Exact confidence intervals of the extended Orey index for Gaussian processes

Abstract

In this paper exact confidence intervals for the Orey index of Gaussian processes are obtained using concentration inequalities for Gaussian quadratic forms and discrete observations of the underlying process. The obtained result is applied to Gaussian processes with the Orey index which not necessarily have stationary increments.

Keywords: concentration inequality, confidence intervals, Gaussian processes with the Orey index, fractional Ornstein-Uhlenbeck process, sub-fractional Brownian motion

This research was funded by a grant (No. MIP-048/2014) from the Research Council of Lithuania.

AMS Subject Classification: primary 60G15; secondary 60F05, 60H07.

1 Introduction

Let be a second order stochastic process with the incremental variance function defined on with values

Denote by a class of continuous functions such that and , . For example, we can take or for . Set

and

where . Note that and . In paper [13] we used a narrower class of functions , i.e. such functions which additionally satisfy condition . This condition is not necessary for the existence of the Orey index. It is required only for consideration of almost sure asymptotic behavior of the second-order quadratic variations of Gaussian processes.

We give the following extension of the Orey index.

Definition 1 ([13])

Let be a second order stochastic process with the incremental variance function such that as . If for any function , then we say that the process has the Orey index .

Assume that for some the second order stochastic process satisfies conditions:

(C1) , i.e., and are of the same order as ;

(C2) there exist a constant such that

for every function .

If for some constant the second order stochastic process satisfies conditions and , then the Orey index is equal to (see [13]).

Recently much attention has been given to studies and applications of Gaussian processes such as fractional Brownian motion (fBm), sub-fractional Brownian motion (subfBm), bifractional Brownian motion (bifBm), fractional Ornstein-Uhlenbeck process. All of them are Gaussian processes and they have the Orey indexes. Consequently, examining Gaussian processes with the Orey index we thus examine the processes listed above.

Many authors (see [9], [10], [12], [8], [7], [1], [2], [17], [15]) considered an almost sure convergence and asymptotic normality of the generalized quadratic variations associated to the filter (see [12]) of a wide class of processes with Gaussian increments. The strong consistency of the Orey index estimator was proven in [13].

In the papers of Breton et al. [4] and Breton and Coeurjolly [5], an exact (non-asymptotic) confidence interval for the Hurst index of fBm was derived with the aid of concentration inequalities for quadratic forms of Gaussian process. The obtained confidence intervals for the Hurst parameter were based on a single observation of a discretized sample path of the interval of fBm. Exact confidence intervals for sub-fractional Brownian motion were considered in [14] but are not sufficiently precise.

The purpose of article is to extend the results of Breton et al. [4] and Breton and Coeurjolly [5] as well as to apply them to Gaussian processes with the Orey index which may not have stationary increments.

The paper is organized in the following way. In Section 2 we give exact confidence intervals for the Orey index of Gaussian process. Section 3 contains some application results for known Gaussian processes which may not have stationary increments. Finally, in Section 4 some simulations are given in order to illustrate the obtained results. In addition, Appendix includes the R code listings of simulations.

2 Confidence intervals

First, we formulate a concentration inequality for a family of Gaussian r.v.’s. Consider a finite centered Gaussian family , and write . Define two quadratic forms associated with and with some real coefficient :

| (1) |

The following statement characterizes the tail behavior of .

Theorem 2

Suppose that is not a.s. zero and fix and . Assume that , a.s.-. Then, for all , we have

Remark 3

[5] Note that (resp. ) is a bijective function from (resp. ) to .

Next, we apply the obtained concentration inequality to second order quadratic variations.

Let be a a centered Gaussian process satisfying conditions and with the Orey index . Denote , where

and is a constant defined in condition . Set .

Proposition 4

Assume that there exists a sequence of real numbers not depending on and such that

| (2) |

Then for all we have

where

Proof. Denote

and

Then

where

Thus

| (3) | |||

| (4) |

and the proof is completed.

Remark 5

For any and (), denote by and . For convenience we define

Note that Remark 3 above ensures that for any and for all , we have . Set

and

The function is a strictly increasing bijection from to if .

Theorem 6

Let . Assume that conditions of Proposition 4 are satisfied and there are constants such that . Then

where

Proof. Denote

where

Then

Note that

Thus

The proof is completed.

3 Applications

In this section we obtain the confidence intervals for subfBm, bifBm and the fractional Ornstein-Uhlenbeck process. For this purpose we apply the Theorem 6. In order to apply the Theorem 6, it suffices to find the sequence of real numbers in the estimation (2) and estimate . In the considered cases as the special case appears the Brownian motion. We exclude it from consideration in view of its properties (in particular, independent increaments). It is easy to see that

where and is Brownian motion.

3.1 Sub-fractional Brownian motion

Definition 7

([3]) A sub-fractional Brownian motion (subfBm) with the index , , is a mean zero Gaussian stochastic process with the covariance function

The case corresponds to the Brownian motion. For this process has some of the main properties of fBm, but its increments are not stationary.

The incremental variance function of subfBm is of the following form

| (5) |

For any the inequalities (see [3])

| (6) | |||

| (7) |

hold.

It is known that for subfBm the Orey index is equal to (see [13]). Now we prove the following lemma.

Lemma 8

Assume that is a subfBm. If then

where

Proof. Observe that the following equality

holds. Thus

For simplicity we shall omit the index for . Using computer modeling we obtain the inequalities

| (8) |

Let and denote , where is an integer part of . Then

It is clear that

Now we estimate for . Using the formula

we obtain

Note that the sign of is the same as that of . Thus

since

So

Let . It belongs to the class of functions . After putting into the obtained inequality we get

Lemma 9

Assume that is a subfBm. If then

| (9) |

where

Proof. The fourth order mixed partial derivative of the covariance function is of the following form

for each such that , where . Since the covariance function is continuous in and the derivative is continuous in then for and or

Assume that is the covariance function of the fBm . Then the derivative

of the covariance function is continuous in and

where

Note that and

for . Thus

It still remains to prove the cases when and or and . Set and . Since

then the inequality

holds. A similar argument yields

3.2 Bifractional Brownian motion

Definition 10

([11]) A bifractional Brownian motion (bifBm) with parameters and is a centered Gaussian process with the covariance function

It is known that for bifBm the Orey index is equal to (see [13]). If then bifBm becomes fBm, hence we ignore this case.

Lemma 11

Assume that is a bifBm with and . Then

where

Remark 12

Without this restriction for the expressions becomes more complicated.

Proof. The proof of the lemma follows the outlines of the proof of Lemma 8. Observe that the following equality

holds, where

By computer modeling we obtain inequalities

| (11) |

for all . Let and . Then

and

Using the inequality , , , and the formula

we obtain

Note that the sign of is the same as that of . Thus the estimate of depends on the signs of and . Then for and

Thus

Let . It belongs to the class of functions . After plugging it into the obtained inequality we get

Lemma 13

Assume that is a bifBm with and . Then

| (12) |

Proof. The fourth order mixed partial derivative of the covariance function has the form

for each such that , where

Since and , it follows that

| (13) | ||||

| (14) |

Let be a fBm with the Orey index . Assume that and or . Using the inequalities (13), (14) and

we obtain

for , where

So

The cases when and or and can be proven in a way analogous to that of subfBm. Next, we obtain

Since

then by the inequality (11) we get

Reasoning as in [5], Appendix A we obtain

Furthermore,

It is clear that

and

Thus

since the numerator of the second term is a decreasing function, and the numerator of the third term is an increasing function.

3.3 Ornstein-Uhlenbeck process

The fractional Ornstein-Uhlenbeck (fO-U) process of the first kind is the unique solution of the stochastic differential equation

| (15) |

with , where , , is a fBm. Its explicit solution is given by

where the integral exists as a Riemann-Stieltjes integral for all (see, e.g., [6]). First we show the following lemma.

Lemma 14

Let be the solution of equation (15). Assume that is a fBm with , where a real number is known. Then for

where and

Lemma 15

Let be the solution of the equation (15). Then

Proof. To prove this lemma, observe that

From the inequality

it follows that the statement of the lemma holds.

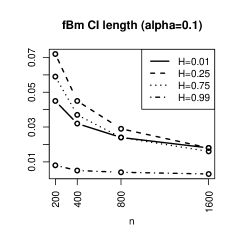

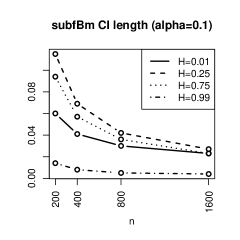

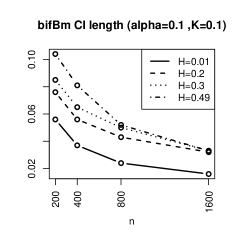

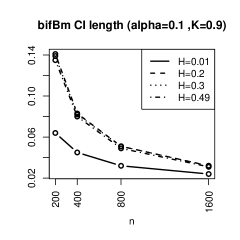

4 Simulations

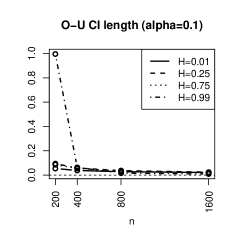

The simulations of the obtained confidence intervals presented below were performed using the R software environment [16]. Sample paths of fBm were generated using the circulant matrix embedding method and were further used to simulate the sample paths of the fractional Ornstein-Uhlenbeck process (15). The constants for the latter were (arbitrarily) chosen as and . Sample paths of the sub-fractional and bifractional Brownian motion were simulated using the Cholesky method. Due to the notable computational requirements of this method the maximum sample path length considered was . Figures presented below correspond to the case of the confidence level , . The observed coverage percentages in all cases were at least as good as claimed in Theorem 6.

Figures 2 - 6 present the confidence interval (CI) lengths for all the process types considered in this paper. Figure 6 shows the median ratios of the confidence intervals lengths, where the CI lengths of the subfBm, bifBm and fO-U processes were divided by the corresponding CI lengths of fBm. It can be seen that in almost all cases the confidence intervals behave in a similar way, one notable exception being the case of fO-U as the value of approaches 1. This is hardly unexpected given the normalization used in Lemma 14, and in this scenario the CI covers the whole interval of possible parameter values .

References

- [1] A. Bégyn, Quadratic variations along irregular partitions for Gaussian processes, Electronic Journal of Probability, 10 (2005), 691–717.

- [2] A. Bégyn, Asymptotic development and central limit theorem for quadratic variations of Gaussian processes, Bernoulli, 13(3) (2007), 712–753.

- [3] T. Bojdecki, L. G. Gorostiza, A. Talarczyk, Sub-fractional Brownian motion and its relation to occupation time, Stat. & Probab. Lett. 69 (2004), 405-419.

- [4] Breton J-C, Nourdin I, Peccati G., Exact confidence intervals for the Hurst parameter of a fractional Brownian motion. Electron J. Stat. 3, 416 425 (2009).

- [5] Breton J-C, J.-F. Coeurjolly, Confidence intervals for the Hurst parameter of a fractional Brownian motion based on finite sample size, Stat Inference Stoch Process (2012) 15, 1 26.

- [6] P. Cheridito, H. Kawaguchi, and M. Maejima, Fractional Ornstein-Uhlenbeck processes. Electronic Journal of Probability, 8, p. 1-14 (2003).

- [7] J.-F. Coeurjolly, Estimating the parameters of a fractional Brownian motion by discrete variations of its sample paths, Statistical Inference for Stochastic Processes, 4 (2001), 199–227.

- [8] A. Benassi, S. Cohen, J. Istas, and S. Jaffard, Identification of filtered white noises, Stochastic Processes and their Applications, 75 (1998), 31–49.

- [9] Gladyshev, E. G., A new Limit theorem for stochastic processes with Gaussian increments, Theory Probab. Appl., 6(1), p. 52-61, (1961).

- [10] X. Guyon and J. Léon. Convergence en loi des H-variations d’un processus gaussien stationnaire sur R. Ann. Inst. Poincaré, 25, p. 265-282 (1989).

- [11] C. Houdré and J. Villa, An example of infinite dimensional quasi-helix, Contemporary Mathematics 366 (2003), 195-201.

- [12] J. Istas, G. Lang. Quadratic variations and estimation of the local H older index of a Gaussian process. Ann. Inst. Henri Poincaré, Probab. Stat., 33, p. 407-436 (1997).

- [13] K. Kubilius, On estimation of the extended Orey index for Gaussian processes. To appear in Stochastics An International Journal of Probability and Stochastic Processes.

- [14] J. Liu, L. Yan, Z. Peng, and D. Wang, Remarks on confidence intervals for self-similarity parameter of a subfractional Brownian motion, Abstract and Applied Analysis, 2012, Article ID 804942, 14 pages (2012).

- [15] R. Malukas, Limit theorems for a quadratic variation of Gaussian processes, submited to Nonlinear Analysis: Modelling and Control.

- [16] R Core Team (2014), R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. URL http://www.R-project.org/.

- [17] R. Norvaiša, A coplement to Gladyshev’s theorem, Lith. Math. J., 51(1), 26-35 (2011).

- [18] R. Norvaiša, Gladyshev’s theorem for integrals with respect to a Gaussian process, Preprint, 2011.

Appendix. Code listings

genFBM.r

Cholesky.r

fbmCI.r

The following code evaluates the confidence intervals for the fractional Brownian motion. Simulations for other processes considered in this paper were performed in a similar way.