Almost Worst Case Distributions in Multiple Priors Models111ICs acknowledges support by the Hungarian National Foundation for Scientific Research OTKA, grant No. K105840. TB acknowledges support by the Josef Ressel Centre for Applied Scientific Computing.

Abstract

A worst case distribution is a minimiser of the expectation of some random payoff within a family of plausible risk factor distributions. The plausibility of a risk factor distribution is quantified by a convex integral functional. This includes the special cases of relative entropy, Bregman distance, and -divergence. An (-)-almost worst case distribution is a risk factor distribution which violates the plausibility constraint at most by the amount and for which the expected payoff is not better than the worst case by more than . From a practical point of view the localisation of almost worst case distributions may be useful for efficient hedging against them. We prove that the densities of almost worst case distributions cluster in the Bregman neighbourhood of a specified function, interpreted as worst case localiser. In regular cases, it coincides with the worst case density, but when the latter does not exist, the worst case localiser is perhaps not even a density. We also discuss the calculation of the worst case localiser, and its dependence on the threshold in the plausibility constraint.

1 Introduction

Let the monetary payoff or utility of some action, e.g. of a portfolio choice, be described by a function of a collection of random risk factors. Suppose the probability distribution which governs the risk factors is not known exactly but may be assumed to belong to a set of distributions on the sample space of scenarios (multiple priors model). Then the worst case expected payoff

| (1) |

may be taken as (the negative of) the model risk caused by the lack of knowledge about . The same expression emerges also in the theory of preferences. Ambiguity averse decison makers may rank possible actions by the criterion of expected utility in the worst case over . Risk measures or preference criteria of a more general kind involve penalised expected payoff or utility

| (2) |

where is a suitable penalty term. For details, including axiomatic considerations leading to (1) or (2), we refer for example to Föllmer and Schied [9], Hansen and Sargent [12], or Gilboa [10].

Any risk measure satisfying some natural postulates (in which case they are dubbed coherent) can be represented as the negative of (1) for some convex set of distributions . Relaxing coherence to “convexity” yields (2), with some convex penalty term . For our purposes, axiomatic theory serves as motivation only. In that theory the infimum in (1) typically equals a minimum. In models treated in this paper, a worst case distribution attaing the minimum in (1) need not exist.

If a “best guess” of the unknown risk factor distribution is available, it is natural to use (1) with consisting of those distributions that do not deviate much from . In the literature many measures of deviation of distributions are available; the majority are non-symmetric. The most versatile one, in various scientific disciplines, is -divergence or relative entropy. For an axiomatic approach distinguishing -divergence in the context of inference see Csiszár [7] and references therein. Relaxing some axioms, that approach leads as alternatives to other frequently used measures of deviation of distributions, known as -divergences and Bregman distances, see Section 2 for definitions. In the context of risk and preferences several authors, perhaps first Hansen and Sargent [11], have considered (1) with equal to an -divergence ball around , or (2) with equal to a constant times the -divergence of from . The preference relation based on (2) with this choice of , called multiplier preferences in [12], has been axiomatically distinguished by Strzalecki [15]. Moreover, according to Ahmadi-Javid [1] the coherent risk measure he calls entropic value at risk, obtained by taking an -divergence ball for in (1), is superior to others from the point of view of computability. General -divergences have been employed in this context by Maccheroni et al.[13] and Ben-Tal and Teboulle [2], see also references in [2] to prior work of its authors. Bregman distance could be used similarly but to this we do not have references.

We consider problem (1) with of the following form, including as special cases -divergence balls, -divergence balls and Bregman balls:

| (3) |

where is a given measure on and is a convex integral functional as specified in Section 2.1. A corresponding choice of in (2) is , .

Our main focus in this paper is the location of the infimum, rather than the value of the worst case expected payoff (1) or the related infimum (2). In cases the infimum is not achieved, there is no worst case distribution, then it is not obvious what the location of infimum should mean. We introduce the concept and prove the existence of a “localiser of almost worst case distributions”, which in the following sense characterises the location of the infimum, whether or not the minimum is achieved: almost worst case distributions achieving values ever closer to the infimum are in ever smaller Bregman balls around the localiser. Part of the results were presented in the symposium contribution [4].

The problem of minimising subject to is related to the problem of minimising convex integral functionals subject to moment constraints. This problem, an extension of the celebrated “information geometric” problem of -divergence minimisation has been extensively studied in the literature. We rely upon those results in the form presented by Csiszár and Matúš [8] and we use the basic framework of Breuer and Csiszár [5] presented in Section 2.

The new results are presented in Section 3. Theorem 1 in Subsection 3.1 extends a result of Ahmadi-Javid [1, Theorem 5.1] on computing the infimum in (1) for of form (3) to our framework222This framework does include some assumptions, adopted for other purposes. which were absent in [1]. that admits also non-autonomous integrands and unbounded payoff function . Our main result, Theorem 2 in Subsection 3.2, addresses the worst case and almost worst case distributions (densities) that attain or almost attain the minimum in (1). The almost worst case densities are shown to cluster, in Bregman distance, around a specified function called worst case localiser. A similar result is obtained also for problem (2). The worst case localiser equals the worst case density if the minimum is attained, while otherwise it is perhaps not a density at all. Finally, Subsection 3.3 addresses the effect of the threshold in (3). Theorems 3 and 4 show that in many situations, including the case of -divergence balls, either a worst case distribution exists for all or else it does/does not exist for less/larger than a critical value . It remains open whether a similar result also holds in general—apart from the possibility demonstrated by an example with Bregman balls that no worst case distribution exists for any .

2 Preliminaries

2.1 General framework

Let be any set equipped with a (finite or -finite) measure on a -algebra not mentioned in the sequel. Probability measures will be represented by their densities . The notation will be used also for nonnegative (measurable) functions on which are not densities, i.e., do not have integral . Equality of functions on will be meant in the -almost everywhere (-a.e.) sense.

Let be a convex integral functional defined on the vector space of measurable functions333This functional will be considered only for nonnegative functions , with no loss of generality since -a.e.) is a necessary condition for , see (5). on by

| (4) |

Here is a function of , measurable in for each , strictly convex and differentiable444Strict convexity appears essential for our main results. Differentiability is assumed for convenience, it could be dispensed with as in [8]. in on for each , and satisfying

| (5) |

Then is a convex normal integrand in the sense of Rockafellar and Wets [14], which ensures the measurability of in (4) and of similar functions later on.

Let be any measurable function interpreted as payoff function, and a default distribution on with , , such that the expectation

exists. Let and denote the -ess inf and -ess sup of , and adopt as standing assumptions

| (6) | |||||

| (7) |

Due to strict convexity of , the inequality in (7) is strict if .

Example 1.

Take , thus , and let be an autonomous convex integrand, with to ensure (7). Then in (4) for is the -divergence , introduced in Csiszár [6]. If is cofinite, i.e. if , then is a necessary condition for , hence in that case in (3) equals the -divergence ball . If is not cofinite, -divergence may be finite also in absence of absolute continuity. Still, with some abuse of terminology, the set in (3) will be called -divergence ball also in that case.

Example 2.

Let be any strictly convex and differentiable function on , and for let where

| (8) |

Here and are defined as limits; if , we set for and otherwise.

In this example is arbitrary, except that in case we assume that -a.e.. Then equals the Bregman distance [3]

| (9) |

and is a Bregman ball of radius around . Note that here the assumption is not needed to guarantee (7), but may be adopted anyhow for the function is not affected by adding a constant to .

In the special case both examples give the -divergence ball where

As another special case, the choice gives and which is the squared -distance between and .

For of the form (3) the infimum in (1) equals

| (10) |

and for , , the infimum in (2) equals

| (11) |

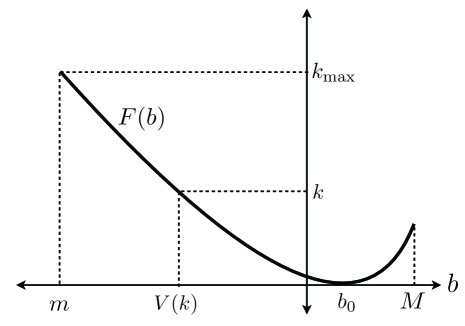

The next lemma relates the solution of problem (10) to that of the following minimisation problem, see Fig. 1:

| (12) |

is a convex function with minimum attained at . A standing assumption will be, in addition to (6),(7), that

| (13) |

This is a necessary condition for the functional to yield a nontrivial measure of risk for the payoff function , since would imply for each . Note that if then (subject to (13)), while if is finite then where the strict inequality is possible.

Lemma 1.

Remark 1.

The assumption on is not restrictive, for if or then trivially equals or .

2.2 Basic concepts and facts

Lemma 1 admits to treat Problem (10) using known results about minimising convex integral functionals under moment constraints, specifically with moment mapping defined by . We will rely upon results in Csiszár and Matúš [8]555Many of these results have been known earlier, though typically under less general conditions., specified for this moment mapping. Then the value function in [8] becomes

| (14) |

thus .

The function in (14) is convex, and its effective domain has interior

| (15) |

by [8, Lemma 6.6]. The function is proper (not identically and never equal to ) because it equals zero at , see (6), (7). Hence its convex conjugate is a closed (i.e., lower semicontinuous) proper convex function. A crucial fact is the instance of [8, Theorem 1.1] that

| (16) |

where is the convex conjugate of ,

| (17) |

The conjugate and derivatives of are by the second variable.

Below, derivatives at and are interpreted as limits of derivatives at and . For fixed the function equals for , it is strictly convex in the interval , and equals if is finite and . This function is differentiable in the interval . Its dervative is positive and strictly increasing in , and approaches or as or .

Since implies , and (equal to the closure of ) may differ from only on the boundary of ,

| (18) |

except possibly for equal to or , see (15). This can be rewritten as

| (19) |

where

| (20) |

The function will play a similar role as the logarithmic moment generating function does when in (3) is an -divergence ball, see Example 3. A consequence of (19) applied to : is the simple bound

| (21) |

The following family of non-negative functions on will play a key role like exponential families do for -divergence minimisation:

| (22) |

where

| (23) |

Remark 3.

It may happen that different parameters give rise to equal functions (22), but only in case of functions that equal zero except for in a set where is constant -a.e. This follows because for any fixed , the fact that is strictly increasing for implies that in (22), if positive, uniquely determines . In particular, for positive valued functions (22) the parameters are always unique, due to the standing assumption (6).

As implies for each , the sets and have the same projection to the -axis. This projection will be denoted by . It is a (finite or infinite) interval. The standing assumptions (6), (7) imply that contains the origin, and the default density belongs to the family (22) with , see [5, Remark 4]. The left endpoint of the interval will be denoted by . By [5, Theorem 2], the standing assumption is equivalent to

| (24) |

By [8, Lemma 3.6], the directional derivatives of the function in (16) can be expressed, at any and for any , as

| (25) |

where the integral is well-defined and is not equal to . In particular, is differentiable in the interior of its effective domain, with

| (26) | |||||

| (27) |

The same equations hold at on the boundary of for those one-sided partial derivatives of which are defined there, thus (26) holds for the left partial derivative at each .

The following lemma gives relevant information about evaluating the function in (20). Its proof is effectively contained in the proof of [5, Proposition 2], but for convenience a full proof will be given in the Appendix. Clearly,

Lemma 2.

Given any , either (i) some satisfies , , or (ii) is finite, , . In either case, in (20) the minimum is attained, and the unique minimiser is respectively .

2.3 Generalised Pythagorean identity

Given the convex integrand , define as in (8), with the convex function playing the role of . The mapping is a normal integrand [8, Lemma 2.10], hence if and are non-negative measurable functions on then so is also , denoted briefly by . Extending the concept of Bregman distance (9), define

| (28) |

Like its special case in (9), it is non-negative and equals only if . If , as in Example 2, then is equal to the of (9).

The following lemma, crucial for this paper, is an instance of [8, Lemma 4.15], combined with [8, Remark 4.13]

Lemma 3.

For each density with finite, and each ,

| (29) |

If is a density, the special case of (3) (or direct calculation) gives that

| (30) |

| (31) |

for each density satisfying

| (32) |

Identities like (31) frequently occur in the literature, primarily in cases when the last term vanishes (it trivially does if ). They are referred to as Pythagorean identities,666If then and (31) reduces to the classical Pythagorean identity provided that (32) holds for with and (3) will be called generalised Pythagorean identity.

The above results admit a short proof of the following key lemma, see [5, Theorem 1] for a related result.

Lemma 4.

(i) Let , . Then is finite if and only if is. In that case the density uniquely777Uniqueness is meant for the function, in the -a.e. sense. See Remark 3. attains the minimum in the definition (12) of for , and

| (33) |

Supposing , here is less or larger than according as is negative or positive.

(ii) For , a density attains the minimum in the definition (10) of if and only if for some with and

| (34) |

Proof.

The first assertion holds by (30), and the second one since (31), (32) imply for each density with . Then (33) follows by (30) and the consequence of Lemma 2. Finally, (21) and (33) yield , proving the last assertion of part (i).

(ii) For sufficiency, it is enough to verify the equivalence (34), under the given hypotheses. The function is the inverse of , see Lemma 1 and Remark 2. This and the result of part (i) imply (34), because if then (the upper bound follows from , due to the last assertion of part (i)). Regarding necessity, a density that attains the minimum in (10) clearly satisfies the constraint with the equality. We skip the proof of the remaining assertion that has to be of form with , for this will be an immediate consequence of Theorem 2. ∎

3 New results

3.1 Calculating V(k)

A procedure to calculate in (10) is to first determine the function in (16), then the function via (18) (this may be done in two steps, first determining the function in (20)), and finally as the solution of the equation , see Lemma 1. In regular cases, is characterised by equations involving partial derivatives of the function , see [5, Corollary 1], which may facilitate its computation. The following Theorem, combined with Lemma 2, may help to reduce computational complexity even in “irregular”cases. Previously, Ahmadi-Javid [1, Theorem 5.1] proved an identity equivalent to (35) for autonomous integrands and bounded payoff functions.

A lemma is sent forward that will be proved in the Appendix.

Lemma 5.

.

Note that while immediately follows from (19), it appears nontrivial that the function is closed.

Theorem 1.

Proof.

The conditions , are equivalent to , , see Lemma 1 and Remark 2. The condition that is a maximiser of means, by (19), that

| (36) |

or equivalently, see Lemma 5, that . This proves that is a maximiser of if and only if888Here and denote one-sided derivatives; the differentiability of the function is not addressed. . In particular, a (perhaps non-unique) maximiser does exist.

The calculation of in (11) is somewhat less costly than that of . It requires the calculation of only for a single value of , since for we have (using Lemma 5 in the final step)

| (38) |

Remark 4.

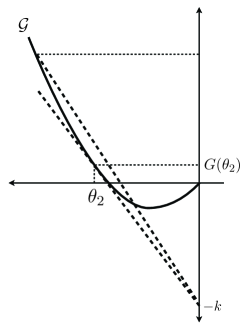

The following geometric interpretation of the proof of Theorem 1 deserves emphasis, see Fig. 2. Denote by

| (39) |

the graph of restricted to nonpositive arguments. Recall that, by Lemma 5, is a closed convex function with . Then (37) is the slope of the straight line through and , which is maximised by the supporting line to through . The proof of Theorem 1 shows that this supporting line (exists and) has slope . The maximum of (37) is attained if and only if is on this supporting line.

3.2 Almost worst case distributions

For the problem (10), call a density an --Almost-Worst-Case-Density (AWCD), where , if

| (40) |

Thus, an --AWCD is a density which does not violate the constraint by more than and for which the expected payoff does not exceed by more than the worst possible one subject to the constraint. A worst case density (WCD) is a --AWCD.

An - almost worst case distribution or a worst case distribution is a distribution whose density is an --AWCD or a WCD.

Theorem 2 below establishes a clustering property of the --AWCDs, as well as a similar result for densities that almost attain the minimum in (11). From a practical point of view, this may be relevant for efficient hedging against the almost worst scenarios, but this issue is not entered here.

Let us assign to each the unique attaining the minimum in the definition (20) of , determined in Lemma 2, and denote

| (41) |

Given , we will denote by the function with attaining the second maximum in Theorem 1, i.e.,

| (42) |

Theorem 2.

(i) For , each --AWCD belongs to the

Bregman neighborhood of

radius of in (42), i.e.,

see (28),

| (43) |

(ii) For with , set . Then for each density

| (44) |

Corollary 1.

Let be a sequence of --AWCDs with in case (i), or a sequence of densities with in case (ii). Then converges to respectively to locally in measure.999This means that for each with finite, and any . If is a finite measure, this is equivalent to standard (global) convergence in measure. In particular, the function is unique.

Proof.

(i) By the generalised Pythagorean identity Lemma 3, applied to in (42),

| (45) |

for each density . As attains the maximum in Theorem 1, here and . Hence, (3.2) implies (43) for each density which is an --AWCD, thus satisfies (40).

(ii) In this case, (3.2) holds as before. Multiplying it by and using that , see (3.1), we obtain (44).

The Corollary follows since implies convergence of to locally in measure [8, Corollary 2.14]. ∎

Remark 5.

The function in Theorem 2(i) will be called worst case localiser, for the almost worst case densities are clustering in its (Bregman) neighborhood. This nice intuitive interpretation of the function is complemented by the additional intuitive fact that, by (43), its parameter controls the radius of that neighborhood. Most appealing is the special case of (43) that all densities that satisfy and yield expected payoff not excceding the worst case by more than , are contained in a Bregman neighborhood of of radius proportional to , with proportionality factor . The essence of the Corollary is that the Bregman distance of from goes to . For certain choices of the integrand this implies convergence even in a stronger sense than locally in measure, see Example 3.

Clearly, the worst case localiser coincides with the WCD whenever the latter exists (apply (43) to ). A necessary and sufficient condition for the existence of a WCD is given in Lemma 4(ii). There, we have skipped the proof that a WCD has to be of form with , which is obvious now as the WCD is a worst case localiser. Lemma 6 below will also be useful in identifying situations when the worst case localiser is actually a WCD. Its Corollary addresses the simplest such situation. When in (10) the minimum is not attained, the worst case localiser may or may not be a density, see the examples below, though it always satisfies , see Theorem 1. Note that the computation of the worst case localiser is not harder than the computation of along the lines of Subsection 3.1, for that calculation does provide the parameters of that attain the double maximum in Theorem 1.

Lemma 6.

A function in (22) with is the worst case localiser for if and only if the vector belongs to the normal cone of at , i.e., for each

| (46) |

Corollary 2.

If the worst case localiser has parameters in the interior of , then it is a WCD.

Proof.

By Theorem 1, the condition in the definition (42) is equivalent to the condition that attains the maximum of where . The latter is satisfied if and only if for each , the concave function

is maximised by , i.e., its (right) derivative at is nonpositive. On account of (2.2), that condition is equivalent to (46). The Corollary follows since the normal cone of at an interior point consists of alone. Thus Lemma 6 gives the conditions , which mean by Lemma 4 that is a WCD. ∎

Example 3.

Let be the -divergence, formally (see Example 1) let be the autonomous integrand given by and let . Then , , and

for . The minimum in the definition of is attained for . If and on a set of -measure then101010Note that Theorems 1, 2 do not apply to . Here, in that case the WCD equals on the set and elsewhere. It does not belong to the family (22), and the almost worst case densities do not cluster in its Bregman neighborhood. , otherwise (assuming (24)).

For , Theorem 1 gives and Theorem 2 gives the worst case localiser , with attaining the above maximum. This worst case localiser is always a density. It also satisfies and hence is actually a WCD, except for the case when contains its left endpoint , is finite, and . In that case the maximiser in Theorem 1, equal to the parameter of the worst case localiser, is . Note that for this example, the formula for appears in [1] and [5] show that in the above exceptional case the minimum in (10) is not attained. The result of Theorem 2 appears new even for this special case.

In this example, the Bregman distance (28) of densities coincides with -divergence, hence Theorem 2 gives for each --AWCD . In the Corollary of Theorem 2, now the almost worst case densities converge to the worst case localiser in a much stronger sense than in measure. Indeed, the result that their -divergence from the worst case localiser approaches is stronger than convergence to the worst case localiser.

Example 4.

Again in the setting of Example 1, take now . Then equals reverse -divergence, i.e., the -divergence of the default distribution from the distribution with density . As is not cofinite, the standing assumption holds if and only if .

Take specifically , and take for the distribution with Lebesgue density . As , then and for . Simple calculus shows that for the minimum in the definition of is attained for such that is a density, but the functions and can not be given explicitly. If then this minimum is attained for , and . One sees that ranges from to as ranges from to . Hence in case the WCD exists, it equals that which is a density and satisfies . In case the worst case localiser is with attaining . By simple calculus, this maximiser is , the maximum is , and the worst case localiser is , which is not a density unless .

Example 5.

Let be as in Example 4, but this time let the default distribution be the uniform distribution whose -density is . Take for the Bregman distance in Example 4, i.e., the integral functional (4) with . Then , , . The set (equal to ) of this example consists of those for which belongs to the set of Example 4. Moreover, for such the function coincides with the function of Example 4, which can not be a density if . This proves that in the present Example no WCD exists for any .

3.3 Effect of the threshold on the existence of a WCD

This subsection addresses the effect of the choice of the threshold on the worst case localiser, in particular on whether that localiser is also a WCD.

Examples 3, 4, and 5 demonstrate that a WCD may exist for all or for no , or there may exist a critical value such that a WCD exists if but does not exist if . It appears a plausible conjecture that these three alternatives are exhaustive, i.e., that if a WCD exists for some , it also exists for each . While this conjecture remains open in general, it will be proved under conditions that cover many typical cases.

Recall that with denotes the left endpoint of the interval , the projection of to the axis. The condition is necessary for and sufficient for .

Theorem 3.

(i) If for some the worst case localiser is a density, it is a WCD for unless111111Here means the right derivative.

| (47) |

and

| (48) |

Proof.

(i) Suppose in (42) is a density. By Lemma 4 it is a WCD for if and only if

| (49) |

Since is a worst case localiser and , Lemma 6 gives that

| (50) |

This immediately implies (49) if , or equivalently (see Remark 4) if the supporting line through to the curve does not contain . This is always the case if (47) does not hold, and also when (47) holds but , the largest slope of supporting lines to at , is less than . As the last condition is equivalent to , only the case remains to cover to complete the proof that is a WCD unless (47) and (48) hold.

In that remaining case, with , and instead of (49) only the inequality follows from (50). Suppose indirectly that it is strict, then Lemma 1 implies that for some (as the integral is less than by Lemma 4). This means by Lemma 4 that (with ) is a WCD for . Hence, by Remark 4, the supporting line through to the curve contains , contradicting the fact that among the supporting lines to at the one through has the largest slope. This contradiction proves that (49) holds and hence is a WCD also when .

The last assertions of part (i) are obvious. Indeed, if (47) holds and then the supporting line through to meets the curve at , just as the supporting line through does, hence . As it is a WCD for , it can not be a WCD for with .

(ii) The hypothesis implies that a vector in can belong to the normal cone of at some only if the first component of this vector is . On account of Lemma 6, this proves that the worst case localiser , for any , has to satisfy . ∎

Corollary 3.

The function is differentiable at each for which in (41) is a density.

Proof.

Finally, we discuss for -divergence balls, see Example 1, the dependence on the threshold (the “radius” of the ball) of the worst case localiser and whether it is a WCD. Formally, let be an autonomous integrand, strictly convex and differentiable on , , , let be a probability measure, and .

The case of cofinite is covered by Theorem 3(ii), the integral in its hypothesis being equal to , finite for each . Therefore we focus on the non-cofinite case, supposing

| (51) |

Then the standing assumption (equivalent to ) holds if and only if . With no loss of generality, assume that (clearly, the minimisation problem (10) is not affected by adding a constant to ).

Under the above assumptions, with is finite if and infinite if , because (51) implies that is finite for but not for . It follows for any that the associated in Lemma 2 is equal to , hence Lemma 2 gives that the function in (41) is a density if and only if

| (52) |

Moreover, if then

| (53) |

Theorem 4.

Under the assumptions (51) and , if for each then the WCD exists for all . Otherwise, denote

| (54) |

| (55) |

Then , , and for the WCD exists. For the worst case localiser is of form (53); it is not a density if , while for it is a density (and hence a WCD) unless121212It is left open whether that exceptional case is possible. for each with .

Proof.

Since in the current case , Theorem 3 implies that the worst case localiser is a WCD if and only if it is a density. By the passage preceding the Theorem, the latter holds if and only if with satisfying (52). This immediately proves the first assertion.

Suppose next that is finite for some , and denote the supremum of such parameters by . One verifies via monotone convergence and dominated convergence that is a continuous, strictly increasing function of that approaches or as goes to or . Hence if then is equal to the unique with , whereas if then . In both cases , using that .

By the definition (55) of , the supporting line to at of slope intersects the vertical axis at . Hence , unless the function is linear in the interval ; the latter possibilty will be ruled out in the Appendix. It follows, too, that the supporting line to through with or meets the curve at a point (or points) with argument respectively . Moreover, the latter inequality is strict if (equivalent to ), for in that case is differentiable at due to Corollary 3.

Referring to Remark 4, the above considerations prove that the parameter in the representation in (42) satisfies or does not satisfy the condition (52) if respectively , no matter whether or not. These facts, and that if , imply all remaining assertions of the Theorem, see the first passage of the proof. ∎

Appendix

Proof of Lemma 2

Proof.

Fix , define as in the lemma. Then for all , and the function is convex, closed, and differentiable in its effective domain , with

| (56) |

see (26). If then (56) holds also for the left derivative at . Hence the last assertion of the Lemma immediately follows.

To prove that one of the alternatives (i) and (ii) indeed takes place, note that the properties of stated in the passage after (17) imply, by monotone convergence, that in (56) goes to if and to if and . Hence, due to continuity of , alternative (i) fails only if

| (57) |

and (57) can hold only if . Further, (57) implies that , for in the opposite case the derivative (56) of the closed convex function would go to as .

Proof of Lemma 5

Proof.

Fix and consider the (not necessarily proper) convex function

Then

where the third equality holds since , and the fourth one holds since is in the interior of . Here

Recalling the definition (20) of , this completes the proof. ∎

Completion of the proof of Theorem 4

It remains to rule out the possibility that the function is linear in the interval . Suppose indirectly that for some

| (58) |

Here necessarily , by (21). As (58) implies , which means by (19) that , it follows by Remark 2 that actually .

As by the proof of Theorem 4, the value in (41) attaining for is equal to . Thus Lemma 3 applied to and gives

Here the integral equals by definition, and in (58) has been shown to equal . Hence it follows that , which means that equals (-a.e.). By Remark 3, this contradicts , proving that the indirect assumption (58) is false.

References

- [1] Amir Ahmadi-Javid. Entropic Value at Risk: a new coherent risk measure. Journal of Optimizaton Theory and Applications, 155(3):1105–1123, 2011.

- [2] Aharanov Ben-Tal and Marc Teboulle. An old-new concept of convex risk measures: The optimized certainty equivalent. Mathematical Finance, 17:449–476, 2007.

- [3] Lev M. Bregman. The relaxation method of finding the common point of convex sets and its application to the solution of problems in convex programming. USSR Computational Mathematics and Mathematical Physics, 7:200–217, 1967.

- [4] Thomas Breuer and Imre Csiszár. Information geometry in mathematical finance: Model risk, worst and almost worst scenarios. In IEEE International Symposium on Information Theory Proceedings (ISIT), pages 404–408, 2013.

- [5] Thomas Breuer and Imre Csiszár. Measuring distribution model risk. Mathematical Finance, 2013. DOI: 10.1111/mafi.12050.

- [6] Imre Csiszár. Eine informationstheoretische Ungleichung und ihre Anwendung auf den Beweis der Ergodizität von Markoffschen Ketten. Publications of the Mathematical Institute of the Hungarian Academy of Sciences, 8:85–108, 1963.

- [7] Imre Csiszár. Why least squares and maximum entropy? An axiomatic approach to inference for linear inverse problems. Annals of Statistics, 19(4):2032–2066, 1991.

- [8] Imre Csiszár and František Matúš. On minimization of entropy functionals under moment constraints. Kybernetika, 48:637–689, 2012.

- [9] Hans Föllmer and Alexander Schied. Stochastic Finance: An Introduction in Discrete Time, volume 27 of de Gruyter Studies in Mathematics. Walter de Gruyter, 2nd edition, 2004.

- [10] Itzhak Gilboa. Theory of Decision under Uncertainty, volume 45 of Econometric Society Monographs. Cambridge University Press, 2009.

- [11] Lars Peter Hansen and Thomas Sargent. Robust control and model uncertainty. American Economic Review, 91:60–66, 2001.

- [12] Lars Peter Hansen and Thomas Sargent. Robustness. Princeton University Press, 2008.

- [13] Fabio Maccheroni, Massimo Marinacci, and Aldo Rustichini. Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74:1447–1498, 2006.

- [14] Ralph Tyrell Rockafellar and Roger J-B. Wets. Variational Analysis, volume 317 of Grundlehren der Mathematischen Wissenschaften. Springer, 1997.

- [15] Tomasz Strzalecki. Axiomatic foundations of multiplier preferences. Econometrica, 79:47–73, 2011.