Bootstrap for -Statistics: A new approach

Abstract.

Bootstrap for nonlinear statistics like -statistics of dependent data has been studied by several authors. This is typically done by producing a bootstrap version of the sample and plugging it into the statistic. We suggest an alternative approach of getting a bootstrap version of -statistics, which can be described as a compromise between bootstrap and subsampling. We will show the consistency of the new method and compare its finite sample properties in a simulation study.

Key words and phrases:

primary 62G09, secondary 60G10, Mixing Processes, -Statistics, Bootstrap, Subsampling1. Introduction

In many statistical applications, the asymptotic limit distribution cannot be used to construct tests or confidence intervals, as the limit might be unknown or dependent on unknown parameters, which are hard to estimate. Bootstrap versions of the statistical estimator provide a nonparametric alternative, so establishing the consistency of such bootstrap procedure is important. In the case of independent and identically distributed (iid) random variables, the main idea of the bootstrap consists of replacing the original sample of observations with unknown marginal distribution function by a new iid sample with the marginal distribution function which is the empirical distribution function constructed from the original sample (see Efron [8]). As a bootstrap version of a statistic one can take the plug-in version . The validity of bootstrap for the sample mean of iid observations was first established by Bickel and Freedman [2] and Singh [21]. It is well-known that in some cases the bootstrap method provides a better approximation to the distribution of the statistic than, for instance, normal approximation (see Hall [10]). Especially when sample size is relatively small, bootstrap has some preferences.

In the case of dependent observations this idea of getting a new sample does not work since a new iid sample does not capture the dependence structure, see Singh [21]. Therefore several so-called blockwise bootstrap methods of getting a new sample were introduced (for overview of blockwise bootstrap methods see Lahiri [12]). In all these methods, we resample from blocks of consecutive observations, so that inside the blocks the dependence structure will be kept. We will consider two of them: The circular block bootstrap method introduced by Politis and Romano [15] and nonoverlapping block bootstrap method by Carlstein [3]. In the case of circular block bootstrap method we extend the original sample to where is a block length. To get a new sample we choose randomly and independently consecutive observations of the sample times with

for Here and in what follows we denote by the conditional probability, conditional expectation and conditional variance respectively. For instance the bootstrap version of sample mean will be

In the case of nonoverlapping block bootstrap method we construct a new sample by choosing randomly and independently blocks of consecutive observations of the sample as above times with

for . In this case the bootstrap version of the sample mean is

For weakly dependent observations strong consistency (almost surely convergence) of the and were proved in Shao and Yu [19] and Peligrad [18]. Gonçalves and White [9] and Dehling, Sharipov and Wendler [5] extended these results to functionals of mixing processes. In this paper we will concentrate on bootstrap for -statistics of weakly dependent observations. Bootstrap for -statistics of independent observations were studied by Bickel and Freedman [2], Arcones and Gine [1], Dehling and Mikosch [4], Leucht and Neumann [13]. Recently, Dehling and Wendler [6], Sharipov and Wendler [20] and Leucht and Neumann [14] established the consistency of bootstrap estimators for -statistics of weakly dependent observations. In the aforementioned papers the same idea of getting bootstrap versions of -statistics have been used, which is based on the plug-in principle. We will now introduce -statistics. Let be a stationary sequence of random variables with a common distribution function . For simplicity reasons we consider -statistics of degree two i.e.:

where is the symmetric and measurable kernel. The kernel is called degenerate, if

If this does not hold we call the kernel and the corresponding -statistics nondegenerate. In what follows we will only consider -statistics with a nondegenerate kernel. In the case of iid observations Bickel and Freedman [2] used the bootstrap sample of conditional independent observations with common distribution function , which is the empirical distribution function constructed by original sample. In order to get bootstrap versions of -statistics they plugged the bootstrapped observations in -statistics i.e.

In the case of dependent observations, the same idea was explored by Dehling, Wendler [6] using the circular block bootstrap method, the corresponding bootstrap version is

while in the case of nonoverlapping block bootstrap method the corresponding bootstrap version of -statistics is

Consistency of (and ) can be proved using the Hoeffding decomposition (see [11]):

where

In order to prove consistency of it is enough to show the convergence of bootstrapped distribution of the sample mean for the second summand of this decomposition and convergence to zero (in probability or almost surely) of the third summand. The goal of this paper is to suggest a new resampling method for -statistics. The main idea is the following: We suggest to draw with replacement from the -statistics calculated on subsamples instead of drawing with replacement from blocks of observations and then plug them in -statistics. We introduce subsets by

where us called block length. Furthermore, let and be two sequences of iid random variables with distributions:

A fixed realisations of the sample we denote by . We set

where is the indicator function. So respectively are the -statistics calculated from the -th block and and are the results of the drawing with replacement from these -statistics. In the case of we assume that if . As the bootstrap versions of -statistics we take the following:

Note that

In the next sections we will state our main result: the strong consistency of the bootstrap based on , . The new approach reduces the computational burden of the Monte Carlo method usually used for the bootstrap. After calculating the values , for every run of the Monte Carlo evaluation one need only calculation steps, while for the plug-in method, in every run the -statistic has to be calculated again in steps. As the linear parts of the plug-in bootstrap version and the new bootstrap version of a -statistic are the same, we expect a similar behaviour.

We will give an upper bound for the mean square error (MSE) of the variances of , , which suggest a choice of the block length of order . In section 3, we will present our simulation results. We consider the sample variance as a -statistic and we will compare the new bootstrap approach with plug-in bootstrap and subsampling. The proofs of the main results will be given in section 4.

2. Main results

Let be a stationary sequence of random variables with values in a separable linear space. We will assume that this sequence satisfies some form of short range dependence. Namely we will consider strong mixing and absolute regularity conditions. Recall that strong mixing coefficients and absolute regularity coefficients are defined as

where is the - field generated by . Now we can formulate our results.

Theorem 2.1.

Let be a stationary sequence of absolutely regular random variables. Assume that the following conditions hold (for some )

-

•

for some ,

-

•

for all ,

-

•

for some ,

-

•

for some .

Then as for

in probability.

In the next theorem we consider strongly mixing random variables. This is a weaker assumption on the dependence, but in this case we assume that the kernel satisfies the following condition: We say that a kernel is -Lipschitz-continuous, if there exists a constant such that

for every , every pair and with the common distribution for some or and and also with one of these common distributions. For the examples of kernels which satisfy above condition see [6], [20].

Theorem 2.2.

Let be a stationary sequence of strongly mixing random variables. Assume that the following conditions hold

-

•

,

-

•

for all ,

-

•

for some ,

-

•

is -Lipschitz-continuous,

-

•

for some ,

-

•

for some .

Then the statements of Theorem 2.1 hold.

In the next theorem we give bounds for the mean squared error to give a deeper insight into the properties of bootstrap versions of -statistics.

Theorem 2.3.

Let be a stationary sequence of absolutely regular random variables. Assume that the following conditions hold:

-

•

for some ,

-

•

for all ,

-

•

for some .

Then for

Choosing a block length of order , we can achieve that the mean squared error of is of order .

3. Simulation

We consider the estimator for the variance which is a -statistic with the kernel :

is a stationary, Gaussian, autoregressive process with , where is a sequence of iid standard normal random variables and . We will compare three methods for constructing confidence intervals:

-

•

The circular plug-in bootstrap (already used in Dehling, Wendler [6]).

-

•

The new bootstrap version , the drawing with replacement from -statistics caculated on subsamples.

-

•

Subsampling: The estimator of the unkown distribution is given by the empirical distribution function of the -statistics caculated on subsamples, see Politis and Romano [16].

For each combination of construction method, AR-coefficient, sample size ( ) and block length, we have simulated 10.000 samples and evaluated the empirical probability of the 95% confidence interval to cover the true parameter. The two bootstrap version are evaluated by the Monte Carlo method with 1000 times drawing with replacement. The results are summarized in the table below.

| 0.2 | 0.4 | 0.6 | ||

| 50 | 3 | 0.876/0.895/0.827 | 0.863/0.791/0.693 | 0.794/0.600/0.569 |

| 5 | 0.865/0.884/0.823 | 0.838/0.819/0.737 | 0.765/0.677/0.583 | |

| • | 7 | 0.862/0.871/0.814 | 0.823/0.818/0.753 | 0.762/0.718/0.614 |

| • | •10 | 0.835/0.849/0.787 | 0.808/0.814/0.743 | 0.757/0.730/0.607 |

| 100 | 3 | 0.908/0.922/0.823 | 0.894/0.817/0.730 | 0.852/0.600/0.507 |

| 5 | 0.911/0.910/0.852 | 0.896/0.838/0.770 | 0.851/0.682/0.617 | |

| • | 7 | 0.909/0.909/0.849 | 0.874/0.857/0.793 | 0.853/0.737/0.676 |

| • | 10 | 0.890/0.902/0.851 | 0.880/0.859/0.815 | 0.849/0.767/0.716 |

| 200 | 5 | 0.926/0.930/0.873 | 0.908/0.859/0.813 | 0.883/0.684/0.620 |

| 7 | 0.925/0.926/0.881 | 0.905/0.870/0.831 | 0.891/0.738/0.704 | |

| • | 10 | 0.924/0.920/0.889 | 0.911/0.885/0.857 | 0.887/0.805/0.761 |

| • | 15 | 0.910/0.910/0.884 | 0.902/0.893/0.849 | 0.885/0.835/0.800 |

| 400 | 7 | 0.927/0.932/0.896 | 0.927/0.887/0.855 | 0.920/0.748/0.711 |

| 10 | 0.931/0.927/0.906 | 0.924/0.901/0.873 | 0.920/0.814/0.777 | |

| 15 | 0.923/0.929/0.901 | 0.923/0.904/0.882 | 0.902/0.847/0.828 | |

| • | 20 | 0.924/0.918/0.906 | 0.902/0.909/0.887 | 0.904/0.866/0.849 |

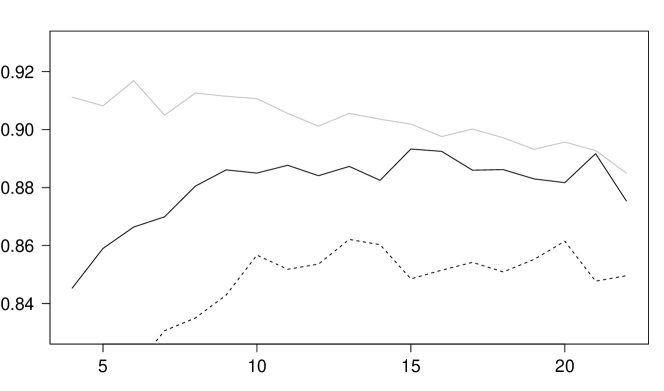

In general, we draw the following conclusions from the simulation study: All three methods lead to confidence intervals with a coverage probabilty lower than the nominal confidence level of 95%. The performance of the subsampling is worse than the performance of two bootstrap methods in all situations. If the dependence in the AR-process is weak (), both bootstrap methods lead to comparable results, while for stronger dependence (), the plug-in bootstrap has a better performance.

For the plug-in bootstrap, the block length can be choosen smaller than for the new bootstrap method or for subsampling, especially in the case of stronger dependence (). In Figur 1 below, we give a more detailed picture of the coverage probabilities for different block lengths in the case , .

4. Proofs of the theorems

4.1. Preliminary results

In this section we formulate some necessary results that will be used in the proofs of our theorems.

Lemma 4.1.

(Dehling,Wendler [7]) Let be a stationary sequence and a degenerate kernel satisfying for some and for all . Let be such that one of the following two conditions holds:

-

(1)

is absolutely regular and .

-

(2)

is strongly mixing, for a , is -Lipschitz-continuous with constant and .

Then:

Lemma 4.2.

(Yoshihara [23]) Let be a stationary sequence of absolutely regular random variables. Assume that the the following conditions hold (for some ) and

Then

Lemma 4.3.

(Yokoyama [22]) Let be a stationary strongly mixing sequence of random variables with and for some . Suppose that and

Then there exists a constant depending only on and the mixing coefficients such that

4.2. Proof of Theorem 2.1

Let us introduce blocks of indices

Note that the blocks and correspond to the circular and nonoverlapping blocking methods, respectively. In the circular blocking method instead of the sample we consider the completed sample A fixed realization of the sample we denote by and set

First we will prove the statement of the theorem for (circular bootstrap). Using Hoeffding decomposition we have

Using the latter

In order to prove the first statement of Theorem 2.1, we first show that as . Note that

By Lemma 4.1 we have as

and consequently in probability as . With the Chebyshev inequality, it follows that in conditional probability.

It remains to show the convergence of . By Theorem 3.2 of Lahiri [12] we have as

in probability. Furthermore, we have by Lemma 4.1 and can conclude that

Using Slutzky’s lemma and in probability, we arrive at at the first statement of the Theorem:

For the second statement, we make use of Theorem 3.2 of Lahiri [12] again, which also states that

This together with in probability and (see Lemma 4.1) leads to

in probability as .

4.3. Proof of Theorem 2.2

4.4. Proof of Theorem 2.3

To shorten the proof, we concentrate on the case (circular bootstrap). We split the mean squared error into three parts

For the first summand, we know by Theorem 3.1 of Politis and White [17] that

For the second summand, we make use of the equation and the Hölder-inequality (first for the bootstrap expectation and then for the unconditional expectation) to obtain

We will treat these two factors separately, starting with . By the definition of the bootstrap procedure and the stationarity of the sequence, we get the following:

as we know from Lemma 3 of Yoshihara [23] that

With the help of the inequality , we split the second summand into two parts:

so it suffices to study . We use again stationarity and the definition of the bootstrap:

The last inequality follows from Lemma 4.3. This shows that . In the same way one can show that is of the same order, which completes the proof.

References

- [1] M.A. Arcones, E. Gine, On the bootstrap for U and V statistics, Ann. Stat. 20 (1992) 655-674.

- [2] P.J. Bickel, D.A. Freedman, Some asymptotic theory for the bootstrap, Ann. Stat. 9 (1981) 1196-1217.

- [3] E. Carlstein, The use of subseries values for estimating the variance of a general statistic from stationary sequence, Ann. Stat. 14 (1986) 1171-1179.

- [4] H. Dehling, T. Mikosch, Random quadratic forms and the bootstrap for -statistics, J. Multivariate Anal. 51 (1994) 392-413.

- [5] H. Dehling, O.Sh. Sharipov, M. Wendler, Bootstrap for dependent Hilbert space-valued random variables with application to von Mises statistics, J. Multivariate Anal. 133 (2015) 200-215.

- [6] H. Dehling, M. Wendler, Central limit theorem and the bootstrap for -statistics of strongly mixing data, J. Multivariate Anal. 101 (2010) 126-137.

- [7] H. Dehling, M. Wendler, Law of the iterated logarithm for -statistics of weakly dependent observations, in: Berkes, Bradley, Dehling, Peligrad, Tichy (Eds): Dependence in Probability, Analysis and Number Theory, Kendrick Press, Heber City (2010).

- [8] B. Efron, Bootstrap methods: another look at the jackknife, Ann. Stat. 7 (1979) 1-26.

- [9] S. Gonçalves, H. White, The bootstrap of the mean for dependent hetereogeneous arrays, Econometric Theory 18 (2002) 1367-1384.

- [10] P. Hall, The bootstrap and Edgeworth expansions, Springer, New York (1992).

- [11] W. Hoeffding, A class of statistics with asymptotically normal distribution, Ann. Math. Stat. 19 (1948) 293-325.

- [12] S.N. Lahiri, Resampling methods for depenent data, Springer, New York (2003).

- [13] A. Leucht, M.H. Neumann, Consistency of general bootstrap methods for degenerate U- and V-type statistics, J. Mult. Anal. 100 (2009) 1622-1633.

- [14] A. Leucht, M.H. Neumann, Dependent wild bootstrap for degenerate U- and V-statistics. J. Mult. Anal., 117 (2013) 257-280.

- [15] D.N. Politis, J.P. Romano, A circular block-resampling procedure for stationary data,In: Exploring the Limits of the Bootstrap (R. Lepage and L. Billard ,eds.) (1992) 263-270.Wiley, New York.

- [16] D.N. Politis, J.P. Romano, Large sample confidence regions based on subsamples under minimal assumptions, Ann. Stat. 22 (1994) 2031-2050.

- [17] D.N. Politis, H. White, Automatic block-length selection for the dependent bootstrap, Econometric Reviews 23 (2004) 53-70.

- [18] M. Peligrad, On the blockwise bootstrap for empirical processes for stationary sequences, Ann. Prob. 2 (1998) 877-901.

- [19] Q. Shao, H. Yu, Bootstrapping the sample means for stationary mixing sequences, Stochastic Process. Appl. 48 (1993) 175-190.

- [20] O.Sh. Sharipov, M. Wendler, Bootstrap for the sample mean and for -statistics of mixing and near-epoch dependent processes, Journal of Nonparametric Statistics 24 (2012) 317-342.

- [21] K. Singh, On the asymptotic accuracy of Efron’s bootstrap, Ann. Stat. 9 (1981) 1187-1195.

- [22] R. Yokoyama, Moment bounds for stationary mixing sequences, Z. Wahrsch. verw. Gebiete 52 (1980) 45-57.

- [23] K. Yoshihara, Limiting behavior of -statistics for stationary, absolutely regular processes, Z. Wahrsch. verw. Gebiete 35 (1976) 237-252.