A New Perspective on Boosting in Linear Regression via Subgradient Optimization and Relatives

Abstract

In this paper we analyze boosting algorithms [21, 24, 15] in linear regression from a new perspective: that of modern first-order methods in convex optimization. We show that classic boosting algorithms in linear regression, namely the incremental forward stagewise algorithm () and least squares boosting (LS-Boost), can be viewed as subgradient descent to minimize the loss function defined as the maximum absolute correlation between the features and residuals. We also propose a modification of that yields an algorithm for the Lasso, and that may be easily extended to an algorithm that computes the Lasso path for different values of the regularization parameter. Furthermore, we show that these new algorithms for the Lasso may also be interpreted as the same master algorithm (subgradient descent), applied to a regularized version of the maximum absolute correlation loss function. We derive novel, comprehensive computational guarantees for several boosting algorithms in linear regression (including LS-Boost and ) by using techniques of modern first-order methods in convex optimization. Our computational guarantees inform us about the statistical properties of boosting algorithms. In particular they provide, for the first time, a precise theoretical description of the amount of data-fidelity and regularization imparted by running a boosting algorithm with a prespecified learning rate for a fixed but arbitrary number of iterations, for any dataset.

1 Introduction

Boosting [38, 19, 24, 39, 28] is an extremely successful and popular supervised learning method that combines multiple weak111this term originates in the context of boosting for classification, where a “weak” classifier is slightly better than random guessing. learners into a powerful “committee.” AdaBoost [20, 39, 28] is one of the earliest boosting algorithms developed in the context of classification. [6, 5] observed that AdaBoost may be viewed as an optimization algorithm, particularly as a form of gradient descent in a certain function space. In an influential paper, [24] nicely interpreted boosting methods used in classification problems, and in particular AdaBoost, as instances of stagewise additive modeling [29] – a fundamental modeling tool in statistics. This connection yielded crucial insight about the statistical model underlying boosting and provided a simple statistical explanation behind the success of boosting methods. [21] provided an interesting unified view of stagewise additive modeling and steepest descent minimization methods in function space to explain boosting methods. This viewpoint was nicely adapted to various loss functions via a greedy function approximation scheme. For related perspectives from the machine learning community, the interested reader is referred to the works [32, 36] and the references therein.

Boosting and Implicit Regularization

An important instantiation of boosting, and the topic of the present paper, is its application in linear regression. We use the usual notation with model matrix , response vector , and regression coefficients . We assume herein that the features have been centered to have zero mean and unit norm, i.e., for , and is also centered to have zero mean. For a regression coefficient vector , the predicted value of the response is given by and denotes the residuals.

Least Squares Boosting – LS-Boost

Boosting, when applied in the context of linear regression leads to models with attractive statistical properties [21, 28, 7, 8]. We begin our study by describing one of the most popular boosting algorithms for linear regression: LS-Boost proposed in [21]:

Algorithm: Least Squares Boosting – LS-Boost

Fix the learning rate and the number of iterations .

Initialize at , , .

-

1.

For do the following:

-

2.

Find the covariate and as follows:

-

3.

Update the current residuals and regression coefficients as:

-

-

and .

-

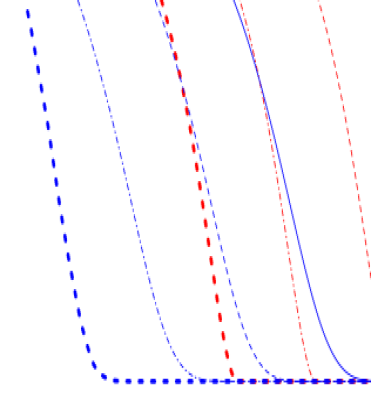

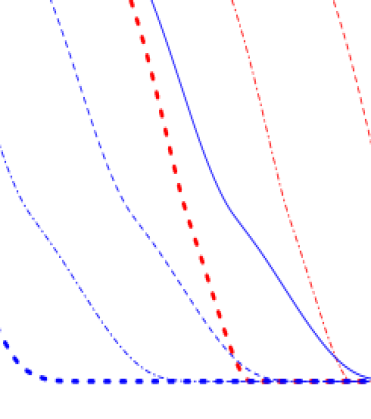

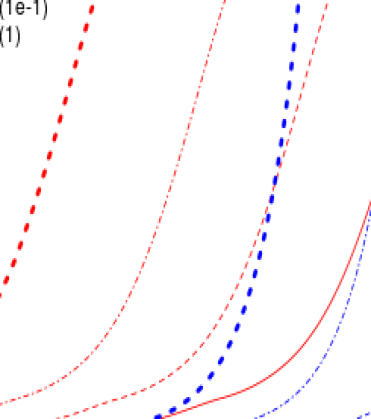

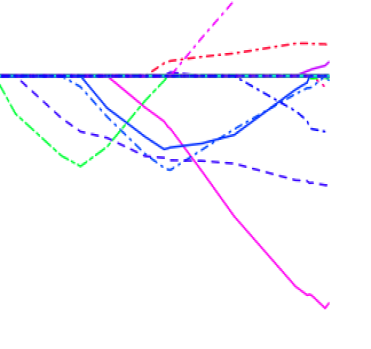

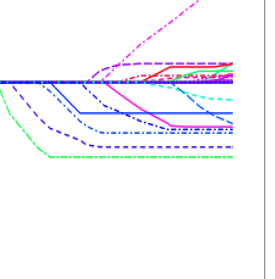

A special instance of the LS-Boost algorithm with is known as LS-Boost[21] or Forward Stagewise [28] — it is essentially a method of repeated simple least squares fitting of the residuals [8]. The LS-Boost algorithm starts from the null model with residuals . At the -th iteration, the algorithm finds a covariate which results in the maximal decrease in the univariate regression fit to the current residuals. Let denote the best univariate fit for the current residuals, corresponding to the covariate . The residuals are then updated as and the -th regression coefficient is updated as , with all other regression coefficients unchanged. We refer the reader to Figure 1, depicting the evolution of the algorithmic properties of the LS-Boost algorithm as a function of and . LS-Boost has old roots — as noted by [8], LS-Boost with is known as “twicing,” a method proposed by Tukey [42].

LS-Boost is a slow-learning variant of LS-Boost, where to counterbalance the greedy selection strategy of the best univariate fit to the current residuals, the updates are shrunk by an additional factor of , as described in Step 3 in Algorithm LS-Boost. This additional shrinkage factor is also known as the learning rate. Qualitatively speaking, a small value of (for example, ) slows down the learning rate as compared to the choice . As the number of iterations increases, the training error decreases until one eventually attains a least squares fit. For a small value of , the number of iterations required to reach a certain training error increases. However, with a small value of it is possible to explore a larger class of models, with varying degrees of shrinkage. It has been observed empirically that this often leads to models with better predictive power [21]. In short, both (the number of boosting iterations) and together control the training error and the amount of shrinkage. Up until now, as pointed out by [28], the understanding of this tradeoff has been rather qualitative. One of the contributions of this paper is a precise quantification of this tradeoff, which we do in Section 2.

The papers [9, 7, 8] present very interesting perspectives on LS-Boost, where they refer to the algorithm as -Boost. [8] also obtains approximate expressions for the effective degrees of freedom of the -Boost algorithm. In the non-stochastic setting, this is known as Matching Pursuit [31]. LS-Boost is also closely related to Friedman’s MART algorithm [25].

Incremental Forward Stagewise Regression –

A close cousin of the LS-Boost algorithm is the Incremental Forward Stagewise algorithm [28, 15] presented below, which we refer to as .

Algorithm: Incremental Forward Stagewise Regression –

Fix the learning rate and number of iterations .

Initialize at , , .

-

1.

For do the following:

-

2.

Compute:

-

3.

-

-

and .

-

In this algorithm, at the -th iteration we choose a covariate that is the most correlated (in absolute value) with the current residual and update the -th regression coefficient, along with the residuals, with a shrinkage factor . As in the LS-Boost algorithm, the choice of plays a crucial role in the statistical behavior of the algorithm. A large choice of usually means an aggressive strategy; a smaller value corresponds to a slower learning procedure. Both the parameters and the number of iterations control the data fidelity and shrinkage in a fashion qualitatively similar to LS-Boost . We refer the reader to Figure 1, depicting the evolution of the algorithmic properties of the algorithm as a function of and . In Section 3 herein, we will present for the first time precise descriptions of how the quantities and control the amount of training error and regularization in , which will consequently inform us about their tradeoffs.

Note that LS-Boost and have a lot of similarities but contain subtle differences too, as we will characterize in this paper. Firstly, since all of the covariates are standardized to have unit norm, for same given residual value it is simple to derive that Step (2.) of LS-Boost and lead to the same choice of . However, they are not the same algorithm and their differences are rather plain to see from their residual updates, i.e., Step (3.). In particular, the amount of change in the successive residuals differs across the algorithms:

| (1) |

where is the gradient of the least squares loss function . Note that for both of the algorithms, the quantity involves the shrinkage factor . Their difference thus lies in the multiplicative factor, which is for LS-Boost and is for . The norm of the successive residual differences for LS-Boost is proportional to the norm of the gradient of the least squares loss function (see herein equations (5) and (7)). For , the norm of the successive residual differences depends on the absolute value of the sign of the -th coordinate of the gradient. Note that depending upon whether is negative, zero, or positive; and only when , i.e., only when and hence is a least squares solution. Thus, for the norm of the difference in residuals is almost always during the course of the algorithm. For the LS-Boost algorithm, progress is considerably more sensitive to the norm of the gradient — as the algorithm makes its way to the unregularized least squares fit, one should expect the norm of the gradient to also shrink to zero, and indeed we will prove this in precise terms in Section 2. Qualitatively speaking, this means that the updates of LS-Boost are more well-behaved when compared to the updates of , which are more erratically behaved. Of course, the additional shrinkage factor further dampens the progress for both algorithms.

Our results in Section 2 show that the predicted values obtained from LS-Boost converge (at a globally linear rate) to the least squares fit as , this holding true for any value of . On the other hand, for with , the iterates need not necessarily converge to the least squares fit as . Indeed, the algorithm, by its operational definition, has a uniform learning rate which remains fixed for all iterations; this makes it impossible to always guarantee convergence to a least squares solution with accuracy less than . While the predicted values of LS-Boost converge to a least squares solution at a linear rate, we show in Section 3 that the predictions from the algorithm converges to an approximate least squares solution, albeit at a global sublinear rate.222For the purposes of this paper, linear convergence of a sequence will mean that and there exists a scalar for which for all . Sublinear convergence will mean that there is no such that satisfies the above property. For much more general versions of linear and sublinear convergence, see [3] for example.

Since the main difference between and LS-Boost lies in the choice of the step-size used to update the coefficients, let us therefore consider a non-constant step-size/non-uniform learning rate version of , which we call . replaces Step 3 of by:

- residual update:

-

- coefficient update:

-

and ,

where is a sequence of learning-rates (or step-sizes) which depend upon the iteration index . LS-Boost can thus be thought of as a version of , where the step-size is given by .

In Section 3.2 we provide a unified treatment of LS-Boost , , and , wherein we show that all these methods can be viewed as special instances of (convex) subgradient optimization. For another perspective on the similarities and differences between and LS-Boost , see [8].

|

Training Error |

|

|

|

|---|---|---|---|

|

norm of Coefficients |

|

|

|

Both LS-Boost and may be interpreted as “cautious” versions of Forward Selection or Forward Stepwise regression [33, 44], a classical variable selection tool used widely in applied statistical modeling. Forward Stepwise regression builds a model sequentially by adding one variable at a time. At every stage, the algorithm identifies the variable most correlated (in absolute value) with the current residual, includes it in the model, and updates the joint least squares fit based on the current set of predictors. This aggressive update procedure, where all of the coefficients in the active set are simultaneously updated, is what makes stepwise regression quite different from and LS-Boost — in the latter algorithms only one variable is updated (with an additional shrinkage factor) at every iteration.

Explicit Regularization Schemes

While all the methods described above are known to deliver regularized models, the nature of regularization imparted by the algorithms are rather implicit. To highlight the difference between an implicit and explicit regularization scheme, consider -regularized regression, namely Lasso [41], which is an extremely popular method especially for high-dimensional linear regression, i.e., when the number of parameters far exceed the number of samples. The Lasso performs both variable selection and shrinkage in the regression coefficients, thereby leading to parsimonious models with good predictive performance. The constraint version of Lasso with regularization parameter is given by the following convex quadratic optimization problem:

| (2) |

The nature of regularization via the Lasso is explicit — by its very formulation, it is set up to find the best least squares solution subject to a constraint on the norm of the regression coefficients. This is in contrast to boosting algorithms like and LS-Boost , wherein regularization is imparted implicitly as a consequence of the structural properties of the algorithm with and controlling the amount of shrinkage.

Boosting and Lasso

Although Lasso and the above boosting methods originate from different perspectives, there are interesting similarities between the two as nicely explored in [28, 15, 27].

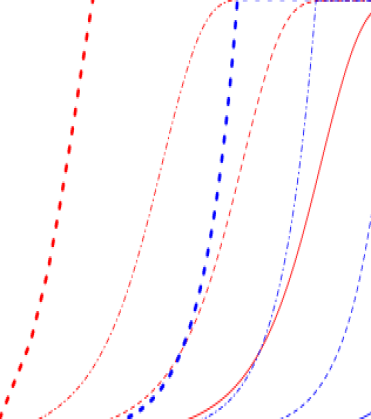

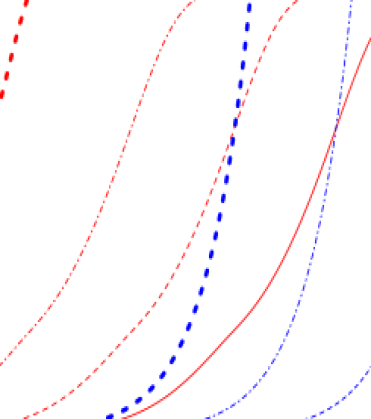

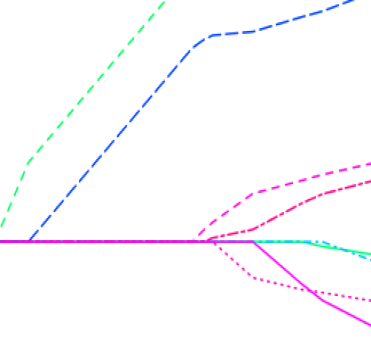

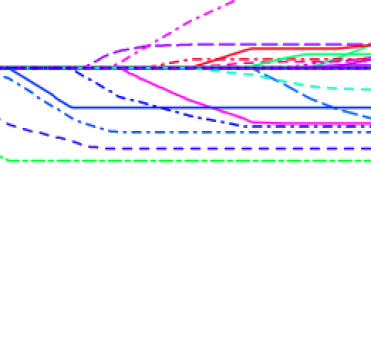

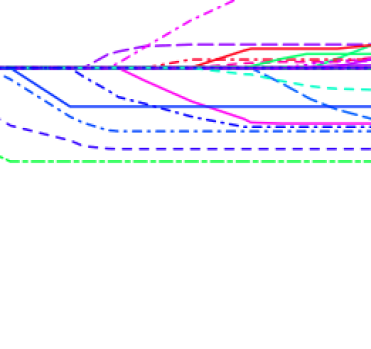

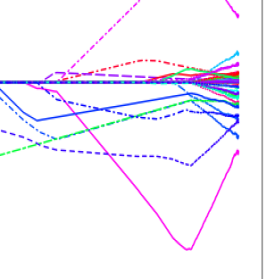

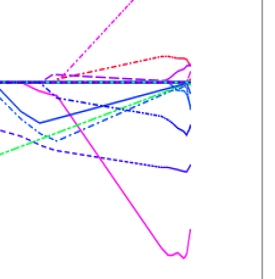

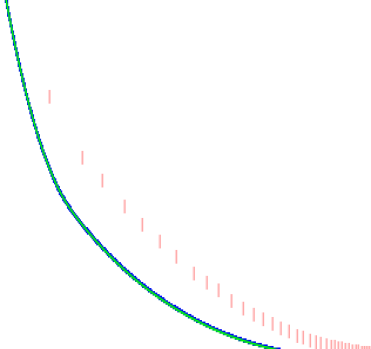

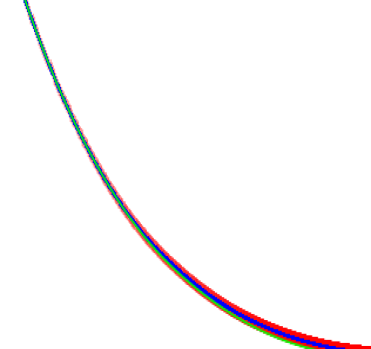

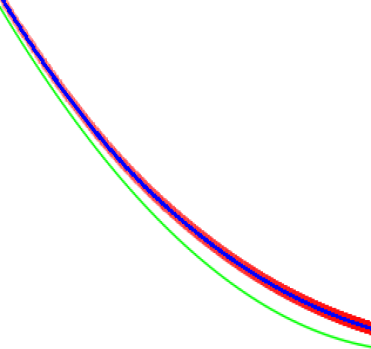

For certain datasets the coefficient profiles333By a coefficient profile we mean the map where, indexes a family of coefficients . For example, the family of Lasso solutions (2) indexed by can also be indexed by the norm of the coefficients, i.e., . This leads to a coefficient profile that depends upon the norm of the regression coefficients. Similarly, one may consider the coefficient profile of as a function of the norm of the regression coefficients delivered by the algorithm. of Lasso and are exactly the same [28], where denotes the limiting case of the algorithm as . Figure 2 (top panel) shows an example where the Lasso profile is similar to those of and LS-Boost (for small values of ). However, they are different in general (Figure 2, bottom panel). Under some conditions on the monotonicity of the coefficient profiles of the Lasso solution, the Lasso and profiles are exactly the same [15, 27]. Such equivalences exist for more general loss functions [37], albeit under fairly strong assumptions on problem data.

Efforts to understand boosting algorithms in general and in particular the algorithm paved the way for the celebrated Least Angle Regression aka the Lar algorithm [15] (see also [28]). The Lar algorithm is a democratic version of Forward Stepwise. Upon identifying the variable most correlated with the current residual in absolute value (as in Forward Stepwise), it moves the coefficient of the variable towards its least squares value in a continuous fashion. An appealing aspect of the Lar algorithm is that it provides a unified algorithmic framework for variable selection and shrinkage – one instance of Lar leads to a path algorithm for the Lasso, and a different instance leads to the limiting case of the algorithm as , namely . In fact, the Stagewise version of the Lar algorithm provides an efficient way to compute the coefficient profile for .

| Coefficient Profiles: LS-Boost , and Lasso | |||||

| Lasso | LS-Boost , | , | |||

|

Regression Coefficients |

|

|

|

||

|

Regression Coefficients |

|

|

|

||

| shrinkage of coefficients | shrinkage of coefficients | shrinkage of coefficients | |||

Due to the close similarities between the Lasso and boosting coefficient profiles, it is natural to investigate probable modifications of boosting that might lead to the Lasso solution path. This is one of the topics we study in this paper. In a closely related but different line of approach, [45] describes BLasso, a modification of the algorithm with the inclusion of additional “backward steps” so that the resultant coefficient profile mimics the Lasso path.

Subgradient Optimization as a Unifying Viewpoint of Boosting and Lasso

In spite of the various nice perspectives on and its connections to the Lasso as described above, the present understanding about the relationships between Lasso, , and LS-Boost for arbitrary datasets and is still fairly limited. One of the aims of this paper is to contribute some substantial further understanding of the relationship between these methods. Just like the Lar algorithm can be viewed as a master algorithm with special instances being the Lasso and , in this paper we establish that , LS-Boost and Lasso can be viewed as special instances of one grand algorithm: the subgradient descent method (of convex optimization) applied to the following parametric class of optimization problems:

| (3) |

and where is a regularization parameter. Here the first term is the maximum absolute correlation between the features and the residuals , and the second term is a regularization term that penalizes residuals that are far from the observations (which itself can be interpreted as the residuals for the null model ). The parameter determines the relative importance assigned to the regularization term, with corresponding to no importance whatsoever. As we describe in Section 4, Problem (3) is in fact a dual of the Lasso Problem (2).

The subgradient descent algorithm applied to Problem (3) leads to a new boosting algorithm that is almost identical to . We denote this algorithm by (for Regularized incremental Forward Stagewise regression). We show the following properties of the new algorithm :

-

•

is almost identical to , except that it first shrinks all of the coefficients of by a scaling factor and then updates the selected coefficient in the same additive fashion as .

-

•

as the number of iterations become large, delivers an approximate Lasso solution.

-

•

an adaptive version of , which we call , is shown to approximate the path of Lasso solutions with precise bounds that quantify the approximation error over the path.

-

•

specializes to , LS-Boost and the Lasso depending on the parameter value and the learning rates (step-sizes) used therein.

-

•

the computational guarantees derived herein for provide a precise description of the evolution of data-fidelity vis-à-vis shrinkage of the models obtained along the boosting iterations.

-

•

in our experiments, we observe that leads to models with statistical properties that compare favorably with the Lasso and . It also leads to models that are sparser than .

We emphasize that all of these results apply to the finite sample setup with no assumptions about the dataset nor about the relative sizes of and .

Contributions

A summary of the contributions of this paper is as follows:

-

1.

We analyze several boosting algorithms popularly used in the context of linear regression via the lens of first-order methods in convex optimization. We show that existing boosting algorithms, namely and LS-Boost , can be viewed as instances of the subgradient descent method aimed at minimizing the maximum absolute correlation between the covariates and residuals, namely . This viewpoint provides several insights about the operational characteristics of these boosting algorithms.

-

2.

We derive novel computational guarantees for and LS-Boost . These results quantify the rate at which the estimates produced by a boosting algorithm make their way towards an unregularized least squares fit (as a function of the number of iterations and the learning rate ). In particular, we demonstrate that for any value of the estimates produced by LS-Boost converge linearly to their respective least squares values and the norm of the coefficients grows at a rate . on the other hand demonstrates a slower sublinear convergence rate to an -approximate least squares solution, while the norm of the coefficients grows at a rate .

-

3.

Our computational guarantees yield precise characterizations of the amount of data-fidelity (training error) and regularization imparted by running a boosting algorithm for iterations. These results apply to any dataset and do not rely upon any distributional or structural assumptions on the data generating mechanism.

-

4.

We show that subgradient descent applied to a regularized version of the loss function , with regularization parameter , leads to a new algorithm which we call , that is a natural and simple generalization of . When compared to , the algorithm performs a seemingly minor rescaling of the coefficients at every iteration. As the number of iterations increases, delivers an approximate Lasso solution (2). Moreover, as the algorithm progresses, the norms of the coefficients evolve as a geometric series towards the regularization parameter value . We derive precise computational guarantees that inform us about the training error and regularization imparted by .

-

5.

We present an adaptive extension of , called , that delivers a path of approximate Lasso solutions for any prescribed grid sequence of regularization parameters. We derive guarantees that quantify the average distance from the approximate path traced by to the Lasso solution path.

Organization of the Paper

The paper is organized as follows. In Section 2 we analyze the convergence behavior of the LS-Boost algorithm. In Section 3 we present a unifying algorithmic framework for , , and LS-Boost as subgradient descent. In Section 4 we present the regularized correlation minimization Problem (3) and a naturally associated boosting algorithm , as instantiations of subgradient descent on the family of Problems (3). In each of the above cases, we present precise computational guarantees of the algorithms for convergence of residuals, training errors, and shrinkage and study their statistical implications. In Section 5, we further expand into a method for computing approximate solutions of the Lasso path. Section 6 contains computational experiments. To improve readability, most of the technical details have been placed in the Appendix A.

Notation

For a vector , we use to denote the -th coordinate of . We use superscripts to index vectors in a sequence . Let denote the -th unit vector in , and let denote the vector of ones. Let denote the norm for with unit ball , and let denote the number of non-zero coefficients of the vector . For , let be the operator norm. In particular, is the maximum norm of the columns of . For a scalar , denotes the sign of . The notation “” denotes assigning to be any optimal solution of the problem . For a convex set let denote the Euclidean projection operator onto , namely . Let denote the subdifferential operator of a convex function . If is a symmetric positive semidefinite matrix, let , , and denote the largest, smallest, and smallest nonzero (and hence positive) eigenvalues of , respectively.

2 LS-Boost : Computational Guarantees and Statistical Implications

Roadmap

We begin our formal study by examining the LS-Boost algorithm. We study the rate at which the coefficients generated by LS-Boost converge to the set of unregularized least square solutions. This characterizes the amount of data-fidelity as a function of the number of iterations and . In particular, we show (global) linear convergence of the regression coefficients to the set of least squares coefficients, with similar convergence rates derived for the prediction estimates and the boosting training errors delivered by LS-Boost . We also present bounds on the shrinkage of the regression coefficients as a function of and , thereby describing how the amount of shrinkage of the regression coefficients changes as a function of the number of iterations .

2.1 Computational Guarantees and Intuition

We first review some useful properties associated with the familiar least squares regression problem:

| (4) |

where is the least squares loss, whose gradient is:

| (5) |

where is the vector of residuals corresponding to the regression coefficients . It follows that is a least-squares solution of if and only if , which leads to the well known normal equations:

| (6) |

It also holds that:

| (7) |

The following theorem describes precise computational guarantees for LS-Boost: linear convergence of LS-Boost with respect to (4), and bounds on the shrinkage of the coefficients produced. Note that the theorem uses the quantity which denotes the smallest nonzero (and hence positive) eigenvalue of .

Theorem 2.1.

(Linear Convergence of LS-Boost for Least Squares) Consider the LS-Boost algorithm with learning rate , and define the linear convergence rate coefficient :

| (8) |

For all the following bounds hold:

-

(i)

(training error):

-

(ii)

(regression coefficients): there exists a least squares solution such that:

-

(iii)

(predictions): for every least-squares solution it holds that

-

(iv)

(gradient norm/correlation values):

-

(v)

(-shrinkage of coefficients):

-

(vi)

(sparsity of coefficients): . ∎

Before remarking on the various parts of Theorem 2.1, we first discuss the quantity defined in (8), which is called the linear convergence rate coefficient. We can write where is defined to be the ratio . Note that . To see this, let be an eigenvector associated with the largest eigenvalue of , then:

| (9) |

where the last inequality uses our assumption that the columns of have been normalized (whereby ), and the fact that . This then implies that – independent of any assumption on the dataset – and most importantly it holds that .

Let us now make the following immediate remarks on Theorem 2.1:

-

•

The bounds in parts (i)-(iv) state that the training errors, regression coefficients, predictions, and correlation values produced by LS-Boost converge linearly (also known as geometric or exponential convergence) to their least squares counterparts: they decrease by at least the constant multiplicative factor for part (i), and by for parts (ii)-(iv), at every iteration. The bounds go to zero at this linear rate as .

-

•

The computational guarantees in parts (i) - (vi) provide characterizations of the data-fidelity and shrinkage of the LS-Boost algorithm for any given specifications of the learning rate and the number of boosting iterations . Moreover, the quantities appearing in the bounds can be computed from simple characteristics of the data that can be obtained a priori without even running the boosting algorithm. (And indeed, one can even substitute in place of throughout the bounds if desired since .)

Some Intuition Behind Theorem 2.1

Let us now study the LS-Boost algorithm and build intuition regarding its progress with respect to solving the unconstrained least squares problem (4), which will inform the results in Theorem 2.1. Since the predictors are all standardized to have unit norm, it follows that the coefficient index and corresponding step-size selected in Step (2.) of LS-Boost satisfy:

| (10) |

Combining (7) and (10), we see that

| (11) |

Using the formula for in (10), we have the following convenient way to express the change in residuals at each iteration of LS-Boost:

| (12) |

Intuitively, since (12) expresses as the difference of two correlated variables, and , we expect the squared norm of (i.e. its sample variance) to be smaller than that of . On the other hand, as we see from (1), convergence of the residuals is ensured by the dependence of the change in residuals on , which goes to 0 as we approach a least squares solution. In the proof of Theorem 2.1 in Appendix A.2.2 we make this intuition precise by using (12) to quantify the amount of decrease in the least squares objective function at each iteration of LS-Boost . The final ingredient of the proof uses properties of convex quadratic functions (Appendix A.2.1) to relate the exact amount of the decrease from iteration to to the current optimality gap , which yields the following strong linear convergence property:

| (13) |

The above states that the training error gap decreases at each iteration by at least the multiplicative factor of , and clearly implies item (i) of Theorem 2.1.

Comments on the global linear convergence rate in Theorem 2.1

The global linear convergence of LS-Boost proved in Theorem 2.1, while novel, is not at odds with the present understanding of such convergence for optimization problems. One can view LS-Boost as performing steepest descent optimization steps with respect to the norm unit ball (rather than the norm unit ball which is the canonical version of the steepest descent method, see [35]). It is known [35] that canonical steepest decent exhibits global linear convergence for convex quadratic optimization so long as the Hessian matrix of the quadratic objective function is positive definite, i.e., . And for the least squares loss function , which yields the condition that . As discussed in [4], this result extends to other norms defining steepest descent as well. Hence what is modestly surprising herein is not the linear convergence per se, but rather that LS-Boost exhibits global linear convergence even when , i.e., even when does not have full column rank (essentially replacing with in our analysis). This derives specifically from the structure of the least squares loss function, whose function values (and whose gradient) are invariant in the null space of , i.e., for all satisfying , and is thus rendered “immune” to changes in in the null space of .

2.2 Statistical Insights from the Computational Guarantees

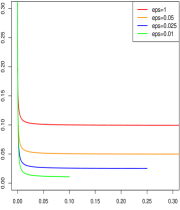

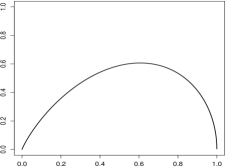

Note that in most noisy problems, the limiting least squares solution is statistically less interesting than an estimate obtained in the interior of the boosting profile, since the latter typically corresponds to a model with better bias-variance tradeoff. We thus caution the reader that the bounds in Theorem 2.1 should not be merely interpreted as statements about how rapidly the boosting iterations reach the least squares fit. We rather intend for these bounds to inform us about the evolution of the training errors and the amount of shrinkage of the coefficients as the LS-Boost algorithm progresses and when is at most moderately large. When the training errors are paired with the profile of the -shrinkage values of the regression coefficients, they lead to the ordered pairs:

| (14) |

which describes the data-fidelity and -shrinkage tradeoff as a function of , for the given learning rate . This profile is described in Figure 9 in Appendix A.1.1 for several data instances. The bounds in Theorem 2.1 provide estimates for the two components of the ordered pair (14), and they can be computed prior to running the boosting algorithm. For simplicity, let us use the following crude estimate:

which is an upper bound of the bound in part (v) of the theorem, to provide an upper approximation of . Combining the above estimate with the guarantee in part (i) of Theorem 2.1 in (14), we obtain the following ordered pairs:

| (15) |

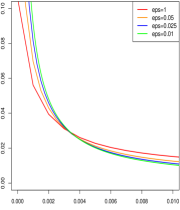

which describe the entire profile of the training error bounds and the -shrinkage bounds as a function of as suggested by Theorem 2.1. These profiles, as described above in (15), are illustrated in Figure 3.

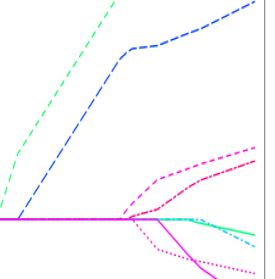

| LS-Boost algorithm: -shrinkage versus data-fidelity tradeoffs (theoretical bounds) | |||

|---|---|---|---|

| Synthetic dataset | Synthetic dataset | Leukemia dataset | |

|

Training Error |

|

|

|

| shrinkage of coefficients | shrinkage of coefficients | shrinkage of coefficients | |

It is interesting to consider the profiles of Figure 3 alongside the explicit regularization framework of the Lasso (2) which also traces out a profile of the form (14):

| (16) |

as a function of , where, is a solution to the Lasso problem (2). For a value of the optimal objective value of the Lasso problem will serve as a lower bound of the corresponding LS-Boost loss function value at iteration . Thus the training error of delivered by the LS-Boost algorithm will be sandwiched between the following lower and upper bounds:

for every . Note that the difference between the upper and lower bounds above, given by: converges to zero as . Figure 9 in Appendix A.1.1 shows the training error versus shrinkage profiles for LS-Boost and Lasso for different datasets.

|

|

|

|

|

|

For the bounds in parts (i) and (iii) of Theorem 2.1, the asymptotic limits (as ) are the unregularized least squares training error and predictions — which are quantities that are uniquely defined even in the underdetermined case.

The bound in part (ii) of Theorem 2.1 is a statement concerning the regression coefficients. In this case, the notion of convergence needs to be appropriately modified from parts (i) and (iii), since the natural limiting object is not necessarily unique. In this case, perhaps not surprisingly, the regression coefficients need not converge. The result in part (ii) of the theorem states that converges at a linear rate to the set of least squares solutions. In other words, at every LS-Boost boosting iteration, there exists a least squares solution for which the presented bound holds. Here is in fact the closest least squares solution to in the norm — and the particular candidate least squares solution may be different for each iteration.

Interpreting the parameters and algorithm dynamics

There are several determinants of the quality of the bounds in the different parts of Theorem 2.1 which can be grouped into:

-

•

algorithmic parameters: this includes the learning rate and the number of iterations , and

-

•

data dependent quantities: , , and .

The coefficient of linear convergence is given by the quantity , where . Note that is monotone decreasing in for , and is minimized at . This simple observation confirms the general intuition about LS-Boost : corresponds to the most aggressive model fitting behavior in the LS-Boost family, with smaller values of corresponding to a slower model fitting process. The ratio is a close cousin of the condition number associated with the data matrix — and smaller values of imply a faster rate of convergence.

In the overdetermined case with and , the condition number plays a key role in determining the stability of the least-squares solution and in measuring the degree of multicollinearity present. Note that , and that the problem is better conditioned for smaller values of this ratio. Furthermore, since it holds that , and thus by (9). Thus the condition number always upper bounds the classical condition number , and if is close to , then and the two measures essentially coincide. Finally, since in this setup is unique, part (ii) of Theorem 2.1 implies that the sequence converges linearly to the unique least squares solution .

In the underdetermined case with , and thus . On the other hand, since is the smallest nonzero (hence positive) eigenvalue of . Therefore the condition number is similar to the classical condition number restricted to the subspace spanned by the columns of (whose dimension is . Interestingly, the linear rate of convergence enjoyed by LS-Boost is in a sense adaptive — the algorithm automatically adjusts itself to the convergence rate dictated by the parameter “as if” it knows that the null space of is not relevant.

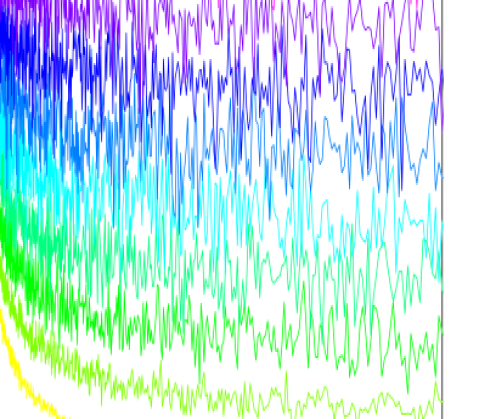

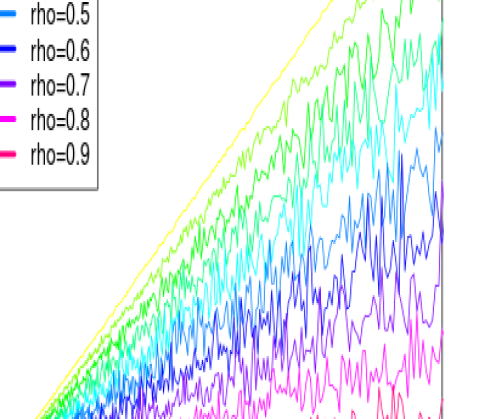

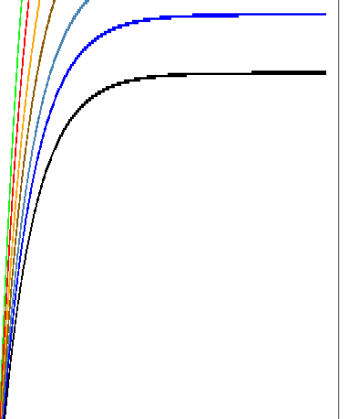

| Dynamics of the LS-Boost algorithm versus number of boosting iterations | |||

|---|---|---|---|

|

Sorted Coefficient Indices |

|

|

|

| Number of Boosting Iterations | Number of Boosting Iterations | Number of Boosting Iterations | |

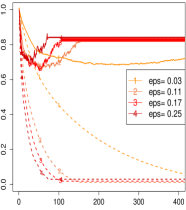

As the dataset is varied, the value of can change substantially from one dataset to another, thereby leading to differences in the convergence behavior bounds in parts (i)-(v) of Theorem 2.1. To settle all of these ideas, we can derive some simple bounds on using tools from random matrix theory. Towards this end, let us suppose that the entries of are drawn from a standard Gaussian ensemble, which are subsequently standardized such that every column of has unit norm. Then it follows from random matrix theory [43] that with high probability. (See Appendix A.2.4 for a more detailed discussion of this fact.) To gain better insights into the behavior of and how it depends on the values of pairwise correlations of the features, we performed some computational experiments, the results of which are shown in Figure 4. Figure 4 shows the behavior of as a function of for a fixed and , for different datasets simulated as follows. We first generated a multivariate data matrix from a Gaussian distribution with mean zero and covariance , where, for all ; and then all of the columns of the data matrix were standardized to have unit norm. The resulting matrix was taken as . We considered different cases by varying the magnitude of pairwise correlations of the features — when is small, the rate of convergence is typically faster (smaller ) and the rate becomes slower (higher ) for higher values of . Figure 4 shows that the coefficient of linear convergence is quite close to — which suggests a slowly converging algorithm and confirms our intuition about the algorithmic behavior of LS-Boost . Indeed, LS-Boost , like any other boosting algorithm, should indeed converge slowly to the unregularized least squares solution. The slowly converging nature of the LS-Boost algorithm provides, for the first time, a precise theoretical justification of the empirical observation made in [28] that stagewise regression is widely considered ineffective as a tool to obtain the unregularized least squares fit, as compared to other stepwise model fitting procedures like Forward Stepwise regression (discussed in Section 1).

The above discussion sheds some interesting insight into the behavior of the LS-Boost algorithm. For larger values of , the observed covariates tend to be even more highly correlated (since ). Whenever a pair of features are highly correlated, the LS-Boost algorithm finds it difficult to prefer one over the other and thus takes turns in updating both coefficients, thereby distributing the effects of a covariate to all of its correlated cousins. Since a group of correlated covariates are all competing to be updated by the LS-Boost algorithm, the progress made by the algorithm in decreasing the loss function is naturally slowed down. In contrast, when is small, the LS-Boost algorithm brings in a covariate and in a sense completes the process by doing the exact line-search on that feature. This heuristic explanation attempts to explain the slower rate of convergence of the LS-Boost algorithm for large values of — a phenomenon that we observe in practice and which is also substantiated by the computational guarantees in Theorem 2.1. We refer the reader to Figures 1 and 5 which further illustrate the above justification. Statement (v) of Theorem 2.1 provides upper bounds on the shrinkage of the coefficients. Figure 3 illustrates the evolution of the data-fidelity versus -shrinkage as obtained from the computational bounds in Theorem 2.1. Some additional discussion and properties of LS-Boost are presented in Appendix A.2.3.

3 Boosting Algorithms as Subgradient Descent

Roadmap

In this section we present a new unifying framework for interpreting the three boosting algorithms that were discussed in Section 1, namely , its non-uniform learning rate extension , and LS-Boost. We show herein that all three algorithmic families can be interpreted as instances of the subgradient descent method of convex optimization, applied to the problem of minimizing the largest correlation between residuals and predictors. Interestingly, this unifying lens will also result in a natural generalization of with very strong ties to the Lasso solutions, as we will present in Sections 4 and 5. The framework presented in this section leads to convergence guarantees for and . In Theorem 3.1 herein, we present a theoretical description of the evolution of the algorithm, in terms of its data-fidelity and shrinkage guarantees as a function of the number of boosting iterations. These results are a consequence of the computational guarantees for that inform us about the rate at which the training error, regression coefficients, and predictions make their way to their least squares counterparts. In order to develop these results, we first motivate and briefly review the subgradient descent method of convex optimization.

3.1 Brief Review of Subgradient Descent

We briefly motivate and review the subgradient descent method for non-differentiable convex optimization problems. Consider the following optimization problem:

| (17) |

where is a closed convex set and is a convex function. If is differentiable, then will satisfy the following gradient inequality:

which states that lies above its first-order (linear) approximation at . One of the most intuitive optimization schemes for solving (17) is the method of gradient descent. This method is initiated at a given point . If is the current iterate, then the next iterate is given by the update formula: . In this method the potential new point is , where is called the step-size at iteration , and the step is taken in the direction of the negative of the gradient. If this potential new point lies outside of the feasible region , it is then projected back onto . Here recall that is the Euclidean projection operator, namely .

Now suppose that is not differentiable. By virtue of the fact that is convex, then will have a subgradient at each point . Recall that is a subgradient of at if the following subgradient inequality holds:

| (18) |

which generalizes the gradient inequality above and states that lies above the linear function on the right side of (18). Because there may exist more than one subgradient of at , let denote the set of subgradients of at . Then “” denotes that is a subgradient of at the point , and so satisfies (18) for all . The subgradient descent method (see [40], for example) is a simple generalization of the method of gradient descent to the case when is not differentiable. One simply replaces the gradient by the subgradient, yielding the following update scheme:

| (19) |

The following proposition summarizes a well-known computational guarantee associated with the subgradient descent method.

Proposition 3.1.

The left side of (20) is simply the best objective function value obtained among the first iterations. The right side of (20) bounds the best objective function value from above, namely the optimal value plus a nonnegative quantity that is a function of the number of iterations , the constant step-size , the bound on the norms of subgradients, and the distance from the initial point to an optimal solution of (17). Note that for a fixed step-size , the right side of (20) goes to as . In the interest of completeness, we include a proof of Proposition 3.1 in Appendix A.3.1.

3.2 A Subgradient Descent Framework for Boosting

We now show that the boosting algorithms discussed in Section 1, namely and its relatives and LS-Boost, can all be interpreted as instantiations of the subgradient descent method to minimize the largest absolute correlation between the residuals and predictors.

Let denote the affine space of residuals and consider the following convex optimization problem:

| (21) |

which we dub the “Correlation Minimization” problem, or CM for short. Note an important subtlety in the CM problem, namely that the optimization variable in CM is the residual and not the regression coefficient vector .

Since the columns of have unit norm by assumption, is the largest absolute correlation between the residual vector and the predictors. Therefore (21) is the convex optimization problem of minimizing the largest correlation between the residuals and the predictors, over all possible values of the residuals. From (6) with we observe that if and only if is a least squares solution, whereby for the least squares residual vector . Since the objective function in (21) is nonnegative, we conclude that and the least squares residual vector is also the unique optimal solution of the CM problem (21). Thus CM can be viewed as an optimization problem which also produces the least squares solution.

The following proposition states that the three boosting algorithms , and LS-Boost can all be viewed as instantiations of the subgradient descent method to solve the CM problem (21).

Proposition 3.2.

Consider the subgradient descent method (19) with step-size sequence to solve the correlation minimization (CM) problem (21), initialized at . Then:

-

(i)

the algorithm is an instance of subgradient descent, with a constant step-size at each iteration,

-

(ii)

the algorithm is an instance of subgradient descent, with non-uniform step-sizes at iteration , and

-

(iii)

the LS-Boost algorithm is an instance of subgradient descent, with non-uniform step-sizes at iteration , where .

Proof.

We first prove (i). Recall the update of the residuals in :

We first show that is a subgradient of the objective function of the correlation minimization problem CM (21) at . At iteration , chooses the coefficient to update by selecting , whereby

, and therefore for any it holds that:

Therefore using the definition of a subgradient in (18), it follows that is a subgradient of at . Therefore the update is of the form where . Last of all notice that the update can also be written as , hence , i.e., the projection step is superfluous here, and therefore , which is precisely the update for the subgradient descent method with step-size .

The proof of (ii) is the same as (i) with a step-size choice of at iteration . Furthermore, as discussed in Section 1, LS-Boost may be thought of as a specific instance of , whereby the proof of (iii) follows as a special case of (ii).∎

Proposition 3.2 presents a new interpretation of the boosting algorithms and its cousins as subgradient descent. This is interesting especially since and LS-Boost have been traditionally interpreted as greedy coordinate descent or steepest descent type procedures [28, 25]. This has the following consequences of note:

-

•

We take recourse to existing tools and results about subgradient descent optimization to inform us about the computational guarantees of these methods. When translated to the setting of linear regression, these results will shed light on the data fidelity vis-à-vis shrinkage characteristics of and its cousins — all using quantities that can be easily obtained prior to running the boosting algorithm. We will show the details of this in Theorem 3.1 below.

-

•

The subgradient optimization viewpoint provides a unifying algorithmic theme which we will also apply to a regularized version of problem CM (21), and that we will show is very strongly connected to the Lasso. This will be developed in Section 4. Indeed, the regularized version of the CM problem that we will develop in Section 4 will lead to a new family of boosting algorithms which are a seemingly minor variant of the basic algorithm but deliver (-approximate) solutions to the Lasso.

3.3 Deriving and Interpreting Computational Guarantees for

The following theorem presents the convergence properties of , which are a consequence of the interpretation of as an instance of the subgradient descent method.

Theorem 3.1.

(Convergence Properties of ) Consider the algorithm with learning rate . Let be the total number of iterations. Then there exists an index for which the following bounds hold:

-

(i)

(training error):

-

(ii)

(regression coefficients): there exists a least squares solution such that:

-

(iii)

(predictions): for every least-squares solution it holds that

-

(iv)

(correlation values)

-

(v)

(-shrinkage of coefficients):

-

(vi)

(sparsity of coefficients): . ∎

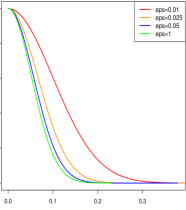

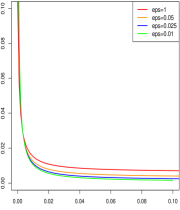

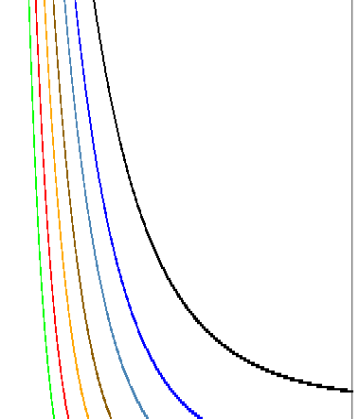

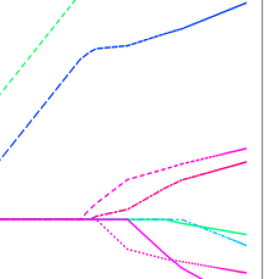

| algorithm: shrinkage versus data-fidelity tradeoffs (theoretical bounds) | |||

|---|---|---|---|

| Synthetic dataset | Leukemia dataset | Leukemia dataset (zoomed) | |

|

Training Error |

|

|

|

| shrinkage of coefficients | shrinkage of coefficients | shrinkage of coefficients | |

Interpreting the Computational Guarantees

Theorem 3.1 accomplishes for what Theorem 2.1 did for LS-Boost — parts (i) – (iv) of the theorem describe the rate in which the training error, regression coefficients, and related quantities make their way towards their (-approximate) unregularized least squares counterparts. Part (v) of the theorem also describes the rate at which the shrinkage of the regression coefficients evolve as a function of the number of boosting iterations. The rate of convergence of is sublinear, unlike the linear rate of convergence for LS-Boost . Note that this type of sublinear convergence implies that the rate of decrease of the training error (for instance) is dramatically faster in the very early iterations as compared to later iterations. Taken together, Theorems 3.1 and 2.1 highlight an important difference between the behavior of algorithms LS-Boost and :

-

•

the limiting solution of the LS-Boost algorithm (as ) corresponds to the unregularized least squares solution, but

-

•

the limiting solution of the algorithm (as ) corresponds to an approximate least squares solution.

As demonstrated in Theorems 2.1 and 3.1, both LS-Boost and have nice convergence properties with respect to the unconstrained least squares problem (4). However, unlike the convergence results for LS-Boost in Theorem 2.1, exhibits a sublinear rate of convergence towards a suboptimal least squares solution. For example, part (i) of Theorem 3.1 implies in the limit as that identifies a model with training error at most:

| (22) |

In addition, part (ii) of Theorem 3.1 implies that as , identifies a model whose distance to the set of least squares solutions is at most:

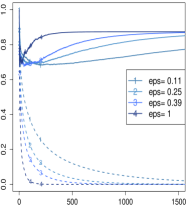

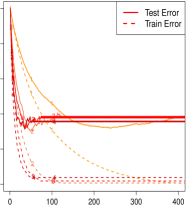

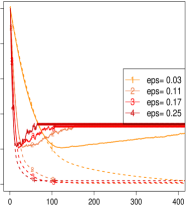

Note that the computational guarantees in Theorem 3.1 involve the quantities and , assuming and are fixed. To settle ideas, let us consider the synthetic datasets used in Figures 4 and 1, where the covariates were generated from a multivariate Gaussian distribution with pairwise correlation . Figure 4 suggests that decreases with increasing values. Thus, controlling for other factors appearing in the computational bounds444To control for other factors, for example, we may assume that and for different values of we have with fixed across the different examples. , it follows from the statements of Theorem 3.1 that the training error decreases much more rapidly for smaller values, as a function of . This is nicely validated by the computational results in Figure 1 (the three top panel figures), which show that the training errors decay at a faster rate for smaller values of .

Let us examine more carefully the properties of the sequence of models explored by and the corresponding tradeoffs between data fidelity and model complexity. Let TBound and SBound denote the training error bound and shrinkage bound in parts (i) and (v) of Theorem 3.1, respectively. Then simple manipulation of the arithmetic in these two bounds yields the following tradeoff equation:

The above tradeoff between the training error bound and the shrinkage bound is illustrated in Figure 6, which shows this tradeoff curve for four different values of the learning rate . Except for very small shrinkage levels, lower values of produce smaller training errors. But unlike the corresponding tradeoff curves for LS-Boost , there is a range of values of the shrinkage for which smaller values of actually produce larger training errors, though admittedly this range is for very small shrinkage values. For more reasonable shrinkage values, smaller values of will correspond to smaller values of the training error.

Part (v) of Theorems 2.1 and 3.1 presents shrinkage bounds for and LS-Boost , respectively. Let us briefly compare these bounds. Examining the shrinkage bound for LS-Boost , we can bound the left term from above by . We can also bound the right term from above by where recall from Section 2 that is the linear convergence rate coefficient . We may therefore alternatively write the following shrinkage bound for LS-Boost :

| (23) |

The shrinkage bound for is simply . Comparing these two bounds, we observe that not only does the shrinkage bound for grow at a faster rate as a function of for large enough , but also the shrinkage bound for grows unbounded in , unlike the right term above for the shrinkage bound of LS-Boost .

One can also compare and LS-Boost in terms of the efficiency with which these two methods achieve a certain pre-specified data-fidelity. In Appendix A.3.3 we show, at least in theory, that LS-Boost is much more efficient than at achieving such data-fidelity, and furthermore it does so with much better shrinkage.

4 Regularized Correlation Minimization, Boosting, and Lasso

Roadmap

In this section we introduce a new boosting algorithm, parameterized by a scalar , which we denote by (for Regularized incremental Forward Stagewise regression), that is obtained by incorporating a simple rescaling step to the coefficient updates in . We then introduce a regularized version of the Correlation Minimization (CM) problem (21) which we refer to as RCM. We show that the adaptation of the subgradient descent algorithmic framework to the Regularized Correlation Minimization problem RCM exactly yields the algorithm . The new algorithm may be interpreted as a natural extension of popular boosting algorithms like , and has the following notable properties:

-

•

Whereas updates the coefficients in an additive fashion by adding a small amount to the coefficient most correlated with the current residuals, first shrinks all of the coefficients by a scaling factor and then updates the selected coefficient in the same additive fashion as .

-

•

delivers -accurate solutions to the Lasso in the limit as , unlike which delivers -accurate solutions to the unregularized least squares problem.

-

•

has computational guarantees similar in spirit to the ones described in the context of – these quantities directly inform us about the data-fidelity vis-à-vis shrinkage tradeoffs as a function of the number of boosting iterations and the learning rate .

The notion of using additional regularization along with the implicit shrinkage imparted by boosting is not new in the literature. Various interesting notions have been proposed in [26, 10, 45, 14, 22], see also the discussion in Appendix A.4.4 herein. However, the framework we present here is new. We present a unified subgradient descent framework for a class of regularized CM problems that results in algorithms that have appealing structural similarities with forward stagewise regression type algorithms, while also being very strongly connected to the Lasso.

Boosting with additional shrinkage –

Here we give a formal description of the algorithm. is controlled by two parameters: the learning rate , which plays the same role as the learning rate in , and the “regularization parameter” . Our reason for referring to as a regularization parameter is due to the connection between and the Lasso, which will be made clear later. The shrinkage factor, i.e., the amount by which we shrink the coefficients before updating the selected coefficient, is determined as . Supposing that we choose to update the coefficient indexed by at iteration , then the coefficient update may be written as:

Below we give a concise description of , including the update for the residuals that corresponds to the update for the coefficients stated above.

Algorithm:

Fix the learning rate , regularization parameter such that , and number of iterations .

Initialize at , , .

-

1.

For do the following:

-

2.

Compute:

-

3.

-

-

and

-

Note that and are structurally very similar – and indeed when then is exactly . Note also that shares the same upper bound on the sparsity of the regression coefficients as , namely for all it holds that: . When then, as previously mentioned, the main structural difference between and is the additional rescaling of the coefficients by the factor . This rescaling better controls the growth of the coefficients and, as will be demonstrated next, plays a key role in connecting to the Lasso.

Regularized Correlation Minimization (RCM) and Lasso

The starting point of our formal analysis of is the Correlation Minimization (CM) problem (21), which we now modify by introducing a regularization term that penalizes residuals that are far from the vector of observations . This modification leads to the following parametric family of optimization problems indexed by :

| (24) |

where “RCM” connotes Regularlized Correlation Minimization. Note that RCM reduces to the correlation minimization problem CM (21) when . RCM may be interpreted as the problem of minimizing, over the space of residuals, the largest correlation between the residuals and the predictors plus a regularization term that penalizes residuals that are far from the response (which itself can be interpreted as the residuals associated with the model ).

Interestingly, as we show in Appendix A.4.1, RCM (24) is equivalent to the Lasso (2) via duality. This equivalence provides further insight about the regularization used to obtain . Comparing the Lasso and RCM, notice that the space of the variables of the Lasso is the space of regression coefficients , namely , whereas the space of the variables of RCM is the space of model residuals, namely , or more precisely . The duality relationship shows that (24) is an equivalent characterization of the Lasso problem, just like the correlation minimization (CM) problem (21) is an equivalent characterization of the (unregularized) least squares problem. Recall that Proposition 3.2 showed that subgradient descent applied to the CM problem (24) (which is with ) leads to the well-known boosting algorithm . We now extend this theme with the following Proposition, which demonstrates is equivalent to subgradient descent applied to .

Proposition 4.1.

The algorithm is an instance of subgradient descent to solve the regularized correlation minimization () problem (24), initialized at , with a constant step-size at each iteration.

4.1 : Computational Guarantees and their Implications

In this subsection we present computational guarantees and convergence properties of the boosting algorithm . Due to the structural equivalence between and subgradient descent applied to the problem (24) (Proposition 4.1) and the close connection between and the Lasso (Appendix A.4.1), the convergence properties of are naturally stated with respect to the Lasso problem (2). Similar to Theorem 3.1 which described such properties for (with respect to the unregularized least squares problem), we have the following properties for .

Theorem 4.1.

(Convergence Properties of for the Lasso ) Consider the algorithm with learning rate and regularization parameter , where . Then the regression coefficient is feasible for the Lasso problem (2) for all . Let denote a specific iteration counter. Then there exists an index for which the following bounds hold:

-

(i)

(training error):

-

(ii)

(predictions): for every Lasso solution it holds that

-

(iii)

(-shrinkage of coefficients):

-

(iv)

(sparsity of coefficients): . ∎

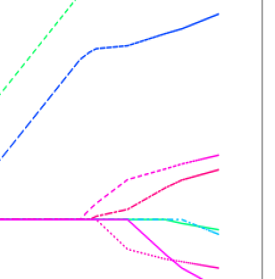

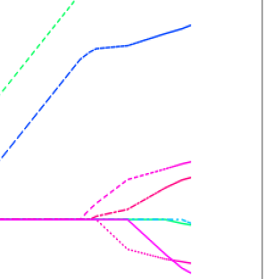

| algorithm, Prostate cancer dataset (computational bounds) | ||||

|

-norm of coefficients (relative scale) |

|

Training Error (relative scale) |

|

|

| Iterations | Iterations | Iterations | ||

Interpreting the Computational Guarantees

The statistical interpretations implied by the computational guarantees presented in Theorem 4.1 are analogous to those previously discussed for LS-Boost (Theorem 2.1) and (Theorem 3.1). These guarantees inform us about the data-fidelity vis-à-vis shrinkage tradeoffs as a function of the number of boosting iterations, as nicely demonstrated in Figure 7. There is, however, an important differentiation between the properties of and the properties of LS-Boost and , namely:

- •

-

•

For , our results (Theorem 4.1) characterize how the estimates approach a (-approximate) Lasso solution.

Notice that like , traces out a profile of regression coefficients. This is reflected in item (iii) of Theorem 4.1 which bounds the -shrinkage of the coefficients as a function of the number of boosting iterations . Due to the rescaling of the coefficients, the -shrinkage may be bounded by a geometric series that approaches as grows. Thus, there are two important aspects of the bound in item (iii): (a) the dependence on the number of boosting iterations which characterizes model complexity during early iterations, and (b) the uniform bound of which applies even in the limit as and implies that all regression coefficient iterates are feasible for the Lasso problem (2).

On the other hand, item (i) characterizes the quality of the coefficients with respect to the Lasso solution, as opposed to the unregularized least squares problem as in . In the limit as , item (i) implies that identifies a model with training error at most This upper bound on the training error may be set to any prescribed error level by appropriately tuning ; in particular, for and fixed this limit is essentially . Thus, combined with the uniform bound of on the -shrinkage, we see that the algorithm delivers the Lasso solution in the limit as .

It is important to emphasize that should not just be interpreted as an algorithm to solve the Lasso. Indeed, like , the trajectory of the algorithm is important and may identify a more statistically interesting model in the interior of its profile. Thus, even if the Lasso solution for leads to overfitting, the updates may visit a model with better predictive performance by trading off bias and variance in a more desirable fashion suitable for the particular problem at hand.

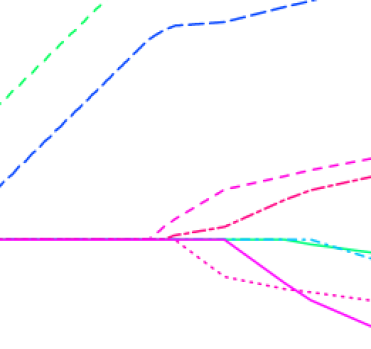

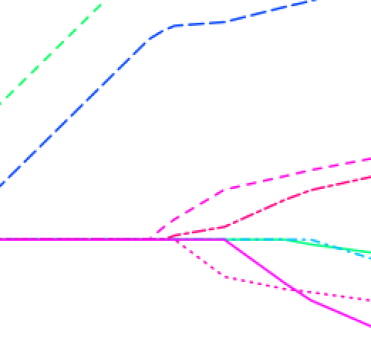

Figure 8 shows the profiles of for different values of , where is the -norm of the minimum -norm least squares solution. Curiously enough, Figure 8 shows that in some cases, the profile of bears a lot of similarities with that of the Lasso (as presented in Figure 2). However, the profiles are in general different. Indeed, imposes a uniform bound of on the -shrinkage, and so for values larger than we cannot possibly expect to approximate the Lasso path. However, even if is taken to be sufficiently large (but finite) the profiles may be different. In this connection it is helpful to draw the analogy between the curious similarities between the (i.e., with ) and Lasso coefficient profiles, even though the profiles are different in general.

| , | , | , | ||

|

Regression Coefficients |

|

|

|

|

| , | , | , | ||

|

Regression Coefficients |

|

|

|

|

| -norm of coefficients | -norm of coefficients | -norm of coefficients | -norm of coefficients |

5 A Modified Forward Stagewise Algorithm for Computing the Lasso Path

In Section 4 we introduced the boosting algorithm (which is a very close cousin of ) that delivers solutions to the Lasso problem (2) for a fixed but arbitrary , in the limit as with . Furthermore, our experiments in Section 6 suggest that may lead to estimators with good statistical properties for a wide range of values of , provided that the value of is not too small. While by itself may be considered as a regularization scheme with excellent statistical properties, the boosting profile delivered by might in some cases be different from the Lasso coefficient profile, as we saw in Figure 8. Therefore in this section we investigate the following question: is it possible to modify the algorithm, while still retaining its basic algorithmic characteristics, so that it delivers an approximate Lasso coefficient profile for any dataset? We answer this question in the affirmative herein.

To fix ideas, let us consider producing the (approximate) Lasso path by producing a sequence of (approximate) Lasso solutions on a predefined grid of regularization parameter values in the interval given by . (A standard method for generating the grid points is to use a geometric sequence such as for , for some .) Motivated by the notion of warm-starts popularly used in the statistical computing literature in the context of computing a path of Lasso solutions (55) via coordinate descent methods [23], we propose here a slight modification of the algorithm that sequentially updates the value of according to the predefined grid values , and does so prior to each update of and . We call this method , whose complete description is as follows:

Algorithm:

Fix the learning rate , choose values , , satisfying such that .

Initialize at , , .

-

1.

For do the following:

-

2.

Compute:

-

3.

Set:

-

-

and

-

Notice that retains the identical structure of a forward stagewise regression type of method, and uses the same essential update structure of Step (3.) of . Indeed, the updates of and in are identical to those in Step (3.) of except that they use the regularization value at iteration instead of the constant value of as in .

Theoretical Guarantees for

Analogous to Theorem 4.1 for , the following theorem describes properties of the algorithm. In particular, the theorem provides rigorous guarantees about the distance between the algorithm and the Lasso coefficient profiles – which apply to any general dataset.

Theorem 5.1.

(Computational Guarantees of ) Consider the algorithm with the given learning rate and regularization parameter sequence . Let denote the total number of iterations. Then the following holds:

-

(i)

(Lasso feasibility and average training error): for each , provides an approximate solution to the Lasso problem for . More specifically, is feasible for the Lasso problem for , and satisfies the following suboptimality bound with respect to the entire boosting profile:

-

(ii)

(-shrinkage of coefficients): for .

-

(iii)

(sparsity of coefficients): for . ∎

Corollary 5.1.

( approximates the Lasso path) For every fixed and it holds that:

(and the quantity on the right side of the above bound goes to zero as ). ∎

Interpreting the computational guarantees

Let us now provide some interpretation of the results stated in Theorem 5.1. Recall that Theorem 4.1 presented bounds on the distance between the training errors achieved by the boosting algorithm and Lasso training errors for a fixed but arbitrary that is specified a priori. The message in Theorem 5.1 generalizes this notion to a family of Lasso solutions corresponding to a grid of values. The theorem thus quantifies how the boosting algorithm simultaneously approximates a path of Lasso solutions.

Part (i) of Theorem 5.1 first implies that the sequence of regression coefficient vectors is feasible along the Lasso path, for the Lasso problem (2) for the sequence of regularization parameter values . In considering guarantees with respect to the training error, we would ideally like guarantees that hold across the entire spectrum of values. While part (i) does not provide such strong guarantees, part (i) states that these quantities will be sufficiently small on average. Indeed, for a fixed and as , part (i) states that the average of the differences between the training errors produced by the algorithm and the optimal training errors is at most . This non-vanishing bound (for ) is a consequence of the fixed learning rate used in – such bounds were also observed for and .

Thus on average, the training error of the model will be sufficiently close (as controlled by the learning rate ) to the optimal training error for the corresponding regularization parameter value . In summary, while provides the most amount of flexibility in terms of controlling for model complexity since it allows for any (monotone) sequence of regularization parameter values in the range , this freedom comes at the cost of weaker training error guarantees with respect to any particular value (as opposed to which provides strong guarantees with respect to the fixed value ). Nevertheless, part (i) guarantees that the training errors will be sufficiently small on average across the entire path of regularization parameter values explored by the algorithm.

6 Some Computational Experiments

We consider an array of examples exploring statistical properties of the different boosting algorithms studied herein. We consider different types of synthetic and real datasets, which are briefly described here.

Synthetic datasets

We considered synthetically generated datasets of the following types:

-

•

Eg-A. Here the data matrix is generated from a multivariate normal distribution, i.e., for each , . Here denotes the row of and has all off-diagonal entries equal to and all diagonal entries equal to one. The response is generated as , where . The underlying regression coefficient was taken to be sparse with for all and otherwise. is chosen so as to control the signal to noise ratio

Different values of SNR, and were taken and they have been specified in our results when and where appropriate.

-

•

Eg-B. Here the datasets are generated similar to above, with for and otherwise. We took the value of SNR=1in this example.

Real datasets

We considered four different publicly available microarray datasets as described below.

-

•

Leukemia dataset. This dataset, taken from [12], was processed to have and . was created as ; with for all and zero otherwise.

-

•

Golub dataset. This dataset, taken from the R package mpm, was processed to have and , with artificial responses generated as above.

-

•

Khan dataset. This dataset, taken from the website of [28], was processed to have and , with artificial responses generated as above.

-

•

Prostate dataset. This dataset, analyzed in [15], was processed to create three types of different datasets: (a) the original dataset with and , (b) a dataset with and , formed by extending the covariate space to include second order interactions, and (c) a third dataset with and , formed by subsampling the previous dataset.

For more detail on the above datasets, we refer the reader to the Appendix B.

Note that in all the examples we standardized such that the columns have unit norm, before running the different algorithms studied herein.

6.1 Statistical properties of boosting algorithms: an empirical study

We performed some experiments to better understand the statistical behavior of the different boosting methods described in this paper. We summarize our findings here; for details (including tables, figures and discussions) we refer the reader to Appendix, Section B.

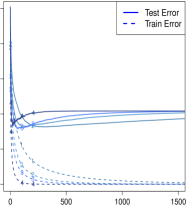

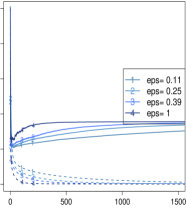

Sensitivity of the Learning Rate in LS-Boost and

We explored how the training and test errors for LS-Boost and change as a function of the number of boosting iterations and the learning rate. We observed that the best predictive models were sensitive to the choice of —the best models were obtained at values larger than zero and smaller than one. When compared to Lasso , stepwise regression [15] and [15]; and LS-Boost were found to be as good as the others, in some cases the better than the rest.

Statistical properties of , Lasso and : an empirical study

We performed some experiments to evaluate the performance of , in terms of predictive accuracy and sparsity of the optimal model, versus the more widely known methods and Lasso. We found that when was larger than the best for the Lasso (in terms of obtaining a model with the best predictive performance), delivered a model with excellent statistical properties – led to sparse solutions and the predictive performance was as good as, and in some cases better than, the Lasso solution. We observed that the choice of does not play a very crucial role in the algorithm, once it is chosen to be reasonably large; indeed the number of boosting iterations play a more important role. The best models delivered by were more sparse than .

Acknowledgements

The authors will like to thank Alexandre Belloni, Jerome Friedman, Trevor Hastie, Arian Maleki and Tomaso Poggio for helpful discussions and encouragement. A preliminary unpublished version of some of the results herein was posted on the ArXiv [18].

References

- [1] M. Avriel. Nonlinear Programming Analysis and Methods. Prentice-Hall, Englewood Cliffs, N.J., 1976.

- [2] F. Bach. Duality between subgradient and conditional gradient methods. SIAM Journal on Optimization, 25(1):115–129, Jan. 2015.

- [3] D. Bertsekas. Nonlinear Programming. Athena Scientific, Belmont, MA, 1999.

- [4] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, Cambridge, 2004.

- [5] L. Breiman. Arcing classifiers (with discussion). Annals of Statistics, 26:801–849, 1998.

- [6] L. Breiman. Prediction games and arcing algorithms. Neural Computation, 11(7):1493–1517, 1999.

- [7] P. Bühlmann. Boosting for high-dimensional linear models. The Annals of Statistics, pages 559–583, 2006.

- [8] P. Bühlmann and T. Hothorn. Boosting algorithms: regularization, prediction and model fitting (with discussion). Statistical Science, 22(4):477–505, 2008.

- [9] P. Bühlmann and B. Yu. Boosting with the l2 loss: regression and classification. Journal of the American Statistical Association, 98(462):324–339, 2003.

- [10] P. Bühlmann and B. Yu. Sparse boosting. The Journal of Machine Learning Research, 7:1001–1024, 2006.

- [11] K. Clarkson. Coresets, sparse greedy approximation, and the Frank-Wolfe algorithm. 19th ACM-SIAM Symposium on Discrete Algorithms, pages 922–931, 2008.

- [12] M. Dettling and P. Bühlmann. Boosting for tumor classification with gene expression data. Bioinformatics, 19(9):1061–1069, 2003.

- [13] D. L. Donoho, I. M. Johnstone, G. Kerkyacharian, and D. Picard. Wavelet shrinkage: asymptopia? Journal of the Royal Statistical Society. Series B (Methodological), pages 301–369, 1995.

- [14] J. Duchi and Y. Singer. Boosting with structural sparsity. In Proceedings of the 26th Annual International Conference on Machine Learning, pages 297–304. ACM, 2009.

- [15] B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani. Least angle regression (with discussion). Annals of Statistics, 32(2):407–499, 2004.

- [16] M. Frank and P. Wolfe. An algorithm for quadratic programming. Naval Research Logistics Quarterly, 3:95–110, 1956.

- [17] R. M. Freund and P. Grigas. New analysis and results for the Frank-Wolfe method. to appear in Mathematical Programming, 2014.

- [18] R. M. Freund, P. Grigas, and R. Mazumder. Adaboost and forward stagewise regression are first-order convex optimization methods. CoRR, abs/1307.1192, 2013.

- [19] Y. Freund. Boosting a weak learning algorithm by majority. Information and computation, 121(2):256–285, 1995.

- [20] Y. Freund and R. Schapire. Experiments with a new boosting algorithm. In Machine Learning: Proceedings of the Thirteenth International Conference, pages 148–156. Morgan Kauffman, San Francisco, 1996.

- [21] J. Friedman. Greedy function approximation: A gradient boosting machine. Annals of Statistics, 29(5):1189–1232, 2001.

- [22] J. Friedman. Fast sparse regression and classification. Technical report, Department of Statistics, Stanford University, 2008.

- [23] J. Friedman, T. Hastie, H. Hoefling, and R. Tibshirani. Pathwise coordinate optimization. Annals of Applied Statistics, 2(1):302–332, 2007.

- [24] J. Friedman, T. Hastie, and R. Tibshirani. Additive logistic regression: a statistical view of boosting (with discussion). Annals of Statistics, 28:337–307, 2000.

- [25] J. H. Friedman. Greedy function approximation: A gradient boosting machine. Annals of Statistics, 29:1189–1232, 2000.

- [26] J. H. Friedman and B. E. Popescu. Importance sampled learning ensembles. Journal of Machine Learning Research, 94305, 2003.

- [27] T. Hastie, J. Taylor, R. Tibshirani, and G. Walther. Forward stagewise regression and the monotone lasso. Electronic Journal of Statistics, 1:1–29, 2007.

- [28] T. Hastie, R. Tibshirani, and J. Friedman. Elements of Statistical Learning: Data Mining, Inference, and Prediction. Springer Verlag, New York, 2009.

- [29] T. J. Hastie and R. J. Tibshirani. Generalized additive models, volume 43. CRC Press, 1990.

- [30] M. Jaggi. Revisiting Frank-Wolfe: Projection-free sparse convex optimization. In Proceedings of the 30th International Conference on Machine Learning (ICML-13), pages 427–435, 2013.

- [31] S. G. Mallat and Z. Zhang. Matching pursuits with time-frequency dictionaries. Signal Processing, IEEE Transactions on, 41(12):3397–3415, 1993.

- [32] L. Mason, J. Baxter, P. Bartlett, and M. Frean. Boosting algorithms as gradient descent. 12:512–518, 2000.

- [33] A. Miller. Subset selection in regression. CRC Press Washington, 2002.

- [34] Y. E. Nesterov. Introductory lectures on convex optimization: a basic course, volume 87 of Applied Optimization. Kluwer Academic Publishers, Boston, 2003.

- [35] B. Polyak. Introduction to Optimization. Optimization Software, Inc., New York, 1987.

- [36] G. Rätsch, T. Onoda, and K.-R. Müller. Soft margins for adaboost. Machine learning, 42(3):287–320, 2001.