†Department of Statistics, School of Mathematics, Statistics and computer Science,

College of Science, University of Tehran, P.O. Box 14155-6455, Tehran, Iran

‡Department of Statistics, Allameh Tabataba’i University, Tehran, Iran

Abstract

We introduce the problem of estimation of the parameters of a dynamically selected population in an infinite

sequence of random variables and provide its application in the statistical inference based

on record values from a non-stationary scheme.

We develop unbiased estimation of the parameters of the dynamically selected population

and evaluate the risk of the estimators. We provide comparisons with natural estimators and

obtain asymptotic results. Finally, we illustrate the applicability of the results using real data.

Keywords: Extreme value theory,

General record models, Partial maxima, Pfeifer model, Selected population, Uniformly minimum

variance unbiased estimator.

1 Introduction

The problem of estimating parameters of selected populations has wide practical

applications in estimation of experimental data in agriculture, industry and medicine.

Some of the real world applications of this theory are the

problem of estimating the average yield of a selected variety of plant with maximum yield (Kumar and Kar, 2001), estimating the average fuel efficiency of the

vehicle with minimum fuel consumption (Kumar and Gangopadhyay, 2005) and selecting the regimen with maximal efficacy or minimal toxicity from a

set of regimens and estimating a treatment effect for the selected regimen (Sill and Sampson, 2007).

The problem of estimation

after selection has received considerable attention by many

researches in the past three decades. Interested readers are referred to, for example, Gibbons et

al. (1977) for more details. Some other

contributions in this area include Sarkadi (1967), Dahiya (1974), Kumar

and Kar (2001), Misra et al. (2006a,b), Kumar et al. (2009) and Nematollahi and Motammed-Shariati (2012). For

a summary of results, as well as a list of references until 2006, see Misra et

al. (2006 a,b).

In this paper, we introduce and develop the problem of estimation

of the parameters of a dynamically selected population

from a sequence of infinite populations which

is not studied in the literature, according to the best of our knowledge.

Let be a sequence of random variables where

is drawn from population with corresponding cumulative

distribution function (cdf) and probability

density function (pdf) . The traffic volume trend, daily temperatures,

sequences of stock quotes, or sequences of

estimators of interior water volume in a dam reservoir are examples

of such sequences.

Suppose we want to estimate the parameter of the population

corresponding to the largest value of the sequence

yet seen, that is

where , with probability one, and for

or similarly the parameter of the population corresponding to the

smallest value of the sequence yet seen, that is

where , with probability one, and for

We want to estimate , and similarly the lower ones .

This happens for example, when we want to estimate the largest value of traffic volume

or stock quotes yet seen, the

temperature of the coldest day or the largest volume of the

coming water into the dam reservoir, up to now.

For simplicity, we denote by hereafter.

We may write

(1)

where

(4)

(5)

The statistics and are called upper and lower records, respectively.

In the sequence , the sequences of partial

maxima and upper record statistics are defined by and , respectively, where with

probability 1, and for

. The record statistics could be

viewed as the dynamic maxima of the original random variables. So, we call the

problem of estimating as the estimation of the parameter of a dynamically selected population.

There is a vast literature on records for iid as well as non-stationary random variables.

A thorough survey of available results,

until 1998, is given in the book of Arnold et al. (1998).

More recent articles on record values include, among others,

Amini and Balakrishnan (2013, 2015), Doostparast and Emadi (2013), Salehi et al. (2013),

Ahmadi and Balakrishnan (2013, 2010), Psarrakos and Navarro (2013),

Raqab and Ahmadi (2012), Zarezadeh and Asadi (2010), Kundu et al. (2009) and Baklizi (2008).

This problem is related to the so-called general record

model. The geometrically increasing

populations, the Pfeifer, the linear drift and the record models are some of the generally used record models.

The basics of non-stationary schemes for the record values are

due to Nevzorov (1985, 1986) and Pfeifer (1989, 1991),

who considered the so-called -scheme, that is the

sequences of independent random variables with distribution

, where is a

continuous cdf and ’s are positive parameters. Further

generalization of the -scheme was suggested by Ballerini and

Resnick (1987). Although non-stationary schemes could be employed in

the most general setting, the special case of improving populations is usually of special interest. Alternative

non-stationary schemes include geometrically increasing populations,

linear trend and Pfeifer models.

In all the above

models, strict assumptions are made on the sequence of parameters

. For instance, in record

model, the sequence of the parameters is assumed to be known or depend

on a fixed unknown parameter. In the linear drift model, a linearly

increasing population is assumed as the underlying population.

However, certain natural phenomena may behave otherwise. For example, an

earthquake is produced by a natural phenomenon which has a pivotal parameter that

varies based on an unknown model. In order to

predict extremely destructive earthquakes, a very important question

is on the value of the parameters which cause a

new record in the sequence of earthquakes?

This motivates us to study the problem of dynamic after-selection

estimation.

The rest of this paper is organized as follows. The theoretical results of the dynamic after-selection

problem, consisting unbiased estimation of the parameters of the

model as well as unbiased estimation of the risk of the estimators

are presented in Sections 2 and 3. In Section 4,

we compare the proposed estimators with some natural estimators.

Asymptotic distributional results for studying the limiting behavior

of the risks of the estimators

are studied in Section 5. Finally, a real

data example is considered in section 6 to illustrate the

applicability of the results.

2 Minimum variance unbiased estimation

Let , and be a random parameter (a function of and ). Suppose that

is estimated by . Following Lehmann (1951), the estimator is said to be risk unbiased for under the loss function , if it satisfies

In this section, we use the U-V method of Robbins (1988), to find Uniformly Minimum Variance Unbiased (UMVU) estimator of

under the two models 1 and 2, presented below.

Model 1: Let be a sequence of

independent absolutely continuous random variables with pdf

(8)

where is a complete sufficient statistic with the

Gamma)-distribution. Some well-known members of the

above family are:

1. Exponential(), with , and

;

2. Gamma(), with and ;

3. Normal(0,), with

, , and

;

4. Inverse Gaussian(), with , , and

;

5. Weibull(), with known , , , and

;

6. Rayleigh(), with , , and

.

To estimate in the family of distributions (8), we first consider the estimation of

under the Gamma()-distribution with pdf

(9)

By using the U-V

method of Robbins (1988), we have the following lemma (see also

Vellaisamy and Sharma, 1989).

Lemma 1

Let be a sequence of independent random variables

with densities defined in (9). Let

be a real-valued function such that for

(i)

(ii)

Then the functions

satisfy

The next result obtains the unbiased estimator of

, under the SEL function, for the Gamma() distribution with the pdf of as in (9).

Theorem 1

For the Gamma() distribution with the pdf of as in (9),

an unbiased estimator of

, under SEL function, which satisfies (7) with , is

(10)

where is the upper record value of the sequence .

Proof

From (1), (4) and Lemma 1, an unbiased

estimator of , under SEL function, based on

is given by

To find an unbiased estimator of under the Model 1 with the pdf of as in (8), let , and . Then, by replacing with in Theorem 1, an unbiased

estimator of , under the SEL function, for the general family (8), can be obtained as

(11)

where is the upper record value of the sequence .

For a monotone function (available in all of the above

examples, except in the normal distribution), can be obtained simply as for an increasing

and as for a decreasing . For example, for the

Rayleigh()-distribution, an unbiased estimator for

is

Model 2: For , consider

two families of distributions, the first with having the survival function

(12)

and the second with having the cdf

(13)

in which is a cdf, free of , and

. We assume to be known. These are called proportional hazard rate and proportional reversed hazard rate families, or simply models

in the context of record values. Some

well-known members of the above families are:

By making use of U-V method of Robbins (1988) for the family

(12), we have the following lemma.

Lemma 2

Let be a sequence of independent random variables

with survival function defined in (12). Let

be a real-valued function such that for

(i)

(ii)

in which is the hazard function of and is the

corresponding pdf of . Then the functions

satisfy

Proof

For one component problem (i.e., a single random variable , ), let . Then, we have

For the sequence , the result follows by a similar calculation.

The next result gives the unbiased estimator of

, under SEL function, for the general family (12).

Theorem 2

Assume to be known and let be the cumulative hazard function of . For the general family (12), an unbiased estimator of

, under the SEL function, is

(14)

Proof

From (1), (4) and Lemma 2, an unbiased estimator

of is given by

Remark 1

Similarly, for the family (13),

an unbiased estimator for , under the SEL function, is

where is the cumulative reversed hazard function of the known cdf .

Remark 2

Note that is a complete sufficient statistic

for . Hence, the above

unbiased estimators of are indeed UMVU estimators of

.

3 Estimation of the Risks

To compare the UMVU estimator with other estimators, we need to compute

the risk function of the proposed estimators.

Under the SEL function, the risk of an estimator is

The UMVU estimators obtained in Section 3 are functions of

. Suppose

we want to estimate the risk of an estimator of which

depend on only through and , i.e.

. Then, we have the following results, under

Models 1 and 2, respectively.

Theorem 3

Under the Model 1 and the SEL function, an unbiased estimator of the risk of an

estimator of is

Proof

From Lemma 1 with , we have

where

Therefore

Furthermore

Which completes the proof.

An immediate corollary of Theorem 3

is as follows.

Corollary 1

Under the Model 1 and the SEL function, an unbiased estimator of the risk of

is

Theorem 4

For the general family (12), and under the SEL function, an unbiased

estimator of the risk of an estimator of

is

Proof

From Lemma 2 and using similar argument as in the proof of Theorem 3, we have

Furthermore

This completes the proof.

An immediate

corollary of Theorem 4 is as follows.

Corollary 2

For the general family (12) and under the SEL function,

(i) an unbiased

estimator of the risk of

is

(ii) the risk of is

Remark 3

The results for the general family (13) can be obtained by

replacing with in Theorem

4 and Corollary 2.

Remark 4

Since is a complete sufficient statistic

for , the above

unbiased estimators of are indeed, UMVU

estimators of .

The following result presents the distribution

of the unbiased estimator in the family (12).

Lemma 3

In the general family (12), the following identities hold:

(i) For every and ,

(ii) For every , and ,

Proof Let and , . We only prove part (i). Part (ii) is proved in a simillar way.

Using the fact that and the lack of memory property of the exponential distribution,

Thus, a natural estimator for , for this family of

distributions is . For the general family with the survival

function (12), we have

which candidates as a natural estimator of .

So a risk comparison of the natural estimators with UMVUEs of

, for both families of distributions is considered.

The following Corollary of Theorem 4 states that, under Model 2, the UMVUE dominates the natural estimator.

Corollary 3

For the general family (12) and under the SEL function, we have

Proof

First, we have

Consequently,

This completes the proof.

However, under Model 1, no explicit results can be obtained for domination of the UMVUE or the natural estimator with respect to the other, since

we have similarly

To compare the UMVUE and the natural estimator under Model 1, we run a simulation study, which is described in the following section.

4.1 Simulation study

We assume . To compare the risks of the UMVUE

, with that of the natural estimator

, for

, , we consider three different models for the sequence of

parameters as follows:

Model 1 (An stochastic, positive error auto-regressive model):

Model 2 (An stochastic Geometrically increasing population):

Model 3 (White noise model):

The simulated bias and risks of the estimators are tabulated in Table 1. As one can observe

from Table 1, the simulated risks of are less than those of .

Also, biases and risks are increasing in , except the risks of , under the white noise

Model 3.

Table 1: Simulated bias and risk of the UMVUE and the natural estimator of under three different models from

gamma distribution for different values of and .

Model 1

2

3

4

0.5

Risk

9.440638

14.75326

18.54895

Bias

1.524951

4.747217

9.160673

Risk

23.1851

84.08421

209.7748

2

Risk

3.224838

6.856674

10.66222

Bias

0.5978639

1.782032

3.29696

Risk

3.886525

12.33907

27.96078

Model 2

2

3

4

0.5

Risk

2.224561

53.26235

1785.95

Bias

0.7864656

2.342428

6.334353

Risk

5.501025

94.40079

2499.64

2

Risk

0.5376576

2.314486

19.68881

Bias

0.3038626

0.72345

1.335166

Risk

0.6209572

2.658157

19.79643

Model 3

2

3

4

0.5

Risk

161.3311

146.8202

125.2359

Bias

13.682

30.34559

47.98977

Risk

685.7074

1851.813

3543.839

2

Risk

64.93679

74.52687

82.06017

Bias

7.023687

13.47608

19.60645

Risk

131.9781

297.2568

537.5641

5 Asymptotic results

From Corollary 2, the risk of the UMVUE of for the general family (12), , is

where is the upper record value form the sequence , with .

Hence, asymptotic joint distribution of and would be useful for computing the risks of the estimators. The following theorem

proposes the required asymptotic distribution.

Theorem 5

Let and be such that

as for all real , where is one of the three extreme value cdfs (see Resnick, 1987, p. 38). Then, for the family (12) with , and letting and , we have, for all ,

as , where is the corresponding pdf of .

Proof. Letting , and

is the order statistic of .

Using the independence of and under the model (Ballerini and Resnick, 1987), we have

Consequently, since satisfies the Von-Mises conditions (see Resnick, 1987) and , as , we have

Thus, the proof is complete.

When is standard exponential distribution, we have , and .

Therefore, letting and , as , we have

and consequently for each and , as , we have

However, and depend on the unknown . The following result solves this problem

using the fact that under the model, converges in law to the standard

normal distribution (see Nevzerov, 1995).

Theorem 6

Under the family (12) with , with the assumptions of Theorem

5, and letting , as , for fixed

, and , we have

where is the cdf of the standard normal distribution.

as , which is the upper Fréchet Höeffding bound; see, e.g., Fréchet (1951) or Nelsen (1999, p. 9).

The following Corollary, presents an approximate formula for the risk of UMVUE of , for the family (12).

Corollary 4

For the family (12), under the assumptions of Theorem 5, we have

The above double integral can be simplified by algebraic manipulations as

in which is the pdf of the standard normal distribution.

Thus, we have

as .

6 Rainfall data: an illustrative example

In this section, we utilize the data set which represents the

records of the amount of annual (January 1-December 31) rainfall in

inches recorded at Los Angeles Civic Center LACC during the 100-year

period from 1890 until 1989, presented by Arnold et al. [1998, p.

180].

A member of the model (Model 2) with survival function as in (12), that is the Rayleigh distribution with cdf

(16)

is well-fitted to the data.

The -value for two-sample Kolmogorov-Smirnov test is 0.3333. Figure 1 shows the empirical distribution function of the rainfall data and the cdf in (16). Thus, we take

to be the known cumulative hazard rate function of the base distribution .

Figure 1: Empirical cdf of the rainfall data.

Suppose that the only observations are the sequence of upper record values as follows:

12.69

12.84

18.72

21.96

23.92

27.16

31.28

34.04.

We consider two hypotheses:

(Stationary model) ;

(Non-stationary model) and s are independent.

Under , , with

probability 1. Hence, is the

UMVUE of . Also, ,

with unbiased estimator .

Under , and the

unbiased estimator of its risk is .

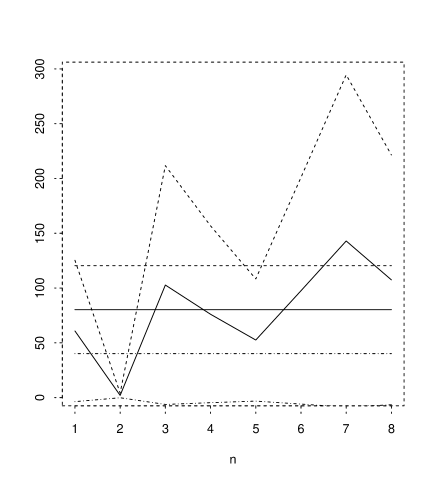

Figure 2 shows the values of and their

corresponding 3- region

under and .

Figure 2: Estimates path (solid line) and 3- regions (upper and lower dashed lines) of , under the stationary (straight lines) and non-stationary (zigzag lines) assumptions, for the rainfall data.

To test against using the record sequence we propose the scale invariant test statistic

(17)

Since, under , all s are equal, the null hypothesis is rejected for large values of .

We use the fact that under , the random variables

, are iid exponential, to deduce that under ,

(18)

where stands for the identically distributed and .

Deriving the exact distribution of is far from reach. However, one can estimate the distribution quantiles of using a Monté Carlo simulation study.

Table 2: The critical values of the test statistic (18)

n

0.01

0.025

0.05

0.1

2

8645.63

1368.24

326.02

64.61

3

19003.73

3113.96

723.25

164.76

4

27929.12

4681.26

1093.01

264.36

5

37018.72

6343.56

1529.97

355.73

6

49769.98

7707.69

2007.57

456.78

7

64315.21

9211.87

2388.29

563.19

8

70630.56

10801.06

2698.59

655.51

9

73372.31

11655.77

3131.44

747.15

10

92847.93

13727.53

3500.69

883.22

To generate random variables identically distributed as

, one may generate an iid sample form standard exponential, namely, , and return .

Table 2 presents the simulated values of -critical values of , , for , and , which

are generated using R.14.1 package with iterations. The hypothesis is rejected at level as

For the rainfall data we obtain , which is less than .

Therefore, is not rejected in favor of at level .

7 Concluding remarks

The problem of estimating parameters of the dynamically selected populations can be extended to the Bayesian

context. Moreover, the problem of unbiased estimation of the selected parameters under other loss functions is of interest.

The distributional models which are not members of studied families can be studied separately, specially the discrete distribution.

Another problem is to find the two stage (conditionally) unbiased estimators of the

parameters of the dynamically selected populations.

These problems are treated in an upcoming work, to appear in subsequent papers.

Acknowledgements

The authors thank the anonymous referee for his/her useful comments and suggestions on an earlier version of this manuscript which resulted in this improved version.

References

[1] Ahmadi J. and Balakrishnan N. (2010). Prediction of order statistics and record values from two independent sequences, Statistics,

44, 417 – 430.

[2] Ahmadi J. and Balakrishnan N. (2013). On the nearness of record values to order statistics from Pitman’s measure of closeness, Metrika, 76, 521 – 541.

[3] Amini M. and Balakrishnan N. (2013). Nonparametric Meta-Analysis of Independent Samples of Records. Computational Statistics & Data Analysis, 66, 70 – 81.

[4] Amini M. and Balakrishnan N. (2015). Pooled Parametric Inference for minimal repair systems. Computational Statistics, DOI: 10.1007/s00180-014-0552-8.

[5] Arnold B. C., Balakrishnan N. and Nagaraja H. N. (1998). Records, John Wiley & Sons, New York.

[6] Baklizi A. (2008). Likelihood and Bayesian estimation of using lower record values from the generalized exponential distribution, Computational Statistics & Data Analysis, 52, 3468 – 3473.

[7] Ballerini R. and Resnick S.I. (1987). Embedding sequences of successive maxima in extremal processes with

applications. Journal of Applied Probability, 24, 827 – 837.

[8] Dahiya, R. C. (1974). Estimation of the Mean of the Selected Population,

Journal of the American Statistical Association, 69, 226 – 230.

[9] Doostparast, M. and Emadi M. (2013). Evidential inference and optimal sample size determination

on the basis of record values and record times under random sampling scheme, Statistical Methods & Applications,

doi:10.1007/s10260-012-0228-x.

[10] Fréchet, M. (1951). Sur les tableaux de corrélation dont les marges sont données.

Annales de l’Université de Lyon Section A. (3), 14, 53 – 77.

[11] Gibbons, J. D., Olkin, I. and Sobel, M. (1977). Selecting and Ordering Populations. A New

Statistical Methodology. New York: John Wiley and Sons.

[12] Kumar S. and Kar A. (2001). Estimation quantiles of a selected exponential population. Statistics & Probability Letters, 52, 9 - 19.

[13] Kumar S. and Gangopadhyay A.K. (2005). Estimation parameters of a selected Pareto population. Statistical Methodology, 2, 121 - 130.

[14] Kumar S., Mahapatra A.K. and Vellaisamy P. (2009). Reliability estimation of the selected exponential populations. Statistics & Probability Letters, 79, 1372 - 1377.

[15] Kundu C., Nanda A. K. and Hu T. (2009). A note on reversed hazard rate of order statistics and record values, Journal of Statistical Planning and Inference, 139, 1257 – 1265.

[16] Lehmann, E.L. (1951). A general concept of unbiasedness. Annals of Mathematical Statistics, 22, 578-592.

[17] Misra N., Vander Meulen E.C. and Branden K.V. (2006a). On estimating the scale parameter of the selected gamma population under the scale invariant

squared error loss function. Journal of Computational and Applied Mathematics, 186, 268 - 282.

[18] Misra N. Vander Meulen E.C. and Brandan K.V. (2006b). On some inadmissibility results for the scale parameters of selected gamma populations. Journal of Statistical Planning and Inference, 136, 2340 - 2351.

[19] Nelsen, R. B. (1999). An Introduction to Copulas. Lecture Notes in Statistics.

Springer, New York.

[20] Nematollahi, N. and Motammed-Shariati, F. (2012). Estimation of the parameter of the selected

uniform population under the entropy loss function, Journal of Statistical Planning and Inference, 142, 2190 – 2202.

[21] Nevzorov V.B. (1985). On record times and inter-record times for sequences of non-identically distributed

random variables. Zap. Nauehn. Sere. LOMI., 142, 109 – 118.

[22] Nevzorov V.B. (1986). Two characterizations using records. Lecture Notes in Mathematics, 1233,

79 – 85.

[23] Nevzorov V. (1995). Asymptotic distributions of records in non-stationary schemes.

Journal of Statistical Planning and Inference, 45, 261 – 273.

[24] Pfeifer D. (1989). Extremal processes, secretary problems and the 1/e law, Journal of Applied Propagability, 27, 722 – 733.

[25] Pfeifer D. (1991). Some remarks on Nevzorov’s record model. Advances in Applied Propagability, 23, 823 – 834.

[26] Psarrakos, G. and Navarro, J. (2013). Generalized cumulative residual entropy and record values, Metrika, 76,623 – 640.

[27] Raqab M. Z. and Ahmadi J. (2012). Pitman closeness of record values from two sequences to population quantiles, Journal of Statistical Planning and Inference, 142, 855 – 862.

[28] Resnick, S. (1987). Extreme Values, Regular Variation, and Point

Processes., Springer-Verlag, New York.

[29] Robbins H. (1988). The U.V methods of estimation. In: Gupta, S.S., Berger, J.O. (Eds.), Statistical Decision Theory and Related Topics IV, vol.1. Springer -

Verlag, NewYork, pp. 265 - 270.

[30] Salehi M. Ahmadi J. and Balakrishnan, N. (2013). Prediction of order statistics and record values based on ordered ranked set sampling,

Journal of Statistical Computation and Simulation, doi = 10.1080/00949655.2013.803194.

[31] Sarkadi, K. (1967). Estimation after selection. Studia Scientarium Mathematicarum Hungarica, 2, 341–350.

[32] Sill, M. W. and Sampson, A. R. (2007).

Extension of a Two-Stage Conditionally Unbiased Estimator of the Selected Population to the Bivariate Normal Case,

Communications in Statistics - Theory and Methods,

36, 801 – 813.

[33] Vellaisamy P. and Sharma D. (1989). A note on the estimation of the mean of the selected gamma population. Communications in Statistics - Theory and Methods, 18, 555 – 560.

[34] Zarezadeh S. and Asadi M. (2010). Results on residual Rényi entropy of order statistics and record values, Information Sciences, 180, 4195 – 4206.