Many-to-one contagion of economic growth rate across trade credit network of firms

Abstract

We propose a novel approach and an empirical procedure to test direct contagion of growth rate in a trade credit network of firms. Our hypotheses are that the use of trade credit contributes to contagion (from many customers to a single supplier - “many to one” contagion) and amplification (through their interaction with the macrocopic variables, such as interest rate) of growth rate. In this paper we test the contagion hypothesis, measuring empirically the mesoscopic “many-to-one” effect. The effect of amplification has been dealt with in our paper [1].

Our empirical analysis is based on the delayed payments between trading partners across many different industrial sectors, intermediated by a large Italian bank during the year 2007. The data is used to create a weighted and directed trade credit network. Assuming that the linkages are static, we look at the dynamics of the nodes/firms. On the ratio of the 2007 trade credit in Sales and Purchases items on the profit and loss statements, we estimate the trade credit in 2006 and 2008.

Applying the “many to one” approach we compare such predicted growth of trade (demand) aggregated per supplier, and compare it with the real growth of Sales of the supplier. We analyze the correlation of these two growth rates over two yearly periods, 2007/2006 and 2008/2007, and in this way we test our contagion hypotheses. We could not find strong correlations between the predicted and the actual growth rates. We provide an evidence of contagion only in restricted sub-groups of our network, and not in the whole network. We do find a strong macroscopic effect of the crisis, indicated by a coincident negative drift in the growth of sales of nearly all the firms in our sample.

1 Introduction

In this paper we use the trade credit network of Italian firms to test a model of “many-to-one” contagion of economic growth or economic crisis. Academic research on inter-firm trade credit networks is still in its infancy, as the data on trade-credit transactions is not easily accessible. An exception is the analysis of the trade credit network of Japanese firms, which have been rather extensively characterized by, for example, Tamura et al. [2], Miura et al. [3] and Watanabe et al. [4].

Our approach to direct contagion of economic growth rate is built on the assumptions based on the previous results published in various economic literature on balance sheet contagion (e.g. Kiyotaki & Moore [5], Boissay [6], Petersen & Rajan [7], economic growth Schumpeter [8]), and from our own previously developed methods and models following complex systems approach (Solomon & Richmond [9], Challet et al. [10]).

When many firms simultaneously borrow from and lend to each other, and in particular when these firms are speculative and dependent on the credit flow, shocks to the liquidity of some firms may cause the other firms to also get into financial difficulties. As obvious as this argument might sound, it is very difficult to prove the effect of direct contagion in the data, exactly for the reason that the linearity is lost as soon as the firms are simultaneously interacting with each other.

The “many-to-one” contagion relies on the hypothesis that the change in the annual sales of a supplier follows the change in the mesoscopically aggregated demand, i.e. that the yearly growth of sales of a supplier would be proportional to the yearly growth of demand of its customers. Assuming that the growth of purchases of all customers of a supplier in a yearly period is known to us, shouldn’t we be able to predict the growth in the sales of the supplier? Indeed we should, as long as:

-

•

the linkages between the customers and the supplier are constant over the longer period (at least two years, as the growth rate of financial indicators reported in balance or profit and loss statements is available on yearly basis)

-

•

the growth of demand (purchases) of a customer is assumed to be uniformly distributed among all its suppliers.

Assuming that the above conditions are satisfied, we compare the prediction of the growth of sales with the real growth as measured from the profit and loss statements, and so we can test our hypotheses of growth contagion from customers to suppliers.

The paper is organized as follows. In section 2 we describe the nature and applications of different interaction mechanisms that can be involved in the self-amplifying auto-catalytic loops in supporting both peer interactions and the bi-directional feedback between the micro and the macro structures of the economy. Following that, we describe the possible methodologies that could be used in order to empirically show the existence and operation of an auto-catalytic feedback. In section 3, we give the detailed description of the data that were used for the network model and internal properties of the nodes. In that section the reader can also find the definitions of the variables and the algebraic notations. In section 4, we elaborate on the empirical results and provide their interpretation and implications. Finally we discuss the results in section 5.

2 Applicability of the methods of statistical physics to stochastic processes in economics

One of the major issues in economics is to understand how relativelly small and temporary endogeneous changes in technology or wealth distribution may generate macroscopic effects in aggregate productivity, asset prices etc. For this purpose, it is necessary to identify self-amplifying mechanisms, filtering out the main mechanisms that may trigger dynamics leading to a systemic change, from other interactions destined to drown in the noise of local, short lived perturbations. This implies that the vast majority of microeconomic interactions that may affect the macroeconomic/systemic level do so by a kind of auto-catalytic positive feedback loop. This idea was already proposed in various contexts, but was often dismissed in the absence of concrete mechanisms that realize it.

Below, we list three mechanisms that might effectively amplify microscopic events to macroscopic dynamics in economic systems. In this paper we deal only with the first mechanism, with the second one we dealt in [1], and the third mechanism we might tackle in the future.

‘Peer-to-peer’, ‘One to many’ and ‘Many-to-one’ interactions between firms in the network

The domino effect, or contagion can be best understood using powerful mathematical and statistical-mechanics tools developed in percolation theory. They allow the rendition of precise predictions that correspond to real world stylized facts: macroscopic transitions caused by minute parameter changes, fractal spatial and temporal propagation patterns, delays in growth or crisis diffusion between economic sectors or geographical regions. For a formal discussion of social and market percolation models the reader is referred to Goldenberg et al. [11].

In this paper we deal with the many-to-one contagion principle (in the cases when a supplier has a single customer it reduces to peer-to-peer principle). The peers are tied financially, and also physically by the goods they pass. We introduce the assumption that the peers are correlated though their growth rate and we empirically test it. We attempt and succeed to find only partial evidence in our data that the Many-to-one is responsible for the propagation of the growth rate on the trade network consisting of suppliers and their customers. This mechanism is only partly responsible for the congation of growth rate, and other mechanisms, such as the following ones, should also be considered.

Inter scale macro-to-micro reaction between firms and the system

For a long while, one of the drawbacks of the dynamical models inspired by physics was the absence of interaction between scales. A model that introduces this interaction was introduced by Solomon and Golo [12]. This is a financial model extending the ideas of Minsky [13], where not only the fate of individual firms (e.g. failure) influences the system state (risk aversion leads to rise in corporate interest rates), but also the state of the system is feeds back onto its own components (e.g. a rise in interest rate leads to more failures). Together with contagion across the network, the model generates a bounty of predictions that agree with the stylized facts. For example: delaying or arresting the propagation of distress by targeted intervention in key individual components or in system properties (such as the interest rate). This model has been confronted with empirical data in [1] and provided a significant contribution in the interpretation of the economic collapse in 2008.

Self-interaction: firms acting upon themselves

A model for self-dependent reproduction was proposed by Shnerb et al. [14], generalizing on the ideas of Malthus that proliferation in the microscopic level in stochastic systems leads to the spontaneous emergence of a collection of adaptive objects. The model is analytically tractable by statistical-mechanics method as mentioned above. It generates a host of qualitative (phase transitions) and quantitative predictions about the macroscopic behavior of the system. These predictions were precisely confirmed by empirical measurements in many cases: crossing exponentials between decaying and emerging economic sectors after a shock [15], identity of the wealth inequality ‘Pareto-Zipf’ exponent [16] and the market instability exponent [17] [18], etc. The self-interaction mechanisms are not in the scope of this paper, and the microeconomics models of firms are not considered as well.

2.1 The difficulty of the empirical confrontation

In the analysis of contagion, causality is the key. The mechanisms we sketched in the preceding subsection call for testing, but the analysis should account for causality, rather than correspondence.

The microscopic behavior of agents in a network should be revealed in the structure of the links between the agents and their interaction patterns. In a financial network, the visible communication between agents is through the invoices they issue and the payments they make.

The structure of links between the nodes in a network is formally termed the ‘topology of the network’. The metrics (indicators) typically used for measuring topology are for example: node degree being the number of connections from/to each node, clustering being the number of distinct groups of nodes, and connected-component sizes. However, the description of the topology is not the subject of our paper. We aim to justify the existence of the network and the application of the network analysis by trying to measure the significance of the interaction across the network nodes. In our work, we focus on a selection of certain neighborhoods that consist of buyers from a single supplier. Thus, the clustering coefficients and component size are used only for validating that the selection process does not destroy the statistical properties of the complete sample.

We are taking into account that the properties of firms influence the interaction between them. In financial networks, the strength and the interaction patterns cannot be interpreted without understanding the level of financial exposure to risk that the agents (firms) are in. The financial risk of providing and extending the trade credit relation is an interplay between a firm’s own liquidity position, its social neighborhood (its industry and its particular buyers and suppliers), and systemic effects such as the interest rate. Since the risk exposure of a firm cannot be directly measured, the ability to meet obligations subject to the environment and the system we have used a quantity available in our data termed the ‘RATING score’. This quantity will be defined in the data section below.

3 Description of the dataset

The data on individual firms come from a dataset (further on abbreviated as BS) of Italian limited liability companies end-of-year balance sheet and Profit & Loss statements, which is a part of a proprietary database 111 The data base is proprietary of one of the main Italian banks and all the analysis have been performed in a fully anonymous way fulfilling both the data license policy, the privacy constraints and the bank’s research department policy. Only aggregated data has been disseminated and distributed to the research group. The network is assembled from the sales invoices issued by suppliers to their customers when they sell an item. Some of these invoices were presented to a bank in order to acquire trade-credit (TC). The borrower in most cases was the seller in the supplier-customer pair. It is these invoices that the bank recorded and which we have been able to analyse. In this study we combined the two datasets (BS) and (TC) in order to select the suppliers that are most appropriate for this analysis.

Balance sheets database

In Italy, all limited liability firms are obliged to submit their annual financial report (balance sheet) to the local Chamber of Commerce. Items contained in the firm’s balance sheet are assets and liabilities of the firm such as: Equity, Net-Sales, Accounts Receivable, Inventory, Bank loans, Accounts Payable, Financial Costs, etc .

Other than balance data, these reports contain financial ratios. Financial ratios are ratios of quantities within the balance sheet items, such as Acid Test or the Receivables Conversion Period and their purpose is to help quickly estimate the financial status of the firm.

The balance sheets are collected and stored by an external agency. The firms, no matter whether defaulting or non-defaulting at the end of the period, are ranked with a ‘RATING score’ ranging from 1 to 9 in increasing order of default probability: 1 is attributed to firms that are predicted to be highly solvent, and 9 identifies firms displaying a serious risk of default. Notice that the ranking is an ordinal: firms rated as 9 are not implied to have 9 times the probability of defaulting as compared to firms rated 1. A good description of the RATING score is given in a paper by Bottazzi et al [20].

For the purpose of our analysis, and in accordance to the practitioners’ behavior, we divide all companies into three groups, using the Rating score: one group with an easy Access to Bank Credit (rating 1-3), one with the Access to Bank Credit (ABC) at medium risk (rating 4-6) and the third group at high risk and little or no Access to Bank Credit (rating 7-9).

| Rating 1 - 3 | ABC A |

|---|---|

| Rating 4 - 6 | ABC B |

| Rating 7 - 9 | ABC C |

Trade Credit data

The Trade Credit database222TC data is private. All the analyses were performed within the bank on completely anonymous data and only aggregated information was disseminated to the research group. (TC) contains all inter-firm delayed payment transactions during 2007 that were intermediated by a large Italian bank. This bank covers about 15% of the entire trade credit in Italy, according to the official statistics of the Bank of Italy.

Algebraic notation

We use the symbols and to mark a supplier and a customer, respectively. Transactions between a supplier and a customer will be presented by magnitude and direction of the money flow. A general event of goods or services sold to a customer can be graphically described by .

The 2007 TC (Trade Credit) records are invoices that account for goods/services supplied by firm to firm that were presented to the bank for discounting in 2007. These transactions were booked as accounts receivable in firm ’s assets, and as accounts payable in firm ’s liabilities. We can write

-

the sum of all payable trade invoices and cash payments from a customer to a supplier accounting for purchases of goods or services in 2007.

-

the total invoices used by firm as collateral on a credit line in 2007.

We may also define the following notation from the BS (Balance Sheet) records of firm :

-

: balance sheet item of total sales (cash and credit) of firm in year y

-

: balance sheet item of total purchases (cash and credit) of firm in year y

Testing for completeness of firm-level information

To ensure that we have sufficient coverage in the TC database of each firm’s sales, we selected the firms for which the expression

| (1) |

is greater than a pre-defined value. We call this the ‘Matching threshold’ or ‘Matching’. We vary the threshold between 0 and 1 in order to create the best sample for our empirical analysis. We choose a representative sample with high level of completeness by setting the matching threshold so it is the maximal value that still renders a single large connected component of size , and that the consequent connectivity of firms spans from 1 to approximately the size of the component ().

The matching ratio reaches values greater than than 1 (more than 100% completeness), perhaps due to misalignment of the time windows between the trade credit network and balance sheet data. This will be discussed below. The analysis in this paper is, therefore, restricted to the sample of suppliers that have a matching proportion of 0.8 and up to 1.2 (i.e. 80% to 120%, or formally ). The reason to prefer a range with a top-cap is that much larger proportion signals to us a mismatch: that the sample of invoices for the selected firm may be incorrect. Possibly due to an error in invoice registration.

We did not expect to retrieve a large network from the firms exhibiting high matching proportion. Several factors reduce the matching. The two most prominent ones are:

-

•

trade credit data do not record changes in cash holdings. They do, however, record an accounts receivable on the supplier’s side and an accounts payable on the customer side. When accounts receivables are cashed by the customer, a ‘sale’ item will be booked to the supplier. Now, outstanding invoices and payments made in 2007 may have been booked as accounts receivables in 2006. We estimate a delay of 3 months on average for discounts and 9 months for payments (cf. the misalignment of the time frames).

-

•

the Sales () are all sales of the firm including sales performed in other monetary channels. The TC database holds information on invoices only.

4 Results

Out of firms that were initially available both as creditors in the TC data (have incoming links) and in the BS data (have sales in ), only 671 companies fulfill the Matching range . Lowering this threshold would grow the sample exponentially but at the cost of unavoidably entering suppliers with lesser proportions of their total debt owed. In Table 1 we list some statistics of this network, assuming that the links are directional. Out of the total 671 suppliers, 190 companies are of reasonable size in accordance with bank practices ( EUR).

| Feature | Count |

|---|---|

| Number of supplier/creditor nodes | 671 |

| Number of customer/debtor nodes | 10,762 |

| Number of links | 12,198 |

| Multi-edge node pairs | 150 |

| Average number of IN-neighbors | 18.17 |

| Average number of OUT-neighbors | 1.2 |

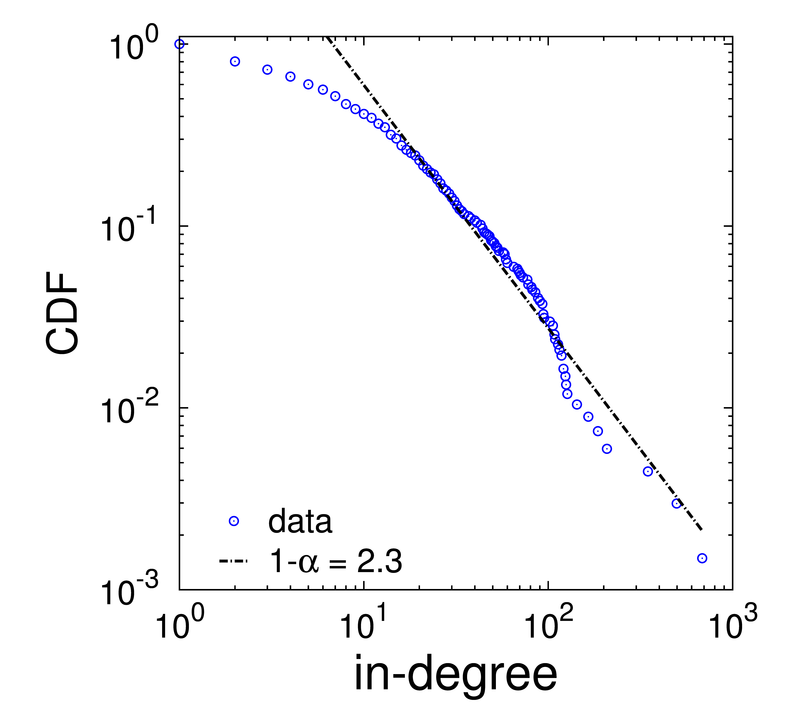

4.1 In-degree distribution

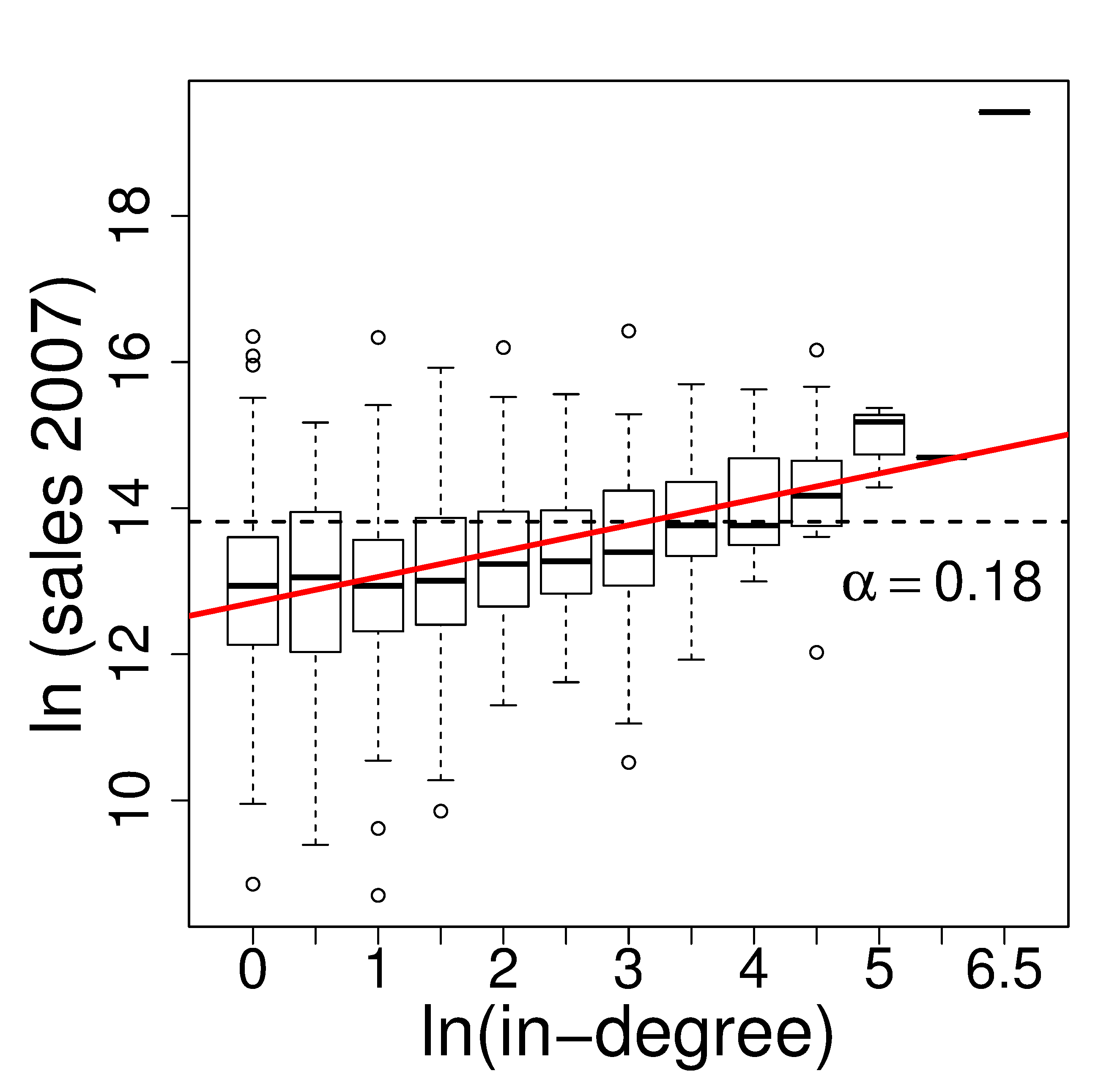

In our inter-firm network, the in-degree of a supplier is the number of its customers. In a previous study, Miura et al. [3] obtained power laws of the in- and out-degree distributions, with exponents of . In our network, we were able to confirm a similar finding of , i.e a negative exponent . As for the in-degree vs. size, a statistically significant correlation was recovered in our sample with a slope of . In the Japanese network of Miura et al., a slope of was obtained. Both results appear in figure 1.

In the second observation, the correlation between Sales in 2007 and in-degree (panel 1(b)) Pearson’s correlation coefficient is . The broken line marks a net-sales of 1 million EUR. The crossing between the broken and the red linear fitting line is characteristic of a firm with . Below the dashed line we can find the small companies, and it is clear that most of them also appear left of the crossing point, indicating a client-base smaller than .

4.2 Key customers

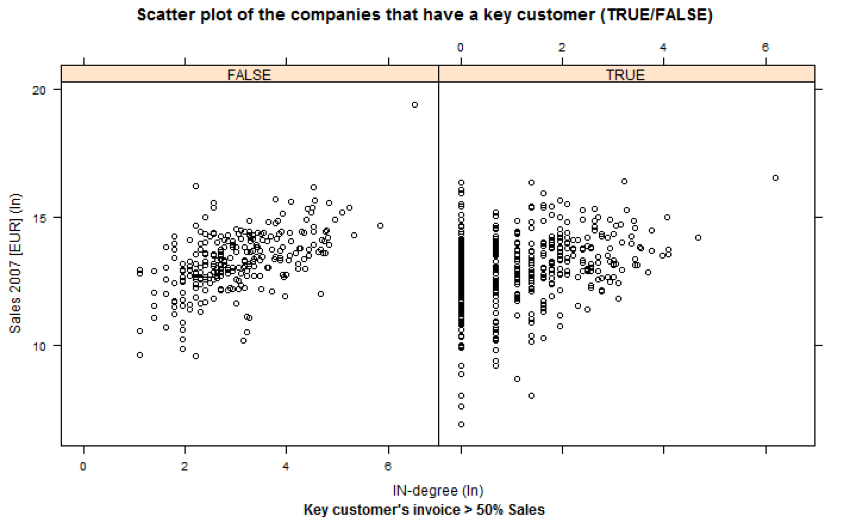

In order to quantify the relevance of the many-to-one approach, we measure the number of suppliers in our selection that do not have a key customer but are permanently related with a large number of customers. A supplier with a single key-customer is a firm that is to a large extent (50 %) dependent on a single customer. Such a seller could be more fragile towards his customer’s financial environment than a supplier who has no single key customer.

However, the nature of the key-customer relations is not known to us. It could be the nature of small businesses, though it is obvious from figurel 1(b) that the firms that have low IN-degree correspond to a very large confidence interval (meaning that there are firms that have very large sales, in the order of million euro, and yet a single customer). This might have a significant (negative) impact on the experiments that we are performing. Namely, it might indicate that that there are some incidental events of sales that do not reflect the regular trading pattern. The vast number of key-customers in our dataset could also be connected with the fact that the data are preceding the economic crisis and it is probable that an increased number of liquidations, mergers etc happened which can be reflected in the incidental transactions.

Figure 2 displays two subgroups of the suppliers presented in Figure 1. On the right panel are the suppliers that have a ‘key-customer’, and on the left appear the suppliers that do not have such a customer. We define a key-customer as one that purchases of at least 50% of the supplier’s annual sales. Out of the 671 firms in the sample there are 414 creditors with a key-customer and 235 without one. Having a key-customer is a feature of the supplier and clearly all suppliers that have one customer () qualify for it. We can appreciate that the range of firms that have a key-customer is dominated by suppliers with a small in-degree. However, we also find that suppliers with a large in-degree () have a key-customer. The reason is that in many situations, the payment distribution to a single supplier is fat-tailed, i.e. the largest customer pays an order of magnitude more than the second largest one. A good example of this is a phone company: it has few very large customers and the majority are single-time walk-in clients. We can then expect that the suppliers with a key-customer will be subject to transmission of financial signals from their key customer, either directly by peer-to-peer interaction or indirectly by responding quickly to the factors that influence the key-customer.

In this small subgroup of the firms, as the ratio of suppliers with a key customer to those without is 2:1, we should expect to see a contagion effect that spans the firms with a key customer at the very least.

4.3 Contagion of growth or distress

We checked the contagion of the growth between the Customers and the Suppliers on the selected sample of suppliers with the Matching 80-120%. We compared the actual measured growth in net-sales (cash and credit) from 2007 to 2008 of each supplier :

| (2) |

against an estimated aggregated growth of purchases from all its customers, We assume that the change in purchases of a buyer between one year to the next is uniform across all his suppliers. So the estimated purchases of buyer from supplier in 2008 is the payment received in 2007, , weighed by the trend in purchases of :

Summing over all supplier ’s customers gives an estimate of the growth in his sales from 2007 to 2008:

| (3) |

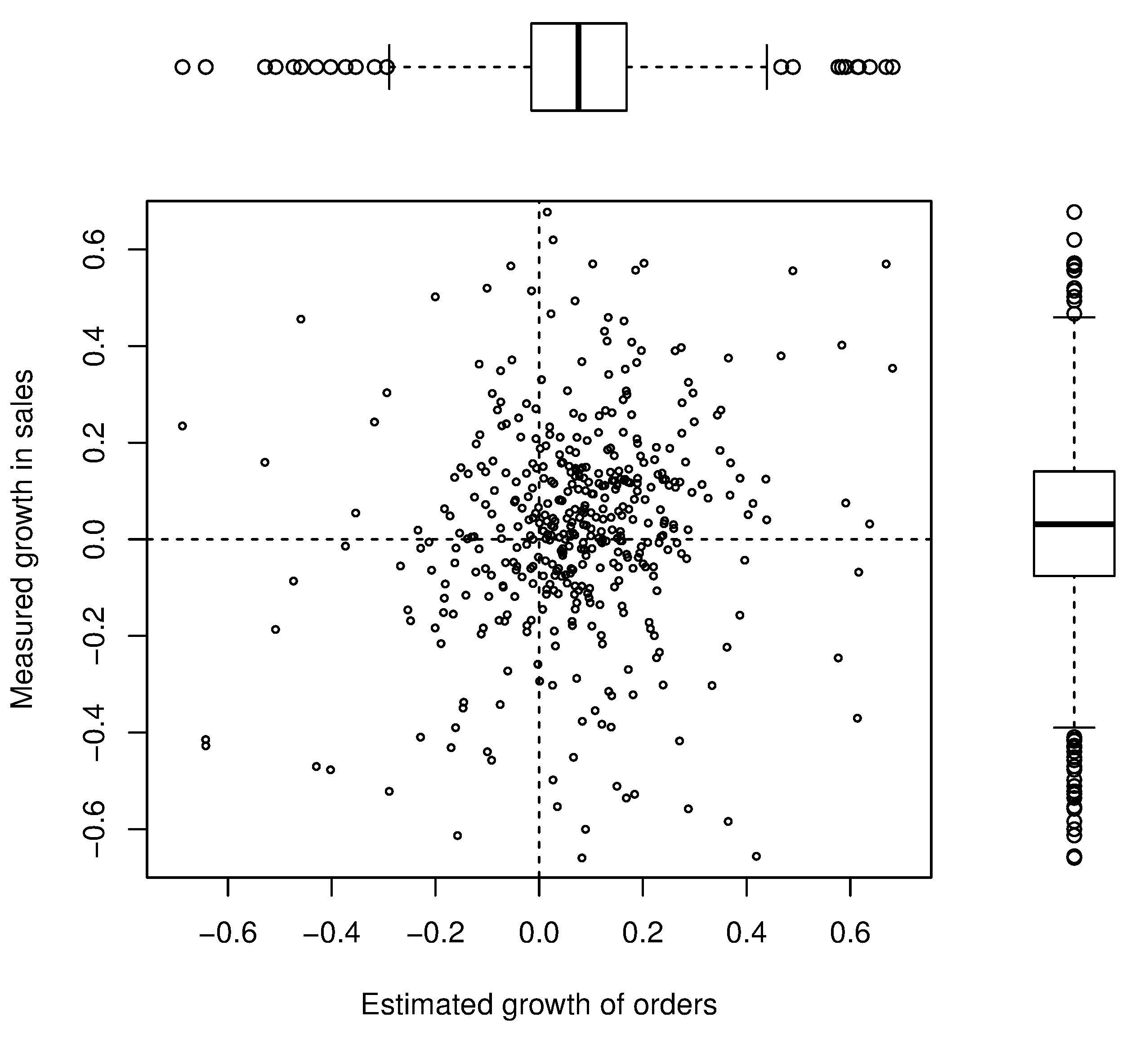

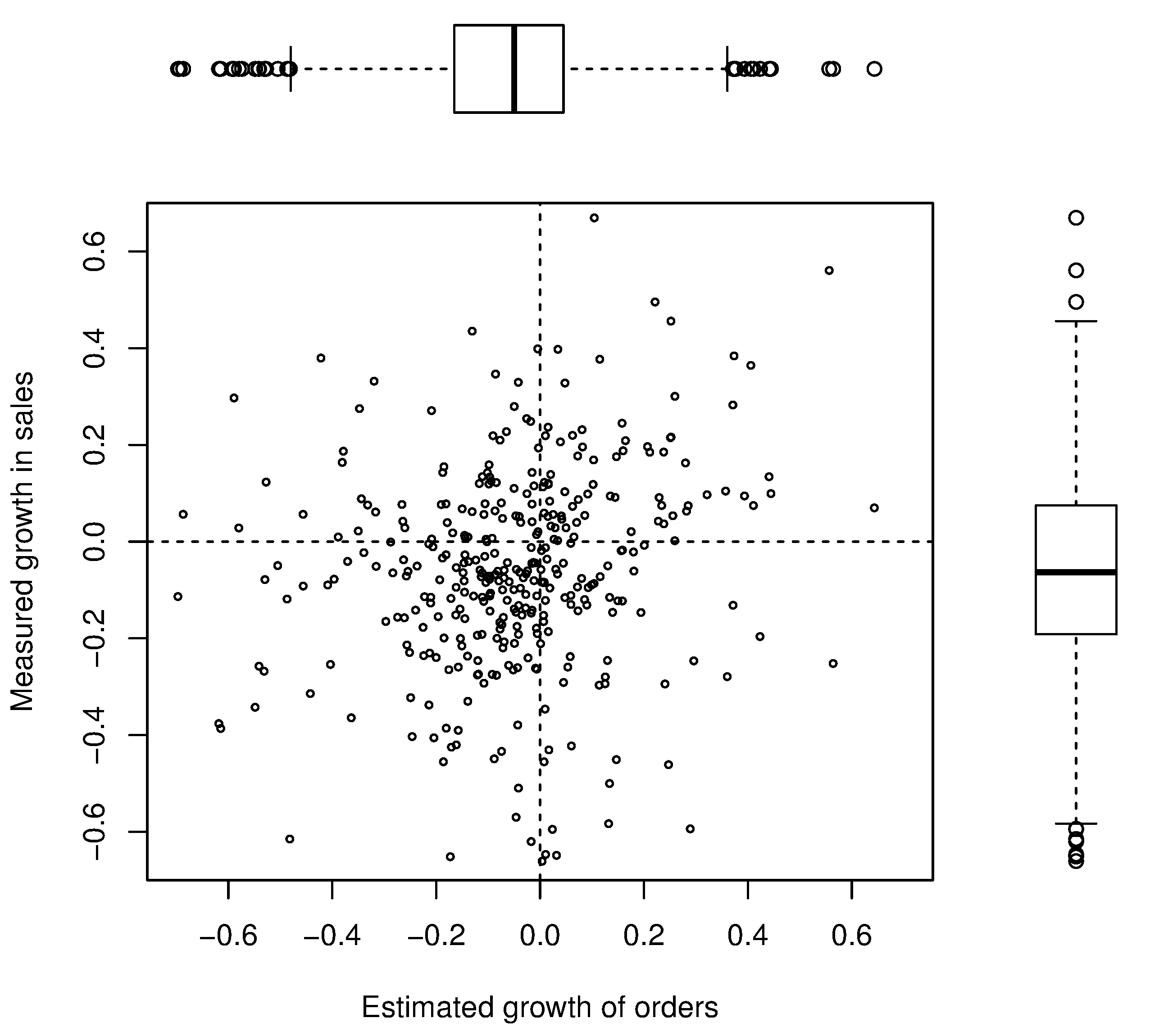

If we place (2) on the Y-axis and (3) on the X-axis we obtain a 2-dimensional scatter in which a dot will travel in the upward direction away from the origin to mark a firm with growing sales, and will travel to the right of the origin to designate growing predicted growth in sales. This scatter plot is shown in figure 3(b).

Assuming that the links in the 2007 network are constant across the three-year frame (2006, 2007, 2008) and that customer’s purchases correspond to supplier’s sales, the resulting pattern is expected to form a straight line through the origin with a slope of .

We applied the same aggregation and estimation procedure to the prior period. Applying similar reasoning, we write the growth in sales (2006-2007) as

| (4) |

again, assuming that any change in the customer pool of a supplier between 2006 and 2007 is negligible, we write the aggregated growth in orders for that period as

| (5) |

Figure 3(a) displays this scatter plot.

It is important to note the magnitude of the growth rates: for the majority of the suppliers, a small increase in orders to the supplier correspond with a small increase in the annual net-sales. This is the reason that the bulk of the points are close to the origin of the axes. i.e. the growth rate distribution is extremely narrow and deviations are dominated by the rare events. We should still expect that by the scaling nature of the growth rates [21], the rare events will render the same occurrence as the frequent ones.

In the subplots of figure 3 we added (top and right side of each subplot) a box-and-whisker plot on the sides to mark the univariate growth rate and predicted growth distributions. In these sidebars we can note two features: (1) that the estimated growth rate distribution is also narrow, i.e. shows similarity to the tent-shaped actual growth rate distributions, and that (2) the positions of the median growth rate values indicate that the centroid of the pattern in the period 2007/2006 (panel 3(a)), the median value of both, the estimated and the real growth of all suppliers is positive. The growth in the estimated sales is larger then the measured one. In contaxt to that, in the next period, 2008/2007 (panel 3), the centroid sits in the third quadrant, i.e. the meadian values of the box plots in show negative growth of both the estimated and the real sales of the suppliers.This is an evidence of the transition between an economic boom (a positive growth in sales and demand) in the first period and a bust (negative growth in demand and sales) in the second period. The results show that a decline of growth in sales and purchases in the second period (an incline in the first) occurred concurrently for suppliers and buyers.

This simultaneous switch in the typical behavior is the effect of the credit crunch: the purchasing power of the customers has shrunk as most of the suppliers were not able to allow credit to their customers.

However, figure 3 fails to prove the correlation between the estimated and the real sales of customers. Even by visual inspection, it is evident that the slope of is not present. The conclusion we draw from the plot is that in the selected sample little or no correlation exists between the aggregated changes in purchases by a supplier’s customers and the growth rate in that supplier’s Sales.

Some companies, however, do not ‘follow the crowd’ by going negative for several reasons apply, among which are regulatory actions and the sectoral behavior which we will analyze in the sequel.

4.4 Sectoral differences

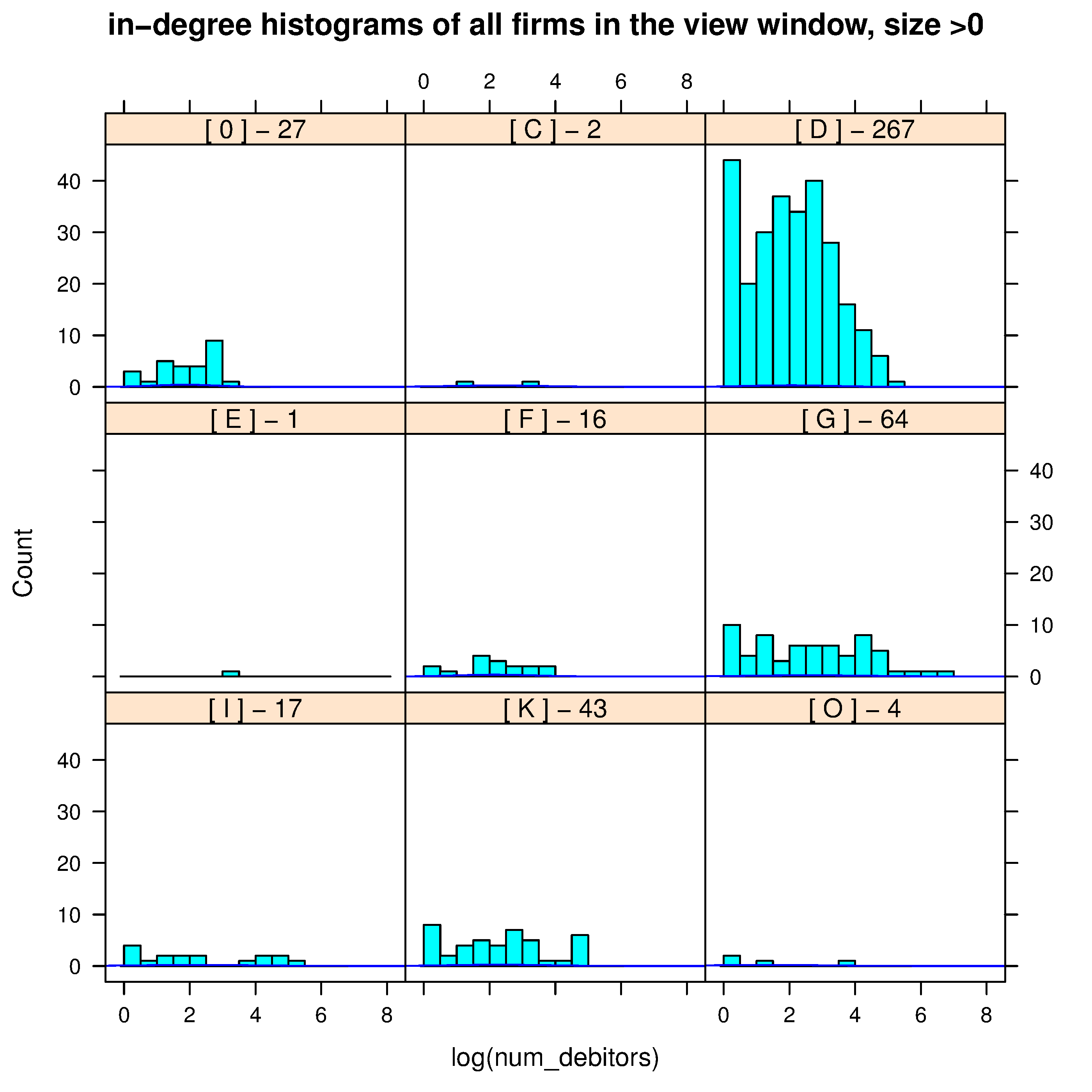

The sub-sample of the network () consists of a heterogeneous set: there is a large variability in the connectivity pattern (in-degree) and in the net-sales. But the most relevant diversification factor (and possibly related to the previous ones) is that the companies come from different industries. About a half of the selected suppliers are in the Manufacturing sector (industrial classification numbers 15xx-37xx). The other half of the sample are in other industries, primarily in Construction, Wholesale, and Transport. The degree distributions and the composition of the sample satisfying the 80-120% Matching criterion are given in figure 4.

There is a striking difference in the connectivity between the sub-samples from different industrial sectors. The Manufacturing sector (D) is the most populated, and the in-degree histogram of the companies within this sample shows that the companies follow the general in-degree distribution of figure 1. The second largest sector is Wholesale trade and Retail (G). We note that the number of companies with large in-degree in sector G is exaggerated. Comparing with the histogram of sector D, in G, the number of firms with is as large as that in D although the total number of firms is 4 times smaller. This is due to the different nature of their businesses as will be explained further in the text. The third largest sector is K. In our data set, most of the companies in this sector are IT (software) companies. Again, the accounting procedures in IT are different from the ones in Manufacturing. Software companies will often provide services rather than goods.

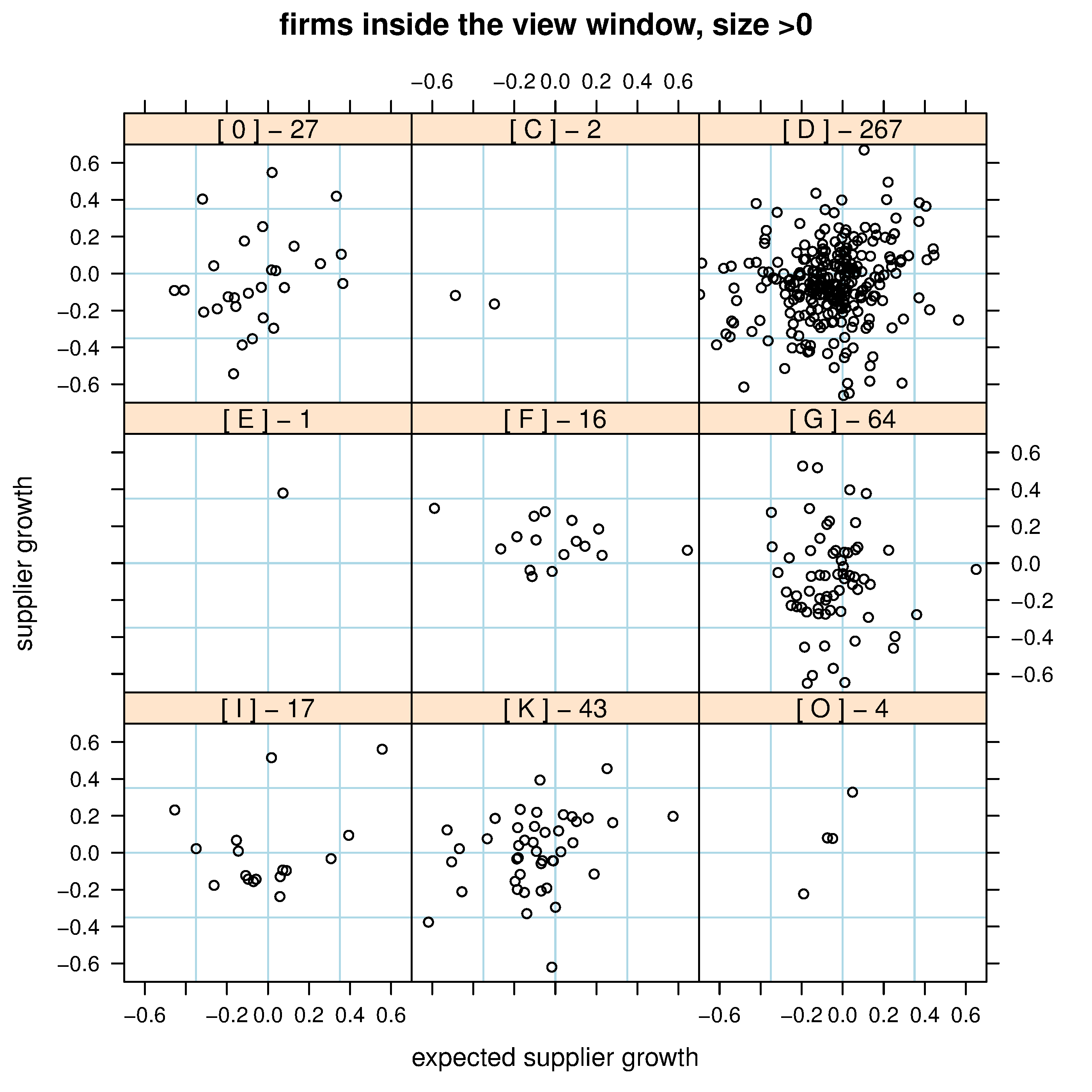

In order to understand the differences in growth rate correlation between the suppliers coming from different industrial sectors and their customers, the scatter plot in figure 3 was split by sectoral subgroups. The subgroups are shown in figure 4, and the split growth rate scatter plots are given in figure 5. In this figure, there are significant differences on the sectoral level. Most remarkable is the characteristic behavior of the G sector (the general name is ‘Wholesale and Retail’, but in our database it is mostly composed of Wholesale firms). In this sector a significant number of firms has an estimated growth of orders close to one333shows as zero on a logarithmic scale, and the meaning is ‘no growth’, but the measured growth in sales shows a notable variability away from no-growth.

Another sector that shows uncommon behavior is sector F, Construction. In this sector the growth response is opposite to the situation in sector G: there’s a large variability in the expected growth of customer orders but the recorded growth of supplier Sales shows very little deviation from a state of no-growth. The atypical in-degree distribution in the Construction industry is discussed in Miura et al. [3]. In the Japanese industrial business network, they ran a flow algorithm and observed a difference between in-degree and the ability to source or receive money. In Construction, a large in-degree of a firm may not indicate large amounts of inflowing funds since at times they may relay funds via small single-customer subcontracting firms that dominate their payment distribution (firms that exist only to operate in a single one project).

In our network we also observe greater intra-industry trade in Construction, more than would be expected by chance. However, as can be seen from figure 4, sector F (center panel) is small in total number of firms.

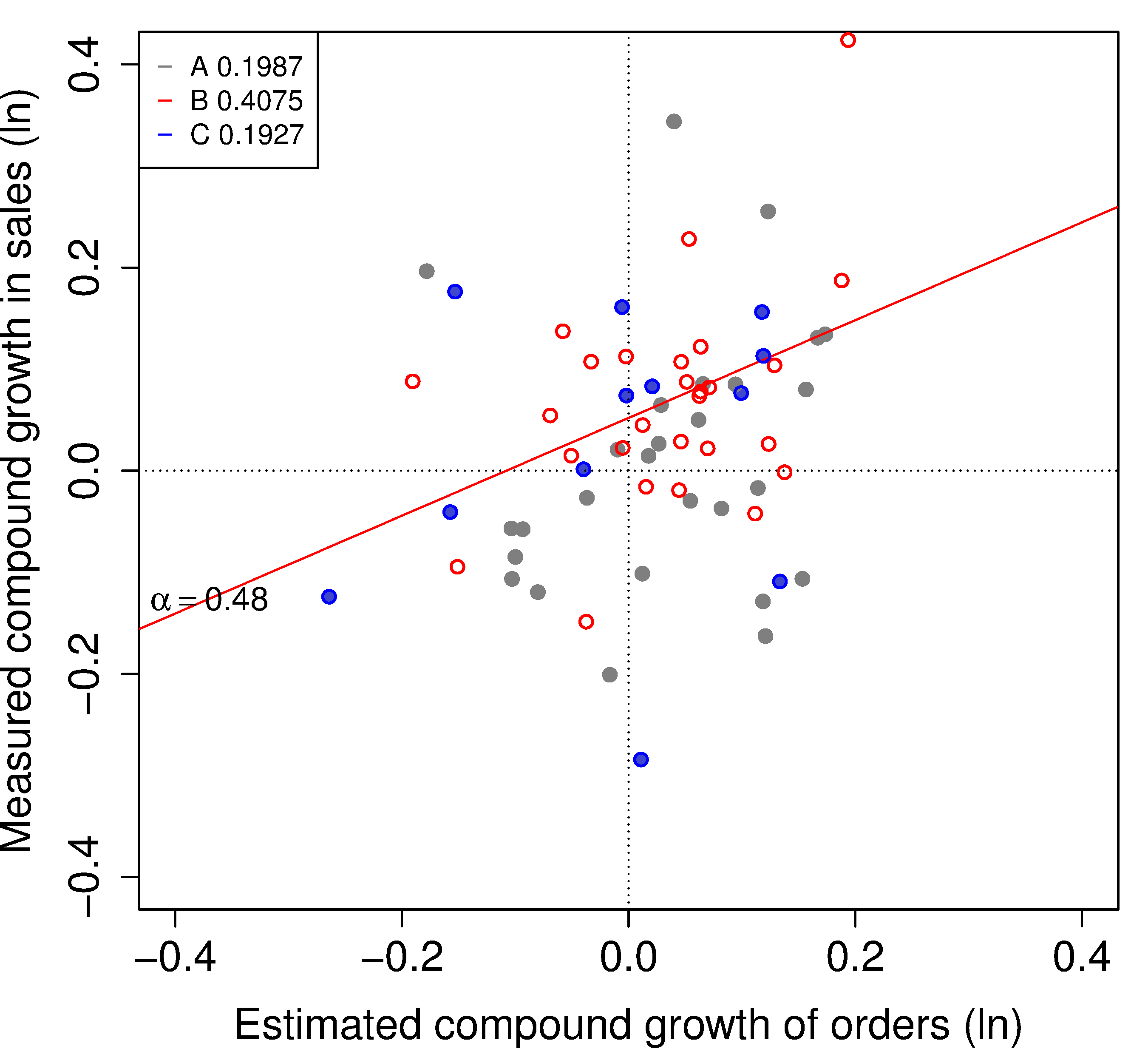

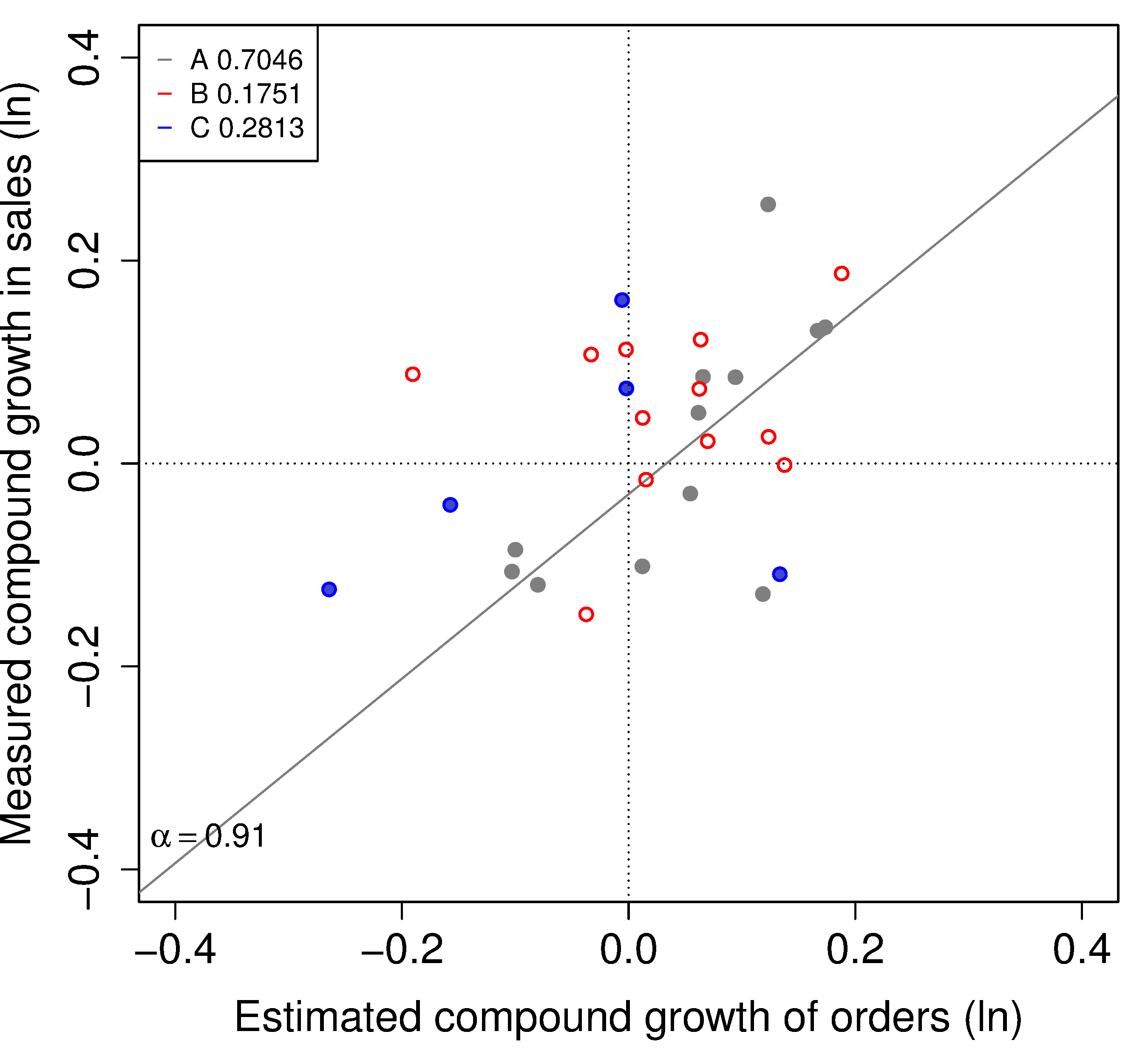

In order to factor out the possible cause of heterogeneity in behavior we chose suppliers that belong in a single industrial sector. Being the largest in the sample, we chose a sub-sector of Manufacturing, ‘Machinery and mechanical equipment’. This sector is well represented in the Italian trade network. We further tried to distill the effect of contagion by observing the geometric mean of growth rates in two consecutive periods 2007/6 and 2008/7. This is commonly termed the Compound Annual Growth Rate (CAGR). The plots of CAGR are given in figure 6. There we placed the CAGR of the supplier on the Y-axis versus the predicted CAGR from the sum of the purchases of his trade-credit customers on the X-axis. Colors of the dots mark the Rating class of the companies: ABC=A in gray, B in red, and C in blue.

The scatter plot in figure 6 may be interpreted in the following way: the companies in the first quadrant have managed to keep positive growth of both sales and orders in the two-year period. In both panels we observe that points in this quadrant are red. This means that the suppliers with Rating class B (4-6) managed to maintain their sales and orders with the same partners over the two year period and through the financial crisis. Although this result is in contrast with the hypotheses proposed in [22], it did not come as a surprise. The homophily measurement on the same data set that is discussed in Kelman et al [23] gives clear evidence that same Rating-class firms have a greater probability to attach to each other, with a small tendency of the customer to create business with a higher rated supplier.

In the second quadrant are locate suppliers that kept their growth in sales, opposing the downward trend in orders by their customers. Negative estimated growth but positive real growth could happen for many reasons. The most obvious one draws from our assumption that the network is static. This is only an approximation and although in the Manufacturing sector it is mostly a good one, in some cases it is possible that financial changes take place and trading partners change over time, especially the ones that are credit-constrained. According to Delli Gatti et al. [24], the origin of fluctuations is due to the ever-changing configuration of the network of heterogeneous firms and the entire dynamics is being shaped by financial variables. The number of companies in this quadrant is also very small (only 4 firms with Sales larger than 1 million EUR out of only 13 firms in the sample).

The suppliers in the third quadrant were affected by the crisis the most. Both the orders from them and their own sales have decreased. In this range, surprisingly, we find the suppliers from the top Rating class ‘A’. Having a good credit-rating is related with the Current Ratio and liquidity of the firm as previously demonstrated by Beaver [25] and later by Ohlson [26] and others. Also, having a good credit-rating corresponds with easy access to bank credit. i.e. the borrower is able to obtain a greater proportion of his collateral on loan, with a low interest. However, a good liquid position does not correspond with the state of the market in general, therefore these companies were not able to maintain their growth rate in the time frame of the crisis.

Last, in the fourth quadrant are the suppliers, which estimated aggregated orders grew while their sales decreased. There could be several reason for this, though this might also be a sign that the network was not stable as expected, so the customers have purchased from a new supplier.

The most interesting outcome of these measurements is the correlation of the CAGR with both Rating and firm size: Observing the Pearson’s correlation coefficients, given in the keys of the subfigures of figure 6, we could see that the correlation between the compound annual growth rates in sales and orders are the highest () in the case of large sized A-class companies. In the second place come the medium credit-rated B-class companies, in the case of all firms, with the correlation coefficient of . The companies with Rating class C did not exhibit correlations greater than either in the case of all firms or large firms.

An additional support for the very good correlation between the expected growth of customers’ orders and the growth of sales in the companies with top Ranking (and therefore good access to credit), can be find in the literature. Recently, several scholars [22], [27] attempted to model and empirically confirm the effect of the 2007-2008 financial crisis on between-firm liquidity provision. Searching for a causal effect of a credit-rationing by the banks, Garcia-Appendini & Montoriol-Garriga [27] tested the hypothesis that firms with high liquidity levels before the crisis, increased the trade credit extended to other corporations and subsequently experienced better performance compared to ex-ante cash-poor firms. They conclude that trade credit taken by constrained firms increased during this period. Therefore, they have intested in mainaining their customers and this might explain the high correlation which we measured.

5 Conclusion

This work examines correlation of the estimated growth rates of customers’ orderd with the measured growth rate of suppliers’ sales in a many-to-one setting, where the customers of each supplier are responsible for at least 80% of the supplier’s sales, measured at the beginning of the second time period. By establishing their trade connections in during one year period, a growth rate prediction is made from a combination of the trend in purchases by these customers, and the social structure in the supplier’s neighborhood. This prediction is compared with the real growth in sales of the suppliers. Results indicate the existence of growth rate contagion only inside the following restricted sub-selections of the manufacturing firms, and compound over two years: (1) the large firms with A-class credit-rating, and (2) suppliers of any size that have medium credit-rating (B-class).

This gives evidence that direct contagion of growth rates between customers and suppliers is sensitive to the following factors:

-

•

sectoral heterogeneity: in general, the industry of a supplier and a customer may or may not be the same. Each industrial sector has a behavior that is characteristic to it due to the accounting procedures required in that industry.

-

•

in data coming from the bank, microscopic effects are still secondary compared to macroscopic effects, even during a state of crisis since the problematic customers may avoid approaching the bank.

-

•

missing data: while carefully considering numerical drift and retaining the overall statistics, the cleaned and filtered sample is still three orders of magnitude smaller than the number of firms in the full data set.

We are also aware that performing the mesoscopic many-to-one approach in the rather limited (especially in terms of network dynamics) data has been based on the assumptiosn that may not be valid - especially in the case of the crisis. It is expected that the customers, in the case when they have to shrink their orders, would be selective in the choice of the suppliers and they would not shrink their orders uniformly as our model assumes. However in order to know how the customers make these decision we would need to have more data.

As a final note, the macroscopic effect that was captured by the measurements in figure 3 is realistic and its interpretation is supported by the official statistics on industrial production and business confidence in the given period: the statistics show that the Italian industrial production peaked in 2007 and then declined, reaching a 10-year low in 2009.

Acknowledgments

The work presented in this article is partly supported by the project “A Large Scale Network Analysis of Firm Trade Credit”, project grant IN01100017, Institute for New Economic Thinking (INET).

References

- [1] Golo N, Bree DS, Kelman G, Ussher L, Lamieri M, Solomon S (2015). Too dynamic to fail - Empirical support for an autocatalytic model of Minsky’sfinancial instability hypothesis. To appear in the Journal of Economic Interaction and Coordination.

- [2] Tamura K, Miura W, Takayasu M, Takayasu H, Kitajima S, et al. (2012) Estimation of Flux Between Interacting Nodes on Huge Inter-Firm Networks. World Scientific, volume 16, pp. 93– 104.

- [3] Miura W, Takayasu H, Takayasu M (2012) The origin of asymmetric behavior of money flow in the business firm network. European Physical Special Topics 212: 65-75.

- [4] Watanabe H, Takayasu H, Takayasu M (2012) Biased diffusion on Japanese inter-firm trading network: Estimation of sales from network structure. New J Phys 14.

- [5] Kiyotaki, Nobuhiro, and John Moore. Credit cycles. No. w5083. National Bureau of Economic Research, 1995.

- [6] Boissay F (2006) Credit chains and the propagation of financial distress. Technical Report 573, European Central Bank. URL http://ideas.repec.org/p/ecb/ecbwps/20060573.html.

- [7] Petersen MA, Rajan RG (1997) Trade Credit: Theories and Evidence. The Review of Financial Studies 10: 661–691.

- [8] Schumpeter JA (1976) Capitalism, Socialism and Democracy. New York: Allen & Unwin.

- [9] Solomon S, Richmond P (2002) Stable power laws in variable economies; Lotka-Volterra implies Pareto-Zipf. The European Physical Journal B - Condensed Matter and Complex Systems 27: 257–261.

- [10] Challet D, Solomon S, Yaari G (2009) The universal shape of economic recession and recovery after a shock. Economics: The Open-Access, Open-Assessment E-Journal 3.

- [11] Goldenberg J, Libai B, Solomon S, Jan N, Stauffer D (2000) Marketing percolation. Physica A: Statistical Mechanics and its Applications 284: 335–347.

- [12] Solomon S, Golo N (2013) Minsky Financial Instability, Interscale Feedback, Percolation and Marshall–Walras Disequilibrium. Accounting, Economics and Law 3: 167–260.

- [13] Minsky HP (1982) The Financial-Instability Hypothesis: Capitalist Processes and the Behavior of the Economy. In: Kindleberger C, Laffargue JP, editors, Financial Crises: Theory, History and Policy, Cambridge University Press. pp. 13-38.

- [14] Shnerb NM, Louzoun Y, Bettelheim E, Solomon S (2000) The importance of being discrete: Life always wins on the surface. Proceedings of the National Academy of Sciences 97: 10322–10324.

- [15] Louzoun Y, Shnerb NM, Solomon S (2007) Microscopic noise, adaptation and survival in hostile environments. The European Physical Journal B-Condensed Matter and Complex Systems 56: 141–148.

- [16] Klass OS, Biham O, Levy M, Malcai O, Solomon S (2007) The Forbes 400, the Pareto power-law and efficient markets. The European Physical Journal B 55: 143-147.

- [17] Choi Y, Douady R (2012) Financial crisis dynamics: attempt to define a market instability indi- cator. Quantitative Finance 12: 1351–1365.

- [18] Huang ZF, Solomon S (2001) Finite market size as a source of extreme wealth inequality and market instability. Physica A: Statistical Mechanics and its Applications 294: 503–513.

- [19] Krugman P (1999) Balance sheets, the transfer problem, and financial crises. International Tax and Public Finance 6: 459–472.

- [20] Bottazzi G, Grazzi M, Secchi A, Tamagni F (2011) Financial and economic determinants of firm default. Journal of Evolutionary Economics 21: 373–406.

- [21] Schwarzkopf Y, Axtell RL, Farmer JD (2010) The cause of universality in growth fluctuations. ArXiv Nonlinear Sciences e-prints .

- [22] Shenoy J, Williams R (2011) Customer-Supplier Relationships and Liquidity Management: The Joint Effects of Trade Credit and Bank Lines of Credit. SSRN .

- [23] Kelman G, Bree D, Manes E, Lamieri M, Golo N, et al. (2015) Dissortative From the Outside, Assortative From the Inside: Social Structure and Behavior in the Industrial Trade Network. In: Proceedings of the 48th Annual Hawaii International Conference on System Sciences. IEEE, Computer Society Press, 2015, p. 10.

- [24] Delli Gatti D, Gaffeo E, Gallegati M, Giulioni G, Palestrini A (2008) Emergent macroeconomics: an agent-based approach to business fluctuations. Springer.

- [25] Beaver WH (1966) Financial Ratios As Predictors of Failure. Journal of Accounting Research (4) Empirical Research in Accounting: Selected Studies: 71-111.

- [26] Ohlson JA (1980) Financial Ratios and the Probabilistic Prediction of Bankruptcy. Journal of Accounting Research 18: 109-131.

- [27] Garcia-Appendini E, Montoriol-Garriga J (2012) Firms as liquidity providers: Evidence from the 2007-2008 financial crisis. Available at SSRN 2023583 . Petersen:1997kx