Robust recoverable and two-stage selection problems

Abstract

In this paper the following selection problem is discussed. A set of items is given and we wish to choose a subset of exactly items of the minimum total cost. This problem is a special case of 0-1 knapsack in which all the item weights are equal to 1. Its deterministic version has an -time algorithm, which consists in choosing items of the smallest costs. In this paper it is assumed that the item costs are uncertain. Two robust models, namely two-stage and recoverable ones, under discrete and interval uncertainty representations, are discussed. Several positive and negative complexity results for both of them are provided.

Keywords: robust optimization; computational complexity; approximation algorithms; selection problem

1 Introduction

In this paper we wish to investigate the following Selection problem. Let be a set of items. Each item has a nonnegative cost and we wish to choose a subset of exactly items of the minimum total cost, , where . This problem has a trivial -time algorithm which works as follows. We first determine in -time the th smallest item cost, say (see, e.g., [11]), and then choose items from whose costs are not greater than . Selection is a special, polynomially solvable version of the 0-1 knapsack problem, in which all the items have unit weights. It is also a special case of some other discrete optimization problems such as minimum assignment or a single machine scheduling problem with the weighted number of late jobs criterion (see [19] for more details). It can be seen as a basic resource allocation problem [18]. It is also a matroidal problem, as the set of feasible solutions is composed of all bases of an uniform matroid [29].

Suppose that the item costs are uncertain and we are given a scenario set , which contains all possible vectors of the item costs, called scenarios. We thus only know that one cost scenario will occur, but we do not know which one before a solution is computed. The cost of item under scenario is denoted as and we assume that . No additional information for scenario set , such as a probability distribution, is provided. Two methods of defining scenario sets are popular in the existing literature (see, e.g, [25]). In the discrete uncertainty representation, contains explicitly listed scenarios. In the interval uncertainty representation, for each item an interval of its possible costs is specified and is the Cartesian product of these intervals. The cost of solution depends now on scenario , , and will be denoted as . In order to choose a solution two robust criteria, namely the min-max and min-max regret can be applied, which lead to the following two optimization problems:

where is the set of all feasible solutions and is the cost of an optimal solution under scenario . The quantity is called a regret of solution under scenario . Both robust versions of the Selection problem have attracted a considerable attention in the recent literature. It turns out that their complexity depends on the way in which scenario set is defined. It has been shown in [3] that, under the discrete uncertainty representation, Min-Max Regret Selection is NP-hard even for two scenarios. Repeating a similar argument as the one used in [3] gives the result that Min-Max Selection remains NP-hard even for two scenarios. Both problems become strongly NP-hard when the number of scenarios is a part of input [19]. Furthermore, in this case Min-Max Selection is also hard to approximate within any constant factor [19]. Several approximation algorithms for Min-Max Selection have been recently proposed in [20, 19, 13]. The best known, designed in [13], has an approximation ratio of . For the interval uncertainty representation both robust problems are polynomially solvable. The min-max version is trivially reduced to a deterministic counterpart, as it is enough to solve the deterministic problem for scenario . On the other hand, Min-Max Regret Selection is more involved and some polynomial time algorithms for this problem have been constructed in [3, 10]. The best known algorithm with running time has been shown in [10].

Many real world problems arising in operations research and optimization have a two-stage nature. Namely, a complete or a partial solution is determined in the first stage and can be then modified or completed in the second stage. Typically, the costs in the first stage are known while the costs in the second stage are uncertain. This uncertainty is also modeled by providing a scenario set , which contains all possible vectors of the second stage costs. If no additional information with is provided, then the robust criteria can be applied to choose a solution. In this paper we investigate two well known concepts, namely robust two-stage and robust recoverable ones and apply them to the Selection problem. In the robust two-stage model, a partial solution is formed in the first stage and completed optimally when a true scenario reveals. In the robust recoverable model a complete solution must be formed in the first stage, but it can be modified to some extent after a true scenario occurs. A key difference between the models is that the robust two-stage model pays for the items selected only once, while the recoverable model pays for items chosen in both stages with the possibility of replacing a set of items from the first to the second stage, controlled by the recovery parameter.

Both models have been discussed in the existing literature for various problems. In particular, the robust two-stage versions of the covering [12], the matching [22] and the minimum spanning tree [21] problems have been investigated. The two-stage model has been also considered in the stochastic setting, i.e. when a probability distribution in scenario set is available. Namely, it has been applied to the minimum spanning tree [14], the 0-1 knapsack [24, 23], the matching [22] and the maximum weighted forest [1] problems. The robust recoverable approach has been applied to linear programming [26], some network problems [6, 7, 28], the 0-1 knapsack [8], and recently to the traveling salesperson [9] and the minimum spanning tree [17] problems.

Our results

In Section 3 we will investigate the robust recoverable model. We will show that it is strongly NP-hard and not at all approximable, when the number of scenarios is a part of input. A major part of Section 3 is devoted to constructing a polynomial algorithm for the interval uncertainty representation, where is the recovery parameter. In Section 4 we will study the robust two-stage model. We will prove that it is NP-hard for two second-stage cost scenarios. Furthermore, when the number of scenarios is a part of input, then the problem becomes strongly NP-hard and it has an approximability lower bound of . For scenario set , we will construct a randomized algorithm which returns an -approximate solution with high probability. If , then the randomized algorithm gives the best approximation up to a constant factor. We will also show that for the interval uncertainty representation the robust two-stage model is solvable in time.

2 Problems formulation

Before we show the formulations of the problems we recall some notations and introduce new ones. Let us fix and define

-

•

,

-

•

,

-

•

,

-

•

, ,

-

•

is the deterministic, first-stage cost of item ,

-

•

is the second-state cost of item under scenario , where .

-

•

, for any subset .

We now define the two-stage model as follows. In the first stage we choose a subset of the items, i.e. such that , and we add additional items to , after observing which scenario in has occurred. The cost of under scenario is defined as

In the robust two-stage selection problem we seek , which minimizes the maximum cost over all scenarios, i.e.

We now define the robust recoverable model. In the first stage we must choose a complete solution , i.e. such that . In the second stage additional costs occur for the selected items. However, a limited recovery action is allowed, which consists in replacing at most items in with some other items from , where is a given recovery parameter. The cost of under scenario is defined as follows:

In the robust recoverable selection problem we wish to find a solution , which minimizes the maximum cost over all scenarios, i.e.

3 Robust recoverable selection

In this section we deal with the Recoverable Selection problem. Consider first the discrete uncertainty representation, i.e. the problem with scenario set . It is easy to observe that when all the first stage costs are equal to zero and , then Recoverable Selection is equivalent to Min-Max Selection with scenario set . It follows from the fact that the solution formed in the first stage cannot be changed in the second stage and thus and . Hence, we have an immediate consequence of the results obtained in [3, 19]. Namely, under scenario set , the Recoverable Selection problem is weakly NP-hard when . Furthermore, it becomes strongly NP-hard and hard to approximate within any constant factor when is a part of input. We now strengthen this result if the recovery parameter is allowed to be positive.

Theorem 1.

If is a part of input and , then Recoverable Selection with scenario set is strongly NP-hard and not at all approximable unless P=NP.

Proof.

The reduction is similar to that in [20]. Consider an instance of the strongly NP-complete E3-SAT problem [15], in which we are given a set of boolean variables and a collection of clauses , where each clause is disjunction of exactly three literals (variables or their negations). We ask if there is a truth assignment to the variables which satisfies all the clauses. We now construct the corresponding instance of the Recoverable Selection problem as follows. We associate with each clause three items , , corresponding to three literals in . We also create one recovery item . This gives us the item set , such that . The first-stage cost of the recovery item is set to and the first-stage costs of the remaining items are set to zero. The scenario set is formed as follows. For each pair of items and , that corresponds to contradictory literals and , i.e. , we create scenario such that under this scenario the costs of and are set to 1 and the costs of all the remaining items are set to 0. For each clause , , we form scenario in which the costs of , , are set to 1 and the rest of items have zero costs. We complete the reduction by setting and . An example of the reduction is shown in Table 1. We will show that the answer to E3-SAT is yes if and only if in the corresponding Recoverable Selection problem.

| 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | |

| 0 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 1 | 1 | 0 | 1 | 0 | 0 | |

| 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | |

| 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | |

| 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | |

| 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | |

| 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

It is easy to check that if the answer to E3-SAT is yes, then there is a selection out of such that , containing items that do not correspond to contradictory literals and literals from the same clauses. We form by choosing exactly one item out of for each , which corresponds to a true literal in the truth assignment. Thus the costs of under each scenario are at most 1. Hence we can decrease them to zero by replacing an item from with the cost of 1 under any scenario with recovery item and . On the other hand, if the answer to 3-SAT is no, then all selections , , must contain at least two items corresponding to contradictory literals or at least two literals from the same clause. Note that the recovery action under each scenario is limited to one. So, . Accordingly, Recoverable Selection with scenario set is strongly NP-hard and not at all approximable unless P=NP. ∎

In the remaining part of this section we will provide a polynomial algorithm for the interval uncertainty representation. The Recoverable Selection problem with scenario set can be rewritten as follows:

| (1) |

In problem (1) we need to find a pair of solutions and . Since , the problem (1) is equivalent to:

| (2) |

In the following, for notation convenience, we will use to denote and to denote for . Let us introduce 0-1 variables , and , , that indicate the chosen parts of , and , respectively, . Problem (2) can be then represented as the following IP model:

| (3) |

Let , be an optimal solution to (3). Then if or , and if or . The following theorem shows the unimodularity property of the constraint matrix of (3).

Theorem 2.

The constraint matrix of (3) is totally unimodular.

Proof.

We will use the following Ghouira-Houri’s characterization of totally unimodular matrices [16]. An integral matrix is totally unimodular if and only if each set can be partitioned into two disjoint sets and such that

| (4) |

This criterion can alternatively be stated as follows. An integral matrix is totally unimodular if and only if for any subset of rows there exists a coloring of rows of , with 1 or -1, i.e. , , such that the weighted sum of every column (while restricting the sum to rows in ) is , or . The constraint matrix of (3) is shown in Table 2.

| … | … | … | |||||||||||||

| : | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | |||

| : | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |||

| : | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | |||

| : | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | |||

| : | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | |||

| : | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | |||

| ⋮ | |||||||||||||||

| : | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | |||

| : | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | |||

| : | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | |||

| : | 0 | 0 | 0 | 0 | 0 | 0 | 1 | … | 0 | 0 | 0 | 1 | 0 | ||

| : | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 |

Consider a subset of rows , where , , . We examine the following cases and for each of them we show a valid coloring.

-

1.

. Then for and for .

-

2.

. Then , for and if .

-

3.

. Symmetric to Case 2.

-

4.

. Then , for and if .

-

5.

. Then , , for and for .

-

6.

. Then , , for and for .

-

7.

. Symmetric to Case 6.

-

8.

. Then , , , for , for .

∎

From Theorem 2 we immediately get that every extreme solution of (3), after removing the integrality constraints, is integral and in consequence Recoverable Selection for the interval uncertainty representation is polynomially solvable. Our goal is now to construct an efficient combinatorial algorithm for this problem. In order to do this, we first apply Lagrangian relaxation (see, e.g., [2]) to (3). Relaxing the cardinality constraint with a nonnegative multiplier , we obtain the following linear programming problem:

| (5) |

The Lagrangian function for any is a lower bound on the optimum value . It is well-known that is concave and piecewise linear function. We now find a nonnegative multiplier together with an optimal solution , , to (5) which is also feasible in (3) and satisfies the complementary slackness condition, i.e. . By the optimality test, such a solution is optimal to the original problem (3). We will do this by iteratively increasing the value of , starting with . For the following lemma holds:

Lemma 1.

The value of can be computed in time.

Proof.

Let be a set of items of the smallest values of and let be the set of items of the smallest , . Clearly, is a lower bound on . A feasible solution of the cost can be obtained by setting for , for and for . The sets and can be found in time (see the comments in Section 1), and the lemma follows. ∎

Given a optimal solution to for a fixed (such a solution must exist due to Theorem 2), let , , . For the sets , and are pairwise disjoint and thus form a partition of the set into , and , respectively. Indeed, and by the constraints of (5). If , then we can find a better solution by setting , and . The same property holds for the optimal solution when (see the construction in the proof of Lemma 1). Let us state the above reasoning as the following property:

Property 1.

For each there is an optimal solution , , to (5) such that , and form a partition of the set into , and , respectively.

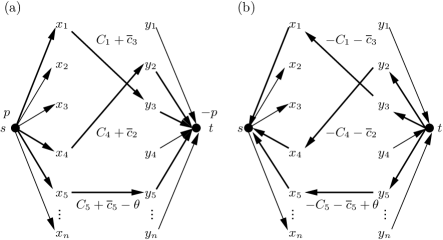

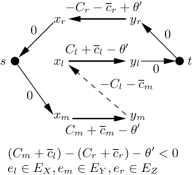

From now on, we will represent an optimal solution to (5) for any as a triple that has Property 1. It is easily seen that (5) is equivalent to the minimum cost flow problem in the network shown in Figure 1a. All the arcs in have capacities equal to 1. The costs of arcs and for are equal to 0. The costs of the arcs for are , and the costs of the arcs , , are . The supply at the source is of and the demand at the sink is of .

Let be an optimal solution to (5). The corresponding integer optimal flow in is constructed as follows. We send 1 unit of flow along arcs , and if ; we then pair the items from and in any fashion and send 1 unit of flow along the arcs , and for each such a pair . An example for , and is shown in Figure 1a, where , , . Assume that is an optimal flow in . We can assume that this flow is integer by the integrality property of optimal solutions to the minimum cost flow problem (see, e.g., [2]). Let be the set of indices of all nodes which receive 1 unit of flow from and let be the set of indices of nodes which send 1 unit of flow to in . Clearly . Let , , . It is easy to see that the cost of the resulting feasible solution to (5) is the same as the cost of .

Consider now an optimal solution to (5) for some fixed . Without loss of generality we can assume that this optimal solution has Property 1. Let be the corresponding optimal flow in . The residual network with respect to is depicted in Figure 1b. By the negative cycle optimality condition (see, e.g., [2]), does not contain any negative cost directed cycle. Suppose we increase in . Then, a negative cost directed cycle may appear in , which means that the flow becomes not optimal in . We now investigate the structure of such negative cycles. This will allow us to find the largest value of for which the flow (and thus the corresponding solution to (5)) remains optimal.

Denote by the set of arcs of the form in (the forward arcs) and by the set of arcs of the form in (the backward arcs). These arcs will play a crucial role as only their costs depend on in . Clearly, the costs of the arcs in decrease and the costs of the arcs in increase when the value of increases. In the example shown in Figure 1b the arc is a backward arc and all the remaining arcs are forward arcs.

We start by establishing the following lemma:

Lemma 2.

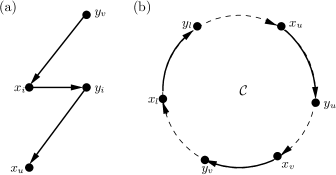

The residual network does not contain a path composed of arcs , and , where and .

Proof.

The following lemma is crucial in investigating the structure of cycles in .

Lemma 3.

Each simple cycle in contains at most two arcs from .

Proof.

Suppose we increase to some value in and denote the resulting residual network as . Assume that a negative cycle appears in . It is obvious that must contain at least one arc from , since only the costs of these arcs decrease when increases. By Lemma 3, the cycle contains either one or two arcs from .

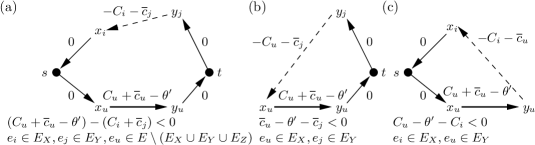

Consider first the case when contains exactly one arc from , say . Then cannot contain any arc from . Otherwise, when computing the cost of , the value of would be canceled and is a negative cycle in , a contradiction. All the possible cases are shown in Figure 3. Notice that in the case (b), by Lemma 2, the arc must belong to . The dashed arcs represent paths between nodes, say and , that do not use any arcs from and and none of the nodes or . An easy computation shows that the cost of such paths equals as the remaining terms are canceled while traversing this path.

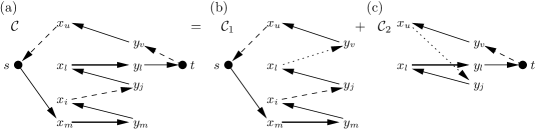

We now turn to the case when contains two arcs from , say and . It is easy to check that in this case may also contain an arc from , but at most one such arc. The cycle must traverse and . Accordingly, it is of the form presented in Figure 4a, which is a consequence of Lemma 2 and Lemma 3.

Assume that a path from to in uses arc such that (see Figure 4a). Let us add to two arcs and whose costs are and , respectively (see Figure 4a). A trivial verification shows that the cost of the cycle is 0. Hence the cost of is the sum of the costs of two disjoint cycles and (see Figures 4b and 4c). Since the cost of is negative, the cost of at least one of and must be negative. If no arc from belongs to , then the cycle is of the form depicted in Figure 3c and is of the form given in Figure 3b. Now suppose that contains one arc from . If that arc is in path from to or from to , then it belongs to cycle . In this case is negative and is of the form shown in Figure 3b. If that arc is in path from to , then we get a symmetric case. Consequently, the case , can be reduced to the cases presented in Figure 3. The last case of cycle , which cannot be reduced to any cases previously discussed, and thus must be treated separately, is shown in Figure 5. Observe that in this case contains two arcs from and one arc from .

We are thus led to the following optimality conditions.

Lemma 4.

Let be an optimal solution to for . Then remains optimal for all which satisfy the following inequalities:

| for | (6) | ||||

| for | (7) | ||||

| for | (8) | ||||

| for | (9) |

Proof.

Consider the optimal flow associated with and the corresponding residual network . Fix so that the conditions (6)-(9) are satisfied and suppose that is not optimal in . Then a negative cost directed cycle must appear in with respect to . This cycle must be of the form depicted in Figures 3 and 5. In consequence, at least one of the conditions (6)-(9) must be violated. ∎

Assume that is an optimal solution to (5) for some . This solution must satisfy the optimality conditions (6)-(9) (when ). Suppose that one of the inequalities (6)-(9) is binding, i.e. it is satisfied as equality. In this case we can construct a new solution whose cost is the same as by using the following transformations:

-

1.

If (6) is binding, then , , ,

-

2.

If (7) is binding, then , , ,

-

3.

if (8) is binding, then , , ,

-

4.

if (9) is binding, then , , .

It is worth pointing out that the above transformations correspond to augmenting a flow around the corresponding cycle in whose cost is 0. In consequence the cost of is the same as the cost of . Hence is also optimal to (5) for . Furthermore it must satisfy conditions (6)-(9) (otherwise we could decrease the cost of by augmenting a flow around some negative cycle). Observe that and also has Property 1. If none of the inequalities (6)-(9) is binding, then we increase until at least one inequality among (6)-(9) becomes binding, preserving the optimality of . We start with and we repeat the procedure described until we find a optimal solution to (5) for , which is feasible in (3) and satisfies the complementary slackness condition: . Notice that , when . Such a solution is an optimal one to the original problem (3). Indeed,

| (10) | ||||

| (11) |

The inequality (10) follows from the Lagrangian bounding principle (see, e.g., [2]). Applying the complementary slackness condition yields the equality (11). Moreover is feasible in (3), and so it is optimal solution to (3). We have thus arrived to the following lemma.

Lemma 5.

The problem (2) is solvable in time.

Proof.

By Lemma 1 the first solution for can be computed in time. Given an optimal solution for some , the next optimal solution can be found in times, since we need to analyze inequalities (6)-(9). The cardinality of increases by 1 at each step until . Hence, the overall running time of the algorithm is . ∎

Theorem 3.

For scenario set , the Recoverable Selection problem is solvable in time.

4 Robust two stage selection

In this section we explore the complexity of Two-Stage Selection. We begin with a result on the problem under scenario set .

Theorem 4.

Under scenario set , Two-Stage Selection is solvable in time.

Proof.

Define , . Let be the set of items of the smallest values of . Clearly, is a lower bound on . A solution with the cost can be now constructed as follows. For each , if , then we add to ; otherwise we add to . It holds and must be optimal. It is easy to see that can be computed in time. ∎

The problem under consideration is much harder for scenario set . The following theorems hold.

Theorem 5.

Under scenario set , Two-Stage Selection is NP-hard when the number of scenarios equals two.

Proof.

In order to prove this theorem we will adapt the idea from [4]. Consider the following Subset Sum problem, which is known to be NP-hard [15]. We are given a collection of nonnegative integers and a nonnegative integer , . We ask if there is a subset such that . Given an instance of Subset Sum we build the corresponding instance of Two-Stage Selection in the following way. We create a set of items . Let . The first stage costs of all the items in are set to . For each , the second stage cost of under is and under it is equal to . The second stage cost of the item is equal to under and under . We complete the reduction by fixing . Observe that all the items must be selected and the problem consists in determining a subset of the items chosen in the first stage (then all the items in must be selected in the second stage under each scenario). The reduction is presented in Table 3.

We now show that the answer to Subset Sum is yes if and only if there is a solution whose cost is not greater than . By the construction, such a solution does not contain the item ( is not chosen in the first stage). Indeed, if , then the cost of under is not less than . Thus we can assume that . Define by the set of indices of the items from (note that ) and let . Since , the cost of can be expressed as follows:

By the definition of the first and second stage costs we get

Now it is easily seen that if and only if , i.e. when the answer to Subset Sum is yes. ∎

Theorem 6.

When is a part of input, then Two-Stage Selection under scenario set is strongly NP-hard. Furthermore, there exists a constant , such that the problem is NP-hard to approximate within a factor of .

Proof.

Consider the following Min-Set Cover problem. We are given a finite set , called the universe, and a collection of subsets of . A subset covers (it is called a cover) if for each element , there exists such that . We seek a cover of the smallest size . Min-Set Cover is known to be strongly NP-hard (see, e.g, [15]) and there exists a constant such that it is NP-hard to approximate within a factor of [31]. We now show a cost preserving reduction from Min-Set Cover to Two-Stage Selection. Given an instance of Min-Set Cover we construct the corresponding instance of Two-Stage Selection as follows. For each set we create an item with first-stage cost equal to 1. We also create additional items labeled as with the first-stage costs equal to a sufficiently large number , say . Thus , . The scenario set is constructed in the following way. For each element we form scenario under which the cost of if and 0 otherwise, . Let be the number of ’s created under scenario for the items , . Hence is the number of sets in which contain . We set the costs of equal to 0 and the costs of equal to . Notice that under each scenario exactly items have costs equal to 0. We fix . An example of the reduction is depicted in Table 4.

| 1 | 0 | 0 | 0 | 0 | |||||

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| 1 | 0 | 0 | 0 | 0 | 0 | ||||

| 1 | 0 | 0 | 0 | ||||||

| 1 | 0 | 0 | 0 | 0 | |||||

| 1 | 0 | 0 | 0 | 0 | 0 | ||||

| 0 | |||||||||

| 0 | 0 | ||||||||

We now show that there is a cover of size if and only if there is a solution such that for every . Let be a cover of size . In the first stage we choose the items for each ; let be this set, . Consider any scenario . Let . Since the element is covered, there must exist at least elements in with 0 costs under . We use these elements in the second stage and form set so that , which gives and, consequently, for every . Assume now that there is a solution such that for every . By the construction and the fact that , and contains only the items corresponding to . Let , . Consider scenario . Since , we must be able to form set , such that , with items of 0 cost under . This is possible only when the cost of some under is , i.e. when the element is covered by . In consequence, each element is covered by and is of size . It is clear that the presented reduction is cost preserving and the theorem follows. ∎

We now present a positive result for Two-Stage Selection under scenario set . Namely, we construct an LP-based randomized approximation algorithm for this problem, which returns an -approximate solution with high probability. Consider the following linear program:

| (12) | ||||||

| (13) | ||||||

| (14) | ||||||

| (15) | ||||||

| (16) | ||||||

| (17) | ||||||

| (18) |

where and . Minimizing subject to (12)-(18), we obtain an LP relaxation of Two-Stage Selection. Let denote the smallest value of the parameter for which is feasible. Obviously, is a lower bound on , and can be determined in polynomial time by using binary search. We lose nothing by assuming, from now on, that , and all the item costs are such that , , . One can easily meet this assumption by dividing all the item costs by . Notice that we can assume that . Otherwise, when , there exists an optimal integral solution of the zero total cost. Such a solution can be constructed by picking all the items with zero first and second stage costs under all scenarios.

Now our aim is to convert a feasible solution to into a feasible solution of Two-Stage Selection. Let -coin be a coin which comes up head with probability . We use such a device to construct a randomized algorithm (see Algorithm 1) for the problem. If Algorithm 1 outputs a solution such that for each , then the sets and can be converted into a feasible solution in the following way. For each scenario , If , then we remove from . Next, if , then we remove arbitrary items, first from and then from so that . Notice that this operation does not increase the total cost of the selected items under any scenario. The algorithm fails if for at least one scenario . We will show, however, that this bad event occurs with a small probability. Let us first analyze the cost of the obtained solution.

Lemma 6.

Fix scenario . The probability that the total cost of the items selected in the first and the second stage under , after the randomized rounding, is at least is at most , where .

Proof.

Fix scenario . Let be a random variable such that if item is included in ; and otherwise, and let be a random variable such that if item is included in ; and otherwise. Obviously, and . Because and , an easy computation shows that and . Define and let be the event that , we recall that . The following inequality holds:

| (19) |

The item costs are such that , . Thus using (19) and applying Chernoff-Hoeffding bound given in [30, Theorem 1 and inequality (1.13) for ], we obtain

| (20) |

which completes the proof. ∎

We now analyze the feasibility of the obtained solution. In order to do this, it is convenient to see steps 5 and 6 of the algorithm in the following equivalent way. In a round we flip an -coin for each and add to when it comes up head; we then flip an -coin for each and and add to if it comes up head. Clearly, steps 5 and 6 can be seen as performing such rounds independently. Let us fix scenario . Let and be the sets of items selected in the first and second stage under (i.e. added to and ), respectively, after rounds. Define and . Initially, , . Let denote the number of items remaining for selection out of the set under scenario after the th round. Initially . We say that a round is “successful” if either (at most 4 items are to be selected) or ; otherwise, it is “failure”.

Lemma 7.

Fix scenario . The conditional probability that round is “successful”, given any set of items and number , is at least .

Proof.

If , then we are done. Assume that and consider the set of items , and the number of items , remaining for selection in round (i.e. after round ). Let be a random variable such that if item is picked from ; and , otherwise. It is easily seen that . The expected number of items selected out of in round is

The first inequality follows from the fact that for any (indeed, ). The last inequality follows from the fact that the feasible solution satisfies constraints (13). Using Chernoff bound (see, e.g.,[27], Theorem 4.2 and inequality (4.6) for ), we get

Thus, with probability at least , the number of selected items in round is at least . Hence, with probability at least it holds

Consequently, when we get

with probability at least . ∎

Lemma 8.

Fix scenario . The probability of the event that is at most , where .

Proof.

Let be the event that , i.e. that the number of items remaining for selection after rounds is at least 5. We now estimate the number of successful rounds which are enough to achieve . It is easy to see that satisfies . In particular, this inequality holds when . Let be a random variable denoting the number of “successful” rounds among performed rounds. We estimate from above by , where is a binomial random variable. This can be done, since we have a lower bound on success of given any history. Applying Chernoff bound (see, e.g., [27, Theorem 4.2 and inequality (4.6) for ] and ) and the fact that , we obtain the following upper bound:

| (21) |

and the lemma follows. ∎

Lemma 6 and Lemma 8 (see also inequalities (20) and (21)) and the union bound imply that . Therefore after rounds the cost of solution found is and the number of items remaining for selection is at most for every with probability at least . The addition of 4 items to in step 7 can increase the cost of the computed solution by at most . As all the costs are nonnegative, repairing , , to obtain a feasible solution cannot increase the cost of the computed solution. Since , we get the following result:

Theorem 7.

There is a polynomial time randomized algorithm for Two-Stage Selection that returns an -approximate solution with high probability.

It is worth pointing out that if , then our randomized algorithm gives the best approximation ratio up to a constant factor (see Theorem 6).

5 Conclusions and open problems

In this paper we have discussed two robust versions of the Selection problem, which have a two-stage nature. In the first problem, a partial solution is formed in the first stage and completed optimally when a true state of the world reveals. In the second problem a complete solution must be formed in the first stage, but it can be modified to some extent after a true state of the world becomes known. Such two-stage problems often appear in practical applications. In this paper we have presented some positive and negative complexity results for two types of uncertainty representations, namely the discrete and interval ones. In particular, we have shown that both problems are polynomially solvable for the interval uncertainty representation. We believe that a similar method might be applied to other combinatorial optimization problems, in particular for those possessing a matroidal structure. When the number of scenarios is a part of input, then the recoverable model is not at all approximable and the two-stage model has an approximability lower bound of . We have shown that the latter one admits a randomized -approximation algorithm.

There are still some open questions concerning the considered problems. A deterministic -approximation algorithm for the two-stage problem may exist and it can be a subject of further research. When is constant, then both robust problems are only proven to be weakly NP-hard. So, they might be solved in pseudopolynomial time and even admit an FPTAS. The interval uncertainty representation can be generalized by adopting the scenario set proposed in [5]. The complexity of both robust problems under this scenario set is open.

Acknowledgements

This work was supported by the National Center for Science (Narodowe Centrum Nauki), grant 2013/09/B/ST6/01525.

References

- [1] P. Adasme, R. Andrade, M. Letournel, and A. Lisser. Stochastic maximum weight forest problem. Networks, 65:289–305, 2015.

- [2] R. K. Ahuja, T. L. Magnanti, and J. B. Orlin. Network Flows: theory, algorithms, and applications. Prentice Hall, Englewood Cliffs, New Jersey, 1993.

- [3] I. Averbakh. On the complexity of a class of combinatorial optimization problems with uncertainty. Mathematical Programming, 90:263–272, 2001.

- [4] F. Baumann, C. Buchheim, and A. Ilyina. A Lagrangean decomposition approach for robust combinatorial optimization. Technical report, Optimization Online, 2014.

- [5] D. Bertsimas and M. Sim. Robust discrete optimization and network flows. Mathematical Programming, 98:49–71, 2003.

- [6] C. Büsing. Recoverable robustness in combinatorial optimization. PhD thesis, Technical University of Berlin, Berlin, 2011.

- [7] C. Büsing. Recoverable robust shortest path problems. Networks, 59:181–189, 2012.

- [8] C. Büsing, A. M. C. A. Koster, and M. Kutschka. Recoverable robust knapsacks: the discrete scenario case. Optimization Letters, 5:379–392, 2011.

- [9] A. Chassein and M. Goerigk. On the recoverable robust traveling salesman problem. Optimization Letters, 10:1479–1492, 2016.

- [10] E. Conde. An improved algorithm for selecting items with uncertain returns according to the minmax regret criterion. Mathematical Programming, 100:345–353, 2004.

- [11] T. Cormen, C. Leiserson, and R. Rivest. Introduction to Algorithms. MIT Press, 1990.

- [12] K. Dhamdhere, V. Goya, R. Ravi, and M. Singh. How to Pay, Come What May: Approximation Algorithms for Demand-Robust Covering Problems. In Annual IEEE Symposium on Foundations of Computer Science (FOCS), pages 367–378, 2005.

- [13] B. Doerr. Improved approximation algorithms for the Min-Max selecting Items problem. Information Processing Letters, 113:747–749, 2013.

- [14] B. Escoffier, L. Gourves, J. Monnot, and O. Spanjaard. Two-stage stochastic matching and spanning tree problems: Polynomial instances and approximation. European Journal of Operational Research, 205:19–30, 2010.

- [15] M. R. Garey and D. S. Johnson. Computers and Intractability. A Guide to the Theory of NP-Completeness. W. H. Freeman and Company, 1979.

- [16] A. Ghouila-Houri. Caractérisation des matrices totalement unimodulaires. C. R. Acad. Sci. Paris, 254:1192–1194, 1962.

- [17] M. Hradovich, A. Kasperski, and P. Zieliński. Recoverable robust spanning tree problem under interval uncertainty representations. Journal of Combinatorial Optimization, 34: 554-573, 2017.

- [18] T. Ibaraki and N. Katoh. Resource Allocation Problems. The MIT Press, 1988.

- [19] A. Kasperski, A. Kurpisz, and P. Zieliński. Approximating the min-max (regret) selecting items problem. Information Processing Letters, 113:23–29, 2013.

- [20] A. Kasperski and P. Zieliński. A randomized algorithm for the min-max selecting items problem with uncertain weights. Annals of Operations Research, 172:221–230, 2009.

- [21] A. Kasperski and P. Zieliński. On the approximability of robust spanning problems. Theoretical Computer Science, 412:365–374, 2011.

- [22] I. Katriel, C. Kenyon-Mathieu, and E. Upfal. Commitment under uncertainty: two-stage matching problems. Theoretical Computer Science, 408:213–223, 2008.

- [23] S. Kosuch. Approximability of the two-stage stochastic knapsack problem with discretely distributed weights. Discrete Applied Mathematics, 165:192–204, 2014.

- [24] S. Kosuch and A. Lisser. On two-stage stochastic knapsack problems. Discrete Applied Mathematics, 159:1827–1841, 2011.

- [25] P. Kouvelis and G. Yu. Robust Discrete Optimization and its Applications. Kluwer Academic Publishers, 1997.

- [26] C. Liebchen, M. E. Lübbecke, R. H. Möhring, and S. Stiller. The concept of recoverable robustness, linear programming recovery, and railway applications. In Robust and Online Large-Scale Optimization, volume 5868 of Lecture Notes in Computer Science, pages 1–27. Springer-Verlag, 2009.

- [27] R. Motwani and P. Raghavan. Randomized Algorithms. Cambridge University Press, 1995.

- [28] E. Nasrabadi and J. B. Orlin. Robust optimization with incremental recourse. CoRR, abs/1312.4075, 2013.

- [29] C. H. Papadimitriou and K. Steiglitz. Combinatorial optimization: algorithms and complexity. Dover Publications Inc., 1998.

- [30] P. Raghavan. Probabilistic Construction of Deterministic Algorithms: Approximating Packing Integer Programs. Journal of Computer and System Sciences, 37:130–143, 1988.

- [31] R. Raz and S. Safra. A Sub-Constant Error-Probability Low-Degree Test, and a Sub-Constant Error-Probability PCP Characterization of NP. In Proceedings of the Twenty-Ninth Annual ACM Symposium on the Theory of Computing, pages 475–484, 1997.