The extremogram and the cross-extremogram for a bivariate GARCH process

Abstract.

In this paper, we derive some asymptotic theory for the extremogram and cross-extremogram of a bivariate GARCH process. We show that the tails of the components of a bivariate GARCH process may exhibit power law behavior but, depending on the choice of the parameters, the tail indices of the components may differ. We apply the theory to 5-minute return data of stock prices and foreign exchange rates. We judge the fit of a bivariate GARCH model by considering the sample extremogram and cross-extremogram of the residuals. The results are in agreement with the iid hypothesis of the two-dimensional innovations sequence. The cross-extremograms at lag zero have a value significantly distinct from zero. This fact points at some strong extremal dependence of the components of the innovations.

Key words and phrases:

Regular variation, bivariate GARCH, Kesten’s theorem, extremogram, extremal dependence2000 Mathematics Subject Classification:

Primary 60G70, 62M10, Secondary 60G10,91B841. The extremogram and the cross-extremogram

In this paper we conduct an empirical study of extremal serial dependence in a bivariate return series. Our main tools for describing extremal dependence will be the extremogram and the cross-extremogram. For the sake of argument and for simplicity, we restrict ourselves to bivariate series , . We assume that has the following structure:

| (1.1) |

where constitutes an iid bivariate noise sequence and

where is the (non-negative) volatility of . We will assume that , constitute strictly stationary sequences and that is predictable with respect to the filtration generated by . We also assume that has mean zero and covariance matrix (standardized to correlations)

| (1.4) |

where . Later, we will choose parametric models for such as univariate GARCH models both for , or a vector GARCH(1,1) model; see Section 2.2 for model descriptions. In the context of these parametric models, the choice of the covariance matrix as a correlation matrix is a matter of identifiability of the model since one can always swap a positive constant multiplier between and .

The extremogram and cross-extremogram for a stationary sequence were introduced in Davis and Mikosch [12] and further developed in Davis et al. [13, 14]. In standardized forms, the extremogram and cross-extremogram of a bivariate sequence are given by

where

| (1.14) |

Here are sets bounded away from zero. Typically, we choose intervals , for and we also suppress the dependence on in the -notation. Notice that has interpretation as an extreme event if is sufficiently large. Thus, the extremogram describes the likelihood of an extreme event at lag given there is an extreme event in the th component at time zero. Correspondingly, the cross-extremogram for describes the likelihood of an extreme event at time lag in the th component given there is an extreme event at time zero in the th component. In general, . The limits can be understood as generalizations of the (upper) tail dependence coefficient for a bivariate vector to the time series context. Here are the -quantiles of the distributions of , respectively. The tail dependence coefficients have been propagated for measuring extremal dependence in a bivariate vector in the context of quantitative risk management; see e.g. McNeil et al. [21].

Moreover, each of the quantities has interpretation as a limiting covariance or cross-covariance function. For example.

The limits in (1.14) do not automatically exist. A convenient theoretical assumption for their existence is the condition of regular variation of the time series . This notion is explained in Section 2.1. Its close relationship with GARCH models is investigated in Section 2.2. Return series are often heavy-tailed and therefore it is attractive to model them by a regularly varying model. For example, under mild conditions the GARCH model automatically ensures that sufficiently high moments of the series are infinite. In particular, univariate and multivariate GARCH models exhibit power laws. This will be explained in Section2.2.

2. Some preliminaries

2.1. Regularly varying time series

We say that an -valued strictly stationary time series is regularly varying with index if its finite-dimensional distributions are regularly varying in the following sense: for every , the following limits in distribution exist

| (2.1) |

where the limit vector has the same distribution as , the distribution of is given by , , and and are independent. Of course, the distribution of , the spectral measure, is concentrated on the unit sphere . The spectral measure describes the likelihood of the directions of extreme values of the lagged vector . Here denotes weak convergence and denotes any norm in ; from now on we choose the Euclidean one. The aforementioned definition of a regularly varying time series is based on work by Basrak and Segers [3] which yields a convenient description of the topic. Davis and Hsing [11] introduced the notion of a regularly varying time series which is attractive for describing serial extremal dependence in the presence of heavy tails. They used an alternative definition of multivariate regular variation which is equivalent to the definition above.

A direct consequence of the regular variation of a time series is that

| (2.2) | , , for a slowly varying function , |

i.e., is a positive function on such that as for any . Then we also have

| (2.3) |

Regular variation of the marginal distribution of the time series is equivalent to the set of relations (2.2) and (2.3). A further consequence is that as for any choice of and some function such that for some and , . For proofs of the aforementioned properties and further reading on regular variation, we refer to Resnick [24, 25].

A particular consequence of the property of regular variation of a time series is the fact that the limits in (1.14), leading to the extremogram and cross-extremogram, are well defined. For this reason, we will assume that is regularly varying or we will assume that a deterministic monotone increasing transformation of the components , , of results in a regularly varying time series. Such transformations can be necessary, for example, if both components are not regularly varying or if both components have rather different tail behavior. These cases are relevant for real-life time series. For the sake of argument, assume that is a bivariate strictly stationary Gaussian time series. This is not a regularly varying time series. However, the extremogram and cross-extremogram of this sequence exist for various sets , for example, if (a corresponding remark applies if or is the set ). If denotes the distribution function of a -distribution with degrees of freedom then calculation yields that

| (2.4) |

has -distributed marginals and one can indeed show that the transformed time series is regularly varying with index . The same transformation arguments apply to a non-Gaussian time series. In contrast to a Gaussian time series, in general one cannot ensure that the resulting time series is regularly varying in the sense defined above. Given that a transformation of the type (2.4) yields a regularly varying time series, one can modify the cross-extremogram e.g. for the sets in the following way:

For practical purposes, we will replace the high quantiles , , by their empirical versions, such as the , ,… componentwise empirical quantiles, depending on the sample size available.

Regular variation of a time series is a convenient theoretical property but it cannot be tested on data. Therefore we will assume a GARCH model for . This model assumption ensures regular variation.

2.2. Univariate GARCH models

From Bollerslev [5] recall the notion of a univariate GARCH model

| (2.5) |

where is an iid unit variance mean zero sequence and is a positive volatility sequence whose dynamics is given by the causal non-zero solution to the stochastic recurrence equation

| (2.6) |

Here and , are constants. The probabilistic structure of can be investigated in the context of solutions to the general stochastic recurrence equation

| (2.7) |

where , , constitutes an -valued iid sequence. Indeed, satisfies this equation with and . Based on the theory for these equations (see Bougerol and Picard [8]), we conclude that a strictly stationary positive solution to (2.6) exists if and only if

| (2.8) |

In view of Jensen’s inequality and since , . Therefore the condition ensures strict stationarity as well as second order stationarity of and , but the condition (2.8) is much more general and also allows for certain choices of such that ; see Nelson [23], Bougerol and Picard [8]. In the latter cases, .

The solution to (2.7) has a rather surprising property which was discovered by Kesten [18]; see also Goldie [16]. Under mild conditions, there exists a positive constant such that for some . We apply the aforementioned theory to (2.6) and get the following result which can be found in Goldie’s [16] paper as regards the marginal distributions. Mikosch and Stărică [22] proved that and are regularly varying time series.

Proposition 2.1.

Assume that , has Lebesgue density and there exists such that

| (2.9) |

and . Then there exist a unique strictly stationary causal non-zero solutions to (2.6) and (2.5), and there exists a constant such that

| (2.10) |

Moreover, as ,

| (2.11) |

where . In addition, the sequences and are regularly varying with index .

3. Bivariate GARCH processes and their properties

Our next goal is to consider multivariate extensions of the GARCH model of the type described in (1.1). A simple way of doing this is by assuming that both component sequences , , constitute univariate GARCH processes, i.e., in (1.1) is specified via the vector recursion

and is an iid sequence with covariance matrix given in (1.4). We can apply the univariate theory to the components , . There exist unique strictly stationary solutions , , if and only if and for . Then we may also conclude that the resulting unique bivariate processes and are strictly stationary. Notice that the dependence structure between the univariate component processes is then completely determined by the dependence structure of the components of the noise . We can also apply Proposition 2.1 to get conditions for power law tails and regular variation of the component processes of .

Remark 3.1.

The crucial condition for the componentwise tail behavior is (2.9). Since the distributions of , , and the parameter sets , , may be distinct, and will in general have different tail indices and , respectively. This fact can be considered an advantage when studying multivariate return series. Indeed, it is not likely that the tail indices of the univariate components of real-life time series coincide.

There exist various extensions of a univariate GARCH model to the multivariate case. We stick here to the constant conditional correlation model of Bollerslev [6]. It is the model (1.1) with specification

| (3.3) |

Writing ,

| (3.8) |

we see that we are again in the framework of the stochastic recurrence equation (2.7), but this time for vector-valued and matrix-valued :

| (3.9) |

Kesten [18] also provided the corresponding theory for stationarity and tails in this case. Stărică [26] dealt with the corresponding problems for vector GARCH processes, making use of the theory in Kesten [18], Bougerol and Picard [8] and its specification to the tails of GARCH models in Basrak et al. [2]. In the bivariate GARCH case the theory in Stărică [26] can be written in a more compact form due to the representation (3.3); in the case of higher order GARCH models (3.3) has to be written as an equation for vectors involving both - and -terms at more than 1 lag.

According to Bougerol and Picard [8], (3.3) has a unique strictly stationary solution if the top Lyapunov exponent associated with the sequence is negative, i.e.,

| (3.10) |

where denotes the matrix norm and the limit on the right-hand side exists a.s. In view of Remark on p. 122 in [8], a sufficient condition for is that the matrix

| (3.15) |

has spectral radius smaller than 1. We assume that all entries of are positive. Then, by the Perron–Frobenius theorem (see Lancaster [19], Section 9.2), has a dominant single positive eigenvalue. Keeping this fact in mind, the largest positive solution to the characteristic equation yields the sufficient condition

| (3.16) |

Next we give sufficient conditions for the regular variation of a bivariate GARCH process . The proof is based on Kesten’s fundamental results [18], in particular Theorem 4. Stărică [26] gave a similar result, referring to Basrak et al. [2] for a related proof in the situation of a univariate GARCH process. We give a proof by verifying Kesten’s conditions.

Proposition 3.2.

Consider the bivariate GARCH model and assume the following conditions:

-

(1)

Condition (3.10).

-

(2)

has Lebesgue density in .

-

(3)

There exists such that

(3.17) -

(4)

All entries of are positive a.s., , , and not all values , , vanish.

Then there exists a unique such that

| (3.18) |

there exists a strictly stationary causal non-zero solution to (1.1) with specification (3.3) and is regularly varying with index . In particular, for every , there exists a non-null Radon measure on such that

Here denotes vague convergence.

Proof.

According to Kesten [18], Theorem 4, there exist

-

•

a unique strictly stationary solution to the equation (3.9),

-

•

a positive value and a non-negative function on such that

(3.19) and the function is positive for such that ,

if the following conditions hold:

-

1.

and and , where (resp. ) implies all entries in are non-negative (resp. positive).

-

2.

The additive group generated by the numbers is dense in , where are elements in the support of the distribution of such that has positive entries and is the spectral radius.

-

3.

Condition (3.10) holds.

-

4.

There is such that (3.18) holds.

-

5.

and .

Condition 1 holds in view of the assumptions a.s. and .

Condition 2. We assume that a.s.

Therefore for any and any in the support of . Since we assume a Lebesgue

density for there exists an open set in where this density is

positive. Therefore

and since not all values vanish,

there exists a continuum of values for in

the support of .

Conditions 3 and 5 follow from the assumptions.

Condition 4. The existence of such an

follows from the existence of such that (3.17) holds. Then .

Thus Kesten’s Theorem 4 can be applied. In particular, (3.19) holds. Due to results in Boman and Lindskog [7] and since is positive, (3.19) implies that is regularly varying with index in the sense of Section 2.1.

Next we show that the finite-dimensional distributions of are regularly varying. This follows from the representation

| (3.20) |

where for , , have moment of order and are independent of . Now an application of the multivariate Breiman theorem in Basrak et al. [1] yields the regular variation of the finite-dimensional distributions of with index , due to the regular variation of with the same index. Hence inherits regular variation with index . Here for any matrix or vector refers to taking square roots for all entries.

It remains to show that is regularly varying with index . We write . It is not difficult to see that is dominated by for some constant and this bound has finite th moment. Therefore

Since is regularly varying with index an application of the multivariate Breiman result (see Basrak et al. [1]) shows that is regularly varying with index as well. Combining these facts, we conclude that

have the same tail behavior and are regularly varying with index ; cf. Jessen and Mikosch [17]. In particular, we have

where , , is independent of and has the spectral distribution of . ∎

Remark 3.3.

In view of Kesten’s result, relation (3.19) holds for any and for . In particular, for and we conclude that as , where both constants are positive. In turn, Breiman’s result [10] ensures that

This means that the right and left tails of the distribution of are equivalent and they have the same tail index . This is in contrast to the case when for (see Remark 3.1), where the components of may have different tail behavior. From a modeling point of view, this property does not allow for much flexibility as regards the componentwise extremes in a multivariate return series. This fact can be understood as a disadvantage of the constant conditional correlation model with respect to more realistic modeling of the extremes of multivariate return models.

The crucial condition in Proposition 3.2 which makes the difference to Proposition 2.1 is the assumption that all entries of must be positive and random. This condition is also satisfied if , and , , i.e., the off-diagonal elements in the matrix may be positive constant.

The case when is an upper or lower triangular matrix is not covered by Proposition 3.2. For example, assume that . Then we have the GARCH equation

which can be solved and, under the conditions of Proposition 2.1, has tail index . Writing , we get

This is again a 1-dimensional recurrence equation but now the coefficients

, , constitute a dependent strictly stationary

sequence. Appealing to Brandt [9], a unique causal

solution to this equation exists but its theoretical properties

are not straightforward due to the

dependence of the coefficient sequence. However, the tail of is

asymptotically at least as heavy as the tail of . Indeed,

as ,

In the last step we applied Breiman’s theorem and used stationarity.

4. The extremogram and cross-extremogram for a bivariate GARCH process

Davis and Mikosch [12] showed for a univariate GARCH process under the conditions of Proposition 2.1 that

where , . While the value of these quantities is not known it is possible to determine their asymptotic order for large . By convexity of the function and since we have for . Therefore

and the right-hand side converges to zero exponentially fast. The extremogram of the -sequence inherits this rate. Since has a finite th moment, multiple use of Breiman’s result yields

Similar calculations can be done in the bivariate case. We restrict ourselves to the -sequences. We assume the conditions of Proposition 3.2; in this case both components , , of the vector in (3.9) have the same tail index. Using relation (3.20), we see that

The limit of the latter ratio converges to a constant by virtue of regular variation. Thus the extremograms are bounded by the extremogram of times this constant. However, (3.20) and the independence of and imply that for ,

The right-hand side converges to zero at an exponential rate in view of for a sufficiently large .

5. An empirical study of the extremogram and the cross-extremogram

5.1. Estimation of the extremogram and cross-extremogram

Davis and Mikosch [12] and Davis et al. [13] proposed estimators of the quantities for given sets bounded away from zero:

| (5.1) |

for some sequence such that as . In order to ensure standard asymptotic properties such as consistency and asymptotic normality, [12, 13] assumed the strong mixing condition and regular variation for the sequence , possibly after a monotone transformation of its components as explained in Section 2.1. The aforementioned growth conditions on the sequence are standard in extreme value statistics and cannot be avoided. They ensure that sufficiently high thresholds , are chosen. These thresholds guarantee that a certain fraction of the data is taken which may be considered extreme as regards their distance from the origin. For practical purposes, we take the corresponding empirical -quantiles of the components.

Although central limit theory can be shown for at a finite number of lags , the asymptotic covariance structure is not tractable. Davis et al. [13] propose two methods for the construction of credible confidence bands: the stationary bootstrap and random permutations. In this paper, we stick to the latter procedure. It is based on the simple idea that, if the sample were iid, random permutations of the sample would not change its dependence structure, hence the extremogram and cross-extremogram would not change. In what follows, we calculate the (cross-) extremograms based on 100 random permutations of the sample. First we calculate the 100 extremogram values at each lag. Then we choose the 96% empirical quantile at each lag and finally take the maximum over the lags of interest. This value is shown as a solid horizontal line in the corresponding graphs. This procedure is quick and clean: if the sample (cross-) extremogram at a given lag is above the horizontal line this is an indication of disagreement with the iid hypothesis.

5.2. Simulated GARCH data

We provide a brief study of the sample (cross)-extremograms of simulated bivariate GARCH processes and their residuals. We choose bivariate GARCH models with iid bivariate -distributed innovations with degrees of freedom and covariance matrix given in (1.4). We simulate from the model (3.3) with parameters (the magnitude of these parameters is in agreement with values estimated from return data) and specified matrices and correlations

| (5.6) |

We start by considering examples with (Examples (1)–(4)) and (Examples (5)–(6)) with respective symmetric parameter matrices (5.6):

Here we always choose small -values while the diagonal -values are close to 1. This is in agreement with estimated parameters on return data. We generate samples of size , using the R package ’ccgarch’111 Note that estimation with “ccgarch” requires choosing initial values. In most cases, we first examine componentwise univariate GARCH fits by the R package “fGarch” and then we choose these estimates as initial values. If the univariate estimation does not converge we try several initial values on a grid of size . In this case, the estimates sometimes differ by attaining local minima. Judging from the residuals, the eigenvalues of the estimated parameters (3.15) and the values of the likelihood functions, we choose an “optimal” estimator. Except for one case of stock return data (see Section 5.4), this procedure works., and calculate the (cross)-extremograms in (5.1) with .

The simulation results for Examples (1)–(6) are given in Figure 1. These figures indicate that small changes in the - or -values lead to substantial changes in the extremal dependence structure. In all cases we observe serial extremal dependence in extremograms (diagonal parts of graphs). In Examples (5)–(6) we also observe large spikes in the cross-extremograms at lag zero due to . This is in contrast to Examples (1)–(4) with . Example (1) shows clear asymmetry in cross-extremograms compared with Example (2), namely, no-correlation can be can be read in the Example (1), which reflects the componentwise independence setting. Others exhibit dependencies in cross-extremograms to greater or lesser degrees.

In Examples (7)–(8) and (9)–(10) we choose and , respectively, and the asymmetric - and -matrices (5.6) as follows

Figure 2 indicates that the asymmetry manifests through the -matrix rather than the -matrix. Again, we observe large spikes at lag zero for the cross-extremograms when (Examples (8) and (10)). Example (10) shows the effects when diagonal elements are distinct.

Our next goal is to show (cross-) extremograms of the residuals of simulated bivariate GARCH models. Although we know the innovations sequence in this case, we want to illustrate how standard MLE techniques work. Of course, we expect that the residuals of the models have properties close to those of an iid sequence also as regards their extremal behavior. The estimation is done in two ways: (1) we fit component-wise univariate GARCH models, applying MLE and assuming student -distributions for the innovations; (2) following Ling and McAleer [20], we apply bivariate Gaussian quasi-MLE (QMLE). We consider the model (3.3) with given parameter and parameter matrices (5.6) as follows

Component-wise univariate MLE yields the following results:

| Ex. (11) | degree for | ||

|---|---|---|---|

| Ex. (12) | degree for | ||

|---|---|---|---|

Despite the misspefication of a bivariate GARCH model, the univariate estimation leads to reasonable estimation results except for the second component of Example (12), where the estimated parameters are far from the true ones.

Bivariate QMLE yields the following estimation results for parameters (5.6):

Figures 3 and 4 (Bottom left and right graphs) indicate that extremal cross-dependencies are not present in the residuals of bivariate GARCH fits with the exception at lag 0. This is true for the bivariate QMLE (Figures 3 and 4: bottom left) but, to some extent, also for the component-wise univariate fits (Figures 3 and 4: bottom right). However, Figure 4 (bottom right) shows that univariate fits do not remove all cross-dependencies from the residuals (in this case the degrees of freedom were not correctly estimated). We experimented with distinct parameters sets close to those in Example (12) and we also replaced univariate MLE by univariate Gaussian QMLE. In all cases, one cannot remove all cross-dependencies of the residuals. Therefore bivariate GARCH fitting is recommended if one believes in a bivariate GARCH model.

5.3. An analysis of foreign exchange rates

We analyze a bivariate high-frequency time series, consisting of 35,135 five minute returns of USD-DEM and USD-FRF foreign exchange rates. Throughout this subsection we choose the component-wise sample quantiles as threshold for the sample (cross-) extremograms. In each plot the horizontal line shows the quantile obtained from random permutations of the data.

The data exhibits rather strong cross-correlations and autocorrelations (see Figure 5, top left: sample autocorrelations, top right: cross-correlations). So it is not unexpected that we also observe dependence of the extreme values of the two series. This is apparent in the extremograms of Figure 5 (bottom). After fitting a bivariate vector AR model of order to the data which is chosen by the “Schwarz criterion” (“Akaike’s final prediction error criterion” proposes an order of ), we fitted a bivariate GARCH model to the residuals, by employing bivariate QMLE. The estimated matrices (5.6) are as follows:

which satisfy the sufficient condition for stationarity of a bivariate GARCH model; see (3.16).

After the AR fit, the cross-extremograms of the residuals do not vanish at all positive lags; see Figure 6 (left) and therefore a GARCH fit for the residuals is recommendable. After fitting the bivariate GARCH, the residuals exhibit extremal cross-dependence only at time-lag ; see Figure 6 (right). This means that the components of the innovations exhibit extremal dependence. Judging from QQ-plots of the residuals of the vector AR model and the AR-GARCH model against the quantiles of -distributions with 2.5 and 3 degrees of freedom respectively; see Figure 7, these distributions give a good fit to the distribution of the residuals.

5.4. An analysis of stock returns

We consider log-return series of three stock prices from the NY Stock Exchange: “Caterpillar Inc.”, “FedEx Corporation” and “Exxon Mobil Corporation” (“cat”, “fdx” and “xom” for short). In each series, the raw tick-by-tick trade data has been processed into 5-minute grid data by taking the last realized trade price in each interval. Prices have been restricted to exchange trading hours 9:30 a.m. to 4:00 p.m., Monday to Friday, so that 78 data per day have been collected in the time period from 2009-02-18 9:30 to 2013-12-31 16:00. The prices at 16:00 are identified with those at 9:30 of the next days. Since we consider the log-return series, the total size of the data is .

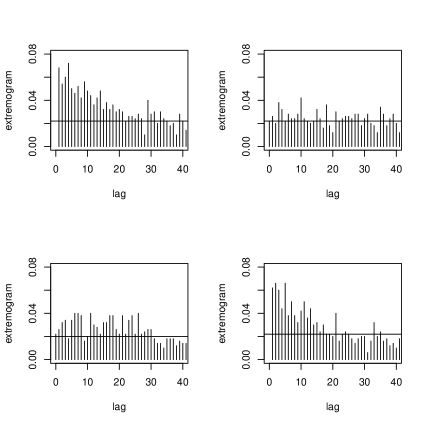

The sample (cross-) extremograms of the log-returns of the stock prices are shown in Figure 8, where we choose the empirical quantiles of the returns as the threshold. We take the quantile obtained from random permutations of the data and show the values as the horizontal line in each plot. Although we observe typical GARCH (cross-) extremograms close to lag 0, there is a clear seasonal component in these plots, appearing as spikes at lag 78, corresponding to the beginning and end of the days. A GARCH model (bivariate or component-wise univariate) cannot explain the seasonal extremal components in the data. However, the (cross-) extremograms of the residuals after a bivariate GARCH fit show that most of the serial dependence has been removed from the data, although the seasonal component is also present in the residuals; see Figure 9.

We fit a bivariate GARCH model to each pair of stock prices, i.e., (cat,fdx), (fdx,xom) and (cat,xom). The estimated values of the bivariate QMLE (5.6) for (cat,fdx), (fdx,xom), (cat,xom), respectively, are

The estimators of the combination (cat, fdx) are unstable and take the boundary value222 In this case, the univariate GARCH fit does not converge. Therefore we examine several initial values for “ccgarch” on a grid of size and choose an “optimal” value based on their likelihoods. We also tried several optimization methods included in “ccgarch”. Then we calculated the eigenvalues of (3.15) from the estimates, including the “optimal” ones. However, the largest eigenvalues are very close to one in all cases. Since “ccgarch” finds the optimal value under the sufficient condition (3.16), the real optima would certainly violate (3.16). of the sufficient condition (3.16) while the estimates for (fdx, xom) and (cat, xom) satisfy (3.16). The obvious seasonal component of the data (corresponding to the end of a trading day at lag 78) probably violates the stationary condition. Nevertheless, the standardized residuals appear “de-volatilized” in all (cross-) extremograms modulo the fact that the seasonal component is always present.

We take QQ-plots of the residuals after bivariate GARCH fits against the quantiles of -distribution with degrees of freedom respectively; see Figure 11. From these plots, -distributions show a good fit to the distribution of the residuals, which also assures that innovations of GARCH model satisfy the regular variation assumption. Only residuals of ’xom’ components (bottom left and bottom right in Figure 11) seem to fit -distribution with different degrees, depending on the pair of stock prices in bivariate estimations.

As predicted, estimated volatilities are affected by periodicity of the day, which is also approved in (cross-) autocorrelation functions of estimated volatility processes in Figure 10. Since the seasonal patterns in these plots are quite clear and intuitive, it is desirable to remove the seasonal component for further analysis.

We further investigated the seasonal effects by plotting the number of

large values in each 5-minute grid during the exchange trading hours; see Figure

12. The large values tend to appear around the begging and end of the

trading hours. This is typically observed in the log-return series of stock

price data.

Acknowledgment. We would like to thank Martin Anders Jönsson for arranging us the stock price data. A major part of this work was done when Muneya Matsui visited the Department of Mathematics at the University of Copenhagen. He is grateful to its hospitality.

References

- [1] Basrak, B., Davis, R.A. and Mikosch. T. (2002) A characterization of multivariate regular variation. Ann. Appl. Probab. 12, 908–920.

- [2] Basrak, B., Davis, R.A. and Mikosch, T. (2002) Regular variation of GARCH processes. Stochastic Process. Appl. 99, 95–116.

- [3] Basrak, B. and Segers, J. (2009) Regularly varying multivariate time series. Stochastic Process. Appl. 119, 1055–1080.

- [4] Bingham, N.H., Goldie, C.M. and Teugels, J.L. (1987) Regular Variation. Cambridge University Press, Cambridge (UK).

- [5] Bollerslev, T. (1986) Generalized autoregressive conditional heteroskedasticity. J. Econometrics 31, 307–327.

- [6] Bollerslev, T. (1990) Modelling the coherence in short-run nominal exchange rates: a multivariate generalised ARCH model. Review of Economics and Statistics 72, 498–505.

- [7] Boman, J. and Lindskog, F. (2009) Support theorems for the Radon transform and Cramér-Wold theorems. J. Theoret. Probab. 22, 683–710.

- [8] Bougerol, P. and Picard, N. (1992) Stationarity of GARCH processes and of some non-negative time series. J. Econometrics 52, 115–127.

- [9] Brandt, A. (1986) The stochastic equation with stationary coefficients. Adv. in Appl. Probab. 18, 211–220.

- [10] Breiman, L. (1965) On some limit theorems similar to the arc-sin law. Theory Probab. Appl. 10, 323–331.

- [11] Davis, R.A. and Hsing, T. (1995) Point process and partial sum convergence for weakly dependent random variables with infinite variance. Ann. Probab. 23, 879–917.

- [12] Davis, R.A. and Mikosch, T. (2009) The extremogram: a correlogram for extreme events. Bernoulli 15, 977–-1009.

- [13] Davis, R.A., Mikosch, T. and Cribben, I. (2012) Towards estimating extremal serial dependence via the boostrapped extremogram. J. Econometrics 170, 142–-152.

- [14] Davis, R.A., Mikosch, T. and Zhao, Y. (2013) Measures of serial extremal dependence and their estimation. Stochastic Process. Appl. 123, 2575–-2602.

- [15] Embrechts, P., Klüppelberg, C. and Mikosch, T. (1997) Modelling Extremal Events for Insurance and Finance. Springer, Berlin.

- [16] Goldie, C.M. (1991) Implicit renewal theory and tails of solutions of random equations. Ann. Appl. Probab. 1, 126–166.

- [17] Jessen, A.H. and Mikosch, T. (2006) Regularly varying functions. Publ. Inst. Math. (Beograd) (N.S.) 80(94), 171–192.

- [18] Kesten, H. (1973) Random difference equations and renewal theory for products of random matrices. Acta Math. 131, 207–248

- [19] Lancaster, P. (1969) Theory of Matrices. Academic Press, New York, London.

- [20] Ling, S. and McAleer, M. (2003) Asymptotic theory for a vector ARMA-GARCH model. Econom. Theory 19, 280–310.

- [21] McNeil, A.J., Frey, R. and Embrechts, P. (2005) Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press, Princeton (NJ).

- [22] Mikosch, T. and Stărică, C. (2000) Limit theory for the sample autocorrelations and extremes of a GARCH(1,1) process. Ann. Statist. 28, 1427–1451.

- [23] Nelson, D.B. (1990) Stationarity and persistence in the GARCH model. Econom. Theory 6, 318–334.

- [24] Resnick, S.I. (1987) Extreme Values, Regular Variation, and Point Processes. Springer, New York.

- [25] Resnick, S.I. (2007) Heavy-Tail Phenomena: Probabilistic and Statistical Modeling. Springer, New York.

- [26] Stărică, C. (1999) Multivariate extremes for models with constant conditional correlations. Journal of Empirical Finance 6, 515–553.

- [27] Vervaat, W. (1979) On a stochastic difference equation and a representation of non-negative infinitely divisible random variables. Adv. in Appl. Probab. 11, 750–783.