widely-used software such as Dynare (and less available Troll) find a stacked-time solution and are based on Newton’s method combined with sparse-matrix techniques (Adjemian, Bastani, Juillard, Karamé, Mihoubi, Perendial, Pfeifer, Ratto, and Villemot, 2011). even for large size models (Hollinger, 2008). For this reason the next stages of the method are implemented assuming that the solution to the deterministic model under given initial conditions is known.

Higher-order systems depend only on quantities of lower orders, hence they can be solved recursively. The homogeneous part of these systems is the same for all orders and depends on the deterministic solution. Consequently, each system can be represented as a rational expectation model with time-varying parameters. In the case of rational expectations models with constant parameters the stable block of equations can be isolated and solved forward. This is not possible for models with time-varying parameters.

The other contribution of the present work is a method proposed for solving general systems of linear rational expectations models with time-varying parameters and determines the conditions under which the solutions of the method exist. The method starts with finding a finite-horizon solution by using backward recursion. Next we prove that as the horizon tends to infinity the finite-horizon solutions approach to a limit solution that is bounded for all positive time. The proposed method for solving linear rational expectations models with time-varying parameters may be valuable in itself, for example, for solving models with anticipated structural and policy changes.

Notice that whenever the deterministic solution is global in state variables so is the approximate solution to the stochastic problem. At the same time, if the parameter is small enough, then the solution obtained is close to the deterministic one. For this reason, we shall call this approach semi-global.

To illustrating how the method works we apply it to the asset pricing model of Burnside (1998). The simplicity of the model allows for obtaining the approximations in an analytical form. We compare the policy functions of the second order solution of the semi-global method with the local Taylor series expansion of orders two and six (Schmitt-Grohé, and Uribe, 2004). The results show that the semi-global solution is more accurate, in some sense, than even the sixth order of the local Taylor expansion.

This paper contributes to a growing literature on using the perturbation technique for solving DSGE models. The perturbation methodology in economics has been advanced by Judd and co-authors as in Judd (1998); Gaspar, and Judd (1997); Judd, and Guu (1997). Jin, and Judd (2002) give a theoretical basis for using perturbation methods in DSGE modeling; namely, applying the implicit function theorem, they prove that the perturbed rational expectations solution continuously depends on a parameter and therefore tends to the deterministic solution as the parameter tends to zero.

Almost all of the literature is concerned with the approximations around the steady state as in Collard, and Juillard (2001); Schmitt-Grohé, and Uribe (2004); Kim et al. (2008); Gomme, and Klein (2011). Lombardo (2010) and Lombardo, and Uhlig (2014) make use of series expansion in powers of to provide a theoretical foundation for pruning methods (Kim et al., 2008), which is aimed to avoid the explosive behavior of a solution. Andreasen, Fernández-Villaverde, and Rubio-Ramírez (2013) develop the same approach for higher-order approximations. Lombardo and Uhlig’s approach can be treated as a special case of the method proposed in the current study, namely a deterministic solution around which the expansion is used is only the steady state. Both approaches based on the perturbation methodology used in applied mathematics ( Nayfeh (1973) and Holmes (2013)). The essence of the methodology is to expand a solution in a series of powers of a small parameter, and thus obtain a set of problems that can be solved recursively. It is supposed that each of this problems is easier to solve than the original one. Actually in applied mathematics literature (Nayfeh (1973) and Holmes (2013)), the zeroth-order approximation is typically a function of time rather than a steady state as in Lombardo (2010), Lombardo, and Uhlig (2014) and Andreasen, Fernández-Villaverde, and Rubio-Ramírez (2013). Judd (1998, Chapter 13) outlines how to apply perturbations around the known entire solution, which is not necessarily the steady state. He considers a simple continuous-time stochastic growth models in the dynamic programming framework. This paper develops an approach to construct approximate solutions to discrete-time DSGE models in general form by using the perturbation method around a global deterministic path.

Despite the fact that the pruning procedure avoids the explosive behavior of a solution, it remains local, and as such may have some undesirable properties. For example, the pruning procedure might provide a first few impulse responses with wrong signs under a sufficiently large shock. This case seems even worse than the explosive dynamics since the impulse responses for a first few periods are most interesting and relevant for theoretical implications of a model as well as a policy analysis; therefore, their incorrect signs could mislead a researcher or a policymaker. In this situation the pruning procedure just conceals the real problem. As we will show in the example, the problem with a wrong sign of impulse responses can occur even in a situation where the pruning is not needed.

The rest of the paper is organized as follows. The next section presents the model set-up. Section 3 provides a detailed exposition of series expansions for DSGE models. In Section 4 we transform the model into a convenient form to deal with. Section 5 presents the method for solving rational expectations models for time-varying parameters. The proposed method is applied to an asset pricing model in Section 6, where it is also compared with the local Taylor series expansions. Conclusions are presented in Section 7.

2 The Model

DSGE models usually have the form

| (1) | |||

| (2) |

where denotes the conditional expectations operator, is an vector containing the -period endogenous state variables; is an vector containing the -period endogenous variables that are not state variables; is an vector containing the -period exogenous state variables; is the vector with the corresponding innovations; and the covariance matrix ; maps into and is assumed to be sufficiently smooth. The scalar () is a scaling parameter for the disturbance terms . We assume that all mixed moments of are finite. All eigenvalues of the matrix have modulus less than one. The problem is to find a stable solution to (1) for a given initial condition . A process is stable if its unconditional expectations are bounded (Klein, 2000).

3 Series Expansion

3.1 The General Case

In this section we shall follow the perturbation methodology used in applied mathematics (see, for example, Nayfeh (1973) and Holmes (2013)) to derive an approximate solution to the model (1)–(2). For small , we assume that the solution444As is conventional in applied mathematics literature (see for example Holmes (2013)), each term of the expansion is not divided by the factorial term at this stage. has a particular form of expansions

| (3) |

| (4) |

The exogenous process can also easily be represented in the form of expansion in

| (5) |

Indeed, plugging (5) into (2) gives

Collecting the terms of like powers of and equating them to zero, we get

| (6) | ||||

| (7) |

Since the expansion (5) must be valid for all at the initial time , the initial conditions are

| (8) |

It is worth noting that in contrast to Lombardo, and Uhlig (2014), where and are the steady state, here and are functions of and, as will be shown below, are a deterministic solution of the problem. In this way the pruning procedure is always local around the steady state, whereas we focus on the case where and are global.

Expanding the left hand side of (9) for small , collecting the terms of like powers of and setting their coefficients to zero, we obtain

Coefficient of

| (10) |

The requirement that (4) and (5) must hold for all arbitrary small implies that the initial conditions for (10) are

| (11) |

The terminal conditions for and are the deterministic steady states

| (12) |

The system of equations (6) and (10) is a deterministic model since it corresponds to the model (1) and (2), where all shocks vanish (for this reason we omit the expectations operator in (10)). The deterministic model (6) and (10) with the initial and terminal conditions (11) and (12), respectively, can be solved globally by a number of effective algorithms, for example the extended path method ( Fair, and Taylor (1983)) or a Newton-like method (for example, Juillard (1996)). As this study is primarily concerned with stochastic models, in what follows we suppose that the deterministic model is already solved and its solution is known.

Coefficient of

| (13) |

The matrices

are the Jacobian matrices of the mapping with respect to the th argument (that is , , , , , and , respectively), at the point The requirement that (4) and (5) must hold for all arbitrary small implies that the initial condition for (13) is

| (14) |

Coefficient of ,

| (15) |

The requirement that (4) must hold for all arbitrary small implies that the initial condition for (15) is

| (16) |

A nice feature of the set of systems of equations (15) is that the linear homogeneous part is the same for all . The difference is only in the non-homogeneous terms that are some mappings for which the set of arguments includes only quantities of order less than

Particularly, for we have

and

| (17) |

respectively; where , , , denotes the mixed partial Frechét derivative of of order two with respect to th and th arguments at the point

| (18) |

In other words, is a bilinear mapping (see, for example, Abraham, Marsden, and Ratiu (2001, p. 55)) depending on vector (18) (and hence on ).555We do not make use tensor notation for brevity. The expectations are bounded if all conditional mixed moments of are bounded up to order and the vectors (18) are bounded for all .

Equation (15) with the initial conditions (16) is a linear rational expectations model with time-varying parameters and bounded the non-homogeneous terms . To solve the problem (15)–(14) is equivalent to finding a bounded solution for under the assumption that the bounded solutions to the problems of all orders less than are already known. Knowing how to solve these types of model and using the structure of mappings , we can find recursively solutions, , to (15) for every order , starting with .

3.2 An Example of the Series Expansion: An Asset Pricing Model

In this section the method of expansion around a deterministic path applies to a simple nonlinear asset pricing model proposed by Burnside (1998) and analyzed by Collard, and Juillard (2001); Schmitt-Grohé, and Uribe (2004). In this model the representative agent maximizes the lifetime utility function

subject to

where is a subjective discount factor, and , denotes consumption, is the price at date of a unit of the asset, represents units of a single asset held at the beginning of period , and is dividends per asset in period . The growth of rate of the dividends follows an AR(1) process666By abuse of our previous notation, we let stand for the exogenous process as in Burnside (1998); Collard, and Juillard (2001); Schmitt-Grohé, and Uribe (2004).

| (19) |

where , and . The first order condition and market clearing yields the equilibrium condition

| (20) |

where is the price-dividend ratio. This equation has an exact solution of the form (Burnside, 1998)

| (21) |

where

| (22) |

and

It follows from (20) that the deterministic steady state of the economy is

We now express a solution to the system (19)–(20) as an expansion in powers of the parameter up to a second-order approximation and decompose the original problem into a set of auxiliary problems. Specifically, assume that the solution can be represented in the form:

| (23) | ||||

| (24) |

Substituting (24) into (19) and collecting the terms containing and , we obtain the representation (24) for

| (25) | ||||

| (26) |

Since the expansion (24) must be valid for all at the initial time , the initial conditions are

| (27) |

Substituting now (23) and (24) into (20) yields

Expanding exponential for small gives

Collecting the terms of like powers of in the last equation, we have

Coefficient of

| (28) | ||||

| (29) |

Coefficient of

| (30) |

| (31) |

Coefficient of

| (32) |

The system (28) and (29) is a deterministic model. Its solution can easily be obtained by, for example, forward induction

| (33) |

Under the assumption that and are already known for , Equations (30) and (31) constitute a linear rational expectations model with time varying deterministic coefficients . The expectations of the term in (15) has the form . Equation (32) is also a linear forward-looking equation with time varying deterministic coefficients , and the term

depending only on solutions of orders less than two, i.e. . Therefore, both the system (30) and (31), and Equation (32) are linear forward-looking models with time varying coefficients. Under the condition that we know how to solve these types of model, they can be solved recursively starting with solving (30) and (31), then passing to (32). In Section 5 we present a method for solving such types of model and prove the convergence of the solutions implied by the method to the exact solution. In the next section we transform equation (15) in a more convenient form to deal with.

4 Transformation of the Model

Define the deterministic steady state as vectors such that

| (34) |

We can represent in (15) as , , where

are the Jacobian matrices of the mapping at the steady state with respect to th argument, and

| (35) |

Note also that as , because a deterministic solution must tend to the deterministic steady state as tends to infinity. Consequently, can be thought of as a perturbation of . As Equations (15) have the same form for all , to shorten notation, further on we omit the superscript when no confusion can arise. Therefore Equations (15) can be written in the vector form

| (36) |

where and . We assume that the matrices are invertible for all . For instance, this assumption always holds in some neighborhood of the steady state if the Jacobian at the steady state is invertible.777This assumption is made for ease of exposition. If is a singular matrix, then further on we must use a generalized Schur decomposition for which derivations remain valid, but become more complicated.

Pre-multiplying (36) by , we get

| (37) |

where and

Particularly, for we have

| (38) |

Notice that . As in the case of rational expectations models with constant parameters it is convenient to transform (37) using the spectral property of . Namely, the matrix is transformed into a block-diagonal one

| (39) |

where

| (40) |

where and are matrices with eigenvalues larger and smaller than one (in modulus), respectively; and is an invertible matrix888A simple Schur triangular factorization is also possible to be employed here, but at the cost of more complicated derivations. The block-diagonal structure of the matrix simplifies algebra. This can be done, for example, by initially transforming in a simple Schur form , where is a unitary matrix, is an upper triangular Schur form with the eigenvalues along the diagonal. We then transform the matrix in the block-diagonal Schur factorization , where is an invertible matrix and is block-diagonal and each diagonal block is a quasi upper-triangular Schur matrix999The function bdschur of Matlab Control System Toolbox performs this factorization.. Hence the matrix in (39) has the form . We also impose the conventional Blanchard-Kan condition (Blanchard, and Kahn (1980)) on the dimension of the unstable subspace, i.e., .

After introducing the auxiliary variables

| (41) |

and pre-multiplying (37) by , we have

| (42) | |||

| (43) |

where and

| (44) |

Particularly, for , we have

where

System (42)-(43) is a linear rational expectations model with time-varying parameters, therefore to solve the system we cannot apply the approaches used in the case of models with constant parameters (Blanchard, and Kahn (1980); Anderson and Moor (1985); Uhlig (1999); Klein (2000); Sims (2001), etc.). In Subsection 5.2 we develop a method for solving this type of models.

5 Solving the Rational Expectations Model with Time-Varying Parameters

5.1 Notation

This subsection introduces some notation that will be necessary further on. By denote the Euclidean norm in . The induced norm for a real matrix is defined by

The matrix in (39) can be chosen in such a way that

| (45) |

where and are the largest eigenvalues (in modulus) of the matrices and , respectively, and is arbitrarily small. This follows from the same arguments as in Hartmann (1982, §IV 9), where it is done for the Jordan matrix decomposition. Note also that for sufficiently small . Let

| (46) |

By definition, put

| (47) | |||

| (48) |

In the sequel, we assume that all the matrices , are invertible. Note that the numbers , , and depend on the initial conditions . From the definitions of , , , , and and the condition , it follows that

| (49) |

This means that and can be arbitrary small and

| (50) |

by choosing close enough to the steady state.

5.2 Solving the transformed system (42)–(43)

Taking into account notation (46), we can rewrite (42)–(43) in the form

| (51) | |||

| (52) |

In this subsection we construct a bounded solution to (51)–(52) for with an arbitrary initial condition and find under which conditions this solution exists. For this purpose, we first start with solving a finite-horizon problem with a fixed terminal condition using backward recursion. Then, we prove the convergence of the obtained finite-horizon solutions to a bounded infinite-horizon one as the terminal time tends to infinity.

Fix a horizon . At the time using the invertibility of and solving Equation (52) backward, we can obtain as a linear function of , the terminal condition and the “exogenous” term

Proceeding further with backward recursion, we shall obtain finite-horizon solutions for each For doing this we need to define the following recurrent sequence of matrices:

| (53) |

where

| (54) |

with the terminal condition . In (53) and (54) the first subscript defines the time horizon, while the second subscript defines all times between and . Let , denote the -time solution obtained by backward recursion that starts at the time . The matrices (53) and (54) are needed for constructing approximate solutions by backward recursion.

Proposition 5.1.

For the proof see Appendix A.

The sequence of matrices (53) exists if all matrices , are invertible. For this we need, in addition, some boundedness condition on the matrices . From (49) the matrices and are bounded, hence this condition boils down to the boundedness of matrices .

For the proof see Appendix A.

Proposition 5.3.

If the inequality (58) holds, then the matrices , , are invertible.

Proof.

For from (55) we have

| (60) |

This is a finite-horizon solution to the rational expectations model with time-varying coefficients (51)–(52) and with a given initial condition . What is left is to show that the solution of the form (60) converges to some limit as .

Proposition 5.4.

For the proof see Appendix A.

Proposition 5.5.

Proof.

From (54) and 5.4 it follows that

Then the limit in (61) can be represented as

| (63) |

Since is bounded (it follows from formula (93) in A) and

we have . Therefore, if is arbitrary small, there is an such that

| (64) |

for , where is the largest eigenvalue (in modulus) of the matrix . From this, the norm property and (63) we obtain

where is some constant.

From Proposition 5.4 and Proposition 5.5 it may be concluded that as tends to infinity Equation (60) takes the form:

| (65) |

Formula (65) provides a unique bounded solution to the transformed rational expectation model with time-varying parameters (51)–(52), and may be treated as a policy function for this type of problems.

Remark 5.1.

Remark 5.2.

The details of derivations for the solution of time-varying rational expectations model corresponding to the first order approximation of the system (15) and (16) are carried out in Appendix B, where we also derive the moving-average representation for and . Having this representation it is not hard to compute all quadratic terms in (17).

Remark 5.3.

5.3 Initial conditions.

It remains to find the initial condition for a stable solution to the system (51)–(52) corresponding the initial condition (16). Recall that we deal with the -order problem (15)–(16), and we now put the superscript back in notation. From (41) and (65) we have

where is a matrix that is involved in the block-diagonal factorization (39) and has the following block-decomposition:

Hence

| (67) | |||

| (68) |

Substituting (67) into (68) , we get

| (69) |

The vector is the initial condition corresponding to a bounded solution to (15) for , hence formula (69) determines the solution to the original rational expectations model with time-varying parameters. In other words, is a policy function for the rational expectations model with time-varying parameters at the point . Particularly, for from (69) and taking into account we have . The condition of the invertibility of matrix corresponds to Proposition 1 of Blanchard, and Kahn (1980).

5.4 Expected dynamics. Restoring the original variables and .

To compute the expected dynamics (impulse response function) it is more convenient to work with auxiliary variables and , then to restore the original variables and Substituting (65) for in (51) and taking expectations at gives

| (70) |

From (67) we can compute the initial condition for (70). Knowing the initial value allows us to obtain the whole trajectory of the solution to (70), i.e. . The expected dynamics of can easily be obtained from (65)

| (71) |

Then the expected dynamics of the original variables is restored by

| (72) | |||

| (73) |

where , , are blocks of the block-decomposition of the matrix . From (70) and (71) it follows that the process is stable, as , but is a stable matrix, , and are bounded matrices for .From this and (72) and (73) it may be concluded that the process is also stable. To sum up, under the assumption that the solutions of lower order than are already computed in the same manner as for the th order, we find the stable solution to the original model (1) in the form

6 Approximate solution: an Asset Pricing Model

To illustrate how the presented method works we apply it to the nonlinear asset pricing model considered above. The simplicity of the model allows us to derive all approximations in the analytical form. We begin with the first order approximation determined by Equations (30) and(31) under the assumption that the deterministic solution and are known for and satisfies (33). Rewriting (30) for and taking into account that gives

| (74) |

Similarly to (74) for we have

| (75) |

Substituting in the last equation (74) for and taking into account that , we obtain

Continuing further in the same way, for we have

| (76) |

If the moment tends to , then the following solution for is valid:

| (77) |

Note that , hence .

We now turn to the second order approximation. Equation (32) is also a linear forward-looking equation with time varying deterministic coefficients and can solved by the backward induction. Indeed, rewriting (32) for yields

| (78) |

Substituting (77) for in (32) and collecting the terms with yields

| (79) |

Substituting for in (79) gives

| (80) |

Inserting from (79) into (80), we have

| (81) |

For we have

| (82) |

If the moment tends to , then the following solution for is valid:

| (83) |

At the time equation (83) provides the second term of the policy function series expansion

| (84) |

The expectation term in the last equation can be obtained by using the moving-average representation for . Indeed, from (31) and (27) we have

Since the sequence of innovations , , is independent it follows that

| (85) |

The sum in exponential in (83) can be obtained from (25)

| (86) |

Finally, inserting (85) and (86) into (83) gives

In computation we need to use a finite terminal time . Despite the fact that the method converges for any terminal condition , the most reasonable choice of the terminal condition is the second order term in the expansion of the stochastic steady state in a series of powers of . To summarize, we find the policy function approximation in the form

Note that both and are functions of . From (83) and using (85), we can get the expected dynamics (in other words, impulse response function) . The solutions for the higher orders , , can be obtained in much the same way as for .

6.1 Comparison with the local perturbation

This subsection compares the policy functions of the second order of the presented method with the local Taylor series expansions of orders two and six(Schmitt-Grohé, and Uribe, 2004).

The parameterization follows Collard, and Juillard (2001), where the benchmark parameterization is chosen as in Mehra, and Prescott (1985). We therefore set the mean of the rate of growth of dividend to , the volatility of the innovations to = 0.015, the parameter to and to . For illustrative purpose, we choose the highly persistent exogenous process with as in Collard, and Juillard (2001).

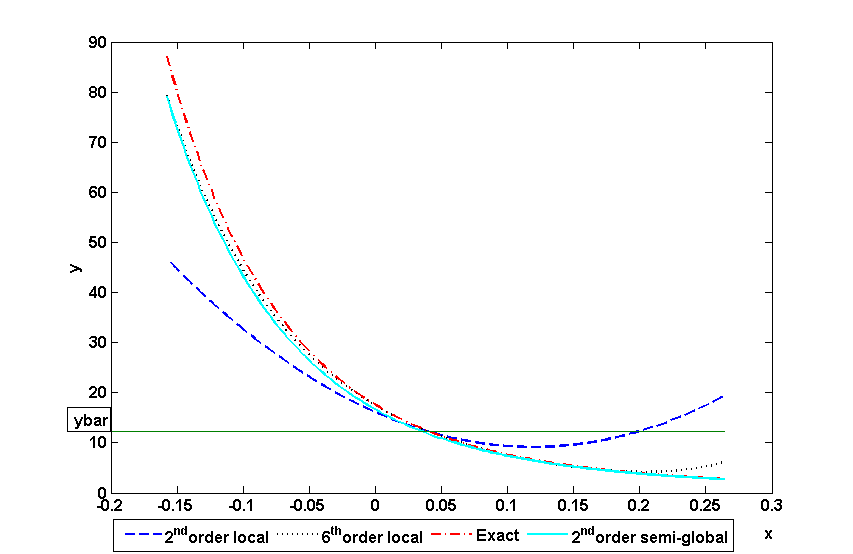

Fig 1 illustrates the exact policy function with the approximate ones constructed by the semi-global method and the local Taylor series expansions. This figure is drawn over the interval , where is the unconditional volatility of the process and . Fig 1 shows that the semi-global approximation has the same accuracy as the sixth order of the Taylor series local expansion at the left endpoint of the interval under consideration. However, at the right endpoint of the interval the semi-global solution is much more accurate than the sixth order of the Taylor series expansion. Actually, the semi-global approximation is indistinguishable from the true solution in this domain. The second order of the Taylor series expansion is much less accurate globally than both the sixth order of the Taylor series expansion and semi-global solution.

From Fig 1 one can also see another undesirable property of the the local Taylor series expansion, namely this method may provide impulse response functions with wrong signs. Indeed, the steady state value of is . After a big positive shock the true impulse response function is negative (the policy function values are below the steady state), whereas the impulse response function implied by the second order of the local perturbation method is positive (the approximate policy function is above the steady state). The sixth order approximation of the local perturbation method has the right sign of impulse response, but wrong shape, which is U-shaped instead of being monotonically increasing. In contrast, the semi-global method, as just mentioned, provides almost exact impulse response.

7 Conclusion

This study proposes an approach based on a perturbation around a deterministic path for constructing global approximate solutions to DSGE models. Under the assumption that the deterministic solution to the model is already found, the approach reduces the problem to solving recursively a set of linear rational expectations models with deterministic time-varying parameters and the same homogeneous part. The paper also proposes a method to solve linear rational expectations models with deterministic time-varying parameters. The conditions under which the solutions exist are found; all results are obtained for DSGE models in general form and proved rigorously.

The paper illustrates the algorithm for the second order of approximation using an nonlinear asset pricing model by Burnside (1998) and compares it with the local Taylor series expansion. The second order approximation of the semi-global method provide more accurate solution than sixth order of the Taylor series expansion around the deterministic steady state.

The approach is applicable to Markov-switching DSGE models in the form proposed by Foerster, Rubio-Ramíres, Waggoner and Zha (2013), where the vector of Markov-switching parameters that would influence the steady state is scaled by a small factor. Actually, under the conditions of ”smallness” of a scaling parameter and existence of higher order moments for stochastic terms, all derivations of Sections 3, 4 and 5 hold irrespective of probability distribution functions for these stochastic terms.

Appendix A Proofs for Section

PROOF OF PROPOSITION 5.1: The proof is by induction on . Suppose that . For the time from (52) we have

As is invertible, we have

where ; and . From (53), (54) and (56) it follows that the inductive assumption is proved for . Assuming that (55) holds for , we will prove it for . To this end, consider Equation (52) for the time . As the matrix is invertible, we obtain

Substituting the induction assumption (55) for yields

Substituting (51) for and using the law of iterated expectations gives

Collecting the terms with , and , we get

Suppose for the moment that the matrix

is invertible. Pre-multiplying the last equation by , we obtain

Note that ; then using the definition of (53), we see that

| (87) |

Using the definition of and ((54) and (56)), we deduce that

| (88) |

From (87) and (88) it follows that

∎

PROOF OF PROPOSITION 5.2: We begin by rewriting (53) as

Rearranging terms, we have

| (89) |

Taking the norms and using the norm properties gives

Rearranging terms, we get

| (90) |

Inequality (90) is a difference inequality with respect to , and with the time-varying coefficients , , and . In (90) we assume that

.

This is obviously true if . We shall show that if the initial condition , then , Indeed, consider the difference equation:

| (91) |

Lemma A.1.

The lemma can be proved by direct calculation. From (48)–(47) the values , , and majorize , , and , respectively. If we consider Equation (88) and inequality (91) as initial value problems with the initial conditions and , then their solutions obviously satisfy the inequality , . In other words, is majorized by . From the last inequality and Lemma A.1 it may be concluded that

| (93) |

From (92), (93) and (48) it follows that

| (94) |

From (57) we see that . Substituting this inequality into (94) gives

| (95) |

where the last inequality follows from (50). ∎

PROOF OF PROPOSITION 5.4: The assertion of the proposition is true if there exist constants and such that and for

| (96) |

Note now that () is a solution to the matrix difference equation (53) at () with the initial condition (). Subtracting (89) for from that for , we have

Adding and subtracting in the right hand side gives

Rearranging terms yields

From Proposition 5.3 it follows that the matrix

is invertible, then pre-multiplying the last equation by this matrix yields

Taking the norms, using the norm property and the triangle inequality, we get

| (97) |

| (98) |

From the norm property and Golub, and Van Loan (1996, Lemma 2.3.3) we get the estimate

By (95), we have

Substituting the last inequality into (98) gives

| (99) |

Using (102) successively for , and taking into account and results in

| (100) |

Recall that depends on the solution to the deterministic problem (10), i.e.

From Hartmann (1982, Corollary 5.1) and differentiability of with respect to the state variables it follows that

| (101) |

where is the largest eigenvalue modulus of the matrix from (40), is some constant and is arbitrary small positive number. In fact, determines the speed of convergence for the deterministic solution to the steady state. Inserting (101) into (102), we can conclude

| (102) |

Denoting and we finally obtain (96). ∎

Appendix B The First Order System

For we have

From (43) for the time we have

Denoting and gives

| (103) |

For we have

| (104) |

Taking conditional expectations at the time from both side (103) and inserting (2) we get

| (105) |

Reshuffling terms, we have

| (107) |

Multiplying (107) by yields

or

Denoting , we obtain

Denoting

and

we have

Following the same derivation as in A for the proof of Proposition 5.1, we obtain the following representation:

| (108) |

where can be computed by backward recursion

Inserting (42) into (108) gives

After reshuffling we get

Denoting and , we have

| (109) |

It is easy to see that

From (109) it follows that

thus, we obtain

| (110) |

Recall now that the initial conditions are and , then for from (110) we have

for

Continuing in this fashion, we get the moving-average representation of :

| (111) |

where the coefficients can be obtained by forward recursion in and backward recursion in

Indeed, inserting (111) into (110) and taking into account , we obtain

| (112) |

Collecting terms with gives

Thus, for each we compute , starting with the first index , then decreasing the index and using at each step . For the variable we also have a moving-average representation. Inserting the moving-average representation of the process and (111) in (108), we have

| (113) |

or in the shorter form

| (114) |

where .

Taking into account that and , we get the moving-average representation for original variables

where and .

References

- Abraham, Marsden, and Ratiu (2001) Abraham, R., J.E. Marsden, and T. Ratiu (2001): Manifolds, Tensor Analysis, and Applications, 2nd ed. Springer-Verlag, Berlin-Heidelberg-New-York-Tokyo.

- Adjemian, Bastani, Juillard, Karamé, Mihoubi, Perendial, Pfeifer, Ratto, and Villemot (2011) Adjemian, S., H. Bastani, M. Juillard, F. Karamé, F. Mihoubi, G. Perendia, J. Pfeifer, M. Ratto, and S. Villemot (2011): “Dynare: Reference Manual, Version 4.” Dynare Working Papers, 1, CEPREMA

- Anderson and Moor (1985) Anderson, G., and G. Moor (1985): “A Linear Algebraic Procedure for Solving Linear Perfect Foresight Models,” Economics Letters 17 247–252

- Andreasen, Fernández-Villaverde, and Rubio-Ramírez (2013) Andreasen, M., J. Fernández-Villaverde, and J. F. Rubio-Ramírez(2013): “The Pruned State-Space System for Non-Linear DSGE Models: Theory and Empirical Applications,” NBER Working Paper No. 18983.

- Blanchard, and Kahn (1980) Blanchard, O.J., and C.M. Kahn (1980): “The Solution of Linear Difference Models Under Rational Expectations,” Econometrica 48 1305–1311.

- Burnside (1998) Burnside, C. (1998): ”Solving asset pricing models with Gaussian shocks,” Journal of Economic Dynamics and Control 22 329–340

- Collard, and Juillard (2001) Collard, F., and M. Juillard (2001): “Accuracy of stochastic perturbation methods: the case of asset pricing models,” Journal of Economic Dynamics and Control 25 979–999.

- Fair, and Taylor (1983) Fair, R., and J.Taylor (1983): “Solution and maximum likelihood estimation of dynamic rational expectation models,” Econometrica 51 1169–1185.

- Foerster, Rubio-Ramíres, Waggoner and Zha (2013) Foerster, A., J. Rubio-Ramíres, D. Waggoner, and T. Zha (2013): “Perturbation Methods for Markov-Switching DSGE Model.” Federal Reserve Bank of Kansas City Research Working Paper, No. RWP 13-01.

- Gaspar, and Judd (1997) Gaspar, J. ,and K. L. Judd (1997): “Solving Large-Scale Rational-Expectations Models,” Macroeconomic Dynamics 1 45–75.

- Golub, and Van Loan (1996) Golub, G.H., and C.F. Van Loan (1996): Matrix Computations, 3rd ed. Johns Hopkins University Press, Baltimore.

- Gomme, and Klein (2011) Gomme, P., and P. Klein (2011): “Second-Order Approximation of Dynamic Models without the Use of Tensors,” Journal of Economic Dynamics and Control 35 604–615.

- Hartmann (1982) Hartmann, P. (1982): Ordinary Differential Equations, 2nd ed. Wiley, New York.

- Hollinger (2008) Hollinger, P. (2008): “How TROLL Solves a Million Equations: Sparse-Matrix Techniques for Stacked-Time Solution of Perfect-Foresight Models”, presented at the 14th International Conference on Computing in Economics and Finance, Paris, France, 26–28 June, 2008, Intex Solutions, Inc., Needham, MA, http://www.intex.com/troll/Hollinger_CEF2008.pdf

- Holmes (2013) Holmes, M. H. (2013): Introduction to Perturbation Methods, 3rd ed Springer-Verlag, Berlin-Heidelberg-New-York-Tokyo.

- Jin, and Judd (2002) Jin, H., and K. L. Judd (2002): “Perturbation methods for general dynamic stochastic models.” Discussion Paper, Hoover Institution, Stanford.

- Judd (1998) Judd, K. L. (1998): Numerical Methods in Economics, The MIT Press, Cambridge.

- Judd, and Guu (1997) Judd K. L., and S.-M. Guu (1997): ”Asymptotic Methods for Aggregate Growth Models,” Journal of Economic Dynamics and Control 21 1025–1042.

- Juillard (1996) Juillard, M. (1996): “DYNARE: a program for the resolution and simulation of dynamic models with forward variables through the use of a relaxation algorithm.” CEPREMAP working paper No. 9602, Paris

- Kim et al. (2008) Kim, J. et al., S.Kim, E.Schaumburg, and C. A.Sims (2008): “Calculating and using second order accurate solutions of discrete time dynamic equilibrium models,” Journal of Economic Dynamics and Control 32 3397–3414.

- Klein (2000) Klein P. (2000): “Using the generalized Schur form to solve a multivariate linear rational expectations model,” Journal of Economic Dynamics and Control 35 1405–1423.

- Lombardo (2010) Lombardo, G. (2010): “On Approximating DSGE Models by Series Expansions,” European Central Bank Working Paper Series, No. 1264.

- Lombardo, and Uhlig (2014) Lombardo, G., and H. Uhlig (2014): “A Theory of Pruning,” European Central Bank Working Paper Series, No. 1696.

- Mehra, and Prescott (1985) Mehra, R., and E.C. Prescott (1985): “The Equity Premium: a Puzzle,” Journal of Monetary Economics 15 145–161.

- Nayfeh (1973) Nayfeh, A. H. (1973): Perturbation Methods, Wiley, New York.

- Schmitt-Grohé, and Uribe (2004) Schmitt-Grohé, S., and M.Uribe (2004): “Solving dynamic general equilibrium models using as second-order approximation to the policy function,” Journal of Economic Dynamics and Control 28 755–775.

- Sims (2001) Sims, C.A. (2001): “Solving Linear Rational Expectations Models,” Computational Economics 20 1–20.

- Uhlig (1999) Uhlig, H. (1999): “A Toolkit for Analysing Nonlinear Dynamic Stochastic Models Easily” in:Computational Methods for the Study of Dynamic Economies ed. by R. Marimon and A. Scott. Oxford, UK, Oxford University Press, 30-61