Transition from lognormal to -superstatistics for financial time series

Abstract

Share price returns on different time scales can be well modeled by a superstatistical dynamics. Here we provide an investigation which type of superstatistics is most suitable to properly describe share price dynamics on various time scales. It is shown that while -superstatistics works well on a time scale of days, on a much smaller time scale of minutes the price changes are better described by lognormal superstatistics. The system dynamics thus exhibits a transition from lognormal to superstatistics as a function of time scale. We discuss a more general model interpolating between both statistics which fits the observed data very well. We also present results on correlation functions of the extracted superstatistical volatility parameter, which exhibits exponential decay for returns on large time scales, whereas for returns on small time scales there are long-range correlations and power-law decay.

I Introduction

Many well established concepts in mathematical finance (such as the Black-Scholes model) are based on the assumption that an index or a stock price follows a geometric Brownian motion, and as consequence the log returns of these processes are Gaussian distributed. But nowadays it is well known that the log returns of realistic stock prices are typically non-Gaussian with fat tails ref1 –tsallisbook . Such behaviour can be well captured by superstatistical models ref2 –thurner . The basic idea of this method borrowed from nonequilibrium statistical mechanics is to regard the time series as a superposition of local Gaussian processes weighted with a process of a slowly changing variance parameter, often called . This approach has been applied to many areas of complex systems research, including turbulence, high energy scattering processes, heterogenous nonequilibrium systems, and econophysics (see e.g. ref9 for a short review). In finance early applications of the superstatistics concept were worked out by Duarte Queiros et al. queiros1 ; queiros2 and Ausloos et al. ausloos . Van der Straeten and Beck ref3 analysed daily closing prices of the Dow Jones Industrial Average index (DJI) and the SP 500 index. They verified that both log-normal superstatistcs and superstatistics result in good approximations. Biro and Rosenfeld ref4 also studied the data sets of the Dow Jones index and verified that the distribution of log returns is well fitted by a Tsallis distribution. Katz and Li Tian ref1 showed that the probability distributions of daily leverage returns of 520 North American industrial companies during the 2006-2012 financial crisis comply with the -Gaussian distribution which can be generated by superstatistics. They also verified in ref2 that the Tsallis entropic parameter obtained by direct fitting to -Gaussians coincides with the obtained from the shape parameters of the distribution fitted to the histogram of the volatility of the returns. Gerig, Vicente and Fuentes ref6 consider a similar model that indicates that the volatility of intra day returns is well described by the distribution, see also ref7 for related work in this direction.

In this paper, we will carefully analyse for various data sets of historical share prices which type of superstatistics is best suited to model the dynamics. While Tsallis statistics (-statistics) is known to be equivalent to superstatistics beck-cohen ; tsallisbook , there are other types of superstatistics, such as lognormal superstatistics and inverse superstatistics ref8 , which are known to be different from -statistics (though all these different statistics generate similar distributions if the variance of the fluctuations in is small beck-cohen ). We show that in our analysis -superstatistics appears best suitable to describe the daily price changes, whereas on much smaller time scales of minutes lognormal superstatistics seems preferable. We analyse the relevant time scale of the changes in the superstatistical parameter and present results for the decay of correlations in . For small return time scales, correlation functions exhibit power law decay and there are long memory effects. In the final section, we develop a synthetic stochastic model that fits the data well. This is kind of a hybrid model interpolating between lognormal and -superstatistics.

This paper is organized as follows. In section II we look at share price returns on large (daily) time scales. In section III we do a similar analysis on small (minute) time scales. In section IV we investigate correlations of the superstatistical volatility parameter on both time scales. In section V the hybrid model is introduced. Our final concluding remarks are given in section VI.

II Superstatistics of log-returns of share prices on a large time scale

Non-equilibrium system dynamics can often be regarded as as superposition of a local equilibrium dynamics and a slowly fluctuating process of some variance variable beck-cohen . These types of ‘superstatistical’ nonequilibrium models are also useful for financial time series queiros1 ; queiros2 . In this article, the empirical data we use as an example is the historical stock prices of Alcoa Inc(AA), which is an American company that engages in the production and management of primary aluminium, fabricated aluminium and alumina. We have looked at shares of many other companies as well (see Tab. 1 in section IV), with similar results. Our data set covers the period January 1998 to May 2013. We study the log return denoted by

| (1) |

where ; and are two successive daily closing prices. We consider the normalised log returns

| (2) |

which have been rescaled to have variance 1. The symbol denotes the long-time average.

From the simplest superstatistics model point of view, the entire time series of stock prices can be divided into smaller time slices . We call optimal window size. Within each , the financial volatility is temporarily constant and the log return of the stock price is Gaussian distributed. has some probability distribution to take a particular value in a given slice. The conditional probability is

| (3) |

and the marginal probability distribution of for long time observation is the average over local Gaussians weighted with the probability density

| (4) |

The integration over yields non-Gaussian behaviour with fat tails.

We now describe our technique to obtain the optimal window size for a given time series. Firstly we split the time series into

| (5) |

equal intervals, where denotes the floor function and is the dimensionless window size, i.e. the number of data points in a given window. is the total number of data points of the entire time series. Generally the kurtosis of a random variable is defined as

| (6) |

and it is equal to 3 for a Gaussian distribution of arbitrary variance. For a given window size , the kurtosis in the th window is given by

| (7) |

where When we have all the values of kurtosis for all windows, we can calculate an average kurtosis of the windows as

| (8) |

The aim is to achieve an optimum window size such that for a given data set the distribution in each window is as close as possible to a Gaussian, but with varying variance. For this purpose the optimal window size should satisfy the condition

| (9) |

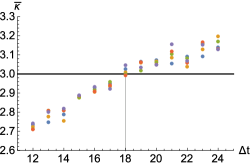

Fig. 1 shows how the average kurtosis changes with the window size. We obtain from condition (9) the optimal window size for this example. The result makes financial sense. 18 trading days correspond to a time scale of about 3-4 weeks. It is a typical time scale where market volatility changes, due to events such as changes in the confidence in the future economic development, anticipated interest changes, and so on. See also camilleri for related work.

With the given optimal window size, we can now calculate the local volatility parameter in each time interval as

| (10) |

where . Note that the variance of in each window is . One can then plot a histogram of the and fit it with some suitable model distribution.

Here we will consider three distributions to be compared with our experimental distribution of , which were previously advocated in ref8 . The first one is the -distribution for which is given by

| (11) |

The second one is the inverse -distribution where

| (12) |

The third distribution that will be tested is the log-normal distribution for which the probability density function is given by

| (13) |

where

| (14) |

The in Eq. (14), (11), (12) is the mean value of , given by

| (15) |

and are parameters. Lognormal superstatistics often occurs for complex systems described by a cascading dynamics ref10 , whereas and inverse superstatistics are more common for additive degrees of freedom contributing to a fluctuating temperature or inverse temperature ref8 .

We have fitted our experimental histograms with the above distributions. Given , we vary and of Eq. (11), (12), (13) in order to obtain the optimum fit to our observed .

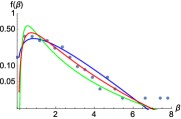

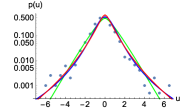

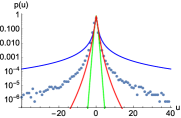

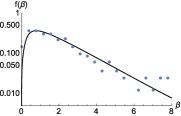

It can be seen in Fig. 2 that lognormal, - and inverse superstatistics all yield a more or less decent fit, though inverse -superstatistics seems less favorable.

Still for consistency we also need to check the validity of Eq. (4). We thus also compare the original histogram of returns with the following integrals where the parameters take the same values as in Fig.2:

| (16) |

As shown in Fig. 3, for the integrated densities superstatistics seems to fit better to the probability density of compared with lognormal superstatistics and inverse superstatistics.

Thus, if independent variation of the volatility parameter in each interval is assumed, then the data clearly point to superstatistics, equivalent to Tsallis statistics tsallisbook . On the other hand, independence of may not always be a good approximation. There can be strong correlations of the volatility parameter , and variations of the time scales where it is approximately constant. In that case more complicated dynamics arise, and one could then possibly get a better fit for the integrated distributions if other effective parameters are used. For this reason, we also allowed the fitting parameters for to take on other possible values. The result of this ‘amended superstatistics’ is shown in Fig. 4.

After the adjustment, we find in Fig.4 that in fact all three superstatistics can describe quite well. To distinguish between them, one would need much more data so that the tail behaviour would be clearer. In practice, more data are available if one considers price changes on much smaller time scales than days. This will be done in the next section.

III Short time scales

Let us extend our analysis to returns on much smaller time scales. A change of statistics as a function of the time scale considered is a common phenomenon for many complex systems, see e.g. peng ; scafetta for work in this direction. Hence it is interesting to also consider return data on much smaller time scales (say, minutes), and see what is similar and what is different as compared to the analysis of the previous section. Let be the stock price for every recorded minute, in our example chosen as that of Alcoa Inc(AA). The total number of data points is about 1.5 million. We look at the returns

| (17) |

where is an integer in units of minutes. The log returns are again normalized to variance 1:

| (18) |

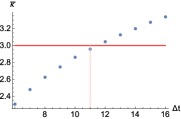

There is one small technical problem for these types of data, as the returns are not given overnight but only during normal working hours. This can lead to big overnight jumps and affect the analysis. For this reason, if and are from two successive trading days, we removed the corresponding . means the log return is extracted every minute. Again we determined the optimal window size, using the same technique as in the previous section. We obtain (see Fig. 5).

Again this time scale of about 11 minutes makes sense. It is a typical time scale on which new relevant information becomes available to the traders, leading to changes in the small-scale volatility. It also coincides with typical time scales on which observed correlations in short-term returns start to decay vicente . Our results of fitting the three types of superstatistics are shown in Fig. 6-8.

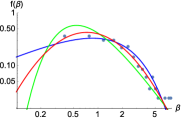

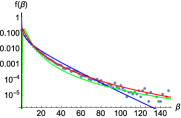

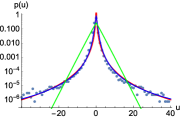

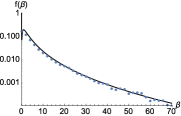

As can be seen in Fig. 6, the lognormal distribution is by far best fit of if the time scale is 1 minute.

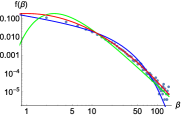

Fig. 7 shows a clear difference as compared to the daily data in Fig. 3: The integrated formula now does not give good fits to . The reason is that the on a time scale of minutes are not anymore statistically independent, hence random sampling of Gaussians with different variance is not appropriate anymore.

After the free adjustment in the parameters of , again both and lognormal superstatistics can provide good fits of . See Fig. 8.

If one does not allow for parameter amendments, then we can conclude that there is a transition from to lognormal superstatistics when the time scale changes from 1 day to 1 minute. Also, a more general conclusion seems to be that the assumption of a sequence of independent volatility parameters is not valid, as we are getting in general differences between the optimum fit of and the corresponding fit of written as an integral over Gaussians with the same corresponding parameters.

IV Correlation functions

For the development of a suitable dynamical model, it is very important to look not only at probability densities but also on correlation functions and memory effects cotter –evans . In our case there are two types of correlation functions: the one of the original data ,

| (19) |

and those of the volatility parameter ,

| (20) |

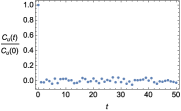

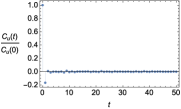

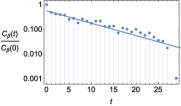

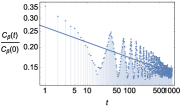

Figs. 9-12 show and , both for the daily returns as well as for the 1-minute returns. As is illustrated in Fig. 9 and 10, decays almost immediately to zero, both for the daily and minute data.

More interesting is the correlation function . We did an analysis of the decay rates of correlation functions of the volatility for many different shares from different sectors, the results are summarized in Tab. 1. We observe that the correlation functions of volatility decay in an exponential way for daily returns, , whereas for minute return there is a power law decay with a periodic modulation, see Figs. 11-12 for the example of AA shares. The strongest correlation decay (largest ) on the daily scale is observed for shares from basic materials, whereas the power law decay (exponent ) on the small time scale is largest for healthcare shares and shares from the consumer good sector. Note that a strong decay of the volatility correlation function in a sense measures a ‘volatility of a volatility’ and is an interesting quantity to study. The period of oscillations that we observe in figures such as Fig. 12 corresponds (roughly) to one trading day and is consistent with periodic oscillations of intraday volatility reported previously in bolleslev .

![[Uncaptioned image]](/html/1506.01660/assets/x15.png)

Tab. 1: Decay rates of correlation functions of volatility for shares of different sectors

V Synthetic model

Based on the results of the previous sections, it is desirable to construct a simple superstatistical dynamical model that incorporates the possibility of both lognormal and superstatistics on different scales, and allows for different decay patterns of correlation functions.

Here we propose the following model. We start from a linear superstatistical Langevin equation

| (21) |

where is Gaussian white noise and the ‘inverse temperature’ , in accordance with Einstein’s theory of Brownian motion, is defined as

| (22) |

Given a fixed , the variance is given by for time . However, for the superstatistical version we allow for fluctuations in the parameter . Then the above Langevin equation is –by construction– superstatistical as we do not keep the parameter constant but regard it as a random variable that fluctuates on a large time scale. Eq. (21) generates a stochastic process and in the end, after has taken on many different values, one may rescale the entire time series to variance 1 using the variance of the complete time series, as we did in eq.(2) and (18)).

Let us now consider Gaussian random variables , which are statistically independent and have the same variance and mean 0 (except for which may have potentially a different variance and different mean). We then write as

| (23) |

where is a parameter. We now see that if , this system generates lognormal superstatistics, as is a Gaussian random variable. On the other hand, if this system generates -superstatistics with degrees of freedom, as in this case is distributed. Choosing any value of one can interpolate between lognormal and superstatistics, getting a mixed type of behaviour.

The Gaussian random variables can again be simulated by ordinary linear Langevin equations of the form

| (24) |

For constant and these equations generate the Ornstein Uhlenbeck process, i.e. a Gaussian Markov process with exponential decay of correlation functions. More complicated dynamics, leading e.g. to power law decay of correlation functions, can be constructed if the driving forces in these linear stochastic differential equations are not Gaussian white noise but more complicated correlated processes, or critical maps with a near-vanishing Liapunov exponent tirnakli .

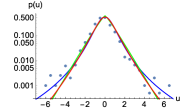

Fig. 13 and Fig. 14 show that indeed the observed distributions of for Alcoa shares are best fitted by intermediate distributions (a superposition of a lognormal and distribution with appropriate weights). The parameter increases if one goes from larger to smaller time scales of returns. The mixed synthetic model is able to reproduce the transition scenario of observed densities from superstatistics to lognormal superstatistics in a quantitatively correct way, giving good fits on any time scale.

We did this analysis for a variety of time scales of returns, taking again the example of Alcoa shares. In Fig. 15 we show how the parameter depends on the time scale of returns. As expected, the parameter that best fits the observations decreases as a function of time scale. In fact we observe a logarithmic dependence if the time scale is not too big, see the straight line fit in Fig. 15.

One final remark is at order: One may generalize the superstatistics concept to more complicated local processes that are not locally Gaussian. Indeed, due to correlations present on small time scales, and/or due to a lack of clear time scale separation different distributions than Gaussians may locally be present. In this case one can still superimpose these local distributions by letting a suitable variance parameter fluctuate. It is remarkable, however, that for the financial data analysed here this generalization to more complicated non-Gaussian local processes is not necessary: The simplest superstatistics model based on local Gaussians fits our data well, assuming the interpolating model eq.(23) where the probability distribution of changes as a function of scale.

VI Conclusion

Many investigations of complex systems in the past have focused on the application of a particular statistics, for example -statistics tsallisbook , and then studying the effect of varying system parameters, which may change the entropic index . Here we have shown that for financial time series it is sometimes useful to consider broader classes of statistics and even proceed from one class of superstatistics to another when the scale or other system parameters under consideration are changed. The example we considered in detail in this paper were share price returns of various companies. We provided evidence that there is a transition scenario from lognormal superstatistics to superstatistics, with lognormal superstatistics giving a better fit to the data on small time scales and superstatistics (-statistics) on larger time scales. We constructed a hybrid superstatistical model that allows to implement both types of superstatistics, with a weighting parameter that describes how far away we are from one of the two cases. Correlation functions of the extracted superstatistical volatility parameter were shown to exhibit different qualitative behavior as a function of the time scale of returns, with exponential decay on large time scales and power law decay on small time scales, modulated by intraday periodicity. The decay parameters of the exponential or power law decay were extracted from the data and were shown to depend slightly on the sector of shares considered. The general transition scenario from lognormal to superstatistics as a function of the time scale of returns, however, is a general phenomenon and occurs for all sectors in a similar way.

References

- (1) Y.A. Katz and L. Tian, q-Gaussian distributions of leverage returns, first stopping times, and default risk,Physica A 392, 4989 (2013)

- (2) Y.A. Katz and L. Tian, Superstatistical fluctuations in time series of leverage returns, Physica A 405, 326 (2014)

- (3) E. Van der Straeten and C. Beck, Superstatistical fluctuations in time series: Applications to share-price dynamics and turbulence, Phys. Rev. E 80, 036108 (2009)

- (4) T. S. Biro and R. Rosenfeld, Microscopic Origin of Non-Gaussian Distributions of Financial Returns, Physica A 387, 1603 1612 (2008)

- (5) M. Ausloos, K. Ivanova, Dynamical model and nonextensive statistical mechanics of a market index on large time windows, Phys. Rev. E 68, 046122 (2003)

- (6) S.M. Duarte Queiros, On the emergence of a generalized Gamma distribution. Application to traded volume in financial markets, Europhys. Lett 71, 339 (2005)

- (7) S.M. Duarte Queiros and C. Tsallis, On the connection between financial processes with stochastic volatility and nonextensive statistical mechanics, Eur. Phys. J. B 48, 139 (2005)

- (8) A. Gerig, J. Vicente and M.A. Fuentes, Model for Non-Gaussian Intraday Stock Returns, Phys. Rev. E 80, 065102(R) (2009)

- (9) C. Vamos and M. Craciun, Separation of components from a scale mixture of Gaussian white noises Phys. Rev. E 81, 051125 (2010)

- (10) C.Beck, E.G.D. Cohen and H.L. Swinney, From time series to superstatistics, Phys. Rev. E 72, 056133 (2005)

- (11) C.Beck, Generalized statistical mechanics for superstatistical systems, Phil. Trans. Royal Soc. 369, 453 (2011)

- (12) C.Beck, Chaotic cascade model for turbulent velocity distributions, Phys. Rev. E 49, 3641 (1994)

- (13) C. Beck, E.G.D. Cohen, Superstatistics, Physica A 322, 267 (2003).

- (14) P. Jizba and H. Kleinert, Superpositions of probability distributions, Phys. Rev. E 78, 031122 (2008)

- (15) R. Hanel, S. Thurner, and M. Gell-Mann, Generalized entropies and the transformation group of superstatistics, PNAS 108, 6390 (2011)

- (16) J. Cotter, Uncovering long memory in high frequency UK futures, UCD Geary Institute discussion paper series (2004)

- (17) T.G. Anderson, T. Bollerslev, Heterogeneous information arrivals and return volatility dynamics: Uncovering the long-run in high frequency returns, Journal of Finance LII, No3 (1997)

- (18) T.G. Anderson, T.Bollerslev, Intraday periodicity and volatility persistence in financial markets, J. Empirical Finance 4, 115 (1997)

- (19) T. Bollerslev, J. Cai, F.M. Song, Intraday periodicity, long memory volatility, and macroeconomic announcement effects in the US Treasury bond market, J. Empirical Finance 7, 37 (2000)

- (20) S.H. Kang, S.-M. Yoon, Long memory features in the high frequency data of the Korean stock market, Physica A 387, 5189 (2008)

- (21) K.P. Evans, A.E.H. Speight, Intraday periodicity, calendar and announcement effects in Euro exchange rate volatility, Res. Int. Business Finance 24, 82 (2010)

- (22) C. Tsallis, Introduction to Nonextensive Statistical Mechanis: Approaching a Complex World, Springer (2009)

- (23) S.J. Camilleri, Month-related seasonality of stock price volatility: Evidence from the Malta stock exchange, Bank of Valletta Review 37, 49 (2008)

- (24) R. Vicente, C.M. de Toledo, V.B.P. Leite, N. Caticha, Underlying dynamics of typical fluctuations of an emerging market price index: The Heston model from minutes to months, Physica A 361, 272 (2006)

- (25) C.-K. Peng, S. Havlin, H.E. Stanley, A Goldberger, Quantification of scaling exponents and crossover phenomena in nonstationary heartbeat time series, Chaos 5, 82 (1995)

- (26) N. Scafetta, P. Grigolini, Scaling detection in time series: diffusion entropy analysis, Phys. Rev. E 66, 036130 (2002)

- (27) U. Tirnakli, C. Tsallis, C. Beck, A closer look at time averages of the logistic map at the edge of chaos, Phys. Rev. E 79, 056209 (2009)