Small-time expansions for state-dependent local jump-diffusion models with infinite jump activity

Abstract

In this article, we consider a Markov process , starting from and solving a stochastic differential equation, which is driven by a Brownian motion and an independent pure jump component exhibiting state-dependent jump intensity and infinite jump activity. A second order expansion is derived for the tail probability in small time , for . As an application of this expansion and a suitable change of the underlying probability measure, a second order expansion, near expiration, for out-of-the-money European call option prices is obtained when the underlying stock price is modeled as the exponential of the jump-diffusion process under the risk-neutral probability measure.

Keywords and phrases: Short-time asymptotics; local jump-diffusion Markov models; stochastic differential equations with jumps; option pricing.

1 Introduction

In this work we consider a Markov process with infinitesimal generator of the form

| (1.1) |

where and , , , and are deterministic function satisfying appropriate conditions for the existence of such a process (see below for further details). Broadly, can be defined in terms of a stochastic differential equation (SDE) of the form:

where is a Wiener process and is an independent pure-jump process, whose jump behavior is dictated by and as follows:

| (1.2) |

for any , , and . Intuitively, (1.2) tells us that the jump intensity of the process “near” time depends on its state immediately before via the function in that if is large (small), then we expect a higher (lower) intensity of jumps immediately after time . In the particular case of , (1.2) reduces to

| (1.3) |

and has the usual interpretation of a stochastic jump intensity as defined in, e.g., [4] and [7]. That is, measures the expected number of jumps, per unit time, with size near when the process is at state . State-dependent jump behavior as described above is an important feature that offers greater modeling flexibility to other commonly studied jump processes. For several applications we refer the reader to [16], [12], [14], [13], [8], [9], [20], and [24].

The generator (1.1) covers a wide range of processes. For a Lévy processes, and are constants, , and , for a Lévy density (i.e., ). When we simply have , we recover the class of (local) jump-diffusion models studied in [10]. In that case, can be constructed as

| (1.4) |

where is a Lévy process with Lévy density and denotes the compensated Poisson sum of the terms therein. The case of with has been studied in [24]. More generally, if is locally bounded, we can construct the process as

where , is a point process on with stochastic intensity and, conditionally on , has density , independently of any other process.

Unlike the just described processes with finite jump activity (i.e., finitely many jumps during any bounded time period), infinite jump activity (IJA) processes are important not only from a mathematical but also practical point of view. This is especially true in financial applications where several statistical tests, based on high-frequency observations, have supported the latter feature. In this work, we study a class of IJA processes (i.e., ) that arises as the thinning of a local jump-diffusion process driven by a Lévy process with stable-like small jump behavior.

An important obstacle for the application of the class of processes described above arise from the lack of tractable transition distributions. In this regard, one stream of the literature has focused on numerical methods for the computational simulation of the process (see, e.g., [13] and [21] and references therein), which in turn can be used to estimate different distributional features via Monte Carlo methods. Another stream of the literature has developed approximations for those distributional properties under different asymptotic regimes. Approximations in short-time are of particular relevance due to their wide range of applications such as statistical estimation and simulation methods. The latter approach was further developed by Figueroa-López, et al. [10], where a second order expansion, in small time, for the tail probability of the process (1.4) was developed. Unfortunately, there is almost no work dealing with short-time approximation methods for the distributional properties of state-dependent jump-diffusion. An exception is [24], where a short-time approximation scheme for the transition densities was developed in the special case that with .

In this article, we generalize the result in [10] by developing a second-order expansion, in small time , for the tail probability () of a state-dependent jump-diffusion process with generator (1.1) and initial value . One of the main motivations for considering both the infinitesimal generator (1.1) and the tail probabilities is their role in the evaluation of out-of-the-money (OTM) European call option prices when the underlying stock price is modeled as the exponential of a state-dependent jump-diffusion under a risk-neutral probability measure:

| (1.5) |

where has initial value and the log-moneyness is such that . An appealing method for evaluating (1.5) is to consider the so-called share measure (cf. [5]), defined as . In that case, the following neat representation for in terms of two tail probabilities holds:

| (1.6) |

When is a Lévy process, it turns out that the law of under is again Lévy, albeit with different Lévy triplet, and the same small-time expansion for the tail probability can be used to deal with the two terms in (1.6) and obtain an expansion for option price (cf. [11]). For a general process with generator (1.1), the law of under is still Markovian with the same generator form (1.1) but replacing and with

| (1.7) |

respectively. Note that, in particular, even if the jump dynamics of were not state-dependent (i.e., ), would still be state-dependent under (i.e., would depend on ). This motivates us to study at once the unifying framework (1.1), which, as explained above, is important in their own right.

Our main results explicitly quantify the effect of the jump state-dependence in the leading and second order terms of the tail probability and OTM call option premium in a small-time setting. Hence, for instance, when (in which case really measures the intensity of jumps with size near when the process’ state is ), the effect of a positive constant drift is to change the probability of a large move of more than within time by

| (1.8) |

Similarly, a nonzero constant volatility will change the probability of a large move of more than by

| (1.9) |

and the OTM call option premium (1.5) by

| (1.10) |

which extends a result in [11] for exponential Lévy models.

Our approach to obtain the expansion of the tail probabilities of follows along the same lines of [10] building on a small-large jump decomposition of the process , similar to that introduced by [18]. An essential ingredient of this method is to show that the small-jump component is a diffeomorphism, which presents some interesting subtleties in the considered model. More concretely, to obtain the latter property under the new state-dependent jump structure, we prove that the state-dependent small jump component has the same law as a regular (i.e., state-free) jump-diffusion with sufficiently regular coefficients (see Section 4 for details). Another novelty in this work is a new, much simpler, proof for estimating the tail probability of the so-called one-jump process (the process conditionally on having one big jump at a specified time) based on the just mentioned diffeomorphism property, time-reversibility, and a suitable application of an iterated Dynkin’s formula (see Lemma 5.1 for details).

The paper is organized as follows. In Section 2, we formally define the model together with the standing assumptions throughout the article. Section 3 introduces some needed notations and probabilistic tools. The key ingredients to obtain the main result are presented in Sections 4 and 5. The second-order expansion for the tail probability is presented in Section 6, while the application thereof to option pricing is developed in Section 7. Finally, Section 8 presents a numerical example to illustrate the performance of the expansions. To this end, we also develop a simulation method for our state-dependent local jumps-diffusion model based on a suitable diffusive approximation of the small jump component of the process. Finally, all the proofs are deferred to several Appendix sections.

General Notation: Throughout, given an Euclidean domain , (resp., ) represents the class of -times differentiable (resp., bounded and -times differentiable) functions with continuous and bounded partial derivatives of order . In particular, . Also, and respectively denote the derivative and the n-th order partial derivative operator with respect to the i-th variable of a multivariate function.

2 Setup and assumptions

In this section, we give a construction of the process of interest and establish the assumptions needed throughout. As mentioned in the introduction, we want to consider an infinite-jump activity Markov process with infinitesimal generator (1.1). We use a thinning technique for the construction of the jump structure of based on the jumps of a suitable Lévy process . To this end, we imposed the following assumption:

-

(S1)

-

(i)

There exists a Lévy density dominating the jump intensity function ; i.e., , for all ;

-

(ii)

We also assume that and are and , respectively, for any and, furthermore,

-

(i)

A necessary and sufficient condition for the first requirement in the previous condition is that is a Lévy density. In that case, we can take ; however, in applications it may be more convenient to choose another whose associate Lévy process can be simulated more easily. The second condition therein imposes some regularity requirements. Note that indeed the derivatives of do appear in the expansions of the tail probability and OTM call option premium (see, e.g., (1.8)-(1.10)), which lead us to believe that some smoothness properties on are needed.

We are now ready to give the construction for . Throughout, we consider a filtered probability space equipped with a standard Brownian motion and an independent Poisson random measure on with mean measure . The compensated Poisson measure of is denoted by . Then, under the condition (S1-i), we have the following construction for the process :

| (2.1) | ||||

where is a thinning function that takes the form

| (2.2) |

Upon the existence and uniqueness of the solution to (2.1), the solution process would be Markovian with infinitesimal generator (1.1). The following conditions on , , and guarantee the well-posedness of (2.1) (as proved in Lemma 5.2 below) and other needed features of the process:

-

(S2)

-

(i)

The functions and belong to ;

-

(ii)

There exists a constant such that for all ;

-

(i)

-

(S3)

The function satisfies the following conditions:

-

(i)

It belongs to , and for all ;

-

(ii)

For all , for some constant ;

-

(iii)

For all , for some constant ;

-

(i)

Remark 2.1.

Some remarks are in order regarding the above conditions:

- 1.

- 2.

- 3.

- 4.

It is worth pointing out that Figueroa-Lopez et al. [10] imposed stronger regularity to the coefficients of their SDE. However, we shall see that most results therein are still valid under the milder regularities imposed in the present manuscript.

Remark 2.2.

As mentioned in the introduction, in the case that , for a Lévy density , we recover the model (1.4), which was studied in [10]. Even though it is not evident, under the condition (S3-ii), the law of the process (2.1) is actually equivalent to that of a process of the form (1.4) with suitably chosen coefficient functions and (see Remark 4.3 below for more details). However, the resulting is relatively intractable and does not meet the regularity conditions of [10] for the second-order expansion therein to be applied directly. Furthermore, there are two other important reasons for directly considering the process (2.1). First, the process (2.1) allows the direct modeling and clearer interpretation of the intensity of jumps via the parameter , which is somehow hidden inside the function in the model (1.4). Second, as already mentioned in the introduction, in order to develop the small-time expansion of out-of-the-money option prices, one needs to deal with processes having the most general generator (1.1), even if the original process is of the form (1.4).

Our final assumption is probably the less intuitive. As mentioned in the introduction, there are two key ingredients in our approach to obtain the small-time expansion of the tail probability of . First, we use a small-large jump decomposition of the process . Second, we need that the small-jump component is a diffeomorphism. To this end, we use the equivalence of the resulting state-dependent small-jump model to a state-free jump diffusion process of the form (1.4), which is possible in light of the above Condition (S3-ii), as described in the previous Remark 2.2. However, to conclude that a model of the form (1.4) is a diffeomorphism, we need some regularity conditions on its coefficients. The main goal of the the following relatively mild condition is to establish such conditions (see Proposition 4.1 below). We refer to the Remark 4.2 below for further discussion and possible relaxation of this condition.

-

(S4)

The Lévy density h introduced in the Condition (S1) is such that, for some , is differentiable in , for some , and

‘

3 Some needed notations and preliminary results

Let be a pure-jump Lévy process with Lévy triplet , for the truncation function . The jump measure of the process is denoted by , where are the atoms of the measure . In that case, the Poisson random measure in (2.1) has the same distribution as a marked point process on , with marks being a random sample from a standard uniform distribution on .

In the sequel, the process is decomposed, in law, into a process with small jumps and an independent process of finite jump activity. To formally define the small-jump component of , we first need to introduce a suitable construction for the Poisson random measure . For any , let

where is a “truncation” function such that , is non-decreasing as increases, and . Next, let and be independent pure-jump Lévy processes, with respective Lévy triplets and , for the truncation function , where . Note that is a compound Poisson process, and we shall denote its intensity by , and the jump probability density function by . Let , , and denote, respectively, the jump times, jump counting process of , and an independent identically distributed random sample from the probability density function . Also, and represent a generic random variable uniformly distributed in and a generic random variable with the probability density function , respectively.

The lemma below from [10] will be useful in the sequel.

Lemma 3.1.

Under the conditions (S1) and (S3) in section 2, the following statements hold:

-

1.

Let . Then, for each , the mapping (resp., ) is invertible and its inverse (resp., ) belongs to .

-

2.

Both and admit densities, denoted by and , respectively, which belong to . Furthermore, they have the representations:

-

3.

The mapping admits an inverse, denoted hereafter by , that belongs to .

Now, we are ready to define the “small-jump component” of . Let denote the jump measure of the process , and let (resp. ) denote the marked point process (resp. compensated marked point process) on the atoms of with independent uniformly distributed marks on . For each , we construct a process , defined as the solution of the SDE

| (3.1) | ||||

where is a Wiener process independent of , and

| (3.2) |

By comparing their infinitesimal generators, it is not hard to see that the process (3.1) has the same distribution law as the process (2.1) (see Section 2 of [10] for a more detailed explanation). Next, we let be the solution of the SDE:

| (3.3) | ||||

The law of the process above can be interpreted as the law of conditioning on not having any jumps. Note that, by conditions (S2) and (S3-i), the process (3.3) is a local martingale with bounded drift whose jumps are bounded by a constant. With equation (9) in [19] followed by the proofs of Proposition 3.1 and Lemma 3.2 in [10], we have

| (3.4) |

for any , where can be made arbitrarily large by taking small enough.

We now proceed to define other related processes. For a collection of times , let be the solution of the SDE:

The law of the process can be interpreted as the law of conditioning on having jumps at the times .

For future reference, let us remark that the infinitesimal generator of the small-jump component , hereafter denoted by , can be written as

| (3.5) | ||||

where is defined in (3.2) and . Note that, for , can be written as

| (3.6) | ||||

which is finite and bounded due to the conditions (S1-i) and (S3-i).

The following first and second order Dynkin’s formula for the process will be needed in the sequel:

| (3.7) | ||||

| (3.8) |

Furthermore, for (resp., ), (resp., ) and, thus, the reminders in (3.7) (resp., (3.8)) is (resp., ) uniformly on and . The proofs of (3.7)-(3.8) follows from Itô’s formula and goes along the same lines as in the proof of Lemma 3.3 in [10].

4 A weak solution process

The main purpose of this section is to introduce an approach to overcome the difficulties posed by the discontinuous jump component in (3.1) and (3.3). To this end, we first show that the state-dependent local jump diffusions (3.1) and (3.3) are equivalent to a state-free local jump-diffusion of the form (1.4) and prove some needed regularity on its coefficients.

Note that the process is a semimartingale (see, e.g., [15, III.2.18]) and, furthermore, comparing the generator (3.9) to that in [15, IX.4.6], it is a homogeneous diffusion process with jumps as defined in [15, IX.4.1]. Then, we can determine the semimartingale characteristics of , relative to the identity truncation function, as

| (4.1) |

By Definition III.2.24 and Theorem III.2.26 in [15], a semimartingale with characteristics specified by (4.1) is a weak solution of the SDE

| (4.2) |

where, under the solution measure in the canonical space , is a one-dimensional Wiener process, is an independent Poisson random measure on with intensity measure and corresponding compensated measure . Here, is a positive -finite measure on to be chosen below, while is a Borel function implicitly determined by , , and via the equation

| (4.3) |

where we recalled from (3.10) that . In what follows, we take

for , with given as in Condition (S4).

In order to identify the function corresponding to the above measure , we introduce the following functions and :

| (4.4) |

Note that the restrictions of the two mappings and on are strictly increasing and one-to-one, with range . Thus, they admit “local” inverses defined on with range , hereafter, denoted by and , respectively.

From the form of the SDE (4.2) and the fact that the support of the mean measure of lies in , it is clear that the values of for are superfluous and we only need to define for . Let be defined as

| (4.5) |

In order to show that the above function satisfies (4.3), observe that, for each and , the mapping is strictly monotone and, thus, its inverse, hereafter denoted by , exists and satisfies

| (4.6) |

Then, and, from the definitions of and , we have the identity

Upon differentiation with respect to , we get

| (4.7) |

which implies (4.3) with the chosen measure .

We now proceed to show some needed regularity properties of the function , with which the almost sure existence of a stochastic flow of diffeomorphisms associated to the SDE (4.2) below is guaranteed by virtue of results in [3] (see Lemma 5.2 below). The proof of Proposition 4.1 is deferred to the Appendix A.1.

Proposition 4.1.

Remark 4.2.

The main purpose of the assumption (S4) in Section 2 is to simplify the verification of the regularity of as stated in Proposition 4.1. However, it is important to note that all what follows, including the main Theorem 6.1, hold true if and are such that the function satisfies the following conditions:

| (4.9) |

In particular, if , for an arbitrary Lévy density that is smooth enough outside any neighborhood of the origin, then (4.9) trivially holds true since . In that case, we recover the results in [10].

Remark 4.3.

Using similar arguments to those at the beginning of this section, it is not hard to check that, under the condition (S3-ii), the model (2.1) is equivalent in law to the model (1.4) with replaced by an appropriate function . Concretely, we need to take

where

However, the regularity of is harder to study than that of the function in (4.5). Indeed, for instance, the first-order partial derivatives of the function are given by

and the behavior of and as is now relevant as well.

5 Tail estimate for the one-big-jump process

In this section, we give an expansion for the tail probability of the process defined in (3.1) conditioned on having only one jump. The following lemma (proof in Appendix A.2) is a counterpart of Lemma A.1 in [10], even though the proof developed in the present article is new and much simpler. Below, we recall the notation and set

Lemma 5.1.

6 The second order expansion for the tail probability

In this section, we obtain a second order expansion, in a short time , for the tail probability for any . The idea is to exploit the equivalence in law of and the process defined in (3.1), and to condition on the number of jumps of . Specifically, we have

| (6.1) |

In order to present the expansion, let us first recall the notation and as well as the functions , , , and , introduced in Lemma 3.1. The following theorem (proof in Appendix A.4) states the main result of this article.

Theorem 6.1.

Remark 6.2.

- 1.

-

2.

The drift and diffusion are absent in the leading term, which can be interpreted by saying that a possible “big” move of the process in a short time happens mostly as a result of a “large” jump. This phenomenon also appears in the expansion of [10]. In the case that is interpreted as the probability density of a mark of the underlying marked point process driving , then .

-

3.

It is tedious but not hard to verify that the above expansion reduces to the expansion of [10] when , in which case the jump intensity does not depend on the state of the process .

-

4.

When and is small enough, the expansion reduces to

In particular, supposed that and are constants. Then, recalling that , the effect of a positive “drift” is to increase the probability of a “large” move of more than by

Note that the second term inside the parentheses above is missing in the absence of a state-dependent jump intensity. Similarly, a nonzero constant volatility will change the probability of a “large” move of more than by

in short-time. Again, the second term inside the parenthesis is the effect of a state-dependent intensity. For a general , it is also intuitive that the net effect depends on the average drift, , at the initial and final points and . The net effect of a general function on the probability of a large positive move of more than depends on the functional

as .

7 The small-time second-order expansion for OTM call prices

In this section, we derive a second-order expansion, in short-time, for the price of an out-of-the-money (OTM) European call option, with maturity and strike , written on a nondividend paying stock, whose risk-neutral price process is modeled by

where the process is given by (2.1) with the initial condition . For simplicity, in the rest of this section, we omit the superscript in .

As explained in the introduction, we shall consider the share measure associated with the stock (namely, the martingale measure obtained by taking the stock as numéraire) to evaluate the premium of the OTM option. Concretely, let be the so-called log-moneymess of this call option and as customary suppose that the risk-free rate is . Then, the price of this option can be written as

| (7.1) |

where is a probability measure, locally equivalent to , defined as for any -measurable set . Hereafter, denotes the corresponding expectation. For to be well-defined, must be a -martingale, for which we impose the following drift restriction:

| (7.2) |

The integral in (7.2) will be well defined under the conditions (S3-i) and (S1) in Section 2 as well as the condition:

That is a -martingale under (7.2) is a consequence of Itô’s formula.

The second-order expansion for the probability appearing on the second term of (7.1) was treated in Section 2. Next, we seek for a second order expansion in for the tail probability . To this end, we impose the following condition:

-

(S5)

The function introduced in Assumption (S4) is such that , where is defined by .

Our first task is to determine the infinitesimal generator of the process under . To that end, we compute the expectation

for an arbitrary function . Let . Then, applying Itô’s formula (see, e.g., [1] Theorem 4.4.7), , where

Thus,

where

Comparing the above formula to the Dynkin’s formula (3.7), we can then identify as the infinitesimal generator of under . Using the martingale condition (7.2), we can further write as

| (7.3) |

where

| (7.4) |

Note that under the Conditions (S3-i) and (S1) in Section 2, the integral appearing in (7.4) is well-defined and, furthermore, it is not hard to see that belongs to and can be written as

| (7.5) |

in light of (7.2).

In order to conclude the second-order expansion for the call option price, it remains to show that the measure satisfies the Conditions (S1) and (S4). This is obtained in the following result whose proof is deferred to Appendix A.5:

Corollary 7.1.

Finally, using the pricing formula for the European call option introduced at the beginning of this section, the price of an OTM European call option has the following expansion in a short maturity , for :

| (7.6) |

The formula (7.6) extends the first order expansion for the option price given in [10] for a non state-dependent jump intensity process (i.e., when ).

Remark 7.2.

-

1.

It is not surprising that the leading term is only determined by the jump component according to the formula

(7.7) In particular, if represents the premium of a call with expiration and strike and , (7.6)-(7.7) suggest that, for ,

thus, the curvature of the call premium is strongly determined by jump intensity .

-

2.

Plugging the expansion given in Remark 6.2-4 into (7.6) and using (7.2) and (7.4), we note that, when , the effect of a nonzero constant volatility in the price of an OTM call option is of order

which extends a result in [11] for exponential Lévy models. We again observe an additional contribution due to the state dependent feature of the model.

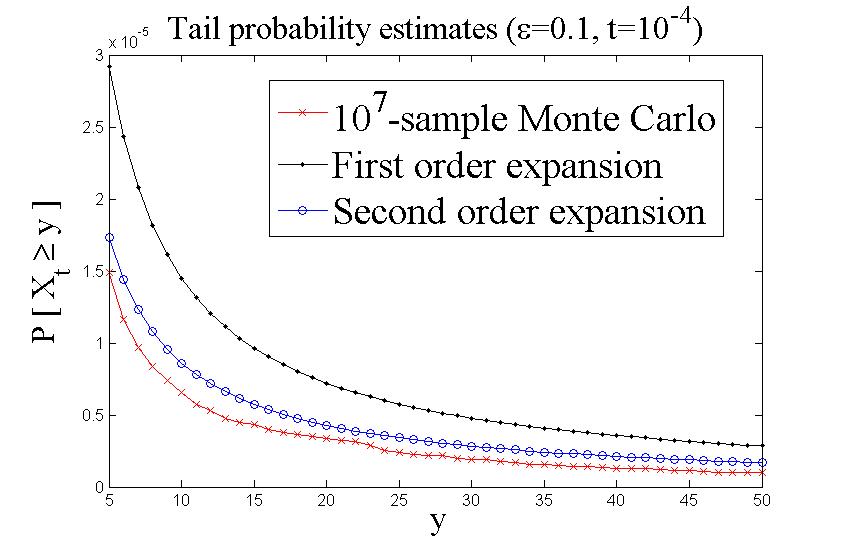

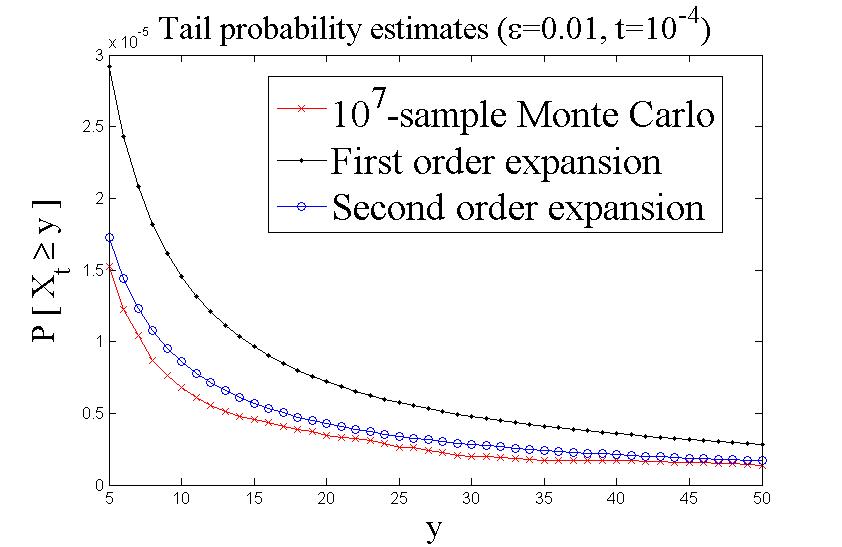

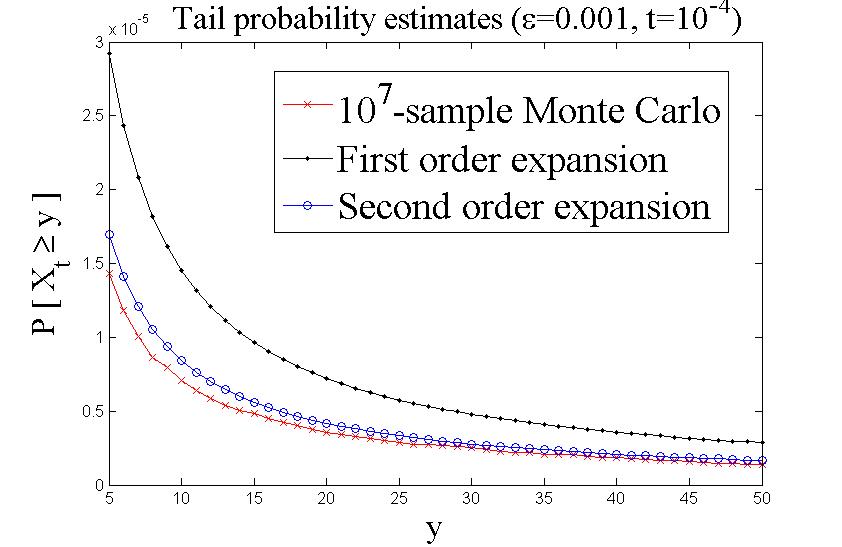

8 A numerical example of tail probability estimates

In this section, we show a comparison of numerical estimates for the tail probability by the first and the second order expansion in a small , and a Monte Carlo estimate based on the simulation of with a jump augmented Euler-Maruyama scheme (cf. [21]), combined with a diffusion approximation of the small-jump component of . For the numerical results, we use the following parameters

| (8.1) | ||||

which satisfy the conditions (S1)-(S4) in Section 2. For simplicity, we set , when computing the coefficients and in the expansion (6.2). This is valid since and don’t depend on and, thus, one can consider a sequence of smooth truncation functions, , that converges to , as .

8.1 Second order approximation for the tail probability

8.2 A Monte Carlo estimate of the tail probability

In the sequel, we present a numerical method to simulate the process defined in SDE (2.1). This is based on a diffusion type approximation of the “small-jump” component of the process together with a jump augmented Euler-Maruyama scheme (cf. [21]) for the “big-jump” component. To introduce the main idea, let us start by writing the infinitesimal generator of , defined in (1.1), as

| (8.2) |

for any and , where . Note that, as , the term in (8.2) can be approximated by

Therefore, for small, the generator is “close” to an operator on , defined as

| (8.3) |

where

The operator is the infinitesimal generator of a Markov process of finite jump activity. Indeed, as stated in Remark 7.2, condition (S3-i) implies that there exists an , depending only on and not on , such that , for all . Therefore, can be defined as the solution of the SDE:

| (8.4) |

where , , is a Wiener process, is an independent Poisson process with jump intensity and jump arrival times , are independent identically distributed with the probability density function , and is a random sample from a standard uniform distribution. The following result, whose proof is deferred to Appendix A.6, justifies that can be asymptotically approximated in law by , as .

8.3 Implementation and numerical results

By Lemma 8.1, we can approximate by simulating the process defined in (8.4). Since is a Poisson process with intensity , the inter-arrival jump times of (8.4) have independent identical exponential distribution with mean . Then, we generate the jump times by setting

where and is a random sample from the exponential distribution with parameter . Also, we use the inverse transformation sampling method to obtain a sample of the jumps . Finally, we construct over the jump-augmented time steps

The algorithm is similar to the one in [21] but with an additional thinning condition at each jump time .

Figures 8.1-Figure 8.3 show the tail probability estimated by the first and the second order expansions and the Monte Carlo approximation, for . We see that the second order expansion is indeed a better estimate than the first order expansion. We also observe that as , the second order expansion approaches to the Monte Carlo approximation and, furthermore, that the latter exhibit little variation for different , which in some sense justifies the diffusion approximation of the small-jump component of .

Appendix A Proofs

A.1 Proposition 4.1

Proof: The first assertion holds true since and and, thus,

This, shows that the function can continuously extended on by defining . Now, we proceed to show the first two assertions in (4.8) for any . We can similarly show the case . Throughout, we use the notation and recall that . For future reference, let us also note that, for any ,

| (A.1) |

because

and the function is chosen to be decreasing as increases.

We start to prove (4.8-i) for . To this end, note that and, by Condition (S3-i), it suffices to show that is bounded. By the definitions in Eq. (4.4) and recalling that and ,

| (A.2) |

for any . Note that, due to (A.1) and Conditions (S1-ii) and (S4), for small enough, and , for any . Using the latter and again (A.1), we conclude that

which, as discussed above, implies (4.8-i).

We proceed to show (4.8-ii), for . The case of follows from (4.8-i) by the mean value theorem and the fact that . For , note that . By Condition (S3-i) and (A.1),

for some constant . Similarly, since , it suffices to show that is bounded. To this end, note that

| (A.3) |

Since and are bounded for in a small neighborhood of the origin and, again, is decreasing in , for some constants and any ,

and one can use the same arguments as those in (A.2) to show that is bounded on and, hence, to conclude the validity of (4.8-i) for . For future reference, note that the previous arguments also show that is bounded on .

For , note can be decomposed as

The first three terms are trivially bounded by , for some constant , by Condition (S3-i), (A.1), and the boundedness of . It remains to show that is bounded. From straightforward differentiation,

We denote each of the three terms on the right hand side above , respectively, and analyze them separately. For the first term, we have:

which can clearly be proved to be bounded using analogous steps to those used for after Eq. (A.3). For the second term,

which is also clearly bounded since is bounded. For the third term,

The above derivatives with respect to generate the following simplified terms:

All the above terms are clearly bounded in light of the Conditions (S1-ii) and (S4) and the facts that and are bounded as already proved above.

A.2 Lemma 5.1

Proof: We want to obtain the second order expansion in of the function

| (A.4) |

where is the solution of (4.2), which has the same distribution law as . Let us start by representing (A.4) in terms of the density of , the inverse of the mapping , and the inverse of the diffeomorphism :

| (A.5) |

Let and recall from the proof of Lemma C.1 in [10] that is a solution to the SDE

where with being the inverse of the mapping . Above, and are the time-reversal processes of and the Lévy process (see, e.g., [22, Section VI.4] for information about time-reversibility). In particular, is a Wiener process, while is an independent Lévy process with the same law of (cf. Theorems VI.20 & VI.21 in [22]).

Next, we write (A.5) in the form:

where , and aim at applying the Dynkin’s formula (3.8) to deduce:

| (A.6) |

where is the infinitesimal generator of . We now proceed to justify (A.6) and the desired boundedness conditions (5.3). To this end, it is easy to see that the following two conditions are sufficient:

| (A.7) |

The condition (A.7-i) follows directly from Condition (S1) and Lemma 3.1. For the other condition in (A.7), let us note that (see [10, Eq. (3.5)])

| (A.8) | ||||

| (A.9) |

and . Clearly, the first two terms in belong to when , provided that , which holds true in light of Conditions (S1), (S2-i), and (S3-i). The boundedness of would hold true provided that and

| (A.10) |

for some constant . Since , it suffices to show that , where . Note that

which is bounded on by Proposition 4.1. The formal differentiation of yields

| (A.11) | ||||

and it is clear that for the derivative to be well-defined and bounded it suffices that , (A.10), and

| (A.12) |

Note that

which can be bounded by on by Proposition 4.1.

Formally differentiating (A.11), generates the following terms:

| (A.13) | ||||

The previous expression shows that in order for the second derivative to be well-defined and bounded it suffices that both conditions (A.10) and (A.12) are satisfied as well as

| (A.14) |

The latter condition again follows from Proposition 4.1 since, for ,

A.3 Lemma 5.2

Proof: Throughout the proof, we write . Let us start by noting that the SDE (4.2) satisfies the Hypotheses 5-9 in [3], with , , and , since obviously , for any , and, by Theorem 4.1, both

are bounded. Then, Theorem 5-10 in [3] guarantees the existence of a unique solution of (4.2). In turn the latter shows the existence of a unique weak solution for the SDE (3.3). Using an interlacing technique similar to that used in Theorem 6.2.9 of [1], one can proceed to show the existence of a unique weak solution to (3.1), which in turn implies the existence of a unique weak solution for the SDE (2.1).

To conclude that is a diffeomorphism, let us frame the family of solutions of the SDE (4.2) in the form (5-22) of [3], indexed by the initial state in a bounded neighborhood of , with , , and . First, note that the SDE (4.2) satisfies the conditions (i), (ii), and (iv) of [3, Hypothesis 5-23] since the coefficients , and are twice differentiable in and their respective partial derivatives with respect to are bounded in light of Assumptions (S1)-(S3) and Proposition 4.1. The assumption (iii) of [3, Hypothesis 5-23], and (i)-(ii) in [3, Theorem 5-24] are trivially satisfied since are deterministic functions independent of . Therefore, by Theorem 5.24 in [3], the mapping is differentiable and its derivative, is the unique solution of the SDE obtained by formal differentiation of (4.2):

| (A.15) |

Note that the coefficients of (4.2) are deterministic functions instead of stochastic processes, so the terms and in (5-25) of [3] are absent in (A.15) above. In particular, is given by

where . Due to (4.8), it is clear that, a.s., , for all . Hence, the mapping admits a differentiable inverse by the implicit function theorem, and, finally, is a diffeomorphism on .

A.4 Theorem 6.1

Proof: Throughout the proof, we only assume that and the function admits an extension on that is in , which is weaker than the technical assumption (S1) in Section 2.

The case .

Recalling that we denote the law of a process (respectively, the conditional law of given an event ) by (resp. ), we have

Consequently, the inequality (3.4) implies that

for any , where can be made arbitrarily large by taking small enough.

The case .

Conditioning on the time of the jump, we have

Let and denote, respectively, a random variable with density function and an independent random variable with standard uniform distribution on . Then, conditioning on , the integrand above can be written as follows:

where is an independent copy of . We denote the last two terms above by and , respectively. By the fact that and from the Markov’s property,

which can be made for any and an arbitrary large in light of (3.4). On the other hand,

where

Using Theorem 5.1, can be written as

| (A.16) |

where and are given in (5.2). By writing as and recalling from Lemma 3.1 that is and the regularity on imposed by (S1), it follows that is in . Then we can apply the second order Dynkin’s formula (3.8) to to get

| (A.17) |

where

| (A.18) | ||||

| (A.19) |

with

From the definition of , one can readily check that

| (A.20) | ||||

| (A.21) | ||||

| (A.22) | ||||

Next, in order to apply the first order Dynkin’s formula (3.7) to , we need to first show that the mapping belongs to . Since with by the regularity of in and by Lemma 3.1-1, we only need to show that . To this end, let us write

| (A.23) |

where

The representation (A.23) follows by the Taylor’s theorem and the fact that . Next, observe that is in since all the involved functions are . Therefore, standard applications of the dominated convergence theorem implies that is in and, furthermore,

Then, we apply the first order Dynkin’s formula (3.7) to :

| (A.24) |

where, using the following relationships obtained by implicit function theorem

we have

| (A.25) | ||||

Finally, substitute (A.17) and (A.24) into (A.16), we have

| (A.26) |

where and are given in (A.18), (A.19) and (A.25), respectively. Thus,

| (A.27) |

The case

Conditioning on the times of the jumps, we have

| (A.28) |

Denote the probability inside the integral above by . Below, let and () be independent copies of and , respectively. Denoting an independent copy of by and conditioning on , we have

| (A.29) |

where

We denote the last two terms on the right-hand side of (A.29) by and , respectively. Conditioning on , we can write as

| (A.30) |

where and are independent copies of . Using that and the Markov’s property, it is clear that

| (A.31) |

as , by taking small enough. To deal with the second term in (A.30), let us define

and note that

Using the facts that and , the last term above converges to as . Therefore, it suffices to study the asymptotic behavior of the expression

Using again that , and , uniformly in as ,

| (A.32) |

where

Using a similar argument as in the proof of Lemma 5.1,

| (A.33) |

where for small enough. Furthermore, the first term on the right-hand side of (A.33) can be expressed as

which is in . The previous fact together with Dynkin’s formula as well as (A.32)-(A.33) imply that

Using the change of variable and the representation

| (A.34) |

together with (A.30)-(A.31), we have

| (A.35) |

We next consider the second term, , in (A.29). By Lemma 5.1,

Conditioning on ,

| (A.36) | ||||

| (A.37) |

Let us denote the expressions in (A.36) and (A.37) by and , respectively. Next, since is ,

| (A.38) |

Using the facts that and , the last term above converges to uniformly in as . Therefore, recalling the definition of , we have

| (A.39) |

Since the expression inside the expectation above has partial derivative with respect to , uniformly bounded in , using again that uniformly in as ,

| (A.40) |

We next consider the term in (A.37). Using (A.38) again and an argument similar to that from (A.39) to (A.40), we deduce as follows.

| (A.41) |

where, in the last equality, we use the change of variable and the representation (A.34) of . Summing up (A.40) and (A.41), we have

| (A.42) | ||||

Therefore, summing up and from (A.35) and (A.42), with

| (A.43) | ||||

and, due to (A.28),

| (A.44) |

A.5 Corollary 7.1

Proof: Let us first note that, due to the Condition (S3-i),

for all and , where is defined as in Condition (S5). Next, define and note that, in view of the Condition (S5), is a valid Lévy density. Furthermore, clearly satisfies the other requirements of Condition (S4), while

can be readily seen to meet all the requirements of Condition (S1). The result is then a consequence of Theorem 6.1.

A.6 Lemma 8.1

Proof.

From the infinitesimal generators (8.2)-(8.3), we can identify the semimartingale characteristics and of and , respectively, relative to the truncation function :

| (A.45) | ||||

| (A.46) |

where , . We also define and as

| (A.47) | ||||

| (A.48) |

Clearly, for , and , in light of the definition of . Also,

for any bounded continuous function that vanishes in a neighborhood of the origin. Therefore, by [15, Theorem IX.4.15], provided that the uniqueness hypothesis [15, IX.4.3] holds true. By [15, Theorem III.2.26], the uniqueness requirement stated in [15, IX.4.3] is equivalent to the weak uniqueness of the solution for the SDE defining . This fact was established in Lemma 5.2. Therefore, we conclude the convergence result claimed in the lemma by [15, Theorem IX.4.15]. ∎

References

- [1] D. Applebaum. Lévy Processes and stochastic calculus. Second edition. Cambridge Studies in Advanced Mathematics, 116. Cambridge University Press, Cambridge, 2009. ISBN: 978-0-521-73865-1.

- [2] I. G. Becheri, F. C. Drost, and B. J. M. Werker. Asymptotic inference for jump diffusions with state-dependent intensity. working paper, available at http://ssrn.com/abstract=2292486

- [3] K. Bichteler, J. Gravereaux and J. Jacod. Malliavin calculus for processes with jumps, Gordon and Breach Science Publishers, New York, 1987. x+161 pp. ISBN: 2-88124-185-9.

- [4] P. Brémaud. Point processes and queues: martingale dynamics, Springer Series in Statistics. Springer-Verlag, New York-Berlin, 1981. xviii+354 pp. ISBN: 0-387-90536-7.

- [5] P. Carr and D. Madan. Saddlepoint methods for option pricing. The Journal of Computational Finance, Vol. 13 (2009), No. 1, pp. 49-61.

- [6] R. Cont and P. Tankov. Financial modelling with jump processes, Chapman & Hall/CRC Financial Mathematics Series. Chapman & Hall/CRC, Boca Raton, FL, 2004. xvi+535 pp. ISBN: 1-5848-8413-4.

- [7] D. J. Daley and D. Vere-Jones. An Introduction to the Theory of Point Processes, Volume I, Elementary theory and methods, Second edition, Probability and its Applications (New York). Springer-Verlag, New York, 2003. xxii+469 pp. ISBN: 0-387-95541-0.

- [8] D. Duffie and R. Kan. A yield-factor model of interest rates. [reprint of Math. Finance Vol. 6 (1996), No. 4, 379 C406]. Financial risk measurement and management, 736 C763, Internat. Lib. Crit. Writ. Econ., 267, Edward Elgar, Cheltenham, 2012.

- [9] D. Duffie and J. Pan. An overview of value at risk. [reprint of The Journal of Derivatives, Vol. 4 (1997), No. 3]. Financial risk measurement and management, 328 C370, Internat. Lib. Crit. Writ. Econ., 267, Edward Elgar, Cheltenham, 2012. DOI: 10.3905/jod.1997.407971.

- [10] J.E. Figueroa-López, Y. Luo, and C. Ouyang. Small-time expansions for local jump-diffusions models with infinite jump activity. Bernoulli, Vol. 20 (2014), No. 3, pp. 1165-1209.

- [11] J.E. Figueroa-López and M. Forde. The small-maturity smile for exponential Lévy models. SIAM Journal on Financial Mathematics, Vol. 3 (2012), No. 1, 33-65. DOI: 10.1137/110820658.

- [12] P. Glasserman and S. G. Kou. The term structure of simple forward rates with jump risk. Mathematical Finance, Vol. 13,(2003), No.3, pp. 383-410.

- [13] P. Glasserman and N. Merener. Convergence of a discretization scheme for jump-diffusion processes with state-dependent intensities. Stochastic analysis with applications to mathematical finance. Royal Society of London Proceedings Series A. Mathematics, Physics, Engineering, Science. Vol. 460 (2004), No. 2041, pp. 111-127.

- [14] P. Glasserman and N. Merener. Numerical solution of jump-diffusion LIBOR Market Models. Finance and Stochastics, Vol. 7 (2003), No. 1, pp 1-27.

- [15] J. Jacod and A. N. Shiryaev. Limit Theorems for stochastic processes. Second edition. Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences], 288. Springer-Verlag, Berlin, 2003. xx+661 pp. ISBN: 3-540-43932-3.

- [16] M. Johnes, R. Kumar and N. G. Polson. State Dependent Jump Models: How do US equity indices jump? availabe at 1997.http://faculty.chicagobooth.edu/nicholas.polson/research/papers/statedep.pdf

- [17] O. Kallenberg. Foundations of modern probability. Probability and its Applications (New York). Springer-Verlag, New York, 1997. xii+523 pp. ISBN: 0-387-94957-7.

- [18] R. Leandre. Densité en temps petit d’un processus de saut. (French) [Density of a jump process for small times]. Séminaire de Probabilités, XXI, 81 C99, Lecture Notes in Mathematics, 1247, Springer, Berlin, 1987.

- [19] J. P. Lepeltier and R. Marchal. Problémes de martingales associées à un opérateur integro différentiel. Annales de l’I. H. P., Section B, Vol. 12 (1976), No. 1, pp. 43-103.

- [20] M. Lorig, S. Pagliarani, and A. Pascucci. A family of density expansions for Lévy-type processes with default. To appear in Annals of Applied Probability, 2013 [arXiv1312.7328]

- [21] E. Mordecki, A. Szepessy, R. Tempone, G. E. Zouraris. Adaptive weak approximation of diffusions with jumps. SIAM Journal on Numerical Analysis, Vol. 46 (2008), No. 4, pp. 1732-1768.

- [22] P. Protter. Stochastic Integration and Differential Equations. Second edition. Stochastic Modelling and Applied Probability, 21. Springer-Verlag, Berlin, 2005. xiv+419 pp. ISBN: 3-540-00313-4.

- [23] K. Sato. Lévy Processes and Infinitely Divisible Distributions. Cambridge Studies in Advanced Mathematics, 68. Cambridge University Press, Cambridge, 2013. xiv+521 pp. ISBN: 978-1-107-65649-9 60G51 (60E07 60G18 60G52 60J45).

- [24] J. Yu. Closed-form likelihood approximation and estimation of jump-diffusions with an application to the realignment risk of the Chinese Yuan. Journal of Econometrics, Vol. 141 (2007), No.2, pp. 1245 C1280.