Change Points via Probabilistically Pruned Objectives

Abstract

The concept of homogeneity plays a critical role in statistics, both in its applications as well as its theory. Change point analysis is a statistical tool that aims to attain homogeneity within time series data. This is accomplished through partitioning the time series into a number of contiguous homogeneous segments. The applications of such techniques range from identifying chromosome alterations to solar flare detection. In this manuscript we present a general purpose search algorithm called cp3o that can be used to identify change points in multivariate time series. This new search procedure can be applied with a large class of goodness of fit measures. Additionally, a reduction in the computational time needed to identify change points is accomplish by means of probabilistic pruning. With mild assumptions about the goodness of fit measure this new search algorithm is shown to generate consistent estimates for both the number of change points and their locations, even when the number of change points increases with the time series length.

A change point algorithm that incorporates the cp3o search algorithm and E-Statistics, e-cp3o, is also presented. The only distributional assumption that the e-cp3o procedure makes is that the absolute th moment exists, for some . Due to this mild restriction, the e-cp3o procedure can be applied to a majority of change point problems. Furthermore, even with such a mild restriction, the e-cp3o procedure has the ability to detect any type of distributional change within a time series. Simulation studies are used to compare the e-cp3o procedure to other parametric and nonparametric change point procedures, we we highlight applications of e-cp3o to climate and financial datasets.

KEY WORDS: Dynamic Programming; Incomplete U-Statistics; Multivariate time series; Pruning

1 Introduction

The analysis of time ordered data, referred to as time series, has become a common practice in both academic and industrial settings. The applications of such analysis span may different fields, each with its own analytical tools. Such fields include network security (Blazek et al., 2001; Siris and Papagalou, 2006), fraud detection (Akoglu and Faloutsos, 2010; Fawcett and Provost, 1997), financial modeling (Andreou and Ghysels, 2002; Dias and Embrechts, 2004), climate analysis (Wang et al., 2013), astronomical observation (Friedman, 1996; Xie et al., 2013), and many others.

However, when analysis is performed it is generally assumed that the data adheres to some form of homogeneity. This could mean a range of things, depending upon the application area. Some common types of assumed homogeneity include: constant mean, constant variance, and strong or weak stationarity. Depending on the nature of these assumptions it may not be appropriate, or practical, to apply a given analytical procedure to many different types of time series. For instance, an algorithm that assumes weak stationarity would not be suitable for analyzing data that follows a Cauchy distribution, because of its infinite expectation. Furthermore many time series of real data can be seen, even through visual inspection, to violate such homogeneity conditions.

Results obtained under such model misspecification can vary in their degree of inaccuracy (Chong et al., 1995). The resulting bias from such misspecification is one of the reasons for the current resurgence of change point analysis. Change point analysis attempts to partition a time series into homogeneous segments. Once again the definition of homogeneity will depend upon the application area. In this paper we will use a notion of homogeneity that is common in the statistical literature. We will say that a segment is homogeneous if all of its observations are identically distributed. Using this definition of homogeneity, change point analysis can be performed in a variety of ways.

In this paper we consider the following formulation of the offline multiple change point problem. Let be a length sequence of independent -dimensional time ordered observations. The dimension of our observations is arbitrary, but assumed to be fixed. Additionally, let be a (possibly infinite) sequence of distributional functions, such that It is also assumed that in the sequence of observations, there is at least one distributional change. Thus, there exists time indices , such that , for . From this notation it is clear that the locations of change points depend upon the sample size. However, we will usually suppress this dependence and use the notation for simplicity. The challenge of multiple change point analysis is to provide a good estimate of both the number of change points, , as well as their respective locations, . In some cases it is also necessary to provide some information about the distributions . However, once a segmentation is provided it is usually straight-forward to obtain such information.

A popular approach is to fit the observed data to a parametric model. In this setting a change point corresponds to a change in the monitored parameter(s). Earlier work in this area assumes Gaussian observations and proceeds to partition the data through the use of maximum likelihood (Maboudou-Tchao and Hawkins, 2013). More recently, extensions to other members of the Exponential family of distributions and beyond have been considered (Chen and Gupta, 2011). In general, all of these approaches rely on the existence of a likelihood function with an analytic expression. Once the likelihood function is known, analysis is reduced to finding a computationally efficient way to maximize the likelihood over a set of candidate parameter values.

Parametric approaches however, rely heavily upon the assumption that the data behaves according to the predefined model. If this is not the case, then the degree of bias in the obtained results is usually unknown (Pitarakis, 2004). In practice, it is almost always difficult, if not impossible, to test for adherence to these assumptions. Under such settings, performing nonparametric analysis is a natural way to proceed (Brodsky and Darkhovsky, 1993). Since nonparametric approaches make much weaker assumptions than their parametric counterparts they can be used in a much wider variety of settings; for example, the analysis of internet traffic data, where there is no commonly accepted distributional model. Even though these methods do not directly impose a distributional model for the data, they do make their own types of assumptions (Zou et al., 2014). For instance, a common assumption is the existence of a density function, which then allows practitioners to perform maximum likelihood estimation by using estimated densities. However, estimation becomes inaccurate and time consuming when the dimension of the time series increases (Hastie et al., 2009).

Performing multiple change point analysis can easily become computationally intractable. Usually the number of true change points is not known beforehand. However, even if such information were provided, finding the locations is not a simple task. For instance, if it is known that the time series contains change points then there are possible segmentations. Thus naive approaches to find the best segmentation quickly become impractical. More refined techniques must therefore be employed in order to obtain change point estimates in a reasonable amount of time.

Most existing procedures for performing retrospective multiple change point analysis can be classified as belonging to one of two groups. The first consists of search procedures which will return what are referred to as approximate solutions, while the second consist of those that produce exact solutions. As indicated by the name, the approximate procedures tend to produce suboptimal segmentations of the given time series. However, their benefit is that they tend to have provably much lower computational complexity than procedures that return optimal segmentations.

Approximate search algorithms tend to rely heavily on a subroutine for finding a single change point. Estimates for multiple change point locations are produced by iteratively applying this subroutine. Such algorithms are commonly referred to as binary segmentation algorithms. In many cases it can be shown that binary segmentation algorithms have a complexity of . This type of approach to multiple change point analysis was introduced by Vostrikova (1981) and has since been adapted by many others. Such adaptations include the Circular Binary Segmentation approach of Olshen and Venkatraman (2004) as well as the E-Divisive approach of Matteson and James (2014). The Wild Binary Segmentation approach of Fryzlewicz et al. (2014) is a variation of binary segmentation that utilizes random intervals in an attempt to further reduce computational time. An extension of this approach to multivariate multiplicative time series called Sparsified Binary Segmentation has been produced by Cho and Fryzlewicz (2012). Each of these procedures have been shown to produce consistent estimates of both the number and locations of change points under a variety of model conditions.

Exact search algorithms return segmentations that are optimal with respect to a prespecified goodness of fit measure, such as a log likelihood function. The naive approach of searching over all possible segmentations quickly becomes impractical for relatively small time series with a few change points. Therefore, in order to achieve a reasonable computational cost, the utilized goodness of fit measures often satisfy Bellman’s Principle of Optimality (Bellman, 1952), and can thus be optimized through the use of dynamic programming. However, in most cases the ability to obtain this optimal solution comes with a computational cost. Usually this results in at least computational complexity. Examples of exact algorithms include the Kernel Change Point algorithm, (Harchaoui and Cappe, 2007) and (Arlot et al., 2012), and the MultiRank algorithm (Lung-Yut-Fong et al., 2011). The complexity of these algorithms also depends upon the number of identified change points. However, a method introduced by Jackson et al. (2005), as well as the PELT algorithm of Killick et al. (2012) can both obtain optimal segmentations with running times that are independent of the number of change points. An additional benefit of the PELT approach is that under certain conditions it is shown to have an expected running time that is linear in the length of the time series.

The second aspect of multiple change point analysis is the determination of the number of change points. The first technique that is commonly used by approximate search algorithms is hypothesis testing. This method continues to identify change points until they are unable to reject the null hypothesis of no change. Such an approach however, is not well suited for many procedures that use exact search algorithms, since many identify all change points at once, instead of sequentially, as is the case with binary segmentation. Many change point algorithms that use an exact search procedure instead turn to penalized optimization. The reasoning behind penalization is that a more complex model, in this case one with more change points, will better fit the observed data. The the penalty thus helps to guard against over segmentation. Yao (1987) showed that using the Schwarz Criterion can produce a consistent estimate of the number of change points. It has since become popular to maximize a penalized goodness of fit measure of the following form,

| (1) |

for a penalty function and measure of segmentation quality . A common choice for the penalty function is , for some user defined positive constant This type of penalization only takes into consideration the number of change points, and not their location. There are other penalization approaches that not only consider the number of change points, but also the change point locations. See for instance Zhang and Siegmund (2007) and Hannart and Naveau (2012).

An alternative to penalization is to instead generate all optimal segmentations with change points, up to some prespecified upper limit. This corresponds to evaluating from Equation 1 for a range of values. However, depending on the choice of it may not be possible to efficiently calculate for a range of values. And thus the search procedure would have to be run numerous times, which can become rather inefficient. Penalization tends to be faster, but does require the specification of a penalty function or constant. This choice is highly dependent upon the application field and will require some sort of knowledge about the data. Some ways to choose these parameters include cross validation (Arlot and Celisse, 2011), generalized degrees of freedom (Shen and Ye, 2002), and slope heuristics (Arlot and Massart, 2009). On the other hand, generating all optimal segmentations avoids having to make such a selection.

In the following sections we introduce a change point search procedure which we call cp3o (Change Points via Probabilisticly Pruned Objectives). This is an exact search procedure that can be applied to a larger number of goodness of fit measures in order to reduce the amount of time taken to estimate change point locations. Additionally, the cp3o algorithm allows for the number of change points to be quickly determined without having to specify a penalty term, while at the same time generating all other optimal segmentations as a byproduct.

As the cp3o procedure can be applied to a general goodness of fit measure we propose one that is based on E-Statistics Székely and Rizzo (2005), which we call e-cp3o. The e-cp3o method is a nonparametric algorithm that has the ability to detect any type of distributional change. The use of E-Statistics also allows the e-cp3o algorithm to perform analysis on multivariate time series without suffering from the curse of dimensionality.

The results from a variety of simulations show that our method makes a reasonable trade off between speed and accuracy in most cases. In addition to the computational benefits, we show that the cp3o procedure generates consistent estimates for both the number and location of change points when equipped with an appropriate goodness of fit measure. Furthermore, under additional assumptions we also show consistency in the setting where the number of change points is increasing with the length of time series.

The remainder of this paper is organized as follows. In Section 2 we discuss the probabilistic pruning procedure used by cp3o, along with conditions necessary to ensure consistency. Section 3 is devoted to the development of the e-cp3o algorithm and showing that it satisfies the conditions outlined in Section 2. Results for applications to both simulated and real datasets are given in Sections 4 and 5. Concluding remarks are left for Section 6.

2 Probabilistic Pruning

When performing change point analysis one must have a quantifiable way of determining whether one segmentation is better than another. When using an exact search procedure this is most commonly accomplished through the use of a goodness of fit measure. Suppose that there are change points . These locations partition the time series into segments . The challenge now is to select the change point locations so that the observations within each segment are identically distributed, and the distribution of observations in adjacent segments are different. Therefore, we will consider sample goodness of fit measures of the following form,

| (2) |

in which is a measure of the sample divergence between observation sets and . The divergence measure is such that larger values indicate that the distributions of the observations in the two sets are more distinct. Since each term of the sum in Equation 2 depends only upon contiguous observations it is possible to obtain the value of through dynamic programming.

Using traditional dynamic programming approaches greatly reduces the computational time required to perform the optimization in Equation 2. However, the running time of such methods is still quadratic in the length of the time series, thus limiting their applicability. Many of the calculations performed during the dynamic programs do not result in the identification of a new change point. These calculations can be viewed as excessive since they do not provide any additional information about the series’ segmentation, and quickly compound to slow down the algorithm. Thus a practical step towards reducing running time, and even possibly the theoretical computational complexity, is to quickly identify such excessive calculations and have them removed. One way to do this is by continually pruning the set of potential change point locations. Rigaill (2010) proposes a pruning method that can be used when the goodness of fit measure is convex, and can also be adapted for online change point detection. Since the sample divergence measure is not necessarily convex this pruning approach may not always be applicable. The cp3o procedure therefore performs pruning that is more in line with the approach taken by Killick et al. (2012) in developing the PELT method.

Let and for . Furthermore, suppose that there exists a constant such that

holds for all . The value of will depend not only on the distribution of our observations, but also the nature of the divergence measure . Therefore, in many settings it may be difficult, if not impossible, to find such a . Instead we consider the following probabilistic formulation. Let , we then wish to find such that for all

Let denote the value of when segmenting with change points. Using this notation we can express our probabilistic pruning rule as follows.

Lemma 1.

Let be the optimal change point location preceding , with . If

then with probability at least , is not the optimal change point location preceding .

Proof.

If

then from the definition of we have that

Since the optimal value attained from segmenting with change points is an upper bound for ,

From this we can see that with probability at least , it would be better to have as the change point prior to . ∎

2.1 Consistency

As has been mentioned before, when performing multiple change point analysis it is of utmost importance to obtain an accurate estimate of the number of change points, as well as their locations. Therefore, in this section we will show that under a certain asymptotic setting, the estimates generated by maximizing Equation 2 generate consistent location estimates.

When showing consistency many authors consider the case in which the number of change points is held constant, while the number of observations tends toward infinity. This seems rather unrealistic, as one would expect to observe additional change points as more data is collected. For this reason we will allow the number of change points, , to possibly tend towards infinity as the length of the time series increases. The asymptotic setting we will consider is similar in nature to that taken by Venkatraman (1992) and Zou et al. (2014).

In order to establish consistency of the proposed estimators we make the following assumptions.

Assumption 1.

Let be a collection of distribution functions, and a collection of doubly indexed positive finite constants. Suppose that and are disjoint sets of observations, such that the observations in have distribution and those of hare distribution , for The constants are such that almost surely as . Furthermore let be a function such that almost surely for all pairs and .

Assumption 2.

Let , and suppose as .

Assumption 2 states that the number of observations between change points tends towards infinity. This later allows us to apply the law of large numbers.

Assumption 3.

The number of change points and its upper bound are such that and .

The above assumption controls the rate at which the number of change points can increase. This is directly related to the rate at which our sample estimates converge almost surely to their population counterparts.

Assumption 4.

Let be the collection of distribution functions from Assumption 1. From this collection we define a set of random variables For each pair of values the random variable has a mixture distribution created with mixture components

Then for , and integers , define,

and for we define to be equal to . Assume that is such that as .

Assumption 4 concerns the rate at which additional change points increase the objective function of interest. We will show that a higher upper bound on the number of change points is necessary when each additional change point has the potential to greatly change the value of .

Assumption 5.

Let and be positive integers. Suppose that the time series is such that and for every sample of size . For we define the following sets and . Assume that there exist a class of functions indexed by , and ; such that almost surely as . Finally we assume that has a unique maximizer at .

Assumption 5 describes the behavior of our goodness of fit measure when it is used to identify a single change point. Essentially this assumption states that the measure will attain its maximum value when the estimated change point location, , and true change point location, , coincide.

Change Point Locations

We begin by showing that under Assumptions 1-5, the cp3o procedure will produce consistent estimates for the change point locations.

Lemma 2.

Let and

Then for all ,

as .

Proof.

Suppose that , then there exists such that Select the largest such and define the following random variables. Let where is the distribution (possibly a mixture) created by the observations between and , for having distribution created by the observations between and . Similarly define for the observations between and , and for the observations between and .

Then the value of the sample goodness of fit measure generated by the estimates of is

which due to Assumptions 1 and 3 is equal to

In the above expressions and are collections of terms that are not affected by the choice of . The and terms are as listed below.

Each of the terms in the sum is maximized when , which corresponds to By our assumptions, we have that the remainder term Therefore, if is strictly bounded away from then the statistic will be strictly less than the optimal value as . However, this contradicts the manner in which is selected. ∎

Number of Change Points

Once we have shown that the procedure generates consistent estimate for the change point locations it is simple to show that it will also produce a consistent estimate for the number of change points. We have chosen to implement the procedure outlined below in Assumption 6 to determine the number of change points. However, other approaches could be used and still have the same consistency result.

Assumption 6.

Define , and . Then suppose our estimated number of change points is given by

| (3) |

The selection procedure in Equation 3 has similar intuition to the one presented by Lavielle (2005). Both procedures work on the principle that a true change point will cause a significant change in the goodness of fit. While spurious change point estimates will only cause a minuscule increases/decrease in value. We thus say that a change is significant if it is more than half a standard deviation above the average change. As previously stated, other methods could be used, this just happens to be the one that we chose to implement.

Before proving that we can obtain a consistent estimate for the number of change points one final assumption is made to ensure that the detection of an additional true change point causes a strictly positive increase in our goodness of fit measure. A similar property is also needed for the finite sample approximation.

Assumption 7.

For every fixed , suppose the values form an increasing sequence. Similarly let be the finite sample estimates of . Additionally, suppose there exists such that for the values also form an increasing sequence.

Lemma 3.

Proof.

If is bounded then the proof for the constant version applies. Suppose that , then . Letting we note the following inequalities:

since for . Thus as .

Next suppose that . This implies that . However, since for , as . ∎

Theorem 4.

For all , as ,

3 Pruning and Energy Statistics

The cp3o procedure introduced in Section 2 can be applied with almost any goodness of fit measure . However, in order to ensure consistency for both the estimated change point locations, as well as the estimated number of change points, some restrictions must be enforced as outlined in Section 2.1.

In this section we make use of a particular class of goodness of fit measures that allows for nonparametric change point analysis. These measures are indexed by 222The choice of is allowed, however, in this case the goodness of fit measure would only be able to detect changes in mean. and allow for the detection of any type of distributional change. When a value of is selected, the only distributional assumptions that are made are that observations are independent and that they all have finite absolute th absolute moments. This class of measures are based upon the energy statistic of Székely and Rizzo (2005), and we thus call the resulting procedure e-cp3o.

The e-cp3o procedure is a nonparametric procedure that makes use of an approximate test statistic and an exact search algorithm in order to locate change points. Computationally the e-cp3o procedure is comparable to other parametric/nonparametric change point methodologies that use approximate search algorithms. In the remainder of this section we give a brief review of E-Statistics, followed by their incorporation into the cp3o framework. Finally, we show that the resulting goodness of fit measure satisfies the conditions necessary for consistency.

3.1 The Energy Statistic

As change point analysis is directly related to the detection of differences in distribution we consider the U-statistic introduced in Székely and Rizzo (2005). This statistic provides a simple way to determine whether the independent observations in two sets are identically distributed.

Suppose that we are given samples and , that are independent iid samples from distributions and respectively. Our goal is to determine if . We then define the following metric on the space of characteristic functions,

i which and are the characteristic functions associated with distributions and respectively. Also is a positive weight function chosen such that the integral is finite. By the uniqueness of characteristic functions, it is obvious that if and only if .

Another metric that can be considered is based on Euclidean distances. Let be an iid copy of , then for define

| (4) |

For an appropriately chosen weight function,

we have the following lemma.

Lemma 5.

For any pair of independent random variables and , and is such that , then and . Moreover, if and only if and are identically distributed.

Proof.

See the appendix of Székely and Rizzo (2005). ∎

3.2 Incomplete Energy Statistic

The computation of the U-statistics presented in Equation 5 require calculations, which makes it impractical for large or . We propose working with an approximate statistic that is obtained by using incomplete U-statistics. In the following formulation of the incomplete U-statistic let .

Suppose that we divide a segment of our time series into two adjacent subseries, and and define the following sets

The set aims at reducing the number of samples needed to compute the between sample distances. While the sets and reduce the number of terms used for the within sample distances. When making this reduction the sets and consider all unique pairs within a window around the split that creates and . This point corresponds to a potential change point location and thus we use as much information about points close by to determine the empirical divergence.

We then define the incomplete U-statistic as

| (6) |

Using this approximation greatly reduces our computational complexity from to . Nasari (2012) shows that a strong law of large numbers result holds for incomplete U-Statistics, and and thus and have the same almost sure limit as .

3.3 The e-cp3o Algorithm

We now present the goodness of fit measure that is used by the e-cp3o change point procedure. In addition, we show that the prescribed measure satisfies the necessary consistency requirements from Section 2.1.

The e-cp3o algorithm uses an approximate test statistics combined with an exact search algorithm in order to identify change points. Its goodness of fit measure is given by the following weighted U-Statistic,

| (7) |

Or an approximation can be obtained by using its incomplete counterpart

By using Slutsky’s theorem and a result of Székely and Rizzo (2010) we have that if then , and otherwise tends almost surely to a finite positive constant, provided that (this means that and ). In fact if we have that almost surely.

In the case of , the result of (O’Neil and Redner, 1993, Theorem 4.1) combined and Slutsky’s theorem show that under equal distributions, , Similarly, also tends towards a positive finite constant provided These properties lead to a very intuitive goodness of fit measure,

By using the dynamic programming approach presented by Lavielle and Teyssière (2006), the values for can be computed in instead of operations. However, the term makes this an inadequate approach, so the procedure (e-cp3o) is implemented with the similarly defined goodness of fit measure , which allows for only operations.

Consistency of e-cp3o

We now show that the goodness of fit measure, , used by e-cp3o satisfies the conditions for a cp3o based procedure to generate consistent estimates. It is assumed that has been chosen so that all of the th moments are finite. In the results below we will consider the goodness of fit measure based upon the complete U-Statistic, even though the e-cp3o procedure is based on its incomplete version . The reason for this is that and have the same almost sure limits, and we are working in an asymptotic setting.

Proposition 6.

Assumption 5 is satisfied by the e-cp3o goodness of fit measure.

Proof.

Using the result of (Matteson and James, 2014, Theorem 1) we have that

Such that and Therefore, and , which can be shown to have a unique maximizer at . ∎

Proposition 7.

The portion of Assumption 7 about holds for the e-cp3o goodness of fit measure.

Proof.

We begin by showing that . Suppose the first change point partitions the time series into two segments, one where observations are distributed according to and another where they are distributed according to . Now suppose that is a created by a linear mixture of the distributions and (which may themselves be mixture distributions). Suppose that the second change point is positioned so as to separate these distributions, and Let random variables and be such that and . Then we have that

where is the mixture coefficient used to create the distribution . It is clear that this will be maximized either when or , in either case we will show that the obtained value is bounded above by

Case : In this setting the value of is equal to the first term in the definition of , and since the distributions and are distinct, the second term is strictly positive. Thus .

Case : In this case . However, since we have a metric, the triangle inequality immediately shows that .

In the above setting the location of the first change point was held fixed when the second was identified. This need not be the optimal way to partition the time series into three segments. Thus since this potentially suboptimal segmentation results in an upper bound for it follows that the optimal segmentation will also bound .

The argument to show that for is identical. ∎

Proposition 8.

The portion of Assumption 7 about holds for the e-cp3o goodness of fit measure.

Proof.

In the paper Székely and Rizzo (2005), the empirical measure used for the statistic is based upon V-statistics, while we instead use U-statistics. The use of V-statistics ensures that the statistic will always have a nonnegative value. This isn’t the case when using U-statistics, but the difference in their value can be bounded by a constant multiple of . Combining this with the fact that , and , we conclude that for large enough the version of the statistics based on U-statistics will also produce nonnegative values. Therefore for large enough . ∎

4 Simulation Study

We now show the effectiveness of our methodology by considering a number of simulation studies. The goal of these studies is to demonstrate that the e-cp3o procedure is able to perform reasonably well in a variety of settings. In these studies we examine both the number of estimated change points as well as their estimated locations.

To assess the performance of the segmentation obtained from the e-cp3o procedure we use Fowlkes and Mallows’ adjusted Rand index (Fowlkes and Mallows, 1983). This value is calculated by comparing a segmentation based upon estimated change point locations to the known true segmentation. The index takes into account both the number of change points as well as their locations, and lies in the interval , where it is equal to if and only if the two segmentations are identical.

For each simulation study we apply various methods to 100 randomly generated time series. We then report the average running time in seconds, the average adjusted Rand value, and the average number of estimated change points.

As the simulations in the following sections will demonstrate, the e-cp3o procedure does not always generate the best running time or average Rand values. However, in every setting it generates results that are either better or comparable to almost all other competitors, when accuracy and speed are viewed together. For this reason we would advocate the use of the e-cp3o procedure as a general purpose change point algorithm, especially for small to moderate length time series.

To perform the probabilistic pruning introduced in Section 2 the value of must be specified. In our implementation we obtain an estimate of in the following way. We uniformly draw random samples from the set

For each sample we calculate

and then set equal to the quantile of these quantities. Any other sampling approach could be used to obtain a value for as long it satisfies the probabilistic criterion.

4.1 Univariate Simulations

We begin our simulation study by comparing the e-cp3o procedure to the E-Divisive and PELT procedures. These two procedures are implemented in the ecp (James and Matteson, 2014) and changepoint R packages respectively. This set of simulations consist of independent Gaussian observations which undergo changes in their mean and variance. The distribution parameters were chosen so that and . For each analyzed time series all of the different change point procedures were run with their default parameter values. For E-Divisive and e-cp3o this corresponds to . And for e-cp3o the minimum segment size was set to 30 observations (corresponding to ), and a value of is used for the probabilistic pruning. Since in this simulation study the number of change points increased with the time series length, the value of would also change. The results of these simulations are in Table 1, which also includes additional information about the time series and upper limit .

| PELT | E-Div | e-cp3o | |

| T=400, k(T)=3, K(T)=9 | |||

| Rand | |||

| # of cps | |||

| Time(s) | |||

| T=1650, k(T)=10, K(T)=50 | |||

| Rand | |||

| # of cps | |||

| Time(s) | |||

As can be seen from Table 1, better results are obtained by combining an exact test statistic with an approximate search algorithm. But these gains in segmentation quality are rather small. Thus, because of the increase in speed and small loss in segmentation quality, we would argue that the e-cp3o procedure should be preferred over the E-Divisive. The PELT procedure was much faster, but the e-cp3o procedure was able to generate segmentations that were similar in quality as measured by the adjusted Rand index.

The next set of simulations also compares to a nonparametric procedure from the npcp R package. This procedure, like the e-cp3o, is designed to detect changes in the joint distribution of multivariate time series. More information about this procedure, which we will denote by NPCP-F, is given in Section 4.2. Time series in this simulation study contain two changes in mean followed by a change in tail index. The changes in mean correspond to the data transitioning from a standard normal distribution to a and then back to standard normal. The tail index change is caused by a transition to a t-distribution with degrees of freedom. We expect that all three methods will be able to easily detect the mean changes and will have a more difficult time detecting the change in tail index. As with the previous set of simulations, all procedures are run with their default parameter values. Results for this set of simulations can be found in Table 2. Surprisingly, in this set of simulations the e-cp3o procedure was not only significantly faster than the E-Divisive and NPCP-F, but also managed to generate slightly better segmentations on average.

| NPCP-F | E-Div | e-cp3o | |

| T=400, k(T)=3, K(T)=9 | |||

| Rand | |||

| # of cps | |||

| Time | |||

| T=1600, k(T)=3, K(T)=9 | |||

| Rand | |||

| # of cps | |||

| Time | |||

These two simulation studies on univariate time series show that the e-cp3o procedure performs well when compared to other parametric and nonparametric change point algorithms. The first set of simulations showed that it generated segmentations whose quality is comparable to that of an efficient parametric procedure when its parametric assumptions were satisfied. While the second set of simulations showed that it is able to handle more subtle distributional changes, such as a change in tail behavior. The flexibility of the e-cp3o method allows for it to be used when parametric assumptions are met, as well as in settings where they aren’t sure to be satisfied.

4.2 Multivariate Simulations

We now examine the performance of the e-cp3o procedure when applied to a multivariate time series. Since a change in mean can be seen as a change in a marginal distribution we could just apply any univariate method to each dimension of the dataset. For this reason we will examine a more complex type of distributional change. In this simulation the distributional change will be due to a change in the copula function (Sklar, 1959), while the marginal distributions remain unchanged. Since the PELT procedure as implemented in the changepoint package only performs marginal analysis it is not suited for this setting, and will thus not be part of our comparison. We instead consider a method proposed by Gombay and Horvath (1999) and implemented in the R package npcp by Holmes et al. (2013). This package provides two methods that can be used in this setting. One that looks for any change in the joint distribution (NPCP-F) and one designed to detect changes in the copula function (NPCP-C).

For a given set of marginal distributions, the copula function is used to model their dependence. Thus a change in the copula function reflects a change in the dependence structure. This is of particular interest in finance where portfolios of dependent securities are typical (Guegan and Zhang, 2010).

In this simulation we consider a two dimensional process where both marginal distributions are standard normal. While the marginal distributions remain static, the copula function evolves over time. For this simulation the copula undergoes two changes. Initially it is a Clayton copula and then changes to the independence copula and finally becomes a Gumbel copula. The density function for each of the used copulas is provided in Table 3 and simulation results in Table 4.

| Copula | Density |

|---|---|

| Clayton | |

| Independence | |

| Gumbel |

| NPCP-C | NPCP-F | e-cp3o | |

| T=300, k(T)=2, K(T)=9 | |||

| Rand | |||

| # of cps | |||

| Time | |||

| T=1200, k(T)=2, K(T)=9 | |||

| Rand | |||

| # of cps | |||

| Time | |||

As was expected, in Table 4 it is clear that the NPCP-C method obtained the best average Rand value in all situations. But this comes at a much increased average running time. This becomes very problematic when analysis of a single longer time series can take almost three hours. For shorter time series the e-cp3o provides the best combination between running time, estimated number of change points, and Rand value. For longer time series the NPCP-F procedure is the clear winner.

5 Real Data

In this section we apply the e-cp3o procedure to two real data sets. For our first application we make use of a dataset of monthly temperature anomalies. The second second consists of monthly foreign exchange (FX) rates between the United States, Russia, Brazil, and Switzerland.

5.1 Temperature Anomalies

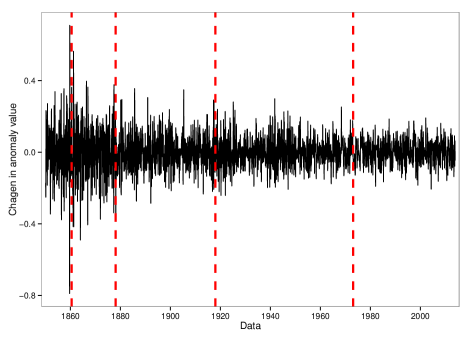

For the first application of the e-cp3o procedure we examine the HadCRUT4 dataset of Morice et al. (2012). This dataset consists of monthly global temperature anomalies from 1850 to 2014. Since the dataset consists of anomalies, it does not indicate actual average monthly temperatures, but instead measured deviations from some predefined baseline. The time period used to create the baseline in this case spans 1960 to 1990.

The HadCRUT4 dataset contains two major components; one for land air temperature anomalies and another for sea-surface temperature anomalies. The analysis performed in this section will only consider the land air temperature anomaly component from the tropical region ( South to North). This region was chosen because it was the most likely of all the presented regions to have a small difference between the minimum and maximum anomaly value, and be affected by changing seasons. More information about the dataset and the averaging process used can be found in the paper by Morice et al. (2012).

From looking at the plot of the tropical land air anomaly time series it is suspected that there is some dependence between observations. This assumption is quickly confirmed by looking at the auto-correlation plot. As a result, we apply the e-cp3o procedure to the differenced data which visually appears to be piecewise stationary. The auto-correlation plot for the differenced data shows that much of the linear dependence has been removed, however, the same plot for the differences squared still indicates some dependence. As with the exchange rate data, we believe that this indicated dependence can be attributed to changes in distribution.

The e-cp3o procedure was applied with a minimum segment length of one year, corresponding to ; a maximum of change points were fit, we chose , and . Upon completion we identified change points at the following dates: July 1860, February 1878, January 1918, and February 1973, which are shown in Figure 3. With these change points we notice that the auto-correlation plots, for both the differenced and squared differenced data, show almost no statistically significant correlations. This is in line with our original hypothesis that the previously observed correlation was due to the distributional changes within the data.

Furthermore, the February 1973 change point occurs around the same time as the United Nations Conference on the Human Environment. This conference, which was held in June 1972, focused on human interactions with the environment. From this meeting came a few noteworthy agreed upon principles that have potential to impact land air temperatures:

-

1.

Pollution must not exceed the environment’s ability to clean itself

-

2.

Governments would plan their own appropriate pollution policies

-

3.

International organizations should help to improve the environment

These measures, undoubtedly played a role in the decreased average anomaly size, as well as an almost decrease in the variance.

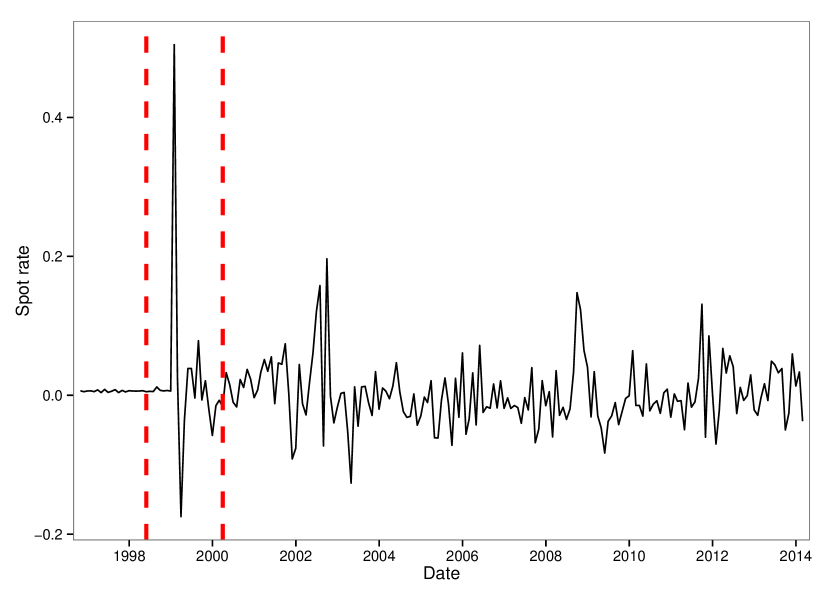

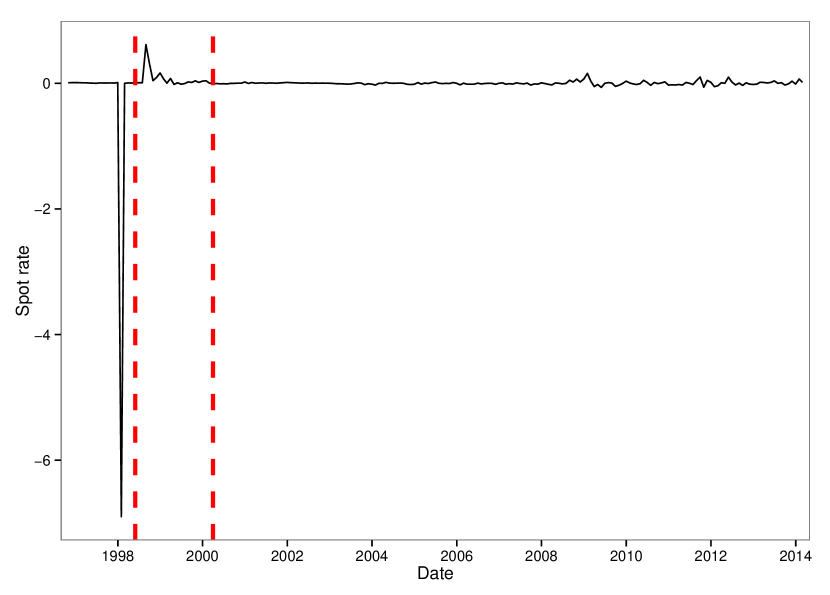

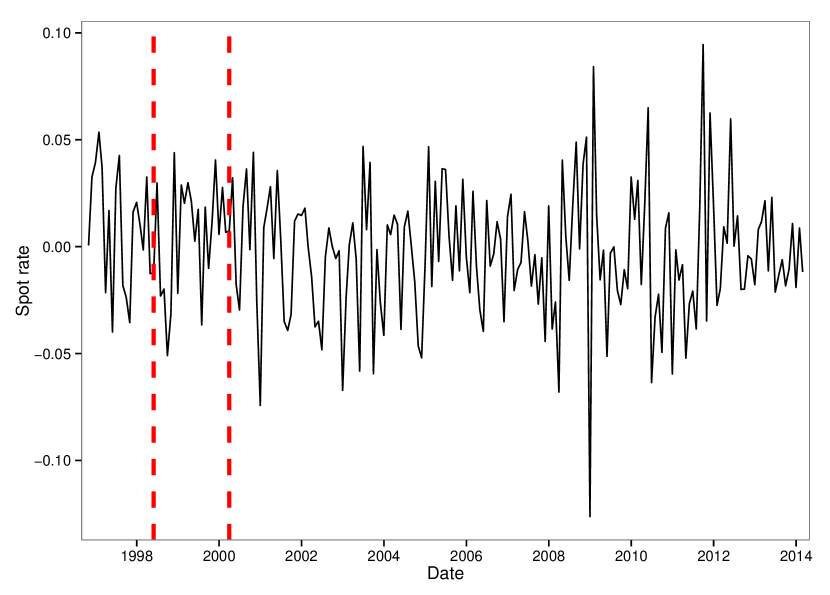

5.2 Exchange Rates

We next apply the e-cp3o procedure to a set of spot FX rates obtained through the R package Quandl (McTaggart and Daroczi, 2013). For our analysis we consider the three dimensional time series consisting of monthly FX rates for Brazil (BRL), Russia (RUB), and Switzerland (CHF). All of the rates are against the United States (USD). The time horizon spanned by this time series is September 30, 1996 to February 28, 2014, which results in a total of 210 observations. Looking at the marginal series it is obvious that each of the individual FX rates does not generate a stationary process. Thus, instead of looking at the actual rate, we look at the change in the log process. This transformation results in marginal processes that appear to at least be piecewise stationary.

Our procedure is only guaranteed to work with independent observations, so we must hope that our data either satisfies this condition or is very close to it. The papers by Hsieh (1988, 1989) provide evidence that changes in the daily exchange rate are not independent, and that there is a reasonable amount of nonlinear dependence. However, they are not able to conclude whether this observed dependence is due to distributional changes or some other phenomena. For this reason we are instead interested in the change in the monthly exchange rate, which is more likely to either be weakly dependent or show no dependence. To check this we examine the auto/cross-correlation plots for both the difference and difference squared data. This preliminary analysis shows that there is no significant auto or cross-correlation within the differenced data, while for the squared differences there is only significant auto-correlation for Switzerland at a lag of one month.

The e-cp3o procedure is applied with a minimum segment length of six observations (half a year), which corresponds to a value of . Furthermore, we have chosen to fit at most change points, and values of and were used. This specific choice of values resulted in change points being identified at May 31, 1998 and March 31, 2000. These results are depicted in Figure 4.

It can be argued that changes in Russia’s economic standing leading up to the 1998 ruble crisis are the causes of the May 31, 1998 change point. During the Asian financial crisis many investors were losing faith in the Russian ruble. At one point, the yield on government bonds was as high as . This paired with a inflation rate would normally have been an investor’s dream come true. However, people were skeptical of the government’s ability to repay these bonds. Furthermore, at this time Russia was using a floating pegged rate for its currency, which resulted in the Central Bank’s mass expenditure of USD’s which further weakened the ruble’s position.

The change point identified at March 31, 2000 also coincides with an economic shift in one of the examined countries. The country most likely to be the cause of this change is Brazil. In 1994 the Brazilian government pegged their currency to the USD. This helped to stabilize the county’s inflation rate; however, because of the Asian financial crisis and the ruble crisis many investors were averse to investing in Brazil. In January 1999 the Brazilian Central Bank announced that they would be changing to a free float exchange regime, thus their currency was no longer pegged to the USD. This change devalued the currency and helped to slow the current economic downturn. The change in exchange regime and other factors led to a debt to GDP ratio, besting the IMF target and thus increasing investor faith in Brazil.

6 Conclusion

We have presented an exact search algorithm that incorporates probabilistic pruning in order to reduce the amount of unnecessary calculations. This search method can be used with almost any goodness of fit measure in order to identify change points in multivariate time series. Asymptotic theory has also been provided showing that the cp3o algorithm can generate consistent estimates for both the number of change points as well as the change point locations as the time series increases, provided that a suitable goodness of fit measure is provided. Furthermore, the decoupling of the search procedure and the determination of the number of estimated change points allows for the cp3o algorithm to efficiently generate a collection of optimal segmentations, with differing numbers of change points. This is all accomplished without the user having to specify any sort of penalty constant or function.

By combining the cp3o search algorithm with E-Statistics we developed e-cp3o, a method to perform nonparametric multiple change point analysis that can detect any type of distributional change. This method combines an approximate statistic with an exact search algorithm. The slight loss in accurately estimating change point locations on finite time series is greatly outweighed by the dramatic increase in speed, when compared to similar methods that combine an exact statistic with an approximate search algorithm.

References

- (1)

- Akoglu and Faloutsos (2010) Akoglu, L., and Faloutsos, C. (2010), Event Detection in Time Series of Mobile Communication Graphs,, in Army Science Conference, pp. 77–79.

- Andreou and Ghysels (2002) Andreou, E., and Ghysels, E. (2002), “Detecting Multiple Breaks in Financial Market Volatility Dynamics,” Journal of Applied Econometrics, 17(5), 579–600.

- Arlot and Celisse (2011) Arlot, S., and Celisse, A. (2011), “Segmentation of the Mean of Heteroscedastic Data via Cross-Validation,” Statistics and Computing, 21(4), 613–632.

- Arlot et al. (2012) Arlot, S., Celisse, A., and Harchaoui, Z. (2012), “Kernel Change-Point Detection,” arXiv preprint arXiv:1202.3878, .

- Arlot and Massart (2009) Arlot, S., and Massart, P. (2009), “Data-driven Calibration of Penalties for Least-Squares Regression,” The Journal of Machine Learning Research, 10, 245–279.

- Bellman (1952) Bellman, R. (1952), “On the Theory of Dynamic Programming,” Proceedings of the National Academy of Sciences of the United States of America, 38(8), 716.

- Blazek et al. (2001) Blazek, R. B., Kim, H., Rozovskii, B., and Tartakovsky, A. (2001), A Novel Approach to Detection of Denial-of-Service Attacks via Adaptive Sequential and Batch-Sequential Change-Point Detection Methods,, in Proceedings of IEEE systems, man and cybernetics information assurance workshop, Citeseer, pp. 220–226.

- Brodsky and Darkhovsky (1993) Brodsky, E., and Darkhovsky, B. S. (1993), Nonparametric Methods in Change Point Problems, number 243 Springer.

- Chen and Gupta (2011) Chen, J., and Gupta, A. K. (2011), Parametric Statistical Change Point Analysis: With Applications to Genetics, Medicine, and Finance Springer.

- Cho and Fryzlewicz (2012) Cho, H., and Fryzlewicz, P. (2012), “Multiple Change-Point Detection for High-Dimensional Time Series via Sparsified Binary Segmentation,” Preprint, .

- Chong et al. (1995) Chong, T.-l. et al. (1995), “Partial Parameter Consistency in a Misspecified Structural Change Model,” Economics Letters, 49(4), 351–357.

- Dias and Embrechts (2004) Dias, A., and Embrechts, P. (2004), “Change-Point Analysis for Dependence Structures in Finance and Insurance,” in Risk Measures for the 21st Century, ed. G. Szegö Wiley.

- Fawcett and Provost (1997) Fawcett, T., and Provost, F. (1997), “Adaptive Fraud Detection,” Data Mining and Knowledge Discovery, 1(3), 291–316.

- Fowlkes and Mallows (1983) Fowlkes, E. B., and Mallows, C. L. (1983), “A Method for Comparing Two Hierarchical Clusterings,” Journal of the American Statistical Association, 78(383), 553–569.

- Friedman (1996) Friedman, P. (1996), A Change Point Detection Method for Elimination of Industrial Interference in Radio Astronomy Receivers,, in Statistical Signal and Array Processing, 1996. Proceedings., 8th IEEE Signal Processing Workshop on (Cat. No. 96TB10004, IEEE, pp. 264–266.

- Fryzlewicz et al. (2014) Fryzlewicz, P. et al. (2014), “Wild Binary Segmentation for multiple change-point detection,” The Annals of Statistics, 42(6), 2243–2281.

- Gombay and Horvath (1999) Gombay, E., and Horvath, L. (1999), “Change-points and Bootstrap,” Environmetrics, 10(6), 725–736.

- Guegan and Zhang (2010) Guegan, D., and Zhang, J. (2010), “Change Analysis of a Dynamic Copula for Measuring Dependence in Multivariate Financial Data,” Quantitative Finance, 10(4), 421–430.

- Hannart and Naveau (2012) Hannart, A., and Naveau, P. (2012), “An Improved Bayesian Information Criterion for Multiple Change-Point Models,” Technometrics, 54(3), 256–268.

- Harchaoui and Cappe (2007) Harchaoui, Z., and Cappe, O. (2007), Retrospective Multiple Change-Point Estimation with Kernels,, in Statistical Signal Processing, 2007. SSP ’07. IEEE/SP 14th Workshop on, pp. 768 –772.

- Hastie et al. (2009) Hastie, T., Tibshirani, R., Friedman, J., Hastie, T., Friedman, J., and Tibshirani, R. (2009), The Elements of Statistical Learning, Vol. 2 Springer.

- Holmes et al. (2013) Holmes, M., Kojadinovic, I., and Quessy, J.-F. (2013), “Nonparametric Tests for Change-point Detection à la Gombay and Horváth,” Journal of Multivariate Analysis, 115, 16–32.

- Hsieh (1988) Hsieh, D. A. (1988), “The Statistical Properties of Daily Foreign Exchange Rates: 1974–1983,” Journal of International Economics, 24(1), 129–145.

- Hsieh (1989) Hsieh, D. A. (1989), “Testing for Nonlinear Dependence in Daily Foreign Exchange Rates,” Journal of Business, 62(3), 339–368.

- Jackson et al. (2005) Jackson, B., Scargle, J. D., Barnes, D., Arabhi, S., Alt, A., Gioumousis, P., Gwin, E., Sangtrakulcharoen, P., Tan, L., and Tsai, T. T. (2005), “An algorithm for optimal partitioning of data on an interval,” Signal Processing Letters, IEEE, 12(2), 105–108.

-

James and Matteson (2014)

James, N. A., and Matteson, D. S. (2014), “ecp: An R Package for Nonparametric Multiple

Change Point Analysis of Multivariate Data,” Journal of Statistical

Software, 62(7), 1–25.

http://www.jstatsoft.org/v62/i07/ - Killick et al. (2012) Killick, R., Fearnhead, P., and Eckley, I. (2012), “Optimal Detection of Changepoints With a Linear Computational Cost,” Journal of the American Statistical Association, 107(500), 1590–1598.

- Lavielle (2005) Lavielle, M. (2005), “Using Penalized Contrasts for the Change-Point Problem,” Signal processing, 85(8), 1501–1510.

- Lavielle and Teyssière (2006) Lavielle, M., and Teyssière, G. (2006), “Detection of Multiple Change-points in Multivariate Time Series,” Lithuanian Mathematical Journal, 46(3), 287 – 306.

- Lung-Yut-Fong et al. (2011) Lung-Yut-Fong, A., Lévy-Leduc, C., and Cappé, O. (2011), “Homogeneity and Change-Point Detection Tests for Multivariate Data Using Rank Statistics,” arXiv:1107.1971, .

- Maboudou-Tchao and Hawkins (2013) Maboudou-Tchao, E. M., and Hawkins, D. M. (2013), “Detection of Multiple Change-Points in Multivariate Data,” Journal of Applied Statistics, 40(9), 1979–1995.

- Matteson and James (2014) Matteson, D. S., and James, N. A. (2014), “A Nonparametric Approach for Multiple Change Point Analysis of Multivariate Data,” Journal of the American Statistical Association, 109(505), 334 – 345.

-

McTaggart and Daroczi (2013)

McTaggart, R., and Daroczi, G. (2013), Quandl: Quandl Data Connection.

R package version 2.1.2.

http://CRAN.R-project.org/package=Quandl - Morice et al. (2012) Morice, C. P., Kennedy, J. J., Rayner, N. A., and Jones, P. D. (2012), “Quantifying Uncertainties in Global and Regional Temperature Change Using an Ensemble of Observational Estimates: The HadCRUT4 Data Set,” Journal of Geophysical Research: Atmospheres (1984–2012), 117(D8).

- Nasari (2012) Nasari, M. M. (2012), “Strong Law of Large Numbers for Weighted U-statistics: Application to Incomplete U-statistics,” Statistics & Probability Letters, 82(6), 1208 – 1217.

- Olshen and Venkatraman (2004) Olshen, A. B., and Venkatraman, E. (2004), “Circular Binary Segmentation for the Analysis of Array-Based DNA Copy Number Data,” Biostatistics, 5, 557 – 572.

- O’Neil and Redner (1993) O’Neil, K. A., and Redner, R. A. (1993), “Asymptotic distributions of weighted U-statistics of degree 2,” The Annals of Probability, pp. 1159–1169.

- Pitarakis (2004) Pitarakis, J.-Y. (2004), “Least Squares Estimation and Tests of Breaks in Mean and Variance Under Misspecification,” Econometrics Journal, 7(1), 32–54.

- Rigaill (2010) Rigaill, G. (2010), “Pruned Dynamic Programming for Optimal Multiple Change-Point Detection,” arXiv preprint arXiv:1004.0887, .

- Shen and Ye (2002) Shen, X., and Ye, J. (2002), “Adaptive Model Selection,” Journal of the American Statistical Association, 97(457), 210–221.

- Siris and Papagalou (2006) Siris, V. A., and Papagalou, F. (2006), “Application of Anomaly Detection Algorithms for Detecting SYN Flooding Attacks,” Computer communications, 29(9), 1433–1442.

- Sklar (1959) Sklar, M. (1959), Fonctions de Répartition à n Dimensions et Leurs Marges Université Paris 8.

- Székely and Rizzo (2005) Székely, G. J., and Rizzo, M. L. (2005), “Hierarchical Clustering Via Joint Between-Within Distances: Extending Ward’s Minimum Variance Method,” Journal of Classification, 22(2), 151 – 183.

- Székely and Rizzo (2010) Székely, G. J., and Rizzo, M. L. (2010), “Disco Analysis: A Nonparametric Extension of Analysis of Variance,” The Annals of Applied Statistics, 4(2), 1034–1055.

- Venkatraman (1992) Venkatraman, E. S. (1992), Consistency Results in Multiple Change-Point Problems, PhD thesis, to the Department of Statistics.Stanford University.

- Vostrikova (1981) Vostrikova, L. (1981), “Detection Disorder in Multidimensional Random Processes,” Soviet Math Dokl., 24, 55 – 59.

- Wang et al. (2013) Wang, H., Killick, R., and Fu, X. (2013), “Distributional Change of Monthly Precipitation Due to Climate Change: Comprehensive Examination of Dataset in Southeastern United States,” Hydrological Processes, .

- Xie et al. (2013) Xie, Y., Huang, J., and Willett, R. (2013), “Change-Point Detection for High-Dimensional Time Series with Missing Data,” Selected Topics in Signal Processing, IEEE Journal of, 7(1), 12–27.

- Yao (1987) Yao, Y. C. (1987), “Estimating the Number of Change-Points via Schwarz Criterion,” Statistics & Probability Letters, 6, 181 – 189.

- Zhang and Siegmund (2007) Zhang, N. R., and Siegmund, D. O. (2007), “A Modified Bayes Information Criterion with Applications to the Analysis of Comparative Genomic Hybridization Data,” Biometrics, 63(1), 22–32.

- Zou et al. (2014) Zou, C., Yin, G., Feng, L., Wang, Z. et al. (2014), “Nonparametric Maximum Likelihood Approach to Multiple Change-Point Problems,” The Annals of Statistics, 42(3), 970–1002.