Weak Convergence of Path-Dependent SDEs in Basket CDS Pricing with Contagion Risk

Abstract

We investigate the computational aspects of the basket CDS pricing with counterparty risk under a credit contagion model of multinames. This model enables us to capture the systematic volatility increases in the market triggered by a particular bankruptcy. The drawback of this problem is its analytical complication due to its path-dependent functional, which bears a potential failure in its convergence of numerical approximation under standing assumptions. In this paper we find sufficient conditions for the desired convergence of the functionals associated with a class of path-dependent stochastic differential equations. The main ingredient is to identify the weak convergence of the approximated solution to the underlying path-dependent stochastic differential equation.

Keywords. Path-dependent SDE, weak convergence, correlated first-passage times, basket CDS, contagion risk, counterparty risk.

JEL Classification. C02, G12.

Mathematics Subject Classification (2010). 60F05, 60H30, 60J60, 91G40.

1 Introduction

It is well known that the first-passage time of a drifting Brownian motion crossing a deterministic level is an inverse Gaussian random variable, as its running maximal process of a drifting Brownian motion can be characterized with the reflection principle and Girsanov theorem. This result has been applied, among others, in studying the default time of a firm with a structural framework in which a firm defaults at the first time when its asset value falls below its liability value. The structural model is acclaimed to have strong economic foundation and is one of the most popular models used in pricing single-name credit derivatives.

It is natural to ask whether one can also characterize the joint distribution of first-passage times of correlated drifting Brownian motions crossing some deterministic levels. When there are two correlated Brownian motions, [10, 18] find the joint distribution of first-passage times, which is an infinite sum of modified Bessel functions of the first kind. Little is known for first-passage times of three or more correlated Brownian motions. This limitation makes it difficult to study the default times of multiple names with a first-passage time structural model and is one of the reasons that intensity-based reduced-form models are used in pricing portfolio credit derivatives. After all, intensity models give more analytic tractability but do not provide economic reasons why firms default (see [5, 26] for some recent results in this direction and the references therein).

In this paper we discuss the pricing of a basket CDS with counterparty (CDS writer) risk. The default times of names in a reference portfolio and that of the counterparty are modeled by a first-passage time structural model and correlated Brownian motions. Furthermore, we include contagion risk in the model, in which the default of a name in the reference portfolio causes a jump increase of volatility of the counterparty, which increases the default probability of the counterparty. The aforementioned model, for instance [6], incorporates both counterparty risk and contagion risk, whereby it can realistically explain the severe difficulties experienced by some seemingly default-remote banks underwriting super senior tranche CDOs (collateralized debt obligations) during the financial crisis of 2007-08.

Since the joint distribution of correlated default times in a structural model is unknown, we compute the price of a basket CDS by the Euler scheme for SDEs and the Monte Carlo simulation. As an effective computational tool, Euler scheme has been widely adopted in the credit risk computing for its simplicity and robustness. Is it possible that a price computed from these “robust” algorithms could be actually over-valued in the trillions dollar market?

As we will illustrate in Example 9, the answer is affirmative in general. Then, is there a set of broad conditions, which ensures the computation going to the correct value? In this paper, we aim to reveal the reasons for the possible mispricing, and further to provide a rigorous justification on the mispricing scenarios. To illustrate the idea, we take a simplified example which indeed motivates our general setting in Section 2.

Example 1

Let be the firm value process of the CDS writer, and those of basket reference names. We assume that the default time of the firm is given by , Moreover, we assume the volatility of firm follows , where

| (1) |

is the total default number of reference names by time . The main interest of this this paper is to compute a premium rate per annum in the form of

| (2) |

for some discontinuous functions and with domain , see also the exact formula (4).

Given that Euler scheme with step size in the approximation of the underlying firm values and further their default times , denoted by and respectively, one can approximate premium rate by replacing by in the formula (2), denoted by . Our question is that whether the convergence holds as ?

Regarding the numerical schemes of SDEs, there have been extensive research on the topics of both weak and strong convergences, see [7, 8, 12, 16, 24] and the references therein for excellent expositions. In particular, the book [12] introduces a systematic and rigorous treatment to the numerical approximation of the various types of SDEs. To the best of our knowledge, essentially all the above literatures on numerical SDEs study the convergence at fixed grid-points in Markovian settings. Back to Example 1, the volatility is path-dependent and the presence of first-passage times requires information on the whole path.

In this regard, we turn our attention to study associated mappings from Skorohod path space to real numbers. For instance, the first passage time can be rewritten by where is a mapping defined by . Similar idea can be applied to rewrite the premium rate by , where each is a functional on -valued path space with its argument . To this end, our work can be clearly divided into two steps: The convergence shall be true by the continuous mapping theorem, if

-

(Q1)

converges to in distribution (see Section 2.3.3) , denoted by ;

-

(Q2)

and are continuous almost surely at with respect to Skorohod topology.

Regarding (Q1), the weak limit theorems for the whole path in non-Markovian setting can be found in [13], and our approach for the weak convergence is also closely related to [13]. However, [13] establishes the convergence based on the continuity assumption of coefficient functions, while the volatility of Example 1 is not continuous as a mapping on a path space, and hence their result can not be directly applied here. The main reason for the discontinuity is due to the dependence on the number of defaults , see also the tangency problem of [14]. Nonetheless, as a function on a path space is almost surely continuous with respect to the probability induced by , see Example 10 for details. As such, we bravely attempt to show the desired weak convergence under almost sure continuity assumption of coefficient functions, i.e.

-

(H)

As a mapping from path space to , the function is continuous under Skorohod topology almost surely with respect to .

In the above, refers to the probability measure on induced by , see more explanation in Section 2.3.3. Although (H) is enough for our purpose to cover our motivated example, it is still inappropriate since the unknown solution shall not be included in the assumption. This leads to Assumption 4, which serves the same role as (H) with the help of Assumption 3.

To this end, it is inevitable to go through the entire procedure and carefully reexamine all the necessary steps in the weak convergence. Firstly, we show the tightness of the discrete Euler processes, and deduce the convergence of approximating processes to a limiting process almost surely by the Skorohod representation theorem. Secondly, we claim the continuity of the limiting process, which plays a crucial role in the proof, see Remark 13. Finally, we complete the proof by showing that the limiting process is the weak solution of the underlying SDE.

Regarding (Q2), provided the completion of (Q1), we shall show the convergence in distribution of (2). Although the form of corresponding to the pricing formula (4) is complicated, it’s enough to examine the weak convergence on the following two simple quantities by the continuous mapping theorem (CMT):

-

1.

(The convergence in single name risk) One shall verify for arbitrary and . Applying CMT, it’s sufficient to show for any , i.e. all underlying firms has zero probability to get into default at a particular time. This is guaranteed by non-degeneracy Assumption 3.

-

2.

(The convergence in counter-party risk) One shall verify for each . Again by CMT, it’s enough to show , i.e. there shall be zero probability that two companies default simultaneously. It boils down two sufficient conditions in turn: if either (a) CDS writer is independent to all reference names; or (b) CDS writer is not perfectly correlated to all reference names and the volatilities are all piecewise constants, then the above convergence holds.

To close up the introduction, our contribution is summarized as follows. We establish the convergence for the approximation of CDS pricing, see Theorem 7. As illustrated above, the major mathematical difficulty compared to the existing literature stems from the following added features in our model: (a) the contagion risk due to the dependence of the volatility in total number of defaults; (b) single/counter-party default risk in terms of first-passage times. As of any other weak limit results on the path space, our result has to be established by many assumptions, for which we add careful explanations why they are needed, see Section 2.3. As a result, the seemingly cumbersome assumptions can be reduced to a simple condition in Example 1: If for all and is not perfectly correlated to any of , then holds.

The paper is organized as follows. Section 2 presents the problem setup and our main result, which is to cover rather general scenarios than Example 1. Note that some notions used in Introduction are also slightly extended in an obvious way. Section 3 includes the technical proof of the main result. Section 4 includes further discussions related to this work.

2 Main Results

2.1 Problem Setting

Let for some positive constant . Denote by the space of càdlàg functions, i.e. functions that are right continuous with left limits defined on taking values in . is abbreviated as . Let be a filtered probability space satisfying the usual conditions, on which a standard dimensional Brownian motion is defined. Here, is the transpose of . Suppose that and are nonanticipating in the sense that and for all and (see [13] for details). We consider companies with the firm value processes satisfying

| (3) |

where the constant is the firm value at , is a diagonal matrix with diagonal elements , and and represent asset appreciation and volatility rates, respectively. The product of and its transpose reflects the covariance between the movements in the asset values of firms, thus playing a critical role in determining the dependence structure among the firm values.

Let stand for and . We impose the following structure to : For any , can be decomposed into a continuous deterministic process and a pure jump process as follows:

where functions (respectively ) and are measurable and nonanticipating in the sense that and . The function is measurable for In the above, and represent the number of jumps of up to time and the jump size for the th jump, respectively. Moreover, the processes and are -adapted.

Without loss of generality, let be the firm value process of a CDS writer and , , be the firm value processes of the companies in the reference portfolio. Each company has an exponential default barrier in the form of

where and are nonnegative constants. The default time for company is defined by

the first time the firm value falls below the default barrier. We denote by the order statistics of , i.e. is the th default time among companies in the reference portfolio.

Note that the definition of the default time is truncated by , but not by the maturity only for its convenience. The advantage is that, our work is reduced to Càdlàg space from infinite time interval to a finite time interval, while we can keep the probability of as zero under non-degenerate condition. This feature will be used to show the weak convergence involved with , while preserve the structure of the swap rate defined in (4).

In pricing derivative securities with the structural model, it is normally assumed that the drift coefficient of in (3) is equal to the risk-free interest rate in a risk-neutral setting. We do not insist that equal to in this paper as the firm value is not a traded asset and cannot be hedged with the no-arbitrage and martingale representation argument. The firm value process is a measure that may have close relation with traded assets but is mainly used to define default events. All results still hold if is replaced by . For the sake of simplicity, the risk-free interest rate is assumed to be a positive constant . The extension to stochastic interest rate model can be done under the framework of this paper (see Remark 23 for details).

A basket CDS is an insurance product in which the underlying is a portfolio of defaultable companies and the writer (seller) of the th default CDS promises to pay to the buyer of the insurance at the th default time if that happens before the maturity time of the contract, in return the buyer of the th CDS agrees to pay the writer a premium fee at rate per annum on each of pre-specified dates as long as the th default has not occurred. (In fact, the triggering time for the basket CDS does not have to be the default time of a company, it can be any predefined event). If the writer defaults before the maturity of the contract or the th default time, then the CDS contract terminates and there are no further cash flows. The risk neutral swap rate is given by

| (4) |

where , , , and is the indicator function which equals 1 if an event occurs and 0 otherwise. The values of and are dependent on the realized path of the process . The evaluation of in (4) involves the expectations of path-dependent functionals, which may naturally be computed with the Monte Carlo and the Euler approximation method.

Let the time interval be partitioned into equally spaced subintervals with grid points , , , and let , valued in , be the Euler approximating process for , defined recursively by

where and . In the rest of the paper, for ease of the notation complexity without ambiguity, we retain the notation to denote the piecewise constant interpolation of sequences , i.e.

| (5) |

Random variables are -measurable, where is the information available at time . Since is a Brownian motion, without changing their distributions, we may generate by the recursive formula

| (6) |

where , , are independent dimensional standard normal variables and are independent of the filtration for and .

Corresponding to the Euler approximating process , the annual swap rate has the same form as that in (4) except , and are replaced by , and , respectively. In this paper we explore under what conditions we have

| (7) |

2.2 The Main Results

In this part, we present the main result after several assumptions.

Assumption 2

With some positive constant for all and , for

Assumption 3

satisfies the uniform nondegeneracy condition, i.e. for all and for some .

We next define as

| (8) |

which is the first time of the càdlàg function hitting the barrier . Let be the collection of continuous functions defined on taking values in . is abbreviated as . For , define two disjoint subsets of the space as

and

Assumption 4

The mappings and are continuous under Skorohod topology at the set .

Assumption 5

For all , , a.s. for .

Assumption 6

is piecewise constant almost surely, i.e. for strictly increasing stopping time sequence such that and , the process is in the following form

where is a nonsingular matrix, measurable with respect to ,

2.3 Discussions on Assumptions with its Application to Example 1

In this part, we discuss the above assumptions combined with Example 1 to illustrate the main result.

2.3.1 Discussion on Assumption 2

Assumption 2 is imposed to guarantee the existence and uniqueness of a solution to (3). As one shall further note from Assumption 2, and are all bounded by some constant . (In this paper, is a generic constant whose value may change at each line). We may relax the Holder- continuity of by a condition , where is a bounded function satisfying and tends to 0 as tends to 0.

2.3.2 Skorohod space

To discuss other assumptions, we shall first state the Skorohod metric for space and related notions, which are adopted by [1]. Define a uniform metric on by

| (9) |

Let denote the class of strictly increasing, continuous mappings of onto itself. Then the function space is equipped with the Skorohod topology with the metric

| (10) |

Since the convergence in Skorohod topology does not imply the convergence in uniform topology. However, if the limit is in then they are equivalent.

Proposition 8

([1, page 124]) Elements of converge to a limit in the Skorohod topology if and only if there exist functions in such that uniformly in and uniformly in . Moreover, if is in , then Skorohod convergence implies uniform convergence.

2.3.3 Convergence in distribution

The notion of the convergence in distribution (see [1]) or weak convergence (see [14]) may be defined in various ways in different literatures. Since it plays an important role in Theorem 7 and throughout the paper, we give a short remark for its clarification. The random elements of our interests and of Theorem 7 are the maps from a probability space to a Skorohod metric space equipped with Skorohod metric defined in (10), and often write it as

or in short if the context has no ambiguity on and . The distribution of the random element refers to , which is indeed the probability measure on the Borel -algebra , i.e.

is sometimes called as the law of , or the probability measure induced by , or the push forward measure. Similarly, is the distribution of .

We say, as , converges to in distribution with respect to Skorohod metric , if the measure weakly converges to , denoted by . It sometimes called converges to weakly with respect to Skorohod metric. By Portmanteau Theorem, one can equivalently define the convergence in distribution in any of five different ways provided by Page 26 of [1]. For instance, a common definition adopted in many references is that, is said to be convergent to in distribution with respect to Skorohod metric , if for all , the space of all bounded continuous (w.r.t. metric ) functions on .

One may already note that the convergence in distribution relies on the topology of . Indeed, under uniform topology induced by of (9) is a bigger space than induced by Skorohod metric of (10). This immediately yields by the definition that the convergence in distribution with respect to the uniform topology implies convergence in distribution with respect to Skorohod topology. In the rest of the paper, unless it is specified, the space is equipped with Skorohod metric by default, and convergence in distribution means by default the convergence in distribution with respect to Skorhod topology.

2.3.4 Discussion on Assumption 3

Recall the hitting time operator of (8). This notion enables us to treat the default time as a function on a random process, i.e. . However, one can not assume is continuous in in general from the following example.

Example 9

One can also adapt the above idea to illustrate the potential issue arising from the numerical computation of the credit risk model. Let’s assume that the firm value follows the deterministic curve , i.e. , and a tradable derivative price is given by , where . One can easily see that an approximation by usual Euler scheme does not guarantee the convergence . Obviously, it is not a realistic example due to its zero volatility. Then, can we avoid mispricing from the computation by assuming non-zero volatility of the firm value?

The nondegenerate condition Assumption 3 is very important throughout the paper. It not only implies any two of firms and are not perfectly correlated, but also makes the barriers regular to the underlying diffusion. As an immediate consequence, we have continuous -almost surely for all ’s.

Another use of Assumption 3 is on the total number of defaults in Example 1. One can rewrite this in terms of by

| (11) |

for some mapping defined on . Example 9 implies that the functional above is not continuous with respect to Skorohod topology, and hence it violates the sufficient condition for the weak convergence given in Condition C5.1 of [13]. However, Example 10 below can verify the almost sure continuity under Assumption 3, which is enough for our purpose.

Example 10

The number of defaults defined in Example 1 can be rewritten by (11). Example 9 implies that is not continuous in general. However, under Assumption 3, is continuous under Skorohod topology almost surely with respect to . Indeed, this follows from the following two facts:

-

1.

By Blumenthal 0-1 law (see [3]), is continuous with respect to Skorohod metric almost surely in for all , i.e.

-

2.

Moreover, is also continuous with respect to Skorohod metric almost surely in , the probability induced by .

2.3.5 Discussion on Assumption 4

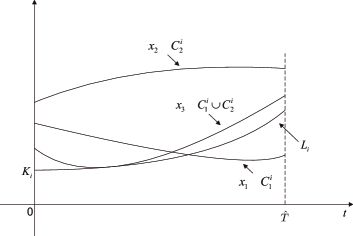

Condition C5.1 in [13] requires the mapping is continuous under Skorohod topology in , while our volatility violates this condition as of Example 10. In contrast, Assumption 4 may be regarded as a continuity requirement of coefficient functions on a smaller space Figure 2 provides some examples to illustrate the concept of and . The paths in the union set of and are regular with respect to the boundary in the sense that once the path touches the boundary the path pushes through the boundary. Continued from Example 10, due to the fact under Assumption 3, also satisfies Assumption 4. We refer Section 2.2 of [23] for more detailed descriptions.

2.3.6 Discussion on Assumption 5 or 6

Assumption 5 or 6, together with Assumption 3 is to ensure the indicator function is continuous -almost surely. Suppose the CDS writer is default free before maturity , then the indicator function is a constant one a.s. . For such a case, Assumption 5 or 6 is not required in Theorem 7. From the financial perspective, Assumption 5 implies that CDS writer and the reference names are independent of each other from exogenous factors ( and are independent). This is realistic in practice since an important criteria adopted by practitioners for choosing an appropriate CDS writer is that the CDS writer has little correlation with the reference names. On the other hand, if the CDS writer has non-zero correlation with reference names (but not perfectly correlated due to Assumption 3, then one can still have almost sure continuity of by requiring the piecewise constant form of , which is indeed the case in reality. Note that the volatility is calibrated in practice form time to time, not continuously.

2.4 Other Operators Related to the CDS Pricing Formula

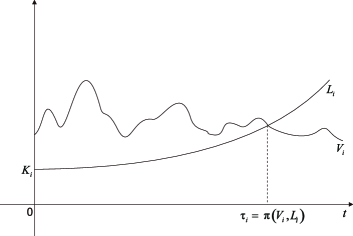

For the later use, we also introduce other related notions here. For any , define as

Finally, define , , as

and

With the help of mappings , and , , the default time of company , the th default time of the reference portfolio, and the swap rates and can be expressed respectively as follows:

The default time for company is illustrated in Figure 3.

3 Proof of Theorem 7

In this section we prove Theorem 7 through a number of lemmas.

3.1 Preliminary Estimates

We discuss some properties of here, which plays a crucial role in the subsequent parts. Let . The Euler scheme can be rewritten in terms of interpolated process in the following way:

For convenience, we also denote and

Lemma 11

If Assumption 2 holds, then satisfies, for and ,

| (12) |

| (13) |

| (14) |

where is the largest integer not greater than .

Proof: For any , and , using Burkholder inequality and Assumption 2 we estimate th moment of as follows:

From above inequality and Gronwall’s inequality, we have

| (15) |

For the case of , (15) still holds by noting when . For any , we have

Since the integral of the second term is a martingale, applying (15), Assumption 2, Burkholder’s inequality and Holder inequality gives us

| (16) | ||||

Setting and , we obtain

A review of the proof shows that the inequality (16) still holds when the expectation is replaced by the conditional expectation. Hence we have (14).

Lemma 12

If Assumption 2 holds, then as , where for .

Proof: Since boundedness of and implies that

we have

where in above inequality the first and second term are denoted by Ih and IIh, respectively.

The convergence of to zero as can be obtained from

The last inequality in the above is due to (12). On the other hand,

The conclusion follows from that converges to 0 in as .

Remark 13

Lemma 12 is the key result that enables us to show that the weak limit process of is continuous. Skorohod representation theorem allows us to treat the limit in almost sure sense, that is

| (17) |

However, it does not imply almost sure limit with uniform topology, i.e.

| (18) |

may not be true. In other words, (17) does not imply

even for a bounded continuous function , which is useful in characterizing properties of . Indeed, one shall prove continuity of (i.e. ) in advance to make use of (18) from Proposition 8. We note that the proof on the continuity of is missing in [22] and the related references therein.

3.2 Weak Convergence of Approximating Solutions

This part shows that the approximating processes converge to in distribution. A general approach to this goal is first to prove tightness of for extracting a weak limit from any subsequence, then to apply the Skorohod representation theorem for passing the limit almost surely, and finally to characterize the limiting process as the solution of the underlying SDE, provided there exists a unique weak solution. The main result of this subsection is Theorem 17.

Proof: For the sake of simple presentation, we assume no jump for . Taking logarithm, it is sufficient to consider the following SDE:

| (19) |

By definition, can be constructed uniquely by the following steps:

-

1.

Let for .

-

2.

Let .

-

3.

Let for , otherwise,

for .

-

4.

Let .

-

5.

Repeat above steps to construct , , until .

According to [25, Theorem 1.6.3], has a unique strong solution from 0 to , hence is well defined. Since is no greater than , has a unique solution from 0 to . [25, Theorem 1.6.3] also implies that , so has a unique strong solution from to with initial value at time . Therefore, has a unique strong solution from 0 to . Since the number of jumps of is finite due to Assumption 2, we can proceed the above procedure inductively until , where is some finite number. Then is the unique strong solution of (19) from 0 to . Hence, the uniqueness of weak solution is ensured according to [20, Theorem 9.1.7].

Lemma 15

If Assumption 2 holds, then is tight.

Proof: According to [4, Theorem 3.8.6] it is sufficient to verify condition a) in [4, Theorem 3.7.2] and condition b) in [4, Theorem 3.8.6] in order to show is tight. To verify condition a) in [4, Theorem 3.7.2] we need to verify that for every and rational , there exists a compact set such that

where . It is worth noting that . Denote by the bound of from (12). For every and , by setting and , we have

To verify condition b) in [4, Theorem 3.8.6], we need to find some positive and a family of nonnegative random variables satisfying

| (20) |

for , , and ; in addition,

| (21) |

and

| (22) |

We claim that and a family of nonnegative random variables satisfy (20), (21) and (22). For (20), since either or is zero when due to piecewise constant form of , we then have

(21) follows from (12) and Cauchy Schwartz inequality that

(22) is shown as follows

So, is tight.

The next result is needed in the proof of Theorem 17.

Lemma 16

(Rosenthal’s inequality, [21]) Let and be a sequence of independent random variables such that, for any and any , and . Then we have

where is some constant depending on .

We now state the main theorem of this subsection on weak convergence of the Euler scheme.

Theorem 17

Proof: Since is tight, hence for an arbitrary infinite sequence, there exists a sub-sequence that has a weak limit. We denote this sub-sequence again by , and its limit by . Due to the uniqueness of weak solution (see Proposition 14), it suffices to show that is the weak solution of (3). Tightness of implies is in . Moreover, since from Lemma 12, is a continuous process due to [1, Theorem 13.4]. Using Skorohod representation (see [14, Theorem 9.17]) we can find and in the same probability space such that their distributions are the same as those of and , respectively, and converges to almost surely. According to Remark 13 and Proposition 8, converges to a.s. under both Skorohod topology and uniform topology. Since is uniformly bounded from below by a positive constant due to Assumption 3, , is regular with respect to (see [23, Proposition A.1]). Hence a.s. for in Skorohod topology as by Assumption 4. Denote by the set . Since the number of discontinuities of is bounded almost surely, we can write as the finite union of disjoint intervals , . Since is Holder-1/2 continuous at each , is uniformly continuous at each . Therefore as ,

For denote by

Noting that is finitely many by Assumption 2 and , we have

Moreover, noting that and have the same law and is uniformly integrable due to (12), we have

which shows that

For the last term above, since is bounded and , we have

Denote by . Using the Euler recursive formula (6) and Assumption 2, we have

| (24) | ||||

which tends to 0 as from (12). Here we have used the fact that is uniformly bounded given Assumption 2 in the last inequality. Therefore, . Using the same procedure one can show for any , thus is a martingale.

Denote the th component of the vector process by , and let be the cross-variation of two real processes and up to time . For denote by

Again, due to the uniform topology of the convergence of to , boundedness of and (3.2), and the uniformly integrability of from (12), we have

Therefore

| (25) |

The second and third limit terms in (25) are bounded by

which is zero from a similar argument for showing (24) goes to zero as and (12). For the first limit term in (25), using Assumption 2 and the Euler recursive formula (6), we have

| (26) |

The first term of (26) clearly converges to zero. We only show the second term converges to zero. The convergence of the other two terms to zero can be shown similarly. Thanks to [3, Theorem 2.5.7] is at the order of . Hence

Therefore once we can justify the exchange of limit and expectation, then the convergence of the expectation to zero is shown. To this end, using Lemma 16 and Young’s inequality, we show uniform integrability of as follows

which is finite for all small , here we have used Lemma 16 in the second last inequality above. Hence we show (26) converges to zero as . Therefore

Thanks to [9, Theorem 7.1], there exists a dimensional Brownian motion such that . Therefore, is the weak solution of (3).

3.3 Properties of First Passage Times

Lemma 18

For any and , the mapping from to is continuous.

Proof: The case of is trivial. For and , functions

are obviously continuous. For (a nonempty set only if ), we may decompose into and , and express as

Given is continuous, and and are continuous, we have is continuous for any .

Proof: Note that firm values , , satisfy (3). For any , we show as follows

| (27) |

where . Due to the uniform nondegeneracy Assumption 3 and boundedness of , there exist some positive constants and such that

Thanks to the property discussed in [15, Appendix A.5], we know the term in (27) is zero. Similarly, for . Finally, .

Remark 20

In the proof of Lemma 19, we need to show a one-dimensional continuous semi martingale never hits a given point within finite time almost surely, more specifically see (27). One may wonder if uniform nondegeneracy of can be relaxed to positive definite to show this result. The answer is negative. The counter example for one dimensional case is provided in [17].

Proof: Since , we have

Observe that for any ,

| (28) |

In the above, we use the fact . Similar to the derivation of (27), the event is equivalent to

Define the processes and to be:

The differential form of the SDE for is as follows

where

and is a standard 2-d Brownian motion, is an adapted process satisfying

and and are th and th row vector of . Rewriting (28) in terms of the process , our target is to show that if Assumption 5 or 6 is true, then

| (30) |

Using Girsanov Theorem, we may assume the drift term is zero:

We first prove (30) is true under Assumption 5. We have is an identity matrix for all almost surely. Since we are investigating the first-passage time before , without loss of generality, we assume

Then we have

Define and . By the time change results for multidimensional continuous local martingales in [20, Theorem 5.1.9], we have

is a standard 2-d Brownian motion under with initial position . Since and are both continuous and strictly increasing, the inverse maps and exist and are both strictly increasing. It suffices to show

This is true due to , and nonattainability of the origin by the 2-d Brownian path shown in [11, Proposition 3.3.22].

We next prove (30) is true under Assumption 6. We have is a piecewise constant process almost surely. In other words, for strictly increasing stopping time sequence such that and , the process is in the form of

where is a nonsingular dimensional matrix, measurable with respect to . Let be any given point in . Partitioning the event in (30), we have

But the integrand in the above integral is seen to be zero from the following derivation.

Here the supremum is taken among any constant 22 nonsingular matrix, since is measurable with respect to and constant from to . Also, denotes a 2-dimensional Brownian motion starting from zero. The last inequality is using Markovian property of Brownian motion and is no greater than almost surely. Hence for each the integral is zero, so is the countable summation.

Assumption 5 or 6 is used to prove (30). Although it is intuitive to think the two dimensional continuous nondegenerate local martingale (without Assumption 5 or 6) should not hit a given point within finite time, it seems difficult to prove this rigorously. Since this unsolved question is interesting on its own, we describe it in detail below.

Remark 22

(an open question) Let be a two dimensional standard Brownian motion with respect to a filtered probability space . Define a continuous local martingale by

with . Assume that is an adapted matrix process satisfying

The question we have is that whether the following equality

is true? We leave this to our future work.

3.4 Completion of the Proof

Now we are ready to complete the proof of Theorem 7. Let and be the sets of the continuities of functions and respectively. Due to [22, Lemma 4], with fixed boundary , the mapping is continuous at each . Notice that and are composition of indicator functions, and , and is continuous by Lemma 18. Hence we have

and

To apply the mapping theorem (see [1, Theorem 2.7]) we need to show and . It can be seen by

Similarly, one can show . With Assumptions 2 and 4, Theorem 17 says that as . Using the mapping theorem, we conclude that

Note that , , are bounded functions, hence are families of uniformly integrable random variables and

Therefore,

Remark 23

(Extension to stochastic interest rate) Suppose the risk-free interest rate is a -adapted continuous process. Let be a dimensional -adapted continuous process which represents , and . Define and as

and

For and we have that converging to in Skorohod metric implies converging to in uniform metric which implies converging to for . This shows the mapping from to , defined by , is continuous at each . Then, the two mappings and are continuous at under Skorohod topology. Since the discounting factors and can be rewritten as and respectively, Theorem 7 still holds for the process under the same setting.

4 Conclusions

We have derived the sufficient conditions for the convergence of the approximation of basket CDS with counterparty risk under a credit contagion model of multinames by generalizing the known weak limit theorems with discontinuous coefficents under non-Markovian setting. The method developed in this paper may be used to study other problems involving running maximal processes of correlated Brownian motions, the joint distribution of which is still unknown for dimension greater than two.

Acknowledgement The authors thank Thomas G. Kurtz for useful discussions on weak convergence of stochastic processes. The authors are very grateful to the anonymous reviewers and the AE whose instructive comments and suggestions have helped greatly to improve the paper of the previous version.

References

- 1. Billingsley, P.: Convergence of Probability Measures. John Wiley & Sons (2009)

- 2. Chan, K.S., Stramer, O.: Weak consistency of the Euler method for numerically solving stochastic differential equations with discontinuous coefficients. Stoch. Proc. Appl. 76, 33-34 (1998)

- 3. Durrett, R.: Probability: Theory and Examples. Cambridge University Press (2010)

- 4. Ethier, S.N., Kurtz, T.G.: Markov Processes: Characterization and Convergence. John Wiley & Sons (2005)

- 5. Gu, J.W., Ching, W.K., Siu, T.K., Zheng, H.: On pricing basket credit default swaps. Quant. Financ. 13, 1845-1854 (2013)

- 6. Haworth, H., Reisinger, C.: Modeling Basket Credit Defaults Swaps with Default Contagion. J Credit Risk. 3, 31-67 (2007)

- 7. Higham, D.J., Mao, X., Stuart, A.M.: Strong convergence of Euler-type methods for nonlinear stochastic differential equations. SIAM J. Numer. Anal. 40, 1041-1063 (2003)

- 8. Hutzenthaler, M., Jentzen, A., Kloeden, P.E.: Strong convergence of an explicit numerical method for SDEs with nonglobally Lipschitz continuous coefficients. Ann. Appl. Probab. 22, 1611-1641 (2012)

- 9. Ikeda, N., Watanabe, S.: Stochastic Differential Equations and Diffusion Processes, 2nd edn. North-Holland/Kodansha (1989)

- 10. Iyengar, S.: Hitting lines with two-dimensional Brownian motion. SIAM J. Appl. Math. 45, 983-989 (1985)

- 11. Karatzas, I., Shreve, S.E.: Brownian Motion and Stochastic Calculus. Springer (1991)

- 12. Kloeden, P.E., Platen, E.: Numerical Solution of Stochastic Differential Equations. Springer (2011)

- 13. Kurtz, T.G., Protter, P.: Weak limit theorems for stochastic integrals and stochastic differential equations. Ann. Appl. Probab. 19, 1035-1070 (1991)

- 14. Kushner, H.J., Dupuis, P.: Numerical Methods for Stochastic Control Problems in Continuous Time. Springer (2001)

- 15. Leung, T., Song, Q., Yang, J.: Outperformance portfolio optimization via the equivalence of pure and randomized hypothesis testing. Financ. Stoch. 17, 839-870 (2013)

- 16. Mao, X., Yuan, C., Yin, G.: Approximations of Euler-Maruyama type for stochastic differential equations with Markovian switching, under non-Lipschitz conditions. J. Comput. Appl. Math. 205, 936-948 (2007)

- 17. MathOverflow, A non-degenerate martingale. Website (version: 2011-12-24). http://mathoverflow.net/questions/84216

- 18. Metzler, A.: On the first passage problem for correlated Brownian motion. Stat. Probabil. Lett. 80, 277-284 (2010)

- 19. Mörters, P., Peres, Y.: Brownian Motion. Cambridge University Press (2010)

- 20. Revuz, D., Yor, M.: Continuous Martingales and Brownian Motion. Springer (1999)

- 21. Rosenthal, H.P.: On the subspaces of spanned by sequences of independent random variables. ISRAEL J. Math. 8, 273-303 (1970)

- 22. Song, Q., Yin, G., Zhang, Q.: Weak convergence methods for approximation of the evaluation of path-dependent functionals. SIAM J. Control Optim. 51, 4189-4210 (2013)

- 23. Song, Q., Yin, G., Zhu, C.: Optimal switching with constraints and utility maximization of an indivisible market. SIAM J. Control Optim. 50, 629-651 (2012)

- 24. Yan, L.: The Euler scheme with irregular coefficients. Ann. Probab. 30, 1172-1194 (2002)

- 25. Yong, J., Zhou, X.Y.: Stochastic Controls: Hamiltonian Systems and HJB Equations. Springer (1999)

- 26. Zheng, H.: Contagion models a la carte: Which one to choose? Quant. Financ. 13, 399-405 (2013)